Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Blue Methanol Market: $34.16B by 2033? Growth Drivers Analyzed

Blue Methanol

Blue Methanol Market: $34.16B by 2033? Growth Drivers Analyzed

Blue Methanol by Feedstock (Natural Gas, Coal, Renewable, Others), by Application (Marine Fuel, Chemical Feedstock, Power Generation, Road Transport Fuel, Industrial Solvents, Others), by End-User Industry (Chemicals & Petrochemicals, Energy & Power, Automotive & Transportation, Industrial Manufacturing, Shipping & Maritime Industry, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 3, 2026|Base Year : 2025|Pages : 87

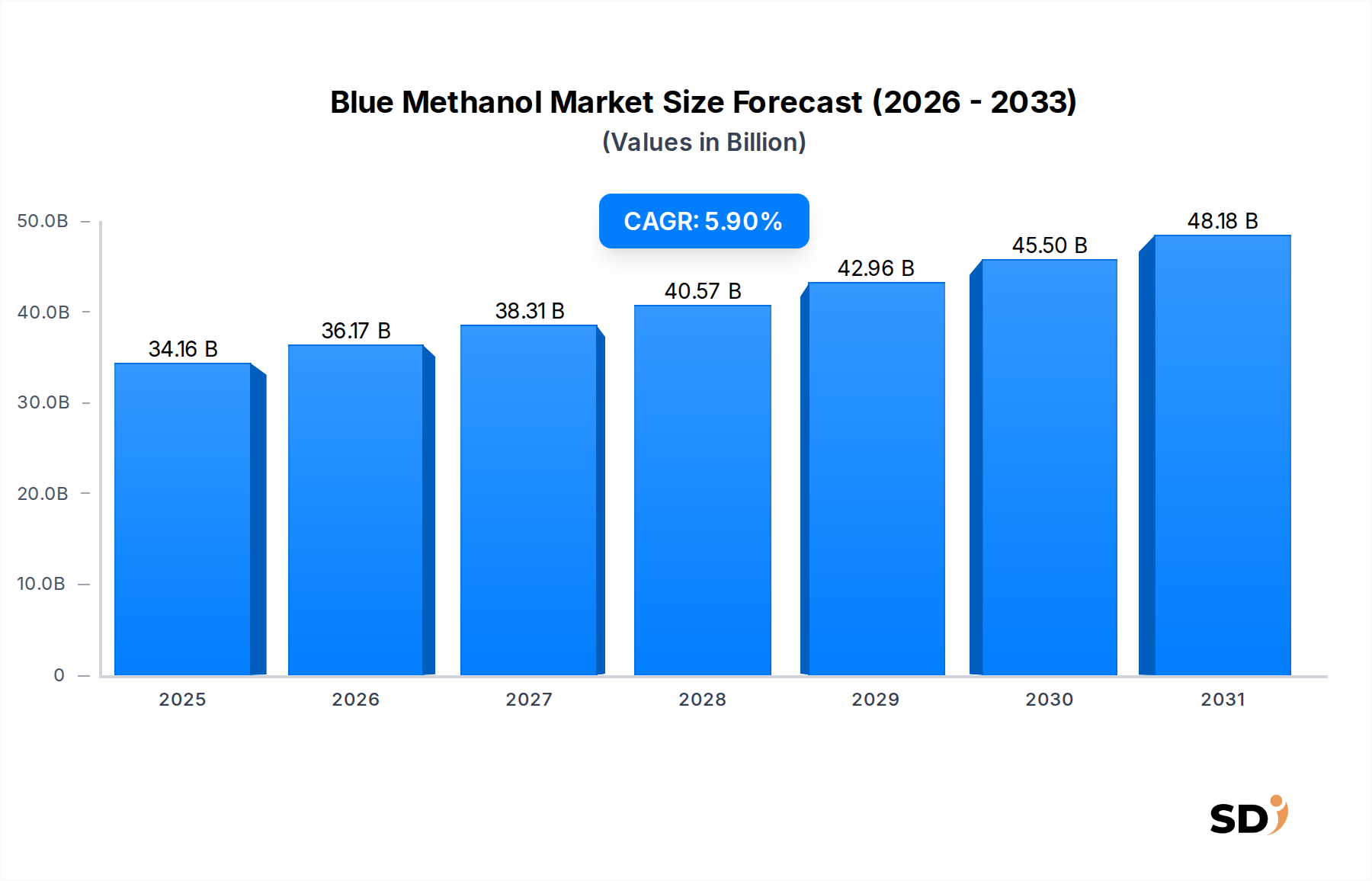

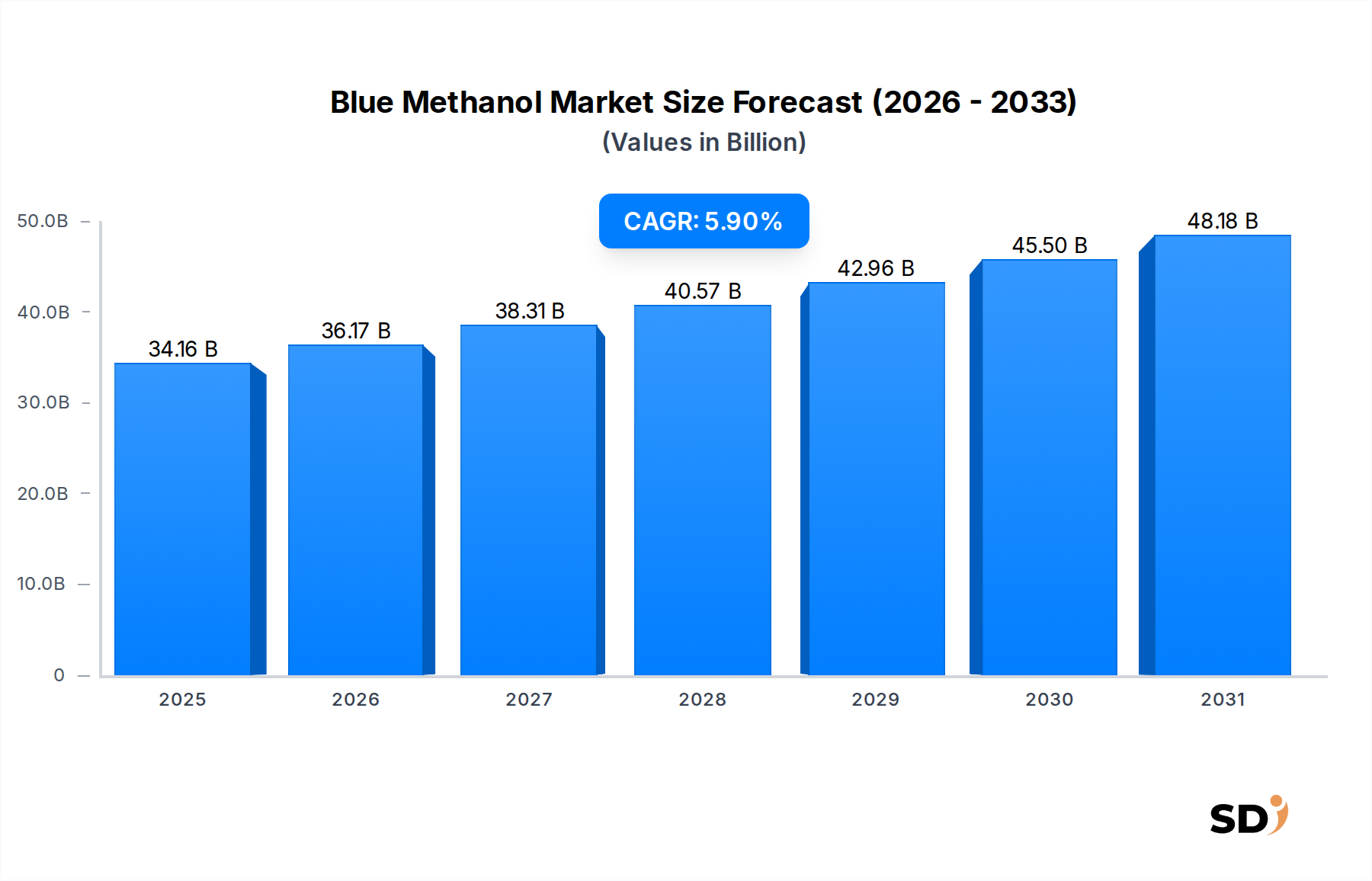

The global Blue Methanol Market is positioned for robust expansion, driven by accelerating decarbonization mandates across various industrial sectors. Valued at 34.16 billion USD in 2025, the market is projected to reach approximately 54.56 billion USD by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 5.9% during the forecast period. Blue methanol, produced from natural gas with integrated Carbon Capture & Storage (CCS) technology, offers a lower-carbon alternative to conventional grey methanol, making it a critical bridge fuel in the energy transition.

Blue Methanol Market Size (In Billion)

50.0B

40.0B

30.0B

20.0B

10.0B

0

34.16 B

2025

36.17 B

2026

38.31 B

2027

40.57 B

2028

42.96 B

2029

45.50 B

2030

48.18 B

2031

The primary demand drivers for blue methanol stem from the urgent need to reduce greenhouse gas emissions in hard-to-abate sectors. The shipping and maritime industries, facing stringent IMO 2030 and 2050 targets, are increasingly exploring methanol as a viable marine fuel, significantly boosting the Marine Fuel Market. Concurrently, the Chemical Feedstock Market, traditionally a major consumer of methanol, is transitioning towards sustainable feedstocks to align with corporate sustainability goals and regulatory pressures. Furthermore, advancements in Carbon Capture & Storage Market technologies are bolstering the economic viability and environmental credibility of blue methanol production.

Macro tailwinds include heightened global climate action, substantial governmental incentives for low-carbon hydrogen and CCS projects, and increasing corporate investment in sustainable chemical value chains. The growing recognition of blue methanol's role in complementing the nascent Green Methanol Market, which relies on renewable energy sources and biogenic CO2, underscores its strategic importance. While the initial capital expenditure for CCS infrastructure remains a hurdle, ongoing technological refinements and scaling efforts are expected to mitigate these costs. The future outlook for the Blue Methanol Market remains highly positive, as it provides a readily implementable solution for immediate emissions reductions, leveraging existing infrastructure and feedstock supplies from the Natural Gas Market, thereby paving the way for a more sustainable global energy and chemicals landscape.

