1. What is the projected growth for the Atorvastatin market?

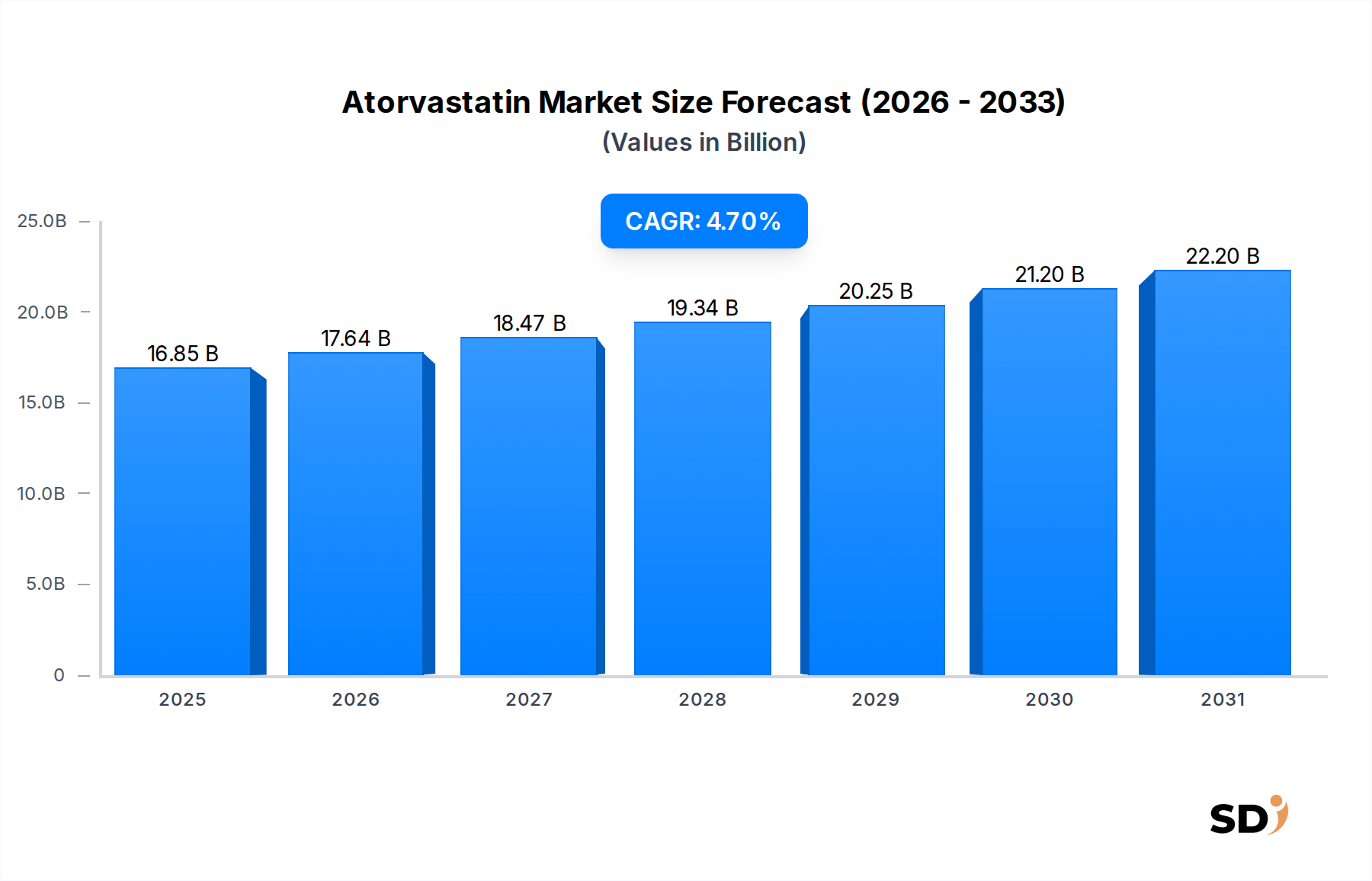

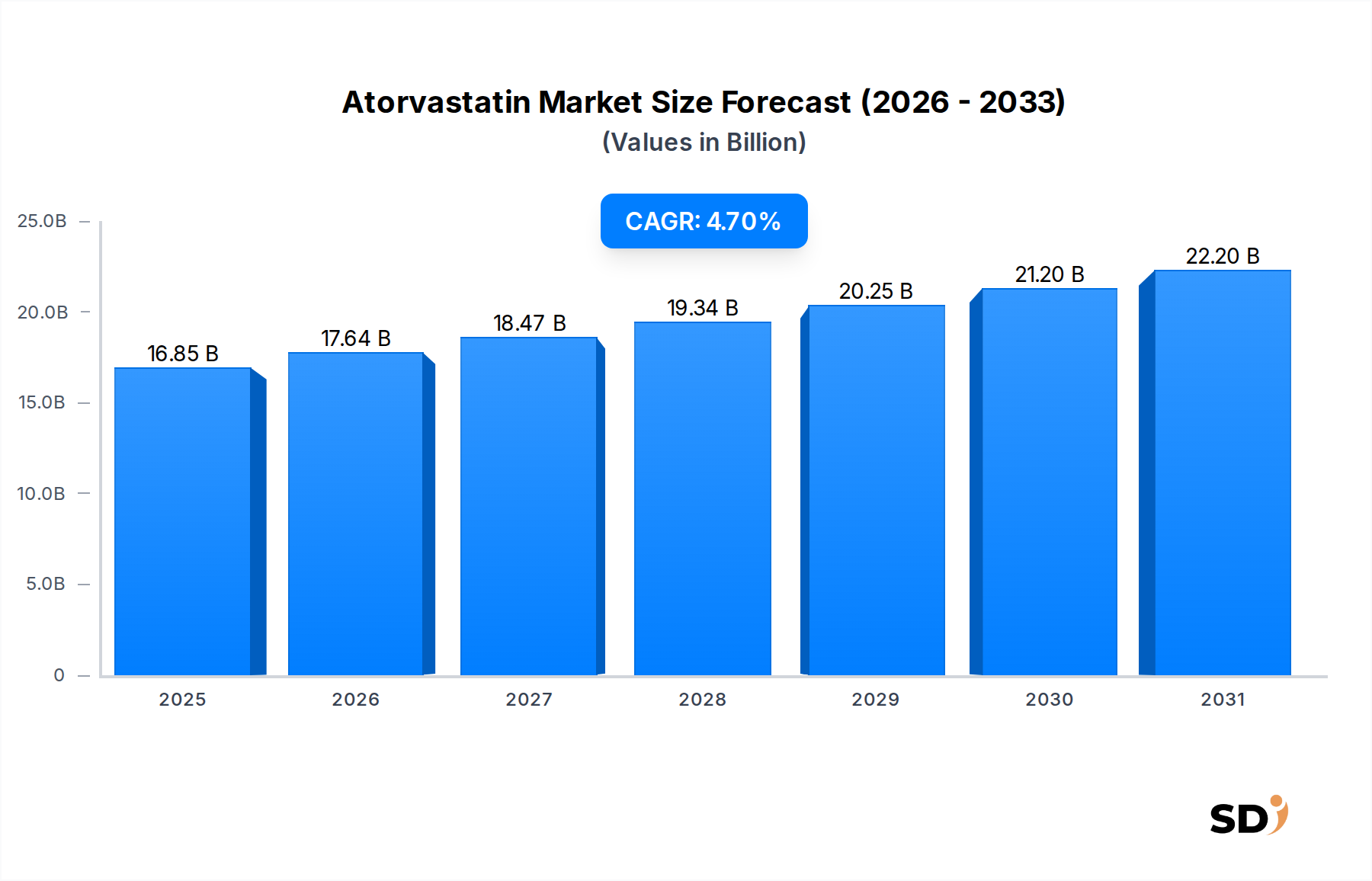

The Atorvastatin market is valued at $16.85 billion in 2024. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.7% through 2034.

