Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Circulating Biomarker by Application (Hospital, Medical Research Center, Others), by Types (Circulating DNA, Circulating Tumor Cells, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 6, 2026|Base Year : 2025|Pages : 99

Key Insights into the Circulating Biomarker Market

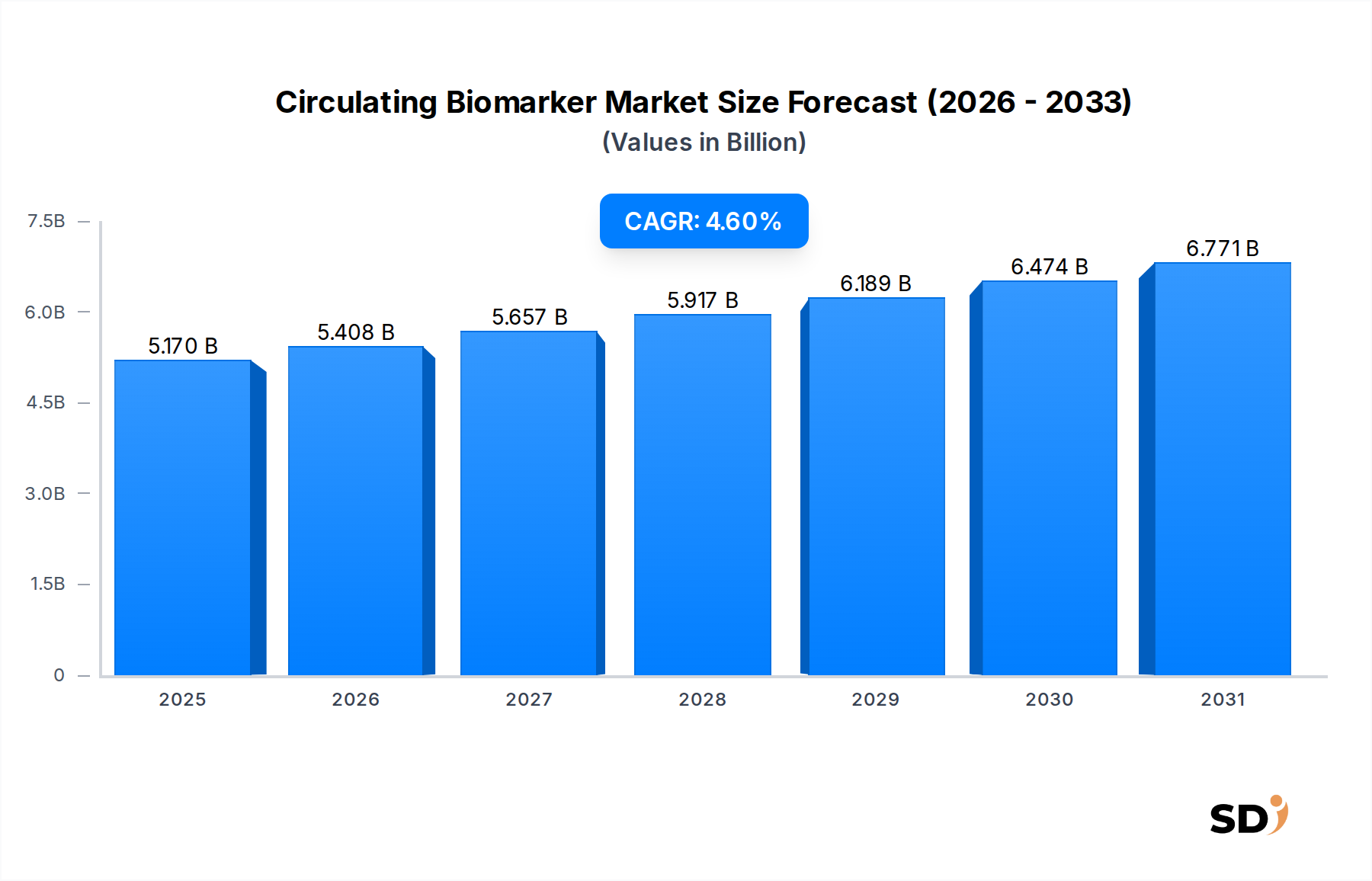

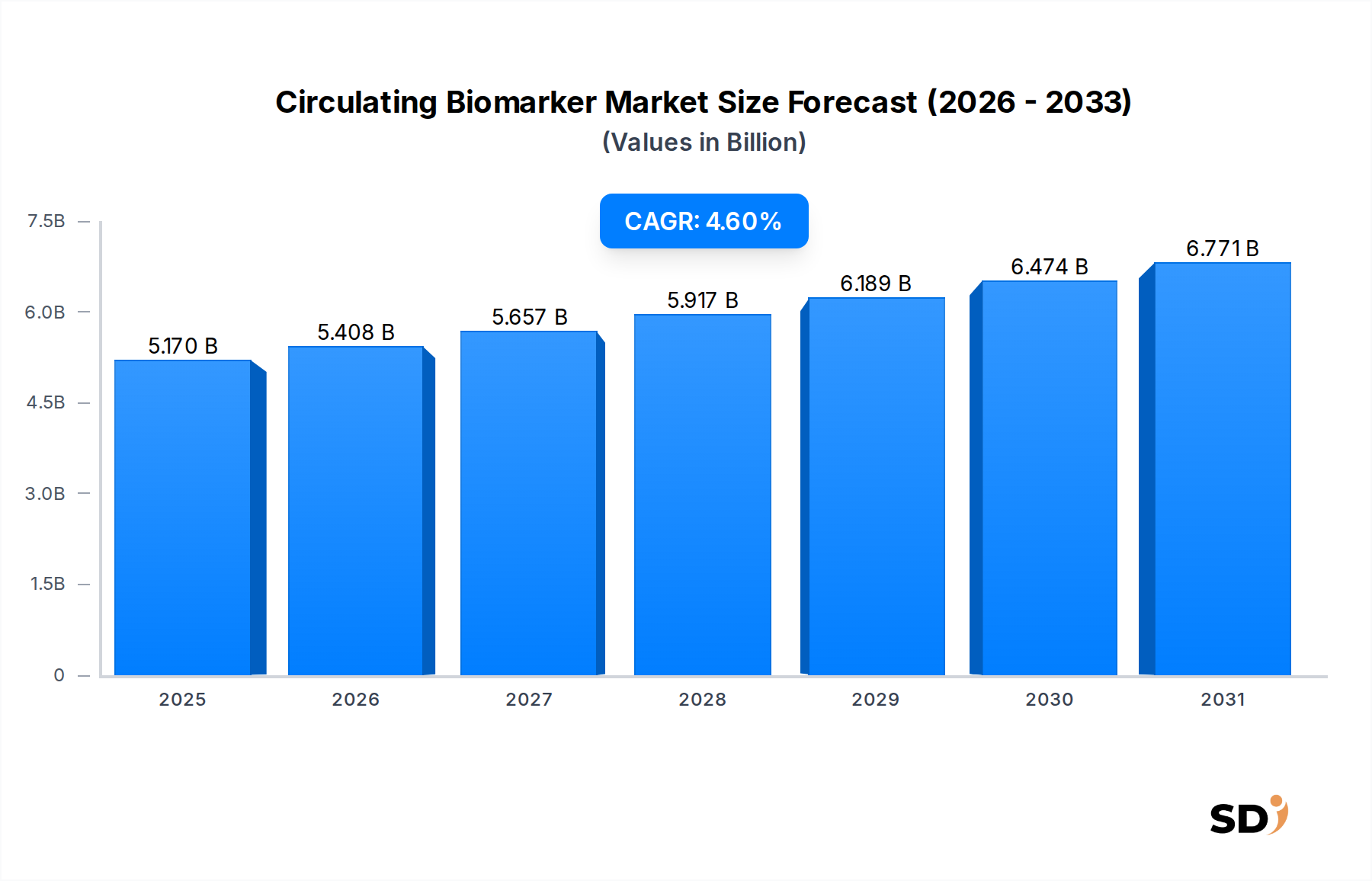

The Circulating Biomarker Market is poised for substantial growth, driven by a paradigm shift towards non-invasive diagnostics and personalized medicine. Valued at an estimated $5.17 billion in 2025, the market is projected to expand at a Compound Annual Growth Rate (CAGR) of 4.6%, reaching approximately $7.03 billion by 2032. This robust expansion is primarily fueled by increasing advancements in omics technologies, rising prevalence of chronic diseases such as cancer and cardiovascular conditions, and a growing emphasis on early disease detection and monitoring. Circulating biomarkers, including circulating tumor cells (CTCs), cell-free DNA (cfDNA), circulating microRNAs, and exosomes, offer critical advantages over traditional biopsy methods, namely reduced invasiveness, capability for serial monitoring, and the potential to provide a comprehensive genetic and proteomic landscape of a disease.

Circulating Biomarker Market Size (In Billion)

7.5B

6.0B

4.5B

3.0B

1.5B

0

5.170 B

2025

5.408 B

2026

5.657 B

2027

5.917 B

2028

6.189 B

2029

6.474 B

2030

6.771 B

2031

The strategic adoption of these advanced diagnostic tools is transforming clinical practice, particularly within oncology where they serve as invaluable assets for screening, prognosis, therapeutic response monitoring, and detecting minimal residual disease. The integration of artificial intelligence and machine learning algorithms is further enhancing the analytical precision and interpretability of complex biomarker data, thereby accelerating diagnostic workflows. Moreover, the expanding scope beyond oncology into areas such as prenatal testing, infectious diseases, and neurodegenerative disorders signifies a broadening application horizon. Collaboration between academic institutions, pharmaceutical companies, and diagnostic developers is crucial for standardizing assays and ensuring clinical validity, thereby overcoming existing challenges related to assay sensitivity and specificity. The rapid evolution of technologies like the Next-Generation Sequencing Market and the burgeoning Liquid Biopsy Market are direct beneficiaries and key drivers of innovation within this space. As healthcare systems globally prioritize patient-centric and outcome-driven care, the Circulating Biomarker Market is set to play an increasingly indispensable role in the future of diagnostics and therapeutic management, underpinning the expansion of the broader Precision Medicine Market.