Chemical Feedstock Segment Dominance in Blue Methanol Market

The Chemical Feedstock Market segment currently holds the largest revenue share within the global Blue Methanol Market, primarily due to methanol's established role as a fundamental building block in the chemical industry. Methanol is an indispensable raw material for producing a vast array of chemicals, including formaldehyde, acetic acid, MTBE, DME, and various olefins, all of which are crucial for numerous downstream industries. The transition from conventional grey methanol to blue methanol in this segment is driven by major chemical producers aiming to decarbonize their supply chains and product portfolios without significantly altering existing production processes or compromising product quality. Blue methanol acts as a drop-in replacement, facilitating a relatively smooth integration into established chemical synthesis routes.

This segment's dominance is further reinforced by the sheer volume of methanol consumed annually by the chemical sector. As corporations and governments worldwide commit to more ambitious climate targets, the demand for lower-carbon feedstocks like blue methanol is escalating. Key players in this space, including companies with significant petrochemical footprints, are actively investing in or partnering for blue methanol supply. For instance, Methanex Corporation, a global leader in methanol production, is exploring avenues for lower-carbon methanol, including blue options. Similarly, SABIC and Celanese Corporation, major chemical producers, are driven by their sustainability mandates to explore cleaner feedstocks. BASF SE, another chemical giant, integrates methanol extensively into its value chain and is a natural fit for blue methanol adoption.

While the Marine Fuel Market is rapidly emerging as a high-growth application for blue methanol, the established, large-scale, and diverse demand from the Chemical Feedstock Market provides a stable foundation for the blue methanol industry. The growth in the Chemical Feedstock Market is characterized not only by replacing grey methanol but also by the expansion of existing chemical production capacity and the development of new methanol-derived products that require a reduced carbon footprint. The ability to leverage existing infrastructure for methanol synthesis and distribution also gives the chemical feedstock application an advantage. Although the initial capital investment in Carbon Capture & Storage technology can be substantial for blue methanol plants, the long-term strategic benefits of meeting decarbonization targets and securing market share in a carbon-constrained economy justify these investments for leading chemical players, thus ensuring the continued dominance and expansion of blue methanol within the Chemical Feedstock Market.

