Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Acoustic Metamaterials for Automotive: $69M Market, 8.5% CAGR

Acoustic Metamaterials for Automotive

Acoustic Metamaterials for Automotive: $69M Market, 8.5% CAGR

Acoustic Metamaterials for Automotive by Product Type (Acoustic Panels, Acoustic Insulation Materials, Acoustic Liners, Sound Absorbing Metamaterials), by Application (Cabin Noise Reduction, Engine Noise Control, Powertrain Noise Management, Road Noise Reduction, Tire Noise Attenuation, Others), by Vehicle Type (Passenger Vehicles, Commercial Vehicles, Others), by End User (Automotive OEMs, Tier-1 Automotive Suppliers, Automotive Aftermarket Service Providers, Research & Development Organizations), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 71

Key Insights into Acoustic Metamaterials for Automotive Market

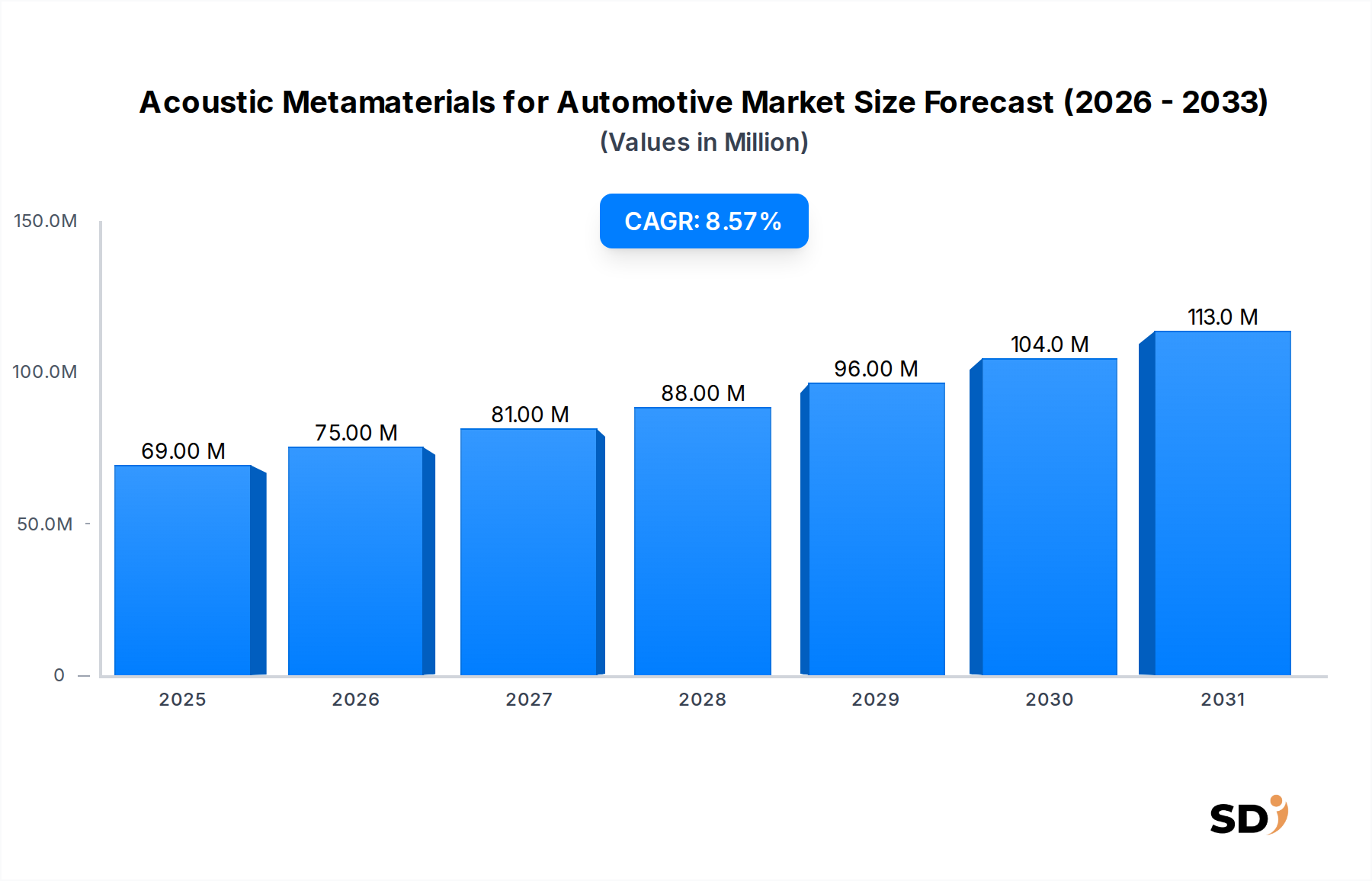

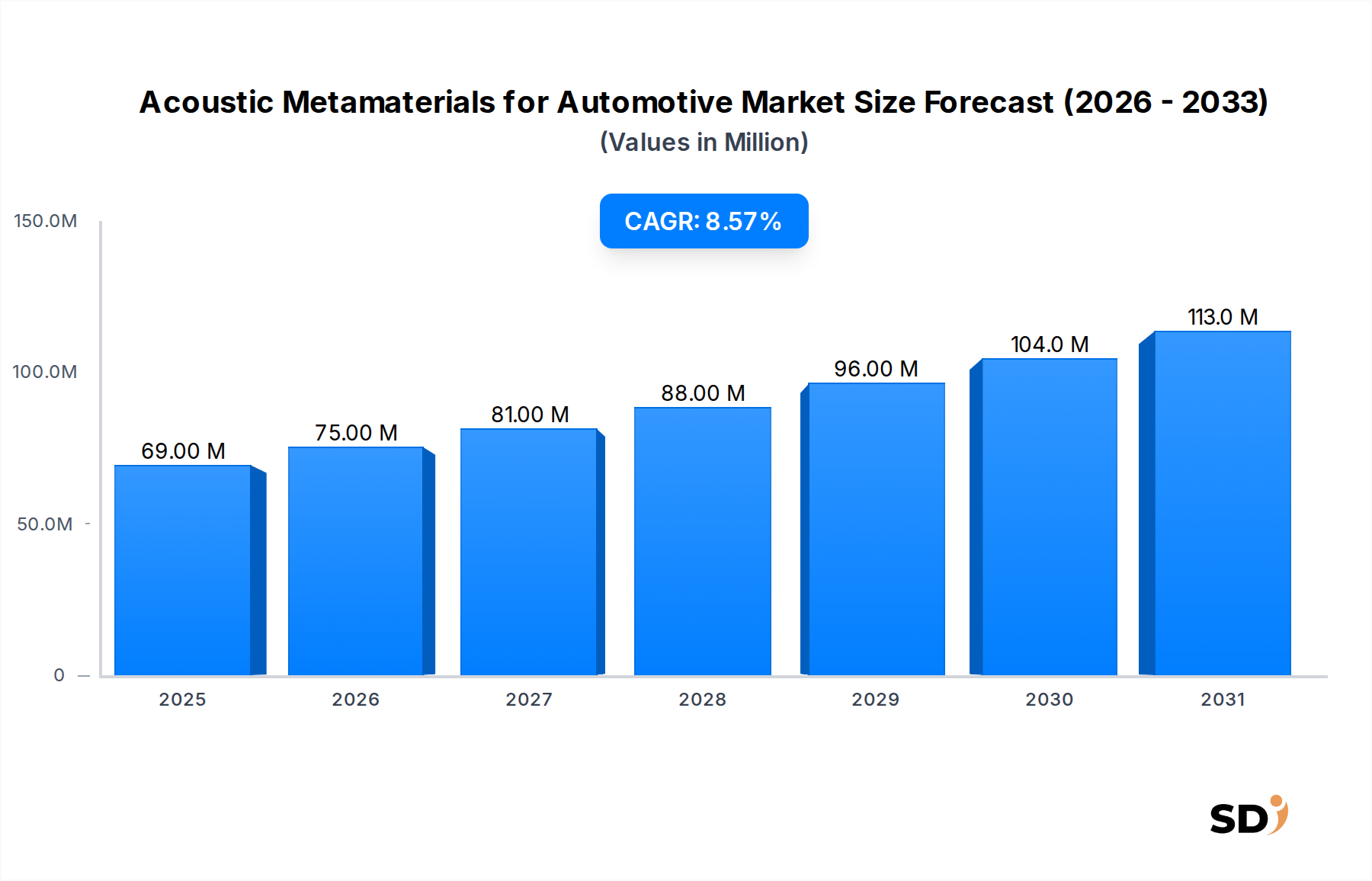

The Global Acoustic Metamaterials for Automotive Market, valued at an estimated $69 million in 2026, is poised for substantial expansion, projecting an impressive Compound Annual Growth Rate (CAGR) of 8.5% through 2033. This growth trajectory is anticipated to elevate the market to approximately $123.5 million by the end of the forecast period. The fundamental driver underpinning this vigorous expansion is the automotive industry's relentless pursuit of enhanced cabin comfort, coupled with increasingly stringent noise, vibration, and harshness (NVH) regulations. Acoustic metamaterials, engineered structures with properties beyond those found in nature, offer unprecedented control over sound waves, enabling superior noise attenuation and absorption within compact and lightweight designs. This makes them particularly appealing for modern vehicle architectures, where space and weight optimization are critical.

