Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

CTLA-4 Antibody Market: $2.5B by 2025, 12% CAGR Analysis

ctla 4 antibody

CTLA-4 Antibody Market: $2.5B by 2025, 12% CAGR Analysis

ctla 4 antibody by Application, by Types, by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 8, 2026|Base Year : 2025|Pages : 103

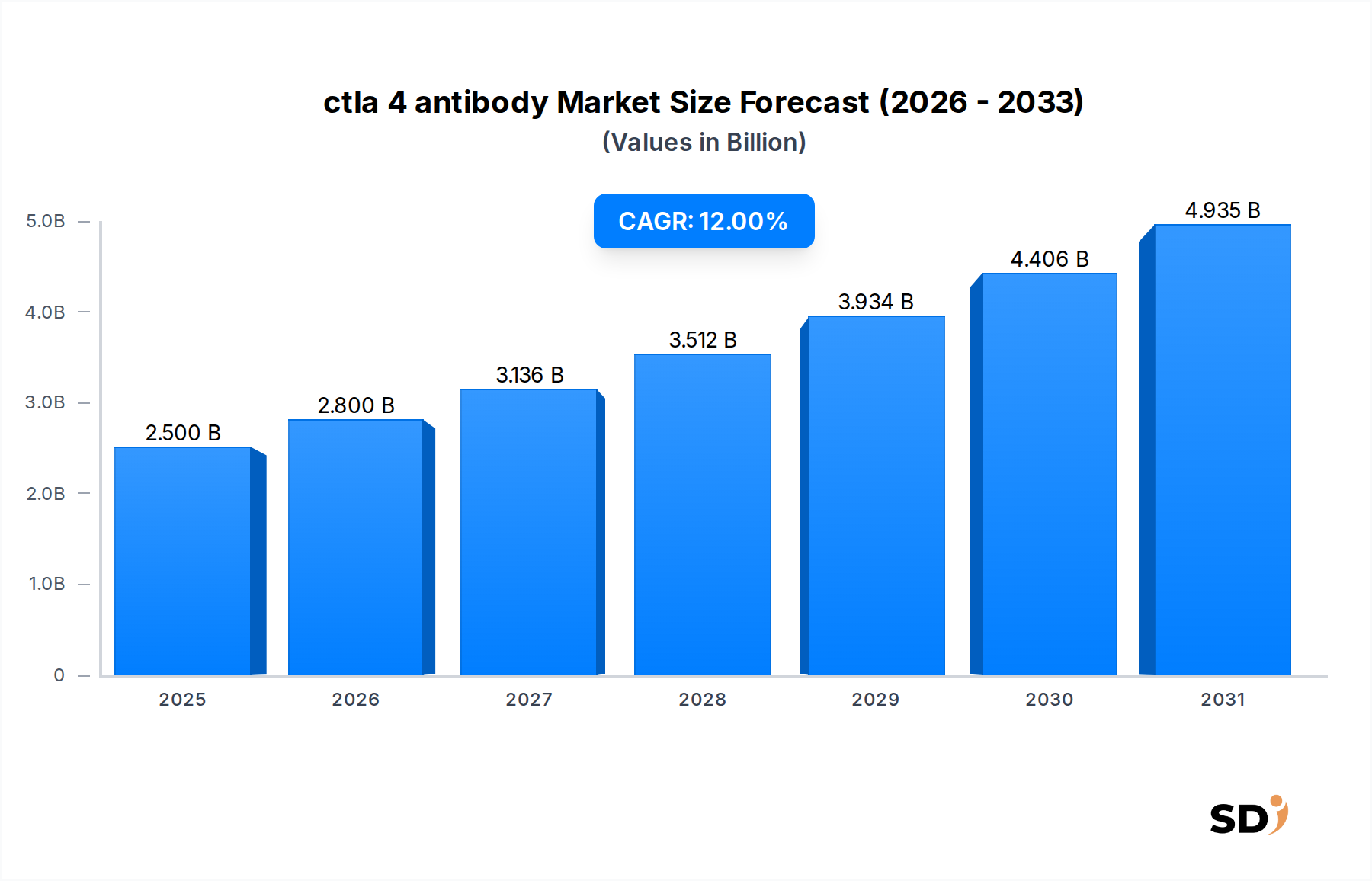

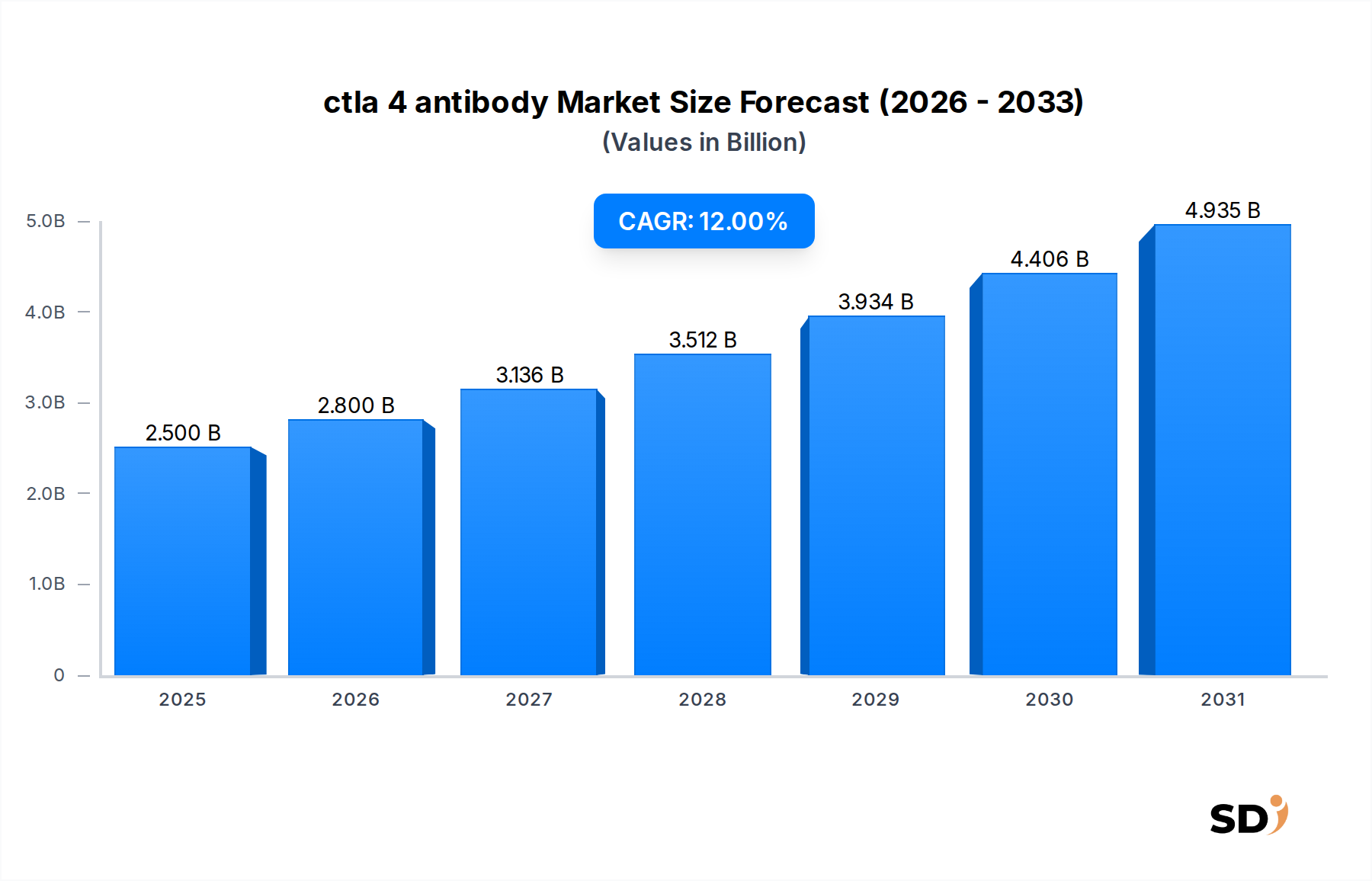

The global ctla 4 antibody Market is poised for substantial expansion, with a valuation projected to reach $2.5 billion by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 12% from the base year. This significant growth is primarily fueled by the increasing incidence of various cancers, particularly melanoma, renal cell carcinoma, and hepatocellular carcinoma, where CTLA-4 inhibitors have demonstrated profound efficacy, especially in combination therapies. The strategic expansion of approved indications, coupled with advancements in biomarker discovery, is further solidifying the therapeutic utility of these antibodies.

ctla 4 antibody Market Size (In Billion)

5.0B

4.0B

3.0B

2.0B

1.0B

0

2.500 B

2025

2.800 B

2026

3.136 B

2027

3.512 B

2028

3.934 B

2029

4.406 B

2030

4.935 B

2031

Macroeconomic tailwinds include increasing healthcare expenditure globally, particularly in developed economies, alongside a growing emphasis on personalized medicine and advanced biologics. The rising geriatric population, which is more susceptible to cancer and autoimmune conditions, also serves as a demographic catalyst for market expansion. Furthermore, significant investments in R&D by pharmaceutical giants are continuously pushing the boundaries of immunotherapy, leading to novel formulations and combination regimens. The broader Immunotherapy Drug Market is experiencing a renaissance, with CTLA-4 antibodies playing a pivotal role. The transition from conventional chemotherapy to targeted biological therapies underscores a paradigm shift in cancer management, creating a fertile ground for the ctla 4 antibody Market.

However, challenges such as the high cost of treatment, potential for severe immune-related adverse events, and stringent regulatory approval processes continue to influence market dynamics. Despite these hurdles, ongoing clinical trials exploring new indications and combination strategies are expected to mitigate some of these constraints. The competitive landscape is marked by continuous innovation, with companies focusing on enhancing drug safety profiles and developing novel adjunctive therapies to maximize patient outcomes. The future outlook for the ctla 4 antibody Market remains exceedingly positive, driven by persistent unmet medical needs in oncology and the burgeoning potential of combination regimens to deliver superior and durable responses across a wider patient spectrum, thereby contributing to the growth of the overarching Oncology Therapeutics Market.

