Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Copper Chromite Market: Unpacking Its 4.5% CAGR & Key Trends

Copper Chromite

Copper Chromite Market: Unpacking Its 4.5% CAGR & Key Trends

Copper Chromite by Application (Laboratory, Chemical Industry, Industrial Application, Others), by Types (Purity 99%, Purity 99.9%, Purity 99.99%, Purity 99.999%, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 7, 2026|Base Year : 2025|Pages : 88

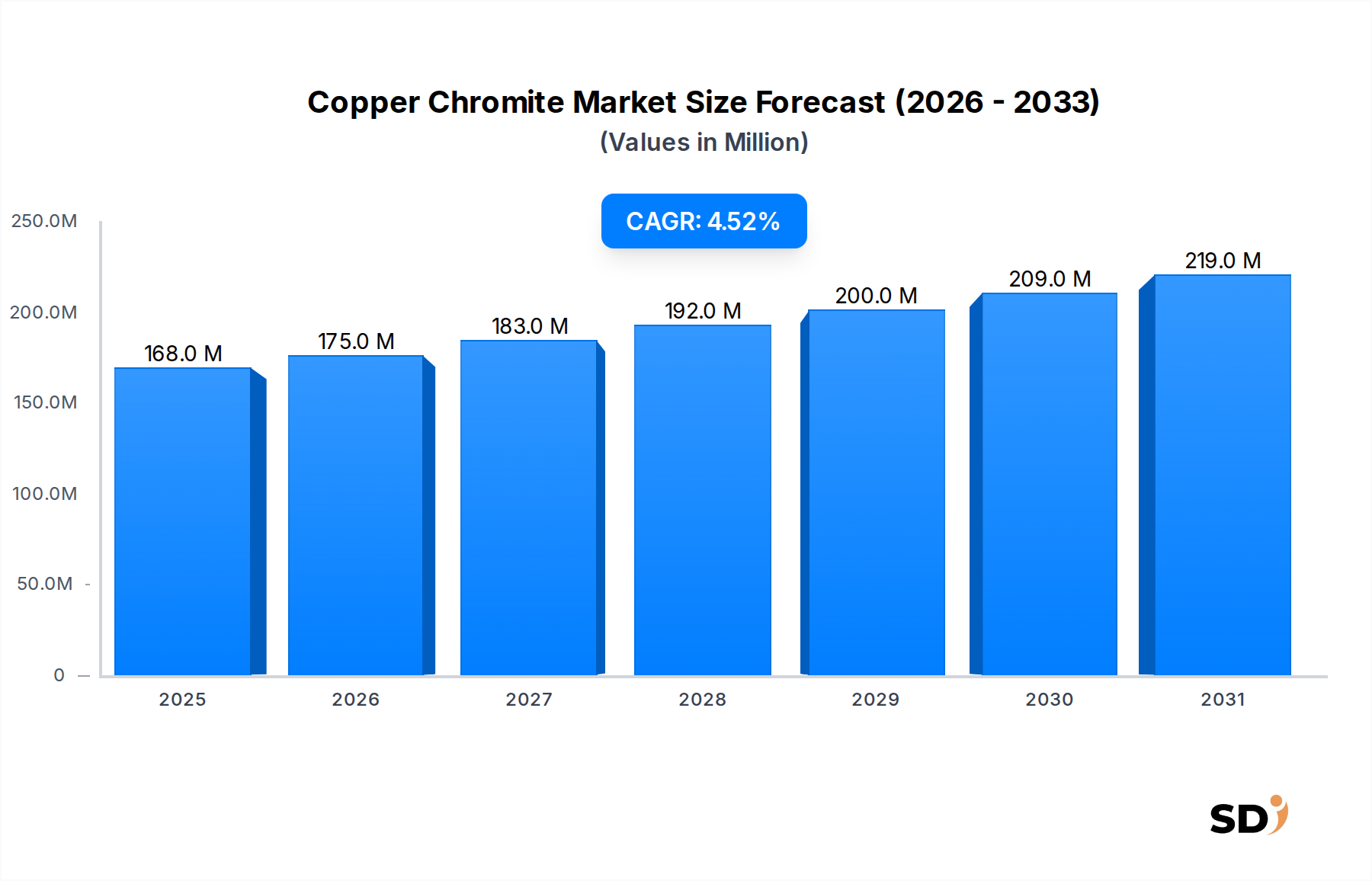

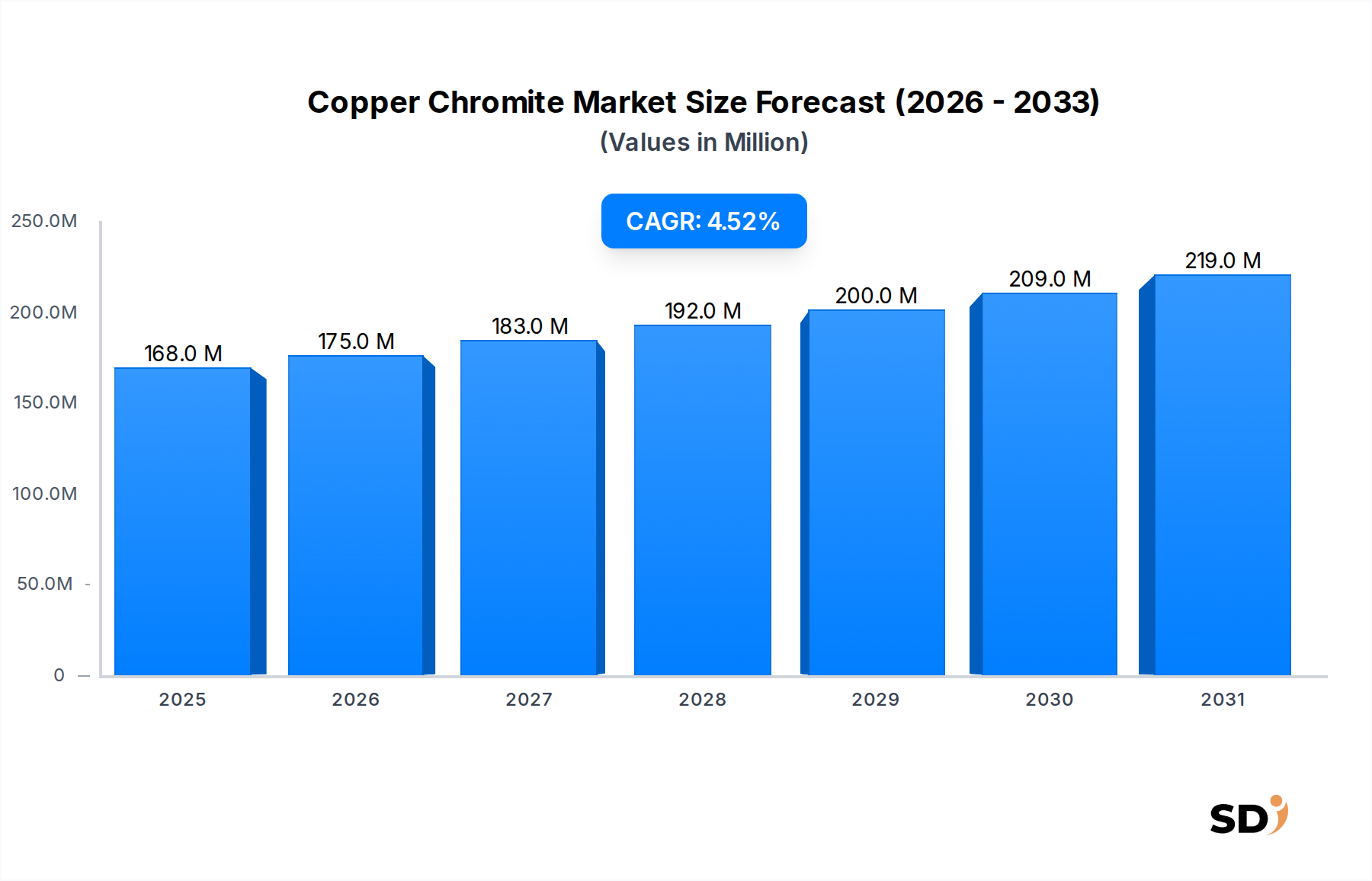

The global Copper Chromite Market was valued at $167.9 million in 2033 and is projected to expand significantly, reaching an estimated $228.06 million by 2040, demonstrating a compound annual growth rate (CAGR) of 4.5% during the forecast period. This robust growth trajectory is underpinned by the versatile applications of copper chromite, primarily as a high-performance catalyst, a durable pigment, and a key component in specialized industrial formulations. The market's expansion is intrinsically linked to increasing demand from the global Chemical Manufacturing Market, where copper chromite serves as an indispensable catalyst for various organic synthesis reactions, including hydrogenation and dehydrogenation processes. Furthermore, its excellent thermal stability and colorfast properties secure its position within the Pigment Market, particularly for ceramics, glass, and specialty coatings that require resilience under extreme conditions.

