Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Brewer’s Spent Grain by Source (Wheat, Barley, Rye, Others), by Form (Wet BSG, Dried BSG), by Application (Animal Feed, Food and Beverages, Biofuel Production, Biogas / Energy Generation, Fertilizers, Others), by Distribution Channel (Direct Sales, Online Sales, Offline), by End-User (Agriculture, Food Processing, Energy & Utilities, Pharmaceuticals & Nutraceuticals), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 4, 2026|Base Year : 2025|Pages : 114

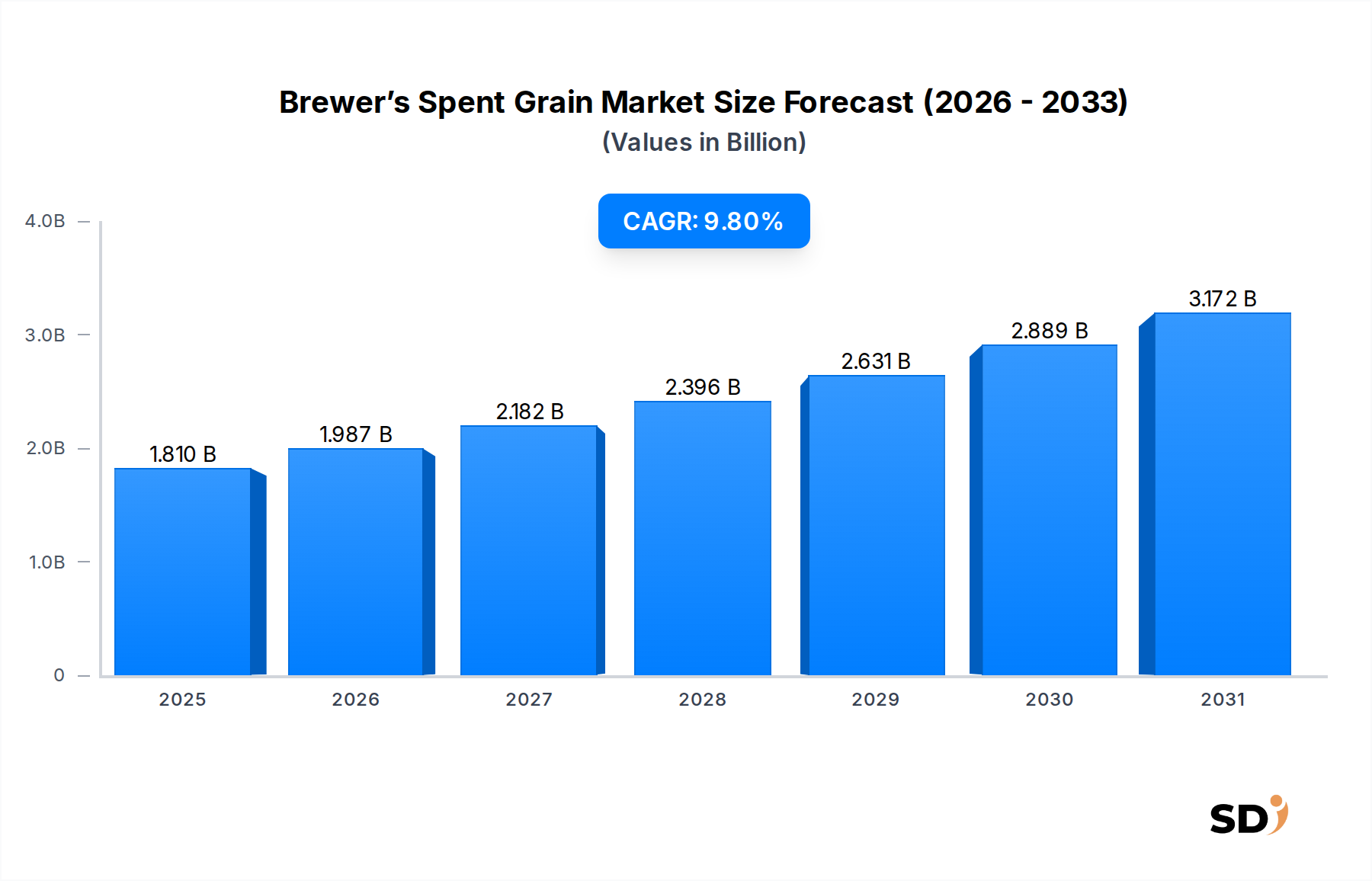

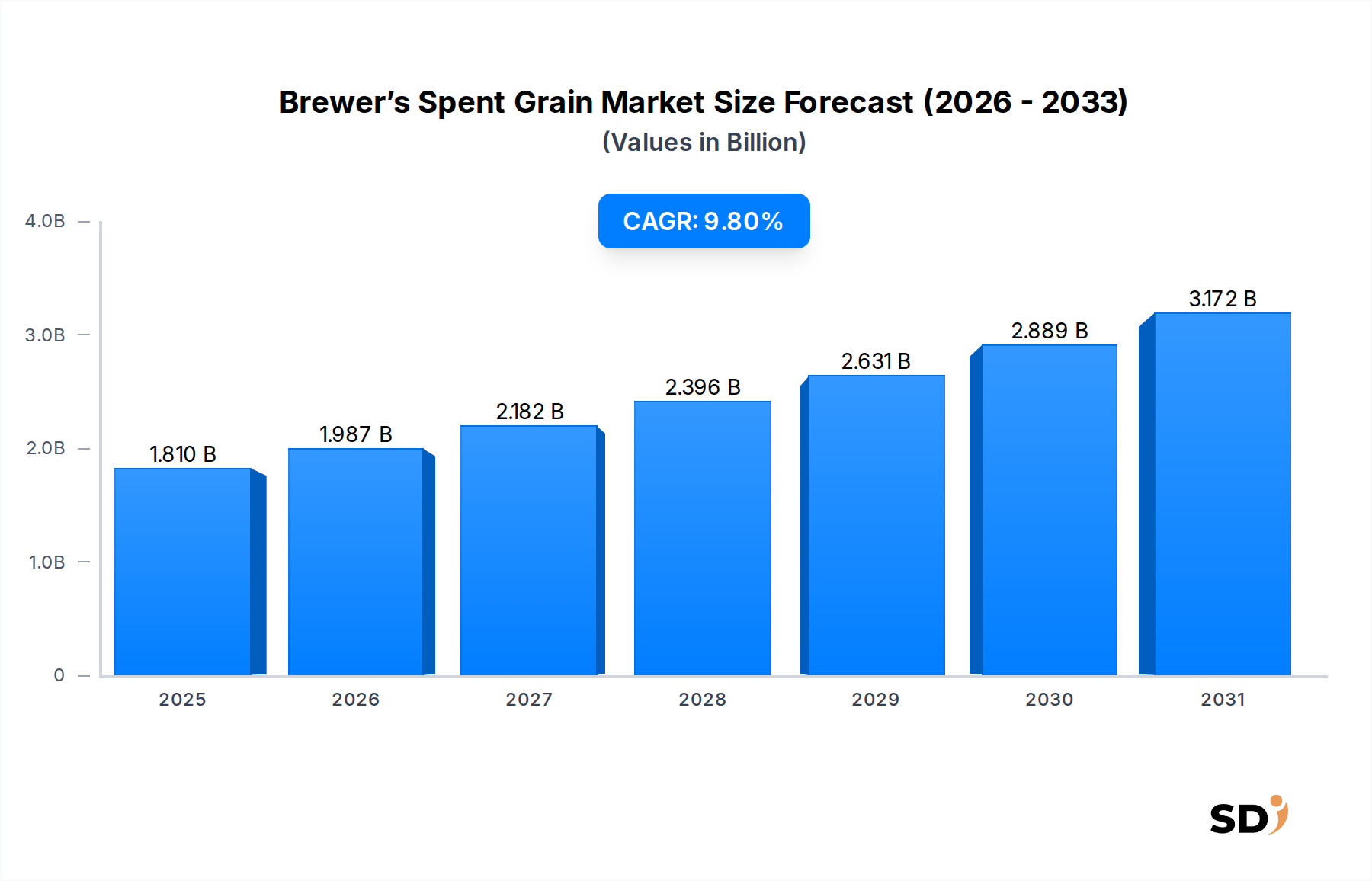

The global Brewer’s Spent Grain Market is currently valued at an impressive $1.81 billion in 2024, underscoring its significant role in the circular bio-economy. Projections indicate a robust expansion, with the market expected to reach approximately $4.59 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 9.8% over the forecast period. This substantial growth is primarily fueled by increasing awareness regarding industrial waste valorization, the surging demand for sustainable and cost-effective raw materials across various industries, and the inherent nutritional profile of brewer's spent grain (BSG).

Brewer’s Spent Grain Market Size (In Billion)

4.0B

3.0B

2.0B

1.0B

0

1.810 B

2025

1.987 B

2026

2.182 B

2027

2.396 B

2028

2.631 B

2029

2.889 B

2030

3.172 B

2031

Key demand drivers include the escalating need for alternative protein sources in the Animal Feed Market, the burgeoning interest in natural and fiber-rich ingredients within the Functional Food Ingredients Market, and the strategic pivot towards bio-based chemicals and energy production. The macro tailwinds supporting this market trajectory are multi-faceted, encompassing global efforts to reduce food waste, the economic attractiveness of transforming a low-value byproduct into high-value applications, and a supportive regulatory landscape that incentivizes sustainable industrial practices. Furthermore, advancements in processing technologies, such as enzymatic hydrolysis and drying techniques, are enhancing the versatility and stability of BSG, thereby expanding its potential applications in sectors like the Nutraceuticals Market and the Biofuel Market. The market is also benefiting from research into novel applications in areas like water filtration, bioplastics, and mushroom cultivation, signifying a broad spectrum of future growth avenues. This forward-looking outlook positions the Brewer’s Spent Grain Market as a critical component in achieving industrial sustainability and resource efficiency objectives globally.

