1. What are the primary application segments for CHDM?

CHDM finds applications in polyester resins, PETG production, coatings, and adhesives & sealants. It is also utilized in engineering plastics, with both fiber and resin grades available.

+1 2315155523

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

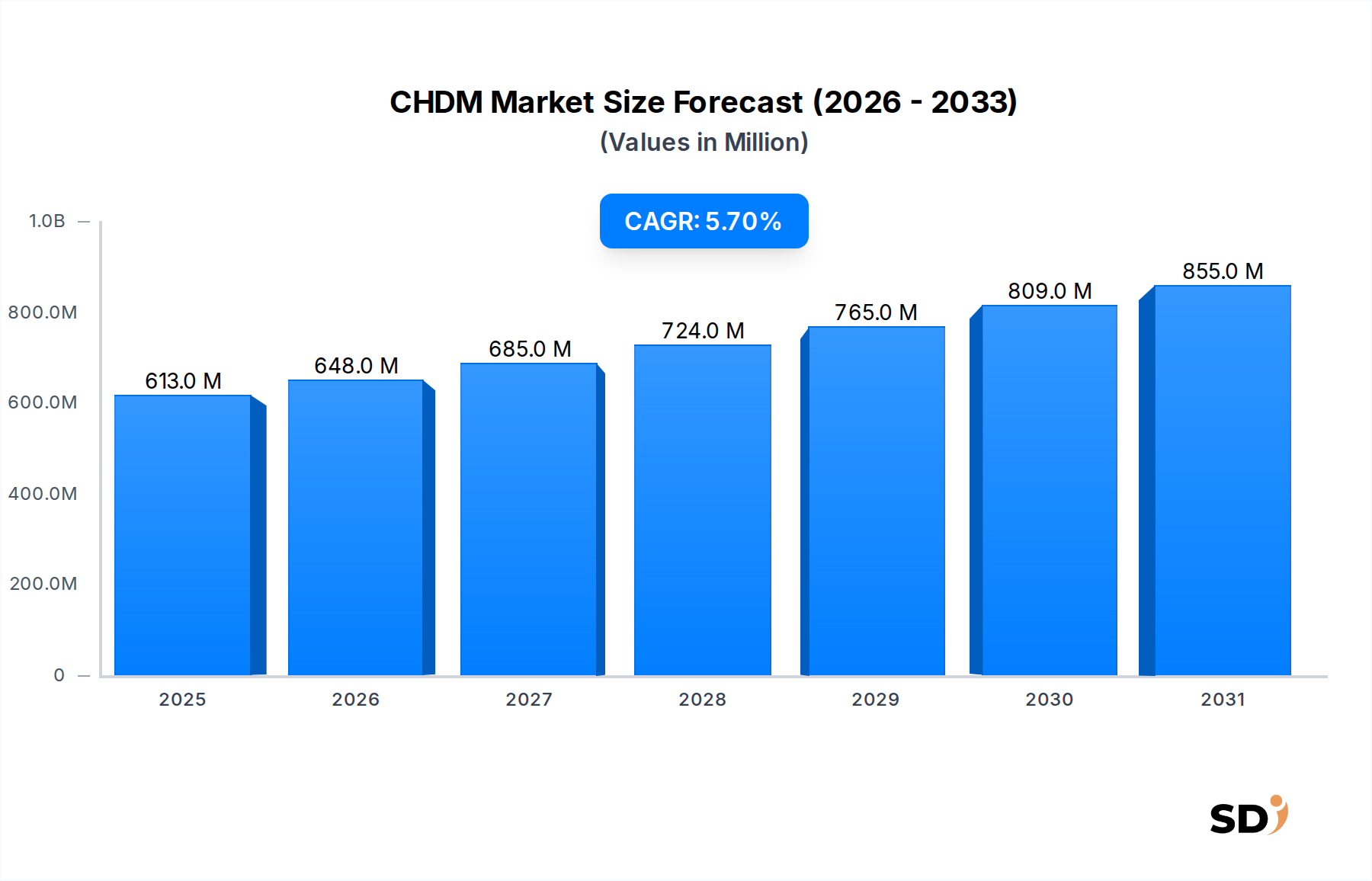

The global 1,4-Cyclohexanedimethanol (CHDM) Market is currently valued at an estimated $613 million as of 2023, demonstrating its critical role in the production of high-performance specialty polymers. This market is poised for robust expansion, projected to reach approximately $907.87 million by 2030, exhibiting a compound annual growth rate (CAGR) of 5.7% over the forecast period. This growth trajectory is primarily fueled by the escalating demand for advanced materials across a spectrum of industries, leveraging CHDM's unique properties to enhance product performance.

