Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

C4 Raffinate Market: $13.31B by 2025, 9.3% CAGR Data

C4 Raffinate

C4 Raffinate Market: $13.31B by 2025, 9.3% CAGR Data

C4 Raffinate by Raffinate Grade (Raffinate-1 (R1), Raffinate-2 (R2), Raffinate-3 (R3)), by Component Composition (n-Butane, Isobutane, 1-Butene, 2-Butene, Others), by Source (Steam Crackers, Fluid Catalytic Cracking (FCC) Units, Refinery C4 Streams), by Processing Stage (Raw C4 Raffinate, Hydrogenated Raffinate, Fractionated Raffinate), by End-Use Industry (Oil & Gas / Refining, Petrochemical Industry, Automotive, Chemical Manufacturing, Energy & Power, Rubber & Plastics, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 4, 2026|Base Year : 2025|Pages : 121

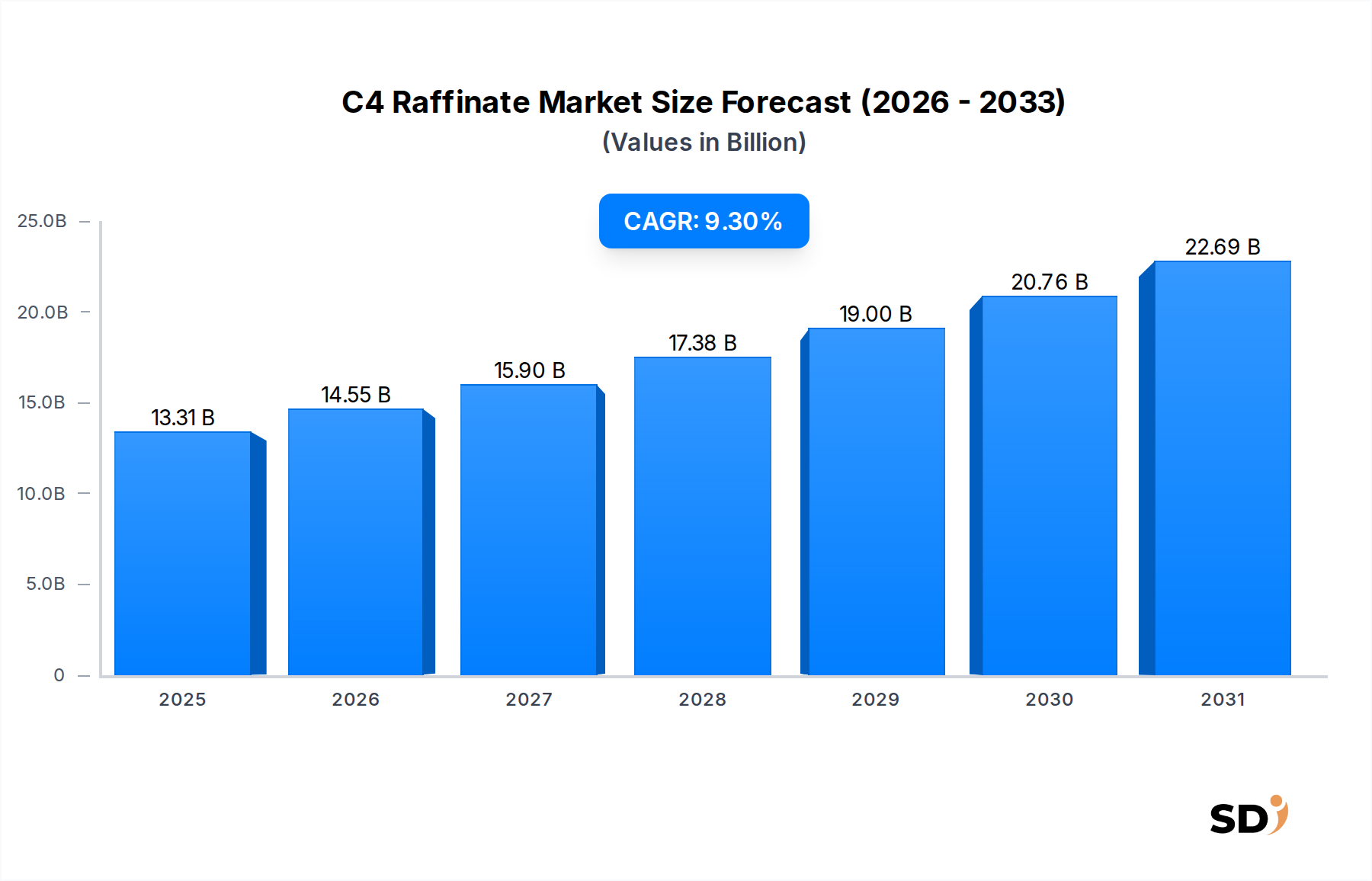

The C4 Raffinate Market is poised for substantial growth, reflecting its critical role as a foundational feedstock in the broader chemicals and materials sector. Valued at an estimated $13.31 billion in 2025, the market is projected to expand significantly, reaching approximately $24.61 billion by 2032, demonstrating a robust Compound Annual Growth Rate (CAGR) of 9.3% during the forecast period. This upward trajectory is fundamentally driven by the escalating demand for C4 raffinate derivatives across diverse end-use industries, most notably the expanding Petrochemicals Market. The primary macro tailwinds fueling this growth include sustained global economic expansion, particularly industrialization and infrastructure development in emerging economies, and the continuous innovation within chemical manufacturing processes.