Acoustic Metamaterials for Automotive Market Size (In Million)

150.0M

100.0M

50.0M

0

69.00 M

2025

75.00 M

2026

81.00 M

2027

88.00 M

2028

96.00 M

2029

104.0 M

2030

113.0 M

2031

The advent and widespread adoption of electric vehicles (EVs) have significantly reshaped the acoustic landscape, foregrounding noise sources previously masked by internal combustion engines. As powertrain noise diminishes, road noise, tire noise, and wind noise become more pronounced, demanding sophisticated solutions that traditional materials often cannot provide without incurring significant weight penalties. Acoustic metamaterials present a compelling answer to this challenge, offering targeted sound manipulation capabilities, such as frequency-selective absorption and anomalous transmission, that can be precisely tuned to address specific noise profiles. Furthermore, the growing consumer expectation for a premium in-cabin experience, characterized by quietness and reduced fatigue, is compelling Automotive OEMs and Tier-1 Automotive Suppliers to integrate these innovative materials. The broader Advanced Materials Market is observing this niche with keen interest, recognizing the potential for cross-sector applications.

Challenges, however, persist, notably concerning the scalability of manufacturing processes, the relatively high production costs associated with intricate metamaterial designs, and the need for robust integration into existing automotive assembly lines. Despite these hurdles, ongoing research and development, coupled with advancements in additive manufacturing and material science, are steadily overcoming these constraints. The market is also seeing increasing activity in the Acoustic Panels Market, where these next-gen materials are being incorporated to provide thinner, lighter, and more effective sound barriers. The overarching outlook remains highly optimistic, driven by innovation and a clear demand for next-generation acoustic solutions capable of meeting the evolving performance and efficiency demands of the global automotive sector.

Dominant Segment: Cabin Noise Reduction in Acoustic Metamaterials for Automotive Market

Within the diverse application landscape of the Acoustic Metamaterials for Automotive Market, the "Cabin Noise Reduction" segment stands as the unequivocal revenue leader. This dominance is intrinsically linked to the core value proposition of vehicle ownership: passenger comfort and the driving experience. A quiet cabin is not merely a luxury but a fundamental expectation in modern vehicles, directly influencing brand perception, customer satisfaction, and overall vehicle quality. The imperative to minimize interior noise, vibration, and harshness (NVH) has become more pronounced with the rapid transition towards electric vehicles. In EVs, the absence of engine noise amplifies other ambient sounds, such as road-tire interaction, aerodynamic whistle, and structural vibrations, making traditional acoustic treatments less effective or prohibitively heavy.

