Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Carbon Negative Cement Market: Trends & 2034 Growth Outlook

Carbon Negative Cement

Carbon Negative Cement Market: Trends & 2034 Growth Outlook

Carbon Negative Cement by Product Type (Carbon Mineralized Cement, Magnesium-Based Carbon Negative Cement, Geopolymer Carbon Negative Cement, Bio-Based Carbon Negative Cement, Others), by Technology Type (Carbon Capture and Utilization (CCU) Cement, Carbon Mineralization Technology, Carbon Injection/Curing Technology, Geopolymer Technology, Magnesium Oxide (MgO)-Based Technology, Alkali-Activated Materials (AAM) Technology, Others), by Cement Form (Ready-Mix Cement, Dry Cement Mix, Others), by Application (Residential, Commercial, Industrial), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 5, 2026|Base Year : 2025|Pages : 133

Key Insights into the Carbon Negative Cement Market

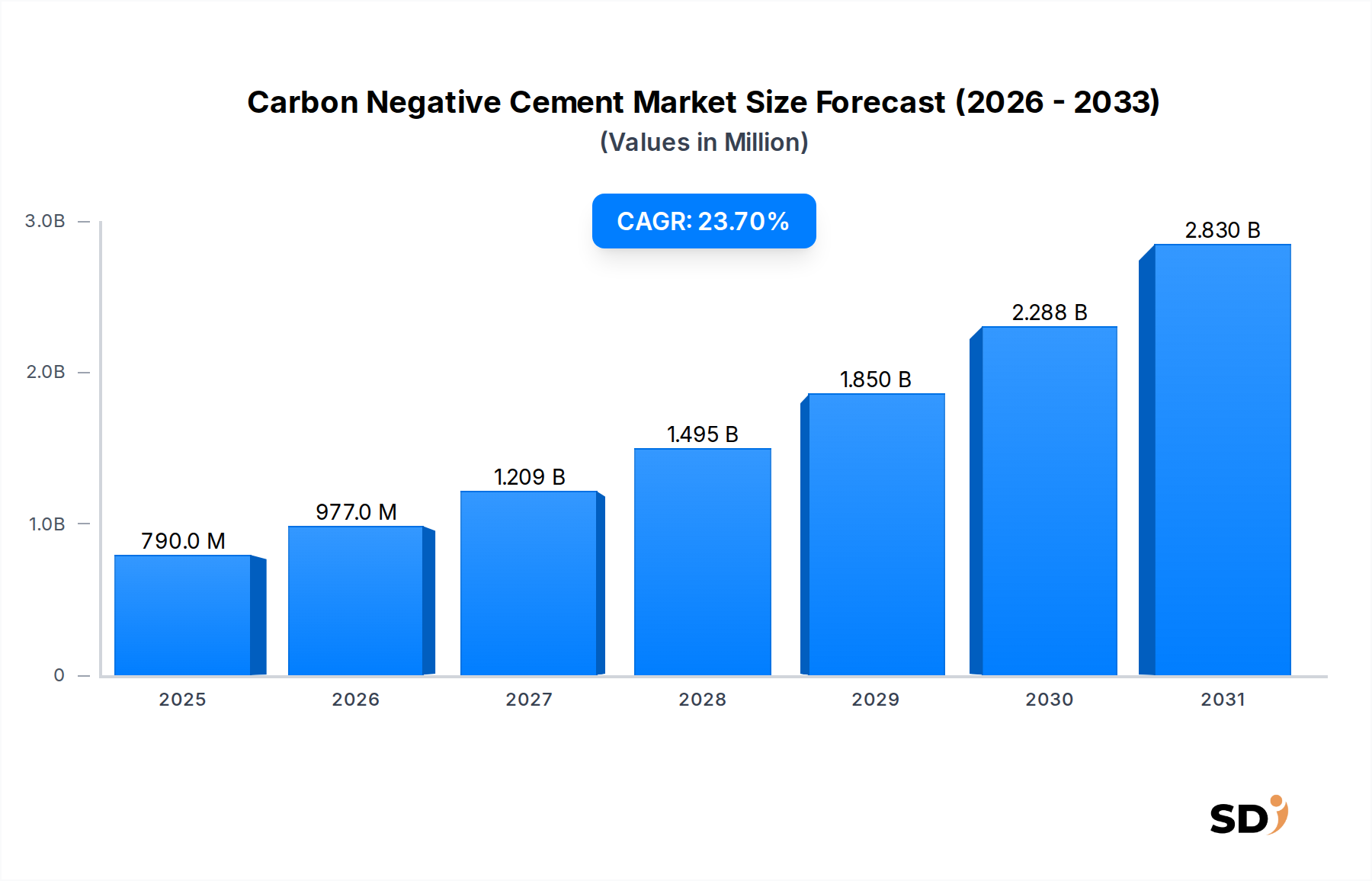

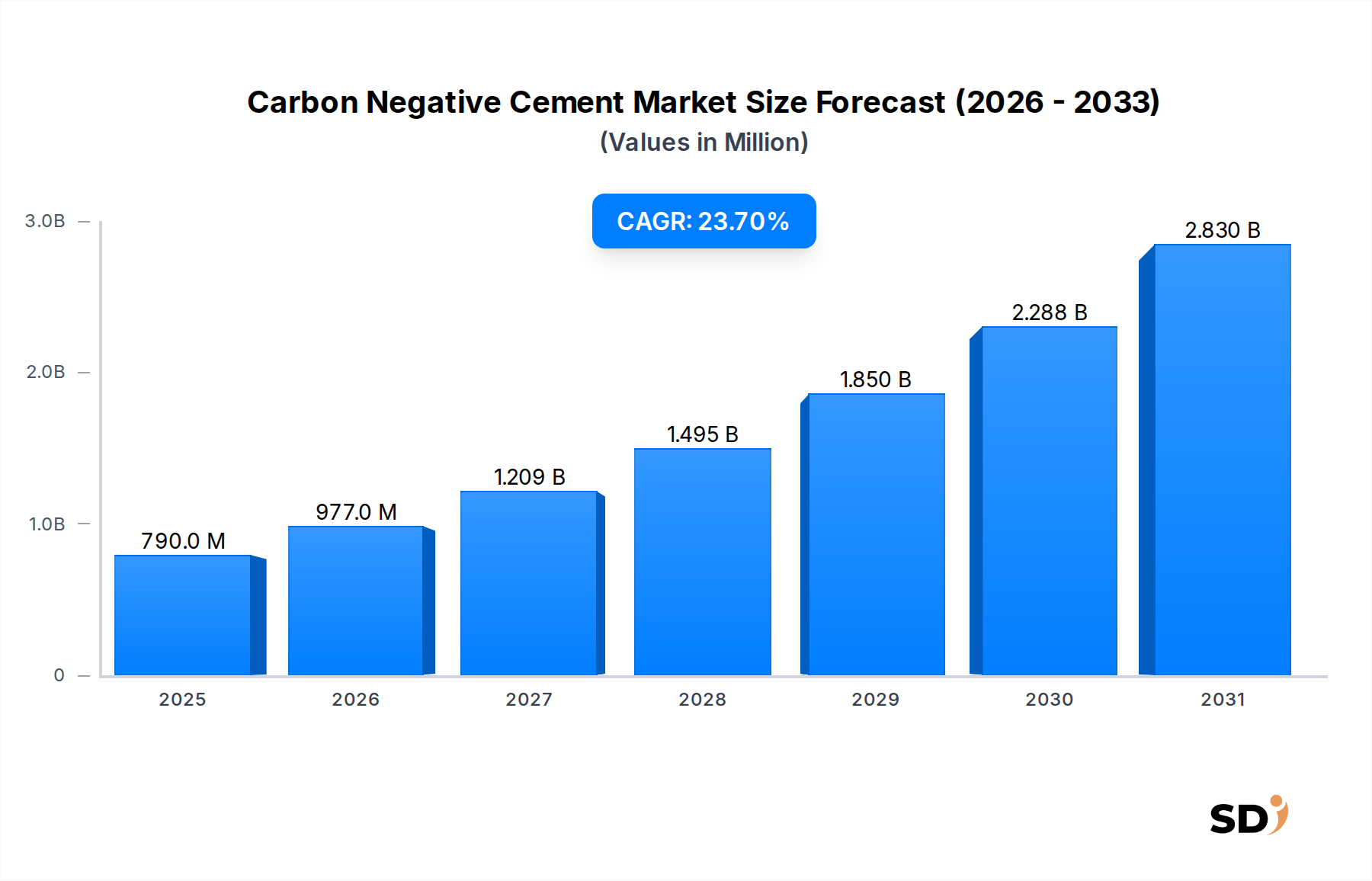

The global Carbon Negative Cement Market is poised for transformative growth, driven by an urgent imperative for decarbonization within the construction industry. Valued at an estimated $0.79 billion in 2025, this nascent market is projected to expand significantly, reaching approximately $5.19 billion by 2034, exhibiting a robust Compound Annual Growth Rate (CAGR) of 23.7% over the forecast period. This remarkable trajectory is underpinned by a confluence of demand drivers, including stringent environmental regulations, escalating carbon pricing mechanisms, and a growing corporate commitment to Environmental, Social, and Governance (ESG) principles. The market encompasses a range of innovative technologies, from carbon mineralization and bio-based binders to advanced geopolymer formulations, all designed to sequester or avoid more CO2 than emitted during their production. Major macro tailwinds include global net-zero emissions targets, increased investment in green infrastructure projects, and a shift in consumer and developer preference towards eco-conscious building materials. The adoption of carbon negative cement is becoming a strategic imperative for developers and governments alike, seeking to reduce the embodied carbon of structures. While the Carbon Negative Cement Market is still in its early stages, it represents a critical frontier in sustainable construction, offering a viable pathway to mitigating the substantial carbon footprint traditionally associated with the broader Cement and Concrete Market. The outlook suggests a rapid evolution from niche application to mainstream adoption, with continuous technological advancements and scaling of production processes anticipated to drive down costs and enhance performance characteristics, further solidifying its market position over the next decade. The confluence of innovation and regulatory support is setting the stage for substantial market expansion and competitive disruption.

