Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Desktop Robots by Application (Offline, Online), by Types (Functional Type, Pet Type), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 11, 2026|Base Year : 2025|Pages : 140

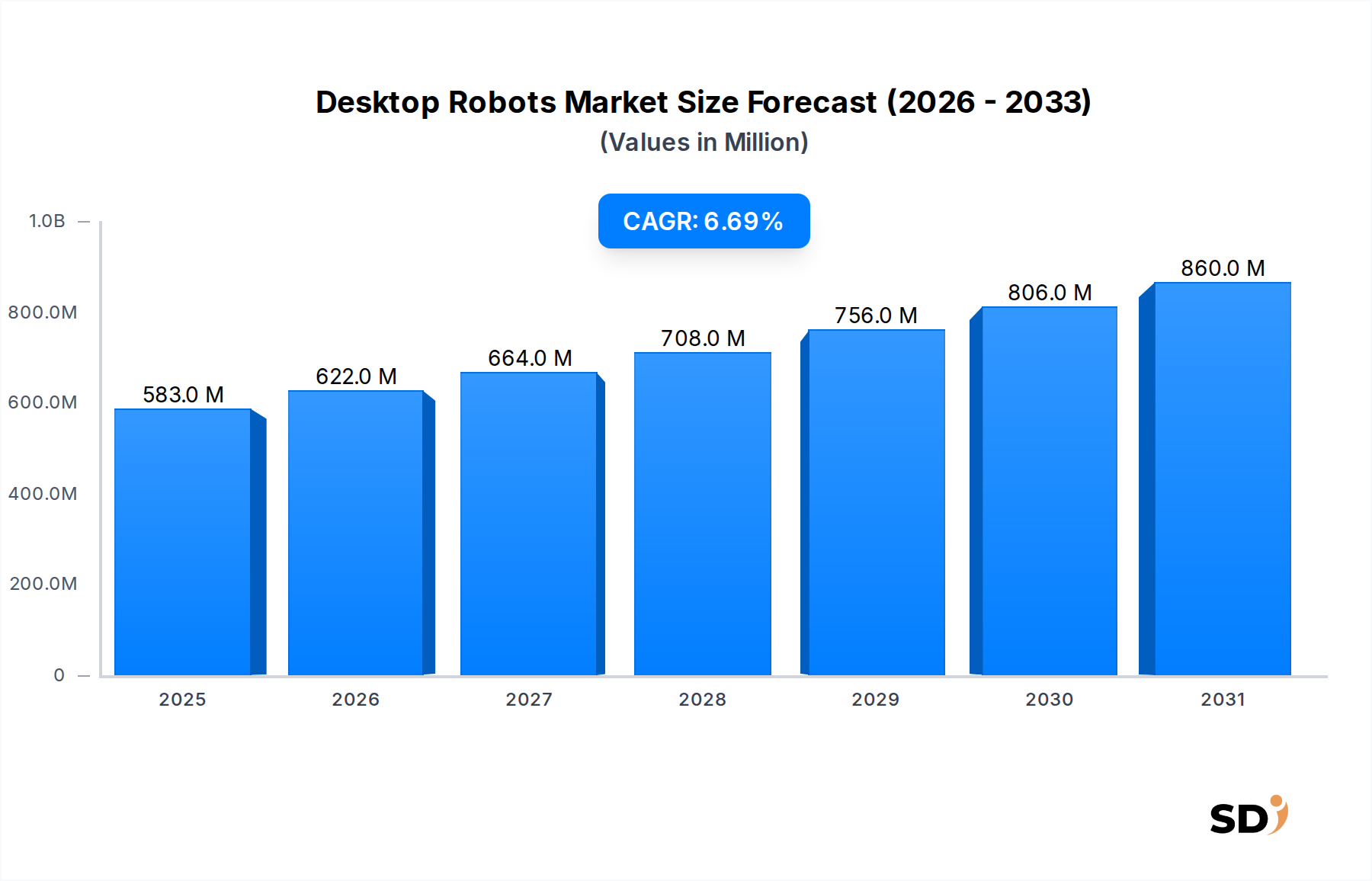

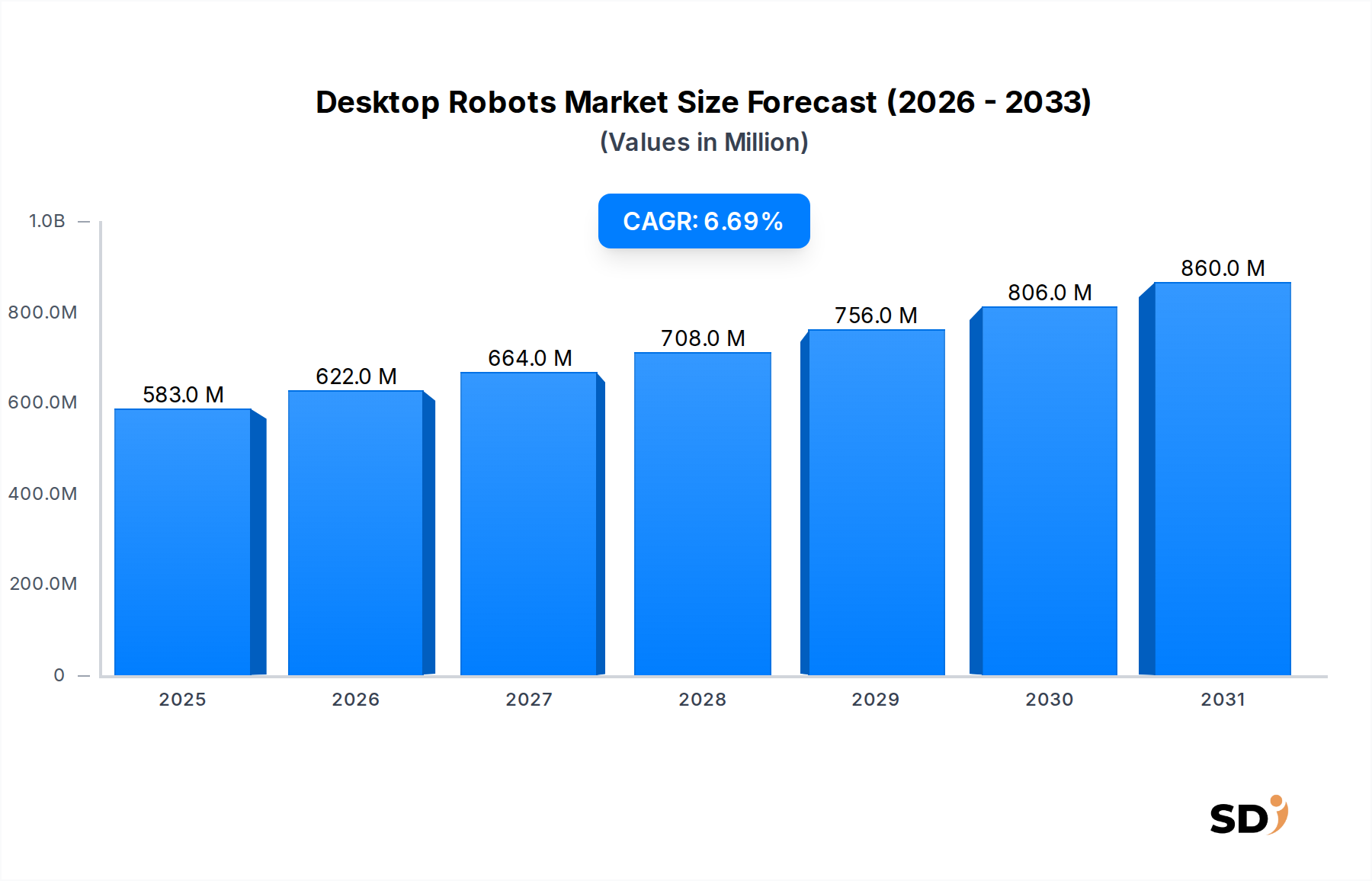

The Desktop Robots Market is poised for significant expansion, driven by advancements in miniaturization, artificial intelligence, and increasing consumer appetite for interactive and functional smart devices. Valued at an estimated $583 million in the base year (note: base year not provided in data, standard assumption for recent historical data point), the market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 6.7% over the forecast period. This growth trajectory is underpinned by several macro tailwinds, including the proliferation of smart home ecosystems, rising disposable incomes in emerging economies, and the growing integration of AI and machine learning capabilities into consumer electronics. The market's current valuation reflects a nascent but rapidly maturing sector, moving beyond novelty to offer tangible utility in various settings.

Desktop Robots Market Size (In Million)

1.0B

800.0M

600.0M

400.0M

200.0M

0

583.0 M

2025

622.0 M

2026

664.0 M

2027

708.0 M

2028

756.0 M

2029

806.0 M

2030

860.0 M

2031

Key demand drivers include the increasing adoption of desktop robots for educational purposes, providing hands-on learning experiences in coding and robotics. Furthermore, the burgeoning demand for companion robots, especially those with advanced emotional intelligence and interactive capabilities, significantly contributes to market expansion. The integration of desktop robots with broader Smart Home Devices Market ecosystems further enhances their value proposition, allowing for seamless automation and control. Technological advancements in areas such as natural language processing (NLP), computer vision, and haptic feedback are continuously improving robot-human interaction, making these devices more intuitive and appealing to a wider demographic. The forecast period anticipates continued innovation, leading to more affordable, versatile, and user-friendly desktop robots, thereby accelerating market penetration across consumer and prosumer segments. The shift towards greater computational power at the edge, coupled with enhanced connectivity options, is also enabling more sophisticated functionalities without relying heavily on cloud processing, improving response times and privacy. This dynamic landscape indicates a strong forward-looking outlook, with sustained investment in R&D driving competitive product differentiation and market growth.