C4 Raffinate Market Size (In Billion)

25.0B

20.0B

15.0B

10.0B

5.0B

0

13.31 B

2025

14.55 B

2026

15.90 B

2027

17.38 B

2028

19.00 B

2029

20.76 B

2030

22.69 B

2031

Key demand drivers encompass the burgeoning production of isobutylene and its derivatives, such as MTBE (methyl tert-butyl ether) for octane enhancement, and various forms of polyisobutylene. Furthermore, the expansion of global Steam Crackers Market capacity, driven by increased demand for ethylene and propylene, inevitably leads to a higher co-production of crude C4 streams, thereby increasing the supply of C4 raffinate. The C4 raffinate stream, primarily composed of isobutylene, n-butane, and 1-butene, serves as an indispensable building block for a myriad of chemicals. The automotive sector's demand for high-performance plastics and rubbers also indirectly stimulates the C4 raffinate market through the requirement for synthetic rubber and specialty elastomers.

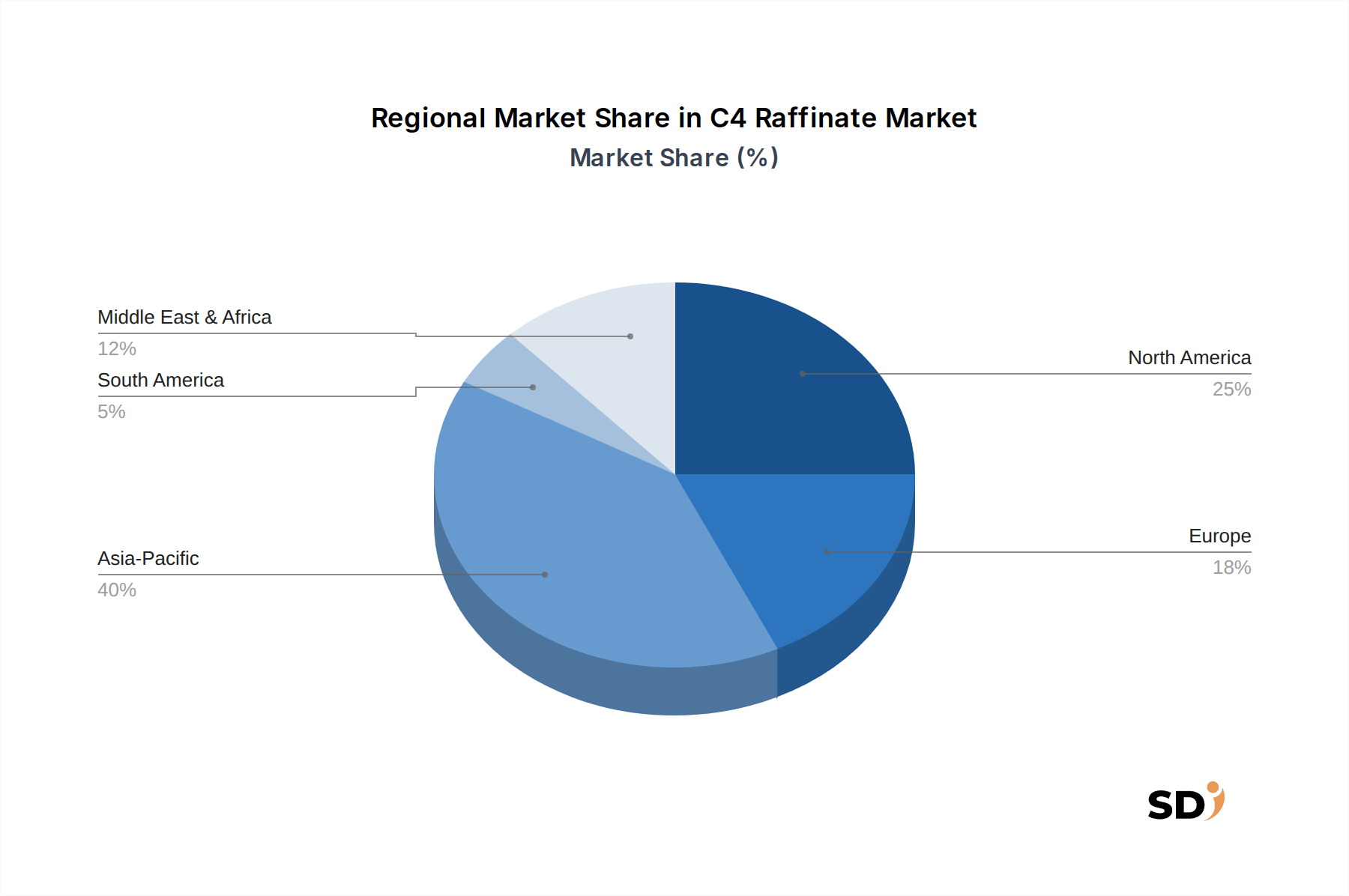

From a regional perspective, Asia Pacific is anticipated to maintain its dominance and exhibit the fastest growth, propelled by massive investments in new petrochemical complexes and a rapidly expanding manufacturing base. North America, benefiting from abundant shale gas resources, offers a stable supply of C4 feedstocks, underpinning steady market growth. The overall outlook for the C4 Raffinate Market remains highly positive, supported by its indispensable nature in downstream chemical processes and the continuous evolution of its derivative applications. Strategic investments in processing technologies and capacity expansions will be crucial for market participants to capitalize on this robust growth trajectory, while navigating the complexities of feedstock price volatility and environmental regulations impacting certain derivatives like those within the MTBE Market."