Acoustic metamaterials offer a paradigm shift in addressing these persistent noise challenges. Unlike conventional Acoustic Insulation Materials Market products that rely on mass and porous absorption, metamaterials can achieve significant noise reduction at a fraction of the weight and thickness. Their ability to manipulate sound waves at sub-wavelength scales allows for the creation of lightweight acoustic barriers, sound-absorbing surfaces, and noise-canceling structures that can be precisely tuned to target specific problematic frequencies. This is particularly crucial for "Cabin Noise Reduction," where space is at a premium and every gram of weight impacts vehicle range and performance. The Lightweight Materials Market intersects significantly here, as metamaterials offer a dual benefit of superior acoustic performance and weight reduction, a key objective for automotive designers striving for fuel efficiency and extended EV battery life.

Key players in this dominant segment include specialized metamaterials developers working in close collaboration with Automotive OEMs and Tier-1 Automotive Suppliers. These collaborations focus on integrating these advanced materials into vehicle headliners, floor pans, door panels, dashboards, and trunk areas. The segment's market share is not only significant but also poised for continued growth. This sustained expansion is fueled by increasing consumer demand for quieter, more serene interior environments, particularly in premium and luxury vehicle segments, and the escalating need for effective NVH management in the burgeoning Electric Vehicle Component Market. As manufacturing processes mature and costs decline through economies of scale and advanced fabrication techniques like 3D printing, the penetration of acoustic metamaterials in the "Cabin Noise Reduction" segment is expected to deepen, further solidifying its leading position within the Acoustic Metamaterials for Automotive Market. The continuous drive for innovation in the Automotive Noise Reduction Market ensures that this segment will remain at the forefront of market development.

Key Market Drivers & Constraints in Acoustic Metamaterials for Automotive Market

The Acoustic Metamaterials for Automotive Market is shaped by a confluence of powerful drivers and inherent constraints, each influencing its trajectory. A primary driver is the escalating consumer demand for superior in-cabin comfort and quieter driving experiences. With the average daily commute increasing and a growing preference for premium vehicle features, noise reduction has become a significant differentiator. Consumers increasingly seek vehicles that offer a serene environment, free from intrusive road, engine, and wind noise. This direct consumer pull translates into OEMs prioritizing advanced NVH solutions, thereby boosting the demand for sophisticated materials like acoustic metamaterials.

Another critical driver is the transformative shift towards electric vehicles (EVs). As highlighted, the absence of a traditional internal combustion engine unmasks other noise sources, presenting new challenges for automotive acoustic engineers. Metamaterials, with their ability to precisely control sound waves across various frequencies, offer bespoke solutions for mitigating tire roar, motor whine, and aerodynamic noise in EVs. This technological synergy with the Electric Vehicle Component Market is a powerful catalyst for growth. Furthermore, global regulatory bodies are continually tightening noise emission standards for vehicles, both interior and exterior. These stricter regulations, particularly in regions like Europe and North America, mandate the adoption of more effective and often lighter acoustic treatments, positioning metamaterials as an ideal compliance solution. The Sound Absorbing Materials Market as a whole is seeing a push towards more efficient, thinner, and lighter options, with metamaterials at the cutting edge.

