Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Dibutyl Lauroyl Glutamide Market: $120M by 2028, 6.5% CAGR

Dibutyl Lauroyl Glutamide

Dibutyl Lauroyl Glutamide Market: $120M by 2028, 6.5% CAGR

Dibutyl Lauroyl Glutamide by Application (Skin Care Products, Hair Care Products, Other), by Types (Above 98%, Above 99%, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 11, 2026|Base Year : 2025|Pages : 77

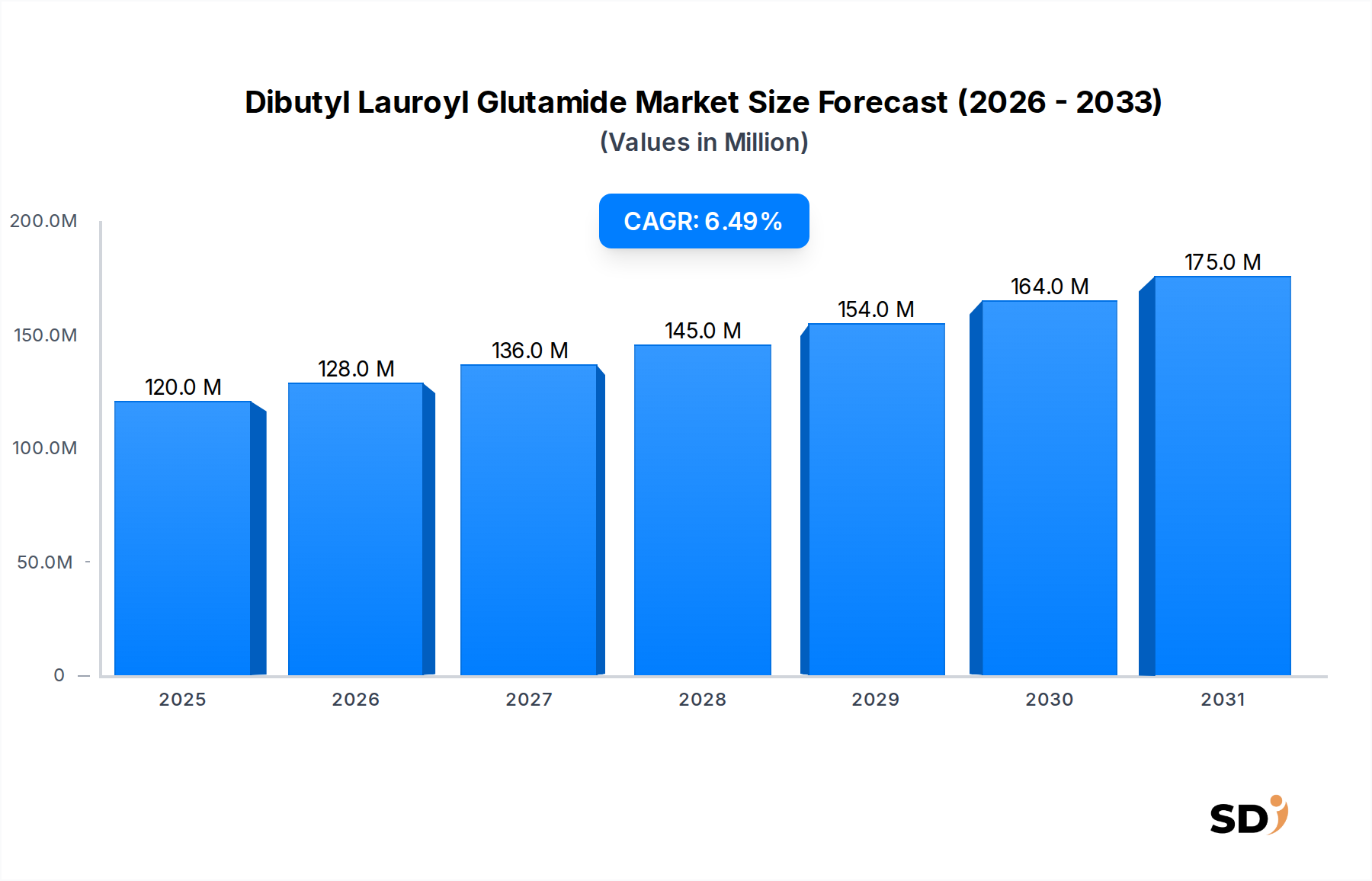

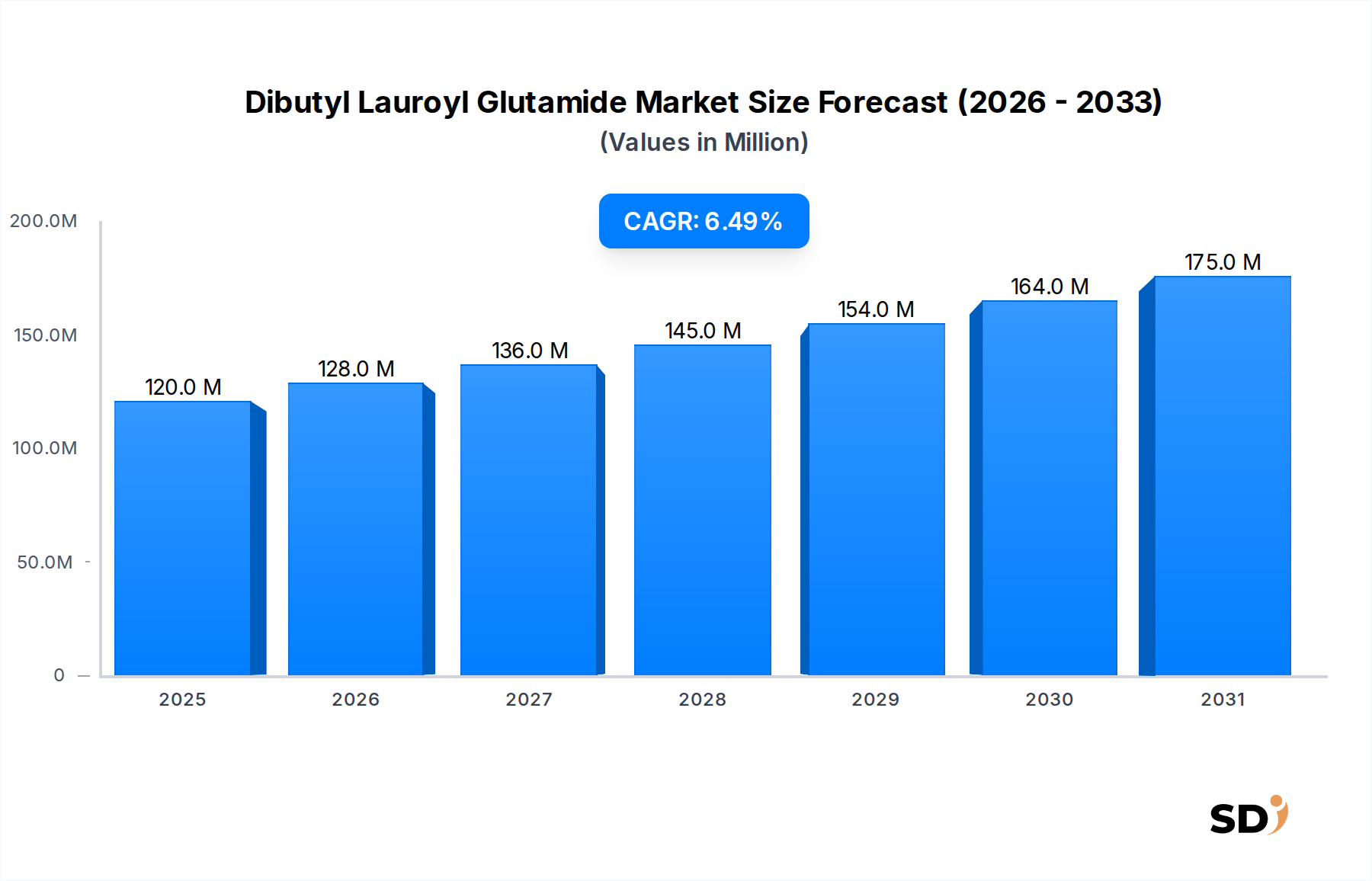

The global Dibutyl Lauroyl Glutamide Market, a specialized segment within the broader Personal Care Ingredients Market, is poised for robust expansion driven by evolving consumer preferences and innovative cosmetic formulations. Valued at an estimated $120 million in 2023, the market is projected to reach approximately $165.48 million by 2028, exhibiting a compelling Compound Annual Growth Rate (CAGR) of 6.5% over the forecast period. This growth trajectory is primarily propelled by the increasing demand for multi-functional cosmetic ingredients that enhance product aesthetics, stability, and sensory appeal.

Dibutyl Lauroyl Glutamide Market Size (In Million)

