Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Dielectric Heat Transfer Fluid Market: 11.27% CAGR Analysis

Dielectric Heat Transfer Fluid

Dielectric Heat Transfer Fluid Market: 11.27% CAGR Analysis

Dielectric Heat Transfer Fluid by Application (Single-phase Immersion Cooling System, Two-phase Immersion Cooling System), by Types (Hydrocarbons, Fluorocarbons, Silicone Fluids, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 11, 2026|Base Year : 2025|Pages : 90

Key Insights into the Dielectric Heat Transfer Fluid Market

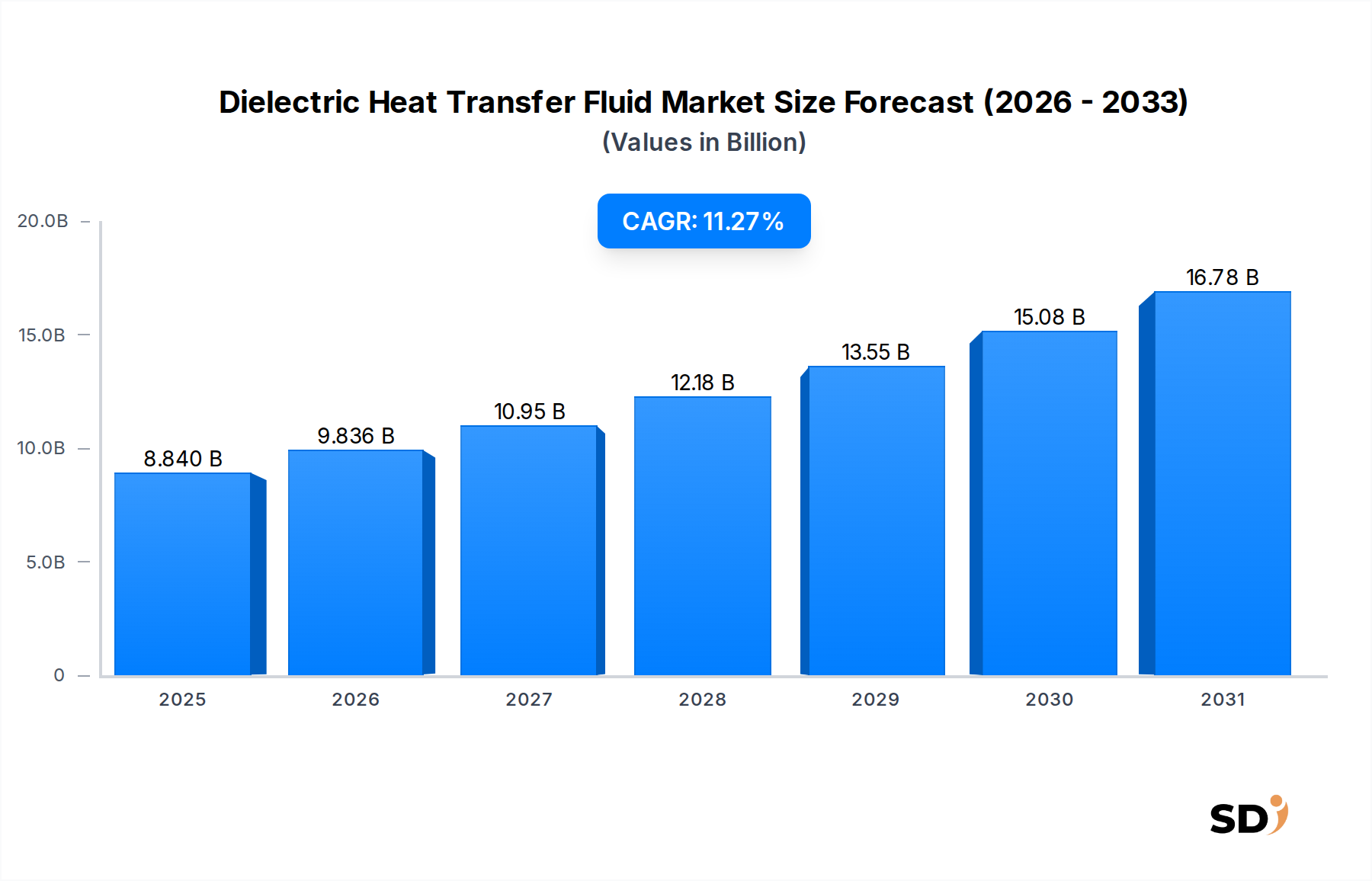

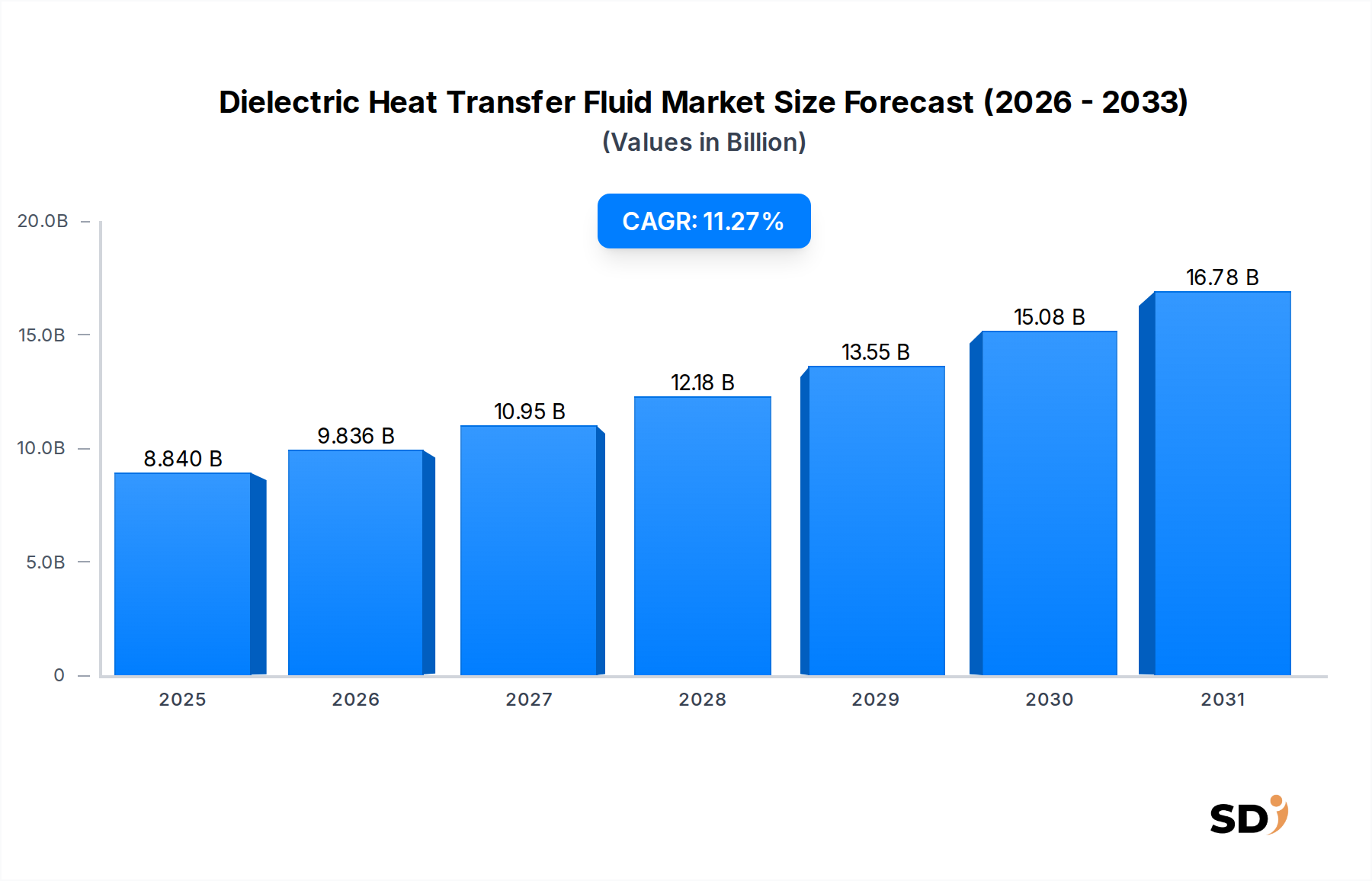

The global Dielectric Heat Transfer Fluid Market is projected for substantial expansion, underpinned by escalating demand across high-performance computing, advanced electronics, and nascent energy storage applications. Valued at an estimated $8.84 billion in 2025, the market is poised to exhibit a robust Compound Annual Growth Rate (CAGR) of 11.27% through the forecast period. This trajectory is primarily driven by the imperative for efficient thermal management in an increasingly power-dense technological landscape.

Dielectric Heat Transfer Fluid Market Size (In Billion)

20.0B

15.0B

10.0B

5.0B

0

8.840 B

2025

9.836 B

2026

10.95 B

2027

12.18 B

2028

13.55 B

2029

15.08 B

2030

16.78 B

2031

