Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Derma Cosmetics by Application (Dry Skin, Oily Skin, Combination Skin, Sensitive Skin), by Types (Cream Products, Liquid & Lotion Products, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 11, 2026|Base Year : 2025|Pages : 92

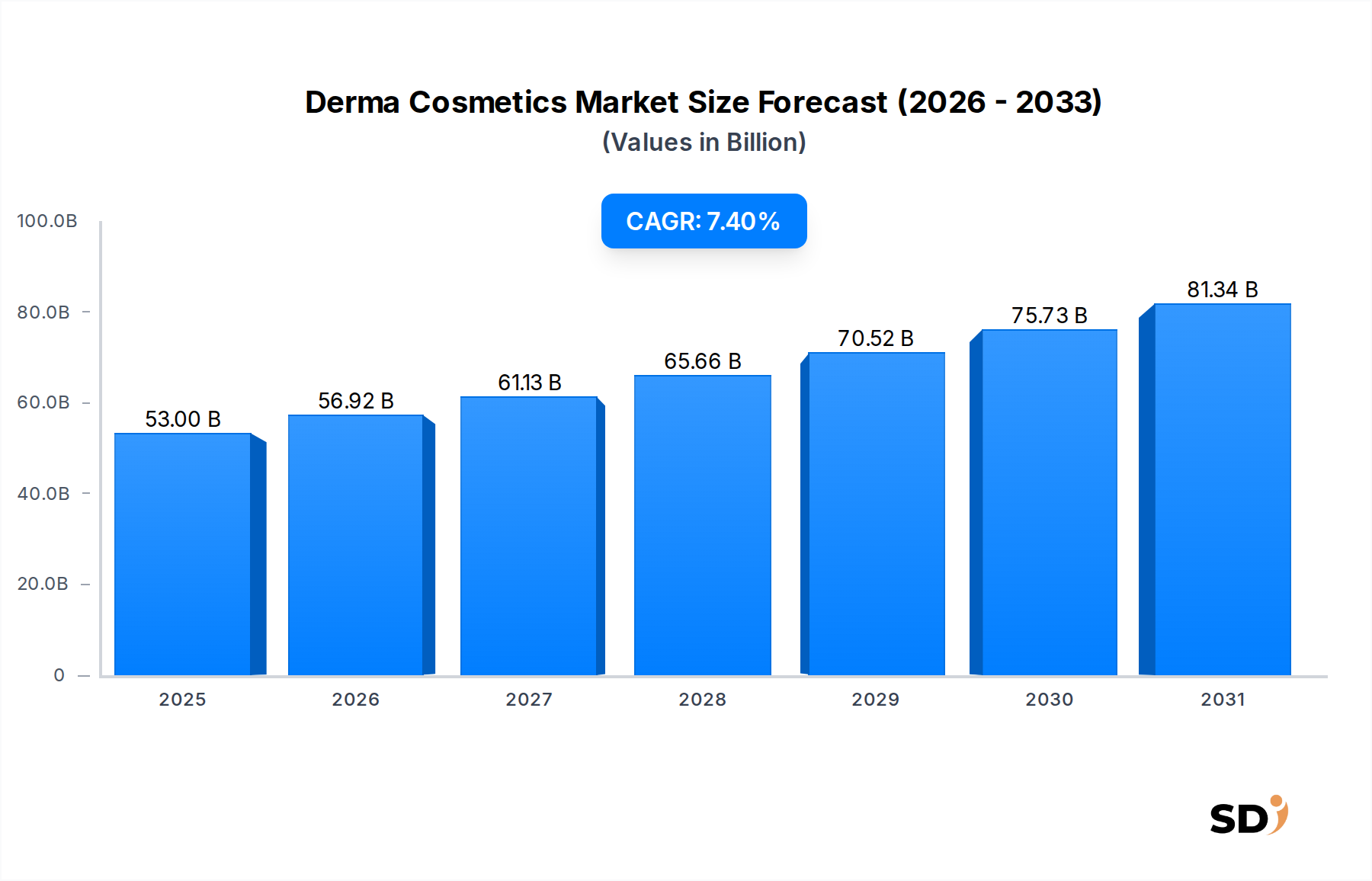

The global Derma Cosmetics Market was valued at USD 53 billion in 2025, demonstrating robust growth driven by escalating consumer awareness regarding skin health and the increasing prevalence of dermatological conditions. Projections indicate that the market is set to expand at a compound annual growth rate (CAGR) of 7.4% from 2025 to 2030, reaching an estimated valuation of USD 75.83 billion by 2030. This upward trajectory is underpinned by several macro tailwinds, including a rising disposable income in emerging economies, an aging global population seeking effective anti-aging solutions, and technological advancements in product formulation and delivery systems. The convergence of cosmetics with dermatology, leading to products that offer both aesthetic enhancement and therapeutic benefits, is a primary catalyst. Furthermore, the growing trend of preventive skincare, coupled with increased consumer demand for scientifically-backed and dermatologist-recommended products, continues to fuel market expansion. Innovations in active ingredients, particularly those derived from natural sources or developed through advanced scientific processes, are enhancing product efficacy and consumer trust. The strategic emphasis by leading players on research and development to address specific skin concerns such as sensitivity, acne, and hyperpigmentation also contributes significantly to market dynamism. The future outlook for the Derma Cosmetics Market remains highly positive, characterized by sustained innovation, expanding geographical reach, and an evolving regulatory landscape that supports product safety and claims validation. This specialized segment is becoming an indispensable part of the broader Skincare Products Market.

Derma Cosmetics Market Size (In Billion)

100.0B

80.0B

60.0B

40.0B

20.0B

0

53.00 B

2025

56.92 B

2026

61.13 B

2027

65.66 B

2028

70.52 B

2029

75.73 B

2030

81.34 B

2031