"## Raffinate-1 (R1) Segment Dominance in C4 Raffinate Market

Within the global C4 Raffinate Market, the Raffinate-1 (R1) grade segment stands out as the single largest and most critical component by revenue share. This dominance stems from its inherent position in the C4 processing value chain. Crude C4 streams, primarily originating from naphtha or gas oil crackers and Fluid Catalytic Cracking (FCC) units in refineries, are typically subjected to butadiene extraction. What remains after the selective hydrogenation and subsequent extraction of butadiene is predominantly Raffinate-1, a mixture rich in isobutylene, 1-butene, and n-butane. Given the scale of global Butadiene Market production, the volume of Raffinate-1 generated as a co-product is substantial, establishing its foundational role.

Raffinate-1's dominance is further solidified by its diverse and high-value downstream applications. It serves as a crucial feedstock for the production of methyl tert-butyl ether (MTBE), a widely used gasoline oxygenate and octane enhancer, and for the synthesis of high-purity Isobutylene Market products. Isobutylene, in turn, is vital for the production of polyisobutylene (PIB), butyl rubber, and various antioxidants and specialty chemicals. The demand for these derivatives directly underpins the strong market presence of Raffinate-1. Furthermore, the n-butane content in Raffinate-1 can be isomerized to isobutane, which is essential for alkylation processes in refining to produce high-octane gasoline components, further embedding its significance in the Refinery C4 Streams Market.

Key players in the C4 Raffinate Market, such as BASF, TPC Group, Shell Plc, and Reliance Industries Limited, have significant capacities for processing Raffinate-1. These companies often operate integrated petrochemical complexes, where crude C4 streams are efficiently separated and processed into various value-added derivatives. The market share of the Raffinate-1 segment is expected to continue its growth trajectory, driven by the expansion of the Petrochemicals Market and the increasing global demand for high-octane fuels and specialty elastomers. While the availability of Raffinate-1 is inherently tied to the upstream operation of Steam Crackers Market and refinery FCC units, its strategic importance as a versatile chemical intermediate ensures its sustained dominance and growth within the C4 Raffinate Market landscape. The continued growth in the Polyisobutylene Market and other high-value derivatives derived from Raffinate-1 further reinforces its leading position."

"## Strategic Drivers & Constraints Shaping the C4 Raffinate Market

The C4 Raffinate Market's growth trajectory is influenced by a confluence of strategic drivers and inherent constraints, each playing a critical role in shaping its dynamics. A primary driver is the escalating global demand for high-octane gasoline components. C4 raffinate, particularly its isobutylene content, is a key feedstock for producing methyl tert-butyl ether (MTBE) and alkylate, both vital for improving fuel octane ratings. This sustained demand from the refining sector underpins a significant portion of the C4 Raffinate Market. Furthermore, the robust expansion of the Petrochemicals Market, particularly in Asia Pacific, drives substantial demand for C4 raffinate as a versatile building block for numerous derivatives. Companies are investing heavily in new steam cracker capacities, which intrinsically increase the co-production of crude C4s, thereby boosting the availability of raffinate streams.

Another significant driver is the continuous growth in downstream applications such as the Synthetic Rubber Market and the Polyisobutylene Market. Isobutylene derived from C4 raffinate is essential for manufacturing butyl rubber (used in tires and sealants) and polyisobutylene (used in lubricants, adhesives, and fuel additives). The increasing automotive production and industrial manufacturing sectors directly correlate with the demand for these derivatives. Moreover, advancements in C4 processing technologies, enabling more efficient separation and conversion of individual components like isobutylene and butenes, enhance the economic viability of C4 raffinate utilization.

Conversely, several constraints pose challenges to the C4 Raffinate Market. The inherent volatility of crude oil and natural gas prices directly impacts feedstock costs for steam crackers and refineries, subsequently affecting the profitability and pricing of C4 raffinate. Environmental regulations, particularly the phase-out or restriction of MTBE in certain regions due to groundwater contamination concerns, has impacted a substantial derivative market, necessitating a shift towards alternative octane enhancers or isobutylene derivatives. Competition from alternative feedstocks or production routes for specific derivatives, such as on-purpose butadiene production that can alter the overall C4 stream composition, also acts as a constraint. Lastly, the significant capital expenditure required for new cracker and refinery projects, along with the complexities of managing the by-product streams, can restrain rapid market expansion."

"## Pricing Dynamics & Margin Pressure in C4 Raffinate Market

The C4 Raffinate Market operates within a complex pricing landscape, heavily influenced by upstream feedstock costs and downstream derivative demand. Average selling prices for C4 raffinate exhibit considerable volatility, primarily tracking crude oil and naphtha prices, as C4 streams are largely by-products of naphtha cracking or refinery operations. Consequently, fluctuations in global energy markets directly translate into price instability for C4 raffinate. The commodity nature of C4 raffinate means that its pricing power is often limited, with value largely captured further downstream in the derivative markets like the Isobutylene Market or MTBE Market.