A significant demand impetus originates from the rapid proliferation of data centers, particularly those adopting high-density server racks and Artificial Intelligence (AI) infrastructure, where traditional air-cooling methods prove insufficient. The burgeoning Electric Vehicle Battery Thermal Management Market also represents a critical growth vector, as advanced dielectric fluids offer superior thermal regulation and safety for lithium-ion battery packs. Furthermore, the relentless miniaturization of electronic components and the increasing thermal loads in industrial processes necessitate highly effective and electrically non-conductive cooling solutions. The strategic importance of these fluids extends into the renewable energy sector, where they ensure optimal operating conditions for concentrated solar power (CSP) systems and wind turbine generators.

Key industry players are intensely focused on developing next-generation dielectric fluids that offer enhanced thermal performance, improved environmental profiles (e.g., non-PFAS formulations), and greater cost-effectiveness. Innovations in fluid chemistry, system design, and material compatibility are critical to overcoming existing challenges, such as the high initial cost of advanced fluids and the complexity associated with implementing immersion cooling solutions. The evolving regulatory landscape, particularly concerning fluorinated compounds, is also shaping product development, driving a shift towards more sustainable and biodegradable options. Geographically, while established economies like North America and Europe demonstrate mature demand, the Asia Pacific region is expected to lead growth, propelled by massive investments in digital infrastructure and industrial expansion.

