Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Chemically Amplified Photoresists: $12.09B by 2025, 15.37% CAGR

Chemically Amplified Photoresists

Chemically Amplified Photoresists: $12.09B by 2025, 15.37% CAGR

Chemically Amplified Photoresists by Application (Semiconductor ICs, Advanced Packaging, MEMS, PCB, Others), by Types (Positive Photoresist, Negative Photoresist), by Technology (KrF, ArF Dry, ArF Immersion, EUV), by End User (Foundries, Integrated Device Manufacturers (IDMs), Research & Development Institutions, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 5, 2026|Base Year : 2025|Pages : 91

Key Insights for Chemically Amplified Photoresists Market

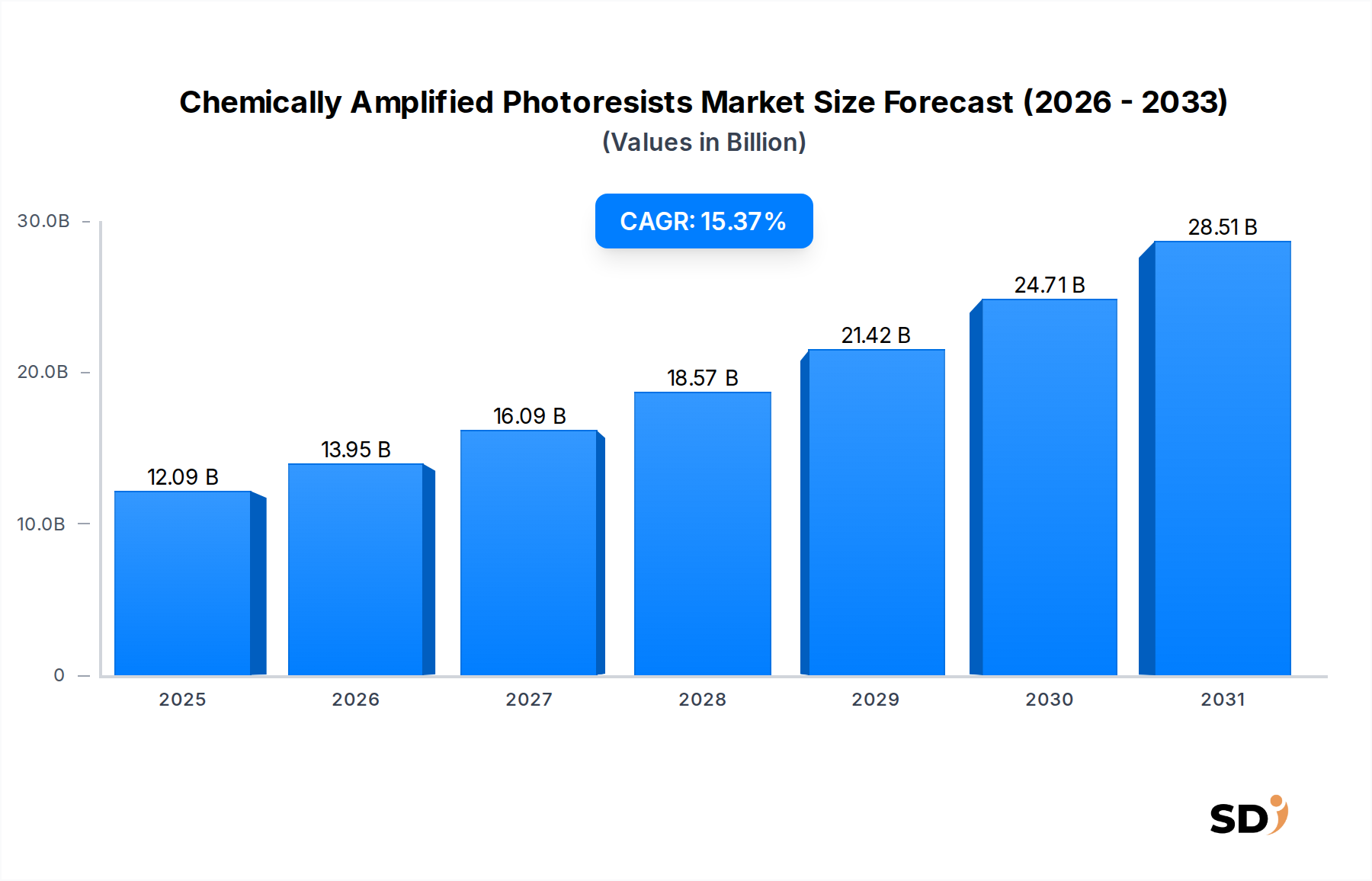

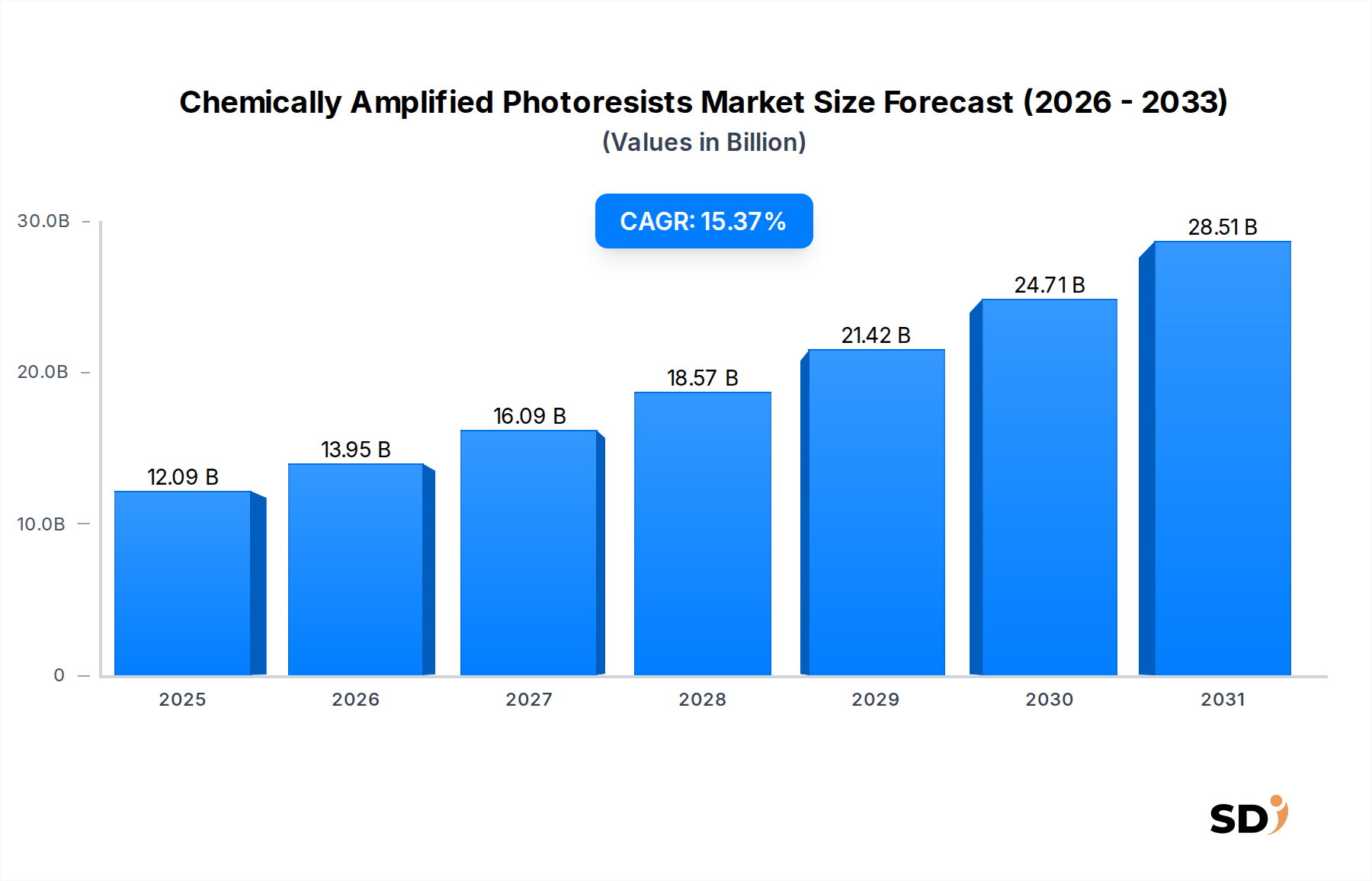

The global Chemically Amplified Photoresists Market was valued at an estimated $12.09 billion in 2025 and is projected to exhibit a robust Compound Annual Growth Rate (CAGR) of 15.37% over the forecast period. This significant expansion is primarily driven by the relentless pursuit of semiconductor miniaturization and the escalating demand for high-performance computing components across various end-use applications. Chemically amplified photoresists (CARs) are critical enablers for advanced lithography processes, particularly in the fabrication of integrated circuits (ICs) at sub-nanometer nodes. The underlying technology relies on a photoacid generator (PAG) to produce acid upon exposure to light, which then catalyzes a chemical reaction in the resist polymer, altering its solubility. This chemical amplification mechanism provides significantly higher sensitivity compared to conventional photoresists, making them indispensable for demanding deep ultraviolet (DUV) and extreme ultraviolet (EUV) lithography.

Chemically Amplified Photoresists Market Size (In Billion)

30.0B

20.0B

10.0B

0

12.09 B

2025

13.95 B

2026

16.09 B

2027

18.57 B

2028

21.42 B

2029

24.71 B

2030

28.51 B

2031

Key demand drivers include the pervasive integration of artificial intelligence (AI), the expansion of 5G infrastructure, and the proliferation of IoT devices, all of which necessitate more powerful and compact semiconductor chips. The increasing complexity of chip designs and the imperative for higher transistor density directly translate into an escalating requirement for advanced photoresist solutions capable of resolving ever-finer features. Furthermore, the growth in the Advanced Packaging Market is creating new avenues for CARs tailored for intricate 3D interconnects and wafer-level packaging. Regional dynamics indicate Asia Pacific's continued dominance, fueled by its robust semiconductor manufacturing ecosystem. Innovations in resist formulations, particularly for EUV Lithography Market applications, are pivotal for sustaining the market's growth trajectory. Strategic collaborations between material suppliers, equipment manufacturers, and foundries are vital to overcome technical challenges and accelerate the commercialization of next-generation photoresist materials. The broader Semiconductor Materials Market heavily relies on these innovations to maintain its growth momentum.