Decarbonization Mandates & CCS Advancements Driving the Blue Methanol Market

The Blue Methanol Market's growth is predominantly propelled by stringent decarbonization mandates and significant advancements in Carbon Capture & Storage (CCS) technologies. Global legislative and corporate commitments to net-zero emissions, such as the EU's Green Deal and the IMO's revised GHG strategy targeting a 20% reduction in shipping emissions by 2030 and 70% by 2040, are creating an imperative for lower-carbon fuels and chemical feedstocks. For instance, the demand for cleaner marine fuels is projected to grow by an estimated 30-40% by 2030 as shipping companies convert existing fleets or order new methanol-fueled vessels, directly stimulating the Marine Fuel Market.

A key driver is the increasing efficacy and economic viability of CCS solutions. Innovations in capture technologies, including advanced sorbents and membrane separation, are lowering the energy penalty and operational costs associated with CO2 capture from industrial flue gases. Large-scale CCS projects, such as those in the North Sea and Gulf Coast regions, are demonstrating the technical feasibility and scalability of safely storing captured CO2, providing the critical infrastructure required for blue methanol production. The Global CCS Institute reported that over 150 new commercial CCS facilities were in various stages of development globally by 2023, representing a substantial increase in potential capacity for the Blue Methanol Market. This expansion is vital as it directly addresses the 'blue' component of blue methanol, ensuring a significantly reduced carbon footprint compared to conventional production methods that rely solely on the Natural Gas Market as a feedstock.

Furthermore, government policies offering tax credits, grants, and carbon pricing mechanisms for CCS deployment are providing crucial financial incentives. For example, the 45Q tax credit in the United States offers up to 85 USD per tonne of CO2 stored, significantly improving the economic calculus for blue methanol projects. These policies not only de-risk investments in CCS but also narrow the cost gap between blue methanol and its grey counterpart, making blue methanol a more competitive and attractive option for industries aiming to reduce their carbon intensity, particularly within the Chemical Feedstock Market and the broader Power Generation Market for clean energy applications.

Competitive Ecosystem of Blue Methanol Market

BASF SE: A global chemical giant deeply involved in the production and consumption of methanol for various downstream products, actively exploring sustainable pathways for its chemical value chain, including blue methanol.

OCI N.V.: A leading global producer and distributor of nitrogen fertilizers and methanol, focusing on decarbonization initiatives through its "clean fuels" platform, which includes significant investments in blue and green methanol projects.

Mitsubishi Gas Chemical Company Inc.: A key player in the Japanese chemical sector with substantial methanol production capacity, increasingly focused on developing and implementing low-carbon methanol solutions to meet regional environmental targets.

Celanese Corporation: A technology and specialty materials company with a significant methanol-to-chemicals footprint, driven by corporate sustainability goals to source and produce lower-carbon feedstocks.

Methanex Corporation: The world's largest producer and supplier of methanol, strategically positioned to leverage its extensive production network for blue methanol opportunities as demand for low-carbon fuels and chemicals grows.

SABIC: A prominent diversified manufacturing company active in petrochemicals, exploring various sustainability initiatives, including the adoption of blue methanol to reduce the carbon footprint of its vast product portfolio.

Proman AG: A major player in the global methanol industry, actively developing and operating integrated methanol and petrochemical facilities, with a strong focus on advancing lower-carbon methanol production technologies.

Methanol Holdings Trinidad Limited: A key producer in the Caribbean, leveraging its access to natural gas feedstock, with potential to integrate CCS technologies to produce blue methanol for global export markets.

Atlantic Methanol Production Company LLC: A significant methanol producer in North America, well-positioned to capitalize on regional natural gas supplies and emerging CCS infrastructure to serve the evolving Blue Methanol Market.

Recent Developments & Milestones in Blue Methanol Market

May 2025: A major European consortium announced plans for a large-scale blue methanol production facility in the Netherlands, integrating CO2 capture from a local industrial cluster, targeting production capacity of 500,000 tonnes per year by 2029 to supply the Marine Fuel Market.

November 2024: A North American energy firm partnered with a leading CCS technology provider to commence a feasibility study for a blue methanol plant in Texas, leveraging abundant natural gas resources and existing pipeline infrastructure for CO2 transport.

August 2024: The International Maritime Organization (IMO) updated its guidelines for methanol as a marine fuel, providing further clarity on safety and operational standards, which is expected to accelerate adoption rates across the global shipping fleet.

March 2024: A significant investment fund specializing in sustainable infrastructure allocated 300 million USD towards a portfolio of blue and Green Methanol Market projects across Scandinavia, underscoring growing investor confidence in low-carbon methanol.

October 2023: A joint venture between a chemical major and an oil and gas company successfully completed a pilot project demonstrating the efficient capture of CO2 from a methanol synthesis plant, achieving over 90% capture efficiency, paving the way for full-scale blue methanol production.

June 2023: The German government unveiled new incentives for industrial decarbonization, specifically highlighting support for projects integrating Carbon Capture & Storage technology with existing chemical facilities, a direct boost for blue methanol producers and consumers within the Chemical Feedstock Market.