Carbon Negative Cement Market Size (In Million)

3.0B

2.0B

1.0B

0

790.0 M

2025

977.0 M

2026

1.209 B

2027

1.495 B

2028

1.850 B

2029

2.288 B

2030

2.830 B

2031

Carbon Mineralized Cement Dominance in the Carbon Negative Cement Market

Within the nascent but rapidly expanding Carbon Negative Cement Market, the Carbon Mineralized Cement segment stands out as the single largest and most promising product type by revenue share. This dominance stems from its direct and verifiable ability to sequester atmospheric or industrial CO2 within the cement matrix itself, either through direct injection during the mixing process or by chemically reacting CO2 with industrial by-products or natural minerals to form stable carbonates. The appeal of carbon mineralized cement lies in its tangible contribution to net-zero targets and its potential to transform concrete from a significant carbon emitter into a carbon sink. This segment leverages advanced Carbon Capture and Utilization Market technologies, converting waste CO2 into a valuable input material. Key players like Blue Planet and CarbiCrete are at the forefront, developing proprietary processes that enhance the performance and durability of concrete while effectively locking away carbon. Blue Planet, for instance, creates synthetic limestone aggregates by mineralizing captured CO2, which can then be used in concrete production. CarbiCrete's solution involves injecting CO2 into fresh concrete during mixing, triggering a mineralization process that strengthens the concrete and sequesters carbon. The inherent versatility of these technologies, allowing for integration with existing concrete production infrastructure, further bolsters this segment's leadership. Furthermore, ongoing research is focused on optimizing reaction kinetics and material properties to ensure long-term stability and widespread applicability across various construction types. As regulatory pressures intensify and carbon credits become more valuable, the economic viability of carbon mineralized cement is improving, attracting significant investment and fostering rapid innovation. While other segments, such as Geopolymer Cement Market and bio-based cements, offer compelling low-carbon alternatives, the direct CO2 sequestration attribute positions carbon mineralized cement as a crucial component in achieving truly carbon-negative construction. This segment is not only growing rapidly but is also consolidating through strategic partnerships and acquisitions as companies vie for market leadership in this critical sustainability frontier. The emphasis on measurable carbon reduction provides a strong competitive advantage, driving its increasing share within the overall Carbon Negative Cement Market.