200.0M

150.0M

100.0M

50.0M

0

120.0 M

2025

128.0 M

2026

136.0 M

2027

145.0 M

2028

154.0 M

2029

164.0 M

2030

175.0 M

2031

Dibutyl Lauroyl Glutamide (DBLG) is an amino acid derivative known for its excellent gelling, thickening, and emollient properties, making it indispensable in modern personal care applications. It is particularly valued for its ability to create stable, transparent, and aesthetically pleasing gel networks in oil-based systems, offering a non-greasy, luxurious feel. The surge in consumer preference for solid cosmetic formats, such as stick foundations, lip balms, and deodorants, further accentuates the demand for DBLG as a structuring agent that provides firmness and ease of application. Furthermore, the rising adoption of "clean beauty" principles and the growing emphasis on naturally derived ingredients align perfectly with DBLG's profile as a biodegradable and skin-friendly component, bolstering its appeal in the Sustainable Cosmetics Market. Asia Pacific, particularly China and Japan, remains a pivotal region due to its expansive cosmetics manufacturing base and high consumer uptake of premium personal care products. Strategic investments in R&D by key players to develop novel applications and optimize ingredient performance are expected to sustain market momentum, navigating potential challenges such as raw material price volatility and competition from synthetic alternatives. The market is also benefiting from increasing awareness among formulators regarding DBLG's superior performance characteristics compared to traditional gelling agents, offering a distinct competitive advantage in product differentiation.

Dominant Application Segment: Skin Care Products in Dibutyl Lauroyl Glutamide Market

The Skin Care Products Market stands as the single largest and most influential application segment within the Dibutyl Lauroyl Glutamide Market, commanding a substantial revenue share. This dominance is attributable to DBLG's multifaceted functionalities, which are critically valued in a wide array of skin care formulations. As a potent gelling agent, Dibutyl Lauroyl Glutamide excels in structuring oil phases, enabling the creation of transparent or translucent gels, sticks, and emulsions that possess superior aesthetic appeal and tactile properties. Its ability to impart a smooth, non-tacky, and luxurious skin feel makes it a preferred choice for high-end serums, facial creams, body lotions, sunscreens, and make-up primers. Formulators leverage DBLG to enhance product stability, prevent oil separation, and achieve desired viscosity without compromising on spreadability or absorption.

Beyond its textural contributions, Dibutyl Lauroyl Glutamide also functions as an effective emollient, contributing to skin hydration and barrier function. This dual action of gelling and emolliency is particularly valuable in formulations targeting anti-aging, moisturizing, and protective skin care, where both performance and sensory attributes are paramount. The increasing consumer demand for novel textures, lightweight formulations, and innovative product formats, such as solid facial cleansers or serum sticks, further solidifies the position of DBLG in the Skin Care Products Market. Key players in this segment are continuously exploring DBLG's potential in hybrid formulations, combining the benefits of oil-based and water-based systems. The market share of skin care applications is expected to continue growing, propelled by ongoing innovation in dermatological cosmetics, the proliferation of specialized skin treatment products, and the global expansion of beauty regimens. The segment's growth is also influenced by geographical trends, with mature markets in North America and Europe adopting sophisticated skin care technologies, while emerging economies in Asia Pacific and Latin America witness a rapid increase in basic and advanced skin care product consumption. The versatility of Dibutyl Lauroyl Glutamide in various skin care matrices, coupled with its favorable safety profile, ensures its continued prominence and reinforces its critical role in shaping the future of skin care product development. This ingredient also plays a role in the broader Emollients Market, providing superior sensorial properties.

Key Market Drivers & Trends in Dibutyl Lauroyl Glutamide Market

The Dibutyl Lauroyl Glutamide Market is significantly influenced by several data-centric drivers and emerging trends:

Surging Demand for Solid and Stick Formulations: A primary driver is the escalating consumer preference for convenient, travel-friendly, and often plastic-reducing solid cosmetic and personal care products. Dibutyl Lauroyl Glutamide is an essential structuring agent for oil-based stick formulations, including lip balms, solid deodorants, sunscreen sticks, and solid foundations. Its unique ability to form stable, high-clarity gels and provide firmness directly addresses the technical challenges of developing these formats, which are projected to see a 5-7% annual growth in various categories over the next five years. This shift away from traditional liquid and cream formats boosts the utilization of DBLG.

Growth in Multi-functional Cosmetic Ingredients: The market is driven by formulators seeking ingredients that offer multiple benefits to simplify formulations and enhance product performance. Dibutyl Lauroyl Glutamide provides gelling, thickening, and emollient properties simultaneously, reducing the need for multiple single-function additives. This aligns with the industry trend towards streamlined ingredient lists and "clean" formulations. The compound's versatility makes it highly attractive for innovative product development across the Hair Care Products Market and skin care applications, where ingredient synergy is highly valued.

Rising Consumer Interest in Naturally Derived and 'Clean' Ingredients: Consumers are increasingly scrutinizing ingredient lists and favoring products with natural origins, biodegradability, and perceived safety. As an Amino Acid Derivatives Market ingredient, Dibutyl Lauroyl Glutamide is derived from amino acids and fatty acids, positioning it favorably within the "clean beauty" and natural cosmetics movements. This trend has led to a significant increase in the market share of natural and naturally derived cosmetic ingredients, which has grown by an estimated 8-10% annually over the past three years. This shift directly supports the adoption of DBLG over synthetic alternatives.