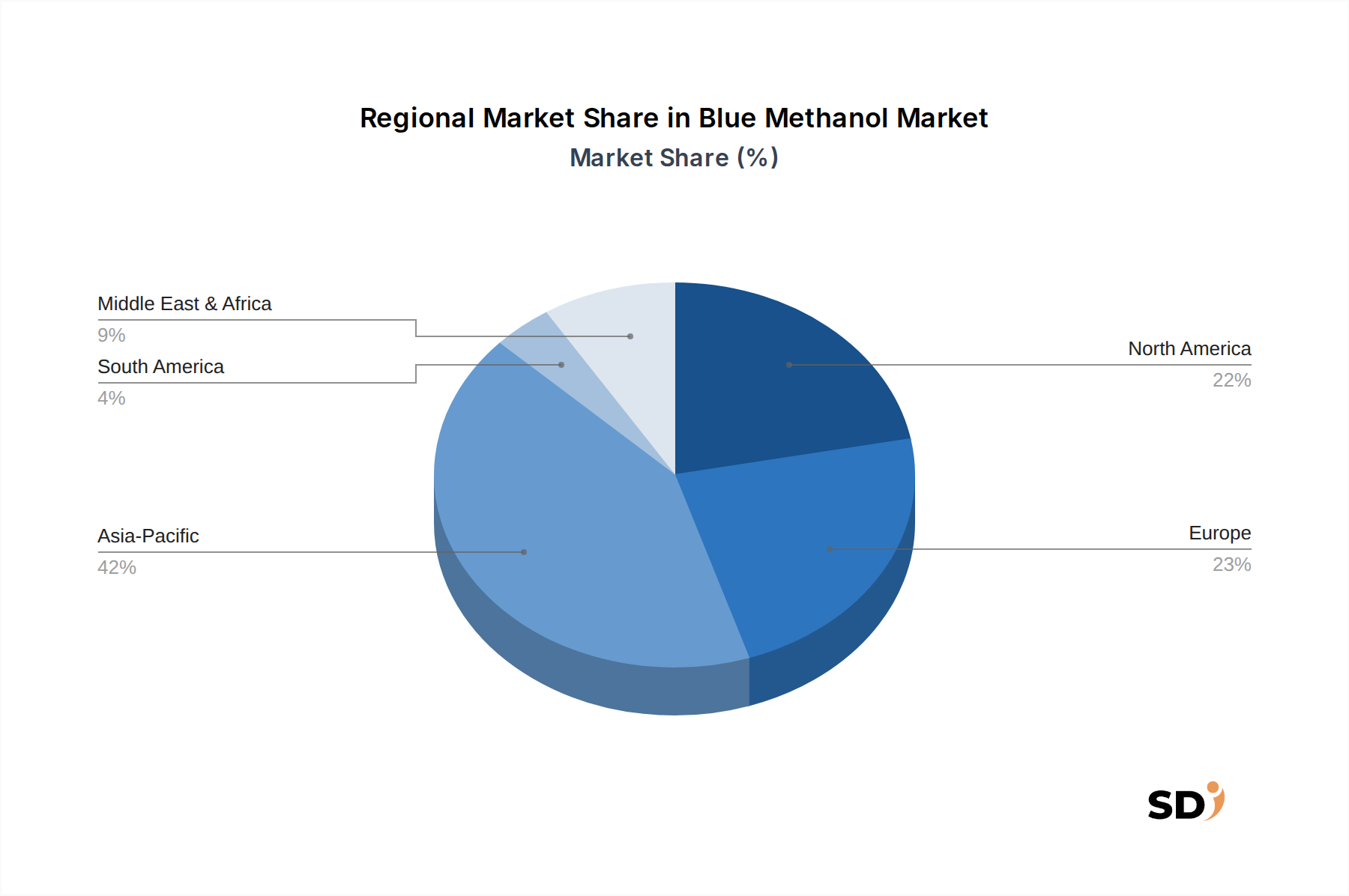

Regional Market Breakdown for Blue Methanol Market

The Blue Methanol Market exhibits diverse growth dynamics across key global regions, driven by varying regulatory landscapes, feedstock availability, and industrial demand. Asia Pacific currently accounts for the largest revenue share, primarily due to the region's massive chemical and industrial manufacturing base, especially in China and India. The robust Chemical Feedstock Market demand, coupled with increasing governmental pressure for emissions reduction, is propelling investments in blue methanol production, even though the region’s CCS infrastructure is still developing. However, the region’s high industrial output means its blue methanol CAGR, while substantial, might be slightly below the fastest-growing regions, estimated at approximately 5.5% over the forecast period, as it scales up its CCS capacity.

Europe is poised to be the fastest-growing region, with an estimated CAGR exceeding 6.5%. This accelerated growth is attributed to stringent environmental regulations, ambitious decarbonization targets set by the European Union, and significant investments in CCS infrastructure, particularly in countries like Norway, the UK, and the Netherlands. The strong focus on sustainable shipping and the burgeoning Marine Fuel Market in European ports are also major drivers. Policies promoting green hydrogen and carbon capture are creating a fertile ground for blue methanol projects, aiming to provide a bridge to a fully renewable energy system. The region is leveraging its technological prowess and regulatory framework to lead in clean energy transitions.

North America represents a significant market, driven by abundant natural gas resources and growing federal incentives for CCS technology, such as the 45Q tax credit in the United States. This region's primary demand stems from the industrial and chemical sectors, along with emerging interest from the Automotive & Transportation Market and Power Generation Market seeking lower-carbon fuel alternatives. North America's blue methanol market is expected to grow at a CAGR of around 6.0%, benefiting from established energy infrastructure and a growing commitment to industrial decarbonization. Countries like Canada are also advancing CCS hubs, further supporting regional blue methanol initiatives.

The Middle East & Africa region is emerging as a crucial hub for future blue methanol production, particularly the GCC countries. Leveraging vast Natural Gas Market reserves and strategic geographic locations, these nations are investing heavily in large-scale blue hydrogen and blue methanol projects, often co-locating with existing petrochemical complexes. While currently having a smaller market share, the region's long-term growth potential is significant, estimated at a CAGR of approximately 6.2%, as it aims to diversify its energy exports towards low-carbon fuels.

Export, Trade Flow & Tariff Impact on Blue Methanol Market

The Blue Methanol Market, while nascent, is intrinsically linked to global trade flows, mirroring and evolving from the established Methanol Market. Major trade corridors for blue methanol are anticipated to connect regions with abundant natural gas resources and developing Carbon Capture & Storage infrastructure (e.g., North America, Middle East, and parts of Europe) to demand centers with stringent decarbonization targets and large industrial consumption (e.g., Asia Pacific, Northern Europe). Leading exporting nations are expected to be those with cost-effective natural gas and robust CCS capabilities, such as the United States, Norway, and GCC states. Conversely, key importing nations will include China, Japan, South Korea, and Germany, driven by their substantial chemical industries and increasing demand from the Marine Fuel Market.

Trade flow dynamics are heavily influenced by the regional availability of CO2 storage sites and the economics of carbon capture. While traditional methanol trade routes are largely sea-borne, the added complexity of CCS could influence logistics. For instance, integrated "blue" production facilities located near CO2 sequestration hubs would naturally become export centers. The impact of tariffs and non-tariff barriers on blue methanol is still evolving. However, carbon border adjustment mechanisms (CBAMs), such as those being implemented by the EU, pose a significant future consideration. These policies aim to level the playing field for domestic products with high environmental standards, meaning blue methanol, with its certified lower carbon intensity, could potentially benefit from reduced tariffs or carbon costs compared to conventional grey methanol imports. Conversely, a lack of harmonized international standards for carbon accounting in blue methanol production could create trade friction, leading to additional certification requirements or potential market access barriers. Preferential trade agreements that include provisions for low-carbon products could also accelerate the adoption and trade of blue methanol, particularly for sectors like the Chemical Feedstock Market and the Industrial Solvents Market.