Dominant Therapeutic Applications in ctla 4 antibody Market

The Application segment stands as the largest contributor to the revenue share within the ctla 4 antibody Market, with oncology applications, specifically melanoma, renal cell carcinoma (RCC), and hepatocellular carcinoma (HCC), dominating this segment. The breakthrough approval of ipilimumab (Yervoy) for unresectable or metastatic melanoma marked a significant milestone, revolutionizing the treatment landscape for this aggressive skin cancer. Its mechanism of action, which involves blocking CTLA-4 to enhance T-cell activation and proliferation, has proven critical in elicating durable anti-tumor responses. This success has cemented melanoma as the primary application area, where the drug is often utilized as a monotherapy or, increasingly, in combination with PD-1 inhibitors for synergistic effects.

Beyond melanoma, the utility of CTLA-4 antibodies has expanded into other challenging cancers. In renal cell carcinoma, combination regimens involving a CTLA-4 antibody have shown improved overall survival rates compared to monotherapy or targeted therapies alone, positioning RCC as a rapidly growing application. Similarly, hepatocellular carcinoma, a liver cancer with limited treatment options, has seen favorable outcomes with CTLA-4-based immunotherapies, particularly in advanced stages. The dominance of these applications stems from several factors: the significant unmet needs in these aggressive cancers, the robust clinical data supporting the efficacy of CTLA-4 inhibitors, and their inclusion in established treatment guidelines by major oncology organizations globally. The high prevalence and mortality rates associated with these cancers ensure a continuous demand for effective therapeutic interventions.

Key players in the ctla 4 antibody Market, such as Bristol-Myers Squibb with ipilimumab, have strategically focused on expanding indications and securing regulatory approvals for these critical applications, thereby solidifying their market positions. The ongoing research into biomarker identification is also refining patient selection, ensuring that CTLA-4 therapies are administered to those most likely to benefit, thereby optimizing treatment outcomes and resource utilization. The successful integration of CTLA-4 antibodies into standard of care for these specific oncology indications underpins the sustained dominance of the Application segment, driving significant revenue growth and innovation within the broader Oncology Therapeutics Market. As research progresses, there is also emerging interest in the potential of CTLA-4 antibodies in various Autoimmune Disease Treatment Market applications, although oncology currently holds the largest share due to established efficacy and approvals.

Key Market Drivers for ctla 4 antibody Market

The ctla 4 antibody Market is principally propelled by a confluence of critical drivers, prominently including the escalating global incidence of various cancers and the undeniable efficacy of combination immunotherapies. Data from the World Health Organization (WHO) indicates a projected rise in global cancer cases by nearly 60% by 2040, with melanoma, renal cell carcinoma, and hepatocellular carcinoma—key indications for CTLA-4 antibodies—contributing significantly to this burden. This increasing disease prevalence directly translates into a heightened demand for innovative and effective treatments, thereby boosting the ctla 4 antibody Market.

A second significant driver is the growing adoption of combination immunotherapies, which have demonstrated superior clinical outcomes compared to monotherapy. For instance, the combination of a CTLA-4 inhibitor with a PD-1 inhibitor has shown a 58% reduction in the risk of death in metastatic melanoma patients, according to pivotal clinical trials. This synergistic effect, leveraging distinct immunological pathways, maximizes therapeutic benefits and expands the addressable patient population. Such evidence-based improvements in patient survival and progression-free survival are accelerating the integration of these combination regimens into standard clinical practice, significantly impacting the broader Checkpoint Inhibitor Market.

Furthermore, advancements in biomarker identification and Precision Medicine Market approaches are enhancing the ability to select patients most likely to respond to CTLA-4 antibody therapies, thereby improving treatment efficacy and reducing unwarranted exposure to adverse events. Research efforts are continually uncovering new biomarkers that can predict response and resistance, optimizing clinical outcomes and driving targeted therapeutic strategies. Lastly, the expansion of regulatory approvals for CTLA-4 antibodies across new indications and lines of therapy acts as a strong market accelerator. Recent approvals in combination settings for advanced renal cell carcinoma and metastatic colorectal cancer have significantly broadened the therapeutic reach of these drugs, reinforcing their commercial viability and growth trajectory within the global Pharmaceuticals Market.

Pricing Dynamics & Margin Pressure in ctla 4 antibody Market

The pricing dynamics within the ctla 4 antibody Market are characterized by premium pricing strategies, reflecting the significant R&D investments, the complexity of Biologics Manufacturing Market processes, and the life-saving potential of these therapies. Average selling prices for CTLA-4 antibodies, such as ipilimumab, are substantial, often exceeding $100,000 for a full course of treatment, particularly when used in combination regimens. This high cost is a direct reflection of the extensive clinical trials required for regulatory approval and the innovative nature of the drugs. The margin structures across the value chain are generally robust for originators, who bear the primary R&D and manufacturing costs but also command significant pricing power due to patent protection and clinical differentiation.