+1 2315155523

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

The Atorvastatin Market is currently valued at an impressive $16.85 billion in 2024, demonstrating its critical role within global healthcare. Projections indicate a robust expansion, with the market anticipated to grow at a Compound Annual Growth Rate (CAGR) of 4.7% from 2024 to 2034. This growth trajectory is expected to elevate the market valuation to approximately $26.63 billion by 2034, underscoring sustained demand and strategic investments. The primary impetus behind this significant growth is the escalating global prevalence of cardiovascular diseases (CVDs) and associated conditions such as hyperlipidemia. As a leading HMG-CoA reductase inhibitor, atorvastatin remains a cornerstone in lipid management and primary/secondary prevention of cardiovascular events.

Key demand drivers include the aging global population, which inherently carries a higher risk of developing hyperlipidemia and CVDs. Furthermore, increased public awareness campaigns regarding cholesterol management and the importance of preventive healthcare contribute significantly to market expansion. The widespread availability of generic atorvastatin formulations post-patent expiration has democratized access to this essential medication, significantly expanding its adoption across diverse socioeconomic strata. This affordability factor is crucial for the overall expansion of the Generic Drugs Market, allowing more patients to access effective treatment. Macro tailwinds, such as advancements in diagnostic capabilities for lipid disorders and the continuous expansion of healthcare infrastructure in emerging economies, further amplify market potential. The Lipid-Lowering Drugs Market as a whole benefits from these trends, with atorvastatin maintaining a prominent position due to its proven efficacy and safety profile. The market's forward-looking outlook is characterized by a balance between the continued dominance of generic versions and ongoing innovation in drug delivery and combination therapies, ensuring its enduring relevance in the global pharmaceutical landscape.

The Generic Drugs Market segment, specifically Generic Atorvastatin, represents the single largest and most influential component within the broader Atorvastatin Market. Its dominance is overwhelmingly driven by the patent expiration of Pfizer's Lipitor (atorvastatin calcium) in 2011 in the United States, followed by similar expirations in other major global markets. This event triggered a rapid and profound shift towards generic formulations, which are therapeutically equivalent but significantly more cost-effective. The affordability factor has been a paramount determinant in its widespread adoption, especially in regions with burgeoning healthcare expenditures and a focus on cost-efficient patient care. Generic versions are now the preferred choice for healthcare providers, payers, and patients alike, contributing to a substantial revenue share for this segment.

Several key players have capitalized on the genericization wave, establishing strong footholds within this segment. Companies like Teva Pharmaceutical Industries, Sun Pharmaceutical Industries, Apotex Pharmachem, and Cadila Pharmaceuticals are prominent manufacturers, leveraging their robust manufacturing capabilities and extensive distribution networks to ensure broad availability. These companies often compete on price, supply chain efficiency, and regulatory compliance, solidifying their positions in the highly competitive Pharmaceutical Manufacturing Market. The market share of generic atorvastatin is not merely growing; it has largely consolidated the market, making it challenging for new entrants without significant economies of scale or innovative product differentiation. This consolidation is driven by the need for large-scale production to meet global demand and the intensive regulatory approval processes required for generic drugs.

The widespread acceptance of generic atorvastatin is further bolstered by its inclusion in essential medicines lists and its preferential status in formularies by insurance providers and national health systems. This ensures broad reimbursement and access, making it a cornerstone of Cardiology Treatment Market protocols worldwide. The shift has also impacted the Branded Drugs Market, where original branded products, while still commanding a premium in certain niche segments or patient populations, have seen their market share significantly eroded by generic alternatives. The robust demand for affordable, effective lipid-lowering agents continues to fuel the expansion of generic atorvastatin, underpinning its sustained leadership in the Atorvastatin Market.

The trajectory of the Atorvastatin Market is shaped by a confluence of potent drivers and discernible constraints. A primary driver is the pervasive and increasing burden of cardiovascular diseases (CVDs) globally. According to the World Health Organization (WHO), CVDs remain the leading cause of death worldwide, accounting for an estimated 17.9 million lives each year. As a critical component of Statins Market and a cornerstone therapy, atorvastatin plays an indispensable role in mitigating this public health challenge, directly driving demand.

