1. What is the projected growth for the Customized Cell Culture Media market?

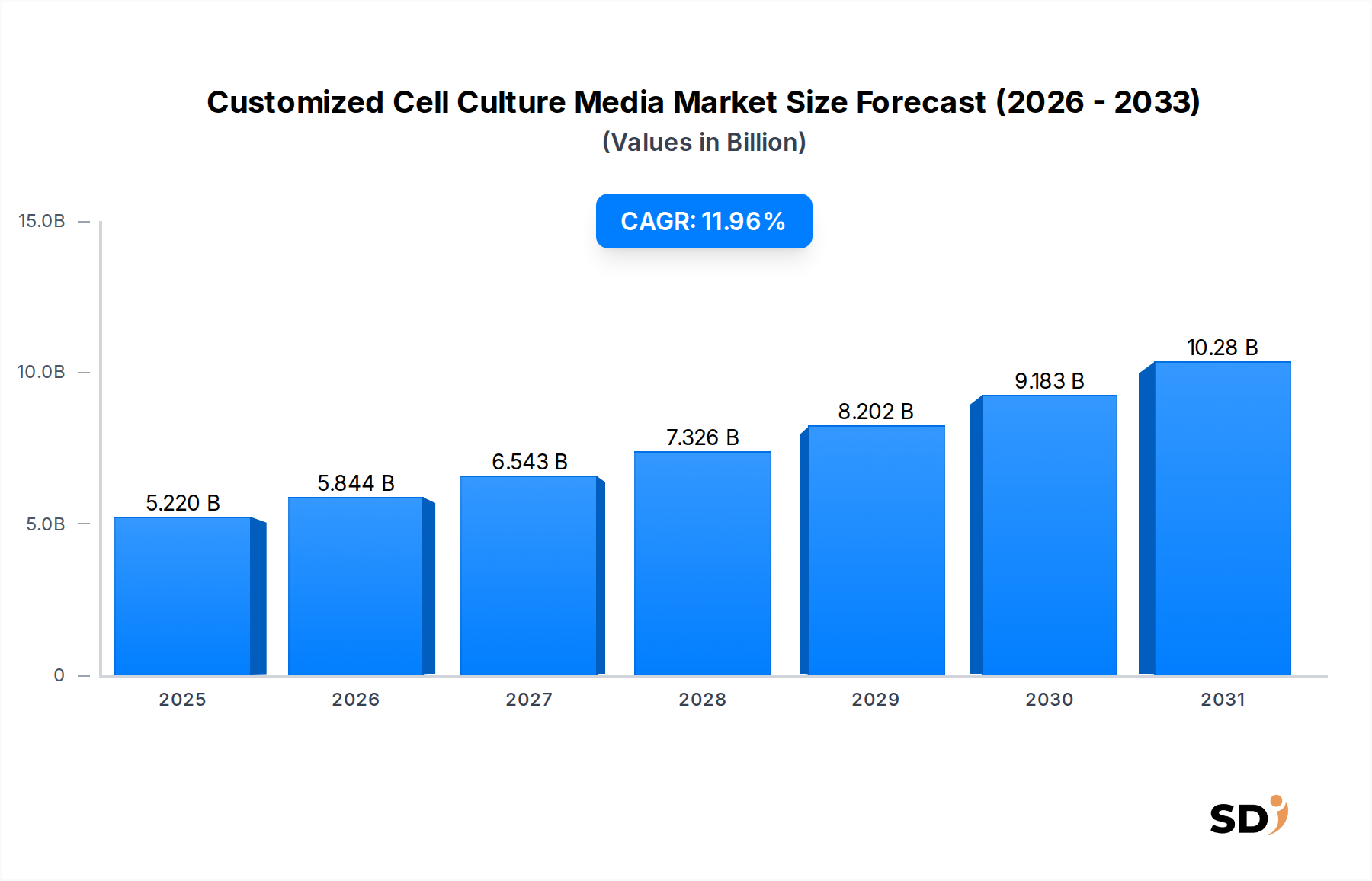

The Customized Cell Culture Media market was valued at $5.22 billion in 2025. It is projected to expand at an 11.96% CAGR through 2033, driven by biopharmaceutical demand.