Innovation in Sensory Aesthetics and Texturizing Agents: The cosmetic industry places a high premium on product sensory profiles, including feel, spreadability, and after-feel. DBLG significantly contributes to enhancing the luxurious feel and non-greasy finish of oil-based products, a crucial differentiator in competitive markets. Formulators are continuously seeking ingredients that can deliver superior sensorial experiences, and DBLG's unique rheological properties make it a key enabler for next-generation textures, ensuring its continued relevance as a premium texturizing agent.

Competitive Ecosystem of Dibutyl Lauroyl Glutamide Market

The Dibutyl Lauroyl Glutamide Market is characterized by a focused competitive landscape, with a few key players dominating the production and innovation of this specialized ingredient. These companies leverage their R&D capabilities, supply chain efficiencies, and strategic partnerships to maintain their market positions and expand their product portfolios. Below are prominent entities shaping the market:

Ajinomoto: A global leader in amino acid technology, Ajinomoto is a pioneer and a significant producer of Dibutyl Lauroyl Glutamide. The company leverages its extensive expertise in biochemicals to offer high-purity, high-performance cosmetic ingredients, focusing on sustainable and innovative solutions for the personal care industry. Their strong intellectual property and global distribution network give them a considerable competitive edge.

DJC: DJC operates as a specialty chemical manufacturer, providing a range of ingredients for personal care and cosmetics. While perhaps not as globally ubiquitous as Ajinomoto, DJC focuses on regional market penetration and tailored ingredient solutions, often emphasizing cost-effectiveness and customer-specific formulations in the Dibutyl Lauroyl Glutamide Market.

Sino Lion: Based in China, Sino Lion is a major player in the Asian personal care ingredient sector, known for its comprehensive portfolio of cosmetic raw materials. The company emphasizes research and development to offer innovative, high-quality, and often bio-derived ingredients, including various gelling agents and emollients, catering to the rapidly expanding Asian cosmetics market.

Guangzhou Trojan Pharmatec: This company specializes in the R&D, production, and sales of pharmaceutical and cosmetic raw materials. Guangzhou Trojan Pharmatec focuses on providing specialized ingredients, including Dibutyl Lauroyl Glutamide, to support the growing demands of both local and international cosmetic manufacturers, often with a focus on meeting specific technical specifications for diverse applications.

Recent Developments & Milestones in Dibutyl Lauroyl Glutamide Market

Innovation and strategic initiatives are key drivers in the Dibutyl Lauroyl Glutamide Market, reflecting the industry's response to evolving consumer demands and regulatory landscapes. Recent developments showcase efforts to enhance product versatility, expand applications, and improve sustainability:

March 2024: A leading manufacturer launched a new, ultra-fine particle grade of Dibutyl Lauroyl Glutamide, specifically engineered for enhanced dispersion and improved transparency in complex oil-based gels, targeting the premium facial serum and anti-aging segment. This development aims to provide formulators with greater flexibility in achieving desired aesthetic and textural properties.

November 2023: A significant partnership was announced between a major DBLG producer and a European contract manufacturer specializing in natural cosmetics. The collaboration focuses on developing palm-free and sustainably sourced variants of Dibutyl Lauroyl Glutamide, addressing growing consumer and regulatory pressures for environmentally friendly ingredients within the Sustainable Cosmetics Market.

July 2023: Research findings were published highlighting the efficacy of Dibutyl Lauroyl Glutamide in stabilizing anhydrous sunscreen formulations, demonstrating superior photostability and water resistance compared to traditional thickeners. This research opens new avenues for DBLG's application in high-performance sun care products, particularly in the sports and outdoor segments.

April 2023: An Asian chemical company successfully scaled up its production capacity for Dibutyl Lauroyl Glutamide, aiming to meet the burgeoning demand from the rapidly expanding cosmetic manufacturing hubs in China and Southeast Asia. This expansion is critical for ensuring a stable supply chain and competitive pricing in the region.

January 2023: A technical seminar series was hosted across North America and Europe by a prominent ingredient supplier, educating formulators on the optimal incorporation techniques and synergistic effects of Dibutyl Lauroyl Glutamide with other advanced emollients and Cosmetic Thickeners Market ingredients. The initiative aimed to broaden the ingredient's application scope and overcome formulation challenges.