Margin structures across the C4 raffinate value chain are typically thin at the primary raffinate production stage. Profitability is largely determined by the efficiency of feedstock utilization, the scale of operations, and the ability to convert raffinate into higher-value products. Integrated petrochemical players benefit from cost efficiencies by processing their own C4 streams into a diverse portfolio of derivatives. Key cost levers include the price of crude C4 feedstock, energy costs associated with separation and processing units, and logistics for transportation. Any upward pressure on these costs, without a corresponding increase in derivative selling prices, directly erodes margins.

Commodity cycles exert a profound impact. During periods of high crude oil prices, feedstock costs rise, potentially compressing C4 raffinate margins unless derivative demand is strong enough to allow for price pass-through. Conversely, during down cycles, lower feedstock costs can improve margins, but often coincide with weaker derivative demand. Competitive intensity is high due to the presence of numerous large-scale, integrated chemical manufacturers globally. This intense competition, coupled with the standardized nature of C4 raffinate, further limits individual producers' pricing power. Furthermore, the increasing focus on sustainability and the potential for new regulations could introduce additional costs, creating further margin pressure in the C4 Raffinate Market."

"## Technology Innovation Trajectory in C4 Raffinate Market

Innovation within the C4 Raffinate Market is primarily focused on enhancing feedstock efficiency, improving separation processes, and developing novel conversion pathways to higher-value derivatives. One of the most disruptive emerging technologies involves advanced separation techniques, such as membrane separation and reactive distillation. Traditional extractive distillation for separating C4 components is energy-intensive. New membrane technologies, for instance, offer the potential for more energy-efficient and selective separation of isobutylene or n-butane from complex raffinate mixtures, leading to higher purity products and reduced operational costs. Adoption timelines for these technologies are typically long, spanning 5-10 years, due to the high capital investment required and the need for rigorous validation in large-scale operations. R&D investments are significant, often spearheaded by major chemical engineering firms and integrated petrochemical companies aiming to optimize existing assets and reduce their carbon footprint.

A second area of innovation involves catalytic conversion technologies designed for direct valorization of C4 raffinate components. This includes the development of highly selective catalysts for the direct dehydrogenation of n-butane to butenes or butadiene, or the isomerization of butenes to isobutylene, effectively optimizing the product mix from a given raffinate stream. While the Butane Market already provides feedstocks for some of these conversions, innovations in catalyst design aim to improve yields and reduce energy consumption. These advancements threaten incumbent business models reliant on older, less efficient separation processes by offering more sustainable and economically attractive alternatives. They also reinforce models by enabling producers to extract greater value from their C4 streams, catering to specific demands in the Polyisobutylene Market or other specialty chemical sectors.

Furthermore, the drive towards circular economy principles is fostering R&D into converting C4 raffinate components, including the Refinery C4 Streams Market, into bio-based or recycled content derivatives. While still in nascent stages, this long-term trajectory seeks to decouple petrochemical production from fossil feedstocks, potentially transforming the C4 Raffinate Market's supply chain over the next 10-20 years. These innovations are crucial for maintaining competitiveness, improving environmental performance, and adapting to evolving market demands, particularly as the Petrochemicals Market shifts towards more sustainable practices."

"## Competitive Ecosystem of C4 Raffinate Market

Nouri Petrochemical Company: An Iranian petrochemical producer, integral to the regional supply chain of C4 derivatives, focusing on maximizing value from locally sourced feedstocks.

Faravaresh Bandar Imam Co: A key player in the Middle East's petrochemical sector, specializing in the production of various hydrocarbon derivatives, including those from C4 streams.

ONGC Mangalore Petrochemicals Ltd: An Indian petrochemical company, part of a larger oil and gas conglomerate, contributing to the domestic supply of C4 raffinate and its downstream products.

Buali Sina Petrochemical Co: Another significant Iranian producer, playing a strategic role in the Middle Eastern C4 Raffinate Market with capabilities in processing and distributing various chemical streams.

Braskem: A leading Brazilian petrochemical company with a strong presence in the Americas, known for its extensive range of polyolefins and other derivatives from C4 streams, impacting the global Polyisobutylene Market.

PT Chandra Asri Petrochemical, Tbk: An Indonesian petrochemical giant, crucial for supplying the Southeast Asian market with basic and intermediate chemicals derived from C4 raffinate.

TPC Group: A North American leader specializing in C4 processing, offering a broad portfolio of high-value C4 derivatives, including isobutylene, which feeds into the Isobutylene Market.

Shell Plc: A global energy and petrochemical company, operating large-scale steam crackers and refineries that generate substantial C4 raffinate, actively involved in its processing and distribution.

Reliance Industries Limited: An Indian multinational conglomerate, a major player in the global petrochemical industry with extensive cracking capacities, thus a significant producer and consumer of C4 raffinate.

Resonac Holdings Corporation: A prominent Japanese chemical company, contributing to the C4 Raffinate Market through its advanced material solutions and specialty chemical production.

BASF: A global chemical leader, operating integrated chemical sites worldwide, with significant involvement in the C4 value chain, producing a wide range of derivatives including those for the Synthetic Rubber Market.