Dominant Technology Segment: ArF Immersion in Chemically Amplified Photoresists Market

The technology segmentation of the Chemically Amplified Photoresists Market reveals several critical categories, including KrF, ArF Dry, ArF Immersion, and EUV. While EUV technology represents the bleeding edge and holds significant promise for future growth, the ArF Immersion segment currently commands a substantial revenue share due to its established infrastructure, cost-effectiveness for volume production at sub-45nm nodes, and continued application in a wide array of advanced semiconductor manufacturing processes. ArF immersion photoresists are crucial for manufacturing ICs down to 28nm and often for critical layers even at 14nm and 7nm through multi-patterning techniques. The dominance of ArF Immersion stems from its capability to achieve high resolution and pattern fidelity by increasing the numerical aperture (NA) of the exposure system through the introduction of a liquid medium (typically deionized water) between the final lens element and the wafer. This effectively allows for the projection of smaller features than what is possible with dry lithography.

Major players in the Chemically Amplified Photoresists Market, such as JSR, TOK, Shin-Etsu Chemical, and Fujifilm, have heavily invested in and perfected their ArF immersion photoresist formulations. These companies continuously innovate to improve critical dimensions (CD) uniformity, line edge roughness (LER), and defectivity. Despite the increasing adoption of EUV for the most advanced nodes, ArF immersion remains economically viable and technologically sufficient for a vast segment of chip production, particularly for layers that do not demand the absolute highest resolution. Its well-understood process window, mature supply chain, and lower capital expenditure compared to EUV tools ensure its continued strong presence. However, the rapidly expanding EUV Lithography Market, driven by the shift to 5nm and 3nm nodes, is gradually eroding ArF immersion's long-term growth prospects, necessitating a strategic pivot for many photoresist suppliers. Nonetheless, for the foreseeable future, ArF immersion will continue to be a cornerstone technology within the Chemically Amplified Photoresists Market, supporting a broad spectrum of advanced semiconductor devices.

Key Market Drivers Fueling the Chemically Amplified Photoresists Market

The Chemically Amplified Photoresists Market is significantly propelled by several distinct, quantifiable drivers tied to the evolving landscape of microelectronics. Firstly, the unrelenting demand for increased computing power and data storage drives miniaturization. For instance, the transition to sub-7nm and sub-5nm manufacturing nodes by leading foundries necessitates advanced lithography techniques like ArF immersion multi-patterning and EUV. This directly translates to a greater reliance on high-performance CARs, with the global semiconductor capital equipment spending projected to exceed $100 billion in certain years, much of which is directed towards advanced lithography and associated materials. This investment underpins the need for high-resolution photoresists.

Secondly, the proliferation of emerging technologies such as Artificial Intelligence (AI), the Internet of Things (IoT), and 5G communications infrastructure dramatically increases the consumption of sophisticated integrated circuits. Each new generation of AI processors, 5G modems, and IoT chipsets requires higher transistor density and improved performance, achievable only through advanced patterning. For example, the number of connected IoT devices is expected to surpass 25 billion by 2030, driving persistent demand for specialized semiconductor components and, consequently, high-fidelity photoresists. This surge in device complexity and volume directly feeds into the Chemically Amplified Photoresists Market. Thirdly, significant government investments and incentives for domestic semiconductor manufacturing capabilities globally are stimulating the construction of new fabs and the upgrade of existing facilities. For instance, legislation like the CHIPS Act in the U.S. and similar initiatives in Europe and Asia are channeling billions of dollars into semiconductor fabrication, enhancing production capacity that directly consumes vast quantities of CARs. These strategic national investments bolster the overall demand for advanced materials within the Semiconductor Materials Market and the Lithography Equipment Market, reinforcing the growth trajectory of chemically amplified photoresists.

Competitive Ecosystem of Chemically Amplified Photoresists Market

The Chemically Amplified Photoresists Market is characterized by intense competition among a specialized group of global chemical manufacturers, with a strong emphasis on continuous innovation and intellectual property. Key players consistently invest in R&D to develop next-generation formulations for advanced lithography nodes.

TOK: A leading Japanese supplier of photoresists and other semiconductor materials, known for its extensive portfolio catering to DUV and EUV lithography, continuously advancing its resist technology to support cutting-edge chip manufacturing processes.

JSR: A prominent global player specializing in high-performance materials for the semiconductor industry, JSR is a key supplier of advanced photoresists for ArF immersion and EUV applications, focusing on innovation in material science.

Shin-Etsu Chemical: A diversified chemical company with a significant presence in silicon wafers and semiconductor materials, Shin-Etsu Chemical is a major supplier of high-purity photoresists, including chemically amplified types, critical for advanced node fabrication.

Fujifilm: With a strong heritage in imaging science, Fujifilm has leveraged its expertise to become a significant supplier of photoresists, particularly for DUV and EUV applications, emphasizing materials for finer resolution and higher throughput.

Sumitomo Chemical: A diversified Japanese chemical company providing a wide range of materials for various industries, Sumitomo Chemical offers critical photoresist materials and related chemicals for semiconductor manufacturing, focusing on advanced lithography solutions.

Dongjin Semichem: A South Korean chemical company recognized for its electronic materials, including photoresists, Dongjin Semichem serves the domestic and international semiconductor markets with a growing portfolio for advanced patterning technologies.

DuPont: A global science and innovation company, DuPont's Electronics & Industrial segment is a key supplier of advanced materials for the semiconductor industry, including a broad range of photoresists and ancillary materials critical for chip fabrication.