Copper Chromite Market Size (In Million)

250.0M

200.0M

150.0M

100.0M

50.0M

0

168.0 M

2025

175.0 M

2026

183.0 M

2027

192.0 M

2028

200.0 M

2029

209.0 M

2030

219.0 M

2031

Macroeconomic tailwinds such as accelerated industrialization in emerging economies, alongside continuous research and development in advanced materials, are further bolstering market growth. The increasing focus on material science innovations aims to enhance the efficiency and expand the application scope of copper chromite, particularly in high-growth sectors like automotive (for brake pads) and aerospace (as a burning rate modifier in solid rocket propellants). The demand for high-purity grades of the compound is also on an upward trend, driven by the stringent requirements of the High-Purity Chemicals Market for advanced catalytic converters and other sensitive applications. While facing scrutiny due to environmental regulations concerning chromium compounds, the market is characterized by a strategic shift towards sustainable synthesis methods and responsible product lifecycle management. This enables the Copper Chromite Market to maintain stable growth, driven by specialized, high-value applications despite environmental considerations.

Industrial Application Segment in the Copper Chromite Market

The "Industrial Application" segment, encompassing a broad spectrum of end-use industries, stands as the dominant category by revenue share within the global Copper Chromite Market. This segment's preeminence is attributable to copper chromite's versatile functionalities as a high-performance catalyst, a thermally stable pigment, and a critical component in various specialized industrial formulations. Its exceptional catalytic activity makes it invaluable in the Chemical Manufacturing Market for key organic synthesis reactions, particularly hydrogenation of esters to alcohols, and dehydrogenation processes essential for producing a wide range of chemicals. The demand here is driven by the global output of petrochemicals, specialty chemicals, and fine chemicals, where efficient and selective catalysis is paramount. The increasing need for such processes directly translates into sustained demand for copper chromite catalysts, bolstering the overall Industrial Catalysis Market.

Beyond catalysis, the Industrial Application segment also benefits from the demand for durable, heat-resistant pigments. Copper chromite imparts stable color in challenging environments, making it a preferred choice for coloring ceramics, glass, and high-temperature coatings used in construction and various manufacturing processes. Its inclusion as a burning rate modifier in solid rocket propellants and as a friction material component in automotive brake pads further underscores its critical role across diverse industrial verticals. Key players such as American Elements, Tanyun Chemical, and Alfa Chemistry cater to this broad and demanding segment, providing various grades and formulations of copper chromite to meet specific industrial requirements. The growth of this segment is particularly pronounced in Asia Pacific, driven by rapid industrial expansion and increased manufacturing output. The continued investment in research and development to optimize catalytic properties and expand pigment applications, alongside the ongoing push for advanced materials in sectors like automotive and aerospace, further solidifies the Industrial Application segment's dominant position and ensures its sustained expansion within the global Copper Chromite Market.

Key Market Drivers & Constraints in the Copper Chromite Market

Market Drivers:

Demand in Specialty Catalysis: Copper chromite's efficacy in facilitating a range of hydrogenation and dehydrogenation reactions is a primary driver. For instance, global production of fatty alcohols, which heavily relies on copper chromite catalysts for the hydrogenation of fatty esters, experienced an average annual growth of approximately 3-4% between 2021 and 2023. This consistent growth in downstream chemical processes significantly boosts the Catalyst Market and, by extension, the Chemical Manufacturing Market's demand for copper chromite.

Growth in Pigment and Colorant Applications: Copper chromite is valued for its high thermal stability and opacity, making it an ideal pigment for ceramics, glass, and high-temperature coatings. The global ceramics market alone witnessed an average annual growth of 3.5% from 2020 to 2023, translating into a steady increase in demand for copper chromite as a durable colorant, thereby propelling the Pigment Market. This consistent demand underscores its irreplaceable role in applications requiring long-lasting color under harsh conditions.

Aerospace and Defense Sector Applications: Its critical role as a burning rate modifier in solid rocket propellants and in certain pyrotechnic compositions ensures a niche but high-value demand. Global defense spending, which saw an increase of 9% in 2023, particularly in advanced propulsion systems, provides a stable revenue stream for copper chromite manufacturers in specialized applications.