However, the market faces significant constraints. The high manufacturing complexity of acoustic metamaterials is a notable barrier. Designing and fabricating these structures, which often involve intricate geometric patterns at sub-wavelength scales, requires specialized tooling, advanced materials, and precise manufacturing processes, leading to elevated production costs compared to conventional damping materials. This cost factor can deter mass-market adoption. Secondly, scalability remains a challenge. While prototypes demonstrate exceptional performance, transitioning from laboratory-scale production to the high-volume requirements of the automotive industry is complex. Ensuring consistent quality and performance across millions of units necessitates robust and cost-effective manufacturing techniques. Finally, the integration of novel materials into existing automotive supply chains and vehicle architectures presents hurdles, including material compatibility, durability in harsh automotive environments, and regulatory approval. The adoption of new materials such as those for the Polymer Composites Market in automotive requires extensive validation, adding to development timelines and costs.

Competitive Ecosystem of Acoustic Metamaterials for Automotive Market

The competitive landscape of the Acoustic Metamaterials for Automotive Market is characterized by specialized firms, often emerging from strong R&D backgrounds, collaborating with larger automotive entities. These companies are focused on innovating material science and manufacturing processes to deliver advanced acoustic solutions.

Applied Metamaterials: A key player leveraging its expertise in engineered materials to develop lightweight and high-performance acoustic solutions for the automotive sector. The company focuses on customized designs that meet specific NVH requirements, addressing complex noise issues in modern vehicles.

Merford: While known for broader industrial acoustic solutions, Merford is increasingly applying its sound control expertise to automotive applications, developing tailored systems that can incorporate metamaterial principles for enhanced noise reduction and acoustic comfort.

Lios: Specializes in advanced lightweight insulation materials and acoustic solutions, exploring metamaterial structures to achieve superior sound absorption and damping properties. Lios aims to integrate these innovations into vehicle interiors to improve driver and passenger experience.

Metacoustic: Focused specifically on the development and commercialization of acoustic metamaterial technologies, Metacoustic is a pure-play contender. The company is at the forefront of designing and producing engineered structures that offer unprecedented control over sound waves for various automotive noise reduction applications. This innovation supports the broader Automotive Components Market by introducing novel solutions for acoustic management.

Recent Developments & Milestones in Acoustic Metamaterials for Automotive Market

Recent developments in the Acoustic Metamaterials for Automotive Market underscore a dynamic environment characterized by research breakthroughs, strategic partnerships, and advancements in manufacturing, all aimed at bringing these innovative solutions to commercial viability and scale.

Q4 2023: Several research institutions and companies announced breakthroughs in 3D printing techniques for acoustic metamaterials, enabling the creation of complex, high-performance structures with greater precision and at potentially lower costs. This development is crucial for expanding the Advanced Materials Market applications within automotive.

Q3 2023: A leading automotive OEM partnered with a metamaterials startup to integrate prototype acoustic metamaterial liners into an upcoming electric vehicle platform. This collaboration aims to test the real-world performance of lightweight noise-reduction solutions in a production-oriented environment.

Q2 2023: Development of new bio-inspired acoustic metamaterial designs, utilizing natural geometries and material combinations to achieve broadband sound absorption. This research highlights efforts towards more sustainable and environmentally friendly acoustic solutions for the automotive industry.

Q1 2023: Introduction of advanced simulation software tools specifically tailored for the design and optimization of acoustic metamaterials. These tools reduce development cycles and facilitate more efficient prototyping, thereby accelerating market adoption.

Q4 2022: Successful validation of a novel lightweight acoustic metamaterial panel that significantly reduced road noise within a test vehicle, demonstrating comparable performance to traditional heavy damping materials but with a substantial weight saving. This directly impacts the Automotive Noise Reduction Market by offering more efficient solutions.