Brewer Science: Specializing in materials for microelectronics, Brewer Science is known for its advanced photoresist ancillary materials, such as anti-reflective coatings (ARCs) and temporary bond materials, which are integral to optimizing photoresist performance.

Inpria Corporation: A leader in metal oxide EUV photoresists, Inpria offers innovative solutions that promise higher resolution and better process control for the most demanding EUV lithography applications, representing a significant technological advancement.

Recent Developments & Milestones in Chemically Amplified Photoresists Market

January 2026: A leading photoresist manufacturer announced a significant breakthrough in its EUV photoresist formulation, achieving enhanced sensitivity and improved line-edge roughness (LER) for sub-3nm patterning, addressing critical challenges in advanced node fabrication.

March 2026: A strategic partnership was forged between a major semiconductor foundry and a specialty chemical provider to co-develop new CARs optimized for advanced packaging applications. This collaboration aims to enhance the performance and reliability of solutions for the Advanced Packaging Market.

June 2026: A key player in the Photoacid Generator Market unveiled a new generation of PAGs designed to offer higher photoefficiency and lower outgassing, thereby improving the overall performance and defectivity control of chemically amplified photoresists.

September 2026: An investment of $150 million was made by a consortium of venture capital firms into a startup focused on novel resist platforms, including chemically amplified approaches for next-generation lithography beyond EUV, signaling future directions for the Chemically Amplified Photoresists Market.

November 2026: A major producer of KrF photoresists announced capacity expansion plans in Southeast Asia, aimed at meeting the consistent demand for mature node manufacturing and certain MEMS applications, highlighting the continued relevance of established technologies.

February 2027: The introduction of new negative tone photoresist solutions specifically tailored for high-resolution grayscale lithography was announced, targeting applications in the MEMS and specialty sensor fabrication sectors.