However, the market is not immune to margin pressures. As key patents approach expiration, the anticipated entry of biosimilars will inevitably exert downward pressure on prices, introducing a new dimension of competition. This trend is already observable in other segments of the Monoclonal Antibody Market. Payers and healthcare systems globally are increasingly scrutinizing drug costs, leading to more aggressive reimbursement negotiations and the implementation of value-based pricing models. These mechanisms aim to link drug costs to patient outcomes, potentially impacting the net revenue per treatment course.

Key cost levers for manufacturers include optimizing Biologics Manufacturing Market processes to improve yield and reduce operational expenses, as well as managing the extensive supply chain. Intense competitive intensity, particularly from next-generation checkpoint inhibitors and novel combination therapies, also compels manufacturers to continuously demonstrate superior efficacy and safety profiles to justify premium pricing. Furthermore, the global trend towards healthcare cost containment, coupled with the rising prevalence of chronic diseases, ensures that pricing will remain a critical point of contention, necessitating strategic pricing and access initiatives by companies operating in the ctla 4 antibody Market to maintain profitability.

The regulatory and policy landscape significantly shapes the ctla 4 antibody Market, influencing drug development, approval, and market access across key geographies. Major regulatory bodies such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and Japan's Pharmaceuticals and Medical Devices Agency (PMDA) play a crucial role. These agencies apply stringent approval processes, requiring extensive preclinical and clinical data to demonstrate both efficacy and safety. For instance, accelerated approval pathways, such as the FDA's Breakthrough Therapy designation, have been instrumental in expediting the review of CTLA-4 antibodies for serious conditions like melanoma, based on preliminary clinical evidence.

Policy initiatives often focus on encouraging innovation while ensuring patient access and affordability. Orphan drug designations have been valuable in incentivizing the development of CTLA-4 antibodies for rare cancer indications. Recent policy changes have also emphasized the need for robust pharmacovigilance post-marketing, given the potential for immune-related adverse events associated with these powerful immunotherapies. This impacts development strategies by requiring comprehensive safety monitoring plans.

Furthermore, the regulatory environment for combination therapies, which are increasingly prevalent in the ctla 4 antibody Market, is becoming more complex, requiring careful coordination between manufacturers of different agents. International harmonization efforts, such as those by the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH), aim to streamline global development. The growing focus on real-world evidence (RWE) in regulatory decisions, especially for post-market surveillance and label expansions, also influences how companies generate and utilize data. These frameworks collectively ensure drug quality, safety, and efficacy, while also influencing market dynamics by controlling entry barriers and fostering competition within the broader Immunotherapy Drug Market, especially concerning the Monoclonal Antibody Market segment.

Competitive Ecosystem of ctla 4 antibody Market

The competitive ecosystem of the ctla 4 antibody Market is primarily characterized by a limited number of established players and a robust pipeline of investigational therapies, often focusing on combination approaches. Due to the highly specialized nature of these biologics and the significant R&D investment required, market entry barriers are high.

Bristol-Myers Squibb (BMS): A dominant force in the ctla 4 antibody Market with its flagship product, ipilimumab (Yervoy). BMS has strategically expanded the indications for ipilimumab, both as monotherapy and, crucially, in combination with PD-1 inhibitors across multiple cancer types, including melanoma, renal cell carcinoma, and hepatocellular carcinoma, maintaining a significant market share and driving innovation in the Checkpoint Inhibitor Market.

Other Pharmaceutical Innovators: Several other pharmaceutical companies are actively involved in the broader Oncology Therapeutics Market and are exploring CTLA-4 inhibition through their pipelines. This includes companies with next-generation CTLA-4 antibodies or those developing novel combination regimens that incorporate CTLA-4 blockade to enhance efficacy and overcome resistance mechanisms. Their strategies often involve collaborations and licensing agreements to leverage existing expertise in immunotherapy development.

Biotechnology Start-ups: A growing number of biotechnology firms are entering the competitive landscape, albeit typically in earlier stages of development. These companies often focus on novel CTLA-4 variants, bispecific antibodies, or cellular therapies that target CTLA-4 to offer differentiated therapeutic profiles or improved safety. Their success hinges on strong preclinical data and securing strategic partnerships for clinical development and commercialization within the Precision Medicine Market.

Biosimilar Developers: With original CTLA-4 antibody patents nearing expiration in some regions, a segment of biosimilar developers is emerging. These companies aim to offer more affordable alternatives, which could introduce significant price competition and expand access to CTLA-4 therapies in various global markets. Their entry will likely reshape the market dynamics, putting pressure on originator companies to further innovate or adjust pricing strategies within the Monoclonal Antibody Market.

Recent Developments & Milestones in ctla 4 antibody Market

March 2026: A major pharmaceutical company announced positive Phase III trial results for a novel CTLA-4 antibody in combination with a PD-1 inhibitor for metastatic colorectal cancer, demonstrating superior overall survival rates compared to existing treatments. This development is expected to lead to new regulatory submissions in the coming year, expanding the reach of the Checkpoint Inhibitor Market.