Sustainability & ESG Pressures on Blue Methanol Market

The Blue Methanol Market's very existence is a direct response to escalating sustainability and ESG (Environmental, Social, and Governance) pressures. Environmental regulations, such as global carbon pricing schemes, national emissions reduction targets, and sector-specific mandates (e.g., IMO 2030/2050 for shipping), are compelling industries to decarbonize. Blue methanol offers a crucial pathway by significantly reducing the carbon footprint of methanol production compared to traditional methods that rely on the Natural Gas Market without CCS. The integration of Carbon Capture & Storage (CCS) directly addresses the "E" in ESG by preventing substantial volumes of industrial CO2 from entering the atmosphere, thereby contributing to climate change mitigation targets.

Circular economy mandates are also influencing product development and procurement. While blue methanol primarily focuses on carbon emission reduction, future iterations could explore capturing biogenic CO2 or industrial waste CO2 for synthesis, further enhancing its circularity credentials. ESG investor criteria are increasingly shaping capital allocation decisions. Investors are scrutinizing companies' environmental performance, supply chain sustainability, and commitment to low-carbon transitions. Companies investing in blue methanol production or adoption are often viewed favorably by ESG-conscious investors, attracting capital for expansion and innovation. This financial pressure incentivizes chemical producers to shift towards blue methanol for their Chemical Feedstock Market needs and shipping companies to adopt it for the Marine Fuel Market, improving their overall ESG scores.

Furthermore, stakeholder expectations from consumers, employees, and local communities are pushing for greater corporate responsibility. Brands are seeking to reduce the embodied carbon in their products, creating pull demand for lower-carbon raw materials. This extends to the Automotive & Transportation Market, where vehicles are increasingly designed for lower emissions, and the Industrial Solvents Market, where demand for greener solvents is rising. These multifaceted pressures collectively accelerate the research, development, and commercialization of blue methanol, positioning it as a pivotal component in the global effort to build a more sustainable industrial and energy landscape.

Blue Methanol Segmentation

1. Feedstock

1.1. Natural Gas

1.2. Coal

1.3. Renewable

1.4. Others

2. Application

2.1. Marine Fuel

2.2. Chemical Feedstock

2.3. Power Generation

2.4. Road Transport Fuel

2.5. Industrial Solvents

2.6. Others

3. End-User Industry

3.1. Chemicals & Petrochemicals

3.2. Energy & Power

3.3. Automotive & Transportation

3.4. Industrial Manufacturing

3.5. Shipping & Maritime Industry

3.6. Others

Blue Methanol Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Blue Methanol REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 5.9% from 2020-2034