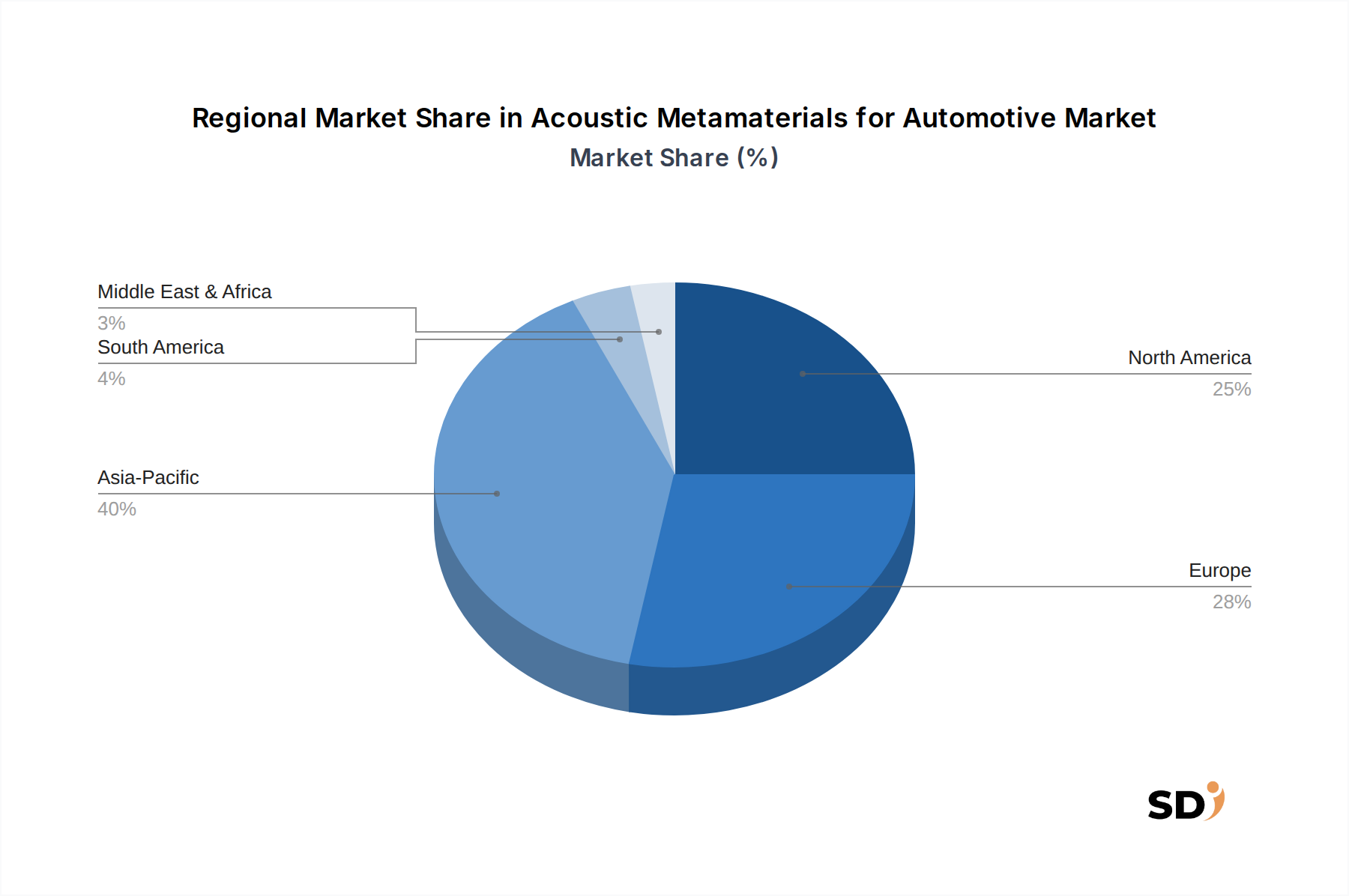

Regional Market Breakdown for Acoustic Metamaterials for Automotive Market

Global demand for acoustic metamaterials in automotive applications exhibits significant regional variations, driven by differing regulatory landscapes, automotive production volumes, and consumer preferences. While specific regional CAGR and revenue shares are dynamic, an analysis of the primary demand drivers offers clear insights.