December 2025: The FDA granted Breakthrough Therapy designation to an investigational next-generation CTLA-4 antibody for a rare form of soft tissue sarcoma, highlighting its potential to address significant unmet medical needs. This designation could accelerate its development and approval pathway.

August 2025: A significant partnership was forged between a leading biotech firm and a global pharmaceutical giant to co-develop and commercialize a new CTLA-4 targeted bispecific antibody. The collaboration aims to enhance the precision and reduce the systemic toxicity associated with traditional CTLA-4 blockade, potentially revolutionizing treatment within the Oncology Therapeutics Market.

June 2025: Updated long-term follow-up data was presented for ipilimumab in combination with nivolumab for advanced melanoma, reinforcing the durable responses and long-term survival benefits observed in previously published trials. This data further solidifies the role of CTLA-4 antibodies in first-line treatment for this indication.

April 2025: European regulators approved an expanded label for a CTLA-4 antibody in combination with another immunotherapy for the treatment of advanced hepatocellular carcinoma, offering a new therapeutic option for patients in the region and contributing to the growth of the Immunotherapy Drug Market.

Regional Market Breakdown for ctla 4 antibody Market

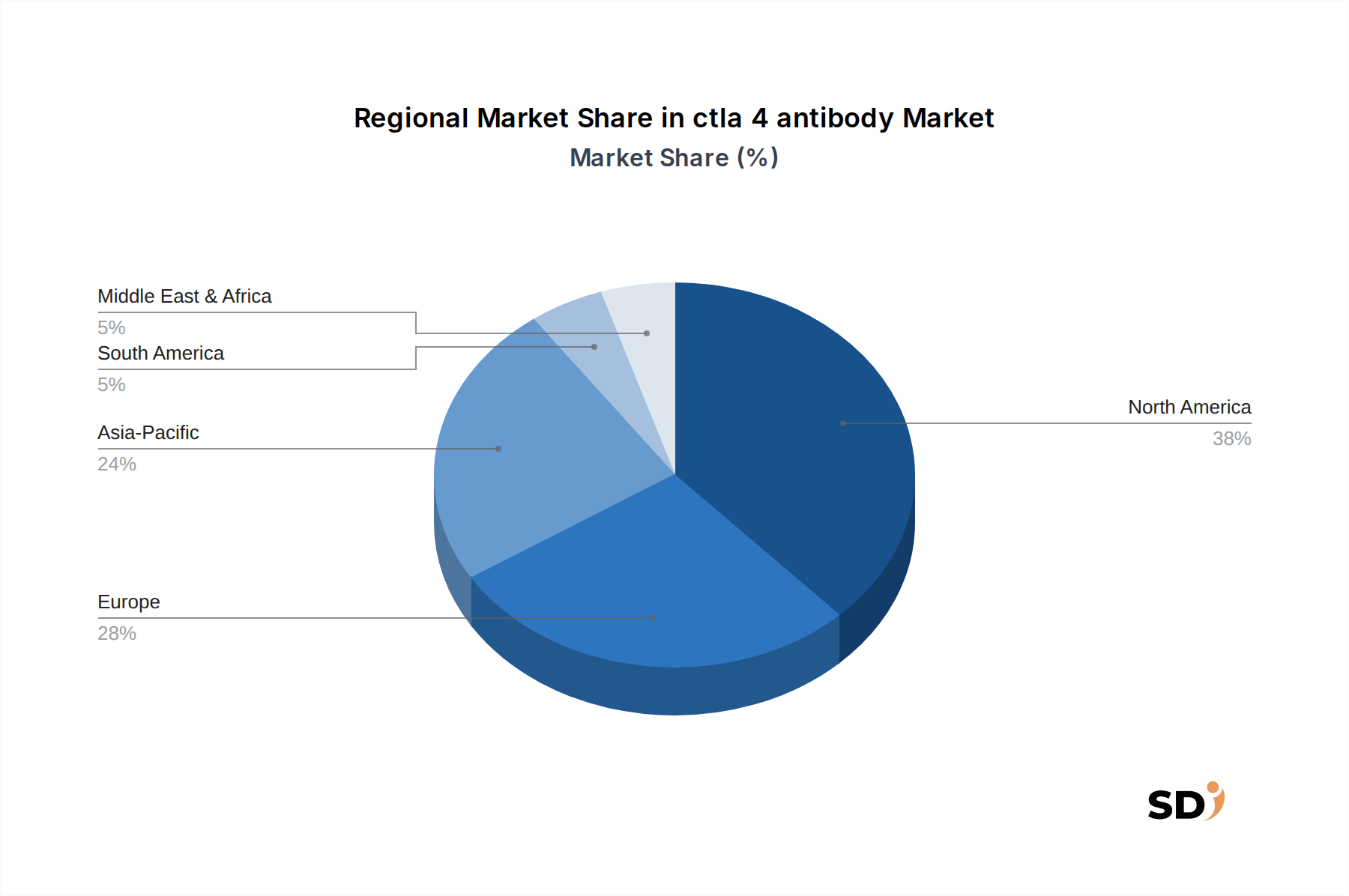

The global ctla 4 antibody Market exhibits varied dynamics across key geographical regions, driven by disparate healthcare infrastructures, regulatory landscapes, disease prevalence, and economic conditions. North America, particularly the United States, holds the largest revenue share in the ctla 4 antibody Market. This dominance is attributable to a high incidence of target cancers like melanoma, advanced healthcare facilities, robust R&D investment in the Pharmaceuticals Market, and favorable reimbursement policies. The region is characterized by early adoption of novel therapies and a strong presence of key market players, contributing to its projected steady growth.

Europe represents the second-largest market, with countries like Germany, France, and the UK contributing significantly. The region benefits from well-established healthcare systems, increasing awareness of immunotherapy, and supportive government initiatives for cancer research. However, stringent pricing and reimbursement policies, particularly in countries with nationalized healthcare, can pose challenges compared to the U.S. market. The adoption of CTLA-4 antibodies in Europe is steadily increasing, driven by expanding indications and a growing focus on personalized medicine.

Asia Pacific is projected to be the fastest-growing region in the ctla 4 antibody Market, albeit from a smaller base. This rapid growth is fueled by a burgeoning patient population with increasing cancer incidence, improving healthcare infrastructure, and rising healthcare expenditure in emerging economies like China and India. Government initiatives to enhance access to advanced cancer treatments and a growing number of clinical trials in the region are also significant drivers. Japan and South Korea are notable for their advanced medical research and early adoption of innovative treatments within the Monoclonal Antibody Market. The growing demand for advanced Biologics Manufacturing Market capabilities in this region further underscores its potential.