Market Constraints:

Environmental and Health Regulations: Chromium compounds, including copper chromite, face increasingly stringent environmental and health regulations globally due to the potential toxicity of hexavalent chromium byproducts. Regulatory bodies like the European Chemicals Agency (ECHA) and the U.S. Environmental Protection Agency (EPA) continue to tighten permissible limits and impose stricter handling and disposal guidelines. These regulations increase operational costs for producers and end-users, affecting the overall Copper Chromite Market.

Availability and Price Volatility of Raw Materials: The market is highly susceptible to the price fluctuations and supply chain disruptions of its primary raw materials: copper and chromium. The Copper Compounds Market saw significant price swings, with copper futures peaking at over $10,000 per metric ton in 2021 and 2022, directly impacting manufacturing costs. Similarly, the Chromium Oxide Market experiences volatility, largely tied to the demand from the stainless steel industry for ferrochrome, leading to unpredictable raw material costs.

Emergence of Alternative Materials: For some catalytic applications, alternatives such as palladium, nickel, or iron-based catalysts are gaining traction due to lower toxicity, cost-effectiveness, or superior performance in specific reactions. This substitution pressure poses a challenge, particularly in the High-Purity Chemicals Market, where innovation in non-chromite catalysts offers competitive alternatives.

Competitive Ecosystem of the Copper Chromite Market

The Copper Chromite Market features a diverse competitive landscape comprising established chemical manufacturers, specialty material suppliers, and research chemical providers. These entities primarily focus on product purity, application-specific formulations, and global distribution capabilities.

American Elements: A leading producer and supplier of advanced materials, specialty chemicals, and high-purity metals, offering a diverse portfolio including various forms of copper chromite tailored for demanding R&D and industrial applications.

Tanyun Chemical: Specializes in fine chemicals and custom synthesis, providing high-quality copper chromite solutions that are precisely engineered for specific industrial catalytic and pigment applications, with a strong focus on technical support.

Biosynth Carbosynth: A global supplier of life science reagents and specialty chemicals, offering high-purity grades of copper chromite primarily for demanding research applications and catering to the specialized needs of the Laboratory Chemicals Market.

HIMEDIA: A prominent biotechnology and pharmaceutical company that also operates in the specialty chemicals sector, supplying copper chromite for analytical and industrial uses with a strong emphasis on quality control and compliance.

Alfa Chemistry: A global supplier of chemicals, materials, and laboratory supplies, providing a wide array of purities of copper chromite to cater to both research-grade requirements and industrial bulk procurement across various sectors.

Otto Chemie Pvt Ltd: An Indian-based manufacturer and supplier of laboratory chemicals and industrial raw materials, offering competitive solutions for copper chromite, particularly serving the domestic and regional Chemical Manufacturing Market with a focus on cost-efficiency.

Recent Developments & Milestones in the Copper Chromite Market

October 2022: Researchers at the University of California published findings on enhanced catalytic activity of copper chromite nanoparticles in selective hydrogenation, marking a significant step towards more efficient and environmentally friendly industrial processes.

March 2023: Tanyun Chemical announced the expansion of its production capacity for high-purity copper chromite, aiming to meet the rising global demand from the High-Purity Chemicals Market for advanced catalytic converters and specialty pigment formulations.

July 2023: A consortium of leading European chemical manufacturers initiated a collaborative research project focused on exploring sustainable synthesis routes for chromium-based catalysts, including copper chromite, to mitigate environmental impact and ensure long-term viability.

November 2023: American Elements introduced a new ultra-fine powdered copper chromite variant specifically optimized for aerospace propellant applications, offering improved combustion stability and enhanced energy efficiency for high-performance systems.

February 2024: Regulatory updates from the European Chemicals Agency (ECHA) initiated a comprehensive review process for certain chromite compounds, prompting manufacturers within the Specialty Chemicals Market to invest further in R&D for safer handling and application methods.