+1 2315155523

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

The Customized Cell Culture Media Market is projected for substantial expansion, underpinned by the accelerating pace of biopharmaceutical research and development, particularly in advanced therapies. Valued at USD 5.22 billion in 2025, the market is poised for robust growth, exhibiting a compound annual growth rate (CAGR) of 11.96% over the forecast period. This trajectory is driven by an increasing demand for specialized media formulations that optimize cell growth, productivity, and viability across various applications, ranging from biologics manufacturing to cutting-edge regenerative medicine. The paradigm shift towards personalized medicine and cell and gene therapies necessitates highly tailored media solutions, moving beyond off-the-shelf products to formulations precisely calibrated for specific cell lines and therapeutic objectives.

Key demand drivers include the escalating global pipeline for monoclonal antibodies, recombinant proteins, and vaccines, which demand optimized cultivation environments to maximize yields and product quality. Furthermore, the rapid advancements in the Gene Therapy Market and Regenerative Medicine Market are creating an imperative for bespoke media to support the complex ex vivo expansion and differentiation of various cell types, including stem cells and immune cells. Macro tailwinds, such as increased R&D investment by pharmaceutical and biotechnology companies, government funding for life sciences research, and technological innovations in bioprocessing, are collectively propelling the Customized Cell Culture Media Market forward. The integration of advanced analytical techniques and machine learning in media design is enabling more efficient and targeted optimization, reducing development timelines and costs. As the industry strives for greater efficiency, consistency, and regulatory compliance in biomanufacturing, the reliance on highly specialized and customized cell culture media will only intensify. The outlook remains highly positive, with significant opportunities for providers capable of offering flexible, high-performance, and regulatory-compliant media solutions that address the unique requirements of next-generation therapeutics. Innovations in the broader Cell Culture Media Market are consistently pushing the boundaries of what is possible in cell-based research and production, highlighting the critical role of customized solutions.

The Biopharmaceutical Manufacturing Market stands as the single largest and most influential application segment within the Customized Cell Culture Media Market, commanding a predominant share of revenue. Its dominance is directly attributable to the intricate and demanding requirements of producing biologics, including therapeutic proteins, monoclonal antibodies, and vaccines. These biological entities often necessitate specific cellular environments to ensure optimal growth, protein expression, glycosylation patterns, and overall product quality. Standard, off-the-shelf media formulations are frequently insufficient to meet these precise requirements, leading to the adoption of customized solutions that are meticulously optimized for individual cell lines, bioreactor systems, and production processes.

The rationale behind this dominance is multifaceted. Firstly, the high value and critical nature of biopharmaceutical products necessitate robust and reproducible manufacturing processes. Customized media contribute significantly to achieving consistent product quality and yield, which are paramount for regulatory approval and commercial success. Secondly, the sheer volume of biologics produced globally, coupled with a continuously expanding pipeline of novel therapeutics, drives sustained demand for specialized media. Companies involved in large-scale bioproduction seek media that can enhance volumetric productivity, reduce manufacturing costs, and minimize batch-to-batch variability. Key players in this sphere, many of whom also operate as media suppliers, include Thermo Fisher, Merck, Corning, and Cytiva, who offer extensive portfolios of base media and customization services to the biopharmaceutical sector. Lonza and FUJIFILM Diosynth Biotechnologies, as prominent Contract Development and Manufacturing Organizations (CDMOs), also heavily rely on and often co-develop customized media to serve their diverse client needs.

Furthermore, the increasing complexity of biologics, such as bispecific antibodies and antibody-drug conjugates, further reinforces the need for tailored media that can support the unique metabolic demands of producing cells. The segment’s share is not only growing but also consolidating, as biopharmaceutical companies increasingly partner with specialized media developers to co-create proprietary formulations. This collaboration ensures intellectual property protection and a competitive edge in product performance. While the Gene Therapy Market and Tissue Culture & Engineering applications are experiencing rapid growth and are increasingly important, the mature and high-volume nature of biopharmaceutical manufacturing ensures its continued supremacy in the Customized Cell Culture Media Market. The ongoing innovation in upstream bioprocessing, including intensified and continuous manufacturing, also places additional demands on media design, further solidifying the Biopharmaceutical Manufacturing Market's leading position.