Sensitive Skin Care Segment Dominance in Derma Cosmetics Market

Within the global Derma Cosmetics Market, the Sensitive Skin Care Market segment, categorized under application, exhibits a dominant revenue share and is poised for continued expansion. This dominance is primarily attributable to a significant increase in the global population experiencing skin sensitivity, often triggered by environmental aggressors, lifestyle changes, and the widespread use of harsh cosmetic products. Consumers are increasingly turning to derma cosmetics specifically formulated to soothe, protect, and restore the barrier function of sensitive skin, driven by recommendations from dermatologists and increasing self-diagnosis. Products catering to sensitive skin typically feature hypoallergenic formulations, are free from irritants such as fragrances, parabens, and certain dyes, and incorporate calming ingredients like ceramides, hyaluronic acid, and thermal spring water. Major players in the Derma Cosmetics Market, including L'Oreal (through brands like La Roche-Posay and Vichy) and Johnson & Johnson (with Aveeno and Neutrogena sensitive skin lines), have heavily invested in this segment, launching extensive product portfolios encompassing cleansers, moisturizers, serums, and sunscreens tailored for delicate skin types. This strategic focus has not only solidified the segment's leading position but also contributed to its consistent growth, as brand loyalty tends to be high among sensitive skin consumers who find products that genuinely work for them. The emphasis on clinical testing and endorsement by dermatological professionals further instills confidence and drives demand within the Sensitive Skin Care Market. While other application segments like Oily Skin, Dry Skin, and Combination Skin also contribute substantially, the acute and often chronic nature of sensitive skin conditions necessitates ongoing, specialized care, translating into sustained purchases and a larger market share. The segment's growth is further bolstered by product innovations, such as microbiome-friendly formulations and advanced soothing complexes, which offer enhanced efficacy and better long-term skin health benefits. This trend reflects a broader consumer shift towards holistic and preventive dermatological solutions.