Regional Market Breakdown for Chemically Amplified Photoresists Market

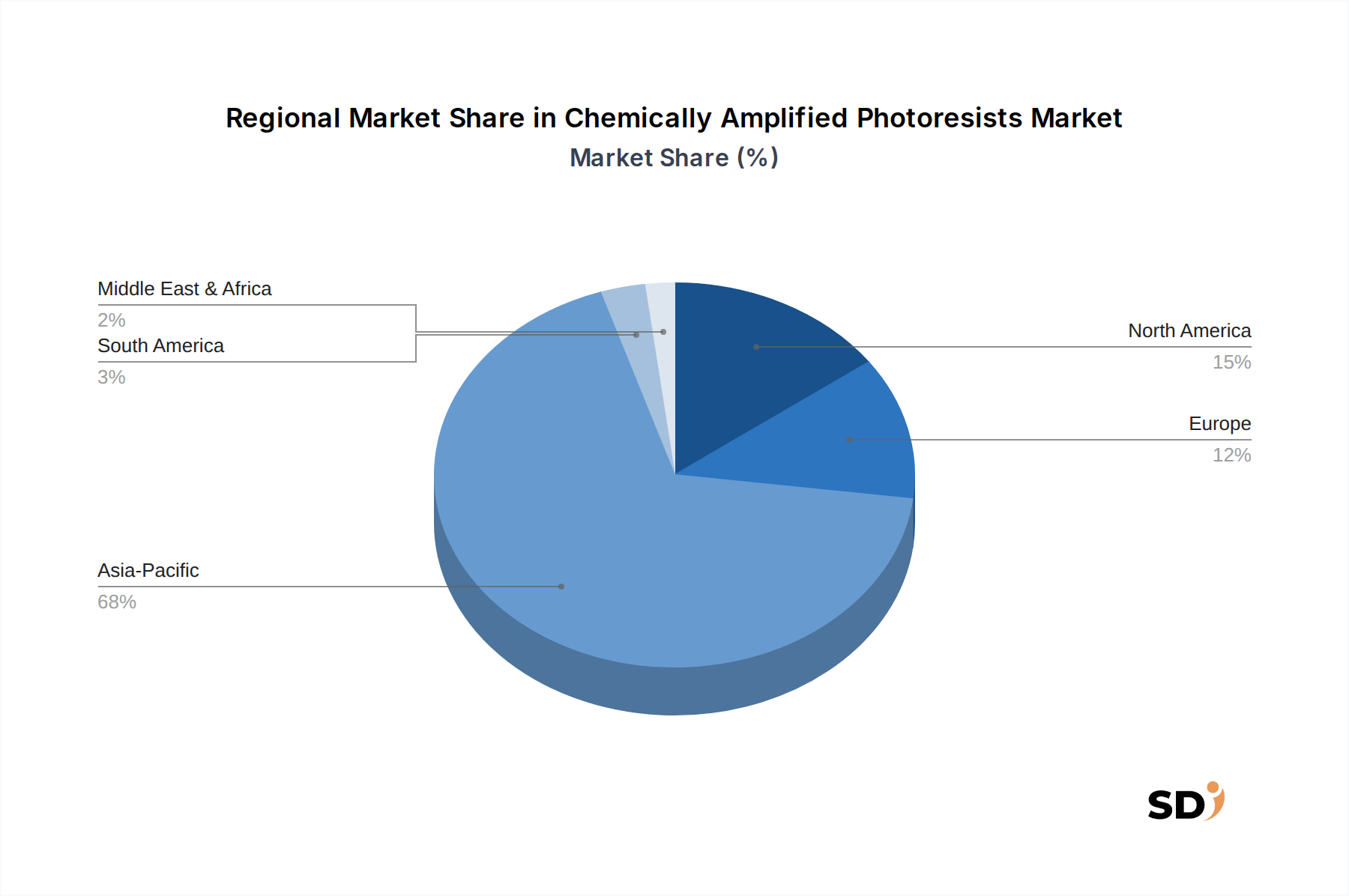

Asia Pacific dominates the global Chemically Amplified Photoresists Market, driven by its unparalleled concentration of semiconductor manufacturing facilities, including leading foundries, Integrated Device Manufacturers (IDMs), and outsourced semiconductor assembly and test (OSAT) companies. Countries like South Korea, Taiwan, Japan, and China are at the forefront of advanced chip production, necessitating a vast supply of high-performance photoresists for applications such as Semiconductor ICs Market. The region is projected to register the fastest CAGR of approximately 17.5%, fueled by ongoing investments in new fab construction and technological advancements, particularly in EUV and ArF immersion lithography. Asia Pacific currently accounts for over 70% of the global market revenue, with significant growth in the Printed Circuit Board Market also contributing to demand.

North America, including the United States and Canada, holds a significant share, driven by robust R&D activities, the presence of major IDMs, and government initiatives aimed at re-shoring semiconductor manufacturing. The region is expected to grow at a CAGR of around 13.8%, focusing on cutting-edge technologies and specialized applications. Europe, with countries like Germany, France, and the UK, also contributes to the Chemically Amplified Photoresists Market, primarily through specialized semiconductor manufacturing, automotive electronics, and a strong research base. The European market is anticipated to grow at a CAGR of approximately 12.5%, emphasizing niche applications and collaborative innovation within the broader Semiconductor Manufacturing Equipment Market.

The Middle East & Africa and South America regions currently hold smaller shares but are expected to witness gradual growth as local semiconductor ecosystems develop and industrialization efforts expand. While these regions may not lead in cutting-edge lithography, demand for less advanced photoresists for power devices and sensors is steadily increasing. Overall, the global landscape underscores the critical role of Asia Pacific as the primary growth engine and manufacturing hub for chemically amplified photoresists, with North America and Europe serving as crucial innovation and specialized production centers.

Investment & Funding Activity in Chemically Amplified Photoresists Market

The Chemically Amplified Photoresists Market has seen a concentrated influx of investment and funding activity, particularly over the past two to three years, driven by the strategic imperative to support next-generation semiconductor manufacturing. The primary beneficiaries of this capital inflow are companies developing advanced materials for EUV lithography and those focusing on specialized resists for advanced packaging. Venture capital firms and corporate investors are keen on startups innovating in novel polymer architectures, photoacid generator (PAG) chemistries, and post-processing solutions that enhance resist performance and defectivity control for the EUV Lithography Market. For instance, companies pioneering metal-containing photoresists, such as Inpria Corporation, have attracted significant funding rounds due to their potential to offer superior resolution and etch resistance compared to traditional organic resists for EUV.

Mergers and acquisitions, while less frequent due to the highly specialized and proprietary nature of photoresist formulations, often occur to consolidate R&D capabilities or expand market reach, particularly in regional markets or specific technology segments. Strategic partnerships between photoresist manufacturers and leading foundries or Lithography Equipment Market providers are commonplace, often involving joint development agreements to tailor resist materials for specific process nodes and equipment platforms. These partnerships are crucial for accelerating the commercialization of new materials and ensuring their compatibility with manufacturing environments. Furthermore, investments are increasingly being directed towards capacity expansion and supply chain resilience for critical raw materials, recognizing the strategic importance of photoresists in the broader Semiconductor Materials Market. This targeted funding ensures that the industry can meet the surging demand for advanced chips, especially in the context of global supply chain vulnerabilities.

Supply Chain & Raw Material Dynamics for Chemically Amplified Photoresists Market

The supply chain for the Chemically Amplified Photoresists Market is intricate and highly dependent on a specialized network of upstream material suppliers, posing inherent sourcing risks. Key raw materials include polymers (resins), photoacid generators (PAGs), dissolution inhibitors, and solvents. The synthesis of high-purity polymers, such as poly(hydroxystyrene) derivatives for DUV resists or specialized acrylic resins for EUV resists, requires stringent quality control and advanced chemical engineering capabilities, often sourced from a limited number of specialized chemical companies. The Photoacid Generator Market, for example, is a critical upstream segment, as PAGs are the active components enabling the chemical amplification mechanism. Any disruption in the supply of these highly specialized chemicals can have cascading effects throughout the semiconductor manufacturing process.

Price volatility of these key inputs, driven by factors such as global chemical market dynamics, geopolitical tensions, and environmental regulations affecting chemical production, directly impacts the cost structure of photoresist manufacturers. For instance, the cost of high-purity monomers or specialized catalysts can experience upward price trends due to constrained supply or increased demand from other high-tech sectors. Historically, supply chain disruptions, such as natural disasters, industrial accidents, or even trade disputes, have underscored the vulnerability of this market, leading to increased efforts by photoresist manufacturers and their customers (foundries) to diversify sourcing and build inventory buffers. The stringent purity requirements for all raw materials, often at parts-per-billion levels, add another layer of complexity and cost, as impurities can lead to defectivity in wafer processing. Ensuring a resilient and robust supply chain for these critical raw materials is paramount for the stable growth of the Chemically Amplified Photoresists Market and, by extension, the entire semiconductor industry.