The Dominant Animal Feed Segment in Brewer’s Spent Grain Market

Within the diverse application landscape of the Brewer’s Spent Grain Market, the Animal Feed segment stands out as the predominant force, commanding the largest revenue share globally. Historically, BSG has been a readily available and cost-effective byproduct of the brewing industry, making its integration into animal diets a logical and efficient pathway for valorization. This dominance stems from BSG's rich nutritional composition, which includes a substantial amount of protein (typically 15-25% on a dry matter basis), a high fiber content (30-70%), and essential minerals and vitamins. These attributes make it an excellent supplementary feed for various livestock, including cattle, poultry, swine, and even aquaculture. The high palatability and digestibility of BSG further enhance its appeal to feed manufacturers, offering a sustainable alternative to conventional, often more expensive, feed ingredients.

The global growth in meat and dairy consumption continues to exert pressure on the Animal Feed Market to find sustainable, affordable, and nutritious feed sources. Brewer's spent grain perfectly aligns with this demand, offering a readily available solution that mitigates feed costs for farmers while simultaneously addressing waste management challenges for breweries. Major players in the animal nutrition sector, such as DSM and Kerry Group plc, are actively involved in research and development to optimize BSG's inclusion rates and processing methods for various animal species. Companies like MGP Ingredients Inc., known for their grain-based products, also indirectly contribute to the valorization chain through their broader operations with grain byproducts. The segment's market share is not only significant but also demonstrating continued growth, driven by increasing awareness of its nutritional benefits and the logistical improvements in its collection and distribution. While the segment's share is substantial, it is not consolidating around a few players; rather, its growth is broad-based, supported by both large-scale industrial feed producers and local farm operations seeking cost efficiencies. The development of dried BSG variants has further extended the reach of this application, overcoming the limitations of spoilage and high transportation costs associated with wet BSG. This allows for wider distribution and integration into feed formulations across regions, cementing the Animal Feed Market as the undisputed leader in the Brewer’s Spent Grain Market.