The strategic outlook for the Dielectric Heat Transfer Fluid Market remains unequivocally positive. The confluence of technological advancement, energy efficiency mandates, and sustainability goals will continue to accelerate its adoption across diverse high-value applications. The Immersion Cooling Market is directly reliant on the advancements in dielectric fluids, signifying a symbiotic growth relationship. As the need for advanced thermal management solutions intensifies across critical sectors, the market for dielectric heat transfer fluids is set to play an indispensable role in enabling future technological innovation and operational efficiency.

Fluorocarbons Dominance in Dielectric Heat Transfer Fluid Market

Within the highly specialized Dielectric Heat Transfer Fluid Market, the fluorocarbons segment, by type, currently commands a significant revenue share and is projected to exhibit sustained growth, primarily due to their unparalleled dielectric strength, non-flammability, and excellent thermal stability. Fluorocarbons, including perfluorocarbons (PFCs) and hydrofluoroethers (HFEs), are inert, low-toxicity, and boast very low global warming potential (GWP) alternatives to earlier generations, making them ideal for mission-critical applications where safety and performance are paramount. Their superior properties make them the preferred choice for single-phase and two-phase immersion cooling systems in high-density computing environments, such as data centers, supercomputers, and blockchain mining operations. The ability of fluorocarbons to effectively dissipate intense heat loads from CPUs, GPUs, and memory modules without electrical conductivity or corrosive effects positions them as a cornerstone technology for the burgeoning high-performance computing sector. This leadership is particularly evident where operational uptime and hardware integrity are non-negotiable.

The dominance of fluorocarbons is further solidified by their role in specialized industrial processes and defense applications, where extreme temperatures and harsh conditions necessitate robust and reliable thermal management. Key players such as 3M (with its Novec™ and Fluorinert™ fluids) and Chemours (with its Opteon™ fluids) have historically driven innovation and market penetration in this segment. These companies continually invest in R&D to enhance fluid properties, reduce environmental impact, and expand application versatility. While the high initial cost of fluorocarbons compared to hydrocarbon or silicone-based alternatives remains a factor, the long-term benefits of reduced energy consumption, extended hardware lifespan, and superior safety profiles often outweigh the upfront investment for critical infrastructure. The demand for these high-performance fluids is further augmented by the increasing complexity and power density of electronic devices, from advanced semiconductor manufacturing to power electronics in electric vehicles.

Despite their dominance, the fluorocarbon segment faces evolving regulatory scrutiny, particularly regarding certain legacy per- and polyfluoroalkyl substances (PFAS). This has prompted manufacturers to invest heavily in developing next-generation, short-chain fluorocarbons and non-PFAS alternatives that retain high performance while mitigating environmental concerns. This strategic shift ensures the continued viability and leadership of fluorocarbons in the Dielectric Heat Transfer Fluid Market. In contrast, the Silicone Fluid Market, while offering excellent temperature stability and good dielectric properties, often has higher viscosity and is less suited for very high heat flux applications compared to fluorocarbons. Hydrocarbon-based fluids are more cost-effective but typically have lower flash points and dielectric strength, limiting their use in environments requiring extreme safety and electrical insulation. The ongoing innovation in fluorocarbon chemistry, aimed at addressing sustainability and cost, ensures its continued position as the dominant segment by value in the dielectric heat transfer fluid landscape, particularly in cutting-edge technological sectors where compromise on performance is not an option.

Key Market Drivers & Constraints in Dielectric Heat Transfer Fluid Market

The Dielectric Heat Transfer Fluid Market's expansion is fundamentally shaped by several potent drivers and critical constraints. A primary driver is the exponential growth of the Data Center Cooling Market. The increasing adoption of AI, machine learning, and cloud computing workloads has led to unprecedented power densities in server racks, where traditional air-cooling systems are reaching their physical limits. Dielectric fluids, particularly in immersion cooling setups, can achieve significantly higher cooling efficiencies, often reducing energy consumption for cooling by 30-50% compared to air-based systems. For instance, a typical hyperscale data center can save millions in operational costs annually by transitioning to efficient liquid cooling.

Another significant driver is the rapid global transition to Electric Vehicles (EVs). The Electric Vehicle Battery Thermal Management Market demands highly efficient and electrically non-conductive fluids to maintain optimal operating temperatures for battery packs, extending their lifespan, enhancing safety, and improving charging rates. As EV production scales, the demand for dielectric fluids that can manage the heat generated by high-power battery cells will surge proportionally. Forecasts suggest that the global EV market could reach over 40 million units annually by 2030, directly fueling demand for specialized thermal management solutions.