Chemically Amplified Photoresists Segmentation

1. Application

1.1. Semiconductor ICs

1.2. Advanced Packaging

1.3. MEMS

1.4. PCB

1.5. Others

2. Types

2.1. Positive Photoresist

2.2. Negative Photoresist

3. Technology

3.1. KrF

3.2. ArF Dry

3.3. ArF Immersion

3.4. EUV

4. End User

4.1. Foundries

4.2. Integrated Device Manufacturers (IDMs)

4.3. Research & Development Institutions

4.4. Others

Chemically Amplified Photoresists Segmentation By Geography

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Semiconductor ICs

5.1.2. Advanced Packaging

5.1.3. MEMS

5.1.4. PCB

5.1.5. Others

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Positive Photoresist

5.2.2. Negative Photoresist

5.3. Market Analysis, Insights and Forecast - by Technology

5.3.1. KrF

5.3.2. ArF Dry

5.3.3. ArF Immersion

5.3.4. EUV

5.4. Market Analysis, Insights and Forecast - by End User

5.4.1. Foundries

5.4.2. Integrated Device Manufacturers (IDMs)

5.4.3. Research & Development Institutions

5.4.4. Others

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Semiconductor ICs

6.1.2. Advanced Packaging

6.1.3. MEMS

6.1.4. PCB

6.1.5. Others

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Positive Photoresist

6.2.2. Negative Photoresist

6.3. Market Analysis, Insights and Forecast - by Technology

6.3.1. KrF

6.3.2. ArF Dry

6.3.3. ArF Immersion

6.3.4. EUV

6.4. Market Analysis, Insights and Forecast - by End User

6.4.1. Foundries

6.4.2. Integrated Device Manufacturers (IDMs)

6.4.3. Research & Development Institutions

6.4.4. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Semiconductor ICs

7.1.2. Advanced Packaging

7.1.3. MEMS

7.1.4. PCB

7.1.5. Others

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Positive Photoresist

7.2.2. Negative Photoresist

7.3. Market Analysis, Insights and Forecast - by Technology

7.3.1. KrF

7.3.2. ArF Dry

7.3.3. ArF Immersion

7.3.4. EUV

7.4. Market Analysis, Insights and Forecast - by End User

7.4.1. Foundries

7.4.2. Integrated Device Manufacturers (IDMs)

7.4.3. Research & Development Institutions

7.4.4. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Semiconductor ICs

8.1.2. Advanced Packaging

8.1.3. MEMS

8.1.4. PCB

8.1.5. Others

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Positive Photoresist

8.2.2. Negative Photoresist

8.3. Market Analysis, Insights and Forecast - by Technology

8.3.1. KrF

8.3.2. ArF Dry

8.3.3. ArF Immersion

8.3.4. EUV

8.4. Market Analysis, Insights and Forecast - by End User

8.4.1. Foundries

8.4.2. Integrated Device Manufacturers (IDMs)

8.4.3. Research & Development Institutions

8.4.4. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Semiconductor ICs

9.1.2. Advanced Packaging

9.1.3. MEMS

9.1.4. PCB

9.1.5. Others

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Positive Photoresist

9.2.2. Negative Photoresist

9.3. Market Analysis, Insights and Forecast - by Technology

9.3.1. KrF

9.3.2. ArF Dry

9.3.3. ArF Immersion

9.3.4. EUV

9.4. Market Analysis, Insights and Forecast - by End User

9.4.1. Foundries

9.4.2. Integrated Device Manufacturers (IDMs)

9.4.3. Research & Development Institutions

9.4.4. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Semiconductor ICs

10.1.2. Advanced Packaging

10.1.3. MEMS

10.1.4. PCB

10.1.5. Others

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Positive Photoresist

10.2.2. Negative Photoresist

10.3. Market Analysis, Insights and Forecast - by Technology

10.3.1. KrF

10.3.2. ArF Dry

10.3.3. ArF Immersion

10.3.4. EUV

10.4. Market Analysis, Insights and Forecast - by End User

10.4.1. Foundries

10.4.2. Integrated Device Manufacturers (IDMs)

10.4.3. Research & Development Institutions

10.4.4. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. TOK

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. JSR

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Shin-Etsu Chemical

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Fujifilm

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Sumitomo Chemical

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Dongjin Semichem

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. DuPont

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Brewer Science

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Inpria Corporation

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Others

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (billion), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (billion), by Technology 2025 & 2033

Figure 7: Revenue Share (%), by Technology 2025 & 2033

Figure 8: Revenue (billion), by End User 2025 & 2033

Figure 9: Revenue Share (%), by End User 2025 & 2033

Figure 10: Revenue (billion), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (billion), by Application 2025 & 2033

Figure 13: Revenue Share (%), by Application 2025 & 2033

Figure 14: Revenue (billion), by Types 2025 & 2033

Figure 15: Revenue Share (%), by Types 2025 & 2033

Figure 16: Revenue (billion), by Technology 2025 & 2033

Figure 17: Revenue Share (%), by Technology 2025 & 2033

Figure 18: Revenue (billion), by End User 2025 & 2033

Figure 19: Revenue Share (%), by End User 2025 & 2033

Figure 20: Revenue (billion), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (billion), by Application 2025 & 2033