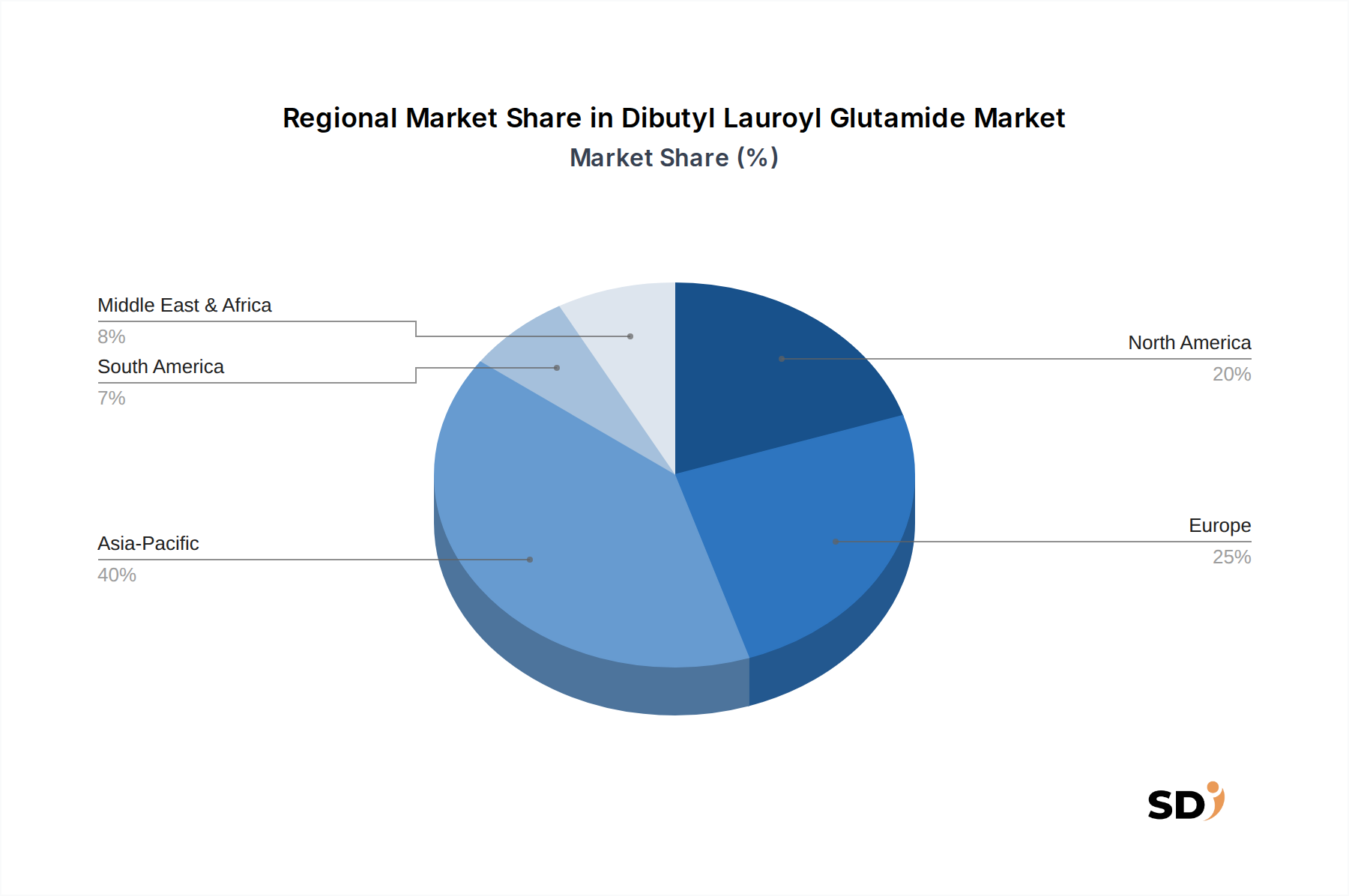

Regional Market Breakdown for Dibutyl Lauroyl Glutamide Market

The global Dibutyl Lauroyl Glutamide Market exhibits distinct regional dynamics, influenced by varying consumer preferences, regulatory frameworks, and the concentration of cosmetic manufacturing capabilities. While precise regional CAGR figures are not provided, an analysis of market drivers allows for a clear breakdown:

Asia Pacific: This region is anticipated to be the largest and fastest-growing market for Dibutyl Lauroyl Glutamide. Countries like China, Japan, and South Korea are at the forefront of cosmetic innovation and consumption. The primary demand driver here is the burgeoning middle class, rising disposable incomes, and a strong cultural emphasis on personal grooming and skin care. The presence of a vast manufacturing base for personal care products, coupled with a preference for novel textures and multi-functional formulations, fuels the adoption of DBLG. India and ASEAN nations also contribute significantly with their rapidly expanding consumer bases and increasing urbanization.

Europe: As a mature market, Europe represents a substantial share of the Dibutyl Lauroyl Glutamide Market. The demand is primarily driven by stringent quality standards, a strong focus on high-end and premium cosmetic products, and an increasing consumer shift towards natural and sustainable ingredients. Innovation in luxury skin care, decorative cosmetics, and specialized personal care formulations keeps the demand for high-performance ingredients like DBLG steady. The regional market is characterized by steady, moderate growth, with a strong emphasis on R&D for advanced product development.