Key Market Drivers & Constraints in Brewer’s Spent Grain Market

The Brewer’s Spent Grain Market is shaped by a confluence of potent drivers and discernible constraints, each influencing its growth trajectory. A primary driver is the accelerating global imperative for Sustainable Materials Market and circular economy principles. With breweries generating approximately 3.4 kg of BSG for every 100 liters of beer produced, amounting to millions of tons globally each year, the need for efficient valorization is immense. This focus on waste reduction and resource recovery, often supported by governmental policies and corporate sustainability goals, provides a powerful impetus for the market. For instance, the European Union’s Circular Economy Action Plan directly encourages the valorization of industrial byproducts like BSG, fostering investment in new processing technologies and applications.

Another significant driver is the high nutritional value of BSG, particularly its protein and fiber content. This makes it an attractive raw material for various applications beyond traditional feed. For example, specific enzymatic treatments can extract valuable proteins for the Functional Food Ingredients Market, addressing the rising consumer demand for plant-based proteins. Furthermore, the high fiber content, including both insoluble and soluble dietary fibers, positions BSG as a valuable ingredient for the Dietary Fiber Market, catering to health-conscious consumers. The cost-effectiveness of BSG as a byproduct, compared to virgin raw materials, offers an economic incentive for its adoption in these new applications, providing a competitive advantage.

However, several constraints temper this growth. The most prominent is the high moisture content of wet BSG (typically 75-80%), which leads to rapid spoilage and high transportation costs. This limits its immediate usability and mandates expensive and energy-intensive drying processes if it is to be stored, transported over long distances, or incorporated into dry formulations. The seasonal availability and regional concentration of BSG supply, dictated by brewing cycles and brewery locations, pose logistical challenges. Large-scale valorization requires a consistent supply chain, which can be difficult to establish and maintain, particularly for smaller breweries. Furthermore, the capital investment required for processing equipment—such as dryers, grinders, and bioreactors for advanced extraction—can be substantial, creating an entry barrier for some potential valorizers and impacting the overall economics of upcycling BSG for high-value applications beyond basic Animal Feed Market usage.

Competitive Ecosystem of Brewer’s Spent Grain Market

The competitive landscape of the Brewer’s Spent Grain Market features a blend of established ingredient manufacturers, brewing giants engaged in valorization, and specialized startups focusing on innovative applications. The market participants are increasingly investing in research and development to unlock new functionalities and improve processing efficiencies for BSG.

Malteurop: As a leading malt producer, Malteurop plays a foundational role in the brewing supply chain, indirectly influencing the availability and quality of Brewer’s Spent Grain through its malting processes. Its strategic position allows for potential integration into BSG valorization.

Anheuser-Busch Companies LLC: One of the world's largest brewers, Anheuser-Busch generates massive volumes of BSG. Its involvement often focuses on sustainable disposal or large-scale valorization projects, especially for animal feed or energy generation, driven by corporate sustainability goals.

MGP Ingredients Inc.: Specializing in distilled spirits and food ingredients, MGP Ingredients leverages its expertise in grain processing, making it a key player in converting grain byproducts, including BSG, into various valuable components for food, feed, and industrial applications.

DSM: A global science-based company in nutrition, health, and sustainable living, DSM is highly active in the animal nutrition and food ingredients sectors. Their involvement with Brewer’s Spent Grain often revolves around developing advanced feed additives or functional food components from its rich protein and fiber content.

Lallemand Inc.: As a global leader in the development, production, and marketing of yeasts and bacteria, Lallemand's expertise is crucial for fermentation processes. Their technologies can be applied to BSG for producing biofuels, Biogas Market, or other bio-based products through microbial conversion.

Leiber GmbH: A prominent German company specializing in yeast products and functional ingredients, Leiber often explores the use of brewing byproducts. Their focus is on high-quality extracts from yeast, which could extend to valorizing components derived from BSG for animal nutrition and human consumption.

Briess Malt & Ingredients: A major maltster and ingredient supplier, Briess provides raw materials to brewers, and thus interacts with the BSG byproduct stream. Their expertise in grain-based ingredients positions them well to develop new applications for Brewer’s Spent Grain.

Kerry Group plc: A global leader in taste and nutrition, Kerry Group is well-placed to incorporate Brewer’s Spent Grain derivatives into its extensive portfolio of food and Functional Food Ingredients Market. Their R&D efforts often focus on extracting high-value compounds for functional foods and beverages.

Bühler Group: A technology company providing solutions for food processing, Bühler Group offers machinery and processes vital for the efficient handling and transformation of raw materials, including BSG. Their equipment is critical for drying, milling, and further processing Brewer’s Spent Grain into stable forms.

ReGrained: A notable startup specifically focused on upcycling Brewer’s Spent Grain into nutritious food products. ReGrained exemplifies the innovation within the market, transforming BSG into flour and other ingredients for human consumption, aligning with the Sustainable Materials Market trend.

Recent Developments & Milestones in Brewer’s Spent Grain Market

Innovation and strategic collaborations are key drivers shaping the trajectory of the Brewer’s Spent Grain Market. These recent milestones highlight the ongoing efforts to enhance BSG's value proposition and expand its application spectrum:

February 2023: A leading research institution announced a breakthrough in enzymatic hydrolysis techniques for Brewer’s Spent Grain, significantly improving protein and fiber extraction yields, thus expanding potential applications in the Functional Food Ingredients Market.

June 2023: A major European consortium launched a pilot project demonstrating commercial-scale conversion of Brewer’s Spent Grain into advanced Biofuel Market precursors, showcasing significant circular economy potential and resource efficiency.

November 2023: An investment fund injected significant capital into a startup specializing in upcycling Brewer’s Spent Grain into high-quality protein concentrates, primarily targeting the burgeoning Nutraceuticals Market and specialized dietary supplements.

April 2024: New regulatory guidelines were introduced in a key Asian market to encourage the wider utilization of agricultural byproducts, including Brewer’s Spent Grain, in various Animal Feed Market formulations, promoting local resource use.

July 2024: A strategic partnership between a large brewery and an advanced processing technology firm led to the commissioning of a new facility dedicated to drying and milling Brewer’s Spent Grain, aiming to produce stable and shelf-ready ingredients for diverse industrial uses.

September 2024: Collaborative research identified novel applications for Brewer’s Spent Grain derivatives as a substrate for producing microbial enzymes, indicating potential for its integration into the Industrial Enzymes Market supply chain.