The Customized Cell Culture Media Market is primarily propelled by the exponential growth in the biopharmaceutical sector and advanced therapeutic development, yet faces specific limitations. A significant driver is the increasing global demand for biologics, including monoclonal antibodies, recombinant proteins, and vaccines. The Biopharmaceutical Manufacturing Market has seen consistent expansion, with novel drug approvals driving the need for highly efficient and specific cell culture conditions. For instance, the approval rate for biologics by regulatory bodies like the FDA has steadily increased, necessitating optimized media formulations to enhance therapeutic protein yield and quality, thereby reducing production costs per batch by an estimated 15-20% through targeted media optimization. This drive for efficiency directly fuels the demand for customized media that can support higher cell densities and productivity in bioreactors.

Another critical driver is the rapid advancement in the Gene Therapy Market and Regenerative Medicine Market. These fields rely heavily on ex vivo cell manipulation and expansion, requiring highly specialized, serum-free, and often Chemically Defined Media Market formulations to ensure cell viability, specific differentiation, and safety for human therapeutic applications. The complexity of these therapies, such as CAR-T cell manufacturing, mandates media free of animal-derived components to mitigate contamination risks and ensure regulatory compliance, creating a strong pull for bespoke, highly characterized media. Furthermore, the push towards personalized medicine requires media that can be optimized for patient-specific cell lines, expanding the scope for customization.

However, the market faces notable constraints. The high cost associated with the development and validation of customized media formulations can be a significant barrier, particularly for smaller biotechnology firms. Custom media development involves extensive R&D, analytical testing, and rigorous quality control, which adds to the final product cost. This is especially true for the Serum-Free Media Market and highly specialized formulations, where raw material sourcing and purity are critical. Regulatory hurdles also pose a challenge; obtaining approval for a new biologic often requires extensive documentation and validation of all components, including cell culture media, which can prolong development timelines. Moreover, the technical complexity in identifying optimal media components for novel or difficult-to-culture cell lines requires specialized expertise and advanced analytical platforms, representing a human capital and technological investment constraint. Managing the supply chain for complex Cell Culture Reagents Market components can also be challenging, leading to potential delays or increased costs.

The Customized Cell Culture Media Market is undergoing a profound technological transformation, driven by the imperative for enhanced performance, scalability, and regulatory compliance. One of the most disruptive emerging technologies is the application of Artificial Intelligence (AI) and Machine Learning (ML) for media optimization. Traditionally, media development relied on extensive experimental design matrices (DoE) and empirical testing, a time-consuming and resource-intensive process. AI/ML algorithms can analyze vast datasets of cell culture performance, identifying optimal nutrient combinations, growth factor concentrations, and metabolic profiles with unprecedented speed and accuracy. This significantly accelerates the media development cycle, potentially reducing it by 30-50%. Adoption timelines are accelerating, with several biopharmaceutical companies and specialized media developers already integrating AI-powered platforms. R&D investment levels are high, as companies seek to gain a competitive edge in developing superior and more cost-effective media. This technology directly threatens incumbent empirical methods by offering a more efficient and data-driven approach, potentially shifting competitive advantage to firms with robust bioinformatics and data science capabilities.

A second critical innovation trajectory involves advanced analytical techniques for real-time media monitoring and spent media analysis. High-throughput mass spectrometry, nuclear magnetic resonance (NMR), and biosensor technologies are enabling a deeper understanding of cellular metabolism and nutrient consumption dynamics during cultivation. This real-time feedback loop allows for dynamic media feeding strategies and precise customization, moving beyond static formulations to adaptive media that respond to the evolving needs of the cell culture. The Bioprocess Technology Market is heavily influenced by these advancements, as they enable more tightly controlled and optimized bioreactor operations. Adoption is currently strong in late-stage R&D and early clinical manufacturing, with broader commercial adoption expected within the next 3-5 years as technologies become more integrated and cost-effective. These innovations reinforce existing business models by improving efficiency and product quality but also demand significant R&D investment in analytical instrumentation and data interpretation expertise.

Finally, the evolution of single-use bioprocessing systems is driving innovations in media delivery and sterilization. Customized media are increasingly provided in ready-to-use, pre-sterilized single-use bags, reducing the risk of contamination and simplifying preparation. This integration is crucial for the efficient operation of modern biomanufacturing facilities, particularly in the production of cell and gene therapies where contamination control is paramount. While not a technology for media formulation itself, it profoundly impacts the logistics and utility of customized media, making them more amenable to flexible manufacturing paradigms. These advancements reinforce incumbent business models by enabling faster facility setup and reducing capital expenditure, aligning with the agile demands of the modern Biopharmaceutical Manufacturing Market.