Key Market Drivers and Constraints in the Derma Cosmetics Market

The Derma Cosmetics Market is influenced by a complex interplay of demand drivers and inherent constraints. One significant driver is the escalating global prevalence of skin disorders and conditions, such as acne, eczema, rosacea, and hyperpigmentation. For instance, according to recent dermatological surveys, nearly 80% of individuals between 11 and 30 years of age experience acne, and a significant portion of the adult population reports sensitive skin issues. This widespread incidence directly translates into a higher demand for specialized derma cosmetic products that offer therapeutic efficacy beyond traditional beauty products. Another key driver is the heightened consumer awareness regarding ingredient efficacy and product safety. Consumers, empowered by digital information, are increasingly scrutinizing product labels and seeking formulations backed by scientific research and clinical trials. This trend is fostering growth in the Biotechnology in Cosmetics Market, as advanced biotechnological ingredients gain traction. Conversely, a primary constraint impacting the Derma Cosmetics Market is the stringent regulatory landscape governing product claims and ingredient safety. Regulatory bodies like the FDA in the U.S. and the European Medicines Agency (EMA) impose rigorous testing and approval processes for ingredients and finished products, leading to prolonged development cycles and elevated R&D costs. For example, obtaining regulatory approval for a novel active ingredient can take several years and millions of dollars in investment. The premium pricing associated with many derma cosmetic products, driven by extensive R&D, specialized ingredients sourced from the Specialty Chemicals Market, and clinical validation, also acts as a constraint, particularly in price-sensitive markets. While consumers are willing to pay more for proven efficacy, this pricing strategy can limit mass-market penetration compared to conventional cosmetic products. Furthermore, the reliance on professional recommendations (dermatologists, pharmacists) can create a bottleneck, as product adoption often hinges on expert endorsement. Despite these constraints, the underlying demand for effective and safe skincare solutions ensures the market’s robust expansion.

Competitive Ecosystem of Derma Cosmetics Market

The Derma Cosmetics Market features a highly competitive landscape, characterized by global conglomerates and specialized dermatological brands vying for market share. Key players are strategically focused on product innovation, clinical validation, and strong professional endorsements.

L'Oreal: A global leader in beauty, L'Oreal boasts a strong presence in the derma cosmetics segment through its active cosmetics division, featuring brands like La Roche-Posay, Vichy, and CeraVe, focusing on dermatological solutions for various skin concerns.

Christine Schrammek Kosmetik: Known for its pioneering Green Peel herbal peeling treatment, this German brand offers a comprehensive range of derma cosmetic products with a focus on problem-solving skincare solutions.

Procter & Gamble: A consumer goods giant, P&G competes in derma cosmetics with brands like Olay and SK-II, integrating advanced scientific research into their skincare formulations for targeted benefits.

Pierre Fabre: A pharmaceutical and dermo-cosmetic group, Pierre Fabre is renowned for brands such as Avène and Ducray, which are specifically developed for sensitive and problematic skin, often leveraging thermal spring water.

Unilever: This multinational consumer goods company has expanded its derma cosmetics portfolio with brands like Murad and Dermalogica, emphasizing science-backed ingredients and professional-grade skincare.

Shiseido: A prominent Japanese beauty company, Shiseido offers high-performance derma cosmetic lines, often incorporating advanced Japanese biotechnology and dermatological science for targeted skin concerns.

Bioderma: A French dermo-cosmetic brand under NAOS, Bioderma is known for its ecological approach to dermatology, offering products that respect the skin's biological ecosystem for sensitive and problematic skin types.

Johnson & Johnson: A diversified healthcare company, J&J participates in derma cosmetics with brands such as Aveeno, Neutrogena, and Clean & Clear, focusing on scientifically proven solutions for everyday skin health.

Sebapharma: A German company, Sebapharma specializes in medicinal skincare products with a focus on maintaining the skin's natural pH 5.5 acid mantle, widely recommended by dermatologists for sensitive and problematic skin.

Dermacept: A Japanese brand, part of Rohto Pharmaceutical Co., Ltd., Dermacept focuses on anti-aging and brightening solutions, leveraging advanced dermatological research and high concentrations of active ingredients, often aligning with the Medical Aesthetics Market segment.

Recent Developments & Milestones in Derma Cosmetics Market

The Derma Cosmetics Market is continually evolving with new product launches, strategic collaborations, and advancements in formulation technology.