CHDM serves as a pivotal chemical intermediate, imparting superior clarity, chemical resistance, thermal stability, and mechanical strength to the polymers it modifies. A significant driver for the CHDM Market is its indispensable role in the production of copolyesters, particularly polyethylene terephthalate glycol-modified (PETG). The rapid expansion of the PETG Market, driven by its widespread adoption in clear packaging, medical devices, and display materials, directly translates to increased CHDM consumption. Furthermore, the robust growth in the Polyester Resins Market, where CHDM-modified polyesters are favored for their improved performance characteristics, continues to underpin market expansion. The versatility of CHDM also extends to the Specialty Coatings Market, where it contributes to the development of durable and weather-resistant formulations, and the Adhesives and Sealants Market, enhancing bond strength and flexibility.

Macroeconomic tailwinds such as rapid urbanization, increasing disposable incomes in emerging economies, and a global shift towards lightweighting in sectors like automotive and aerospace are significantly bolstering demand for high-performance Engineering Plastics Market, which frequently incorporate CHDM. Additionally, a growing emphasis on sustainability and circular economy principles is catalyzing research and development into bio-based CHDM alternatives, positioning the CHDM Market for long-term resilience and innovation. The demand for materials that offer both performance and aesthetic appeal in consumer goods and the Packaging Materials Market further solidifies CHDM's market position, ensuring its sustained growth in the foreseeable future.

The CHDM Market's landscape is significantly shaped by its application segments, with the Polyester Resins Market standing out as the unequivocal leader in terms of revenue share. This segment encompasses the use of CHDM as a key monomer in the synthesis of various high-performance copolyesters, including polyethylene terephthalate glycol-modified (PETG), polycyclohexylenedimethylene terephthalate (PCT), and modified polybutylene terephthalate (PBT). The dominance of the Polyester Resins Market stems from CHDM's exceptional ability to impart superior properties such as enhanced clarity, improved chemical and hydrolytic resistance, higher glass transition temperature, and better thermal stability compared to traditional diols like ethylene glycol (EG) or butanediol (BD).

Within the Polyester Resins Market, CHDM finds widespread application in the production of PETG, which is particularly favored for its excellent transparency, toughness, and ease of processing. The burgeoning demand for PETG across various end-use industries, including the Packaging Materials Market for bottles, sheets, and films, as well as in medical device components and point-of-sale displays, directly correlates with the CHDM market's expansion. The inherent advantages of CHDM-modified polyesters make them highly suitable for demanding applications, thereby solidifying this segment's leading position. Furthermore, the Fiber Grade CHDM Market, a sub-segment focused on polyester fiber production, benefits from CHDM's contribution to improved dyeability and elasticity of synthetic fibers, while the Resin Grade CHDM Market caters to molding and extrusion applications requiring enhanced material properties.

Key players in the broader Polymer Market, particularly those with strong capabilities in polyester synthesis like Eastman Chemical Company and SK Chemicals, are significant consumers of CHDM for their polyester resin portfolios. The growth in the Polyester Resins Market is not only driven by existing applications but also by continuous innovation, leading to new uses for CHDM-based copolyesters in areas requiring high performance and aesthetic appeal. The segment's share is expected to continue growing, albeit with potential shifts in specific application areas, as advancements in material science and increasing demand for sustainable solutions influence product development. The integration of CHDM allows polyester producers to offer premium products that meet the stringent requirements of modern industries, from advanced composites to high-clarity films, thereby reinforcing the segment's stronghold in the CHDM Market.