Conversely, a key constraint for the Dielectric Heat Transfer Fluid Market is the relatively high initial cost associated with advanced dielectric fluids, especially fluorocarbons and certain synthetic esters. These specialized fluids can be several times more expensive per liter than conventional coolants or water-glycol mixtures. This high upfront investment can deter smaller enterprises or those with limited capital expenditure budgets from adopting immersion cooling technologies, despite the long-term operational savings. Additionally, the complexity of designing, implementing, and maintaining immersion cooling systems, which often require specialized infrastructure and expertise, acts as a barrier to wider adoption. This includes challenges related to fluid handling, filtration, and managing fluid evaporation in open-bath systems. Furthermore, regulatory scrutiny, particularly regarding per- and polyfluoroalkyl substances (PFAS) found in some fluorocarbon-based fluids, presents a growing constraint. Restrictive environmental regulations, especially in Europe and North America, are pushing manufacturers to invest heavily in PFAS-free alternatives, which can impact R&D costs and product availability in the short term, thereby affecting the overall Dielectric Heat Transfer Fluid Market.

Competitive Ecosystem of Dielectric Heat Transfer Fluid Market

The Dielectric Heat Transfer Fluid Market is characterized by a concentrated competitive landscape, featuring established chemical manufacturers and specialized thermal management solution providers. These companies vie for market share through product innovation, strategic partnerships, and expansion into emerging applications:

3M: A diversified technology company, 3M is a prominent player in the Dielectric Heat Transfer Fluid Market, renowned for its Novec™ and Fluorinert™ fluid lines which are widely utilized in immersion cooling for data centers and electronics, leveraging its extensive expertise in fluorochemistry.

Shell: As a global energy and petrochemical company, Shell contributes to the Dielectric Heat Transfer Fluid Market with specialized hydrocarbon-based and synthetic fluids designed for industrial applications requiring reliable thermal transfer and electrical insulation.

Chemours: A global chemistry company, Chemours is a key innovator in fluoroproducts, offering advanced dielectric fluids under its Opteon™ brand, which are recognized for their low global warming potential and high-performance characteristics for demanding thermal management needs.

ExxonMobil: A leading oil and gas company, ExxonMobil provides a range of synthetic heat transfer fluids and lubricants, including those with dielectric properties suitable for transformers, switches, and other electrical equipment in the broader Industrial Fluids Market.

Juhua: A major Chinese chemical company, Juhua specializes in fluorochemicals and refrigerants, positioning it as a significant supplier of dielectric fluids, particularly in the Asia Pacific region, supporting industrial and emerging data center cooling demands.

Solvay: A global leader in specialty chemicals, Solvay offers high-performance fluoropolymers and advanced materials, including dielectric fluids that cater to demanding applications in electronics, automotive, and aerospace sectors, focusing on high thermal stability and chemical inertness.

ENEOS: A comprehensive energy, resources, and materials company from Japan, ENEOS produces a variety of industrial fluids, including synthetic heat transfer fluids with dielectric properties, serving power generation, automotive, and industrial thermal management needs.

GRC: Specializing in immersion cooling solutions, GRC offers complete thermal management systems that integrate advanced dielectric fluids, providing end-to-end solutions for high-density computing environments and optimizing fluid performance for maximum efficiency.

Valvoline: Primarily known for its lubricants, Valvoline also develops and supplies industrial fluids, including specialized heat transfer fluids, contributing to various industrial and automotive applications where reliable thermal management is critical.

Enviro Tech: Focused on sustainable solutions, Enviro Tech offers environmentally responsible chemical products, including specialized non-toxic and biodegradable dielectric fluids, catering to market demand for greener thermal management options.

Recent Developments & Milestones in Dielectric Heat Transfer Fluid Market

The Dielectric Heat Transfer Fluid Market is dynamic, with continuous innovation and strategic movements shaping its trajectory:

March 2024: A leading fluorochemical manufacturer announced a significant investment in a new production facility for next-generation, PFAS-free dielectric fluids, aiming to meet rising demand from the Immersion Cooling Market while adhering to stringent environmental regulations.

January 2024: A major data center operator partnered with a dielectric fluid supplier to deploy two-phase immersion cooling systems across its new hyperscale facilities, citing an estimated 35% reduction in cooling energy consumption and enhanced server reliability.

November 2023: A prominent EV battery manufacturer unveiled a new battery module design incorporating a novel dielectric fluid for direct immersion cooling, targeting improved thermal stability and extended battery life for its upcoming vehicle models.

September 2023: Researchers at a prominent university announced a breakthrough in developing bio-based dielectric fluids derived from sustainable plant oils, achieving comparable thermal and dielectric properties to synthetic counterparts, pointing towards a greener future for the Dielectric Heat Transfer Fluid Market.

July 2023: A consortium of technology companies, including a major semiconductor manufacturer and a fluid developer, initiated a joint venture to standardize testing protocols and performance metrics for dielectric fluids used in advanced semiconductor manufacturing processes.

May 2023: A specialty chemicals company launched a new line of non-flammable, low-viscosity dielectric fluids specifically engineered for transformer cooling and high-voltage switchgear, emphasizing improved safety and operational efficiency.

February 2023: A strategic acquisition was finalized between a thermal management system integrator and a dielectric fluid producer, aiming to offer integrated, turn-key immersion cooling solutions that simplify deployment for end-users.