Key Market Drivers and Constraints in the Carbon Negative Cement Market

The Carbon Negative Cement Market is being propelled by powerful macro-economic and regulatory forces, alongside facing inherent challenges. A primary driver is the Global Push for Decarbonization, with governments and industries worldwide committing to net-zero emissions targets, often by 2050. The construction sector, responsible for approximately 11% of global energy-related CO2 emissions from materials and construction processes, faces immense pressure to reduce its environmental footprint. This has translated into policies like the European Green Deal and various national sustainable infrastructure initiatives, mandating or incentivizing the use of low-carbon materials, thereby creating a substantial demand for carbon negative solutions. Furthermore, the expansion of Green Building Certifications such as LEED, BREEAM, and WELL standards plays a pivotal role. These certifications increasingly award points for projects that utilize materials with low embodied carbon, directly fueling demand within the Sustainable Building Materials Market. For instance, projects aiming for higher LEED ratings are actively seeking innovative materials, including carbon negative cement, to meet stringent environmental performance criteria. The Growing Adoption of Carbon Pricing Mechanisms, including carbon taxes and cap-and-trade systems (e.g., EU-ETS), represents another significant driver. These mechanisms increase the cost of traditional high-emission cement production, making carbon negative alternatives more economically competitive. As of 2024, over 70 global jurisdictions have implemented some form of carbon pricing, creating a clear financial incentive for cleaner technologies.

Conversely, the market faces notable constraints. High Initial Capital Investment for establishing new carbon negative cement production facilities or retrofitting existing ones poses a significant barrier. These advanced technologies often require specialized equipment for CO2 capture, mineralization, or novel binder synthesis, leading to substantial upfront costs for manufacturers. Secondly, Scalability Challenges hinder rapid market penetration. Many carbon negative cement technologies are still transitioning from pilot-scale to commercial production, requiring substantial R&D and engineering efforts to achieve economies of scale necessary for widespread adoption. Lastly, a Lack of Standardized Performance Data and Regulatory Frameworks can slow market acceptance. Traditional cement has decades of established performance data and widely recognized standards. For novel carbon negative cements, the slower development of comprehensive industry standards and long-term performance validation studies can create uncertainty among specifiers, engineers, and regulators, impeding their mainstream integration.

Competitive Ecosystem of Carbon Negative Cement Market

The competitive landscape of the Carbon Negative Cement Market is characterized by a mix of innovative startups, established material science companies, and traditional cement players exploring sustainable alternatives. These entities are actively developing and commercializing various carbon negative technologies.

Biomason: Focuses on bio-mineralization to grow cement-based building materials, leveraging microorganisms to produce calcium carbonate within a sand aggregate. This process dramatically reduces energy consumption and eliminates the need for high-temperature kilns, resulting in a significantly lower carbon footprint.

Blue Planet: Specializes in converting captured CO2 emissions into synthetic limestone aggregates for concrete, effectively sequestering carbon while creating a valuable construction material. Their technology aims to create carbon-negative concrete solutions by integrating mineralized CO2.

Picarro, Inc.: Provides high-precision gas measurement and analysis equipment, critical for optimizing carbon capture and utilization processes. While not a direct cement producer, their technology supports the efficient and verifiable sequestration of CO2, indirectly facilitating the carbon negative cement value chain.

Partanna: Develops proprietary cement alternatives utilizing seawater and naturally occurring minerals, enabling robust carbon sequestration. Their innovation centers on creating materials that absorb more carbon than emitted during their production.

Seratech: Innovates with magnesium silicate-based binders, offering a promising carbon-negative solution by utilizing industrial waste streams and sequestering CO2. Their technology targets high-performance, sustainable construction materials.

CarbiCrete: Utilizes industrial by-products and injects captured CO2 into concrete during the mixing process, turning concrete into a carbon sink. This approach offers a drop-in solution for existing concrete manufacturers to reduce their environmental impact.

Glenwood Mason Supply: As a traditional concrete and masonry supplier, Glenwood Mason Supply is exploring the integration of carbon-negative technologies and products into their offerings to meet increasing demand for sustainable building solutions from the Commercial Construction Market.

Terra CO 3 Technologies: Focuses on producing cement from widely available industrial waste streams, significantly reducing both the embodied carbon and raw material extraction associated with traditional cement. Their process enhances resource efficiency and sustainability.

Brimstone: Developing carbon-negative cement from calcium silicate rock, effectively bypassing the CO2-intensive decarbonization of limestone. This innovative approach aims to produce Portland cement clinker without CO2 emissions from raw materials.

CarbonBuilt: Transforms industrial waste and captured CO2 into low-carbon concrete blocks and precast products using a novel CO2 mineralization process. Their technology offers a scalable pathway to carbon negative concrete production.

Prometheus Materials: Develops bio-cement using microalgae, sequestering atmospheric carbon during the binding process. This nature-inspired approach creates construction materials with a significantly reduced carbon footprint, targeting a range of applications in the Residential Construction Market.

Recent Developments & Milestones in Carbon Negative Cement Market

Q4 2023: A leading technology provider in the Carbon Negative Cement Market, specialized in magnesium-based binders, secured a significant Series B funding round totaling $75 million. This investment is earmarked to scale up its commercial production facilities and accelerate R&D into novel applications for its carbon mineralization process.

Q1 2024: A major partnership was announced between a prominent carbon negative cement producer and a large Commercial Construction Market developer for a pilot project in a major metropolitan area. This collaboration aims to construct a multi-story office building using advanced carbon-sequestering concrete, demonstrating its viability and performance in large-scale commercial applications.

Q2 2024: The European Union introduced new policy directives and incentives to integrate low-carbon building materials into public infrastructure projects. This regulatory push is expected to significantly benefit the Alkali-Activated Materials Market and other sustainable alternatives, including various forms of carbon negative cement, by favoring bids that prioritize environmental performance.

Q3 2024: A US-based startup successfully demonstrated a prototype residential dwelling constructed entirely with bio-based carbon negative cement. This proof-of-concept for the Residential Construction Market showcased equivalent or superior structural integrity and durability compared to traditional Portland cement, marking a critical step towards wider adoption in housing.