The CHDM Market's growth trajectory is profoundly influenced by a complex interplay of demand-side drivers and supply-side constraints, necessitating a data-centric analysis. A primary driver is the accelerating demand from the PETG Market, which has seen significant expansion due to its superior properties over conventional plastics. The global PETG production capacity has consistently expanded, driven by its adoption in clear rigid packaging, medical applications, and consumer electronics, where CHDM is a critical building block for transparency and impact resistance. This translates directly to increased CHDM consumption.

Another significant impetus comes from the growing adoption of high-performance copolyesters in the Automotive and Electrical & Electronics end-use industries. As manufacturers prioritize lightweighting initiatives to improve fuel efficiency and reduce emissions, and seek materials with enhanced thermal stability and electrical insulation for advanced electronics, CHDM-modified Engineering Plastics Market formulations are increasingly preferred. For instance, the use of CHDM-based polyesters in interior components, connectors, and casings ensures durability and compliance with stringent industry standards.

Furthermore, the robust expansion of the Specialty Coatings Market fuels CHDM demand. CHDM contributes to the formulation of highly durable, weather-resistant, and chemically inert coatings for industrial, automotive refinish, and architectural applications. The demand for such coatings, driven by infrastructure development and stringent performance requirements, particularly in corrosion protection and UV resistance, directly impacts the CHDM Market.

Conversely, the CHDM Market faces several constraints. Volatility in raw material prices, particularly cyclohexane (a key precursor), poses a significant challenge. Fluctuations in crude oil prices directly impact petrochemical derivatives, leading to unpredictable production costs for CHDM manufacturers. This price instability can affect profit margins and investment decisions. Additionally, competition from alternative diols such as Neopentyl Glycol (NPG), Hexanediol (HDO), and Ethylene Glycol (EG) presents a competitive constraint. While CHDM offers unique performance benefits, the cost-effectiveness of these alternatives in certain applications can limit CHDM's market penetration. Lastly, environmental regulations and sustainability pressures are emerging constraints. The industry faces increasing scrutiny regarding the lifecycle impact of petrochemical-derived chemicals, prompting R&D into bio-based alternatives, which, while promising, are currently at a higher production cost and lower scale, thus potentially constraining growth for conventional CHDM in the short term.

The global CHDM Market is characterized by the presence of a few dominant global players and a growing number of regional manufacturers, especially in Asia Pacific. The competitive landscape is shaped by product innovation, strategic partnerships, and capacity expansions aimed at meeting the diverse demands of end-use industries such as the Polyester Resins Market and the Engineering Plastics Market.

Recent strategic activities and technological advancements underscore the dynamic nature of the CHDM Market, driven by innovation and expanding application needs. These developments often reflect efforts to enhance production efficiency, expand capacity, or explore new sustainable pathways.