Regional Market Breakdown for Dielectric Heat Transfer Fluid Market

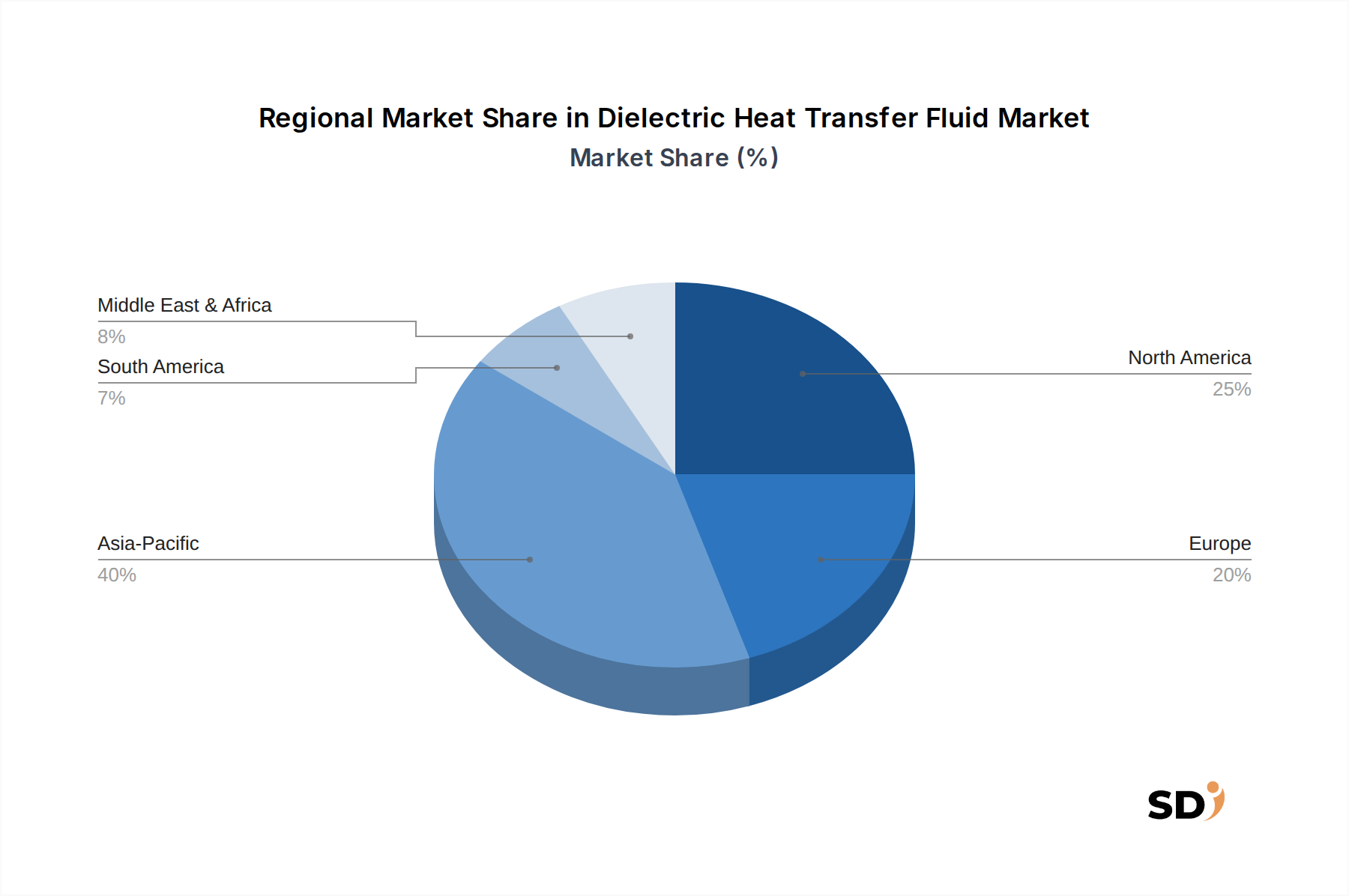

The global Dielectric Heat Transfer Fluid Market exhibits distinct growth patterns and demand drivers across its key regions. North America currently holds a substantial revenue share, driven by extensive investments in hyperscale data centers, a robust electronics manufacturing sector, and early adoption of advanced thermal management technologies. The region benefits from significant R&D capabilities and a strong presence of key market players, leading to rapid integration of innovative dielectric fluids, particularly in the Data Center Cooling Market. The United States, in particular, is a dominant force, with continued expansion in AI and cloud computing infrastructure fueling demand.

Asia Pacific is projected to be the fastest-growing region in the Dielectric Heat Transfer Fluid Market during the forecast period. This accelerated growth is primarily attributed to the burgeoning digital transformation initiatives, rapid industrialization, and massive investments in data center infrastructure across countries like China, India, Japan, and South Korea. The region's expanding Electric Vehicle Battery Thermal Management Market also contributes significantly, as EV production capacities scale up rapidly. Government support for indigenous manufacturing and technological advancement further catalyzes the adoption of dielectric fluids for thermal management across diverse applications.

Europe represents another significant market, characterized by stringent energy efficiency regulations and a strong emphasis on sustainability. The region's push towards green data centers and the widespread adoption of EVs drive the demand for eco-friendly and high-performance dielectric fluids. Countries like Germany, France, and the UK are at the forefront of implementing advanced immersion cooling solutions and developing sustainable fluid chemistries. The European market, while mature in some industrial applications, is seeing renewed growth from data centers and renewable energy sectors.