Functional Type Segment Dominance in Desktop Robots Market

Within the Desktop Robots Market, the 'Functional Type' segment currently holds the dominant revenue share, a trend expected to persist throughout the forecast period. This segment encompasses desktop robots designed for specific tasks and utilities beyond mere companionship, such as those used for coding education, small-scale automation, developer platforms, or even basic home assistance. Its dominance is attributable to the broader applicability and perceived value for money these robots offer. Unlike 'Pet Type' robots, which primarily cater to emotional companionship and entertainment, functional types often serve multiple purposes, making them attractive to a wider consumer base including hobbyists, educators, developers, and early adopters of smart home technology.

Companies like Misty Robotics and Digital Dream Labs (with their Vector and Cozmo robots) exemplify the success within the Functional Type segment. Misty Robotics' platforms are designed for developers, offering programmable interfaces for custom applications in education, research, and business. Digital Dream Labs' robots, while having a companionable aspect, are fundamentally tools for learning coding and robotics concepts, embodying the functional utility. The segment's growth is further propelled by the increasing accessibility of development kits and open-source platforms, fostering a vibrant ecosystem of third-party applications and customizations. This allows functional desktop robots to evolve rapidly, adapting to new user needs and technological advancements. The ongoing expansion of the Educational Robotics Market is a direct driver for this segment, as schools, STEM programs, and individual learners seek engaging tools to teach fundamental coding and engineering principles. The versatility of functional robots also allows them to integrate into nascent Smart Home Devices Market strategies, acting as mobile interfaces or specialized sensors within a connected environment. While the Humanoid Robot Market represents a broader category, many desktop robots, especially those designed for interaction or specific tasks, often adopt a humanoid or pseudo-humanoid form factor to enhance user engagement, further blurring the lines but solidifying the functional aspect as primary. The initial investment in a functional robot is often justified by its ability to perform useful tasks, thereby accelerating its adoption compared to purely recreational counterparts, leading to its sustained market leadership.

Technological Advancements Driving the Desktop Robots Market

The Desktop Robots Market is fundamentally shaped by rapid technological advancements, transforming these devices from simple gadgets into sophisticated, interactive assistants. One key driver is the exponential growth and accessibility of the Artificial Intelligence Market. The integration of advanced AI algorithms, particularly in areas like natural language processing, computer vision, and machine learning, has enabled desktop robots to understand complex commands, recognize faces, interpret emotions, and learn from interactions. For instance, the sophistication of AI allows robots to execute context-aware responses, moving beyond pre-programmed scripts to offer truly personalized experiences, thereby enhancing user engagement and utility. The increasing computational power of miniaturized processors, coupled with optimized AI models, allows for more on-device processing, reducing latency and improving responsiveness, which is crucial for real-time interaction.

Another significant driver is the continuous innovation within the Sensor Market. Modern desktop robots are equipped with an array of sensors, including proximity sensors, touch sensors, microphones, and high-resolution cameras, enabling them to perceive and interpret their environment with increasing accuracy. These sensors feed data to the robot's AI, allowing for more nuanced interactions, obstacle avoidance, and object recognition. For example, advancements in time-of-flight (ToF) sensors or structured light sensors enhance depth perception, crucial for navigation and manipulation tasks. Simultaneously, the Actuators Market plays a pivotal role. Improvements in micro-motors, servo systems, and haptic feedback mechanisms have led to more precise, quieter, and energy-efficient movements, making robots like Living.AI's Eilik or Aibo's robotic pets capable of expressing a wide range of emotions and performing fluid actions. These mechanical advancements are critical for creating realistic and engaging physical interactions, directly impacting the perceived quality and functionality of the robots. The drive towards greater affordability of these advanced components further fuels the market, making sophisticated desktop robots accessible to a broader consumer base, thereby democratizing advanced robotics.

Competitive Ecosystem of Desktop Robots Market

The competitive landscape of the Desktop Robots Market is characterized by a mix of established tech giants exploring the space and innovative startups specializing in consumer robotics. Innovation in AI and hardware design is a primary differentiator.

Living.AI: A company known for its desktop companion robot, Eilik, which aims to provide emotional interaction through advanced animation and personality traits, tapping into the Interactive Entertainment Market for unique pet-like experiences.

Misty Robotics: Focuses on professional and developer-friendly robots, offering a programmable platform for various applications, including education, research, and small business uses, often appealing to the Personal Robotics Market segment looking for customizable solutions.

Digital Dream Labs: Known for acquiring assets like Vector and Cozmo, these robots blend companionable AI with educational programming capabilities, catering to both the companion and Educational Robotics Market.

Aibo (Sony): A veteran in the robotic pet space, Sony's Aibo series represents high-end companion robots with sophisticated AI, movement, and interaction capabilities, leveraging advanced robotics to create lifelike experiences.

Letianpai: A Chinese manufacturer often involved in the broader consumer electronics and robotics market, contributing to the competitive landscape with its offerings, often at a more accessible price point.