Q4 2024: Breakthroughs in materials science led to the development of a new generation of high-performance carbon mineralized cement capable of sequestering up to 20% more CO2 by weight than previous formulations. This advancement promises enhanced environmental benefits without compromising structural performance.

Q1 2025: An Asian consortium announced the commissioning of the region's largest integrated plant for Geopolymer Cement Market production, targeting a significant reduction in CO2 emissions compared to conventional cement. This facility aims to supply low-carbon concrete for urban development projects across several rapidly growing economies.

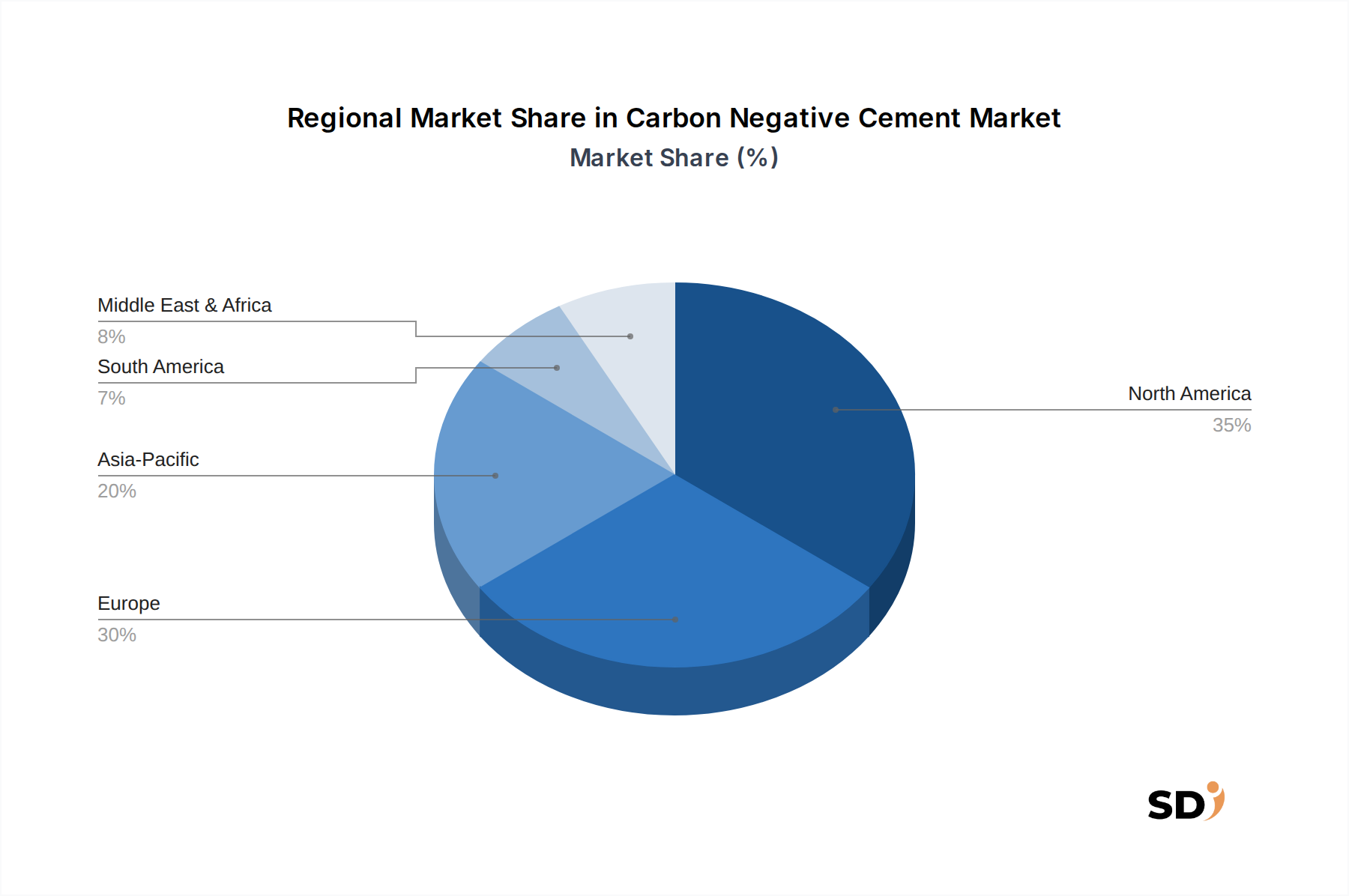

Regional Market Breakdown for Carbon Negative Cement Market

Analysis of the Carbon Negative Cement Market reveals distinct growth patterns and drivers across key global regions. Europe is currently positioned as a leading region, driven by its stringent environmental regulations, aggressive decarbonization targets, and well-established carbon pricing mechanisms. Nations like Germany, France, and the UK have been early adopters, supported by government incentives for green construction and robust research and development activities. The European market, while potentially mature in terms of initial policy adoption, is expected to maintain a strong growth trajectory due to continued emphasis on sustainable building and circular economy principles, possibly growing at a CAGR near the global average of 23.7%. The primary demand driver here is regulatory compliance and a strong institutional commitment to climate neutrality.

North America represents a rapidly expanding market, demonstrating substantial potential for high growth. The region benefits from significant investments in green infrastructure, supportive policies such as the Inflation Reduction Act, and a burgeoning venture capital ecosystem funding innovative startups in sustainable materials. The United States, in particular, is witnessing increasing adoption in both the Residential Construction Market and Commercial Construction Market, driven by corporate ESG goals and a growing consumer preference for eco-friendly homes. This region's growth is fueled by technological advancements and strategic partnerships between material producers and construction firms.

Asia Pacific is emerging as a critical growth engine for the Carbon Negative Cement Market, primarily due to its massive and rapidly expanding construction industry, particularly in countries like China and India. While still in nascent stages, the sheer scale of urban development and infrastructure projects presents an unparalleled opportunity for carbon negative cement. The region's growth is expected to be exponential, albeit from a lower base, as governments begin to implement stricter environmental policies and as major construction players seek to reduce their carbon footprint. Cost-effectiveness and scalability will be key drivers here.