Middle East & Africa (MEA) and South America are emerging markets, currently holding smaller shares but demonstrating promising growth potential. In MEA, investments in smart cities, digitalization projects, and growing industrial sectors are creating new opportunities for dielectric fluids. The GCC countries, with their ambitious infrastructure projects, are particularly noteworthy. South America's market growth is propelled by increasing industrial activities, expanding telecommunications infrastructure, and nascent but growing EV markets, with Brazil and Argentina leading the adoption. The overall Thermal Management Systems Market in these regions is still developing, yet the foundational need for efficient heat dissipation across various sectors ensures a steady, albeit slower, adoption curve for dielectric fluids.

Export, Trade Flow & Tariff Impact on Dielectric Heat Transfer Fluid Market

The Dielectric Heat Transfer Fluid Market is intrinsically linked to global trade dynamics, with major trade corridors facilitating the movement of both raw materials and finished specialized fluids. Leading exporting nations for advanced dielectric fluids and their chemical precursors typically include those with robust chemical manufacturing capabilities, such as the United States, Germany, Japan, and China. These countries possess the technological expertise and infrastructure to produce high-purity fluorocarbons, silicones, and synthetic esters that form the basis of these fluids. Major importing nations are predominantly those with high concentrations of data centers, advanced electronics manufacturing, and significant electric vehicle production – notably countries in North America, Western Europe, and the rapidly industrializing economies of Asia Pacific, including South Korea, Taiwan, and Singapore.

Trade flows are often concentrated along established routes between these industrial powerhouses. For instance, fluorocarbon-based dielectric fluids manufactured in the U.S. or Europe might be exported to Asian markets to support their burgeoning data center and semiconductor industries. Conversely, certain specialty chemical intermediates from Asia could flow to Western manufacturers for final formulation. The global Specialty Chemicals Market, which includes many components of dielectric fluids, often operates under complex international supply chains susceptible to trade policy shifts.

Tariffs and non-tariff barriers can significantly impact the Dielectric Heat Transfer Fluid Market. Recent trade disputes and geopolitical tensions have led to increased tariffs on various chemicals and manufactured goods, potentially raising the cost of imported dielectric fluids or their raw materials. For example, specific import duties imposed on certain fluorinated compounds can increase the manufacturing cost for domestic producers or inflate prices for end-users, affecting the competitiveness of different fluid types. Non-tariff barriers, such as stringent regulatory approvals, complex customs procedures, and evolving environmental standards (e.g., restrictions on PFAS substances), also play a crucial role. These barriers can slow down market entry for new products, require significant investment in re-formulation, or create preferential access for domestically produced fluids. Quantifying recent impacts, a 5-10% increase in tariffs on key chemical inputs has been observed to translate into a 2-4% rise in the final cost of specialized dielectric fluids in affected regions, potentially influencing procurement decisions and leading to localized sourcing where possible.

Sustainability & ESG Pressures on Dielectric Heat Transfer Fluid Market

The Dielectric Heat Transfer Fluid Market is experiencing significant transformation driven by increasing sustainability and Environmental, Social, and Governance (ESG) pressures. Stakeholders, including regulators, investors, and end-users, are demanding more environmentally benign solutions, pushing manufacturers to innovate beyond traditional formulations. Environmental regulations, particularly those targeting per- and polyfluoroalkyl substances (PFAS), are a primary catalyst. Jurisdictions like the European Union and several U.S. states are implementing or proposing bans and restrictions on certain PFAS chemistries due to their persistence in the environment. This legislative shift compels companies in the Dielectric Heat Transfer Fluid Market to invest heavily in R&D for PFAS-free alternatives that maintain superior performance characteristics. This focus extends to developing fluids with lower Global Warming Potential (GWP) and Ozone Depletion Potential (ODP), aligning with broader climate change mitigation efforts and international agreements.

Carbon targets and the drive for a circular economy are also reshaping product development. Manufacturers are exploring bio-based and biodegradable dielectric fluids derived from renewable sources, aiming to reduce the carbon footprint associated with production and disposal. The development of advanced recycling and reclamation technologies for synthetic dielectric fluids is another critical area. Companies are increasingly offering take-back programs and re-processing services to ensure that fluids can be reused, minimizing waste and resource consumption. This aligns with circular economy mandates that prioritize resource efficiency and waste reduction throughout the product lifecycle. Such initiatives are particularly vital for the Glycol Heat Transfer Fluid Market as well, which faces similar pressures but for different chemical profiles.

ESG investor criteria are influencing procurement and R&D strategies. Investors are increasingly screening companies based on their environmental stewardship, social responsibility, and governance practices. This translates into a preference for suppliers who can demonstrate a clear commitment to sustainability, transparent supply chains, and responsible manufacturing processes. As a result, companies in the Dielectric Heat Transfer Fluid Market are integrating ESG metrics into their corporate strategies, not just as compliance, but as a competitive differentiator. This includes efforts to reduce energy consumption in manufacturing, minimize wastewater discharge, and ensure ethical sourcing of raw materials. The holistic impact of these pressures is a market shift towards greener chemistries, enhanced recyclability, and more transparent environmental reporting, fundamentally altering how dielectric heat transfer fluids are developed, produced, and consumed globally.