Figure 23: Revenue Share (%), by Application 2025 & 2033

Figure 24: Revenue (billion), by Types 2025 & 2033

Figure 25: Revenue Share (%), by Types 2025 & 2033

Figure 26: Revenue (billion), by Technology 2025 & 2033

Figure 27: Revenue Share (%), by Technology 2025 & 2033

Figure 28: Revenue (billion), by End User 2025 & 2033

Figure 29: Revenue Share (%), by End User 2025 & 2033

Figure 30: Revenue (billion), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (billion), by Application 2025 & 2033

Figure 33: Revenue Share (%), by Application 2025 & 2033

Figure 34: Revenue (billion), by Types 2025 & 2033

Figure 35: Revenue Share (%), by Types 2025 & 2033

Figure 36: Revenue (billion), by Technology 2025 & 2033

Figure 37: Revenue Share (%), by Technology 2025 & 2033

Figure 38: Revenue (billion), by End User 2025 & 2033

Figure 39: Revenue Share (%), by End User 2025 & 2033

Figure 40: Revenue (billion), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (billion), by Application 2025 & 2033

Figure 43: Revenue Share (%), by Application 2025 & 2033

Figure 44: Revenue (billion), by Types 2025 & 2033

Figure 45: Revenue Share (%), by Types 2025 & 2033

Figure 46: Revenue (billion), by Technology 2025 & 2033

Figure 47: Revenue Share (%), by Technology 2025 & 2033

Figure 48: Revenue (billion), by End User 2025 & 2033

Figure 49: Revenue Share (%), by End User 2025 & 2033

Figure 50: Revenue (billion), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Application 2020 & 2033

Table 2: Revenue billion Forecast, by Types 2020 & 2033

Table 3: Revenue billion Forecast, by Technology 2020 & 2033

Table 4: Revenue billion Forecast, by End User 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Revenue billion Forecast, by Application 2020 & 2033

Table 7: Revenue billion Forecast, by Types 2020 & 2033

Table 8: Revenue billion Forecast, by Technology 2020 & 2033

Table 9: Revenue billion Forecast, by End User 2020 & 2033

Table 10: Revenue billion Forecast, by Country 2020 & 2033

Table 11: Revenue (billion) Forecast, by Application 2020 & 2033

Table 12: Revenue (billion) Forecast, by Application 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue billion Forecast, by Application 2020 & 2033

Table 15: Revenue billion Forecast, by Types 2020 & 2033

Table 16: Revenue billion Forecast, by Technology 2020 & 2033

Table 17: Revenue billion Forecast, by End User 2020 & 2033

Table 18: Revenue billion Forecast, by Country 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Revenue (billion) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Revenue billion Forecast, by Application 2020 & 2033

Table 23: Revenue billion Forecast, by Types 2020 & 2033

Table 24: Revenue billion Forecast, by Technology 2020 & 2033

Table 25: Revenue billion Forecast, by End User 2020 & 2033

Table 26: Revenue billion Forecast, by Country 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue (billion) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Revenue (billion) Forecast, by Application 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue billion Forecast, by Application 2020 & 2033

Table 37: Revenue billion Forecast, by Types 2020 & 2033

Table 38: Revenue billion Forecast, by Technology 2020 & 2033

Table 39: Revenue billion Forecast, by End User 2020 & 2033

Table 40: Revenue billion Forecast, by Country 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue (billion) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Revenue (billion) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue billion Forecast, by Application 2020 & 2033

Table 48: Revenue billion Forecast, by Types 2020 & 2033

Table 49: Revenue billion Forecast, by Technology 2020 & 2033

Table 50: Revenue billion Forecast, by End User 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is foundational to achieving the market insights presented in this report, comprising approximately 75% of our overall research efforts. This intensive approach ensures the most current, specific, and nuanced data is captured directly from industry experts. Our global team of analysts conducts in-depth interviews, surveys, and discussions with key stakeholders across the value chain of the chemically amplified photoresists market. The primary research process is designed to validate secondary findings, gather proprietary data, and uncover emerging trends and perspectives that are not publicly available. This iterative process allows for real-time data refinement and ensures our analysis reflects the most accurate market conditions up to the date of report purchase.

Advanced Packaging Houses (e.g., ASE Technology Holding, Amkor Technology)

Specific Job Titles/Stakeholders Engaged:

Director of Lithography Engineering

Senior Materials Procurement Manager

R&D Lead (Photoresist Development)

Head of Semiconductor Process Technology

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Director of Lithography Engineering

35%

Senior Materials Procurement Manager

25%

R&D Lead (Photoresist Development)

25%

Head of Semiconductor Process Technology

15%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Semiconductor Foundries

30%

Photoresist Manufacturers

25%

Integrated Device Manufacturers (IDMs)

20%

Lithography Equipment Manufacturers

15%

Advanced Packaging Houses

10%

Secondary Research & Industry Benchmarking

Secondary research constitutes the remaining 25% of our methodology, serving as a critical initial phase to establish market landscape, identify key players, understand technological advancements, and gather preliminary data points. This stage involves an extensive review of various credible data sources, which are rigorously vetted for accuracy and relevance. Our analysts leverage a suite of reputable financial databases and official publications to ensure comprehensive coverage and robust validation of market hypotheses.