January 2026: L'Oreal's Active Cosmetics division announced a new partnership with a leading dermatological research institution to accelerate studies into the skin microbiome's role in chronic skin conditions, aiming for novel product formulations.

November 2025: Bioderma launched its latest range of eco-designed sun protection products, incorporating advanced UV filters and active ingredients specifically formulated for sensitive skin, reinforcing its commitment to the Sensitive Skin Care Market.

August 2025: Johnson & Johnson unveiled a new line of anti-acne derma cosmetic treatments featuring patented salicylic acid delivery systems, targeting the growing Acne Treatment Market with enhanced efficacy and reduced irritation.

April 2025: Pierre Fabre strengthened its R&D capabilities by acquiring a biotech firm specializing in plant-derived active ingredients, aiming to integrate sustainable and highly effective compounds into its future derma cosmetic formulations, impacting the Cosmetic Ingredients Market.

February 2025: Shiseido presented preclinical data at a major dermatology conference, showcasing the efficacy of a new peptide complex developed through biotechnology for its anti-aging derma cosmetic range, signaling advancements in the Anti-Aging Products Market.

October 2024: Sebapharma expanded its global distribution network in Eastern Europe, increasing accessibility to its pH-balanced derma cosmetic products in emerging markets.

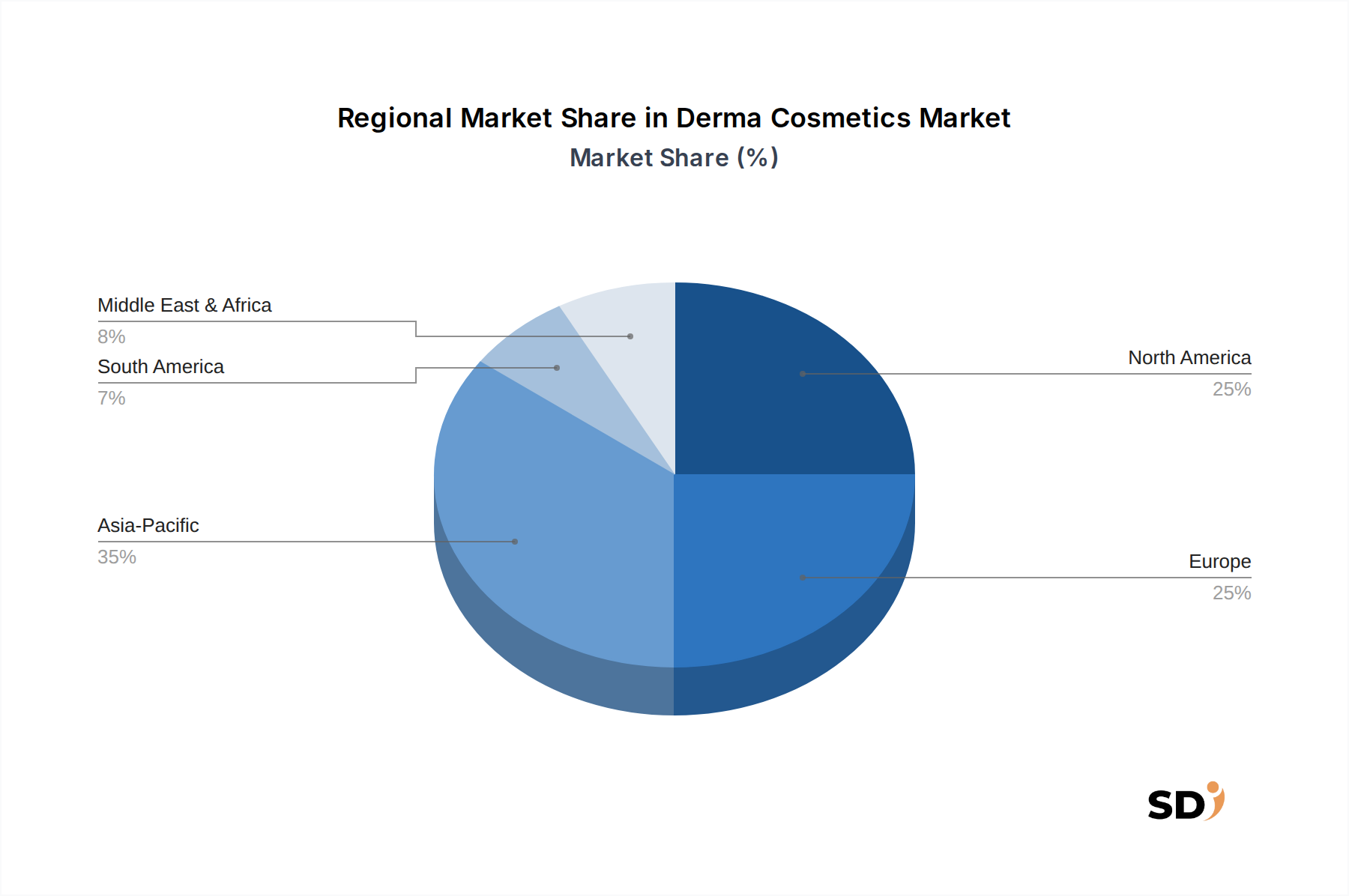

Regional Market Breakdown for Derma Cosmetics Market

The global Derma Cosmetics Market exhibits significant regional variations in terms of size, growth dynamics, and primary demand drivers. North America, comprising the United States, Canada, and Mexico, holds a substantial revenue share, driven by high consumer spending on premium skincare, a strong awareness of dermatological health, and a well-established professional channel. The region's market is mature but continues to grow at a steady CAGR, propelled by innovation in product formulations and the strong influence of medical aesthetics trends. Europe, including key markets like Germany, France, and the UK, also commands a significant share, benefiting from a rich heritage in dermatological science and stringent regulatory standards that foster trust. France, in particular, is a global hub for derma cosmetics innovation, with many leading brands originating there. The