Dielectric Heat Transfer Fluid Segmentation

1. Application

1.1. Single-phase Immersion Cooling System

1.2. Two-phase Immersion Cooling System

2. Types

2.1. Hydrocarbons

2.2. Fluorocarbons

2.3. Silicone Fluids

2.4. Others

Dielectric Heat Transfer Fluid Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Dielectric Heat Transfer Fluid REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 11.27% from 2020-2034

Segmentation

By Application

Single-phase Immersion Cooling System

Two-phase Immersion Cooling System

By Types

Hydrocarbons

Fluorocarbons

Silicone Fluids

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Single-phase Immersion Cooling System

5.1.2. Two-phase Immersion Cooling System

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Hydrocarbons

5.2.2. Fluorocarbons

5.2.3. Silicone Fluids

5.2.4. Others

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Single-phase Immersion Cooling System

6.1.2. Two-phase Immersion Cooling System

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Hydrocarbons

6.2.2. Fluorocarbons

6.2.3. Silicone Fluids

6.2.4. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Single-phase Immersion Cooling System

7.1.2. Two-phase Immersion Cooling System

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Hydrocarbons

7.2.2. Fluorocarbons

7.2.3. Silicone Fluids

7.2.4. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Single-phase Immersion Cooling System

8.1.2. Two-phase Immersion Cooling System

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Hydrocarbons

8.2.2. Fluorocarbons

8.2.3. Silicone Fluids

8.2.4. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Single-phase Immersion Cooling System

9.1.2. Two-phase Immersion Cooling System

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Hydrocarbons

9.2.2. Fluorocarbons

9.2.3. Silicone Fluids

9.2.4. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Single-phase Immersion Cooling System

10.1.2. Two-phase Immersion Cooling System

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Hydrocarbons

10.2.2. Fluorocarbons

10.2.3. Silicone Fluids

10.2.4. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. 3M

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Shell

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Chemours

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. ExxonMobil

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Juhua

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Solvay

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. ENEOS

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. GRC

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Valvoline

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Enviro Tech

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (billion), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (billion), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (billion), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (billion), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (billion), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (billion), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (billion), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (billion), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (billion), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (billion), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (billion), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (billion), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (billion), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (billion), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Application 2020 & 2033

Table 2: Revenue billion Forecast, by Types 2020 & 2033

Table 3: Revenue billion Forecast, by Region 2020 & 2033

Table 4: Revenue billion Forecast, by Application 2020 & 2033

Table 5: Revenue billion Forecast, by Types 2020 & 2033

Table 6: Revenue billion Forecast, by Country 2020 & 2033

Table 7: Revenue (billion) Forecast, by Application 2020 & 2033

Table 8: Revenue (billion) Forecast, by Application 2020 & 2033

Table 9: Revenue (billion) Forecast, by Application 2020 & 2033

Table 10: Revenue billion Forecast, by Application 2020 & 2033

Table 11: Revenue billion Forecast, by Types 2020 & 2033

Table 12: Revenue billion Forecast, by Country 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue (billion) Forecast, by Application 2020 & 2033

Table 15: Revenue (billion) Forecast, by Application 2020 & 2033

Table 16: Revenue billion Forecast, by Application 2020 & 2033

Table 17: Revenue billion Forecast, by Types 2020 & 2033

Table 18: Revenue billion Forecast, by Country 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Revenue (billion) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Revenue (billion) Forecast, by Application 2020 & 2033

Table 23: Revenue (billion) Forecast, by Application 2020 & 2033

Table 24: Revenue (billion) Forecast, by Application 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Revenue (billion) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue billion Forecast, by Application 2020 & 2033

Table 29: Revenue billion Forecast, by Types 2020 & 2033

Table 30: Revenue billion Forecast, by Country 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue (billion) Forecast, by Application 2020 & 2033

Table 37: Revenue billion Forecast, by Application 2020 & 2033

Table 38: Revenue billion Forecast, by Types 2020 & 2033

Table 39: Revenue billion Forecast, by Country 2020 & 2033

Table 40: Revenue (billion) Forecast, by Application 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue (billion) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Revenue (billion) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our market research approach prioritizes primary research, constituting 70-80% of our data collection efforts. This intensive engagement ensures the capture of real-time market dynamics, unquantifiable trends, and granular insights directly from industry participants. Our extensive network of industry experts, key opinion leaders, and stakeholders across the dielectric heat transfer fluid value chain are engaged through structured interviews, surveys, and expert consultations. The objective of primary research is to validate secondary findings, obtain qualitative and quantitative insights on market drivers, restraints, opportunities, competitive landscape, and future outlook.

Key stakeholders interviewed for this market study include:

Head of Data Center Operations/Infrastructure at major cloud service providers and enterprise data centers.

VP/Director of Product Development (Thermal Management) at immersion cooling system integrators and server OEMs.

Senior R&D Chemist/Material Scientist at dielectric fluid manufacturing companies.

Supply Chain Manager (Specialty Chemicals) involved in the procurement of dielectric fluids for large-scale deployments.