The Middle East & Africa region also shows promising growth, largely influenced by ambitious national visions for sustainable development, such as Saudi Vision 2030 and other GCC initiatives. These countries are investing heavily in future-proof urban landscapes, creating a demand for innovative materials. Although starting from a smaller market share, the region's focus on building new, sustainable cities could lead to very high growth rates in specific clusters, driven by national mandates for sustainable construction practices.

Supply Chain & Raw Material Dynamics for Carbon Negative Cement Market

The supply chain for the Carbon Negative Cement Market is inherently complex, diverging significantly from traditional Portland cement production due to its reliance on novel inputs and processes. Upstream dependencies include various sources of carbon dioxide (CO2), such as industrial emissions from power plants or direct air capture (DAC) facilities, which are critical for carbon mineralization and Carbon Capture and Utilization Market technologies. The availability and purity of this captured CO2 represent a significant sourcing risk, with pricing often linked to carbon credit markets or the cost of capture technology, which can experience volatility. Other key inputs include industrial by-products like fly ash and blast furnace slag, calcined clays for Geopolymer Cement Market and Alkali-Activated Materials Market, and specific minerals such as magnesium compounds for magnesium-based cements. The Magnesium Oxide Market, for instance, is crucial for certain carbon negative formulations, and its price trends can be influenced by energy costs and geopolitical factors affecting mining operations.

Price volatility of these key inputs can significantly impact production costs. For example, the cost of industrial by-products can fluctuate based on demand from other industries, while the energy-intensive nature of CO2 capture can make it susceptible to fossil fuel price swings. Disruptions in global shipping, as seen during the 2020-2022 period, have historically affected the timely delivery of specialized equipment and raw materials, leading to project delays and increased logistics costs. Furthermore, the reliance on industrial waste streams presents both an opportunity (waste valorization) and a risk (consistency and availability). Ensuring a consistent supply of high-quality waste materials requires robust partnerships with industries generating these by-products. As the market scales, securing reliable, long-term supplies of these diverse raw materials and CO2 will be paramount, necessitating strategic alliances and potential vertical integration within the Carbon Negative Cement Market ecosystem.

The regulatory and policy landscape is a pivotal determinant in the growth trajectory of the Carbon Negative Cement Market. Across key geographies, governments and international bodies are actively shaping frameworks to encourage the adoption of low-carbon building materials. The European Union leads with its comprehensive EU Taxonomy for sustainable activities, which provides clear criteria for what constitutes a "green" building material, effectively steering investment towards solutions like carbon negative cement. The EU's Emission Trading System (ETS) and forthcoming Carbon Border Adjustment Mechanism (CBAM) are increasing the cost of conventional, high-carbon materials, thereby enhancing the economic competitiveness of sustainable alternatives. In North America, the Inflation Reduction Act (IRA) in the United States offers significant tax credits and incentives for Carbon Capture and Utilization Market technologies and low-carbon manufacturing, directly benefiting producers of carbon negative cement. State-level "Buy Clean" initiatives are also emerging, prioritizing procurement of construction materials with lower embodied carbon for public projects.

Standards bodies such as ASTM International and ISO (International Organization for Standardization) are in the process of developing new testing protocols and performance standards specifically for novel cementitious materials. The lack of universally recognized standards has historically been a hurdle, but ongoing efforts aim to provide clear guidelines for engineers and architects, fostering greater confidence in these innovative products. Recent policy changes, such as revised building codes in several jurisdictions to accommodate novel materials and increased funding for green research, are projected to have a significant positive market impact. These changes help to de-risk investment, accelerate technology commercialization, and create a level playing field for emerging solutions within the Sustainable Building Materials Market. The increasing integration of life cycle assessment (LCA) requirements into regulatory frameworks further underscores the importance of carbon negative materials, pushing the industry towards a more holistic evaluation of environmental impact.

Carbon Negative Cement Segmentation

1. Product Type

1.1. Carbon Mineralized Cement

1.2. Magnesium-Based Carbon Negative Cement

1.3. Geopolymer Carbon Negative Cement

1.4. Bio-Based Carbon Negative Cement

1.5. Others

2. Technology Type

2.1. Carbon Capture and Utilization (CCU) Cement

2.2. Carbon Mineralization Technology

2.3. Carbon Injection/Curing Technology

2.4. Geopolymer Technology

2.5. Magnesium Oxide (MgO)-Based Technology

2.6. Alkali-Activated Materials (AAM) Technology

2.7. Others

3. Cement Form

3.1. Ready-Mix Cement

3.2. Dry Cement Mix

3.3. Others

4. Application

4.1. Residential

4.2. Commercial

4.3. Industrial

Carbon Negative Cement Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Carbon Negative Cement REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 23.7% from 2020-2034

Segmentation

By Product Type

Carbon Mineralized Cement

Magnesium-Based Carbon Negative Cement

Geopolymer Carbon Negative Cement

Bio-Based Carbon Negative Cement

Others

By Technology Type

Carbon Capture and Utilization (CCU) Cement

Carbon Mineralization Technology

Carbon Injection/Curing Technology

Geopolymer Technology

Magnesium Oxide (MgO)-Based Technology

Alkali-Activated Materials (AAM) Technology

Others

By Cement Form

Ready-Mix Cement

Dry Cement Mix

Others

By Application

Residential

Commercial

Industrial

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Type

5.1.1. Carbon Mineralized Cement

5.1.2. Magnesium-Based Carbon Negative Cement

5.1.3. Geopolymer Carbon Negative Cement

5.1.4. Bio-Based Carbon Negative Cement

5.1.5. Others

5.2. Market Analysis, Insights and Forecast - by Technology Type

5.2.1. Carbon Capture and Utilization (CCU) Cement

10.3. Market Analysis, Insights and Forecast - by Cement Form

10.3.1. Ready-Mix Cement

10.3.2. Dry Cement Mix

10.3.3. Others

10.4. Market Analysis, Insights and Forecast - by Application

10.4.1. Residential

10.4.2. Commercial

10.4.3. Industrial

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Biomason

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Blue Planet

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Picarro

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Inc.