European Derma Cosmetics Market is characterized by a high demand for hypoallergenic and sustainably sourced products. Asia Pacific is identified as the fastest-growing region in the Derma Cosmetics Market, projected to exhibit a robust CAGR. Countries such as China, India, Japan, and South Korea are at the forefront, fueled by rising disposable incomes, increasing beauty consciousness, and a burgeoning middle class. South Korea, in particular, is a global trendsetter in skincare innovation, with rapid adoption of advanced derma cosmetic technologies. The demand here is largely driven by a desire for clear, healthy skin and the influence of K-beauty trends, leading to a strong demand for products that often feature novel ingredients from the Biotechnology in Cosmetics Market. The Middle East & Africa region represents an emerging market with significant growth potential, albeit from a smaller base. Demand is spurred by increasing healthcare infrastructure, a rising incidence of skin concerns due to climatic conditions, and a growing adoption of Western beauty standards. The GCC countries lead in per capita spending, creating opportunities for derma cosmetic brands.

European Union (EU) Cosmetics Regulation (EC) No 1223/2009: This is one of the most comprehensive regulatory frameworks globally, dictating strict requirements for cosmetic product safety, labeling, and ingredient restrictions. It mandates safety assessments for all products before market placement and maintains a list of prohibited and restricted substances. Recent policy changes include increased scrutiny on endocrine-disrupting chemicals and the ban on animal testing, influencing product development towards alternative testing methods. This impacts the Cosmetic Ingredients Market by driving demand for verified, safe alternatives.

U.S. Food and Drug Administration (FDA): In the U.S., cosmetics are regulated under the Federal Food, Drug, and Cosmetic Act (FD&C Act). While the FDA doesn't pre-approve cosmetic products or ingredients (except for color additives), it has oversight regarding misbranding and adulteration. Recent proposed legislation, such as the Modernization of Cosmetics Regulation Act of 2022 (MoCRA), significantly expanded the FDA's authority, introducing mandatory adverse event reporting, facility registration, and ingredient listing, which will lead to increased compliance costs and greater transparency in the Derma Cosmetics Market.