North America: Similar to Europe, North America is a mature market driven by consumer demand for innovative, effective, and ethically sourced personal care products. The region's robust research and development ecosystem, coupled with a high prevalence of beauty and wellness trends, underpins the demand for Dibutyl Lauroyl Glutamide. The popularity of stick formulations, clean beauty brands, and premium skin care products acts as a significant demand driver. Growth here is stable, reflecting consistent innovation and consumer willingness to invest in quality ingredients.

South America & Middle East & Africa (SAMEA): These regions represent emerging markets with significant growth potential for Dibutyl Lauroyl Glutamide. While currently holding smaller market shares compared to Asia Pacific or Europe, the rising urbanization, increasing disposable incomes, and growing awareness of personal care products are stimulating demand. In South America, Brazil stands out as a major cosmetics market. In the Middle East, demand is driven by a strong beauty culture and a youthful population. As manufacturing capabilities and consumer product diversity expand in these regions, the adoption of specialized ingredients like DBLG is expected to accelerate, making them key areas for future market expansion.

Sustainability & ESG Pressures on Dibutyl Lauroyl Glutamide Market

The Dibutyl Lauroyl Glutamide Market is increasingly subject to scrutiny from sustainability and ESG (Environmental, Social, and Governance) perspectives, significantly influencing product development and procurement strategies. As an amino acid derivative, DBLG often benefits from a perception of being "naturally derived" or "bio-based," aligning with the broader trend towards greener chemistry in the personal care industry. Consumers and regulators are pushing for ingredients with favorable environmental profiles, including biodegradability, reduced carbon footprint, and sourcing transparency.

Key pressures include the demand for palm oil-free ingredients, as the industry seeks to mitigate deforestation and habitat loss associated with conventional palm cultivation. Manufacturers of Dibutyl Lauroyl Glutamide are therefore under pressure to ensure their fatty acid precursors are sourced sustainably, either through certified palm derivatives or alternative, non-palm-based feedstocks. This extends to the entire supply chain, with an emphasis on ethical labor practices and community engagement (Social aspect of ESG).

Furthermore, regulatory bodies globally are tightening restrictions on certain cosmetic ingredients, pushing for comprehensive safety assessments and environmental impact analyses. Companies in the Dibutyl Lauroyl Glutamide Market must invest in rigorous testing to demonstrate the safety and environmental compatibility of their products. The push for circular economy principles also encourages manufacturers to explore methods for recycling or upcycling by-products and minimizing waste throughout the production process. ESG investors are increasingly factoring these sustainability metrics into their investment decisions, driving companies to not only comply with regulations but also proactively engage in sustainable practices to attract capital and enhance brand reputation. This pressure has led to a greater focus on lifecycle assessments and the development of more environmentally benign synthesis routes for DBLG, positioning it as a key component in the shift towards truly sustainable cosmetic formulations.

Pricing Dynamics & Margin Pressure in Dibutyl Lauroyl Glutamide Market

The pricing dynamics in the Dibutyl Lauroyl Glutamide Market are complex, influenced by a confluence of raw material costs, manufacturing sophistication, competitive intensity, and the ingredient's specialty status. As a high-performance, multi-functional specialty chemical, DBLG typically commands a premium price compared to generic Gelling Agents Market and emollients. Average selling prices (ASPs) are generally stable but subject to fluctuations based on underlying commodity cycles, particularly those impacting its primary raw materials.

Key cost levers for Dibutyl Lauroyl Glutamide production include the cost of amino acids and fatty acids, which are derivatives relevant to the Fatty Acid Esters Market. Volatility in agricultural commodity markets or petrochemical prices (for fatty acid precursors) can directly impact manufacturing costs. Energy costs and labor expenses also contribute significantly, particularly for highly purified grades. The synthesis of DBLG requires specialized chemical processes and expertise, contributing to higher production overheads compared to simpler cosmetic ingredients.

Margin structures across the value chain reflect the innovation and technical service provided. Manufacturers typically operate with healthy but closely managed margins, needing to recoup significant R&D investments in developing and optimizing DBLG grades. Distributors and formulators also add their markups, reflecting storage, logistics, and formulation expertise. Competitive intensity, especially from synthetic gelling agents or other texturizers, exerts a constant downward pressure on pricing. While DBLG offers unique benefits, its higher cost can sometimes be a barrier for mass-market formulations, forcing manufacturers to differentiate through performance, purity, and sustainability credentials. Maintaining pricing power hinges on continuous product innovation, demonstrating superior performance benefits (e.g., enhanced transparency, improved skin feel, superior stability in complex formulations), and securing stable, cost-effective raw material supply chains. The ability to meet the growing demand for "clean beauty" and sustainable sourcing also enables some manufacturers to justify premium pricing.