Companies targeted for primary interviews span critical segments of the value chain:

Dielectric Fluid Manufacturers

Immersion Cooling System Integrators/OEMs

Data Center Operators/Cloud Service Providers

Server/Hardware Manufacturers

Specialty Chemical Distributors

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Head of Data Center Operations

30%

VP/Director of Product Development (Thermal Management)

30%

Senior R&D Chemist/Material Scientist

25%

Supply Chain Manager (Specialty Chemicals)

15%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Dielectric Fluid Manufacturers

25%

Immersion Cooling System Integrators/OEMs

30%

Data Center Operators/Cloud Service Providers

25%

Server/Hardware Manufacturers

10%

Specialty Chemical Distributors

10%

Secondary Research & Industry Benchmarking

The remaining 20-30% of our research methodology is dedicated to rigorous secondary research and comprehensive industry benchmarking. This foundational stage involves extensive data mining from proprietary databases and publicly available information to construct a robust market overview. We leverage leading financial databases such as Bloomberg, Factiva, Hoovers, and PitchBook to gather company financials, market performance indicators, and competitive intelligence. Furthermore, vital data is extracted from government publications (.gov sources), reputable organizational reports (.org sources), and trade association journals that provide unbiased industry perspectives. We strictly avoid data from other market research websites to maintain originality and accuracy.

Key industry associations and regulatory bodies critical to this market include:

ASHRAE (American Society of Heating, Refrigerating and Air-Conditioning Engineers), providing standards and guidelines for thermal management in data centers. https://www.ashrae.org/

REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulations, particularly relevant for the chemical composition and environmental impact of dielectric fluids in the European market. https://echa.europa.eu/regulations/reach/understanding-reach

The Green Grid, an industry consortium focused on improving resource efficiency of IT and data centers. https://www.thegreengrid.org/

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies integrate both top-down and bottom-up approaches, complemented by multi-level data triangulation. The top-down approach involves estimating the total available market based on macroeconomic factors, industry trends, and overall technology adoption rates, then segmenting it down to specific applications and fluid types. The bottom-up approach aggregates market estimates from granular data points, validated through primary research.

Specific metrics and variables utilized for bottom-up market size calculation for dielectric heat transfer fluids include:

Estimated number of new immersion cooling tanks/systems deployed annually by region and application (single-phase vs. two-phase).

Average fluid volume required per immersion cooling tank/system, considering tank dimensions and server density.

Average annual fluid top-up or replacement rate due to evaporation, degradation, or system expansion.

Average price per liter/gallon of dielectric fluid, differentiated by type (hydrocarbons, fluorocarbons, silicone fluids) and regional pricing variations.

Growth in high-performance computing (HPC) and AI/ML server installations requiring advanced cooling solutions.

Multi-level data triangulation involves cross-referencing data points from primary interviews, secondary sources, and our proprietary demand models to ensure consistency and robustness in our market estimates.

Data Accuracy & Quality Check

Ensuring the highest standard of data accuracy and quality is paramount to our deliverables. We guarantee an estimated data accuracy level of 85-90% for our market figures and forecasts. This is achieved through a rigorous validation process that includes:

Cross-Validation: Comparing and reconciling data points from multiple independent sources (primary, secondary, and internal models).

Expert Review: Subject matter experts and senior analysts scrutinize all findings, assumptions, and methodologies.

Sensitivity Analysis: Assessing the impact of varying key assumptions on the overall market forecast to understand potential ranges and risks.

Continuous Updates: Every report is dynamic and updated up to the date of purchase, reflecting the latest market developments, technological advancements, and regulatory changes, ensuring our clients receive the most current and relevant insights.

Frequently Asked Questions

1. Which region offers the most significant growth opportunities for dielectric heat transfer fluids?

Asia-Pacific is projected to offer significant growth opportunities due to rapid industrialization, expanding data center infrastructure, and electronics manufacturing. This region is estimated to hold the largest market share, at 40%.

2. What are the primary drivers propelling the Dielectric Heat Transfer Fluid market's growth?

The market is driven by increasing demand for efficient thermal management in electronics, data centers, and advanced industrial cooling systems. This contributes to the market's projected 11.27% Compound Annual Growth Rate (CAGR).

3. What challenges and restraints impact the Dielectric Heat Transfer Fluid market?

Challenges include the high initial cost of specialized fluids and immersion cooling systems, coupled with evolving regulatory landscapes regarding fluorocarbon use. Supply chain risks for specialty chemical components also pose a restraint.

4. What are the key raw material considerations for dielectric heat transfer fluids?

Raw material sourcing is critical, with key types including specialized hydrocarbons, fluorocarbons, and silicone fluids. Supply chain stability for these chemical precursors directly affects production and pricing.

5. What is the level of investment activity or venture capital interest in this market?

While specific investment rounds are not detailed, the market's substantial value of $8.84 billion by 2025 and an 11.27% CAGR indicate sustained corporate and potential venture interest. Investment focuses on innovation in fluid properties and cooling system integration.

6. Who are the leading companies and market share leaders in the Dielectric Heat Transfer Fluid sector?

Key players dominating the Dielectric Heat Transfer Fluid market include 3M, Shell, Chemours, ExxonMobil, and Solvay. These companies focus on developing advanced fluids for single-phase and two-phase immersion cooling systems.