Japan's Pharmaceutical and Medical Device Act (PMD Act): Japan treats certain derma cosmetics with medicinal claims as 'quasi-drugs', subjecting them to more rigorous approval processes similar to pharmaceuticals. This distinction significantly impacts product classification and marketing strategies for players in the Derma Cosmetics Market aiming for the Japanese market, pushing for higher scientific substantiation of claims.

South Korea's Cosmetic Act: South Korea's Ministry of Food and Drug Safety (MFDS) regulates cosmetics, with a strong emphasis on functional cosmetics (those with brightening, anti-wrinkle, or UV protection claims). Recent regulatory updates often focus on ingredient safety, sustainable packaging, and clear labeling, which significantly influences product innovation and manufacturing practices, particularly for companies operating within the Skincare Products Market.

Export, Trade Flow & Tariff Impact on Derma Cosmetics Market

The Derma Cosmetics Market is heavily reliant on international trade, with specialized ingredients and finished products traversing major global trade corridors. The European Union, particularly France and Germany, are prominent exporters of high-quality derma cosmetics, leveraging their strong R&D capabilities and established brands. Key importing nations include the United States, China, and South Korea, where consumer demand for advanced skincare solutions is robust. Trade flows are often characterized by significant intra-regional movement within the EU and strong bilateral corridors between the EU and North America, as well as the EU and Asia Pacific. South Korea has also emerged as a significant exporter, especially to other Asian markets, influencing the global Cosmetic Ingredients Market with its innovative formulations.

Tariff and non-tariff barriers can significantly impact the cost and accessibility of derma cosmetic products. For instance, the US-China trade tensions in recent years have led to the imposition of tariffs on a range of cosmetic products, including derma cosmetics, increasing import costs for Chinese distributors and impacting American exporters. Similarly, Brexit introduced new complexities for trade between the UK and the EU, necessitating separate regulatory compliance and potentially higher logistics costs, which can reduce trade volume or increase end-consumer prices. Furthermore, non-tariff barriers, such as varying ingredient restrictions (e.g., certain UV filters allowed in Asia but not fully approved in the EU or US) and divergent labeling requirements across countries, create compliance challenges and can impede market entry. The need for precise documentation and adherence to diverse national standards for active ingredients, often sourced from the Specialty Chemicals Market, adds layers of complexity to global supply chains. Changes in trade agreements, such as new free trade pacts, can reduce tariffs and streamline customs procedures, potentially boosting cross-border trade volumes and making derma cosmetics more affordable and widely available in new markets, including aspects related to the Medical Aesthetics Market.

Derma Cosmetics Segmentation

1. Application

1.1. Dry Skin

1.2. Oily Skin

1.3. Combination Skin

1.4. Sensitive Skin

2. Types

2.1. Cream Products

2.2. Liquid & Lotion Products

2.3. Other

Derma Cosmetics Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Derma Cosmetics REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 7.4% from 2020-2034

Segmentation

By Application

Dry Skin

Oily Skin

Combination Skin

Sensitive Skin

By Types

Cream Products

Liquid & Lotion Products

Other

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Dry Skin

5.1.2. Oily Skin

5.1.3. Combination Skin

5.1.4. Sensitive Skin

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Cream Products

5.2.2. Liquid & Lotion Products

5.2.3. Other

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Dry Skin

6.1.2. Oily Skin

6.1.3. Combination Skin

6.1.4. Sensitive Skin

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Cream Products

6.2.2. Liquid & Lotion Products

6.2.3. Other

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Dry Skin

7.1.2. Oily Skin

7.1.3. Combination Skin

7.1.4. Sensitive Skin

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Cream Products

7.2.2. Liquid & Lotion Products

7.2.3. Other

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Dry Skin

8.1.2. Oily Skin

8.1.3. Combination Skin

8.1.4. Sensitive Skin

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Cream Products

8.2.2. Liquid & Lotion Products

8.2.3. Other

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Dry Skin

9.1.2. Oily Skin

9.1.3. Combination Skin

9.1.4. Sensitive Skin

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Cream Products

9.2.2. Liquid & Lotion Products

9.2.3. Other

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Dry Skin

10.1.2. Oily Skin

10.1.3. Combination Skin

10.1.4. Sensitive Skin

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Cream Products

10.2.2. Liquid & Lotion Products

10.2.3. Other

11. Competitive Analysis

11.1. Company Profiles

11.1.1. L'Oreal

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Christine Schrammek Kosmetik