October 2024: Governments in several North American regions initiated grant programs to support the development of Sustainable Materials Market from agricultural waste, indirectly boosting research and commercialization efforts for Brewer’s Spent Grain.

December 2024: A new study published by a leading university showcased the efficacy of Brewer’s Spent Grain as a novel absorbent for heavy metals in wastewater treatment, opening a promising avenue for its use in environmental remediation.

Regional Market Breakdown for Brewer’s Spent Grain Market

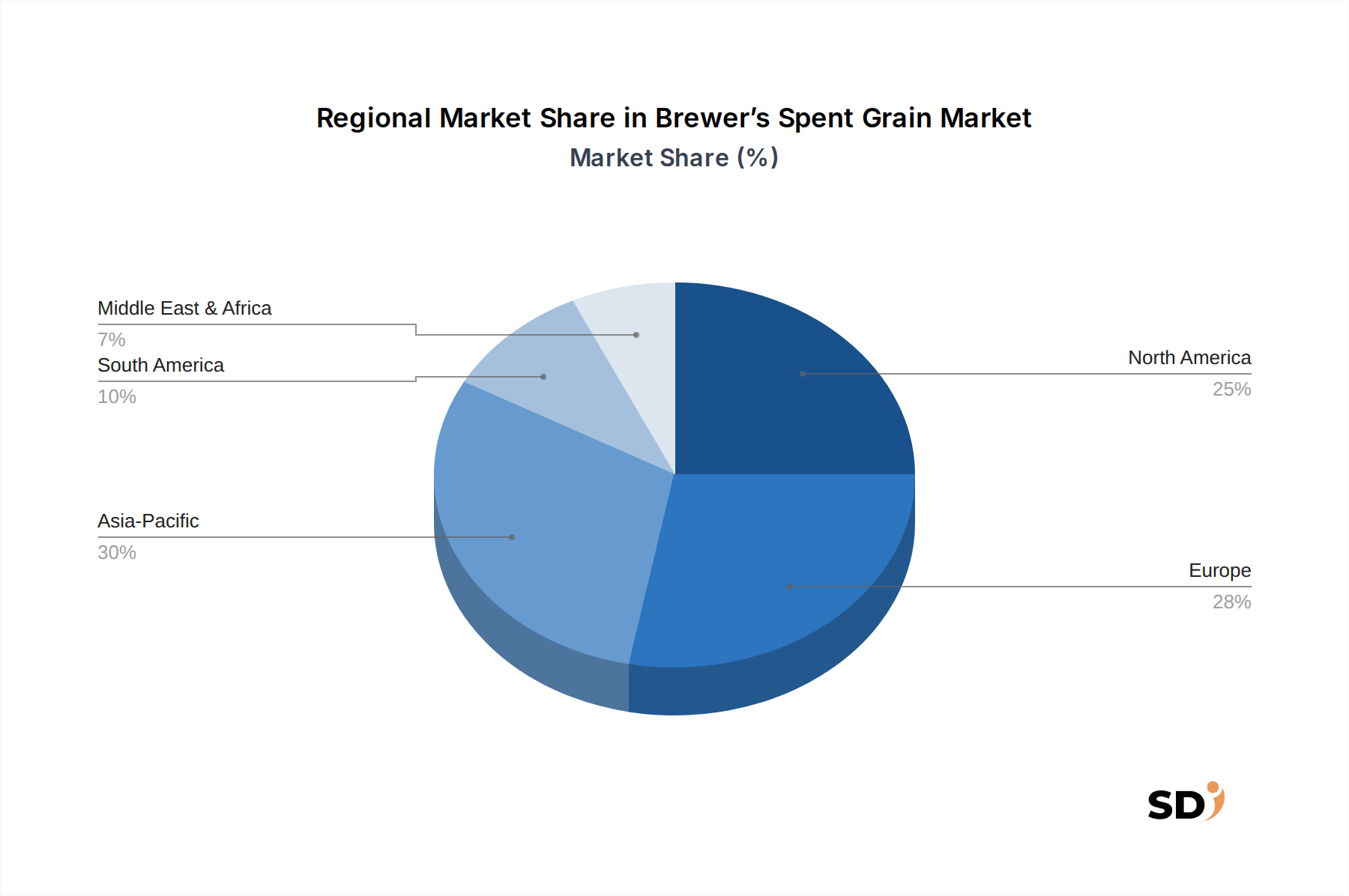

The Brewer’s Spent Grain Market exhibits distinct regional dynamics, influenced by varying brewing capacities, regulatory frameworks for waste management, and the maturity of bio-economy initiatives. Analyzing at least four key regions reveals a diverse landscape of growth and innovation.

Europe currently holds the largest revenue share in the Brewer’s Spent Grain Market, estimated at approximately 38%. This dominance is attributed to a long-standing and robust brewing tradition, coupled with stringent environmental regulations and strong governmental support for the circular economy. European countries, particularly Germany and the UK, have well-established infrastructure for collecting and processing BSG, driving its application primarily in the Animal Feed Market and increasingly in the Functional Food Ingredients Market. Research and development in Europe also heavily focus on extracting high-value compounds like proteins and the Dietary Fiber Market from BSG.

North America commands a significant market share, around 28%, fueled by a thriving craft brewing sector alongside major industrial breweries in the United States and Canada. The region demonstrates a strong demand for sustainable ingredients in both pet food and human food applications. The primary driver in North America is the growing consumer awareness regarding food waste and the increasing interest in natural, plant-based ingredients for the Nutraceuticals Market. The region also sees considerable investment in processing technologies to convert wet BSG into more stable and versatile forms.

Asia Pacific is projected to be the fastest-growing region in the Brewer’s Spent Grain Market, with an estimated CAGR of 11.5%. This rapid expansion is driven by the burgeoning beer consumption across countries like China and India, leading to a substantial increase in BSG availability. Furthermore, the region's rapidly expanding animal agriculture sector creates a massive demand for cost-effective feed ingredients, making BSG an attractive option for the Animal Feed Market. Government initiatives promoting resource efficiency and the development of local bio-industries further accelerate market growth in this region. While starting from a smaller base, the vast potential for industrial valorization and growing environmental consciousness position Asia Pacific as a key growth engine.