Dominant Circulating DNA Segment in the Circulating Biomarker Market

The Circulating Biomarker Market is significantly shaped by its 'Types' segments, among which Circulating DNA emerges as a dominant force. This segment, encompassing cell-free DNA (cfDNA) and circulating tumor DNA (ctDNA), commands a substantial revenue share due to its wide applicability, relative ease of isolation, and the profound advancements in molecular analysis techniques. The dominance of circulating DNA can be attributed to several key factors. Firstly, cfDNA can be harvested from various bodily fluids (blood, urine, CSF), making it a truly non-invasive biomarker source. Its application extends across diverse clinical areas, from non-invasive prenatal testing (NIPT) to transplant monitoring and, most notably, oncology. In cancer diagnostics, ctDNA offers a real-time snapshot of tumor heterogeneity, evolution, and response to treatment, providing actionable insights for personalized therapeutic strategies. This capability is pivotal for the rapidly evolving Oncology Diagnostics Market.

Technological breakthroughs, particularly in the Genomic Sequencing Market and high-throughput platforms, have drastically improved the sensitivity and specificity of cfDNA detection and quantification, allowing for the identification of rare mutations and epigenetic modifications even at very low concentrations. This has positioned ctDNA as a cornerstone of the Liquid Biopsy Market, enabling early cancer detection, recurrence monitoring, and the identification of resistance mechanisms without the need for invasive tissue biopsies. Major players in the Circulating Biomarker Market, including Agilent Technologies and Abbott Laboratories, are heavily invested in developing sophisticated assays and platforms for cfDNA analysis, further solidifying its market position. The increasing adoption of cfDNA analysis in routine clinical settings, driven by a growing body of clinical evidence supporting its utility, also contributes to its dominant share. Furthermore, research into novel applications, such as liquid biopsies for neurological disorders and infectious diseases, continues to expand the potential revenue streams for the circulating DNA segment. While Circulating Tumor Cells (CTCs) also hold immense promise, their technical challenges in isolation and analysis, compared to the relatively simpler process of isolating cfDNA, mean that circulating DNA currently holds a larger and more rapidly growing share. This trend is expected to continue as assay development matures and clinical guidelines increasingly incorporate cfDNA-based testing, particularly as part of the broader Molecular Diagnostics Market strategies.

Key Market Drivers and Constraints in Circulating Biomarker Market

The Circulating Biomarker Market is propelled by several robust drivers, while also navigating significant constraints that shape its trajectory. A primary driver is the escalating demand for non-invasive diagnostics. Traditional tissue biopsies are invasive, carry risks, and may not always be feasible or representative of tumor heterogeneity. Circulating biomarkers offer a less painful, safer, and repeatable alternative, facilitating serial monitoring of disease progression and treatment response. This is particularly critical in cancer management, where the ability to frequently assess molecular changes can optimize therapeutic strategies. For instance, the increasing adoption of the Liquid Biopsy Market technologies for cancer screening and recurrence monitoring underscores this demand, providing a quantifiable shift from invasive procedures.

Another significant driver is the advancement in genomic and proteomic technologies. Innovations in Next-Generation Sequencing Market (NGS), PCR-based assays, and mass spectrometry have dramatically improved the sensitivity, specificity, and multiplexing capabilities of biomarker detection. These technological leaps allow for the identification and quantification of extremely low concentrations of circulating DNA, RNA, proteins, and exosomes, enhancing diagnostic accuracy. This enables more precise applications in the Precision Medicine Market, allowing therapies to be tailored to an individual’s molecular profile. For example, the continuous evolution of sequencing platforms drives down costs and increases throughput, making advanced biomarker testing more accessible.

Conversely, a significant constraint on the Circulating Biomarker Market is the lack of standardization and regulatory hurdles. The diverse nature of circulating biomarkers, coupled with varied isolation techniques, analytical platforms, and data interpretation methods across different manufacturers and laboratories, leads to challenges in assay harmonization and comparability. This absence of standardization can hinder clinical utility and widespread adoption. Additionally, gaining regulatory approval for novel biomarker-based diagnostics, especially those with companion diagnostic claims, is a complex, time-consuming, and expensive process. The stringent requirements for analytical validity, clinical validity, and clinical utility necessitate extensive and costly clinical trials, which can significantly delay market entry and increase product development costs, impacting smaller players within the Companion Diagnostics Market. Overcoming these constraints requires concerted efforts from industry, academia, and regulatory bodies to establish clear guidelines and consensus standards.

Competitive Ecosystem of Circulating Biomarker Market

The Circulating Biomarker Market features a dynamic competitive landscape, with established diagnostic powerhouses alongside innovative biotech firms. Key players are intensely focused on R&D, strategic collaborations, and expanding their product portfolios to capture a larger market share in the In-vitro Diagnostics Market.

Abbott Laboratories: A global healthcare leader, Abbott maintains a strong presence in the diagnostics sector with a broad portfolio of instruments and assays, actively investing in platforms that can detect various circulating biomarkers for disease management, particularly in oncology and infectious diseases.

Becton, Dickinson and Company: Known for its medical technology, Becton, Dickinson and Company offers integrated solutions for specimen collection and preparation, which are crucial upstream components for circulating biomarker analysis, supporting efficient and standardized sample handling.

GE Healthcare: As a prominent provider of medical imaging, monitoring, and diagnostics, GE Healthcare contributes to the market through its expertise in high-precision analytical instruments and technologies applicable to advanced biomarker research and clinical implementation.

Epigenomics AG: This company is specialized in molecular diagnostics, particularly in epigenetics, focusing on novel blood-based tests for cancer detection, leveraging circulating biomarkers for early and accurate diagnosis of prevalent cancers.