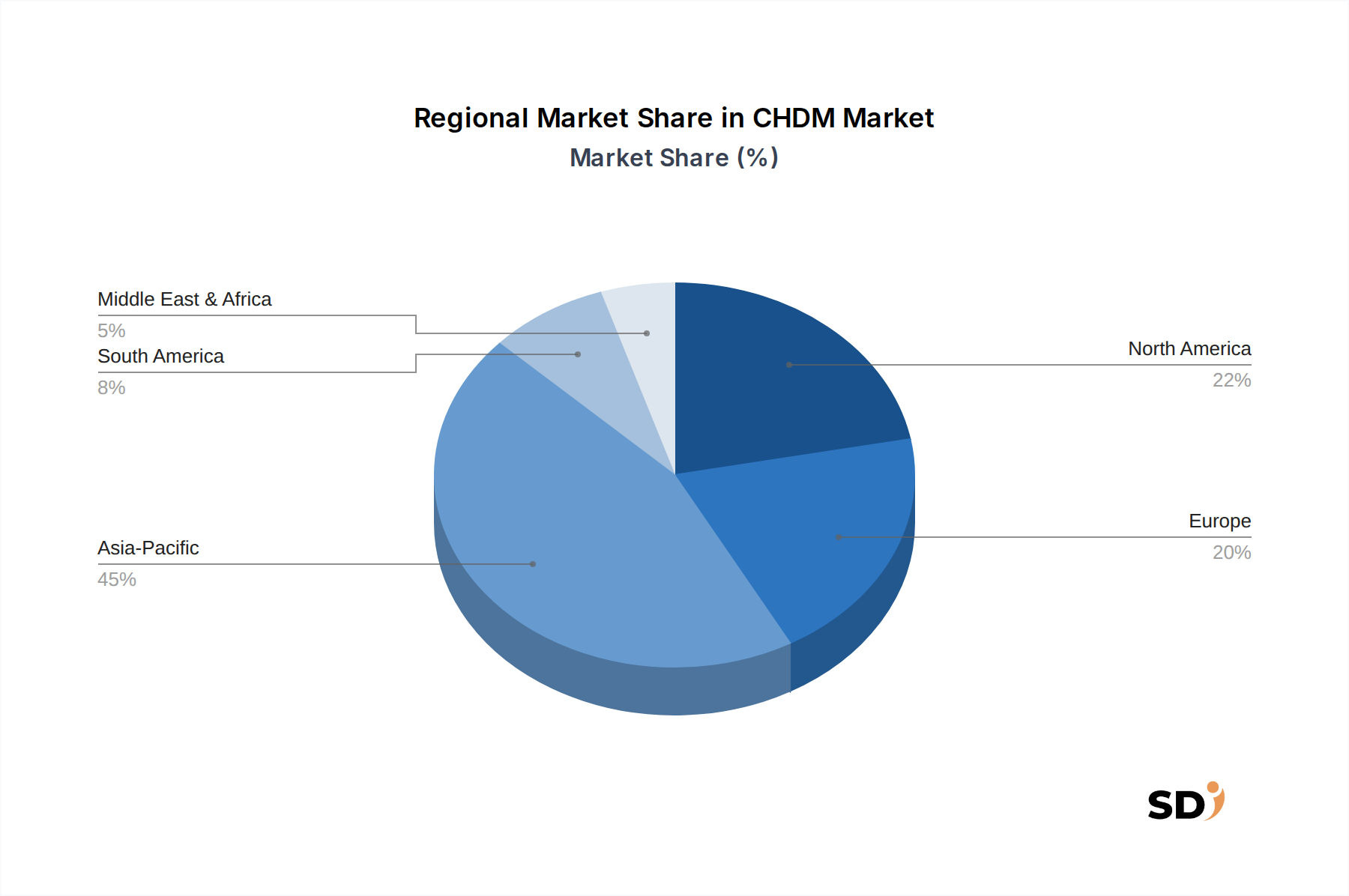

Geographic dynamics play a crucial role in shaping the CHDM Market, with distinct growth patterns and demand drivers observed across key regions. The global CHDM Market is segmented into North America, Europe, Asia Pacific, South America, and Middle East & Africa, each contributing uniquely to the overall market valuation of $613 million in 2023.

Asia Pacific is anticipated to hold the largest market share and emerge as the fastest-growing region in the CHDM Market, projected to exhibit a CAGR exceeding 6.5%. This robust growth is primarily attributable to the rapid industrialization, burgeoning manufacturing sectors, and increasing demand from end-use industries like packaging, automotive, and construction in countries such as China, India, Japan, and South Korea. The region's significant production capacity for Polyester Resins Market and Engineering Plastics Market, coupled with expanding consumer goods and the Packaging Materials Market, underpins its dominant position.

North America represents a mature yet steadily growing market for CHDM, with an estimated CAGR of around 4.8%. The demand here is largely driven by the adoption of high-performance materials in specialized applications, including automotive interiors, medical devices, and advanced coatings. Stringent regulatory frameworks for product quality and sustainability also spur innovation in CHDM-based formulations, particularly for the Adhesives and Sealants Market and Specialty Coatings Market.

Europe follows a similar growth trajectory to North America, with an anticipated CAGR of approximately 4.5%. The region benefits from a strong focus on innovation, sustainable product development, and the high-value specialty chemical sector. Demand is robust in the automotive, Building and Construction Chemicals Market, and electrical & electronics industries, where CHDM contributes to enhanced material properties and longevity. Emphasis on circular economy principles is also promoting research into bio-based CHDM.