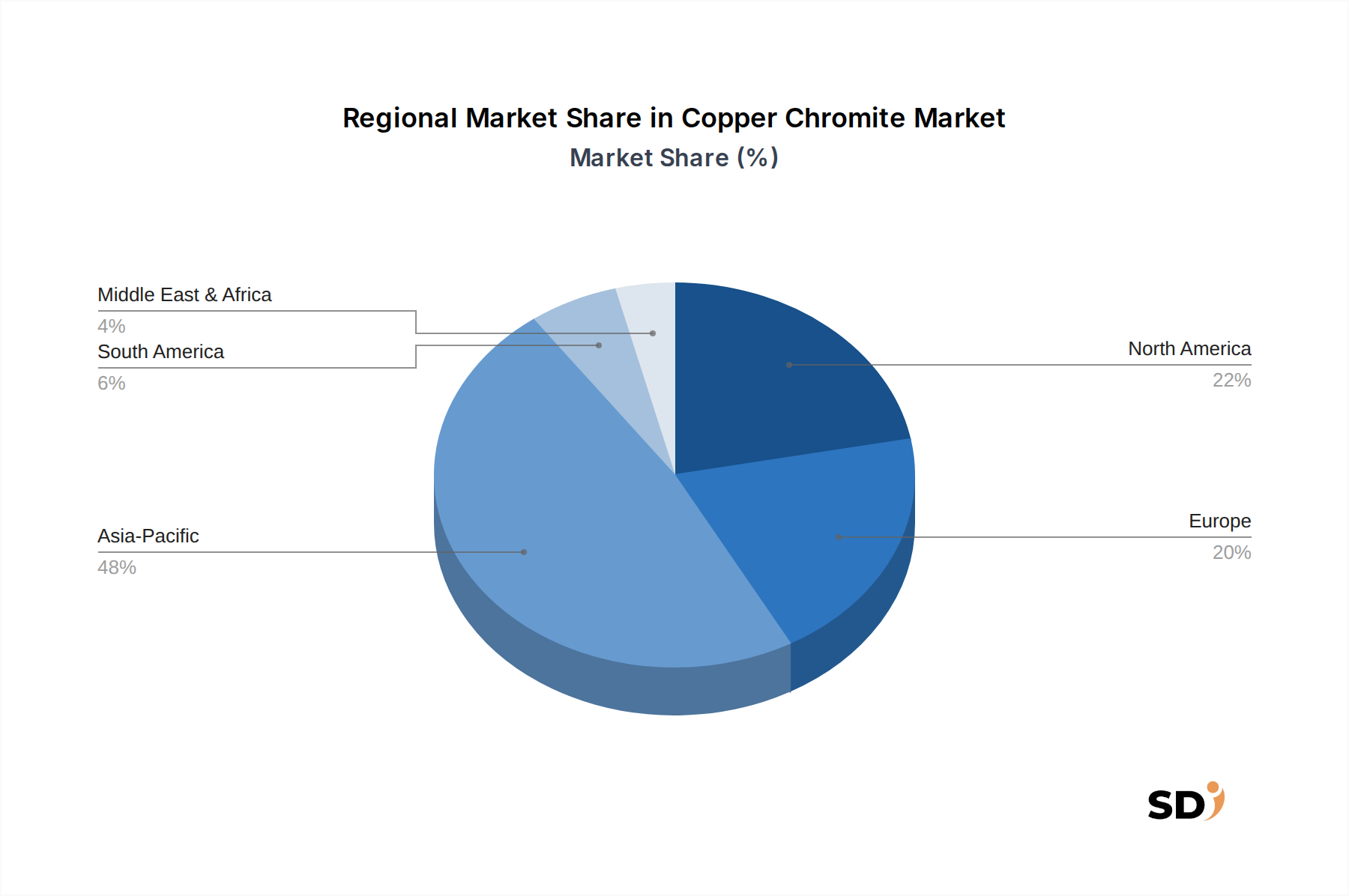

Regional Market Breakdown for the Copper Chromite Market

Geographically, the Copper Chromite Market demonstrates varied growth trajectories and demand dynamics across key regions. The market's overall growth is significantly influenced by industrial output, regulatory frameworks, and technological advancements within each area.

Asia Pacific: This region dominates the Copper Chromite Market, holding an estimated revenue share of 40-45% in 2033 and projected to exhibit the highest CAGR, exceeding 5.5% annually. This robust growth is primarily fueled by rapid industrialization, particularly the burgeoning Chemical Manufacturing Market in China and India, and the escalating demand for pigments and catalysts in sectors such as automotive, construction, and textiles. The region benefits from lower production costs and a vast manufacturing base, making it a critical hub for both production and consumption.

Europe: Representing a substantial share of 20-25% of the global market, Europe maintains a stable CAGR of approximately 3.8%. Demand here is driven by advanced Industrial Catalysis Market applications, stringent quality requirements for the High-Purity Chemicals Market, and a strong presence of specialty chemical manufacturers focusing on niche, high-value applications. However, strict environmental regulations on chromium compounds continue to pose a moderating factor, driving innovation towards cleaner production methods.