Agilent Technologies: A leader in life sciences, diagnostics, and applied chemical markets, Agilent Technologies provides a wide array of instruments, software, and consumables essential for the research and clinical application of circulating biomarkers, including advanced genomic solutions.

Biocept: Biocept is a specialized oncology diagnostics company that develops and commercializes proprietary liquid biopsy tests, primarily focused on circulating tumor cells and cell-free DNA for cancer diagnosis and treatment monitoring.

Affymetrix: Although largely acquired by Thermo Fisher Scientific, Affymetrix historically played a key role in the genomics market, developing microarray technology essential for high-throughput analysis of genetic and epigenetic circulating biomarkers.

Fluxion Biosciences: Fluxion Biosciences develops cell analysis tools that facilitate the study of circulating tumor cells and other rare cells, providing platforms that enable researchers to isolate and characterize these critical biomarkers for cancer research and diagnostics.

Recent Developments & Milestones in Circulating Biomarker Market

January 2026: A major clinical trial published in the New England Journal of Medicine demonstrated the efficacy of a novel ctDNA-based liquid biopsy for minimal residual disease detection in early-stage colorectal cancer, showing superior sensitivity compared to traditional imaging in post-surgical monitoring.

March 2026: A leading diagnostic company received FDA Breakthrough Device designation for its multi-cancer early detection (MCED) test utilizing circulating RNA biomarkers, accelerating its review pathway for broad clinical use.

May 2026: Academic researchers at a prominent oncology center announced the successful validation of a new exosome-based biomarker panel for the non-invasive diagnosis of pancreatic cancer, achieving high specificity and sensitivity in preliminary studies.

July 2026: A strategic partnership was forged between a pharmaceutical giant and a molecular diagnostics firm to integrate companion diagnostics based on circulating biomarkers into late-stage clinical trials for a new immuno-oncology drug, aiming to identify optimal patient populations.

September 2026: New guidelines were issued by a leading professional medical society recommending the use of circulating tumor DNA (ctDNA) for treatment selection in advanced non-small cell lung cancer patients, signaling increased clinical adoption.

November 2026: A startup specializing in AI-driven biomarker analysis secured significant Series B funding to expand its platform for interpreting complex multi-omic circulating biomarker data, enhancing predictive analytics for disease progression.