The Customized Cell Culture Media Market serves a diverse end-user base, each with distinct purchasing criteria and procurement channels. The primary segments include large biopharmaceutical companies, Contract Development and Manufacturing Organizations (CDMOs), academic and government research institutions, and smaller biotechnology startups. Large biopharmaceutical companies represent the most significant segment, typically demanding bulk quantities of highly validated, regulatory-compliant customized media. Their purchasing criteria are stringent, prioritizing performance (e.g., enhanced titer, improved product quality), supply chain reliability, consistency, and extensive documentation for regulatory submissions. Price sensitivity, while present, is often secondary to performance and regulatory compliance, given the high value of the end product. Procurement typically occurs through long-term contracts directly with major media suppliers or specialized service providers.

CDMOs form another crucial segment, characterized by their need for flexible and rapidly customizable media solutions to support a wide array of client projects. Their purchasing decisions are heavily influenced by the media supplier's ability to offer quick turnaround times, broad customization capabilities, and strong technical support. Price sensitivity is moderate, as they often pass media costs on to their clients, but efficiency gains are highly valued. Procurement is often project-specific, involving close collaboration between the CDMO and the media developer. The Cell Line Development Market is particularly critical for CDMOs, requiring specialized media to optimize different cell lines for diverse bioproduction needs.

Academic and government research institutions prioritize cost-effectiveness, ease of use, and the ability to support diverse experimental needs. While they may not require the same level of regulatory documentation as biopharma, they seek media that offer robust performance for basic and translational research. Their procurement is often through institutional purchasing departments, relying on catalogue orders or established vendor relationships. Smaller biotechnology startups, particularly those focused on novel therapies like those in the Gene Therapy Market or Regenerative Medicine Market, require highly specialized, often animal-component-free media. Their purchasing criteria are a balance of performance, scientific support, and scalability, with a higher degree of price sensitivity due to limited budgets. They often rely on specialized media companies that can offer tailored solutions with strong scientific consultation.

Notable shifts in buyer preference in recent cycles include an increased demand for Serum-Free Media Market and Chemically Defined Media Market formulations across all segments, driven by regulatory pressures and the desire for greater consistency. There's also a growing preference for 'media as a service' models, where suppliers provide not just the media but also optimization expertise and analytical services. Furthermore, supply chain resilience and geographical proximity of suppliers have gained importance following global disruptions, leading to a diversification of procurement channels and a greater emphasis on local manufacturing capabilities for Cell Culture Reagents Market and final media products.

The Customized Cell Culture Media Market features a competitive landscape comprising established life science giants and specialized boutique firms, all vying to provide tailored solutions for diverse bioprocessing needs.

The Customized Cell Culture Media Market has seen a series of strategic advancements and product introductions aimed at enhancing performance, expanding capabilities, and meeting evolving regulatory demands.