Segmentation

By Feedstock

Natural Gas

Coal

Renewable

Others

By Application

Marine Fuel

Chemical Feedstock

Power Generation

Road Transport Fuel

Industrial Solvents

Others

By End-User Industry

Chemicals & Petrochemicals

Energy & Power

Automotive & Transportation

Industrial Manufacturing

Shipping & Maritime Industry

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Feedstock

5.1.1. Natural Gas

5.1.2. Coal

5.1.3. Renewable

5.1.4. Others

5.2. Market Analysis, Insights and Forecast - by Application

5.2.1. Marine Fuel

5.2.2. Chemical Feedstock

5.2.3. Power Generation

5.2.4. Road Transport Fuel

5.2.5. Industrial Solvents

5.2.6. Others

5.3. Market Analysis, Insights and Forecast - by End-User Industry

5.3.1. Chemicals & Petrochemicals

5.3.2. Energy & Power

5.3.3. Automotive & Transportation

5.3.4. Industrial Manufacturing

5.3.5. Shipping & Maritime Industry

5.3.6. Others

5.4. Market Analysis, Insights and Forecast - by Region

5.4.1. North America

5.4.2. South America

5.4.3. Europe

5.4.4. Middle East & Africa

5.4.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Feedstock

6.1.1. Natural Gas

6.1.2. Coal

6.1.3. Renewable

6.1.4. Others

6.2. Market Analysis, Insights and Forecast - by Application

6.2.1. Marine Fuel

6.2.2. Chemical Feedstock

6.2.3. Power Generation

6.2.4. Road Transport Fuel

6.2.5. Industrial Solvents

6.2.6. Others

6.3. Market Analysis, Insights and Forecast - by End-User Industry

6.3.1. Chemicals & Petrochemicals

6.3.2. Energy & Power

6.3.3. Automotive & Transportation

6.3.4. Industrial Manufacturing

6.3.5. Shipping & Maritime Industry

6.3.6. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Feedstock

7.1.1. Natural Gas

7.1.2. Coal

7.1.3. Renewable

7.1.4. Others

7.2. Market Analysis, Insights and Forecast - by Application

7.2.1. Marine Fuel

7.2.2. Chemical Feedstock

7.2.3. Power Generation

7.2.4. Road Transport Fuel

7.2.5. Industrial Solvents

7.2.6. Others

7.3. Market Analysis, Insights and Forecast - by End-User Industry

7.3.1. Chemicals & Petrochemicals

7.3.2. Energy & Power

7.3.3. Automotive & Transportation

7.3.4. Industrial Manufacturing

7.3.5. Shipping & Maritime Industry

7.3.6. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Feedstock

8.1.1. Natural Gas

8.1.2. Coal

8.1.3. Renewable

8.1.4. Others

8.2. Market Analysis, Insights and Forecast - by Application

8.2.1. Marine Fuel

8.2.2. Chemical Feedstock

8.2.3. Power Generation

8.2.4. Road Transport Fuel

8.2.5. Industrial Solvents

8.2.6. Others

8.3. Market Analysis, Insights and Forecast - by End-User Industry

8.3.1. Chemicals & Petrochemicals

8.3.2. Energy & Power

8.3.3. Automotive & Transportation

8.3.4. Industrial Manufacturing

8.3.5. Shipping & Maritime Industry

8.3.6. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Feedstock

9.1.1. Natural Gas

9.1.2. Coal

9.1.3. Renewable

9.1.4. Others

9.2. Market Analysis, Insights and Forecast - by Application

9.2.1. Marine Fuel

9.2.2. Chemical Feedstock

9.2.3. Power Generation

9.2.4. Road Transport Fuel

9.2.5. Industrial Solvents

9.2.6. Others

9.3. Market Analysis, Insights and Forecast - by End-User Industry

9.3.1. Chemicals & Petrochemicals

9.3.2. Energy & Power

9.3.3. Automotive & Transportation

9.3.4. Industrial Manufacturing

9.3.5. Shipping & Maritime Industry

9.3.6. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Feedstock

10.1.1. Natural Gas

10.1.2. Coal

10.1.3. Renewable

10.1.4. Others

10.2. Market Analysis, Insights and Forecast - by Application

10.2.1. Marine Fuel

10.2.2. Chemical Feedstock

10.2.3. Power Generation

10.2.4. Road Transport Fuel

10.2.5. Industrial Solvents

10.2.6. Others

10.3. Market Analysis, Insights and Forecast - by End-User Industry

10.3.1. Chemicals & Petrochemicals

10.3.2. Energy & Power

10.3.3. Automotive & Transportation

10.3.4. Industrial Manufacturing

10.3.5. Shipping & Maritime Industry

10.3.6. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. BASF SE

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. OCI N.V.

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Mitsubishi Gas Chemical Company Inc.

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Celanese Corporation

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Methanex Corporation

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. SABIC

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Proman AG

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Methanol Holdings Trinidad Limited

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Atlantic Methanol Production Company LLC

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Others

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Feedstock 2025 & 2033

Figure 4: Volume (K), by Feedstock 2025 & 2033

Figure 5: Revenue Share (%), by Feedstock 2025 & 2033

Figure 6: Volume Share (%), by Feedstock 2025 & 2033

Figure 7: Revenue (billion), by Application 2025 & 2033

Figure 8: Volume (K), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Volume Share (%), by Application 2025 & 2033

Figure 11: Revenue (billion), by End-User Industry 2025 & 2033

Figure 12: Volume (K), by End-User Industry 2025 & 2033

Figure 13: Revenue Share (%), by End-User Industry 2025 & 2033

Figure 14: Volume Share (%), by End-User Industry 2025 & 2033

Figure 15: Revenue (billion), by Country 2025 & 2033

Figure 16: Volume (K), by Country 2025 & 2033

Figure 17: Revenue Share (%), by Country 2025 & 2033

Figure 18: Volume Share (%), by Country 2025 & 2033

Figure 19: Revenue (billion), by Feedstock 2025 & 2033

Figure 20: Volume (K), by Feedstock 2025 & 2033

Figure 21: Revenue Share (%), by Feedstock 2025 & 2033

Figure 22: Volume Share (%), by Feedstock 2025 & 2033

Figure 23: Revenue (billion), by Application 2025 & 2033

Figure 24: Volume (K), by Application 2025 & 2033

Figure 25: Revenue Share (%), by Application 2025 & 2033

Figure 26: Volume Share (%), by Application 2025 & 2033

Figure 27: Revenue (billion), by End-User Industry 2025 & 2033

Figure 28: Volume (K), by End-User Industry 2025 & 2033

Figure 29: Revenue Share (%), by End-User Industry 2025 & 2033

Figure 30: Volume Share (%), by End-User Industry 2025 & 2033

Figure 31: Revenue (billion), by Country 2025 & 2033

Figure 32: Volume (K), by Country 2025 & 2033

Figure 33: Revenue Share (%), by Country 2025 & 2033

Figure 34: Volume Share (%), by Country 2025 & 2033

Figure 35: Revenue (billion), by Feedstock 2025 & 2033

Figure 36: Volume (K), by Feedstock 2025 & 2033

Figure 37: Revenue Share (%), by Feedstock 2025 & 2033

Figure 38: Volume Share (%), by Feedstock 2025 & 2033

Figure 39: Revenue (billion), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (billion), by End-User Industry 2025 & 2033

Figure 44: Volume (K), by End-User Industry 2025 & 2033

Figure 45: Revenue Share (%), by End-User Industry 2025 & 2033

Figure 46: Volume Share (%), by End-User Industry 2025 & 2033

Figure 47: Revenue (billion), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (billion), by Feedstock 2025 & 2033

Figure 52: Volume (K), by Feedstock 2025 & 2033

Figure 53: Revenue Share (%), by Feedstock 2025 & 2033

Figure 54: Volume Share (%), by Feedstock 2025 & 2033

Figure 55: Revenue (billion), by Application 2025 & 2033

Figure 56: Volume (K), by Application 2025 & 2033

Figure 57: Revenue Share (%), by Application 2025 & 2033

Figure 58: Volume Share (%), by Application 2025 & 2033

Figure 59: Revenue (billion), by End-User Industry 2025 & 2033

Figure 60: Volume (K), by End-User Industry 2025 & 2033

Figure 61: Revenue Share (%), by End-User Industry 2025 & 2033

Figure 62: Volume Share (%), by End-User Industry 2025 & 2033

Figure 63: Revenue (billion), by Country 2025 & 2033

Figure 64: Volume (K), by Country 2025 & 2033

Figure 65: Revenue Share (%), by Country 2025 & 2033

Figure 66: Volume Share (%), by Country 2025 & 2033

Figure 67: Revenue (billion), by Feedstock 2025 & 2033

Figure 68: Volume (K), by Feedstock 2025 & 2033

Figure 69: Revenue Share (%), by Feedstock 2025 & 2033

Figure 70: Volume Share (%), by Feedstock 2025 & 2033

Figure 71: Revenue (billion), by Application 2025 & 2033

Figure 72: Volume (K), by Application 2025 & 2033

Figure 73: Revenue Share (%), by Application 2025 & 2033

Figure 74: Volume Share (%), by Application 2025 & 2033

Figure 75: Revenue (billion), by End-User Industry 2025 & 2033

Figure 76: Volume (K), by End-User Industry 2025 & 2033

Figure 77: Revenue Share (%), by End-User Industry 2025 & 2033

Figure 78: Volume Share (%), by End-User Industry 2025 & 2033

Figure 79: Revenue (billion), by Country 2025 & 2033

Figure 80: Volume (K), by Country 2025 & 2033

Figure 81: Revenue Share (%), by Country 2025 & 2033

Figure 82: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Feedstock 2020 & 2033