Eilik: (Already covered as Living.AI's product) As a specific product from Living.AI, it's a direct competitor focusing on emotional intelligence and engaging interactions for individual users.

TangibleFuture: Developing innovative robotics and AI solutions, aiming to push the boundaries of human-robot interaction in various applications.

Amazon: While not having a direct desktop robot product in the traditional sense, Amazon's influence through Alexa-enabled devices and Astro (a larger home robot) indicates strategic interest in home robotics, leveraging its Artificial Intelligence Market leadership.

Google: With its extensive AI and software capabilities, Google continuously explores robotics applications, particularly in AI-driven smart devices and potential future personal robotics, often through research initiatives or partnerships.

Apple: Known for its integrated ecosystem, Apple's potential entry or deeper involvement in home robotics could significantly disrupt the market, focusing on seamless user experience and privacy, leveraging its hardware and software prowess.

Xiaomi: A global consumer electronics giant, Xiaomi frequently enters emerging markets with cost-effective, feature-rich products, including various smart home devices and early ventures into robotics, contributing to the Smart Home Devices Market with intelligent products.

Baidu: As a leading AI company in China, Baidu is heavily invested in AI and autonomous technologies, with potential applications extending to home and desktop robotics, similar to Google's strategic approach.

Recent Developments & Milestones in Desktop Robots Market

December 2023: Living.AI announced new firmware updates for its Eilik robot, enhancing emotional responses and introducing new interactive games, further solidifying its position in the Personal Robotics Market for companion devices.

October 2023: Digital Dream Labs released a major software update for Vector, improving voice recognition accuracy and integrating new smart home functionalities, aiming to broaden its appeal within the Smart Home Devices Market.

August 2023: A leading educational technology provider partnered with a desktop robot manufacturer to integrate programmable robots into their STEM curriculum, highlighting the growing synergy with the Educational Robotics Market.

June 2023: Advancements in the Sensor Market led to the commercial availability of more compact and affordable high-precision LiDAR modules, potentially enabling more sophisticated navigation and environmental mapping capabilities for future desktop robots.

April 2023: A startup specializing in haptic feedback technology secured significant funding to develop next-generation miniature Actuators Market components, promising more realistic tactile interactions for small-scale robots.

February 2023: Researchers unveiled a new AI model for small-form-factor robots, capable of more complex real-time emotional recognition and adaptive learning, showcasing the continuous innovation within the Artificial Intelligence Market relevant to desktop robotics.