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Partanna

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Seratech

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. CarbiCrete

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Glenwood Mason Supply

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Terra CO 3 Technologies

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Brimstone

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. CarbonBuilt

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Prometheus Materials

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Product Type 2025 & 2033

Figure 4: Volume (K), by Product Type 2025 & 2033

Figure 5: Revenue Share (%), by Product Type 2025 & 2033

Figure 6: Volume Share (%), by Product Type 2025 & 2033

Figure 7: Revenue (billion), by Technology Type 2025 & 2033

Figure 8: Volume (K), by Technology Type 2025 & 2033

Figure 9: Revenue Share (%), by Technology Type 2025 & 2033

Figure 10: Volume Share (%), by Technology Type 2025 & 2033

Figure 11: Revenue (billion), by Cement Form 2025 & 2033

Figure 12: Volume (K), by Cement Form 2025 & 2033

Figure 13: Revenue Share (%), by Cement Form 2025 & 2033

Figure 14: Volume Share (%), by Cement Form 2025 & 2033

Figure 15: Revenue (billion), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (billion), by Country 2025 & 2033

Figure 20: Volume (K), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Volume Share (%), by Country 2025 & 2033

Figure 23: Revenue (billion), by Product Type 2025 & 2033

Figure 24: Volume (K), by Product Type 2025 & 2033

Figure 25: Revenue Share (%), by Product Type 2025 & 2033

Figure 26: Volume Share (%), by Product Type 2025 & 2033

Figure 27: Revenue (billion), by Technology Type 2025 & 2033

Figure 28: Volume (K), by Technology Type 2025 & 2033

Figure 29: Revenue Share (%), by Technology Type 2025 & 2033

Figure 30: Volume Share (%), by Technology Type 2025 & 2033

Figure 31: Revenue (billion), by Cement Form 2025 & 2033

Figure 32: Volume (K), by Cement Form 2025 & 2033

Figure 33: Revenue Share (%), by Cement Form 2025 & 2033

Figure 34: Volume Share (%), by Cement Form 2025 & 2033

Figure 35: Revenue (billion), by Application 2025 & 2033

Figure 36: Volume (K), by Application 2025 & 2033

Figure 37: Revenue Share (%), by Application 2025 & 2033

Figure 38: Volume Share (%), by Application 2025 & 2033

Figure 39: Revenue (billion), by Country 2025 & 2033

Figure 40: Volume (K), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Volume Share (%), by Country 2025 & 2033

Figure 43: Revenue (billion), by Product Type 2025 & 2033

Figure 44: Volume (K), by Product Type 2025 & 2033

Figure 45: Revenue Share (%), by Product Type 2025 & 2033

Figure 46: Volume Share (%), by Product Type 2025 & 2033

Figure 47: Revenue (billion), by Technology Type 2025 & 2033

Figure 48: Volume (K), by Technology Type 2025 & 2033

Figure 49: Revenue Share (%), by Technology Type 2025 & 2033

Figure 50: Volume Share (%), by Technology Type 2025 & 2033

Figure 51: Revenue (billion), by Cement Form 2025 & 2033

Figure 52: Volume (K), by Cement Form 2025 & 2033

Figure 53: Revenue Share (%), by Cement Form 2025 & 2033

Figure 54: Volume Share (%), by Cement Form 2025 & 2033

Figure 55: Revenue (billion), by Application 2025 & 2033

Figure 56: Volume (K), by Application 2025 & 2033

Figure 57: Revenue Share (%), by Application 2025 & 2033

Figure 58: Volume Share (%), by Application 2025 & 2033

Figure 59: Revenue (billion), by Country 2025 & 2033

Figure 60: Volume (K), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

Figure 62: Volume Share (%), by Country 2025 & 2033

Figure 63: Revenue (billion), by Product Type 2025 & 2033

Figure 64: Volume (K), by Product Type 2025 & 2033

Figure 65: Revenue Share (%), by Product Type 2025 & 2033

Figure 66: Volume Share (%), by Product Type 2025 & 2033

Figure 67: Revenue (billion), by Technology Type 2025 & 2033

Figure 68: Volume (K), by Technology Type 2025 & 2033

Figure 69: Revenue Share (%), by Technology Type 2025 & 2033

Figure 70: Volume Share (%), by Technology Type 2025 & 2033

Figure 71: Revenue (billion), by Cement Form 2025 & 2033

Figure 72: Volume (K), by Cement Form 2025 & 2033

Figure 73: Revenue Share (%), by Cement Form 2025 & 2033

Figure 74: Volume Share (%), by Cement Form 2025 & 2033

Figure 75: Revenue (billion), by Application 2025 & 2033

Figure 76: Volume (K), by Application 2025 & 2033

Figure 77: Revenue Share (%), by Application 2025 & 2033

Figure 78: Volume Share (%), by Application 2025 & 2033

Figure 79: Revenue (billion), by Country 2025 & 2033

Figure 80: Volume (K), by Country 2025 & 2033

Figure 81: Revenue Share (%), by Country 2025 & 2033

Figure 82: Volume Share (%), by Country 2025 & 2033

Figure 83: Revenue (billion), by Product Type 2025 & 2033

Figure 84: Volume (K), by Product Type 2025 & 2033

Figure 85: Revenue Share (%), by Product Type 2025 & 2033

Figure 86: Volume Share (%), by Product Type 2025 & 2033

Figure 87: Revenue (billion), by Technology Type 2025 & 2033

Figure 88: Volume (K), by Technology Type 2025 & 2033

Figure 89: Revenue Share (%), by Technology Type 2025 & 2033

Figure 90: Volume Share (%), by Technology Type 2025 & 2033

Figure 91: Revenue (billion), by Cement Form 2025 & 2033

Figure 92: Volume (K), by Cement Form 2025 & 2033

Figure 93: Revenue Share (%), by Cement Form 2025 & 2033

Figure 94: Volume Share (%), by Cement Form 2025 & 2033

Figure 95: Revenue (billion), by Application 2025 & 2033

Figure 96: Volume (K), by Application 2025 & 2033

Figure 97: Revenue Share (%), by Application 2025 & 2033

Figure 98: Volume Share (%), by Application 2025 & 2033

Figure 99: Revenue (billion), by Country 2025 & 2033

Figure 100: Volume (K), by Country 2025 & 2033

Figure 101: Revenue Share (%), by Country 2025 & 2033

Figure 102: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Product Type 2020 & 2033