North America: This region accounts for a significant share of 18-22% in the Copper Chromite Market, with a projected CAGR of about 4.0%. Demand stems from mature industrial sectors including aerospace, automotive, and specialized chemical production. Ongoing innovation in the Catalyst Market and a strong focus on high-performance materials continue to drive growth, particularly for advanced and niche applications where product efficacy is paramount.

Middle East & Africa: This region is an emerging market with a modest share of 5-7% but is projected to experience a relatively high CAGR of around 4.8%. Growth is primarily propelled by developing petrochemical industries and increasing infrastructure projects that necessitate specialized pigments and catalysts. Investments in enhancing local manufacturing capabilities are expected to boost regional consumption, albeit from a smaller existing base.

Latin America: Holding a modest share of 5-8% with a CAGR of roughly 4.2%, this region's market is supported by the expansion of the chemical industry, particularly in Brazil and Argentina, alongside developing manufacturing sectors that contribute to demand for copper chromite in various industrial applications.

Investment & Funding Activity in the Copper Chromite Market

The Copper Chromite Market, while specialized, has witnessed targeted investment and funding activity over the past 2-3 years, predominantly centered on enhancing product purity, sustainability, and application-specific performance. In early 2023, a prominent venture capital firm specializing in advanced materials invested an undisclosed sum into a startup focused on researching novel synthesis methods for high-purity copper chromite. This investment was aimed at developing processes that minimize environmental byproducts and improve catalytic efficiency, highlighting a broader industry trend towards sustainable chemistry within the Specialty Chemicals Market. Furthermore, strategic partnerships have been observed, such as a collaboration in late 2022 between a major chemical conglomerate and a leading academic institution. This partnership focused on optimizing copper chromite catalysts for bio-diesel production, reflecting the market's alignment with renewable energy applications and the evolving Catalyst Market landscape. While direct M&A activity specifically for copper chromite producers has been relatively subdued, larger chemical companies have strategically acquired smaller specialty chemical manufacturers to broaden their portfolio of inorganic catalysts and pigments. This indirect consolidation benefits the Copper Chromite Market by integrating supply chains and expanding distribution networks, especially for high-demand areas like the High-Purity Chemicals Market. Investments are primarily channeled into research and development to improve material properties and ensure compliance with stringent environmental standards, rather than merely expanding raw production capacity, underscoring a quality-driven growth strategy.

Supply Chain & Raw Material Dynamics for the Copper Chromite Market

The Copper Chromite Market is critically dependent on the stability and availability of its primary raw materials: copper compounds and chromium compounds. Upstream dependencies are significant, with major global copper production concentrated in Chile, Peru, and China, while chromium is predominantly sourced from South Africa, Kazakhstan, and India. This geographical concentration makes the market vulnerable to geopolitical risks, trade policy fluctuations, and regional supply disruptions. The Copper Compounds Market has historically been characterized by considerable price volatility, influenced by global industrial demand, speculative trading, and operational disruptions such as mining strikes or port congestion. For example, the price of copper experienced a substantial surge in 2021 and 2022, significantly escalating the production costs for copper chromite manufacturers. Similarly, the Chromium Oxide Market faces price pressures that are closely tied to the stainless steel industry's demand for ferrochrome, which can divert raw chromium resources and impact availability. Sourcing risks are further compounded by stringent environmental regulations governing chromium mining and processing, particularly concerns related to hexavalent chromium, necessitating careful and compliant sourcing strategies. Supply chain disruptions, as evidenced during global events like the COVID-19 pandemic, led to increased lead times and inflated logistics costs, putting considerable pressure on the profit margins of copper chromite producers, especially those serving the precision-driven Chemical Manufacturing Market and Laboratory Chemicals Market which demand high reliability. To mitigate these inherent risks, companies are increasingly exploring strategies such as diversifying their supplier base and investigating regional sourcing alternatives, although the global nature of these raw material markets limits complete independence.