JG summit Olefins Corporation: A key petrochemical producer in the Philippines, focused on supplying the domestic and regional markets with essential chemical building blocks from C4 streams.

Basparan Bandar Imam Co: An Iranian firm contributing to the Middle Eastern petrochemical landscape, with operations that encompass C4 stream management and derivative production.

Shimibaft Petrochemical Company: Another Iranian entity within the petrochemical sector, playing a role in the regional supply of C4 raffinate and its subsequent processing.

Royal Global Energy: A company engaged in the energy sector, potentially involved in refining or trading of C4 streams, influencing the Butane Market and broader C4 raffinate availability."

"## Recent Developments & Milestones in C4 Raffinate Market

February 2025: Several major petrochemical players announced plans for significant investments in new steam cracker facilities across Asia, particularly in China and India. These expansions are projected to substantially increase the global supply of crude C4 streams, thereby boosting the availability of C4 raffinate for downstream processing, addressing anticipated growth in the Petrochemicals Market.

October 2024: Breakthroughs in catalyst technology for the selective conversion of n-butane to butenes were reported by a consortium of European chemical companies. This development promises to enhance the efficiency of valorizing components from C4 raffinate, offering more flexible production pathways for key intermediates and potentially influencing the Butane Market dynamics.

June 2024: Several major refiners in North America initiated projects to upgrade their C4 processing capabilities, focusing on increasing the yield of high-purity isobutylene from Refinery C4 Streams Market. This strategic move aims to capitalize on the growing demand for specialty chemicals and derivatives, including those used in the Polyisobutylene Market.

March 2024: Industry leaders announced a joint initiative to explore sustainable pathways for C4 raffinate utilization, including pilot projects for converting C4 components into bio-based polymers and chemicals. This collaboration signals a growing emphasis on circular economy principles within the C4 Raffinate Market, aligning with broader environmental sustainability goals.

January 2024: A leading Asian petrochemical company commissioned a new plant specifically designed for the enhanced separation of 1-butene from C4 raffinate. This expansion is aimed at meeting the increasing demand for linear low-density polyethylene (LLDPE) co-monomers, highlighting the diverse applications and value extraction efforts within the C4 Raffinate Market.

November 2023: New regulatory frameworks in certain European nations imposed stricter guidelines on the use of specific C4 raffinate derivatives in industrial applications. While not a direct ban, these regulations are prompting producers to innovate and offer more environmentally compliant solutions, impacting the MTBE Market and pushing R&D towards greener alternatives."

"## Regional Market Breakdown for C4 Raffinate Market

The C4 Raffinate Market exhibits distinct regional dynamics, driven by varying industrial growth, feedstock availability, and regulatory landscapes. Asia Pacific currently dominates the global market with an estimated 45-50% revenue share, also emerging as the fastest-growing region with a projected CAGR of 10.5%. This robust expansion is fueled by massive investments in new petrochemical complexes and Steam Crackers Market capacity in countries like China, India, and Southeast Asian nations. The region's burgeoning automotive industry and rapid industrialization drive significant demand for C4 raffinate derivatives in the Synthetic Rubber Market, plastics, and fuels sectors.

North America constitutes a substantial portion of the market, holding approximately 20-25% revenue share, with an anticipated CAGR of 8.0%. The region benefits from abundant and cost-effective shale gas-derived C4 feedstocks, underpinning strong domestic production of C4 raffinate. Demand is primarily driven by the well-established Petrochemicals Market, gasoline blending for high-octane fuels (including derivatives for the MTBE Market), and a robust specialty chemicals industry. This is a mature market but continues to see steady growth due to feedstock advantages.

Europe, representing roughly 15-20% of the market, is characterized by a mature and stable growth trajectory, with an estimated CAGR of 7.5%. The region has a highly developed chemical industry with a strong focus on high-value specialty derivatives. Demand drivers include existing applications in elastomers and fuel additives, although environmental regulations have influenced the use of certain C4 raffinate derivatives. Innovation in sustainable processing and product development is a key regional trend.

Middle East & Africa is an emerging growth region, contributing about 10-15% of the market and poised for a CAGR of 9.8%. Growth here is largely propelled by significant investments in integrated refinery-petrochemical complexes, leveraging extensive domestic oil and gas resources. These developments aim to transform the region into a major exporter of C4 raffinate derivatives, serving global demand, particularly from the Butadiene Market and other C4 value chains. South America follows with a smaller share, around 5-8%, with an estimated CAGR of 8.5%, influenced by specific large-scale projects and domestic industrial demand.

C4 Raffinate Segmentation

1. Raffinate Grade

1.1. Raffinate-1 (R1)

1.2. Raffinate-2 (R2)

1.3. Raffinate-3 (R3)

2. Component Composition

2.1. n-Butane

2.2. Isobutane

2.3. 1-Butene

2.4. 2-Butene

2.5. Others

3. Source

3.1. Steam Crackers

3.2. Fluid Catalytic Cracking (FCC) Units

3.3. Refinery C4 Streams

4. Processing Stage

4.1. Raw C4 Raffinate

4.2. Hydrogenated Raffinate

4.3. Fractionated Raffinate

5. End-Use Industry

5.1. Oil & Gas / Refining

5.2. Petrochemical Industry

5.3. Automotive

5.4. Chemical Manufacturing

5.5. Energy & Power

5.6. Rubber & Plastics

5.7. Others

C4 Raffinate Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

C4 Raffinate REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 9.3% from 2020-2034