South America represents an emerging market with a moderate CAGR of approximately 9.0%. Countries like Brazil and Argentina have expanding brewing industries and significant livestock sectors, providing a natural fit for BSG utilization in the Animal Feed Market. However, the infrastructure for collection and advanced processing is still developing compared to more mature markets. Similarly, Middle East & Africa holds the smallest market share but shows promising growth potential (estimated at 8.5%) as brewing operations expand and food security concerns drive interest in local and sustainable feed sources. These regions represent future opportunities for basic valorization and, over time, more advanced applications.

Pricing Dynamics & Margin Pressure in Brewer’s Spent Grain Market

The pricing dynamics within the Brewer’s Spent Grain Market are inherently complex, largely dictated by its nature as a byproduct. Historically, wet BSG has often been considered a waste product, with breweries sometimes incurring disposal costs. This means the 'raw material' cost for wet BSG can range from negative (disposal fee paid by the brewery) to a nominal positive value for local collection. This low-cost or even negative-cost input provides a significant advantage for valorization efforts, driving interest in the Sustainable Materials Market.

However, the value-added journey of BSG introduces significant processing costs, which then dictate the average selling price (ASP) of derived products. Drying wet BSG to produce dried BSG, a more stable and transportable form, is a major cost lever. Energy costs associated with drying represent a substantial portion of the overall production expense. Further processing, such as milling, enzymatic hydrolysis, protein extraction, or fiber fractionation, adds incremental costs but also unlocks higher-value applications, commanding a higher ASP. For instance, BSG-derived protein isolates for the Nutraceuticals Market or specialized Functional Food Ingredients Market will naturally be priced significantly higher than bulk dried BSG for the Animal Feed Market.

Margin pressures in the Brewer’s Spent Grain Market stem from several factors. Firstly, competition from alternative feed ingredients or other plant-based proteins can cap the achievable prices for BSG derivatives. Secondly, the capital expenditure required for advanced processing equipment, such as large-scale dryers or bioreactors, demands a substantial return on investment, which can squeeze margins if end-product prices are not sufficiently high. Commodity cycles, particularly in energy markets, directly impact drying costs, and thus overall profitability. Furthermore, the logistics of collecting BSG from numerous, often dispersed, breweries add to operational costs. Companies like ReGrained, focusing on consumer-facing products, mitigate some of these pressures by adding brand value and targeting premium segments, while larger players like DSM or Kerry Group leverage their scale and existing distribution networks to optimize cost efficiencies across the value chain of Brewing Ingredients Market.

The export and trade flow dynamics for the Brewer’s Spent Grain Market are highly differentiated based on the form of the product. For wet BSG, cross-border trade is severely limited due to its high moisture content, which leads to rapid spoilage and prohibitively high transportation costs. Logistical challenges and the risk of microbial contamination restrict the trade of wet BSG almost exclusively to local or regional markets, typically within a few hundred kilometers of the brewery source. This localized distribution is common for direct sales to the Animal Feed Market and for use in Biogas Market facilities.

Conversely, dried BSG and high-value extracts, such as protein concentrates or fiber-rich flours, possess much greater potential for international trade. These processed forms are stable, have a significantly longer shelf life, and their reduced bulk makes long-distance shipping economically viable. Major trade corridors for these value-added BSG products are emerging between regions with high brewing activity and advanced processing capabilities (e.g., parts of Europe and North America) and demand centers in Asia Pacific, particularly for premium animal feed and Functional Food Ingredients Market. These trade flows involve companies like MGP Ingredients Inc. and DSM, which have global supply chains for various Brewing Ingredients Market and specialized food components.

Tariff and non-tariff barriers currently have a relatively subdued impact on the bulk Brewer’s Spent Grain Market. As an agricultural byproduct, BSG often falls under categories with low or zero tariffs in many trade agreements. However, this can change for more processed and refined derivatives. Non-tariff barriers, such as phytosanitary regulations, import quotas, or specific labeling requirements for novel food ingredients, pose a more significant challenge. For instance, health and safety standards for animal feed ingredients or specific certifications for the Nutraceuticals Market can create hurdles for cross-border movement. Recent trade policy shifts, while generally not targeting BSG directly, could indirectly affect its trade by influencing broader agricultural commodity flows or by creating new barriers for specific value-added ingredients. For example, increased protectionism on certain protein imports might inadvertently boost the domestic demand for BSG-derived proteins. Overall, the market for processed Brewer’s Spent Grain is poised for increasing international trade as its valorization becomes more sophisticated, necessitating careful navigation of diverse regulatory landscapes and potential future trade policy impacts.

Brewer’s Spent Grain Segmentation

1. Source

1.1. Wheat

1.2. Barley

1.3. Rye

1.4. Others

2. Form

2.1. Wet BSG

2.2. Dried BSG

3. Application

3.1. Animal Feed

3.2. Food and Beverages

3.3. Biofuel Production

3.4. Biogas / Energy Generation

3.5. Fertilizers

3.6. Others

4. Distribution Channel

4.1. Direct Sales

4.2. Online Sales

4.3. Offline

5. End-User

5.1. Agriculture

5.2. Food Processing

5.3. Energy & Utilities

5.4. Pharmaceuticals & Nutraceuticals

Brewer’s Spent Grain Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Brewer’s Spent Grain REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 9.8% from 2020-2034