Table 2: Volume K Forecast, by Product Type 2020 & 2033

Table 3: Revenue billion Forecast, by Technology Type 2020 & 2033

Table 4: Volume K Forecast, by Technology Type 2020 & 2033

Table 5: Revenue billion Forecast, by Cement Form 2020 & 2033

Table 6: Volume K Forecast, by Cement Form 2020 & 2033

Table 7: Revenue billion Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue billion Forecast, by Region 2020 & 2033

Table 10: Volume K Forecast, by Region 2020 & 2033

Table 11: Revenue billion Forecast, by Product Type 2020 & 2033

Table 12: Volume K Forecast, by Product Type 2020 & 2033

Table 13: Revenue billion Forecast, by Technology Type 2020 & 2033

Table 14: Volume K Forecast, by Technology Type 2020 & 2033

Table 15: Revenue billion Forecast, by Cement Form 2020 & 2033

Table 16: Volume K Forecast, by Cement Form 2020 & 2033

Table 17: Revenue billion Forecast, by Application 2020 & 2033

Table 18: Volume K Forecast, by Application 2020 & 2033

Table 19: Revenue billion Forecast, by Country 2020 & 2033

Table 20: Volume K Forecast, by Country 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Volume (K) Forecast, by Application 2020 & 2033

Table 23: Revenue (billion) Forecast, by Application 2020 & 2033

Table 24: Volume (K) Forecast, by Application 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue billion Forecast, by Product Type 2020 & 2033

Table 28: Volume K Forecast, by Product Type 2020 & 2033

Table 29: Revenue billion Forecast, by Technology Type 2020 & 2033

Table 30: Volume K Forecast, by Technology Type 2020 & 2033

Table 31: Revenue billion Forecast, by Cement Form 2020 & 2033

Table 32: Volume K Forecast, by Cement Form 2020 & 2033

Table 33: Revenue billion Forecast, by Application 2020 & 2033

Table 34: Volume K Forecast, by Application 2020 & 2033

Table 35: Revenue billion Forecast, by Country 2020 & 2033

Table 36: Volume K Forecast, by Country 2020 & 2033

Table 37: Revenue (billion) Forecast, by Application 2020 & 2033

Table 38: Volume (K) Forecast, by Application 2020 & 2033

Table 39: Revenue (billion) Forecast, by Application 2020 & 2033

Table 40: Volume (K) Forecast, by Application 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Volume (K) Forecast, by Application 2020 & 2033

Table 43: Revenue billion Forecast, by Product Type 2020 & 2033

Table 44: Volume K Forecast, by Product Type 2020 & 2033

Table 45: Revenue billion Forecast, by Technology Type 2020 & 2033

Table 46: Volume K Forecast, by Technology Type 2020 & 2033

Table 47: Revenue billion Forecast, by Cement Form 2020 & 2033

Table 48: Volume K Forecast, by Cement Form 2020 & 2033

Table 49: Revenue billion Forecast, by Application 2020 & 2033

Table 50: Volume K Forecast, by Application 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Volume K Forecast, by Country 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Volume (K) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Volume (K) Forecast, by Application 2020 & 2033

Table 59: Revenue (billion) Forecast, by Application 2020 & 2033

Table 60: Volume (K) Forecast, by Application 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (billion) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (billion) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (billion) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue billion Forecast, by Product Type 2020 & 2033

Table 72: Volume K Forecast, by Product Type 2020 & 2033

Table 73: Revenue billion Forecast, by Technology Type 2020 & 2033

Table 74: Volume K Forecast, by Technology Type 2020 & 2033

Table 75: Revenue billion Forecast, by Cement Form 2020 & 2033

Table 76: Volume K Forecast, by Cement Form 2020 & 2033

Table 77: Revenue billion Forecast, by Application 2020 & 2033

Table 78: Volume K Forecast, by Application 2020 & 2033

Table 79: Revenue billion Forecast, by Country 2020 & 2033

Table 80: Volume K Forecast, by Country 2020 & 2033

Table 81: Revenue (billion) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue (billion) Forecast, by Application 2020 & 2033

Table 84: Volume (K) Forecast, by Application 2020 & 2033

Table 85: Revenue (billion) Forecast, by Application 2020 & 2033

Table 86: Volume (K) Forecast, by Application 2020 & 2033

Table 87: Revenue (billion) Forecast, by Application 2020 & 2033

Table 88: Volume (K) Forecast, by Application 2020 & 2033

Table 89: Revenue (billion) Forecast, by Application 2020 & 2033

Table 90: Volume (K) Forecast, by Application 2020 & 2033

Table 91: Revenue (billion) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Table 93: Revenue billion Forecast, by Product Type 2020 & 2033

Table 94: Volume K Forecast, by Product Type 2020 & 2033

Table 95: Revenue billion Forecast, by Technology Type 2020 & 2033

Table 96: Volume K Forecast, by Technology Type 2020 & 2033

Table 97: Revenue billion Forecast, by Cement Form 2020 & 2033

Table 98: Volume K Forecast, by Cement Form 2020 & 2033

Table 99: Revenue billion Forecast, by Application 2020 & 2033

Table 100: Volume K Forecast, by Application 2020 & 2033

Table 101: Revenue billion Forecast, by Country 2020 & 2033

Table 102: Volume K Forecast, by Country 2020 & 2033

Table 103: Revenue (billion) Forecast, by Application 2020 & 2033

Table 104: Volume (K) Forecast, by Application 2020 & 2033

Table 105: Revenue (billion) Forecast, by Application 2020 & 2033

Table 106: Volume (K) Forecast, by Application 2020 & 2033

Table 107: Revenue (billion) Forecast, by Application 2020 & 2033

Table 108: Volume (K) Forecast, by Application 2020 & 2033

Table 109: Revenue (billion) Forecast, by Application 2020 & 2033

Table 110: Volume (K) Forecast, by Application 2020 & 2033

Table 111: Revenue (billion) Forecast, by Application 2020 & 2033

Table 112: Volume (K) Forecast, by Application 2020 & 2033

Table 113: Revenue (billion) Forecast, by Application 2020 & 2033

Table 114: Volume (K) Forecast, by Application 2020 & 2033

Table 115: Revenue (billion) Forecast, by Application 2020 & 2033

Table 116: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our research methodology places a significant emphasis on primary intelligence, constituting between 70% to 80% (specifically, 75%) of the total research effort. This critical phase involves conducting extensive, in-depth interviews, targeted surveys, and structured discussions with key industry stakeholders and subject matter experts across the carbon-negative cement value chain. This direct engagement provides invaluable qualitative and quantitative insights, validating secondary data and capturing nuanced market dynamics.