Segmentation

By Raffinate Grade

Raffinate-1 (R1)

Raffinate-2 (R2)

Raffinate-3 (R3)

By Component Composition

n-Butane

Isobutane

1-Butene

2-Butene

Others

By Source

Steam Crackers

Fluid Catalytic Cracking (FCC) Units

Refinery C4 Streams

By Processing Stage

Raw C4 Raffinate

Hydrogenated Raffinate

Fractionated Raffinate

By End-Use Industry

Oil & Gas / Refining

Petrochemical Industry

Automotive

Chemical Manufacturing

Energy & Power

Rubber & Plastics

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Raffinate Grade

5.1.1. Raffinate-1 (R1)

5.1.2. Raffinate-2 (R2)

5.1.3. Raffinate-3 (R3)

5.2. Market Analysis, Insights and Forecast - by Component Composition

5.2.1. n-Butane

5.2.2. Isobutane

5.2.3. 1-Butene

5.2.4. 2-Butene

5.2.5. Others

5.3. Market Analysis, Insights and Forecast - by Source

5.3.1. Steam Crackers

5.3.2. Fluid Catalytic Cracking (FCC) Units

5.3.3. Refinery C4 Streams

5.4. Market Analysis, Insights and Forecast - by Processing Stage

5.4.1. Raw C4 Raffinate

5.4.2. Hydrogenated Raffinate

5.4.3. Fractionated Raffinate

5.5. Market Analysis, Insights and Forecast - by End-Use Industry

5.5.1. Oil & Gas / Refining

5.5.2. Petrochemical Industry

5.5.3. Automotive

5.5.4. Chemical Manufacturing

5.5.5. Energy & Power

5.5.6. Rubber & Plastics

5.5.7. Others

5.6. Market Analysis, Insights and Forecast - by Region

5.6.1. North America

5.6.2. South America

5.6.3. Europe

5.6.4. Middle East & Africa

5.6.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Raffinate Grade

6.1.1. Raffinate-1 (R1)

6.1.2. Raffinate-2 (R2)

6.1.3. Raffinate-3 (R3)

6.2. Market Analysis, Insights and Forecast - by Component Composition

6.2.1. n-Butane

6.2.2. Isobutane

6.2.3. 1-Butene

6.2.4. 2-Butene

6.2.5. Others

6.3. Market Analysis, Insights and Forecast - by Source

6.3.1. Steam Crackers

6.3.2. Fluid Catalytic Cracking (FCC) Units

6.3.3. Refinery C4 Streams

6.4. Market Analysis, Insights and Forecast - by Processing Stage

6.4.1. Raw C4 Raffinate

6.4.2. Hydrogenated Raffinate

6.4.3. Fractionated Raffinate

6.5. Market Analysis, Insights and Forecast - by End-Use Industry

6.5.1. Oil & Gas / Refining

6.5.2. Petrochemical Industry

6.5.3. Automotive

6.5.4. Chemical Manufacturing

6.5.5. Energy & Power

6.5.6. Rubber & Plastics

6.5.7. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Raffinate Grade

7.1.1. Raffinate-1 (R1)

7.1.2. Raffinate-2 (R2)

7.1.3. Raffinate-3 (R3)

7.2. Market Analysis, Insights and Forecast - by Component Composition

7.2.1. n-Butane

7.2.2. Isobutane

7.2.3. 1-Butene

7.2.4. 2-Butene

7.2.5. Others

7.3. Market Analysis, Insights and Forecast - by Source

7.3.1. Steam Crackers

7.3.2. Fluid Catalytic Cracking (FCC) Units

7.3.3. Refinery C4 Streams

7.4. Market Analysis, Insights and Forecast - by Processing Stage

7.4.1. Raw C4 Raffinate

7.4.2. Hydrogenated Raffinate

7.4.3. Fractionated Raffinate

7.5. Market Analysis, Insights and Forecast - by End-Use Industry

7.5.1. Oil & Gas / Refining

7.5.2. Petrochemical Industry

7.5.3. Automotive

7.5.4. Chemical Manufacturing

7.5.5. Energy & Power

7.5.6. Rubber & Plastics

7.5.7. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Raffinate Grade

8.1.1. Raffinate-1 (R1)

8.1.2. Raffinate-2 (R2)

8.1.3. Raffinate-3 (R3)

8.2. Market Analysis, Insights and Forecast - by Component Composition

8.2.1. n-Butane

8.2.2. Isobutane

8.2.3. 1-Butene

8.2.4. 2-Butene

8.2.5. Others

8.3. Market Analysis, Insights and Forecast - by Source

8.3.1. Steam Crackers

8.3.2. Fluid Catalytic Cracking (FCC) Units

8.3.3. Refinery C4 Streams

8.4. Market Analysis, Insights and Forecast - by Processing Stage

8.4.1. Raw C4 Raffinate

8.4.2. Hydrogenated Raffinate

8.4.3. Fractionated Raffinate

8.5. Market Analysis, Insights and Forecast - by End-Use Industry

8.5.1. Oil & Gas / Refining

8.5.2. Petrochemical Industry

8.5.3. Automotive

8.5.4. Chemical Manufacturing

8.5.5. Energy & Power

8.5.6. Rubber & Plastics

8.5.7. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Raffinate Grade

9.1.1. Raffinate-1 (R1)

9.1.2. Raffinate-2 (R2)

9.1.3. Raffinate-3 (R3)

9.2. Market Analysis, Insights and Forecast - by Component Composition

9.2.1. n-Butane

9.2.2. Isobutane

9.2.3. 1-Butene

9.2.4. 2-Butene

9.2.5. Others

9.3. Market Analysis, Insights and Forecast - by Source

9.3.1. Steam Crackers

9.3.2. Fluid Catalytic Cracking (FCC) Units

9.3.3. Refinery C4 Streams

9.4. Market Analysis, Insights and Forecast - by Processing Stage

9.4.1. Raw C4 Raffinate

9.4.2. Hydrogenated Raffinate

9.4.3. Fractionated Raffinate

9.5. Market Analysis, Insights and Forecast - by End-Use Industry

9.5.1. Oil & Gas / Refining

9.5.2. Petrochemical Industry

9.5.3. Automotive

9.5.4. Chemical Manufacturing

9.5.5. Energy & Power

9.5.6. Rubber & Plastics

9.5.7. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Raffinate Grade