Copper Chromite Segmentation

1. Application

1.1. Laboratory

1.2. Chemical Industry

1.3. Industrial Application

1.4. Others

2. Types

2.1. Purity 99%

2.2. Purity 99.9%

2.3. Purity 99.99%

2.4. Purity 99.999%

2.5. Others

Copper Chromite Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Copper Chromite REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 4.5% from 2020-2034

Segmentation

By Application

Laboratory

Chemical Industry

Industrial Application

Others

By Types

Purity 99%

Purity 99.9%

Purity 99.99%

Purity 99.999%

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Laboratory

5.1.2. Chemical Industry

5.1.3. Industrial Application

5.1.4. Others

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Purity 99%

5.2.2. Purity 99.9%

5.2.3. Purity 99.99%

5.2.4. Purity 99.999%

5.2.5. Others

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Laboratory

6.1.2. Chemical Industry

6.1.3. Industrial Application

6.1.4. Others

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Purity 99%

6.2.2. Purity 99.9%

6.2.3. Purity 99.99%

6.2.4. Purity 99.999%

6.2.5. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Laboratory

7.1.2. Chemical Industry

7.1.3. Industrial Application

7.1.4. Others

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Purity 99%

7.2.2. Purity 99.9%

7.2.3. Purity 99.99%

7.2.4. Purity 99.999%

7.2.5. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Laboratory

8.1.2. Chemical Industry

8.1.3. Industrial Application

8.1.4. Others

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Purity 99%

8.2.2. Purity 99.9%

8.2.3. Purity 99.99%

8.2.4. Purity 99.999%

8.2.5. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Laboratory

9.1.2. Chemical Industry

9.1.3. Industrial Application

9.1.4. Others

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Purity 99%

9.2.2. Purity 99.9%

9.2.3. Purity 99.99%

9.2.4. Purity 99.999%

9.2.5. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Laboratory

10.1.2. Chemical Industry

10.1.3. Industrial Application

10.1.4. Others

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Purity 99%

10.2.2. Purity 99.9%

10.2.3. Purity 99.99%

10.2.4. Purity 99.999%

10.2.5. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. American Elements

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Tanyun Chemical

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Biosynth Carbosynth

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. HIMEDIA

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Alfa Chemistry

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Otto Chemie Pvt Ltd

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (million), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (million), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (million), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (million), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (million), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (million), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (million), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (million), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (million), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (million), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (million), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Revenue million Forecast, by Types 2020 & 2033

Table 3: Revenue million Forecast, by Region 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Types 2020 & 2033

Table 6: Revenue million Forecast, by Country 2020 & 2033

Table 7: Revenue (million) Forecast, by Application 2020 & 2033

Table 8: Revenue (million) Forecast, by Application 2020 & 2033

Table 9: Revenue (million) Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Application 2020 & 2033

Table 11: Revenue million Forecast, by Types 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Types 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Revenue (million) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue million Forecast, by Application 2020 & 2033

Table 29: Revenue million Forecast, by Types 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue million Forecast, by Application 2020 & 2033

Table 38: Revenue million Forecast, by Types 2020 & 2033

Table 39: Revenue million Forecast, by Country 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

The primary research phase constitutes the cornerstone of our market analysis, accounting for approximately 75% of the total research effort. This robust approach ensures the inclusion of real-time market dynamics, nuanced qualitative insights, and validation of secondary findings directly from industry experts. Our methodology involves extensive telephonic and in-person interviews, along with surveys, conducted with a diverse array of stakeholders across the Copper Chromite value chain. Each interview is structured to gather specific data points, validate market assumptions, and explore emerging trends, technological advancements, and regulatory impacts.

Key stakeholders interviewed include:

Director of R&D, Catalysis & Process Development: Providing insights into product innovation, application specific requirements, and purity trends within chemical synthesis.

Head of Global Procurement, Specialty Inorganic Chemicals: Offering perspectives on supply chain dynamics, pricing strategies, and volume demand by purity grade and application.

Senior Product Manager, Industrial Pigments & Additives: Furnishing data on application growth, competitive landscape, and end-user preferences in industrial settings.

Chief Technology Officer (CTO) / VP Operations, Fine Chemicals Manufacturing: Contributing details on manufacturing processes, operational challenges, and adoption rates of copper chromite in various industrial applications.

Our interview panel spans various company types critical to the Copper Chromite ecosystem:

Secondary research underpins the market sizing, segmentation, and initial competitive landscaping, comprising the remaining 25% of the total research. This phase involves a rigorous review of published data from reputable, non-commercial sources. Our analysts meticulously gather and analyze information from:

Government Publications: Official statistics, trade data, and regulatory guidelines from national and international government bodies (e.g., U.S. Geological Survey, Eurostat).