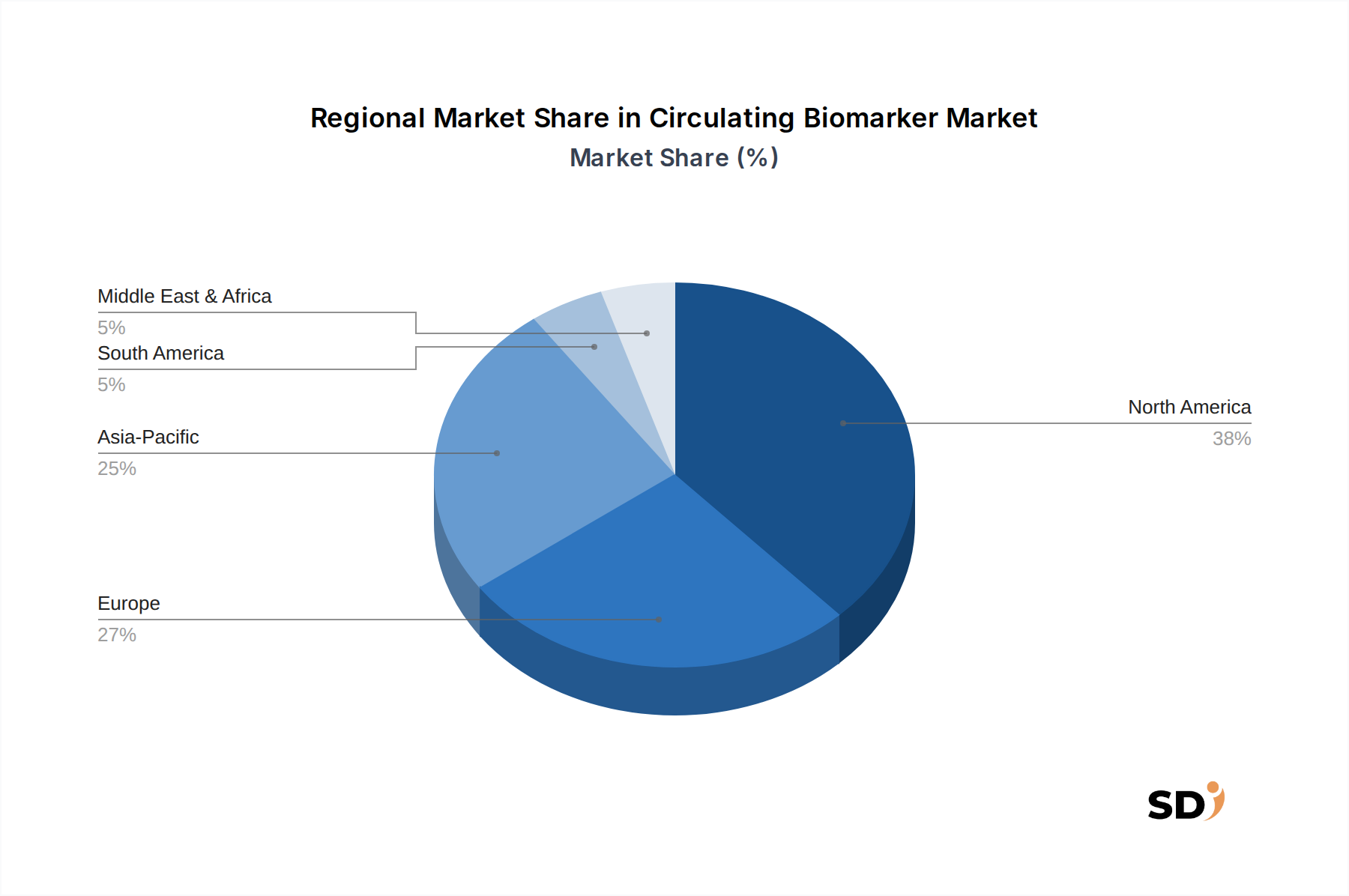

Regional Market Breakdown for Circulating Biomarker Market

Globally, the Circulating Biomarker Market exhibits distinct regional dynamics driven by varying healthcare infrastructures, research investments, and disease prevalence. North America holds the largest revenue share in the market, primarily due to significant R&D investments, a high adoption rate of advanced diagnostic technologies, and the presence of key market players. The region benefits from robust government funding for cancer research and a well-established regulatory framework that facilitates rapid innovation and commercialization of new biomarker tests. The United States, in particular, leads in the development and uptake of the Liquid Biopsy Market and Companion Diagnostics Market solutions.

Europe follows North America, representing a substantial market share, propelled by increasing awareness about early disease detection, a strong focus on personalized medicine initiatives, and growing healthcare expenditure. Countries like Germany, the UK, and France are at the forefront of adopting circulating biomarker technologies, especially in oncology and prenatal screening. Collaborative research efforts across European Union member states further stimulate market growth, though varying reimbursement policies across countries can present a challenge.

Asia Pacific is identified as the fastest-growing region in the Circulating Biomarker Market, exhibiting a higher CAGR compared to other regions. This rapid expansion is attributable to improving healthcare infrastructure, a large patient pool, rising prevalence of chronic diseases, and increasing healthcare spending, particularly in emerging economies like China and India. Government initiatives to promote early disease detection and the rising demand for non-invasive diagnostic tests are significant drivers. Japan and South Korea are also prominent contributors, with strong R&D capabilities and a high adoption rate of advanced molecular diagnostics, including the Next-Generation Sequencing Market.

In the Middle East & Africa and South America regions, the market is in an nascent stage but is expected to grow steadily. Growth here is primarily driven by increasing awareness, improving access to advanced healthcare facilities, and a rising burden of chronic diseases. However, challenges such as limited R&D infrastructure, lower healthcare expenditure compared to developed regions, and a fragmented regulatory landscape can impede faster market expansion. Nonetheless, investments in healthcare modernization and international collaborations are gradually opening up new opportunities for circulating biomarker applications in these regions, making the broader Clinical Diagnostics Market more accessible.

Export, Trade Flow & Tariff Impact on Circulating Biomarker Market

The Circulating Biomarker Market, while primarily focused on diagnostic services and kits, is subject to international trade dynamics concerning reagents, specialized instruments, and processed samples. Major trade corridors include transatlantic routes (North America to Europe) and trans-Pacific routes (North America to Asia-Pacific), reflecting established research collaborations and market demand. Leading exporting nations for advanced diagnostic instruments and high-value reagents often include the United States, Germany, Japan, and Switzerland, known for their strong life science and biotechnology sectors. Importing nations encompass a broader spectrum, particularly rapidly developing economies in Asia-Pacific and parts of South America and the Middle East, seeking to enhance their diagnostic capabilities. The trade in raw biological materials (e.g., purified antibodies, specialized enzymes) and analytical software also plays a role.

Tariffs and non-tariff barriers, such as import quotas, stringent quality control regulations, and complex customs procedures, can significantly impact the cross-border flow of these essential components. Recent global trade tensions have, in some instances, led to increased tariffs on medical devices and laboratory consumables. For example, specific duties imposed on high-precision analytical equipment or certain chemical reagents can increase the cost of importing crucial components for biomarker testing kits. This can inflate the final price of diagnostic services, making them less accessible in price-sensitive markets. Furthermore, non-tariff barriers like complex certification processes for In-vitro Diagnostics Market products can create significant delays and additional costs for manufacturers seeking to enter new markets. The impact of such policies on cross-border volume is often quantified by analyzing shifts in trade statistics for HS codes related to diagnostic reagents and instruments, showing an estimated 5-10% increase in landed costs for certain categories in affected regions over the past year. This necessitates strategic adjustments by companies, including localized manufacturing or diversified supply chains, to mitigate trade-related risks and ensure the steady supply of products essential for the Circulating Biomarker Market.

Sustainability & ESG Pressures on Circulating Biomarker Market

The Circulating Biomarker Market is increasingly facing scrutiny regarding its sustainability practices and adherence to Environmental, Social, and Governance (ESG) criteria. Environmental regulations and carbon targets are compelling manufacturers of diagnostic kits and instruments to re-evaluate their supply chains and operational footprints. This includes demands for reduced energy consumption in manufacturing facilities, minimized water usage, and the adoption of greener chemistry principles in reagent production. The high volume of disposable plasticware and chemical waste generated during biomarker analysis presents a significant challenge; hence, circular economy mandates are driving innovation in recyclable packaging, reusable components, and more efficient waste management protocols for laboratory consumables. Companies are exploring partnerships with specialized recycling firms to handle biohazardous and chemical waste responsibly, thereby reducing landfill impact.