Another significant driver is the global demographic shift towards an aging population. Individuals aged 60 years and above are inherently at a higher risk of developing hyperlipidemia and related cardiovascular complications. The United Nations projects that by 2050, the global population aged 60 years or over is expected to reach 2.1 billion, representing a vast and expanding patient pool requiring lipid-lowering therapies. Concurrently, increasing awareness about cholesterol management and the emphasis on preventive healthcare, supported by public health campaigns, have spurred early diagnosis and treatment initiation. The affordability of generic atorvastatin post-patent expiration has also been a monumental driver, making effective treatment accessible to a much broader patient base and significantly boosting the Generic Drugs Market.

However, the Atorvastatin Market also faces several constraints. Stringent regulatory approval processes, particularly for new formulations or indications, can be lengthy and capital-intensive, potentially delaying market entry. Moreover, the prevalence of side effects, such as muscle pain (myalgia) and elevated liver enzymes, can lead to patient non-adherence or discontinuation, impacting long-term therapy rates. Patients' ability to adhere to prescribed regimens is crucial, and any perceived discomfort can act as a significant barrier. Competition from alternative lipid-lowering therapies, including newer classes like PCSK9 inhibitors or even other statins, presents a competitive constraint. While atorvastatin remains highly effective, the continuous introduction of novel therapeutic options, albeit often at higher price points, could gradually fragment the overall Lipid-Lowering Drugs Market.