The Middle East & Africa and Latin America regions, while currently smaller, are anticipated to witness moderate growth. This growth is spurred by increasing investments in healthcare infrastructure, growing awareness, and a rising prevalence of cancer. However, challenges such as limited access to specialized treatments, economic constraints, and varying regulatory frameworks continue to influence market penetration in these regions. The global ctla 4 antibody Market's regional distribution reflects a clear correlation between advanced healthcare economies and the adoption of high-cost, cutting-edge biological therapies.

ctla 4 antibody Segmentation

1. Application

2. Types

ctla 4 antibody Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

ctla 4 antibody REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 12% from 2020-2034

Segmentation

By Application

By Types

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.2. Market Analysis, Insights and Forecast - by Types

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.2. Market Analysis, Insights and Forecast - by Types

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.2. Market Analysis, Insights and Forecast - by Types

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.2. Market Analysis, Insights and Forecast - by Types

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.2. Market Analysis, Insights and Forecast - by Types

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.2. Market Analysis, Insights and Forecast - by Types

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Global and United States

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Application 2025 & 2033

Figure 4: Volume (K), by Application 2025 & 2033

Figure 5: Revenue Share (%), by Application 2025 & 2033

Figure 6: Volume Share (%), by Application 2025 & 2033

Figure 7: Revenue (billion), by Types 2025 & 2033

Figure 8: Volume (K), by Types 2025 & 2033

Figure 9: Revenue Share (%), by Types 2025 & 2033

Figure 10: Volume Share (%), by Types 2025 & 2033

Figure 11: Revenue (billion), by Country 2025 & 2033

Figure 12: Volume (K), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Volume Share (%), by Country 2025 & 2033

Figure 15: Revenue (billion), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (billion), by Types 2025 & 2033

Figure 20: Volume (K), by Types 2025 & 2033

Figure 21: Revenue Share (%), by Types 2025 & 2033

Figure 22: Volume Share (%), by Types 2025 & 2033

Figure 23: Revenue (billion), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (billion), by Application 2025 & 2033

Figure 28: Volume (K), by Application 2025 & 2033

Figure 29: Revenue Share (%), by Application 2025 & 2033

Figure 30: Volume Share (%), by Application 2025 & 2033

Figure 31: Revenue (billion), by Types 2025 & 2033

Figure 32: Volume (K), by Types 2025 & 2033

Figure 33: Revenue Share (%), by Types 2025 & 2033

Figure 34: Volume Share (%), by Types 2025 & 2033

Figure 35: Revenue (billion), by Country 2025 & 2033

Figure 36: Volume (K), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Volume Share (%), by Country 2025 & 2033

Figure 39: Revenue (billion), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (billion), by Types 2025 & 2033

Figure 44: Volume (K), by Types 2025 & 2033

Figure 45: Revenue Share (%), by Types 2025 & 2033

Figure 46: Volume Share (%), by Types 2025 & 2033

Figure 47: Revenue (billion), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (billion), by Application 2025 & 2033