On the social front, ESG investor criteria emphasize ethical sourcing of biological materials, ensuring patient privacy and data security, and promoting equitable access to advanced diagnostic technologies. The collection and analysis of human biological samples for biomarker research and diagnostics require robust consent processes and anonymization protocols to protect patient data, particularly in the Genomic Sequencing Market. Furthermore, there is growing pressure to address health inequalities, ensuring that the benefits of the Circulating Biomarker Market are not exclusive to affluent populations but are accessible globally. This includes efforts to reduce diagnostic costs and develop point-of-care solutions suitable for resource-limited settings. Governance considerations focus on transparent reporting of clinical trial results, ethical marketing practices, and robust corporate oversight to prevent conflicts of interest. The integration of ESG factors is not just a regulatory compliance exercise but is becoming a strategic imperative for companies in the Circulating Biomarker Market, influencing product development, procurement decisions, and long-term investment attractiveness.

Circulating Biomarker Segmentation

1. Application

1.1. Hospital

1.2. Medical Research Center

1.3. Others

2. Types

2.1. Circulating DNA

2.2. Circulating Tumor Cells

2.3. Other

Circulating Biomarker Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Circulating Biomarker REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 4.6% from 2020-2034

Segmentation

By Application

Hospital

Medical Research Center

Others

By Types

Circulating DNA

Circulating Tumor Cells

Other

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Hospital

5.1.2. Medical Research Center

5.1.3. Others

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Circulating DNA

5.2.2. Circulating Tumor Cells

5.2.3. Other

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Hospital

6.1.2. Medical Research Center

6.1.3. Others

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Circulating DNA

6.2.2. Circulating Tumor Cells

6.2.3. Other

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Hospital

7.1.2. Medical Research Center

7.1.3. Others

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Circulating DNA

7.2.2. Circulating Tumor Cells

7.2.3. Other

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Hospital

8.1.2. Medical Research Center

8.1.3. Others

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Circulating DNA

8.2.2. Circulating Tumor Cells

8.2.3. Other

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Hospital

9.1.2. Medical Research Center

9.1.3. Others

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Circulating DNA

9.2.2. Circulating Tumor Cells

9.2.3. Other

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Hospital

10.1.2. Medical Research Center

10.1.3. Others

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Circulating DNA

10.2.2. Circulating Tumor Cells

10.2.3. Other

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Abbott Laboratories

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Becton

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Dickinson and Company

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. GE Healthcare

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Epigenomics AG

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Agilent Technologies

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Biocept

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Affymetrix

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Fluxion Biosciences

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Application 2025 & 2033

Figure 4: Volume (K), by Application 2025 & 2033

Figure 5: Revenue Share (%), by Application 2025 & 2033

Figure 6: Volume Share (%), by Application 2025 & 2033

Figure 7: Revenue (billion), by Types 2025 & 2033

Figure 8: Volume (K), by Types 2025 & 2033

Figure 9: Revenue Share (%), by Types 2025 & 2033

Figure 10: Volume Share (%), by Types 2025 & 2033

Figure 11: Revenue (billion), by Country 2025 & 2033

Figure 12: Volume (K), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Volume Share (%), by Country 2025 & 2033

Figure 15: Revenue (billion), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (billion), by Types 2025 & 2033

Figure 20: Volume (K), by Types 2025 & 2033

Figure 21: Revenue Share (%), by Types 2025 & 2033

Figure 22: Volume Share (%), by Types 2025 & 2033

Figure 23: Revenue (billion), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (billion), by Application 2025 & 2033

Figure 28: Volume (K), by Application 2025 & 2033

Figure 29: Revenue Share (%), by Application 2025 & 2033

Figure 30: Volume Share (%), by Application 2025 & 2033

Figure 31: Revenue (billion), by Types 2025 & 2033

Figure 32: Volume (K), by Types 2025 & 2033

Figure 33: Revenue Share (%), by Types 2025 & 2033

Figure 34: Volume Share (%), by Types 2025 & 2033

Figure 35: Revenue (billion), by Country 2025 & 2033

Figure 36: Volume (K), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Volume Share (%), by Country 2025 & 2033

Figure 39: Revenue (billion), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (billion), by Types 2025 & 2033

Figure 44: Volume (K), by Types 2025 & 2033

Figure 45: Revenue Share (%), by Types 2025 & 2033

Figure 46: Volume Share (%), by Types 2025 & 2033

Figure 47: Revenue (billion), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (billion), by Application 2025 & 2033

Figure 52: Volume (K), by Application 2025 & 2033

Figure 53: Revenue Share (%), by Application 2025 & 2033

Figure 54: Volume Share (%), by Application 2025 & 2033

Figure 55: Revenue (billion), by Types 2025 & 2033

Figure 56: Volume (K), by Types 2025 & 2033

Figure 57: Revenue Share (%), by Types 2025 & 2033

Figure 58: Volume Share (%), by Types 2025 & 2033

Figure 59: Revenue (billion), by Country 2025 & 2033

Figure 60: Volume (K), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

Figure 62: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Application 2020 & 2033

Table 2: Volume K Forecast, by Application 2020 & 2033

Table 3: Revenue billion Forecast, by Types 2020 & 2033

Table 4: Volume K Forecast, by Types 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Volume K Forecast, by Region 2020 & 2033