Dibutyl Lauroyl Glutamide Segmentation

1. Application

1.1. Skin Care Products

1.2. Hair Care Products

1.3. Other

2. Types

2.1. Above 98%

2.2. Above 99%

2.3. Other

Dibutyl Lauroyl Glutamide Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Dibutyl Lauroyl Glutamide REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 6.5% from 2020-2034

Segmentation

By Application

Skin Care Products

Hair Care Products

Other

By Types

Above 98%

Above 99%

Other

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Skin Care Products

5.1.2. Hair Care Products

5.1.3. Other

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Above 98%

5.2.2. Above 99%

5.2.3. Other

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Skin Care Products

6.1.2. Hair Care Products

6.1.3. Other

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Above 98%

6.2.2. Above 99%

6.2.3. Other

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Skin Care Products

7.1.2. Hair Care Products

7.1.3. Other

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Above 98%

7.2.2. Above 99%

7.2.3. Other

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Skin Care Products

8.1.2. Hair Care Products

8.1.3. Other

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Above 98%

8.2.2. Above 99%

8.2.3. Other

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Skin Care Products

9.1.2. Hair Care Products

9.1.3. Other

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Above 98%

9.2.2. Above 99%

9.2.3. Other

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Skin Care Products

10.1.2. Hair Care Products

10.1.3. Other

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Above 98%

10.2.2. Above 99%

10.2.3. Other

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Ajinomoto

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. DJC

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Sino Lion

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Guangzhou Trojan Pharmatec

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (million), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (million), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (million), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (million), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (million), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (million), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (million), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (million), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (million), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (million), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (million), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Revenue million Forecast, by Types 2020 & 2033

Table 3: Revenue million Forecast, by Region 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Types 2020 & 2033

Table 6: Revenue million Forecast, by Country 2020 & 2033

Table 7: Revenue (million) Forecast, by Application 2020 & 2033

Table 8: Revenue (million) Forecast, by Application 2020 & 2033

Table 9: Revenue (million) Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Application 2020 & 2033

Table 11: Revenue million Forecast, by Types 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Types 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Revenue (million) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue million Forecast, by Application 2020 & 2033

Table 29: Revenue million Forecast, by Types 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue million Forecast, by Application 2020 & 2033

Table 38: Revenue million Forecast, by Types 2020 & 2033

Table 39: Revenue million Forecast, by Country 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our market intelligence is predominantly derived from primary research, constituting approximately 75% of our overall findings. This extensive engagement ensures real-time insights and validation from industry experts. Key stakeholders interviewed include:

Director of R&D, Personal Care

Global Procurement Manager, Specialty Ingredients

Head of Product Development, Skin Care

Senior Formulation Chemist

These experts represent a diverse cross-section of the Dibutyl Lauroyl Glutamide value chain, specifically encompassing:

Specialty Chemical Manufacturers

Cosmetic Ingredient Distributors

Personal Care Product Manufacturers

Contract Manufacturing Organizations (CMOs) for Cosmetics

R&D and Formulation Labs in Cosmetics

Interviews are conducted via in-depth telephone conversations, virtual meetings, and, where feasible, face-to-face discussions. This multi-pronged approach enables us to gather qualitative and quantitative data directly from decision-makers and influencers within the target market.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Director of R&D, Personal Care

30%

Global Procurement Manager, Specialty Ingredients

25%

Head of Product Development, Skin Care

25%

Senior Formulation Chemist

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Specialty Chemical Manufacturers

25%

Cosmetic Ingredient Distributors

20%

Personal Care Product Manufacturers

30%

Contract Manufacturing Organizations (CMOs) for Cosmetics

15%

R&D and Formulation Labs in Cosmetics

10%

Secondary Research & Industry Benchmarking

Secondary research accounts for the remaining 25% of our intelligence gathering, providing foundational data, industry trends, and market validation. Our robust secondary research framework leverages a wide array of credible sources, including:

Government & Regulatory Bodies: Official publications and guidelines from organizations such as the U.S. Food and Drug Administration (FDA) [https://www.fda.gov], European Chemicals Agency (ECHA) [https://echa.europa.eu], and relevant national ministries focusing on cosmetic ingredient safety and regulation.

Trade Associations & Industry Bodies: Reports and data from globally recognized associations such as the Personal Care Products Council (PCPC) [https://www.personalcarecouncil.org], Cosmetics Europe [https://cosmeticseurope.eu], and the International Federation of Societies of Cosmetic Chemists (IFSCC) [https://ifscc.org]. These sources offer crucial insights into market dynamics, regulatory shifts, and emerging ingredient trends pertinent to Dibutyl Lauroyl Glutamide's applications.

Corporate Filings & Investor Presentations: Annual reports, investor presentations, and financial statements of public companies in the specialty chemicals, personal care ingredients, and cosmetic product manufacturing sectors.

Financial Databases: Comprehensive data from leading platforms including Bloomberg, Factiva, Hoovers, and PitchBook are utilized for company profiles, competitive landscape analysis, and financial performance metrics.