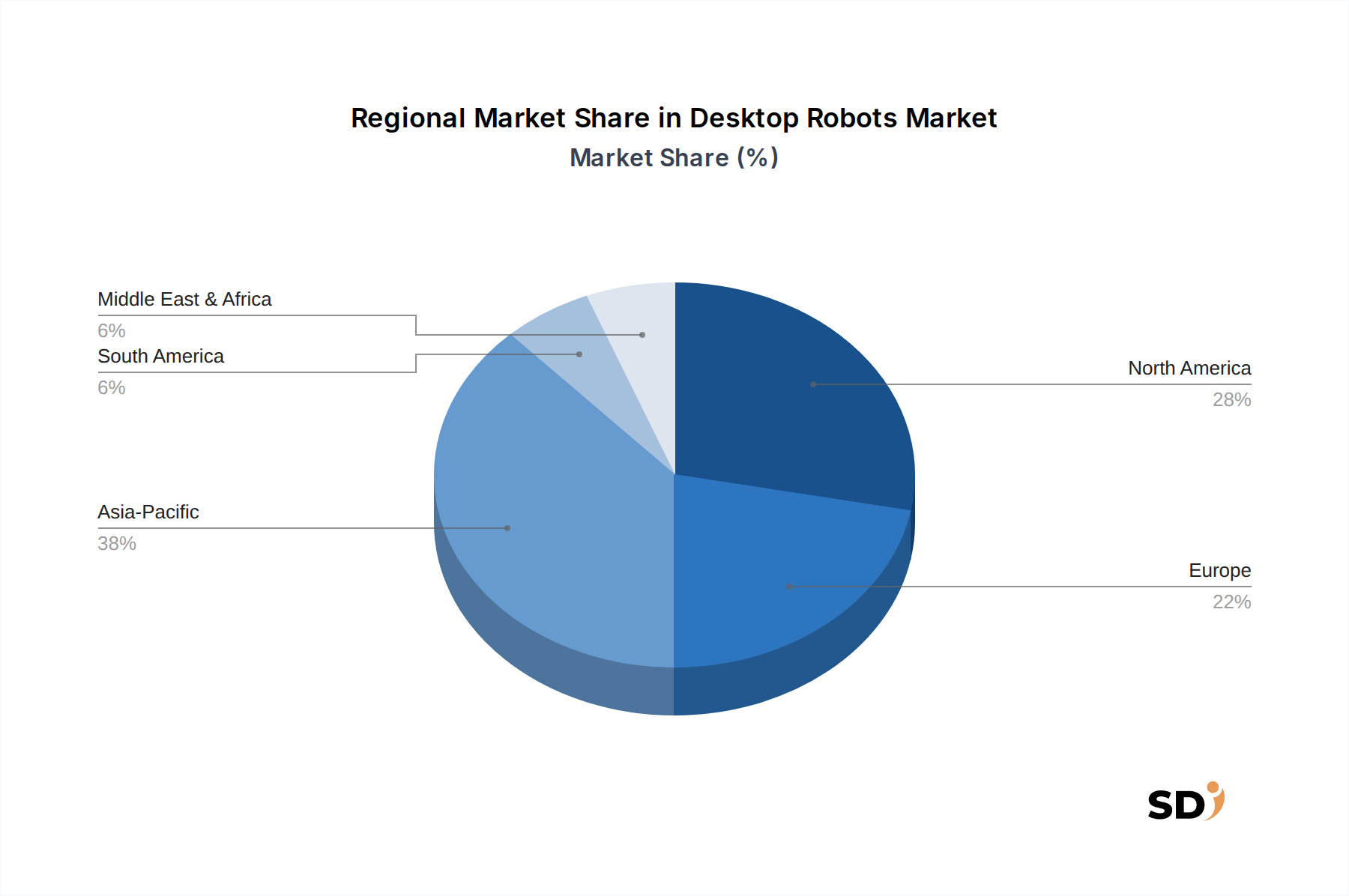

Regional Market Breakdown for Desktop Robots Market

The Desktop Robots Market exhibits diverse growth patterns across key regions, driven by varying technological adoption rates, disposable incomes, and cultural preferences. Asia Pacific currently commands a significant revenue share and is projected to be the fastest-growing region, fueled by robust economic growth, increasing investment in STEM education, and a strong manufacturing base for electronics. Countries like China, Japan, and South Korea are at the forefront of adopting and developing advanced robotics, with a high consumer propensity for innovative tech products, including those in the Personal Robotics Market. The region's CAGR is estimated to be around 8.5%, driven by the expansion of the Educational Robotics Market and the increasing popularity of companion robots in households.

North America represents a mature yet substantial market, holding a considerable revenue share due to high disposable incomes, early adoption of smart home technologies, and a strong presence of key market players and research institutions. The primary demand driver here is the continued integration of desktop robots into smart home ecosystems and their use as sophisticated educational tools. Its CAGR is expected to be steady at approximately 5.8%, reflecting continued innovation and consumer interest in advanced, interactive devices. The demand for products integrating with the Artificial Intelligence Market is particularly strong.

Europe, another established market, follows closely behind North America in terms of revenue share. Demand is primarily driven by strong research and development initiatives, a focus on educational technology, and a growing interest in personalized tech. Countries like Germany, the UK, and France are significant contributors, with a projected CAGR of about 6.2%. The region's regulatory environment, while sometimes stringent, also fosters high-quality product development and consumer trust, impacting the growth of the broader Interactive Entertainment Market for robots.

The Middle East & Africa and South America regions currently hold smaller shares but are emerging markets with significant potential. Growth in these regions is primarily spurred by increasing internet penetration, rising consumer awareness of smart technologies, and government initiatives promoting technological education. While starting from a lower base, these regions are expected to demonstrate higher growth rates in specific segments as affordability improves and awareness grows, particularly for products that integrate with the Smart Home Devices Market and entry-level Personal Robotics Market offerings.

Supply Chain & Raw Material Dynamics for Desktop Robots Market

The Desktop Robots Market supply chain is intricate, characterized by globalized sourcing of specialized components and susceptibility to geopolitical and economic fluctuations. Upstream dependencies are significant, relying heavily on the Semiconductor Market for microcontrollers, processors, and memory chips, which form the computational backbone of these devices. Price volatility in this market, exacerbated by global supply shortages and trade tensions, directly impacts the manufacturing cost of desktop robots. Key raw materials also include various grades of Plastics Market (e.g., ABS, polycarbonate) for chassis and aesthetic components, Metals Market (e.g., aluminum, steel alloys) for structural elements and internal mechanisms, and Rare Earth Elements Market for advanced magnets used in Actuators Market and Sensor Market components.

The sourcing risks are multifaceted, including single-source dependencies for highly specialized sensors or proprietary AI chips, logistical disruptions, and fluctuating energy costs affecting transportation. Historically, events like the COVID-19 pandemic significantly disrupted the supply of electronic components, leading to increased lead times and escalated prices, delaying product launches and impacting profit margins across the Desktop Robots Market. For instance, the demand surge for consumer electronics during lockdowns put immense pressure on Microcontroller Market and Display Panel Market suppliers, with ripple effects felt by robotics manufacturers. Manufacturers continuously seek to diversify their supplier base and optimize inventory management to mitigate these risks. Trends show a move towards regionalized manufacturing where possible to shorten supply lines and reduce reliance on distant supply chains, though core component manufacturing remains highly concentrated in specific Asian regions. Furthermore, the ethical sourcing of raw materials, particularly rare earth elements, is gaining prominence, adding another layer of complexity to supply chain management and potentially influencing material costs.