Table 7: Revenue billion Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue billion Forecast, by Types 2020 & 2033

Table 10: Volume K Forecast, by Types 2020 & 2033

Table 11: Revenue billion Forecast, by Country 2020 & 2033

Table 12: Volume K Forecast, by Country 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Volume (K) Forecast, by Application 2020 & 2033

Table 15: Revenue (billion) Forecast, by Application 2020 & 2033

Table 16: Volume (K) Forecast, by Application 2020 & 2033

Table 17: Revenue (billion) Forecast, by Application 2020 & 2033

Table 18: Volume (K) Forecast, by Application 2020 & 2033

Table 19: Revenue billion Forecast, by Application 2020 & 2033

Table 20: Volume K Forecast, by Application 2020 & 2033

Table 21: Revenue billion Forecast, by Types 2020 & 2033

Table 22: Volume K Forecast, by Types 2020 & 2033

Table 23: Revenue billion Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue billion Forecast, by Application 2020 & 2033

Table 32: Volume K Forecast, by Application 2020 & 2033

Table 33: Revenue billion Forecast, by Types 2020 & 2033

Table 34: Volume K Forecast, by Types 2020 & 2033

Table 35: Revenue billion Forecast, by Country 2020 & 2033

Table 36: Volume K Forecast, by Country 2020 & 2033

Table 37: Revenue (billion) Forecast, by Application 2020 & 2033

Table 38: Volume (K) Forecast, by Application 2020 & 2033

Table 39: Revenue (billion) Forecast, by Application 2020 & 2033

Table 40: Volume (K) Forecast, by Application 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Volume (K) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Volume (K) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Volume (K) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue billion Forecast, by Application 2020 & 2033

Table 56: Volume K Forecast, by Application 2020 & 2033

Table 57: Revenue billion Forecast, by Types 2020 & 2033

Table 58: Volume K Forecast, by Types 2020 & 2033

Table 59: Revenue billion Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (billion) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (billion) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (billion) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (billion) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue billion Forecast, by Application 2020 & 2033

Table 74: Volume K Forecast, by Application 2020 & 2033

Table 75: Revenue billion Forecast, by Types 2020 & 2033

Table 76: Volume K Forecast, by Types 2020 & 2033

Table 77: Revenue billion Forecast, by Country 2020 & 2033

Table 78: Volume K Forecast, by Country 2020 & 2033

Table 79: Revenue (billion) Forecast, by Application 2020 & 2033

Table 80: Volume (K) Forecast, by Application 2020 & 2033

Table 81: Revenue (billion) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue (billion) Forecast, by Application 2020 & 2033

Table 84: Volume (K) Forecast, by Application 2020 & 2033

Table 85: Revenue (billion) Forecast, by Application 2020 & 2033

Table 86: Volume (K) Forecast, by Application 2020 & 2033

Table 87: Revenue (billion) Forecast, by Application 2020 & 2033

Table 88: Volume (K) Forecast, by Application 2020 & 2033

Table 89: Revenue (billion) Forecast, by Application 2020 & 2033

Table 90: Volume (K) Forecast, by Application 2020 & 2033

Table 91: Revenue (billion) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

The foundation of our market analysis for "Circulating Biomarker by Application, by Types, by North America, by South America, by Europe, by Middle East & Africa, by Asia Pacific Forecast 2026-2034" is robust primary research, constituting approximately 75% of our overall data collection efforts. This intensive engagement with industry stakeholders is crucial for validating secondary findings, capturing nuanced qualitative insights, and refining quantitative market estimates. Our primary interviews are meticulously structured to gather direct perspectives on market dynamics, technological advancements, competitive landscapes, pricing strategies, and future growth trajectories specific to circulating biomarkers.

Key stakeholders targeted for in-depth interviews include a diverse range of professionals across the value chain. Specific company types engaged in this research encompass:

Circulating Biomarker Assay Developers and Manufacturers

Specialized Diagnostic Laboratories (e.g., CLIA-certified labs focusing on oncology and genomic testing)

Pharmaceutical and Biotechnology Companies (integrating circulating biomarkers in drug development and companion diagnostics)

Contract Research Organizations (CROs) with expertise in clinical trials involving circulating biomarkers for precision medicine

Instrument Manufacturers providing platforms for circulating biomarker analysis

Specific job titles and decision-makers interviewed include:

Director of Molecular Diagnostics / Pathology (within hospital systems or reference labs)

Head of R&D, Companion Diagnostics (within pharmaceutical or biotechnology firms)

Chief Scientific Officer (CSO) or VP of Translational Medicine (at biomarker development startups or CROs)

Laboratory Director / Manager (within academic medical centers or dedicated research institutes)

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Director of Molecular Diagnostics / Pathology

30%

Head of R&D, Companion Diagnostics

25%

Chief Scientific Officer (CSO) / VP of Translational Medicine

25%

Laboratory Director / Manager

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Circulating Biomarker Assay Developers

30%

Specialized Diagnostic Laboratories/Hospitals

25%

Pharmaceutical & Biotechnology Companies

20%

Contract Research Organizations (CROs) & Research Centers

15%

Instrument Manufacturers

10%

Secondary Research & Industry Benchmarking

The remaining approximately 25% of our research methodology is dedicated to comprehensive secondary research. This initial phase serves to establish a foundational understanding of the market landscape, identify key market players, define segmentations, and gather preliminary data. Our secondary research rigorously avoids market research websites, prioritizing authoritative and verifiable sources to ensure data integrity. Key sources include:

Financial Databases: Bloomberg, Factiva, Hoovers, and PitchBook for company financials, investment trends, and competitive intelligence.