Key stakeholders engaged during this phase include:

Head of R&D, Sustainable Materials at leading carbon-negative cement manufacturers.

VP, Innovation & New Technologies at major construction and engineering firms.

Sustainability Director at large commercial and industrial development companies.

Product Manager, Low-Carbon Solutions at advanced carbon capture and mineralization technology providers.

Our primary research outreach targets a diverse range of companies critical to the market ecosystem:

Carbon Negative Cement Manufacturers

Carbon Capture Technology Providers

Construction & Engineering Firms

Material Science & R&D Labs specializing in sustainable building materials

Industrial Waste & Raw Material Suppliers (e.g., for mineral carbonation processes)

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Head of R&D, Sustainable Materials

30%

VP, Innovation & New Technologies

25%

Sustainability Director

25%

Product Manager, Low-Carbon Solutions

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Carbon Negative Cement Manufacturers

30%

Carbon Capture Technology Providers

25%

Construction & Engineering Firms

20%

Material Science & R&D Labs

15%

Industrial Waste & Raw Material Suppliers

10%

Secondary Research & Industry Benchmarking

Secondary research complements our primary efforts, accounting for the remaining 20% to 30% (specifically, 25%) of the research. This phase is crucial for establishing a foundational understanding of the market, identifying key trends, competitive landscapes, and regulatory frameworks. Our analysts leverage a comprehensive array of credible and proprietary sources, ensuring data integrity and reliability.

Sources utilized include:

Licensed Financial Databases: Bloomberg, Factiva, Hoovers, and PitchBook for corporate financials, investment trends, and competitive analysis.

Government Publications: Official reports and statistics from entities such as the U.S. Department of Energy (DOE), European Commission, and national environmental agencies, providing policy insights and R&D funding data.

Academic Journals and Research Papers: Peer-reviewed studies on carbon mineralization, geopolymer chemistry, and sustainable construction materials.

Company Annual Reports, Investor Presentations, and Press Releases: For detailed operational and strategic insights of market participants.

We strictly exclude data from other market research websites to maintain the independence and originality of our findings.

Demand Modeling & Market Estimation

Our market estimation methodology employs a robust combination of top-down and bottom-up approaches, reinforced by multi-level data triangulation, to ensure accuracy and comprehensive coverage. The top-down approach begins by analyzing macro-economic indicators such as global construction spending, industrial output, and regional GDP growth, progressively narrowing down to the specific carbon-negative cement market segments. Conversely, the bottom-up approach constructs the market size from granular data points, aggregated from primary and secondary research findings.

Key metrics and variables used for bottom-up market sizing include:

Annual production capacity (tonnes) of carbon-negative cement variants (e.g., carbon mineralized, magnesium-based) by key manufacturers across different regions.

Average selling price (USD/tonne) of carbon-negative cement, factoring in product type, technology, and regional variations.

Number and scale of active construction projects (residential, commercial, industrial) specifically utilizing or mandating carbon-negative cement.

Impact of government incentives and carbon credit valuations (USD/tonne of CO2 avoided/sequestered) influencing adoption rates and market economics.

All estimates are rigorously triangulated between these methodologies and validated through expert interviews, ensuring consistency and reliability across various market dimensions. Forecast models integrate historical growth trends, projected technological advancements, evolving regulatory landscapes, and emerging application areas.

Data Accuracy & Quality Check

Ensuring the highest level of data accuracy and quality is paramount to our firm. Every data point and market projection undergoes a stringent, multi-layered validation process. This includes cross-referencing primary insights with corroborated secondary data, employing statistical analysis to identify and correct anomalies, and a comprehensive review by an internal team of seasoned subject matter experts.

We guarantee an estimated data accuracy level of 88% to 90% for all reported figures and forecasts. This commitment reflects our dedication to providing highly reliable and actionable market intelligence. Furthermore, to ensure the utmost relevance, all market data, trends, and projections presented in the report are meticulously updated up to the exact date of purchase, reflecting the latest industry developments and market conditions.

Frequently Asked Questions

1. What are the key product types and applications driving the Carbon Negative Cement market?

Key product types include Carbon Mineralized Cement and Geopolymer Carbon Negative Cement. Primary applications span Residential, Commercial, and Industrial sectors, each requiring tailored solutions.

2. Which technologies are critical for Carbon Negative Cement production?

Critical technologies involve Carbon Capture and Utilization (CCU) Cement, Carbon Mineralization Technology, and Magnesium Oxide (MgO)-Based Technology. These methods capture or embed CO2, offering substitutes for traditional cement.

3. How does Carbon Negative Cement contribute to sustainability goals and ESG objectives?

Carbon Negative Cement significantly reduces the construction industry's carbon footprint by sequestering CO2. This aligns directly with global ESG mandates and promotes a more environmentally responsible building sector.

4. Who are the leading companies innovating in the Carbon Negative Cement market?

Prominent companies include Biomason, Blue Planet, CarbiCrete, and Prometheus Materials. These firms are developing diverse solutions, driving market expansion and technology adoption.

5. What notable developments influence the Carbon Negative Cement market's growth trajectory?

The market is projected to grow at a robust CAGR of 23.7% from 2025 to 2034, driven by technological advancements and increasing regulatory support. This growth indicates expanding commercialization and strategic partnerships.

6. What are the primary raw material and supply chain considerations for Carbon Negative Cement?

Raw material considerations include sourcing CO2 for mineralization and alkali-activated precursors for geopolymers. Supply chain focus involves efficient capture, transport, and integration of these specialized components into the cement production process.