The Desktop Robots Market operates within an evolving regulatory and policy landscape, primarily driven by concerns around data privacy, product safety, and ethical AI deployment. Across key geographies, a patchwork of regulations influences market entry and product design. In the European Union, the General Data Protection Regulation (GDPR) sets stringent requirements for how personal data, including biometric data collected by robot cameras and microphones, is handled. This mandates robust data encryption, clear consent mechanisms, and transparent data processing policies, directly impacting the design of desktop robots with advanced perception capabilities. The upcoming AI Act in the EU further categorizes AI systems based on risk, with companion robots potentially falling under 'limited risk' or 'high-risk' depending on their functionalities, imposing specific compliance obligations regarding transparency, human oversight, and safety. This framework could significantly shape the development of advanced AI in the Personal Robotics Market.

In North America, particularly the United States, consumer protection laws and sector-specific regulations apply. The Federal Trade Commission (FTC) oversees data privacy and fair trade practices, ensuring that marketing claims for desktop robots are not misleading and that user data is protected. Industry standards from organizations like IEEE and ISO also play a crucial role in establishing best practices for robotics safety and interoperability, influencing component selection from the Sensor Market and Actuators Market. Recent policy discussions have also touched upon the ethical implications of AI, especially in relation to algorithmic bias and potential misuse, pushing developers to adopt 'responsible AI' principles from the outset. In Asia Pacific, countries like Japan and South Korea have national strategies to promote robotics innovation, often providing incentives for R&D while also developing specific safety guidelines for human-robot interaction in various settings, including the home. China has also rapidly advanced its regulatory framework for AI and data security, directly impacting domestic and international players in the Desktop Robots Market. Compliance with these diverse and dynamic regulations adds complexity to product development and market expansion, often necessitating significant legal and technical resources for manufacturers to navigate effectively.

Desktop Robots Segmentation

1. Application

1.1. Offline

1.2. Online

2. Types

2.1. Functional Type

2.2. Pet Type

Desktop Robots Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Desktop Robots REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 6.7% from 2020-2034

Segmentation

By Application

Offline

Online

By Types

Functional Type

Pet Type

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Offline

5.1.2. Online

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Functional Type

5.2.2. Pet Type

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Offline

6.1.2. Online

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Functional Type

6.2.2. Pet Type

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Offline

7.1.2. Online

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Functional Type

7.2.2. Pet Type

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Offline

8.1.2. Online

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Functional Type

8.2.2. Pet Type

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Offline

9.1.2. Online

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Functional Type

9.2.2. Pet Type

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Offline

10.1.2. Online

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Functional Type

10.2.2. Pet Type

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Living.AI

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Misty Robotics

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Digital Dream Labs

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Aibo (Sony)

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Letianpai

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Eilik

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. TangibleFuture

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Amazon

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Google

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Apple

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Xiaomi

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Baidu

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (million), by Application 2025 & 2033

Figure 4: Volume (K), by Application 2025 & 2033

Figure 5: Revenue Share (%), by Application 2025 & 2033

Figure 6: Volume Share (%), by Application 2025 & 2033

Figure 7: Revenue (million), by Types 2025 & 2033

Figure 8: Volume (K), by Types 2025 & 2033

Figure 9: Revenue Share (%), by Types 2025 & 2033

Figure 10: Volume Share (%), by Types 2025 & 2033

Figure 11: Revenue (million), by Country 2025 & 2033

Figure 12: Volume (K), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Volume Share (%), by Country 2025 & 2033

Figure 15: Revenue (million), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (million), by Types 2025 & 2033

Figure 20: Volume (K), by Types 2025 & 2033

Figure 21: Revenue Share (%), by Types 2025 & 2033

Figure 22: Volume Share (%), by Types 2025 & 2033

Figure 23: Revenue (million), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (million), by Application 2025 & 2033

Figure 28: Volume (K), by Application 2025 & 2033

Figure 29: Revenue Share (%), by Application 2025 & 2033

Figure 30: Volume Share (%), by Application 2025 & 2033

Figure 31: Revenue (million), by Types 2025 & 2033

Figure 32: Volume (K), by Types 2025 & 2033

Figure 33: Revenue Share (%), by Types 2025 & 2033

Figure 34: Volume Share (%), by Types 2025 & 2033

Figure 35: Revenue (million), by Country 2025 & 2033

Figure 36: Volume (K), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Volume Share (%), by Country 2025 & 2033

Figure 39: Revenue (million), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (million), by Types 2025 & 2033

Figure 44: Volume (K), by Types 2025 & 2033

Figure 45: Revenue Share (%), by Types 2025 & 2033

Figure 46: Volume Share (%), by Types 2025 & 2033

Figure 47: Revenue (million), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (million), by Application 2025 & 2033