Government Publications: Official reports and data from health agencies, regulatory bodies, and statistical offices (e.g., National Cancer Institute - [NCI](https://www.cancer.gov/), Centers for Disease Control and Prevention - [CDC](https://www.cdc.gov/)).

Organizational and Trade Association Data: Publications, guidelines, and statistics from reputable industry bodies relevant to diagnostics, oncology, and laboratory standards. These include:

Clinical and Laboratory Standards Institute (CLSI) [CLSI](https://clsi.org/)

American Association for Cancer Research (AACR) [AACR](https://www.aacr.org/)

European Society for Medical Oncology (ESMO) [ESMO](https://www.esmo.org/)

U.S. Food and Drug Administration (FDA) [FDA](https://www.fda.gov/) for regulatory insights.

Company Filings: Annual reports, investor presentations, and corporate websites of public and private companies.

Academic and Scientific Journals: Peer-reviewed publications detailing advancements in circulating biomarker research, clinical utility, and technological innovations.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies integrate both top-down and bottom-up approaches, coupled with multi-level data triangulation to ensure robust estimates. The top-down approach involves estimating the total available market based on macroeconomic factors, disease prevalence, and overall healthcare expenditure, then segmenting it down to the specific circulating biomarker market. Conversely, the bottom-up approach aggregates data from individual market segments to build a holistic market size.

Key metrics and variables utilized for the bottom-up market sizing include:

Annual volume of circulating biomarker tests (e.g., circulating tumor DNA, circulating tumor cells) performed across various applications (hospitals, medical research centers, clinical labs) by region.

Average selling price (ASP) of circulating biomarker assays, kits, reagents, and associated analytical services.

Prevalence and incidence rates of diseases (particularly cancer and infectious diseases) where circulating biomarkers are clinically relevant, disaggregated by geographic region.

R&D expenditure by pharmaceutical and biotechnology companies specifically on circulating biomarker discovery, validation, and integration into precision medicine pipelines.

Market forecasts from 2026 to 2034 are developed using advanced statistical modeling techniques, considering factors such as technological advancements, regulatory landscape changes, reimbursement policies, competitive intensity, and the evolving clinical adoption rates of circulating biomarkers. Growth drivers, restraints, opportunities, and challenges are meticulously analyzed to project market trajectory across all defined segments.

Data Accuracy & Quality Check

We guarantee an estimated data accuracy level of 85-90% for our market reports. This high degree of accuracy is achieved through a rigorous, multi-stage data validation and quality check process. All quantitative data derived from secondary sources are cross-referenced with multiple independent sources and subsequently validated through primary interviews with industry experts. Qualitative insights gathered during primary research are cross-verified for consistency and representativeness.

An internal expert panel reviews all compiled data and analytical conclusions to identify and rectify any potential discrepancies or biases. Our commitment to delivering timely and relevant insights ensures that every report is updated up to the date of purchase, reflecting the latest market dynamics, technological breakthroughs, and regulatory shifts. This continuous monitoring and refinement process underpins the reliability and actionable nature of our market intelligence.

Frequently Asked Questions

1. How do sustainability and ESG factors influence the Circulating Biomarker market?

While direct environmental impact from manufacturing might be limited, ethical considerations in sample collection and data privacy are crucial. Sustainable lab practices, like waste reduction in hospitals and medical research centers, contribute to broader ESG goals. These practices ensure responsible development and deployment of diagnostic tools.

2. What are the primary export-import dynamics affecting the global Circulating Biomarker market?

The market sees significant international trade in diagnostic kits, reagents, and specialized equipment from leading manufacturers like Abbott Laboratories and Agilent Technologies. Developed regions often import advanced biomarker assays. R&D centers globally contribute to the demand for specialized components, driving cross-border scientific collaboration.

3. Which technological innovations are driving research and development in Circulating Biomarker diagnostics?

Innovations in liquid biopsy techniques, AI-driven data analysis, and highly sensitive detection methods are key. Companies such as Biocept and Fluxion Biosciences are advancing technologies for isolating and analyzing circulating tumor cells and cell-free DNA. These advancements enhance diagnostic accuracy and expand application scope.

4. How have post-pandemic recovery patterns influenced the Circulating Biomarker market's long-term shifts?

The pandemic highlighted the need for rapid, non-invasive diagnostics, accelerating investment in biomarker research and development. This shift has reinforced the market's projected CAGR of 4.6% from a 2025 base value of $5.17 billion. It also emphasizes decentralized testing and remote monitoring capabilities.

5. What end-user industries drive demand for Circulating Biomarker applications?

Key end-user industries include healthcare providers, specifically hospitals and medical research centers. Additionally, pharmaceutical companies utilize these biomarkers for drug development and companion diagnostics. Hospitals use circulating biomarkers for early disease detection and treatment monitoring, representing a significant application segment.

6. What are the key market segments and types within the Circulating Biomarker industry?

The Circulating Biomarker market segments by application include hospitals and medical research centers. By type, the primary segments are circulating DNA and circulating tumor cells. There is a significant focus on their use in cancer diagnostics, personalized medicine, and other disease monitoring.