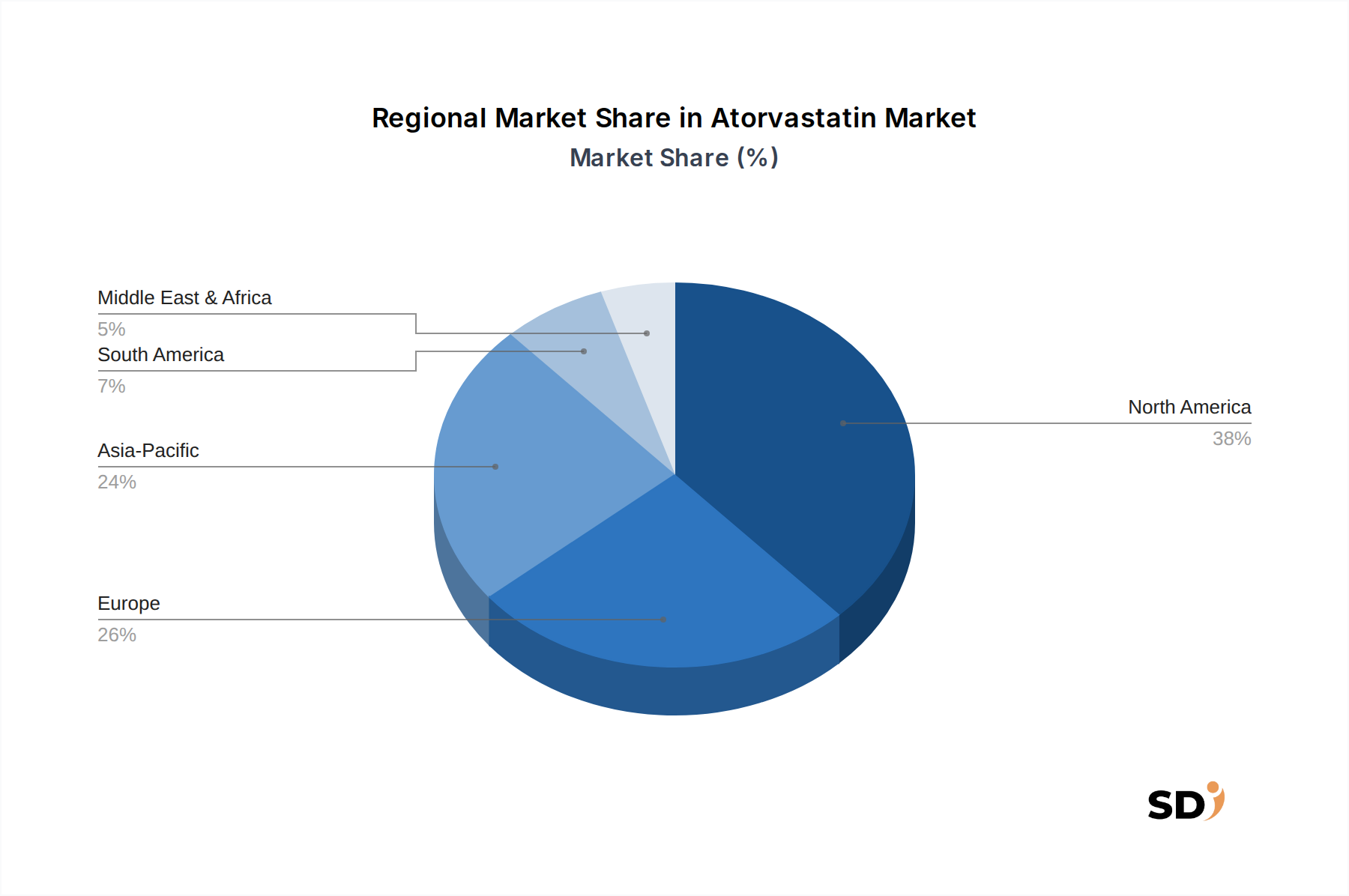

The global Atorvastatin Market exhibits significant regional variations in terms of adoption, growth dynamics, and revenue contribution. North America, comprising the United States, Canada, and Mexico, currently holds the largest revenue share in the market. This dominance is attributable to a high prevalence of cardiovascular diseases, advanced healthcare infrastructure, high per capita healthcare expenditure, and robust awareness programs. The established Hospital Pharmacy Market and retail pharmacy networks ensure broad access to both branded and generic formulations. The United States, in particular, represents a mature market with high generic penetration, leading to consistent demand but potentially lower price realization compared to its branded era.

Europe, including key economies like Germany, France, and the United Kingdom, represents another substantial market segment. Similar to North America, Europe benefits from well-developed healthcare systems, an aging population, and comprehensive public health initiatives focusing on CVD prevention. The adoption of generic atorvastatin is high, driven by cost-containment measures within national health services. However, market growth may be more modest compared to emerging regions, reflecting its maturity.

The Asia Pacific region is unequivocally identified as the fastest-growing market for atorvastatin during the forecast period. This accelerated growth is propelled by several factors: a massive and growing population base, rapidly improving healthcare infrastructure, increasing disposable incomes, and a rising prevalence of lifestyle-related diseases including hyperlipidemia. Countries like China and India are witnessing a surge in Cardiology Treatment Market needs, alongside expanding access to affordable generic medicines. These factors, combined with increasing health awareness and supportive government policies, are expected to fuel substantial market expansion. The Pharmaceutical Manufacturing Market in this region is also expanding, supporting local production and distribution of atorvastatin.

Latin America and the Middle East & Africa (MEA) represent emerging markets with considerable untapped potential. These regions are experiencing improving healthcare access, growing urbanization, and a gradual increase in the diagnosis and treatment of cardiovascular conditions. While currently smaller in market share, these regions are poised for strong growth, driven by increasing patient awareness, expanding pharmaceutical distribution channels, and efforts to make essential medicines more accessible and affordable.

The competitive landscape of the Atorvastatin Market is characterized by a mix of multinational pharmaceutical giants, specialized generic manufacturers, and active pharmaceutical ingredient (API) suppliers. The market has largely shifted towards generic competition following the patent expiration of Lipitor, leading to a highly fragmented yet competitive environment.

Pharmaceutical Manufacturing Market efforts.Biocatalysis Market.Generic Drugs Market, offering a range of generic atorvastatin formulations across various dosage forms.Generic Drugs Market, with a strong portfolio of atorvastatin products available worldwide. Its broad distribution capabilities contribute to its significant market presence.The Atorvastatin Market continues to evolve through strategic maneuvers and regulatory milestones, reflecting ongoing efforts to enhance accessibility and optimize therapeutic outcomes.