Figure 52: Volume (K), by Application 2025 & 2033

Figure 53: Revenue Share (%), by Application 2025 & 2033

Figure 54: Volume Share (%), by Application 2025 & 2033

Figure 55: Revenue (million), by Types 2025 & 2033

Figure 56: Volume (K), by Types 2025 & 2033

Figure 57: Revenue Share (%), by Types 2025 & 2033

Figure 58: Volume Share (%), by Types 2025 & 2033

Figure 59: Revenue (million), by Country 2025 & 2033

Figure 60: Volume (K), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

Figure 62: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Volume K Forecast, by Application 2020 & 2033

Table 3: Revenue million Forecast, by Types 2020 & 2033

Table 4: Volume K Forecast, by Types 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Volume K Forecast, by Region 2020 & 2033

Table 7: Revenue million Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue million Forecast, by Types 2020 & 2033

Table 10: Volume K Forecast, by Types 2020 & 2033

Table 11: Revenue million Forecast, by Country 2020 & 2033

Table 12: Volume K Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Volume (K) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Volume (K) Forecast, by Application 2020 & 2033

Table 17: Revenue (million) Forecast, by Application 2020 & 2033

Table 18: Volume (K) Forecast, by Application 2020 & 2033

Table 19: Revenue million Forecast, by Application 2020 & 2033

Table 20: Volume K Forecast, by Application 2020 & 2033

Table 21: Revenue million Forecast, by Types 2020 & 2033

Table 22: Volume K Forecast, by Types 2020 & 2033

Table 23: Revenue million Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue million Forecast, by Application 2020 & 2033

Table 32: Volume K Forecast, by Application 2020 & 2033

Table 33: Revenue million Forecast, by Types 2020 & 2033

Table 34: Volume K Forecast, by Types 2020 & 2033

Table 35: Revenue million Forecast, by Country 2020 & 2033

Table 36: Volume K Forecast, by Country 2020 & 2033

Table 37: Revenue (million) Forecast, by Application 2020 & 2033

Table 38: Volume (K) Forecast, by Application 2020 & 2033

Table 39: Revenue (million) Forecast, by Application 2020 & 2033

Table 40: Volume (K) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Volume (K) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (million) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue (million) Forecast, by Application 2020 & 2033

Table 50: Volume (K) Forecast, by Application 2020 & 2033

Table 51: Revenue (million) Forecast, by Application 2020 & 2033

Table 52: Volume (K) Forecast, by Application 2020 & 2033

Table 53: Revenue (million) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue million Forecast, by Application 2020 & 2033

Table 56: Volume K Forecast, by Application 2020 & 2033

Table 57: Revenue million Forecast, by Types 2020 & 2033

Table 58: Volume K Forecast, by Types 2020 & 2033

Table 59: Revenue million Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (million) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (million) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (million) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (million) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (million) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (million) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue million Forecast, by Application 2020 & 2033

Table 74: Volume K Forecast, by Application 2020 & 2033

Table 75: Revenue million Forecast, by Types 2020 & 2033

Table 76: Volume K Forecast, by Types 2020 & 2033

Table 77: Revenue million Forecast, by Country 2020 & 2033

Table 78: Volume K Forecast, by Country 2020 & 2033

Table 79: Revenue (million) Forecast, by Application 2020 & 2033

Table 80: Volume (K) Forecast, by Application 2020 & 2033

Table 81: Revenue (million) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue (million) Forecast, by Application 2020 & 2033

Table 84: Volume (K) Forecast, by Application 2020 & 2033

Table 85: Revenue (million) Forecast, by Application 2020 & 2033

Table 86: Volume (K) Forecast, by Application 2020 & 2033

Table 87: Revenue (million) Forecast, by Application 2020 & 2033

Table 88: Volume (K) Forecast, by Application 2020 & 2033

Table 89: Revenue (million) Forecast, by Application 2020 & 2033

Table 90: Volume (K) Forecast, by Application 2020 & 2033

Table 91: Revenue (million) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research strategy forms the cornerstone of our market intelligence, accounting for 75% of the overall research effort. This robust approach involves extensive qualitative and quantitative interviews with key opinion leaders, industry experts, and stakeholders across the value chain. The objective is to gather first-hand insights into market dynamics, trends, competitive landscape, technological advancements, and regional nuances specific to the Desktop Robots market. Our interviews are structured to validate data obtained from secondary sources and to uncover proprietary information crucial for accurate market sizing and forecasting.