Figure 52: Volume (K), by Application 2025 & 2033

Figure 53: Revenue Share (%), by Application 2025 & 2033

Figure 54: Volume Share (%), by Application 2025 & 2033

Figure 55: Revenue (billion), by Types 2025 & 2033

Figure 56: Volume (K), by Types 2025 & 2033

Figure 57: Revenue Share (%), by Types 2025 & 2033

Figure 58: Volume Share (%), by Types 2025 & 2033

Figure 59: Revenue (billion), by Country 2025 & 2033

Figure 60: Volume (K), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

Figure 62: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Application 2020 & 2033

Table 2: Volume K Forecast, by Application 2020 & 2033

Table 3: Revenue billion Forecast, by Types 2020 & 2033

Table 4: Volume K Forecast, by Types 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Volume K Forecast, by Region 2020 & 2033

Table 7: Revenue billion Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue billion Forecast, by Types 2020 & 2033

Table 10: Volume K Forecast, by Types 2020 & 2033

Table 11: Revenue billion Forecast, by Country 2020 & 2033

Table 12: Volume K Forecast, by Country 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Volume (K) Forecast, by Application 2020 & 2033

Table 15: Revenue (billion) Forecast, by Application 2020 & 2033

Table 16: Volume (K) Forecast, by Application 2020 & 2033

Table 17: Revenue (billion) Forecast, by Application 2020 & 2033

Table 18: Volume (K) Forecast, by Application 2020 & 2033

Table 19: Revenue billion Forecast, by Application 2020 & 2033

Table 20: Volume K Forecast, by Application 2020 & 2033

Table 21: Revenue billion Forecast, by Types 2020 & 2033

Table 22: Volume K Forecast, by Types 2020 & 2033

Table 23: Revenue billion Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue billion Forecast, by Application 2020 & 2033

Table 32: Volume K Forecast, by Application 2020 & 2033

Table 33: Revenue billion Forecast, by Types 2020 & 2033

Table 34: Volume K Forecast, by Types 2020 & 2033

Table 35: Revenue billion Forecast, by Country 2020 & 2033

Table 36: Volume K Forecast, by Country 2020 & 2033

Table 37: Revenue (billion) Forecast, by Application 2020 & 2033

Table 38: Volume (K) Forecast, by Application 2020 & 2033

Table 39: Revenue (billion) Forecast, by Application 2020 & 2033

Table 40: Volume (K) Forecast, by Application 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Volume (K) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Volume (K) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Volume (K) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue billion Forecast, by Application 2020 & 2033

Table 56: Volume K Forecast, by Application 2020 & 2033

Table 57: Revenue billion Forecast, by Types 2020 & 2033

Table 58: Volume K Forecast, by Types 2020 & 2033

Table 59: Revenue billion Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (billion) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (billion) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (billion) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (billion) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue billion Forecast, by Application 2020 & 2033

Table 74: Volume K Forecast, by Application 2020 & 2033

Table 75: Revenue billion Forecast, by Types 2020 & 2033

Table 76: Volume K Forecast, by Types 2020 & 2033

Table 77: Revenue billion Forecast, by Country 2020 & 2033

Table 78: Volume K Forecast, by Country 2020 & 2033

Table 79: Revenue (billion) Forecast, by Application 2020 & 2033

Table 80: Volume (K) Forecast, by Application 2020 & 2033

Table 81: Revenue (billion) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue (billion) Forecast, by Application 2020 & 2033

Table 84: Volume (K) Forecast, by Application 2020 & 2033

Table 85: Revenue (billion) Forecast, by Application 2020 & 2033

Table 86: Volume (K) Forecast, by Application 2020 & 2033

Table 87: Revenue (billion) Forecast, by Application 2020 & 2033

Table 88: Volume (K) Forecast, by Application 2020 & 2033

Table 89: Revenue (billion) Forecast, by Application 2020 & 2033

Table 90: Volume (K) Forecast, by Application 2020 & 2033

Table 91: Revenue (billion) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology forms the cornerstone of our market intelligence, accounting for approximately 75% of the total research effort. This robust approach is designed to capture real-time, nuanced insights directly from key stakeholders across the value chain of the CTLA-4 antibody market. We conduct extensive qualitative and quantitative interviews, engaging with industry experts, decision-makers, and thought leaders.

Key primary research participants are drawn from:

Company Types:

Biopharmaceutical Companies (Developers & Manufacturers of CTLA-4 Antibodies)

Contract Research Organizations (CROs) specializing in Oncology Clinical Trials

Specialty Pharmacy & Biologics Distributors

Biotechnology Startups focused on Immuno-Oncology

Academic Research Institutions & Major Cancer Centers

Stakeholder Job Titles:

VP, Clinical Development / Head of Oncology R&D

Director, Market Access & Reimbursement Strategy

Senior Medical Affairs Liaison / Regional Medical Director

Head of Global Commercial Strategy (Biologics/Oncology)

This direct engagement allows us to validate secondary findings, gather proprietary data, understand market dynamics, competitive landscapes, emerging trends, and future growth trajectories for the CTLA-4 antibody market across various applications and geographies.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP, Clinical Development / Head of Oncology R&D

30%

Director, Market Access & Reimbursement Strategy

25%

Senior Medical Affairs Liaison / Regional Medical Director

25%

Head of Global Commercial Strategy (Biologics/Oncology)

Academic Research Institutions & Major Cancer Centers

10%

Secondary Research & Industry Benchmarking

Complementing our primary research, secondary research constitutes the remaining 25% of our methodology, providing foundational data and extensive market context. This phase involves meticulous data collection from credible, authoritative sources to establish a comprehensive understanding of the CTLA-4 antibody market.