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Procter & Gamble

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Pierre Fabre

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Unilever

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Shiseido

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Bioderma

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Johnson & Johnson

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Sebapharma

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Dermacept

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (billion), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (billion), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (billion), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (billion), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (billion), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (billion), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (billion), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (billion), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (billion), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (billion), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (billion), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (billion), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (billion), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (billion), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Application 2020 & 2033

Table 2: Revenue billion Forecast, by Types 2020 & 2033

Table 3: Revenue billion Forecast, by Region 2020 & 2033

Table 4: Revenue billion Forecast, by Application 2020 & 2033

Table 5: Revenue billion Forecast, by Types 2020 & 2033

Table 6: Revenue billion Forecast, by Country 2020 & 2033

Table 7: Revenue (billion) Forecast, by Application 2020 & 2033

Table 8: Revenue (billion) Forecast, by Application 2020 & 2033

Table 9: Revenue (billion) Forecast, by Application 2020 & 2033

Table 10: Revenue billion Forecast, by Application 2020 & 2033

Table 11: Revenue billion Forecast, by Types 2020 & 2033

Table 12: Revenue billion Forecast, by Country 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue (billion) Forecast, by Application 2020 & 2033

Table 15: Revenue (billion) Forecast, by Application 2020 & 2033

Table 16: Revenue billion Forecast, by Application 2020 & 2033

Table 17: Revenue billion Forecast, by Types 2020 & 2033

Table 18: Revenue billion Forecast, by Country 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Revenue (billion) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Revenue (billion) Forecast, by Application 2020 & 2033

Table 23: Revenue (billion) Forecast, by Application 2020 & 2033

Table 24: Revenue (billion) Forecast, by Application 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Revenue (billion) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue billion Forecast, by Application 2020 & 2033

Table 29: Revenue billion Forecast, by Types 2020 & 2033

Table 30: Revenue billion Forecast, by Country 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue (billion) Forecast, by Application 2020 & 2033

Table 37: Revenue billion Forecast, by Application 2020 & 2033

Table 38: Revenue billion Forecast, by Types 2020 & 2033

Table 39: Revenue billion Forecast, by Country 2020 & 2033

Table 40: Revenue (billion) Forecast, by Application 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue (billion) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Revenue (billion) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our research methodology heavily emphasizes primary research, accounting for 75% of our total data collection efforts. This approach ensures the highest level of granularity, real-time validation, and direct insights from key industry participants. We conduct extensive, in-depth interviews and targeted surveys with stakeholders across the derma-cosmetics value chain to validate initial hypotheses, gather qualitative data, and understand emerging market trends.

Key participants in our primary research include:

Company Types:

Derma-cosmetic Product Manufacturers (e.g., L'Oréal Active Cosmetics, La Roche-Posay, Cetaphil)

This real-time engagement allows us to ensure the report reflects the most current market dynamics and is updated up to the date of purchase, providing our clients with timely and relevant intelligence.

The remaining 25% of our research involves comprehensive secondary data analysis and industry benchmarking. This initial phase provides a broad understanding of the market landscape, identifies key players, and establishes foundational data points. Our secondary research draws from a diverse range of credible and authoritative sources, including:

Government & Regulatory Bodies: Official government reports (.gov domains) related to health, trade, and consumer goods regulations. For instance, data from the FDA (www.fda.gov) or relevant national health ministries.

Industry Associations: Trade journals, white papers, and statistics published by leading global and regional derma-cosmetics and personal care industry associations, such as:

International Federation of Societies of Cosmetic Chemists (IFSCC) (www.ifscc.org)

The Cosmetic, Toiletry and Fragrance Association of Canada (CTFA) (www.ctfa.ca)

We strictly avoid using data from other market research websites to maintain originality and ensure the integrity of our findings.