Asia Pacific currently represents the largest market share and is projected to be the fastest-growing region in the Acoustic Metamaterials for Automotive Market. This dominance is primarily attributable to the colossal automotive production base, particularly in countries like China, Japan, South Korea, and India. The rapid adoption and manufacturing of electric vehicles (EVs) in this region further amplify the demand for advanced acoustic solutions, as EV manufacturers seek competitive advantages through superior cabin quietness. Increasing disposable incomes and a growing consumer preference for premium features also contribute to the demand for sophisticated NVH management.

Europe holds a substantial share, driven by its stringent NVH regulations and a strong presence of premium and luxury automotive brands that prioritize advanced acoustic comfort. Countries like Germany, France, and the UK are at the forefront of automotive innovation and EV transition, creating a fertile ground for the adoption of acoustic metamaterials. The region's emphasis on vehicle lightweighting for CO2 emission reduction also aligns well with the properties of these materials.

North America is another significant market, characterized by a robust automotive industry, a high demand for large SUVs and trucks where noise cancellation is paramount, and a strong emphasis on technological innovation. The increasing penetration of EVs and autonomous vehicles in the United States and Canada is driving R&D and pilot projects for integrating advanced acoustic metamaterials to enhance the passenger experience. The Automotive Noise Reduction Market in North America is particularly receptive to new technologies.

Middle East & Africa and South America currently represent nascent markets for acoustic metamaterials in automotive. While automotive production is lower compared to other regions, growing urbanization, improving economic conditions, and increasing foreign investment in automotive manufacturing hubs are expected to spur demand in the long term. However, adoption rates are slower due to cost considerations and a less mature regulatory environment for advanced NVH. Overall, the Asia Pacific region is expected to lead in both volume and growth, while Europe and North America will continue to be critical markets for innovation and high-value applications.

Supply Chain & Raw Material Dynamics for Acoustic Metamaterials for Automotive Market

The supply chain for Acoustic Metamaterials for Automotive Market is inherently complex, given the specialized nature of the materials and intricate manufacturing processes. Upstream dependencies typically involve a range of advanced raw materials, including high-performance polymers, specialty metals (such as aluminum and titanium alloys for structural components), and occasionally ceramics for specific high-frequency attenuation applications. The design freedom offered by these materials, especially for the Lightweight Materials Market, is a significant advantage. The core of metamaterial fabrication often relies on precision manufacturing techniques, including advanced injection molding, additive manufacturing (3D printing), and micro-machining, which in turn require specialized equipment and skilled labor.

Sourcing risks are prevalent and multifaceted. Geopolitical instabilities, trade restrictions, and natural disasters can disrupt the supply of key raw materials, particularly those with concentrated global supply chains. For example, the availability and price volatility of certain specialty polymers, often derivatives of petrochemicals, can be affected by fluctuations in crude oil prices and global refinery output. Similarly, the extraction and processing of metals are susceptible to mining disruptions and environmental regulations. Recent global supply chain disruptions, notably during the COVID-19 pandemic and subsequent geopolitical events, have highlighted vulnerabilities, leading to delays in material procurement and increased lead times for specialized components. This also impacts the Polymer Composites Market, which is a significant input sector.

Price volatility of key inputs directly impacts the overall cost structure of acoustic metamaterials. For instance, the price of engineering plastics and advanced resins has seen significant fluctuations, influenced by feedstock costs, energy prices, and demand from other industrial sectors. Manufacturers in the Acoustic Metamaterials for Automotive Market must strategically manage these material costs through long-term supply agreements, diversification of suppliers, and exploring alternative material compositions. Historical disruptions have demonstrated that a resilient supply chain, capable of adapting to sudden shifts in material availability and pricing, is crucial for sustained market growth and profitability. The drive for miniaturization and performance within the Sound Absorbing Materials Market means that even small fluctuations in raw material costs can have a magnified impact on the final product's economics.