Table 2: Volume K Forecast, by Feedstock 2020 & 2033

Table 3: Revenue billion Forecast, by Application 2020 & 2033

Table 4: Volume K Forecast, by Application 2020 & 2033

Table 5: Revenue billion Forecast, by End-User Industry 2020 & 2033

Table 6: Volume K Forecast, by End-User Industry 2020 & 2033

Table 7: Revenue billion Forecast, by Region 2020 & 2033

Table 8: Volume K Forecast, by Region 2020 & 2033

Table 9: Revenue billion Forecast, by Feedstock 2020 & 2033

Table 10: Volume K Forecast, by Feedstock 2020 & 2033

Table 11: Revenue billion Forecast, by Application 2020 & 2033

Table 12: Volume K Forecast, by Application 2020 & 2033

Table 13: Revenue billion Forecast, by End-User Industry 2020 & 2033

Table 14: Volume K Forecast, by End-User Industry 2020 & 2033

Table 15: Revenue billion Forecast, by Country 2020 & 2033

Table 16: Volume K Forecast, by Country 2020 & 2033

Table 17: Revenue (billion) Forecast, by Application 2020 & 2033

Table 18: Volume (K) Forecast, by Application 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Volume (K) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Volume (K) Forecast, by Application 2020 & 2033

Table 23: Revenue billion Forecast, by Feedstock 2020 & 2033

Table 24: Volume K Forecast, by Feedstock 2020 & 2033

Table 25: Revenue billion Forecast, by Application 2020 & 2033

Table 26: Volume K Forecast, by Application 2020 & 2033

Table 27: Revenue billion Forecast, by End-User Industry 2020 & 2033

Table 28: Volume K Forecast, by End-User Industry 2020 & 2033

Table 29: Revenue billion Forecast, by Country 2020 & 2033

Table 30: Volume K Forecast, by Country 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Volume (K) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Volume (K) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Volume (K) Forecast, by Application 2020 & 2033

Table 37: Revenue billion Forecast, by Feedstock 2020 & 2033

Table 38: Volume K Forecast, by Feedstock 2020 & 2033

Table 39: Revenue billion Forecast, by Application 2020 & 2033

Table 40: Volume K Forecast, by Application 2020 & 2033

Table 41: Revenue billion Forecast, by End-User Industry 2020 & 2033

Table 42: Volume K Forecast, by End-User Industry 2020 & 2033

Table 43: Revenue billion Forecast, by Country 2020 & 2033

Table 44: Volume K Forecast, by Country 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Volume (K) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Volume (K) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Volume (K) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Volume (K) Forecast, by Application 2020 & 2033

Table 59: Revenue (billion) Forecast, by Application 2020 & 2033

Table 60: Volume (K) Forecast, by Application 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue billion Forecast, by Feedstock 2020 & 2033

Table 64: Volume K Forecast, by Feedstock 2020 & 2033

Table 65: Revenue billion Forecast, by Application 2020 & 2033

Table 66: Volume K Forecast, by Application 2020 & 2033

Table 67: Revenue billion Forecast, by End-User Industry 2020 & 2033

Table 68: Volume K Forecast, by End-User Industry 2020 & 2033

Table 69: Revenue billion Forecast, by Country 2020 & 2033

Table 70: Volume K Forecast, by Country 2020 & 2033

Table 71: Revenue (billion) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue (billion) Forecast, by Application 2020 & 2033

Table 74: Volume (K) Forecast, by Application 2020 & 2033

Table 75: Revenue (billion) Forecast, by Application 2020 & 2033

Table 76: Volume (K) Forecast, by Application 2020 & 2033

Table 77: Revenue (billion) Forecast, by Application 2020 & 2033

Table 78: Volume (K) Forecast, by Application 2020 & 2033

Table 79: Revenue (billion) Forecast, by Application 2020 & 2033

Table 80: Volume (K) Forecast, by Application 2020 & 2033

Table 81: Revenue (billion) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue billion Forecast, by Feedstock 2020 & 2033

Table 84: Volume K Forecast, by Feedstock 2020 & 2033

Table 85: Revenue billion Forecast, by Application 2020 & 2033

Table 86: Volume K Forecast, by Application 2020 & 2033

Table 87: Revenue billion Forecast, by End-User Industry 2020 & 2033

Table 88: Volume K Forecast, by End-User Industry 2020 & 2033

Table 89: Revenue billion Forecast, by Country 2020 & 2033

Table 90: Volume K Forecast, by Country 2020 & 2033

Table 91: Revenue (billion) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Table 93: Revenue (billion) Forecast, by Application 2020 & 2033

Table 94: Volume (K) Forecast, by Application 2020 & 2033

Table 95: Revenue (billion) Forecast, by Application 2020 & 2033

Table 96: Volume (K) Forecast, by Application 2020 & 2033

Table 97: Revenue (billion) Forecast, by Application 2020 & 2033

Table 98: Volume (K) Forecast, by Application 2020 & 2033

Table 99: Revenue (billion) Forecast, by Application 2020 & 2033

Table 100: Volume (K) Forecast, by Application 2020 & 2033

Table 101: Revenue (billion) Forecast, by Application 2020 & 2033

Table 102: Volume (K) Forecast, by Application 2020 & 2033

Table 103: Revenue (billion) Forecast, by Application 2020 & 2033

Table 104: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is designed to capture highly nuanced market insights and validate secondary findings directly from industry experts. This intensive phase accounts for 70-80% of our total research effort, ensuring an unparalleled depth of understanding. Our engagement strategy targets key decision-makers and subject matter experts across the blue methanol value chain.

Key stakeholders interviewed include:

Head of Sustainable Fuels / Alternative Fuels Manager: From major shipping lines, energy companies, and maritime technology providers, focusing on blue methanol adoption as marine fuel and its infrastructural requirements.

VP of R&D / Director of New Technologies: From leading methanol producers and technology licensors, providing insights into production advancements, feedstock diversification, and future applications.

Chief Procurement Officer / Supply Chain Director: From large chemical companies and industrial manufacturers, detailing procurement strategies for methanol, supply chain resilience, and shifts towards sustainable feedstocks.