10.1.1. Raffinate-1 (R1)

10.1.2. Raffinate-2 (R2)

10.1.3. Raffinate-3 (R3)

10.2. Market Analysis, Insights and Forecast - by Component Composition

10.2.1. n-Butane

10.2.2. Isobutane

10.2.3. 1-Butene

10.2.4. 2-Butene

10.2.5. Others

10.3. Market Analysis, Insights and Forecast - by Source

10.3.1. Steam Crackers

10.3.2. Fluid Catalytic Cracking (FCC) Units

10.3.3. Refinery C4 Streams

10.4. Market Analysis, Insights and Forecast - by Processing Stage

10.4.1. Raw C4 Raffinate

10.4.2. Hydrogenated Raffinate

10.4.3. Fractionated Raffinate

10.5. Market Analysis, Insights and Forecast - by End-Use Industry

10.5.1. Oil & Gas / Refining

10.5.2. Petrochemical Industry

10.5.3. Automotive

10.5.4. Chemical Manufacturing

10.5.5. Energy & Power

10.5.6. Rubber & Plastics

10.5.7. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Nouri Petrochemical Company

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Faravaresh Bandar Imam Co

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. ONGC Mangalore Petrochemicals Ltd

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Buali Sina Petrochemical Co

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Braskem

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. PT Chandra Asri Petrochemical

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Tbk

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. TPC Group

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Shell Pic

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Reliance Industries Limited

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Resonac Holdings Corporation

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. BASF

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. JG summit Olefins Corporation

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.1.14. Basparan Bandar Imam Co

11.1.14.1. Company Overview

11.1.14.2. Products

11.1.14.3. Company Financials

11.1.14.4. SWOT Analysis

11.1.15. Shimibaft Petrochemical Company

11.1.15.1. Company Overview

11.1.15.2. Products

11.1.15.3. Company Financials

11.1.15.4. SWOT Analysis

11.1.16. Royal Global Energy

11.1.16.1. Company Overview

11.1.16.2. Products

11.1.16.3. Company Financials

11.1.16.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Raffinate Grade 2025 & 2033

Table 56: Revenue billion Forecast, by End-Use Industry 2020 & 2033

Table 57: Revenue billion Forecast, by Country 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Table 59: Revenue (billion) Forecast, by Application 2020 & 2033

Table 60: Revenue (billion) Forecast, by Application 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Revenue (billion) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our market research methodology places a strong emphasis on primary research, constituting 75% of our overall research efforts. This approach ensures that our findings are grounded in real-world perspectives and current market dynamics. We engage directly with key industry stakeholders across the value chain to validate secondary data, gather qualitative insights, and obtain proprietary market intelligence.

Key objectives of our primary research include:

Gaining insights into current market trends, challenges, and opportunities specific to C4 Raffinate grades, compositions, sources, and processing stages.

Validating demand and supply scenarios across various end-use industries and regional markets.

Understanding competitive landscapes, pricing dynamics, and technological advancements.

Collecting granular data points to inform our market size estimations and forecasts.

Our primary interviews target a diverse range of stakeholders through telephonic interviews, virtual meetings, and, where appropriate, in-person discussions. The participant breakdown includes, but is not limited to, the following specific company types and job designations:

Key Company Types Interviewed:

Integrated Oil & Gas Companies / Refiners

Petrochemical Producers (Downstream Derivatives)

Specialty Chemical Manufacturers (Intermediate Products)

Catalyst & Process Technology Providers

Bulk Chemical Distributors

Specific Job Titles/Stakeholders Interviewed:

Head of Feedstock Procurement / Supply Chain Director (Petrochemicals)

Specialty Chemical Manufacturers (Intermediate Products)

20%

Catalyst & Process Technology Providers

15%

Bulk Chemical Distributors

10%

Secondary Research & Industry Benchmarking

The remaining 25% of our research methodology is dedicated to comprehensive secondary research and industry benchmarking. This phase provides the foundational data, establishes initial market sizing, identifies key industry trends, and informs the structure of our primary research efforts. We meticulously analyze a broad spectrum of credible sources to ensure data veracity and relevance.

