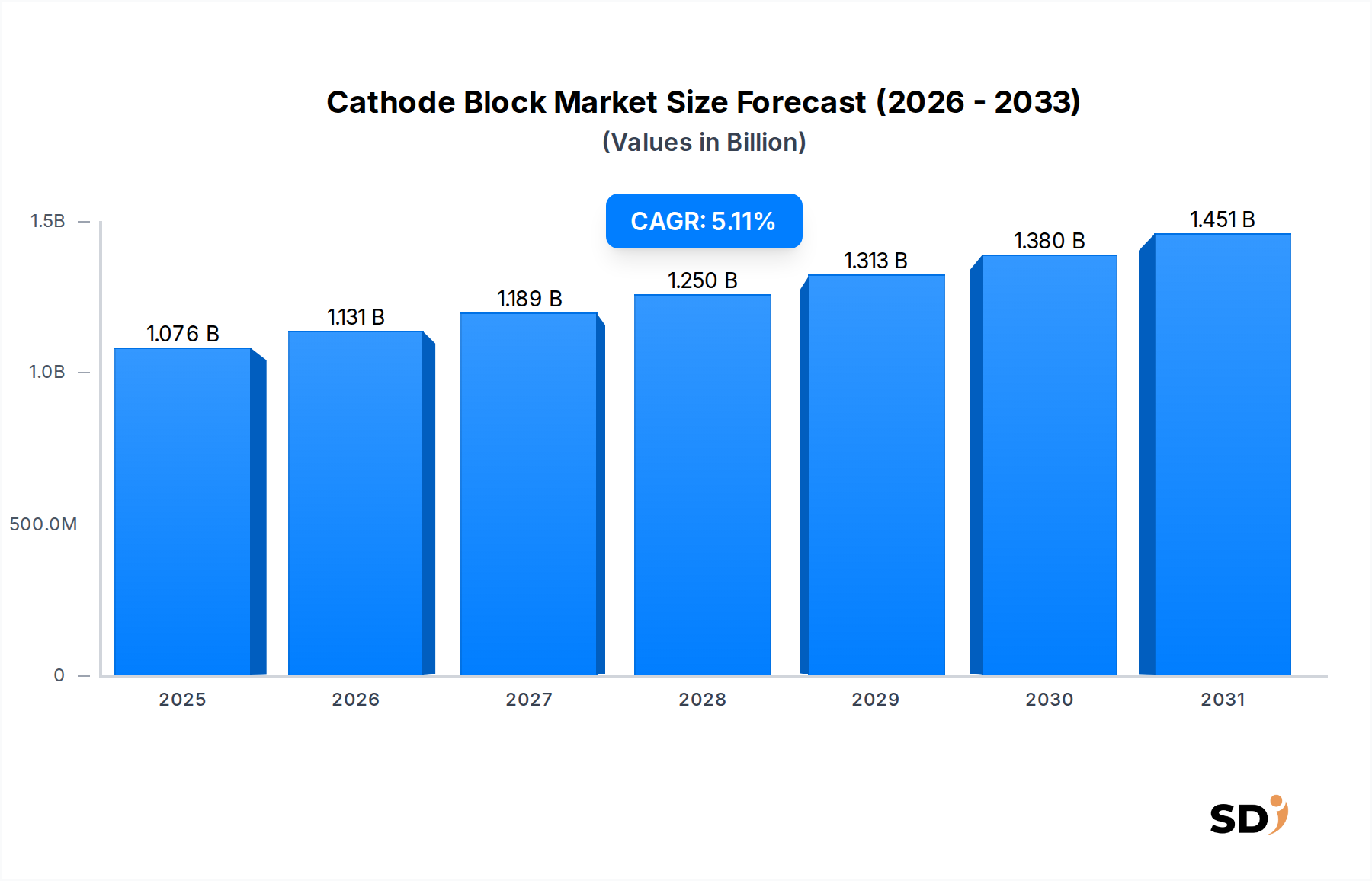

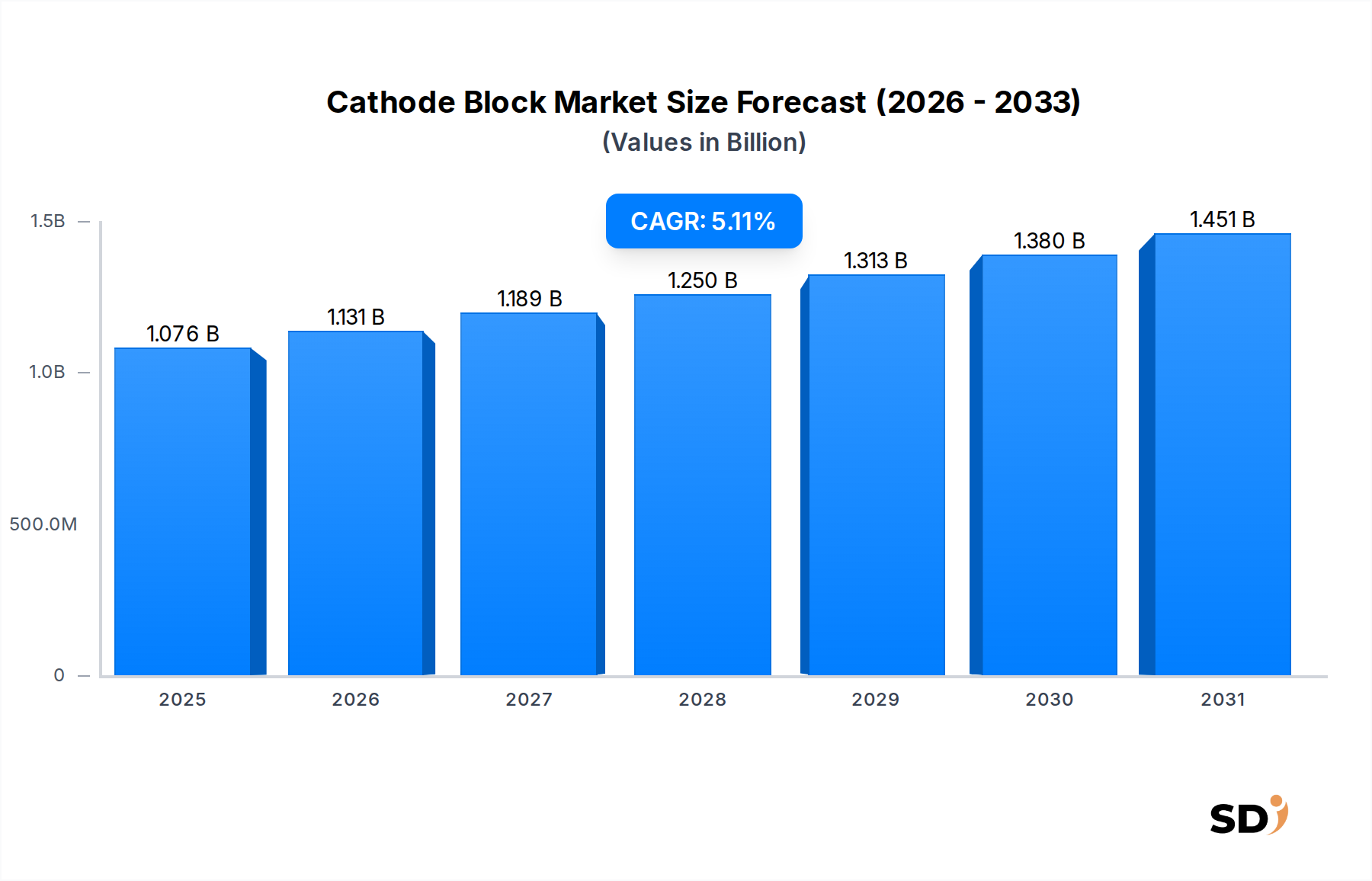

Regulatory & Policy Landscape Shaping Cathode Block Market

The Cathode Block Market is increasingly shaped by a complex web of environmental, energy, and trade regulations across key geographies. These policies directly influence production processes, raw material sourcing, and end-user demand, driving innovation towards more sustainable and efficient solutions.

Environmental Regulations: Stringent environmental protection laws are a primary driver of change. Policies targeting industrial emissions, particularly sulfur dioxide (SO2), nitrogen oxides (NOx), and particulate matter, impact raw material processing (e.g., petcoke calcination) and cathode block manufacturing. Regulations like the European Union's Industrial Emissions Directive (IED) or the US Clean Air Act necessitate significant investments in pollution control technologies for carbon product manufacturers. Furthermore, policies aimed at reducing carbon emissions from energy-intensive industries, such as carbon pricing schemes or emission trading systems (ETS), place economic pressure on aluminum smelters to adopt more energy-efficient technologies, including advanced cathode blocks. This indirectly favors blocks that contribute to lower energy consumption per ton of aluminum.

Chemical and Material Safety Regulations: Regulations concerning hazardous substances, such as those governing polycyclic aromatic hydrocarbons (PAHs) present in coal tar pitch (e.g., REACH in Europe), influence the selection and handling of binder materials. This drives research into low-PAH or PAH-free alternatives, impacting product formulation and manufacturing processes for cathode blocks. Compliance with these regulations adds to operational costs but also enhances worker safety and environmental stewardship.

Energy Efficiency Mandates: Government policies and industry standards promoting energy efficiency in heavy industries, particularly for Aluminum Smelting Market operations, directly impact the demand for high-performance cathode blocks. Incentives or mandates for smelters to reduce specific energy consumption encourage investment in electrolytic cells equipped with optimized cathode designs offering lower electrical resistivity and longer pot life. This aligns with global targets for industrial decarbonization and energy security.