Middle East & Africa and South America are emerging markets, characterized by infrastructure development and industrial expansion. While starting from a smaller base, these regions are expected to demonstrate moderate growth, with CAGRs in the range of 3.5% to 4.0%. The demand in these regions is primarily driven by local manufacturing growth in packaging, construction, and nascent automotive industries, along with a growing Chemical Intermediates Market.

The CHDM Market is undergoing a transformation driven by sustained R&D investments and an emphasis on sustainability, shaping its future technology innovation trajectory. Two to three disruptive emerging technologies are poised to redefine production methods and application scope.

Foremost among these is the development of Bio-based CHDM. Currently, CHDM is predominantly produced from petrochemical feedstocks. However, significant research is underway to synthesize CHDM from renewable resources such as biomass-derived sugars or other bio-alcohols. Companies and research institutions are actively exploring enzymatic and catalytic conversion routes. While still in its nascent stages, bio-based CHDM holds immense promise for reducing the carbon footprint of the CHDM Market and aligning with global sustainability goals. Adoption timelines are expected to be in the mid- to long-term (5-10 years), pending cost-effective scaling and process optimization. This innovation directly threatens incumbent petrochemical-based business models by offering a greener alternative, particularly appealing to brands committed to sustainable sourcing for the Polyester Resins Market and Packaging Materials Market.

Another critical area of innovation involves Advanced Catalysis and Process Intensification in conventional CHDM synthesis. Manufacturers are investing in developing more efficient catalysts and optimizing reaction conditions to improve yield, reduce energy consumption, and minimize waste generation. Technologies like continuous flow reactors and microreactor technology are being explored to enhance throughput and safety. These innovations, with shorter adoption timelines (2-5 years), primarily reinforce incumbent business models by making existing production methods more competitive and environmentally friendly, thus lowering operational costs and improving overall efficiency within the Chemical Intermediates Market.

Finally, Tailored CHDM Derivatives and Co-monomer Systems represent a key innovation trajectory. Research focuses on creating new CHDM derivatives or optimizing its use in conjunction with other monomers to impart very specific, high-performance characteristics to polymers. This includes developing CHDM variants for extreme temperature resistance, enhanced optical clarity, or superior barrier properties for the Engineering Plastics Market and Specialty Coatings Market. This area involves significant R&D investment and typically has a mid-term adoption timeline (3-7 years), primarily reinforcing incumbent models by enabling them to offer higher-value, specialized products that command premium pricing, expanding the utility of CHDM across niche and high-performance applications within the broader Polymer Market.

The global CHDM Market is intricately linked to international trade flows, with significant cross-border movement of both the intermediate chemical and the downstream products it enables. Major trade corridors for CHDM typically extend from key production hubs in Asia Pacific to demand centers in North America and Europe, reflecting the globalized nature of the Chemical Intermediates Market.

Leading exporting nations primarily include China, South Korea, and the United States, which possess substantial petrochemical production capacities and advanced manufacturing infrastructure. These countries produce CHDM for both domestic consumption and export to regions with high demand but limited indigenous production. Conversely, leading importing nations encompass a wide array of economies in Europe (e.g., Germany, France) and North America (e.g., Canada, Mexico), as well as developing markets in Southeast Asia and Latin America, where the demand for CHDM in applications such as the Polyester Resins Market, PETG Market, and Specialty Coatings Market outstrips local supply.

Recent years have seen a noticeable impact from trade policies and tariff adjustments. For instance, the US-China trade tensions have occasionally led to the imposition of tariffs on various chemical products, including some intermediates that could affect CHDM supply chains or raise costs for end-users. While direct tariffs specifically on CHDM may vary, indirect impacts through tariffs on related petrochemicals or downstream products can influence trade volumes and pricing. For example, increased tariffs on certain plastic products entering the U.S. from China could prompt a reallocation of CHDM supplies or a shift in manufacturing locations for products incorporating CHDM.