Our secondary research leverages:

Standard Financial Databases: Bloomberg, Factiva, Hoovers, and PitchBook, providing critical financial data, company profiles, and investment trends.

Government & Organizational Data: Publicly available information from official .Gov and .org websites, including national health registries, patent databases, and clinical trial repositories. We specifically avoid data from other market research websites.

Company annual reports, investor presentations, press releases, and scientific journals.

This stage provides critical market intelligence, historical data, technological advancements, regulatory frameworks, and competitive benchmarking, informing our overall market assessment.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies integrate both top-down and bottom-up approaches, triangulated to ensure robust and reliable estimates. This multi-level data triangulation involves correlating findings from various sources and methodologies to minimize error and enhance predictive accuracy.

Bottom-Up Approach: This method begins with granular data points and aggregates them upwards to derive total market size. For the CTLA-4 antibody market, key variables considered include:

Prevalence and Incidence Rates of specific target indications (e.g., advanced melanoma, non-small cell lung cancer, renal cell carcinoma).

Estimated Number of Diagnosed and Eligible Patient Populations for CTLA-4 antibody therapy.

Average Selling Price (ASP) per Dose/Treatment Course of approved CTLA-4 antibody drugs.

Market Penetration Rate of CTLA-4 antibodies within the addressable patient pool, considering competition and treatment guidelines.

Top-Down Approach: This method starts with overall market estimates or macroeconomic indicators and breaks them down to segment-specific levels. For the CTLA-4 antibody market, this involves analyzing total oncology biologics market size, therapeutic class growth rates, and regional healthcare expenditure trends to derive segment estimates.

Our forecasting model projects market trends from 2026 to 2034, meticulously segmenting data by Application, Types, and comprehensive geographical regions, including North America, South America, Europe, Middle East & Africa, and Asia Pacific.

Data Accuracy & Quality Check

We are committed to delivering highly accurate and reliable market intelligence. Our rigorous methodology guarantees an estimated data accuracy level of 85-90%. This is achieved through:

Multi-Level Data Triangulation: Cross-verification of data points gathered from primary, secondary, and internal proprietary databases to ensure consistency and minimize discrepancies.

Expert Panel Validation: Our findings and forecasts are periodically reviewed and validated by an internal panel of senior analysts and external subject matter experts in the biopharmaceutical and oncology fields.

Continuous Updates: Every report is dynamic and meticulously updated up to the date of purchase, reflecting the latest market developments, clinical trial outcomes, regulatory approvals, and competitive shifts, ensuring clients receive the most current and relevant insights.

Proprietary Analytical Tools: Utilization of advanced statistical and analytical tools to process complex datasets, identify trends, and project future market scenarios with high precision.

This commitment to quality ensures that our clients receive actionable, dependable market insights for strategic decision-making.

Frequently Asked Questions

1. What notable developments are shaping the CTLA-4 antibody market?

The CTLA-4 antibody market is seeing developments primarily in combination therapies and new indications within oncology applications. Key market players, including global and United States-based biopharmaceutical firms, are evolving their product pipelines to leverage these advancements.

2. What is the current investment activity in the CTLA-4 antibody market?

Investment in the CTLA-4 antibody market is robust, driven by the projected 12% CAGR. Venture capital and pharmaceutical companies are directing funds towards research and development, clinical trials, and expansion into various therapeutic areas for these antibodies.

3. What supply chain considerations are important for CTLA-4 antibody production?

Manufacturing CTLA-4 antibodies, as biologics, involves complex supply chain considerations for specialized raw materials and bioprocessing components. Maintaining a secure and efficient global supply chain is critical to meet demand and support the market's growth towards $2.5 billion by 2025.

4. Which region dominates the CTLA-4 antibody market, and what are the reasons?

North America is the dominant region in the CTLA-4 antibody market, accounting for an estimated 38% share. This leadership is attributed to advanced healthcare infrastructure, high research and development spending, and favorable market access for innovative immunotherapies.

5. How does the regulatory environment impact the CTLA-4 antibody market?

The regulatory environment significantly impacts the CTLA-4 antibody market through stringent approval processes from agencies such as the FDA and EMA. Compliance with rigorous safety, efficacy, and manufacturing standards is essential for product launch and commercial success in this therapeutic sector.

6. What emerging geographic opportunities exist for CTLA-4 antibodies?

Asia-Pacific represents a significant emerging geographic opportunity for CTLA-4 antibodies, with an estimated 24% market share. This region is poised for rapid growth due to increasing healthcare expenditure, rising prevalence of target diseases, and expanding biotechnology investments across countries like China and India.