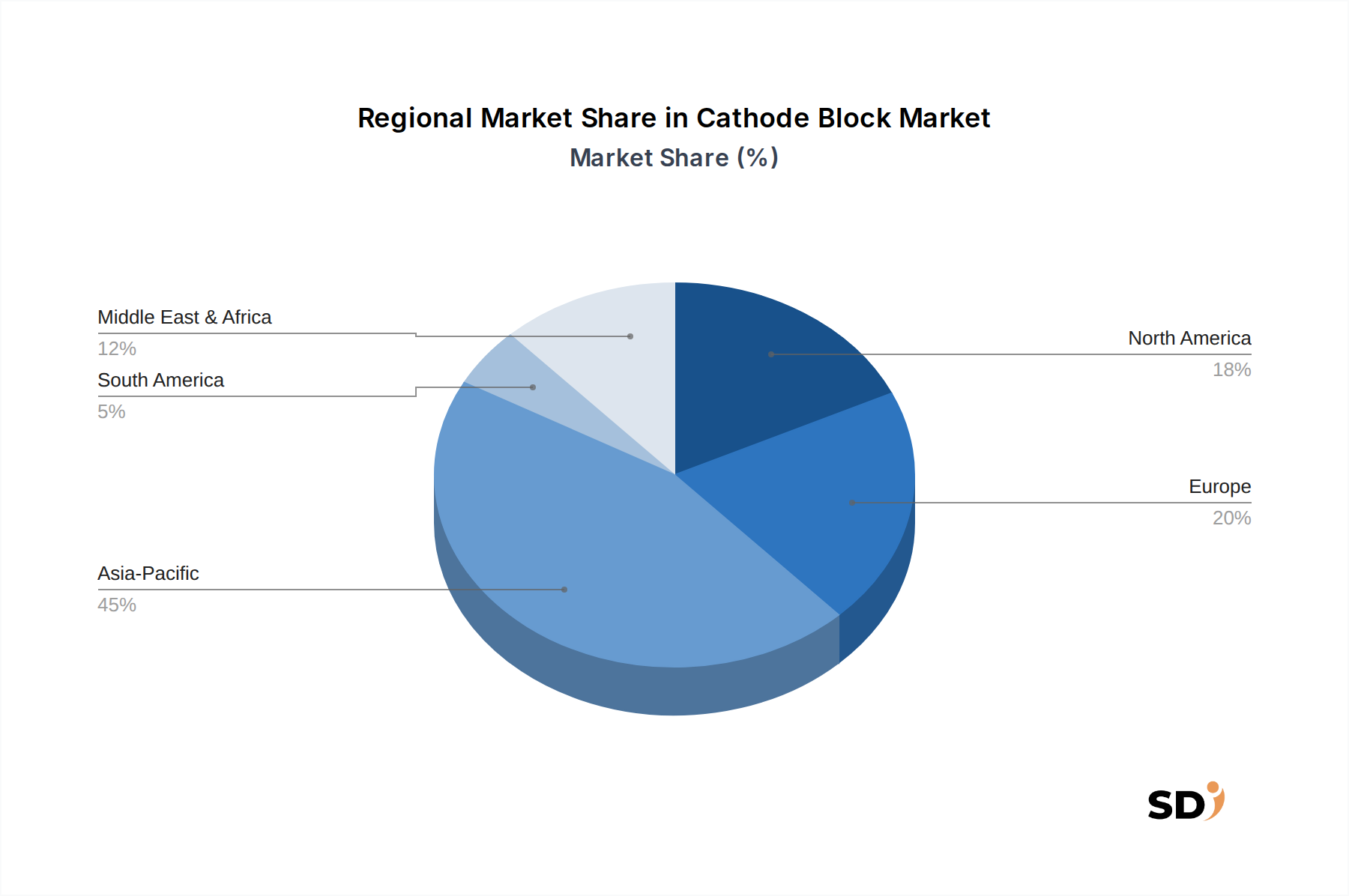

Trade Policies and Tariffs: Global trade policies, including tariffs on raw materials (like Petroleum Coke Market or Needle Coke Market) or finished carbon products, can significantly alter the competitive landscape and supply chain economics of the Cathode Block Market. Protectionist measures or anti-dumping duties can increase the cost of imports, favoring domestic production but potentially limiting material diversity or driving up prices for end-users. Conversely, free trade agreements can facilitate the flow of raw materials and finished products, impacting pricing and market access.

Recent Policy Changes and Impact: Recent years have seen an acceleration in green industrial policies, particularly in Europe and Asia, pushing for cleaner production and circular economy principles. This includes initiatives for industrial symbiosis, where byproducts from one industry (e.g., spent cathode blocks) can be processed for reuse or recycling. While full-scale recycling of spent cathode blocks faces technical challenges due to hazardous components, policies encouraging material recovery are stimulating R&D in this area, which could, in the long term, alter the raw material dependency of the Cathode Block Market and contribute to the broader Carbon Materials Market sustainability.