Cardiology Treatment Market.Generic Drugs Market.Biocatalysis Market techniques for the sustainable production of atorvastatin intermediates, promising reduced environmental impact and potentially lower manufacturing costs for the Pharmaceutical Manufacturing Market.Lipid-Lowering Drugs Market therapies.The customer base for the Atorvastatin Market is diverse, primarily segmented by end-users into hospitals, clinics, cardiology centers, homecare settings, and ambulatory surgical centers. Each segment exhibits distinct purchasing criteria, price sensitivities, and procurement channels, reflecting the multifaceted nature of healthcare delivery.

Hospitals, being major consumers, prioritize bulk purchasing, often through tenders and long-term contracts. Their purchasing criteria heavily weigh on efficacy, safety, consistent supply, and competitive pricing, especially for Generic Drugs Market products. The Hospital Pharmacy Market serves as a primary procurement channel, ensuring stock for inpatients and discharge prescriptions. Clinics and cardiology centers, while also valuing efficacy and safety, often focus on patient convenience and ease of dispensing. Their buying behavior is influenced by physician preference, formulary inclusion, and patient-specific needs, with prescriptions frequently filled via retail or Online Pharmacies.

Patients in homecare settings, often managed by primary care physicians, rely significantly on convenience and accessibility, driving demand through retail and online pharmacy channels. Price sensitivity is particularly high in out-of-pocket markets or for patients with limited insurance coverage, which reinforces the strong preference for generic atorvastatin. The Oral Solid Dosage Market for atorvastatin, predominantly tablets, caters directly to patient convenience and ease of administration. Ambulatory surgical centers, which may prescribe atorvastatin for short-term perioperative use or as part of pre-existing medication regimens, integrate purchasing decisions with their broader surgical supply chain.

Notable shifts in buyer preference include an accelerating move towards generics due to cost pressures across all segments. The rise of Online Pharmacies as a convenient procurement channel, particularly for chronic medications like atorvastatin, is also a significant trend. Furthermore, a growing emphasis on patient adherence solutions and combination therapies suggests a preference for holistic approaches to cardiovascular care within the Lipid-Lowering Drugs Market, influencing what types of formulations and support services are valued.

Investment and funding activity within the Atorvastatin Market, while mature, continues to exhibit strategic movements, primarily focusing on consolidation, supply chain optimization, and select innovation. Over the past 2-3 years, M&A activity has been notable within the Generic Drugs Market segment, driven by larger pharmaceutical players seeking to consolidate market share, enhance manufacturing capacities, and achieve economies of scale. These acquisitions often target smaller generic manufacturers with strong regional presence or specialized production capabilities in the Pharmaceutical Manufacturing Market.

Venture funding rounds specifically targeting "atorvastatin" are less common, given its status as an off-patent, widely available medication. Instead, venture capital and private equity tend to flow into broader adjacent areas, such as novel drug delivery systems that could potentially incorporate statins, or into biotech firms developing next-generation Lipid-Lowering Drugs Market therapies (e.g., gene therapies or RNA-based treatments for hyperlipidemia). Companies involved in the Biocatalysis Market for sustainable and cost-effective API production might also attract investment, as efficiency and environmental considerations become increasingly important in pharmaceutical manufacturing.

Strategic partnerships frequently involve co-marketing agreements for generic atorvastatin in new or underdeveloped markets, particularly in emerging economies where penetration rates are still growing. Supply chain collaborations, aimed at ensuring consistent availability and mitigating geopolitical risks, are also prominent. These partnerships often involve API suppliers, contract manufacturing organizations (CMOs), and regional distributors. Sub-segments attracting the most capital are typically those focused on improving patient adherence through fixed-dose combinations, exploring new indications (though less common for a mature drug like atorvastatin), or enhancing the drug's pharmacokinetic profile through novel formulation technologies. Investment in digital health platforms that support medication management and patient engagement, which indirectly benefits adherence to treatments like atorvastatin, also represents an area of interest for broader healthcare investors.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.7% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Our methodology places significant emphasis on primary research, constituting approximately 75% of our overall data collection and validation efforts. This rigorous approach involves extensive qualitative and quantitative interviews, surveys, and discussions with key stakeholders across the Atorvastatin value chain. These interactions are carefully structured to gather first-hand intelligence, validate secondary data, and gain nuanced perspectives on market dynamics, competitive landscapes, technological advancements, and regional specificities. Our primary respondents include:

Specific Job Titles/Stakeholders Interviewed:

Specific Company Types Engaged:

Interviews are conducted with participants spanning various geographical regions covered in the report, ensuring a comprehensive global perspective on the Atorvastatin market.

| Stakeholder Role | Interview Share (%) |

|---|---|

| VP, R&D and Bioprocess Development | 25% |

| Global Product Manager, Cardiovascular Drugs | 30% |

| Director of API Sourcing & Procurement | 25% |

| Head of Regulatory Affairs | 20% |

| Company Type | Representation (%) |

|---|---|

| API Manufacturers (Chemical Synthesis & Biocatalysis) | 30% |

| Pharmaceutical Formulators (Branded & Generic) | 35% |

| Contract Development & Manufacturing Organizations (CDMOs) | 15% |

| Pharmaceutical Wholesale Distributors & Retail Chains | 20% |

Secondary research accounts for approximately 25% of our data collection, serving as the foundational layer for market understanding and competitive intelligence. This phase involves a meticulous collection of data from authoritative and credible sources. We leverage standard financial databases, including Bloomberg, Factiva, Hoovers, and PitchBook, to extract company financials, competitive intelligence, and investment trends. Additionally, we extensively utilize data from governmental bodies, non-profit organizations, and recognized trade associations to ensure objectivity and accuracy. Key sources include:

Further data is sourced from company annual reports, investor presentations, white papers, scientific journals, press releases, and reputable industry publications. All collected information undergoes rigorous cross-verification to identify market trends, technological advancements, regulatory changes, and the competitive landscape. Every report is meticulously updated to reflect the latest market dynamics and information available up to the date of purchase.

Our market estimation framework employs a robust combination of top-down and bottom-up methodologies, complemented by multi-level data triangulation, to ensure the highest degree of accuracy and reliability in market sizing and forecasting. The bottom-up approach involves segmenting the market at the granular level and then aggregating these segments to derive the total market size. For the Atorvastatin market, specific variables used in our bottom-up calculations include:

The top-down approach involves estimating the overall market size using macro-economic indicators, industry reports, and expert forecasts, which is then disaggregated into specific segments. Both approaches are constantly cross-referenced and validated against each other and against primary research insights. Data triangulation further enhances accuracy by comparing and correlating data points from multiple independent sources, mitigating biases, and ensuring consistency across all market segments, including product type, drug type, dosage form, distribution channel, end-user, and all specified geographic regions (North America, South America, Europe, Middle East & Africa, Asia Pacific).

Our commitment to data integrity is paramount. We guarantee an estimated data accuracy level of 88% to 90%. This high level of precision is achieved through a multi-stage quality assurance process:

The Atorvastatin market is valued at $16.85 billion in 2024. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.7% through 2034.

Consumer purchasing trends for Atorvastatin are influenced by increased access through diverse distribution channels, including Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies. The availability of generic Atorvastatin also shapes these patterns.

Production innovations in the Atorvastatin market include advancements in chemical synthesis methods and the growing adoption of biocatalysis-based production techniques. These methods aim to optimize manufacturing efficiency and product purity.

Specific export-import dynamics for Atorvastatin are not detailed in current data. However, the global presence of manufacturers like Pfizer and Sun Pharmaceutical Industries implies extensive international distribution networks for the drug.

Key companies in the Atorvastatin market include Pfizer, Sun Pharmaceutical Industries, Teva Pharmaceutical Industries, and Apotex Pharmachem. These players compete across both branded and generic drug segments.

Pricing trends in the Atorvastatin market are heavily influenced by the coexistence of branded and generic drug types. Generic versions, offered by companies such as Teva and Sun Pharmaceutical Industries, typically exert downward pressure on overall market prices and impact cost structures.