Trade Associations & Industry Bodies: Reports, white papers, and statistics from recognized industry associations to understand market drivers, restraints, and technological shifts. Examples include the European Chemical Industry Council (CEFIC) (www.cefic.org), the American Chemical Society (ACS) (www.acs.org), and the International Chromium Development Association (ICDA) (www.icdacr.com).

Company Filings & Annual Reports: Publicly available financial statements, investor presentations, and annual reports of key market players to derive revenue, market share, and strategic insights.

Financial Databases: Subscription-based financial intelligence platforms such as Bloomberg, Factiva, Hoovers, and PitchBook are utilized to gather company-specific financial data, M&A activities, and competitive intelligence.

Academic Journals & Patents: Scientific literature and patent databases are reviewed for advancements in copper chromite synthesis, applications, and catalytic properties.

Crucially, data from other market research websites is strictly excluded to maintain the independence and integrity of our findings.

Demand Modeling & Market Estimation

Our market estimation employs a rigorous combination of top-down and bottom-up approaches, triangulated across multiple data sources and analytical models to ensure comprehensive coverage and accuracy. The market size for Copper Chromite is primarily calculated by:

Bottom-Up Approach: This involves aggregating specific market data points from the granular level. Key variables used include:

Production capacity and utilization rates (in tonnes/year) of key Copper Chromite manufacturing facilities globally.

Average Selling Price (ASP) for each purity grade (e.g., Purity 99%, Purity 99.9%, Purity 99.99%) across different regions and applications.

Application-specific consumption coefficients (e.g., kg of copper chromite per tonne of hydrogenated product in the chemical industry, or per batch of laboratory synthesis).

Historical and projected sales volumes (by purity and application) from manufacturers and distributors, verified through primary interviews.

Top-Down Approach: This method begins with macro-level data, such as the total size of the chemical industry or industrial applications where copper chromite is used, and then disaggregates it to estimate the Copper Chromite market share. This includes analyzing GDP growth, industrial output, and R&D spending trends.

Multi-level Data Triangulation: All market figures are triangulated using data from primary interviews, secondary sources, and our internal proprietary databases to ensure robust validation and reduce potential biases. This iterative process allows for cross-referencing and refining estimates at various levels of market segmentation (application, type, region).

Data Accuracy & Quality Check

Our commitment to data integrity is paramount. We guarantee an estimated data accuracy level of 85-90% for all quantitative market figures presented in this report. This high level of accuracy is achieved through:

Expert Validation: All primary data collected is meticulously cross-verified with multiple sources and validated by a panel of internal senior analysts and external industry experts.

Statistical Analysis: Robust statistical models are applied to identify trends, extrapolate data, and forecast future market trajectories, ensuring the reliability of projections.

Continuous Updates: The market data and forecasts are dynamically updated up to the date of purchase, reflecting the latest market shifts, technological advancements, and economic indicators, ensuring that clients receive the most current and relevant insights.

Frequently Asked Questions

1. What are the primary restraints impacting the Copper Chromite market?

The Copper Chromite market, valued at $167.9 million, faces potential restraints such as raw material price volatility and stringent environmental regulations. Supply chain stability, especially for key precursor chemicals, remains a constant consideration for industry participants.

2. What entry barriers exist in the Copper Chromite industry?

High capital investment for production facilities and specialized R&D are significant barriers to entry in the Copper Chromite market. Established players like American Elements and Tanyun Chemical leverage proprietary synthesis methods and extensive distribution networks as competitive moats.

3. Which region offers the fastest growth opportunities for Copper Chromite?

Asia-Pacific is projected to exhibit robust growth, driven by expanding chemical and industrial applications in countries like China and India. This region's industrial development supports the 4.5% CAGR anticipated for the global Copper Chromite market.

4. What are the key raw material sourcing considerations for Copper Chromite?

Sourcing for Copper Chromite primarily involves obtaining high-purity copper and chromium compounds. Reliable access to these metals and their derivatives is crucial, influencing production costs for companies such as Alfa Chemistry and Biosynth Carbosynth.

5. How do sustainability and ESG factors influence the Copper Chromite market?

Sustainability initiatives in the Copper Chromite sector focus on reducing waste generation and optimizing energy consumption during manufacturing processes. Addressing the environmental footprint of industrial applications is increasingly important for market participants.

6. What are the main growth drivers for the Copper Chromite market?

Demand for Copper Chromite is primarily catalyzed by its extensive use in the Chemical Industry and various Industrial Applications. Its utility in laboratory research and specialized industrial processes underpins the market's 4.5% CAGR projected through 2033.