Government & Organizational Publications: Official reports and statistics from national government agencies (e.g., U.S. Department of Commerce, European Commission), international organizations, and academic institutions (.gov and .org domains). These provide macro-economic indicators, trade statistics, and regulatory frameworks impacting the semiconductor industry.

Trade Associations & Industry Bodies: Publications, annual reports, and technical papers from leading industry associations provide invaluable insights into market trends, technological roadmaps, and industry consensus. Examples include:

This secondary research forms the bedrock upon which our primary research efforts are built, providing the necessary context and background for productive expert interviews. We explicitly avoid using data from other market research websites to maintain the originality and integrity of our findings.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies employ a robust combination of top-down and bottom-up approaches, further reinforced by multi-level data triangulation. This ensures a comprehensive and cross-verified estimation of market value and volume.

Bottom-Up Approach: This method involves segmenting the market into its smallest constituent parts, estimating their individual sizes, and then aggregating them to derive the total market size. For chemically amplified photoresists, key variables used for bottom-up calculation include:

Wafer Production Volume (by technology and end-user): Estimating the number of wafers processed across different lithography technologies (KrF, ArF Dry, ArF Immersion, EUV) and by key end-users (Foundries, IDMs).

Average Selling Price (ASP) per kilogram/liter of Photoresist: Analyzing pricing variations across different photoresist types and grades.

Photoresist Consumption Rate per Wafer: Determining the typical amount of photoresist required for processing a single wafer, accounting for varying applications and process efficiencies.

Capital Expenditure on Lithography Equipment: Inferring future demand for advanced photoresists based on investments in new lithography tools, indicating expansion of production capacity.

Top-Down Approach: This methodology begins with a broader market estimate (e.g., global semiconductor materials market or overall lithography market) and then disaggregates it into specific segments (e.g., chemically amplified photoresists) based on market share and penetration rates. Macroeconomic factors, industry growth drivers, and technological shifts are crucial inputs in this approach.

Multi-Level Data Triangulation: All market figures derived from both top-down and bottom-up models are cross-referenced and validated with data obtained through primary interviews with industry experts. This triangulation process minimizes potential errors and biases, leading to highly reliable market estimations.

Data Accuracy & Quality Check

Maintaining the highest standards of data accuracy is paramount to our research integrity. We guarantee an estimated data accuracy level of 85-90% for all quantitative figures presented in this report. This high level of precision is achieved through:

Rigorous Validation: Every data point is subjected to multiple layers of validation, comparing findings from primary interviews with secondary research, and cross-referencing with internal proprietary databases.

Expert Panel Review: Our internal team of senior analysts and external subject matter experts review all final data and analysis to ensure logical consistency and industry alignment.

Continuous Updates: The market dynamics for chemically amplified photoresists are constantly evolving. Therefore, every report produced by our firm is meticulously updated up to the date of purchase, ensuring clients receive the most current and relevant market intelligence available.

Methodological Transparency: Our commitment to transparent methodologies allows clients to understand the rigorous processes undertaken to arrive at our conclusions, fostering trust and confidence in our market intelligence.

Frequently Asked Questions

1. What are the current pricing trends and cost structure dynamics in the Chemically Amplified Photoresists market?

Pricing in the Chemically Amplified Photoresists market is influenced by raw material costs, R&D investments in new technologies like EUV, and manufacturing efficiencies. The specialized nature of these materials for semiconductor fabrication contributes to premium pricing for high-performance variants. Cost structures reflect the intensive capital expenditure for production and quality control.

2. How has the Chemically Amplified Photoresists market recovered post-pandemic, and what are the long-term structural shifts?

The market experienced a robust recovery driven by increased demand for semiconductors powering digital transformation. Long-term structural shifts include accelerated adoption of advanced lithography technologies such as ArF Immersion and EUV, necessitating high-performance photoresists. This shift underpins the projected 15.37% CAGR.

3. What 'consumer behavior' shifts influence purchasing trends for Chemically Amplified Photoresists?

Purchasing trends for Chemically Amplified Photoresists are driven by end-users like Foundries and IDMs, who prioritize performance, yield, and reliability for critical applications such as semiconductor ICs. There is a growing demand for specialized products that enable smaller feature sizes and higher transistor density in advanced manufacturing processes.

4. Who are the leading companies and market share leaders in the Chemically Amplified Photoresists competitive landscape?

Key players dominating the Chemically Amplified Photoresists market include TOK, JSR, Shin-Etsu Chemical, Fujifilm, Sumitomo Chemical, and DuPont. These companies compete on product innovation, material performance, and global supply chain reliability in a concentrated market.

5. What sustainability and ESG factors are impacting the Chemically Amplified Photoresists industry?

The industry faces increasing pressure for greener chemical processes and waste reduction in semiconductor manufacturing. Companies are investing in R&D to develop environmentally benign photoresist formulations and more efficient usage methods. Compliance with global chemical regulations and reducing the environmental footprint are key ESG considerations.

6. What investment activity and venture capital interest are observed in the Chemically Amplified Photoresists sector?

Investment activity is primarily focused on internal R&D by major chemical and material science companies to develop next-generation photoresists for EUV and advanced packaging. While specific venture capital rounds are less common for these specialized materials, strategic investments by large manufacturers ensure supply chain resilience and technological leadership.