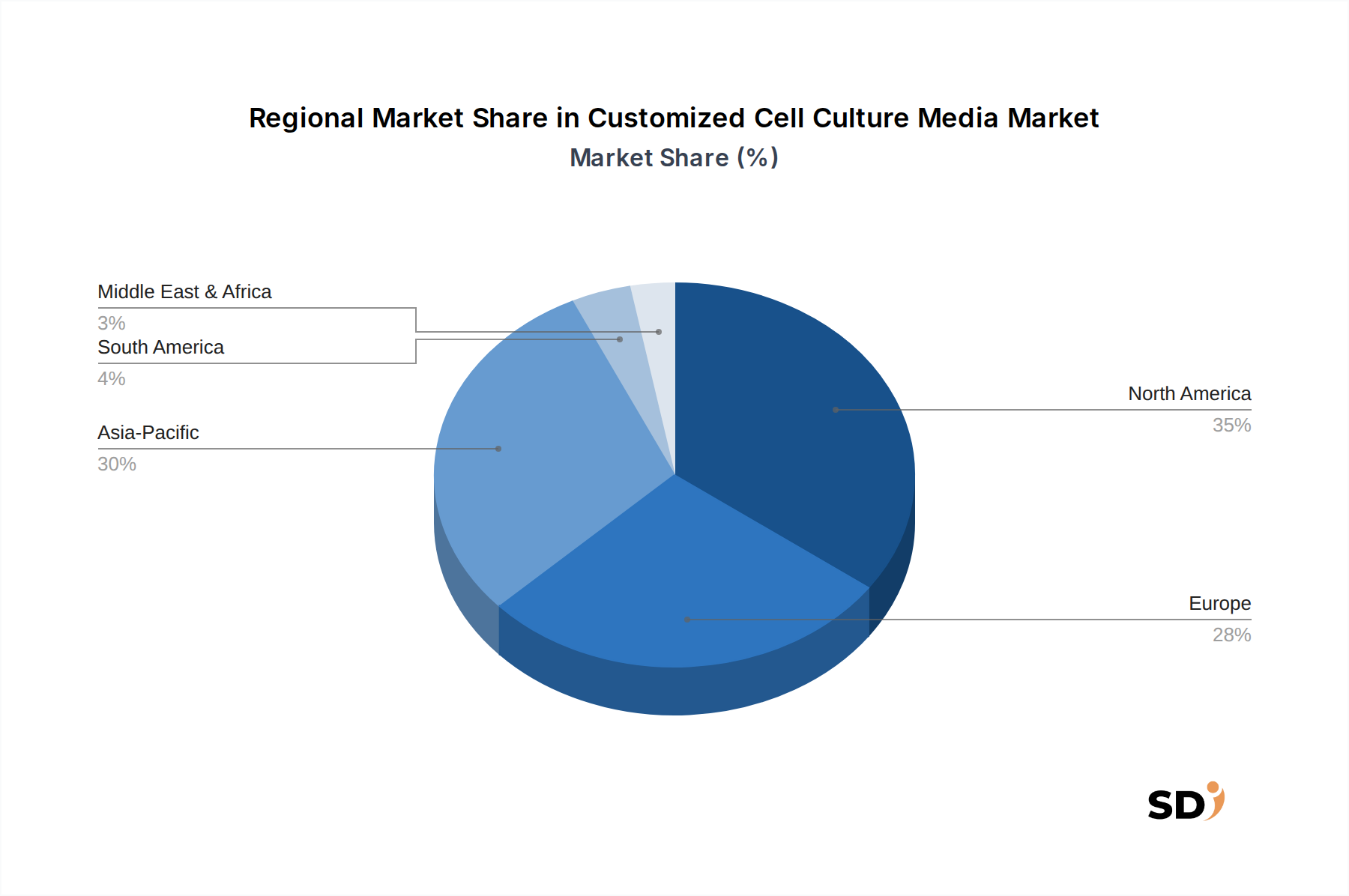

Geographically, the Customized Cell Culture Media Market exhibits distinct patterns in adoption, growth rates, and primary demand drivers. North America, particularly the United States, holds the largest revenue share, primarily due to the presence of a robust biopharmaceutical industry, extensive R&D activities, and significant investment in biotechnology. The region is a hub for novel drug development, including advanced therapies within the Gene Therapy Market, driving consistent demand for highly specialized media. North America’s market is characterized by mature infrastructure, high adoption of advanced bioprocessing technologies, and a strong regulatory framework. The estimated CAGR for North America is projected to be around 10.5%, reflecting sustained innovation and production volumes.

Europe follows closely, constituting the second-largest market. Countries like Germany, the UK, and France are leading contributors, propelled by strong governmental support for life sciences research, a growing pipeline of biologics, and well-established academic and industrial collaborations. The demand for customized solutions here is driven by the need to optimize manufacturing processes for complex biologics and biosimilars. European biopharmaceutical companies are increasingly investing in intensified and continuous bioprocessing, which necessitates tailored media. The CAGR for Europe is anticipated to be approximately 11.2%, indicative of a healthy growth trajectory.

Asia Pacific is projected to be the fastest-growing region in the Customized Cell Culture Media Market, with an estimated CAGR exceeding 14%. This rapid expansion is fueled by increasing foreign direct investment in the region's burgeoning biotechnology sector, particularly in China, India, Japan, and South Korea. These countries are rapidly expanding their biopharmaceutical manufacturing capabilities and R&D pipelines, driven by rising healthcare expenditures, a large patient pool, and supportive government initiatives. The demand is particularly strong for both the Biopharmaceutical Manufacturing Market and growing academic research, leading to a surge in the adoption of customized media solutions to accelerate drug development and production.