Our secondary research leverages a combination of proprietary databases and publicly available information, including:

Government & Regulatory Bodies: Official reports, statistics, and policies from relevant government agencies (.gov) [Source Link] and intergovernmental organizations (.org) [Source Link].

Trade Associations: Publications, annual reports, and industry statistics from globally recognized trade associations specific to the oil, gas, and petrochemical sectors. Examples include:

American Fuel & Petrochemical Manufacturers (AFPM) [Source Link]

European Chemical Industry Council (Cefic) [Source Link]

Gulf Petrochemicals and Chemicals Association (GPCA) [Source Link]

International Energy Agency (IEA) [Source Link]

Company Annual Reports & Investor Presentations: Financial statements, strategic reports, and corporate disclosures of public and private entities operating within the C4 Raffinate value chain.

Technical Journals & Conferences: Peer-reviewed articles, technical papers, and presentations from industry conferences to capture technological advancements and processing insights.

All secondary data is cross-referenced and validated to ensure accuracy before integration into our analysis. Our internal databases are continuously updated, ensuring that every report reflects the most current market conditions up to the date of purchase.

Demand Modeling & Market Estimation

Our market estimation framework employs a rigorous combination of top-down and bottom-up methodologies, complemented by multi-level data triangulation, to arrive at precise market figures. This holistic approach minimizes potential estimation errors and provides a robust forecast for the C4 Raffinate market from 2026 to 2034.

Bottom-Up Approach: This method involves segmenting the market at the most granular level, estimating demand and supply for each segment, and then aggregating these estimates to arrive at the overall market size. For the C4 Raffinate market, this includes:

Estimating market size based on individual C4 Raffinate grades (R1, R2, R3).

Calculating market volumes and values based on specific end-use industry consumption.

Key metrics and variables used for bottom-up calculation include:

Installed production capacity (kT/year) of C4-producing units (Steam Crackers, FCC units)

Average C4 raffinate yield rates (%) from these units

Average market price of C4 Raffinate (USD/MT) by grade (R1, R2, R3)

Consumption volumes (kT/year) by key downstream petrochemical derivative plants

Top-Down Approach: This method begins with a broad market estimate derived from macroeconomic indicators, industrial output data, and overall chemical market trends. This total market size is then disaggregated into various segments based on grade, composition, source, processing stage, end-use industry, and geographical regions (North America, South America, Europe, MEA, Asia Pacific).

Multi-Level Data Triangulation: To ensure the robustness of our market estimates, we cross-reference data points gathered from primary interviews, secondary research, and quantitative modeling. This iterative process allows us to reconcile discrepancies, refine assumptions, and build a cohesive and accurate market picture.

Data Accuracy & Quality Check

We are committed to delivering highly accurate and reliable market intelligence. Our stringent data validation processes ensure an estimated data accuracy level of 85-90%. Every data point, market estimate, and forecast undergoes multiple layers of quality checks.

This includes:

Cross-Validation: Data from primary interviews is rigorously cross-verified with information obtained from secondary sources and our internal databases.

Expert Review: All findings and market models are reviewed by internal subject matter experts with extensive experience in the petrochemical and refining industries.

Sensitivity Analysis: We perform sensitivity analysis on key market drivers and assumptions to assess their potential impact on the forecast and to provide a range of probable outcomes.

Iterative Refinement: Our methodology is iterative, allowing for continuous refinement of data and assumptions throughout the research lifecycle, ensuring that the final output is robust, coherent, and reflective of the current market reality.

This comprehensive approach guarantees that our market research report on C4 Raffinate provides clients with actionable insights based on highly dependable and validated data.

Frequently Asked Questions

1. What are the primary sources and supply chain aspects of C4 Raffinate?

C4 Raffinate is primarily sourced from steam crackers, fluid catalytic cracking (FCC) units, and refinery C4 streams. Its supply chain is integrated with the broader petrochemical and refining industries, making feedstock availability from these units critical.

2. What are the main challenges impacting the C4 Raffinate market?

The C4 Raffinate market faces challenges related to price volatility of crude oil and natural gas, which directly affect feedstock costs. Regulatory pressures on environmental emissions and the fluctuating demand from downstream industries also pose significant risks.

3. What is the projected market size and CAGR for C4 Raffinate through 2033?

The C4 Raffinate market is valued at $13.31 billion in 2025 and is projected to grow at a 9.3% CAGR. This indicates a potential market size exceeding $26 billion by 2033, reflecting robust demand across end-use industries.

4. How do sustainability and environmental factors influence C4 Raffinate production?

Sustainability concerns in C4 Raffinate production focus on energy efficiency in cracking processes and waste management. Companies are pressured to reduce greenhouse gas emissions and enhance resource utilization, impacting operational choices and investment in cleaner technologies.

5. Which region offers the most significant growth opportunities for C4 Raffinate?

Asia Pacific is expected to be a primary growth region due to rapid industrialization and expansion of the petrochemical industry, particularly in China and India. Emerging opportunities also exist in the Middle East with new investments in refining and chemical complexes.

6. What are the key barriers to entry and competitive advantages in the C4 Raffinate market?

Barriers to entry include high capital investment for petrochemical plants and the need for complex refining infrastructure. Established players like BASF, Reliance Industries, and Shell Pic possess significant competitive moats through integrated value chains, proprietary technologies, and established distribution networks.