Segmentation

By Source

Wheat

Barley

Rye

Others

By Form

Wet BSG

Dried BSG

By Application

Animal Feed

Food and Beverages

Biofuel Production

Biogas / Energy Generation

Fertilizers

Others

By Distribution Channel

Direct Sales

Online Sales

Offline

By End-User

Agriculture

Food Processing

Energy & Utilities

Pharmaceuticals & Nutraceuticals

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Source

5.1.1. Wheat

5.1.2. Barley

5.1.3. Rye

5.1.4. Others

5.2. Market Analysis, Insights and Forecast - by Form

5.2.1. Wet BSG

5.2.2. Dried BSG

5.3. Market Analysis, Insights and Forecast - by Application

5.3.1. Animal Feed

5.3.2. Food and Beverages

5.3.3. Biofuel Production

5.3.4. Biogas / Energy Generation

5.3.5. Fertilizers

5.3.6. Others

5.4. Market Analysis, Insights and Forecast - by Distribution Channel

5.4.1. Direct Sales

5.4.2. Online Sales

5.4.3. Offline

5.5. Market Analysis, Insights and Forecast - by End-User

5.5.1. Agriculture

5.5.2. Food Processing

5.5.3. Energy & Utilities

5.5.4. Pharmaceuticals & Nutraceuticals

5.6. Market Analysis, Insights and Forecast - by Region

5.6.1. North America

5.6.2. South America

5.6.3. Europe

5.6.4. Middle East & Africa

5.6.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Source

6.1.1. Wheat

6.1.2. Barley

6.1.3. Rye

6.1.4. Others

6.2. Market Analysis, Insights and Forecast - by Form

6.2.1. Wet BSG

6.2.2. Dried BSG

6.3. Market Analysis, Insights and Forecast - by Application

6.3.1. Animal Feed

6.3.2. Food and Beverages

6.3.3. Biofuel Production

6.3.4. Biogas / Energy Generation

6.3.5. Fertilizers

6.3.6. Others

6.4. Market Analysis, Insights and Forecast - by Distribution Channel

6.4.1. Direct Sales

6.4.2. Online Sales

6.4.3. Offline

6.5. Market Analysis, Insights and Forecast - by End-User

6.5.1. Agriculture

6.5.2. Food Processing

6.5.3. Energy & Utilities

6.5.4. Pharmaceuticals & Nutraceuticals

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Source

7.1.1. Wheat

7.1.2. Barley

7.1.3. Rye

7.1.4. Others

7.2. Market Analysis, Insights and Forecast - by Form

7.2.1. Wet BSG

7.2.2. Dried BSG

7.3. Market Analysis, Insights and Forecast - by Application

7.3.1. Animal Feed

7.3.2. Food and Beverages

7.3.3. Biofuel Production

7.3.4. Biogas / Energy Generation

7.3.5. Fertilizers

7.3.6. Others

7.4. Market Analysis, Insights and Forecast - by Distribution Channel

7.4.1. Direct Sales

7.4.2. Online Sales

7.4.3. Offline

7.5. Market Analysis, Insights and Forecast - by End-User

7.5.1. Agriculture

7.5.2. Food Processing

7.5.3. Energy & Utilities

7.5.4. Pharmaceuticals & Nutraceuticals

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Source

8.1.1. Wheat

8.1.2. Barley

8.1.3. Rye

8.1.4. Others

8.2. Market Analysis, Insights and Forecast - by Form

8.2.1. Wet BSG

8.2.2. Dried BSG

8.3. Market Analysis, Insights and Forecast - by Application

8.3.1. Animal Feed

8.3.2. Food and Beverages

8.3.3. Biofuel Production

8.3.4. Biogas / Energy Generation

8.3.5. Fertilizers

8.3.6. Others

8.4. Market Analysis, Insights and Forecast - by Distribution Channel

8.4.1. Direct Sales

8.4.2. Online Sales

8.4.3. Offline

8.5. Market Analysis, Insights and Forecast - by End-User

8.5.1. Agriculture

8.5.2. Food Processing

8.5.3. Energy & Utilities

8.5.4. Pharmaceuticals & Nutraceuticals

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Source

9.1.1. Wheat

9.1.2. Barley

9.1.3. Rye

9.1.4. Others

9.2. Market Analysis, Insights and Forecast - by Form

9.2.1. Wet BSG

9.2.2. Dried BSG

9.3. Market Analysis, Insights and Forecast - by Application

9.3.1. Animal Feed

9.3.2. Food and Beverages

9.3.3. Biofuel Production

9.3.4. Biogas / Energy Generation

9.3.5. Fertilizers

9.3.6. Others

9.4. Market Analysis, Insights and Forecast - by Distribution Channel

9.4.1. Direct Sales

9.4.2. Online Sales

9.4.3. Offline

9.5. Market Analysis, Insights and Forecast - by End-User

9.5.1. Agriculture

9.5.2. Food Processing

9.5.3. Energy & Utilities

9.5.4. Pharmaceuticals & Nutraceuticals

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Source

10.1.1. Wheat

10.1.2. Barley

10.1.3. Rye

10.1.4. Others

10.2. Market Analysis, Insights and Forecast - by Form

10.2.1. Wet BSG

10.2.2. Dried BSG

10.3. Market Analysis, Insights and Forecast - by Application

10.3.1. Animal Feed

10.3.2. Food and Beverages

10.3.3. Biofuel Production

10.3.4. Biogas / Energy Generation

10.3.5. Fertilizers

10.3.6. Others

10.4. Market Analysis, Insights and Forecast - by Distribution Channel

10.4.1. Direct Sales

10.4.2. Online Sales

10.4.3. Offline

10.5. Market Analysis, Insights and Forecast - by End-User

10.5.1. Agriculture

10.5.2. Food Processing

10.5.3. Energy & Utilities

10.5.4. Pharmaceuticals & Nutraceuticals

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Malteurop

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Anheuser-Busch Companies LLC

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. MGP Ingredients Inc.

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. DSM

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Lallemand Inc.

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Leiber GmbH

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Briess Malt & Ingredients

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Kerry Group plc

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Bühler Group

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. ReGrained

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Others

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Source 2025 & 2033

Figure 3: Revenue Share (%), by Source 2025 & 2033

Figure 4: Revenue (billion), by Form 2025 & 2033

Figure 5: Revenue Share (%), by Form 2025 & 2033

Figure 6: Revenue (billion), by Application 2025 & 2033

Figure 7: Revenue Share (%), by Application 2025 & 2033

Figure 8: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 9: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 10: Revenue (billion), by End-User 2025 & 2033

Figure 11: Revenue Share (%), by End-User 2025 & 2033

Figure 12: Revenue (billion), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (billion), by Source 2025 & 2033

Figure 15: Revenue Share (%), by Source 2025 & 2033

Figure 16: Revenue (billion), by Form 2025 & 2033

Figure 17: Revenue Share (%), by Form 2025 & 2033

Figure 18: Revenue (billion), by Application 2025 & 2033

Figure 19: Revenue Share (%), by Application 2025 & 2033

Figure 20: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 21: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 22: Revenue (billion), by End-User 2025 & 2033