Academic Journals & Patents: Peer-reviewed publications and patent databases provide insights into innovation, new applications, and technological advancements related to Dibutyl Lauroyl Glutamide's use as a gelling agent or rheology modifier in cosmetics.

It is our strict policy to exclude data from other market research websites to maintain the integrity and originality of our findings.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies integrate both top-down and bottom-up approaches, rigorously triangulated across multiple data points to ensure robustness.

Top-Down Approach: Global macroeconomic indicators, regional cosmetic market growth rates, and overall personal care ingredient market trends are analyzed to derive overarching market estimates for Dibutyl Lauroyl Glutamide.

Bottom-Up Approach: This granular methodology involves aggregating data from various market segments. Specific metrics and variables crucial for calculating the bottom-up market size include:

Production capacity (tonnes/kilograms) of key Dibutyl Lauroyl Glutamide manufacturers.

Average selling price (ASP) per kg/tonne across different grades (e.g., Above 98%, Above 99%) and regions.

Consumption volume by end-use application (Skin Care Products, Hair Care Products, Other) within major geographic regions.

Typical formulation inclusion rates/percentages of Dibutyl Lauroyl Glutamide in various cosmetic product types, based on its functional role.

Multi-level data triangulation involves cross-referencing estimates derived from primary interviews, secondary sources, and our proprietary demand models, ensuring consistency and accuracy across all market segments (Application, Types, and Regions).

Data Accuracy & Quality Check

We guarantee an estimated data accuracy level of 85-90% for our market estimations. This high level of precision is achieved through:

Rigorous Validation: All qualitative and quantitative data points collected from primary and secondary sources are meticulously cross-verified. Discrepancies are identified and resolved through further expert consultations or additional data sourcing.

Expert Panel Review: Draft findings and market estimates are subjected to review by an internal panel of senior analysts and, in some cases, external industry experts to challenge assumptions and refine projections.

Dynamic Data Updates: Recognizing the volatile nature of global markets, every report is updated up to the date of purchase. This commitment ensures that clients receive the most current and relevant market intelligence, incorporating recent developments, technological advancements, and shifts in the competitive landscape or regulatory environment. Our methodology is designed to capture market nuances and provide forward-looking insights that are both reliable and actionable.

Frequently Asked Questions

1. How do pricing trends influence the Dibutyl Lauroyl Glutamide market?

Pricing in the Dibutyl Lauroyl Glutamide market is influenced by raw material costs, production efficiency, and competitive dynamics among key players like Ajinomoto and DJC. Strategic sourcing and process optimization are crucial for maintaining competitive pricing. The market's growth at a 6.5% CAGR suggests a stable demand supporting current price structures.

2. What are the main barriers to entry in the Dibutyl Lauroyl Glutamide market?

Significant barriers include the need for specialized chemical synthesis expertise and R&D investment for product efficacy and stability. Established relationships with cosmetic manufacturers provide competitive moats for existing suppliers such as Sino Lion and Guangzhou Trojan Pharmatec. Compliance with varying regional cosmetic regulations also poses an entry hurdle.

3. How does the regulatory environment impact Dibutyl Lauroyl Glutamide market growth?

Regulatory bodies govern the permissible use and concentration of Dibutyl Lauroyl Glutamide in cosmetic products, particularly in skin and hair care. Compliance with regional standards like REACH in Europe or FDA guidelines in the US is mandatory. Strict adherence to safety and purity profiles is essential for market access and product acceptance, influencing development and application scope.

4. Which region dominates the Dibutyl Lauroyl Glutamide market and why?

Asia-Pacific is estimated to be the dominant region in the Dibutyl Lauroyl Glutamide market, holding approximately 40% market share. This leadership is driven by the region's robust cosmetics manufacturing base, high consumer demand for skin and hair care products, and rapid innovation from countries like China and Japan. Significant production capacities also contribute to its prominent position.

5. What are the key export-import dynamics for Dibutyl Lauroyl Glutamide?

International trade for Dibutyl Lauroyl Glutamide primarily involves exporting from regions with advanced chemical synthesis capabilities, such as Asia-Pacific, to major cosmetic formulation hubs globally. Companies like Ajinomoto and DJC facilitate these trade flows. Import regulations and tariffs in consumer markets like Europe and North America can influence supply chain strategies.

6. Are there disruptive technologies or emerging substitutes affecting the Dibutyl Lauroyl Glutamide market?

While Dibutyl Lauroyl Glutamide is valued for its gelling and thickening properties in cosmetic formulations, continuous innovation in natural and bio-based rheology modifiers represents an emerging trend. Advancements in green chemistry could introduce novel alternatives, potentially impacting its long-term market position. Current market growth at 6.5% CAGR suggests stable demand, but R&D in substitutes is ongoing.