Demand Modeling & Market Estimation

Our market estimation leverages a robust combination of top-down and bottom-up methodologies, meticulously triangulated across multiple data layers to ensure accuracy. The process involves:

Top-Down Approach: Analyzing macroeconomic factors, demographic trends, healthcare expenditure related to dermatology, and overall consumer spending on personal care products at regional and global levels. This provides a macro view of the market's potential.

Bottom-Up Approach: Detailed aggregation of market size from the micro-level, considering specific market segments defined by application (Dry Skin, Oily Skin, Combination Skin, Sensitive Skin), product types (Cream Products, Liquid & Lotion Products, Other), and geographies (North America, South America, Europe, Middle East & Africa, Asia Pacific). Key metrics and variables used for bottom-up calculation include:

Average Selling Price (ASP) of Derma-Cosmetic Products per SKU/Region

Annual Sales Volume of Key Derma-Cosmetic Brands by Product Type and Geographic Presence

Patient Demographics with Specific Skin Conditions (e.g., prevalence of sensitive skin, acne) and their adoption rates of derma-cosmetics.

Number of Dermatology Clinics and Med-Spas (by region) and their average derma-cosmetic sales volume.

Data Triangulation: Cross-referencing findings from primary and secondary research, applying statistical models, and validating with expert opinions to converge on a highly reliable market estimate.

Data Accuracy & Quality Check

We are committed to delivering highly accurate and reliable market intelligence. Our stringent quality control measures ensure an estimated data accuracy level of 85-90%. This is achieved through:

Iterative Validation: Data points are continuously validated and refined throughout the research process through ongoing primary interviews and cross-referencing with multiple secondary sources.

Expert Review: All findings, forecasts, and market models are subjected to rigorous review by internal senior analysts and external industry experts.

Statistical Analysis: Advanced statistical tools and econometric models are employed to analyze data, identify trends, and project future market behavior, minimizing potential biases and errors.

Internal Quality Audits: A dedicated quality assurance team conducts thorough audits of the entire research process, from data collection to final report generation, to ensure adherence to our proprietary methodological standards.

Frequently Asked Questions

1. How are sustainability trends impacting the Derma Cosmetics market?

Increasing consumer awareness drives demand for eco-friendly formulations and sustainable packaging in derma cosmetics. Companies like L'Oreal and Procter & Gamble are investing in responsible sourcing and reducing environmental footprints to meet these evolving preferences.

2. What key consumer behaviors shape Derma Cosmetics purchasing decisions?

Consumers prioritize clinical efficacy, ingredient transparency, and solutions for specific concerns like sensitive or dry skin. This shift drives growth for specialized products over general skincare, influencing brand loyalty and product development across regions.

3. Which end-user segments show high demand for Derma Cosmetics?

Medical aesthetics clinics and specialized retail channels are significant end-users for derma cosmetics. Demand is also robust from individuals seeking solutions for conditions such as dry, oily, combination, or sensitive skin types, driving segment growth.

4. Why is raw material sourcing critical in the Derma Cosmetics supply chain?

Sourcing high-quality, clinically proven active ingredients is crucial for product efficacy and consumer trust in derma cosmetics. Strict regulatory standards and demand for natural or hypoallergenic components influence supply chain logistics for companies like Pierre Fabre and Shiseido.

5. What are the primary growth drivers for the Derma Cosmetics market?

Rising prevalence of skin conditions, increased consumer awareness of skin health, and demand for science-backed solutions are key drivers. Technological advancements in formulations and expanding distribution channels also contribute significantly to market expansion.

6. What is the projected market size and CAGR for Derma Cosmetics through 2033?

The Derma Cosmetics market is valued at $53 billion in 2025, projected to grow at a CAGR of 7.4%. This significant expansion is driven by sustained demand for advanced skin health solutions, with projections extending past the base year.