Figure 23: Revenue Share (%), by End-User 2025 & 2033

Figure 24: Revenue (billion), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (billion), by Source 2025 & 2033

Figure 27: Revenue Share (%), by Source 2025 & 2033

Figure 28: Revenue (billion), by Form 2025 & 2033

Figure 29: Revenue Share (%), by Form 2025 & 2033

Figure 30: Revenue (billion), by Application 2025 & 2033

Figure 31: Revenue Share (%), by Application 2025 & 2033

Figure 32: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 33: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 34: Revenue (billion), by End-User 2025 & 2033

Figure 35: Revenue Share (%), by End-User 2025 & 2033

Figure 36: Revenue (billion), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Revenue (billion), by Source 2025 & 2033

Figure 39: Revenue Share (%), by Source 2025 & 2033

Figure 40: Revenue (billion), by Form 2025 & 2033

Figure 41: Revenue Share (%), by Form 2025 & 2033

Figure 42: Revenue (billion), by Application 2025 & 2033

Figure 43: Revenue Share (%), by Application 2025 & 2033

Figure 44: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 45: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 46: Revenue (billion), by End-User 2025 & 2033

Figure 47: Revenue Share (%), by End-User 2025 & 2033

Figure 48: Revenue (billion), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Revenue (billion), by Source 2025 & 2033

Figure 51: Revenue Share (%), by Source 2025 & 2033

Figure 52: Revenue (billion), by Form 2025 & 2033

Figure 53: Revenue Share (%), by Form 2025 & 2033

Figure 54: Revenue (billion), by Application 2025 & 2033

Figure 55: Revenue Share (%), by Application 2025 & 2033

Figure 56: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 57: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 58: Revenue (billion), by End-User 2025 & 2033

Figure 59: Revenue Share (%), by End-User 2025 & 2033

Figure 60: Revenue (billion), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Source 2020 & 2033

Table 2: Revenue billion Forecast, by Form 2020 & 2033

Table 3: Revenue billion Forecast, by Application 2020 & 2033

Table 4: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 5: Revenue billion Forecast, by End-User 2020 & 2033

Table 6: Revenue billion Forecast, by Region 2020 & 2033

Table 7: Revenue billion Forecast, by Source 2020 & 2033

Table 8: Revenue billion Forecast, by Form 2020 & 2033

Table 9: Revenue billion Forecast, by Application 2020 & 2033

Table 10: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 11: Revenue billion Forecast, by End-User 2020 & 2033

Table 12: Revenue billion Forecast, by Country 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue (billion) Forecast, by Application 2020 & 2033

Table 15: Revenue (billion) Forecast, by Application 2020 & 2033

Table 16: Revenue billion Forecast, by Source 2020 & 2033

Table 17: Revenue billion Forecast, by Form 2020 & 2033

Table 18: Revenue billion Forecast, by Application 2020 & 2033

Table 19: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 20: Revenue billion Forecast, by End-User 2020 & 2033

Table 21: Revenue billion Forecast, by Country 2020 & 2033

Table 22: Revenue (billion) Forecast, by Application 2020 & 2033

Table 23: Revenue (billion) Forecast, by Application 2020 & 2033

Table 24: Revenue (billion) Forecast, by Application 2020 & 2033

Table 25: Revenue billion Forecast, by Source 2020 & 2033

Table 26: Revenue billion Forecast, by Form 2020 & 2033

Table 27: Revenue billion Forecast, by Application 2020 & 2033

Table 28: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 29: Revenue billion Forecast, by End-User 2020 & 2033

Table 30: Revenue billion Forecast, by Country 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue (billion) Forecast, by Application 2020 & 2033

Table 37: Revenue (billion) Forecast, by Application 2020 & 2033

Table 38: Revenue (billion) Forecast, by Application 2020 & 2033

Table 39: Revenue (billion) Forecast, by Application 2020 & 2033

Table 40: Revenue billion Forecast, by Source 2020 & 2033

Table 41: Revenue billion Forecast, by Form 2020 & 2033

Table 42: Revenue billion Forecast, by Application 2020 & 2033

Table 43: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 44: Revenue billion Forecast, by End-User 2020 & 2033

Table 45: Revenue billion Forecast, by Country 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Revenue (billion) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Revenue (billion) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Revenue billion Forecast, by Source 2020 & 2033

Table 53: Revenue billion Forecast, by Form 2020 & 2033

Table 54: Revenue billion Forecast, by Application 2020 & 2033

Table 55: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 56: Revenue billion Forecast, by End-User 2020 & 2033

Table 57: Revenue billion Forecast, by Country 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Table 59: Revenue (billion) Forecast, by Application 2020 & 2033

Table 60: Revenue (billion) Forecast, by Application 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Revenue (billion) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is designed to gather direct, first-hand information from key stakeholders across the Brewer's Spent Grain (BSG) market value chain. This robust approach constitutes approximately 75% of our total research efforts, ensuring a deep, nuanced understanding of market dynamics, emerging trends, competitive landscapes, and future growth prospects. We conduct extensive qualitative and quantitative interviews, primarily through telephone and virtual meetings, supplemented by in-person discussions where feasible.

Key stakeholders targeted for primary interviews include:

Brewery Operations Manager: Providing insights into BSG production volumes, disposal methods, initial processing, and current valorization practices.

Procurement Director, Animal Nutrition: Offering perspectives on BSG demand, quality requirements, pricing, and supply chain intricacies within the animal feed sector.

Head of R&D, Food Ingredients: Detailing innovation, product development, regulatory challenges, and consumer acceptance for BSG-derived food and beverage applications.

Biofuel Plant Manager: Explaining operational efficiencies, technology adoption, and feedstock requirements for BSG utilization in biofuel and biogas production.