The Middle East & Africa and South America regions represent emerging markets for customized cell culture media. While smaller in market share, they are demonstrating promising growth potential. In the Middle East, investments in healthcare infrastructure and a focus on diversifying economies are driving nascent biotechnology R&D. South America, especially Brazil and Argentina, is seeing increased biopharmaceutical activities, albeit from a lower base, with a growing emphasis on local production of vaccines and biosimilars. These regions are characterized by a focus on establishing fundamental biomanufacturing capabilities, which often involves importing advanced media solutions, with CAGRs expected to be in the 9-10% range. The global Cell Culture Media Market is experiencing a shift in production and consumption, with Asia Pacific becoming an increasingly critical player.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.96% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary research forms the cornerstone of our market analysis, constituting 70-80% of our total research efforts. This rigorous approach involves in-depth, semi-structured interviews with key industry stakeholders across the Customized Cell Culture Media value chain, ensuring that our insights are grounded in real-world perspectives and current market dynamics. Our global primary research network is robust, encompassing a wide array of participants, with a focused effort on gathering qualitative and quantitative data directly from industry veterans. The insights gathered are critical for validating secondary research findings, identifying emerging trends, understanding competitive landscapes, and obtaining nuanced perspectives on market drivers, restraints, and opportunities specific to Customized Cell Culture Media.

Key Company Types Interviewed:

Key Stakeholders Interviewed:

| Stakeholder Role | Interview Share (%) |

|---|---|

| Head of Cell Culture & Bioprocessing | 30% |

| Senior R&D Scientist (Media Development & Optimization) | 35% |

| VP, Manufacturing Operations | 20% |

| Director of Supply Chain & Procurement (Bioreagents & Custom Media) | 15% |

| Company Type | Representation (%) |

|---|---|

| Customized Cell Culture Media Developers & Manufacturers | 30% |

| Biopharmaceutical & Gene Therapy Developers | 35% |

| CROs/CDMOs (Cell Line Development & Bioprocessing) | 20% |

| Tissue Engineering & Regenerative Medicine Firms | 10% |

| Raw Material & Component Suppliers for Cell Culture | 5% |

Secondary research complements our primary findings, contributing 20-30% of our total research. This phase involves a comprehensive review of existing literature, proprietary databases, and publicly available information to establish a foundational understanding of the market and identify potential interview candidates. Our methodology strictly adheres to the use of credible, authoritative sources, explicitly avoiding data from other market research websites to maintain the integrity and originality of our analysis.

All data collected from secondary sources is meticulously cross-referenced and triangulated with primary research findings to ensure accuracy, relevance, and contextual understanding. Our reports are consistently updated up to the date of purchase, reflecting the most current market information and developments.

Our market estimation process employs a robust combination of top-down and bottom-up approaches, further enhanced by multi-level data triangulation to ensure precision and reliability in forecasting the Customized Cell Culture Media market.

Maintaining the highest standards of data accuracy and quality is paramount to our research integrity and the reliability of our market forecasts. We guarantee an estimated data accuracy level of 85-90% for all market analyses, forecasts, and strategic insights provided in this report. This assurance is built upon a stringent, multi-faceted quality control process:

The Customized Cell Culture Media market was valued at $5.22 billion in 2025. It is projected to expand at an 11.96% CAGR through 2033, driven by biopharmaceutical demand.

The post-pandemic period has driven increased investment in biopharmaceutical manufacturing and vaccine development, accelerating demand for customized media. This created structural shifts towards more resilient and localized supply chains for critical raw materials.

Key export-import dynamics involve established manufacturers like Thermo Fisher and Merck supplying global biopharma hubs. Trade flows are influenced by regional manufacturing capabilities and regulatory requirements, particularly between North America, Europe, and rapidly expanding Asia-Pacific markets.

Raw material sourcing is critical due to the complex array of components required for customized media formulations. Supply chain considerations include ensuring high-purity ingredient availability and managing lead times to support biopharmaceutical manufacturing schedules effectively.

Purchasing trends indicate a preference for highly customized formulations that optimize specific cell lines and processes. Buyers prioritize suppliers like Lonza and Cytiva who offer media optimization panels (MOP) and complete service (CS) solutions to enhance manufacturing efficiency and product yield.

Disruptive technologies include advanced analytical tools for media optimization and AI-driven formulation development. While direct substitutes are limited, innovations in cell-free protein synthesis or microfluidic culture systems could alter future media requirements.