Furthermore, non-tariff barriers, such as stricter environmental regulations and complex import/export procedures in regions like the European Union, can also impact trade flows. The EU's REACH regulations (Registration, Evaluation, Authorization and Restriction of Chemicals) require extensive documentation and compliance for chemical imports, potentially increasing the administrative burden and cost for non-EU CHDM producers. Quantitatively, while precise real-time data on tariff-specific impacts on CHDM volume is proprietary, general industry assessments indicate that trade barriers can elevate import costs by 5% to 15%, leading to localized price increases and potentially encouraging regional sourcing over global supply chains. This has occasionally led to a modest shift in import patterns, favoring suppliers from non-tariff-affected nations and influencing the overall competitiveness within the global Polymer Market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Our primary research methodology is rigorously structured, forming the cornerstone of our market intelligence. This phase accounts for 70-80% of our total research effort, ensuring a profound understanding of market dynamics directly from industry participants. We conduct extensive qualitative and quantitative interviews with a diverse group of stakeholders across the value chain. Key objectives include validating secondary findings, obtaining granular data on market trends, competitive landscape, pricing strategies, technological advancements, and regulatory impacts specific to the CHDM market.

Our interview strategy targets highly specific company types:

Interviews are conducted with senior professionals holding critical roles, such as:

| Stakeholder Role | Interview Share (%) |

|---|---|

| VP of R&D, Polymer Materials | 30% |

| Head of Procurement, Specialty Chemicals | 25% |

| Product Manager, Performance Polymers | 25% |

| Director of Market Development, Industrial Coatings | 20% |

| Company Type | Representation (%) |

|---|---|

| Specialty Chemical Manufacturers | 30% |

| Polyester Resin/Polymer Producers | 25% |

| PETG Film & Sheet Manufacturers | 15% |

| Chemical Distributors & Traders | 15% |

| Advanced Material Compounders | 15% |

The secondary research phase complements our primary efforts, accounting for 20-30% of the total research. This phase involves a comprehensive review of existing literature, company reports, and industry publications to establish a foundational understanding of the CHDM market. Our robust data mining process leverages several proprietary and public databases. We meticulously extract financial data, market statistics, technological trends, and strategic developments.

Sources utilized include:

Our market estimation methodology employs a robust combination of top-down and bottom-up approaches, triangulated across multiple levels of data to ensure accuracy and consistency.

The bottom-up approach focuses on aggregating granular data points to build the total market size. For the CHDM market, this involves analyzing specific metrics or variables such as:

The top-down approach begins with broader macroeconomic indicators and industry-wide statistics, systematically segmenting down to the specific CHDM market. This involves analyzing overall chemical industry growth, polymer demand trends, and specific application market sizes (e.g., global coatings market size, engineering plastics market size), and then calculating CHDM's share within these.

All data points are cross-referenced and validated through multi-level data triangulation, comparing primary insights with secondary data and expert opinions. This iterative process helps in refining initial estimates and ensuring a holistic view of the market.

Our commitment to data integrity ensures an estimated data accuracy level of 85-90% for all market figures. Every data point and market projection undergoes rigorous validation through a multi-stage quality assurance process. This includes:

CHDM finds applications in polyester resins, PETG production, coatings, and adhesives & sealants. It is also utilized in engineering plastics, with both fiber and resin grades available.

The CHDM market features players such as Eastman Chemical Company, SK Chemicals, and Kangheng Chemical. These companies contribute to product innovation and market supply across different purity grades, including those above 99%.

Key end-use industries include packaging, building & construction, automotive, and electrical & electronics. Consumer goods also represent a significant segment, driving downstream demand for CHDM-derived products.

Purchasing trends in end-use sectors like packaging and automotive dictate demand for CHDM-based materials. The preference for high-performance resins and coatings influences product specifications and market volumes.

Challenges in the CHDM supply chain often relate to raw material price fluctuations and securing consistent feedstock. Maintaining purity standards, especially for grades above 99%, also presents operational considerations for manufacturers.

The CHDM market is experiencing growth due to increasing demand for polyester resins and PETG production. Expanding applications in packaging, coatings, and engineering plastics further contribute to the observed 5.7% CAGR.