Participants are carefully selected from various company types to ensure comprehensive market representation. These include:

Craft & Commercial Breweries (primary producers of BSG)

Novel Food Ingredient Developers (innovators in the food & beverages sector)

Biorefinery & Biofuel Companies (key players in renewable energy applications)

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Brewery Operations Manager

30%

Procurement Director, Animal Nutrition

30%

Head of R&D, Food Ingredients

25%

Biofuel Plant Manager

15%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Craft & Commercial Breweries

35%

BSG Collection & Processing Companies

20%

Animal Nutrition/Feed Manufacturers

25%

Novel Food Ingredient Developers

10%

Biorefinery & Biofuel Companies

10%

Secondary Research & Industry Benchmarking

Secondary research forms the remaining 25% of our methodology, providing foundational data, market validation, and industry benchmarking. This phase involves a rigorous review of published literature, regulatory frameworks, company reports, and credible industry statistics. Our analysts meticulously extract relevant data points, market trends, technological advancements, and policy changes to build a comprehensive market overview.

Key sources utilized include:

Financial Databases: Bloomberg, Factiva, Hoovers, and PitchBook for company profiles, financial performance, mergers & acquisitions, and investment trends.

Government Publications: Official reports from national agricultural departments, environmental agencies, and economic ministries (e.g., USDA, European Commission).

Trade Associations & Industry Bodies: Reports and statistics from organizations such as the Brewers Association (https://www.brewersassociation.org), European Feed Manufacturers' Federation (FEFAC) (https://www.fefac.eu), Food and Agriculture Organization of the United Nations (FAO) (https://www.fao.org), and the European Biogas Association (EBA) (https://www.europeanbiogas.eu). These sources provide crucial data on production volumes, consumption patterns, regulatory landscapes, and sustainability initiatives specific to brewing, animal nutrition, and bio-economy sectors.

Academic Journals & Research Papers: Peer-reviewed studies on BSG valorization technologies, nutritional properties, and environmental impacts.

We strictly avoid using data from other market research websites to maintain the independence and integrity of our findings. Every report is meticulously updated with the latest available information up to the date of purchase, ensuring relevance and timeliness.

Demand Modeling & Market Estimation

Our market estimation employs a sophisticated blend of top-down and bottom-up methodologies, complemented by multi-level data triangulation, to ensure robust and accurate market sizing and forecasting. This approach allows for cross-validation of data points and minimizes potential biases.

Bottom-up Approach: This involves aggregating granular data points from the ground up.

Key metrics and variables used for bottom-up calculation include:

Regional beer production volumes (e.g., in hectoliters) as the primary source of BSG.

Average spent grain yield per hectoliter of beer produced, differentiated by grain type (wheat, barley, rye).

Value-added processing rates for dried/modified BSG ingredients across various forms and applications.

Pricing variations across different BSG forms (wet vs. dried) and end-use applications (animal feed, food, biofuel).

We estimate market size by multiplying calculated BSG volumes (derived from beer production and yield rates) by average selling prices for each application and form, then summing these values across all segments and regions.

Top-down Approach: This involves validating the bottom-up estimates by evaluating the overall market potential based on macroeconomic indicators, industry growth rates, and broad market trends.

Data Triangulation: The final market figures are arrived at through triangulation of data obtained from primary interviews, secondary research, and quantitative modeling. This process involves comparing and cross-referencing data from multiple sources to identify inconsistencies, resolve discrepancies, and arrive at the most reliable market estimates.

Data Accuracy & Quality Check

Our commitment to data integrity and accuracy is paramount. We guarantee an estimated data accuracy level of 88-90% for our market figures and forecasts. This high level of precision is achieved through a multi-stage quality assurance process:

Source Validation: All primary and secondary data sources are rigorously vetted for credibility, relevance, and timeliness.

Interviewer Bias Mitigation: Our interviewers are trained to conduct unbiased discussions, employing structured questionnaires to ensure consistency and comparability of responses.

Statistical Analysis: Quantitative data is subjected to advanced statistical analysis, including regression analysis, correlation studies, and trend forecasting, to identify patterns and predict future market behavior.

Expert Panel Review: Draft findings and market estimates are reviewed by an internal panel of senior analysts and external industry experts to challenge assumptions and refine conclusions.

Continuous Updating: As a standard practice, our reports are updated with the latest market developments and data points right up to the date of purchase, ensuring clients receive the most current and relevant information for their strategic decisions.

Frequently Asked Questions

1. What recent developments influence the Brewer's Spent Grain market?

Recent trends focus on valorization of Brewer’s Spent Grain into new food ingredients and sustainable animal feed. Companies such as ReGrained are developing innovative products, while Bühler Group provides processing solutions. These efforts aim to reduce waste and create value from a brewing byproduct.

2. Which key applications drive the Brewer’s Spent Grain market?

The Brewer’s Spent Grain market is primarily driven by its applications in animal feed, food and beverages, and biofuel production. Minor applications include biogas/energy generation and fertilizers, diversifying its end-user value. This multi-sector utility supports its projected 9.8% CAGR.

3. How do pricing trends impact the Brewer’s Spent Grain market?

Pricing for Brewer’s Spent Grain is influenced by processing costs, especially for drying (Wet BSG vs. Dried BSG), and the demand from end-user sectors like animal feed and food. As a byproduct, its value often reflects the cost-effectiveness of alternative ingredients, fostering market growth through competitive pricing strategies.

4. Why is Asia-Pacific a leading region in the Brewer’s Spent Grain market?

Asia-Pacific is a leading region for Brewer’s Spent Grain due to a large and expanding brewing industry, coupled with growing awareness of byproduct valorization. Countries like China and India contribute significantly through both large-scale breweries and emerging craft sectors. This creates substantial supply and demand for BSG applications, driving its estimated 0.30 market share.

5. What regulatory factors influence the Brewer’s Spent Grain market?

The Brewer’s Spent Grain market is subject to regulations concerning food safety, animal feed standards, and waste management. Compliance with regional food and drug administrations, such as those in the United States and Europe, is critical for companies utilizing BSG in food and beverage products. These standards ensure product quality and safety across the supply chain.

6. What are the primary growth drivers for the Brewer’s Spent Grain market?

The primary growth drivers include increasing global beer production, rising demand for sustainable animal feed, and expansion of circular economy principles in the food industry. Its utility in diverse applications like food & beverages and biofuel production further propels the market, contributing to a 9.8% CAGR from 2024 to 2034.