Key participants in our primary research include:

Company Types:

Consumer Robotics Manufacturers

Robotics Component Suppliers

AI/Software Development Firms

E-commerce & Retail Distributors

Educational Robotics Platform Providers

Stakeholder Job Titles:

VP of Product Management, Consumer Robotics

Director of Robotics Software Engineering

Category Buyer/Manager, Smart Home & Personal Robotics

Head of Marketing & Brand Strategy, Robotics Division

Our global outreach ensures representation from all major regions, including North America, South America, Europe, Middle East & Africa, and Asia Pacific, providing a comprehensive understanding of diverse market conditions and growth drivers.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP of Product Management, Consumer Robotics

30%

Director of Robotics Software Engineering

25%

Category Buyer/Manager, Smart Home & Personal Robotics

25%

Head of Marketing & Brand Strategy, Robotics Division

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Consumer Robotics Manufacturers

30%

Robotics Component Suppliers

20%

AI/Software Development Firms

15%

E-commerce & Retail Distributors

25%

Educational Robotics Platform Providers

10%

Secondary Research & Industry Benchmarking

Secondary research contributes approximately 25% to our total research methodology, providing foundational data and industry benchmarks. This phase involves a rigorous review of published reports, company filings, investor presentations, and industry whitepapers. We meticulously extract macroeconomic indicators, technological advancements, regulatory frameworks, and demographic data pertinent to the Desktop Robots market.

Our secondary research sources include, but are not limited to:

Government & Organizational Data: Data from national statistical offices, innovation agencies, and departments of commerce (e.g., U.S. Census Bureau, Eurostat, World Bank Data).

Trade Associations & Industry Bodies: Publications and statistics from globally recognized organizations directly impacting robotics and consumer technology. These include:

International Federation of Robotics (IFR) (ifr.org)

IEEE Robotics and Automation Society (IEEE RAS) (ieee-ras.org)

Association for Advancing Automation (A3) (automate.org)

We strictly avoid data from other market research websites to maintain the originality and integrity of our findings. Every data point and market insight in this report is updated up to the date of purchase, ensuring relevance and timeliness.

Demand Modeling & Market Estimation

Our market estimation process employs a robust combination of top-down and bottom-up methodologies, complemented by multi-level data triangulation to ensure maximum accuracy.

Bottom-Up Approach: This method involves segmenting the total market by application (Offline, Online), type (Functional Type, Pet Type), and granular geographic regions. We estimate the market size by aggregating data from individual companies, distributors, and end-user segments. Key metrics and variables leveraged for bottom-up calculation include:

Average Selling Price (ASP) per Desktop Robot Unit (segmented by type and functionality)

Annual Unit Shipments/Sales Volume (by manufacturer, application, and geography)

Retail Channel Sales Data (online vs. offline distribution percentages)

Consumer Demographics & Disposable Income Trends (correlated with adoption rates for leisure tech)

Top-Down Approach: Simultaneously, we use the top-down approach, starting with broader market indicators such as overall consumer electronics spending, global robotics market size, and relevant demographic trends. This allows us to derive the overall Desktop Robots market size, which is then disaggregated into specific segments and geographies based on established ratios and growth rates.

Data Triangulation: All market figures are subjected to multi-level data triangulation, involving cross-referencing information from primary interviews, secondary sources, and our internal proprietary databases. This iterative process helps to resolve discrepancies and strengthen the reliability of our market estimates, leading to highly defensible market figures.

Data Accuracy & Quality Check

Our commitment to data integrity is paramount. We employ a rigorous, multi-stage data validation and quality check process to ensure the highest degree of accuracy in our market estimations. All collected data, whether from primary or secondary sources, undergoes thorough scrutiny by a dedicated team of analysts. Discrepancies are flagged, re-verified, and reconciled through additional research and expert consultations. We leverage statistical tools and proprietary analytical frameworks to identify and mitigate potential biases, ensuring that the market figures reflect the true market landscape. Through this meticulous process, we guarantee an estimated data accuracy level of 85-90% for our Desktop Robots market report.

Frequently Asked Questions

1. What are the primary export-import dynamics influencing the Desktop Robots market?

The market for Desktop Robots primarily sees manufacturing hubs in Asia-Pacific exporting to North American and European consumer markets. Component sourcing is often global, with final assembly concentrated in specialized tech regions, impacting international trade flows.

2. What is the current market size and projected CAGR for Desktop Robots?

The Desktop Robots market is valued at $583 million. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7%, indicating steady expansion through the forecast period.

3. What are the key barriers to entry in the Desktop Robots market?

Significant barriers include high R&D costs for advanced robotics, the need for specialized software and hardware integration, and establishing brand trust in a consumer electronics segment. Intellectual property and patent portfolios held by major players like Aibo (Sony) and Living.AI also create strong competitive moats.

4. What major challenges or restraints face the Desktop Robots market?

Key challenges include high initial product costs for consumers, limited perceived utility for some models, and privacy concerns associated with connected devices. Supply chain risks for specialized components and rapidly evolving technological standards also pose restraints.

5. How did the Desktop Robots market recover post-pandemic, and what are the long-term shifts?

The post-pandemic period saw accelerated adoption of in-home entertainment and personal assistance technologies, including Desktop Robots, benefiting from increased time spent at home. This led to sustained demand for both functional and pet-type robots, cementing a long-term shift towards smart home integration.

6. What primary growth drivers and demand catalysts influence Desktop Robots?

Growth is driven by advancements in AI and robotics, increasing consumer disposable income, and demand for companionship and automation in homes. The expansion of functional and pet-type robot segments, alongside product innovations from companies like Eilik and Digital Dream Labs, fuels market expansion.