Market Development Manager / Business Development Lead: From feedstock suppliers (e.g., natural gas producers, bio-methane providers) and emerging blue methanol producers, discussing market entry strategies, competitive landscape, and regional demand drivers.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Head of Sustainable Fuels / Alternative Fuels Manager

30%

VP of R&D / Director of New Technologies

30%

Chief Procurement Officer / Supply Chain Director

25%

Market Development Manager / Business Development Lead

15%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Methanol Producers & Chemical Companies

30%

Feedstock Suppliers

20%

Technology Licensors & Engineering Firms

15%

Energy & Shipping Companies

25%

Industrial Chemical Users

10%

Secondary Research & Industry Benchmarking

The remaining 20-30% of our research effort is dedicated to comprehensive secondary research and rigorous industry benchmarking. This phase establishes a foundational understanding of the blue methanol market, identifying macro trends, technological advancements, regulatory frameworks, and competitive landscapes. Our data sources are meticulously selected for reliability and accuracy:

Proprietary Databases: Leveraging our firm’s extensive internal databases for historical market trends and forecasts.

Financial & Business Intelligence Platforms:

Bloomberg: For real-time market data, company financials, and industry news.

Factiva: For extensive news archives, company information, and industry publications.

Hoovers: For company profiles, industry analysis, and competitive intelligence.

PitchBook: For private company data, investment trends, and emerging technology analysis.

Government Publications & Official Statistics: Data from national energy agencies, environmental protection bodies, and statistical offices (e.g., https://www.eia.gov/, https://ec.europa.eu/eurostat/).

Industry Associations & Regulatory Bodies:

Methanol Institute: Providing global market data, advocacy positions, and technical specifications for methanol production and use (https://www.methanol.org/).

International Maritime Organization (IMO): Offering critical insights into shipping regulations, decarbonization targets, and the adoption of alternative marine fuels like methanol (https://www.imo.org/).

International Renewable Energy Agency (IRENA): Supplying data and analysis on renewable energy sources, relevant for green hydrogen (a precursor for renewable methanol) and bio-feedstocks (https://www.irena.org/).

European Chemical Industry Council (CEFIC): Offering insights into the European chemical sector's demand for methanol as a feedstock and solvent (https://cefic.org/).

Academic Research & Scientific Journals: Peer-reviewed publications offering in-depth analysis of methanol production technologies, environmental impacts, and future applications.

Company Annual Reports & Investor Presentations: Publicly available financial statements and corporate communications from key market participants.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies employ a robust combination of top-down and bottom-up approaches, triangulated across multiple data points to ensure accuracy.

Bottom-Up Market Sizing:

Methanol Production Capacity & Utilization: Analyzing current and planned blue methanol production capacities by feedstock type (natural gas, coal, renewable, etc.) across key regions, combined with historical and projected utilization rates in kilotons/annum.

Application-Specific Demand Projections: Estimating demand for blue methanol in specific applications such as marine fuel (based on vessel deliveries and fleet size by fuel type for methanol-enabled vessels), chemical feedstock (based on methanol-to-chemicals (MTC) plant capacities and utilization rates), and power generation (based on gas turbine conversions or new methanol-fueled power plants).

Average Methanol Consumption Rates: Applying industry-standard or inferred consumption rates per unit of application (e.g., per MWh for power generation, per ton of specific chemical product, or per nautical mile traveled by methanol-fueled vessels).

Top-Down Market Sizing: Initiating with global or regional methanol market values and volumes, then segmenting down based on the "blue" aspect (defined by carbon capture utilization and storage - CCUS), feedstock, application, and end-user industry proportions derived from secondary research and primary interviews.

Multi-level Data Triangulation: All market figures are subjected to rigorous cross-validation using data points from primary interviews, secondary sources, and econometric models to minimize discrepancies and enhance reliability. Factors such as economic growth, regulatory changes, technological advancements, and energy price fluctuations are integrated into our forecasting models.

Data Accuracy & Quality Check

We are committed to delivering data with an estimated accuracy level of 85-90%. This high standard is maintained through a multi-stage validation process:

Expert Panel Review: Insights and data points collected are reviewed by an internal panel of senior analysts specializing in energy, chemicals, and sustainable technologies.

Peer Review: All research findings and methodologies undergo a stringent peer review process to identify and correct any potential biases or errors.

Continuous Updates: Every report is meticulously updated to incorporate the latest market developments, regulatory changes, and technological breakthroughs up to the date of purchase. This ensures clients receive the most current and relevant market intelligence.

Source Verification: All statistical data and qualitative insights are traced back to their original sources for verification. Discrepancies between sources are resolved through additional primary research or by prioritizing the most authoritative and credible information.

Proprietary Quality Assurance Framework: Our firm employs a proprietary Quality Assurance (QA) framework that encompasses data collection, analysis, modeling, and reporting stages, designed to meet the highest industry benchmarks for accuracy and integrity.

Frequently Asked Questions

1. Which companies lead the Blue Methanol market?

Key players in the Blue Methanol market include BASF SE, OCI N.V., Mitsubishi Gas Chemical Company Inc., Celanese Corporation, and Methanex Corporation. These entities compete across various applications, driving innovation and market expansion.

2. What are the primary feedstocks for Blue Methanol production?

The primary feedstocks for Blue Methanol production include Natural Gas, Coal, and Renewable sources. Supply chain considerations involve sourcing stability and cost efficiency of these raw materials, impacting production economics.

3. How are technological innovations shaping the Blue Methanol industry?

Technological innovations focus on enhancing conversion efficiency, reducing production costs, and optimizing feedstock utilization. R&D trends are also exploring carbon capture and utilization technologies to improve sustainability credentials.

4. What are the main challenges in the Blue Methanol market?

Major challenges for the Blue Methanol market include volatile raw material prices, particularly natural gas, and the high capital expenditure required for new production facilities. Regulatory landscapes and competition from other fuel sources also pose restraints.

5. What drives international trade in Blue Methanol?

International trade in Blue Methanol is driven by regional supply-demand imbalances, with major production hubs exporting to high-consumption areas. Shipping and maritime transport logistics are crucial for global distribution, influencing trade flows and pricing.

6. What is the projected growth for the Blue Methanol market through 2033?

The Blue Methanol market is projected to grow from $34.16 billion in 2025 at a CAGR of 5.9%. This expansion is forecasted to continue until 2033, driven by increasing adoption in marine fuel and chemical feedstock applications.