Sustainability & ESG Pressures on Acoustic Metamaterials for Automotive Market

The Acoustic Metamaterials for Automotive Market is increasingly subject to rigorous sustainability and ESG (Environmental, Social, and Governance) pressures, fundamentally reshaping product development and procurement strategies. Environmental regulations, particularly those originating from the European Union and progressive national governments, are driving a paradigm shift towards materials with lower lifecycle environmental impacts. This includes mandates for reduced volatile organic compounds (VOCs) in interior materials and an emphasis on recyclability and circular economy principles for all automotive components. Metamaterial developers are thus compelled to explore bio-based polymers, recycled content, and designs that facilitate easy disassembly and material recovery at the end of a vehicle's life.

Carbon targets, both corporate and governmental, are exerting significant pressure on the embodied carbon footprint of materials used in vehicle manufacturing. While acoustic metamaterials offer lightweighting benefits that reduce operational carbon emissions (fuel consumption or EV energy use), their production process and raw material sourcing must also align with decarbonization goals. This involves scrutinizing the energy intensity of manufacturing processes and sourcing materials from suppliers committed to renewable energy and sustainable practices. The overall Sound Absorbing Materials Market is observing a shift towards greener solutions, and metamaterials are no exception.

Circular economy mandates are fostering innovation in material science within the Acoustic Metamaterials for Automotive Market. The focus is on creating closed-loop systems where materials can be re-used or recycled effectively, minimizing waste. This often means designing metamaterial structures that can be easily separated from other vehicle components, or developing thermoplastic composites that can be melted down and reformed. ESG investor criteria are further amplifying these pressures. Investors are increasingly evaluating companies not just on financial performance but also on their environmental stewardship, social responsibility, and governance practices. Companies demonstrating strong ESG credentials often benefit from lower cost of capital and enhanced brand reputation, driving further investment in sustainable R&D and responsible manufacturing processes.

These pressures are leading to a new era of innovation in acoustic metamaterials, where performance is balanced with ecological responsibility. The industry is moving towards developing solutions that are not only superior in noise attenuation but also contribute positively to the vehicle's overall sustainability profile, ensuring long-term viability and market acceptance.

Acoustic Metamaterials for Automotive Segmentation

1. Product Type

1.1. Acoustic Panels

1.2. Acoustic Insulation Materials

1.3. Acoustic Liners

1.4. Sound Absorbing Metamaterials

2. Application

2.1. Cabin Noise Reduction

2.2. Engine Noise Control

2.3. Powertrain Noise Management

2.4. Road Noise Reduction

2.5. Tire Noise Attenuation

2.6. Others

3. Vehicle Type

3.1. Passenger Vehicles

3.2. Commercial Vehicles

3.3. Others

4. End User

4.1. Automotive OEMs

4.2. Tier-1 Automotive Suppliers

4.3. Automotive Aftermarket Service Providers

4.4. Research & Development Organizations

Acoustic Metamaterials for Automotive Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Acoustic Metamaterials for Automotive REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 8.5% from 2020-2034

Segmentation

By Product Type

Acoustic Panels

Acoustic Insulation Materials

Acoustic Liners

Sound Absorbing Metamaterials

By Application

Cabin Noise Reduction

Engine Noise Control

Powertrain Noise Management

Road Noise Reduction

Tire Noise Attenuation

Others

By Vehicle Type

Passenger Vehicles

Commercial Vehicles

Others

By End User

Automotive OEMs

Tier-1 Automotive Suppliers

Automotive Aftermarket Service Providers

Research & Development Organizations

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Type

5.1.1. Acoustic Panels

5.1.2. Acoustic Insulation Materials

5.1.3. Acoustic Liners

5.1.4. Sound Absorbing Metamaterials

5.2. Market Analysis, Insights and Forecast - by Application

5.2.1. Cabin Noise Reduction

5.2.2. Engine Noise Control

5.2.3. Powertrain Noise Management

5.2.4. Road Noise Reduction

5.2.5. Tire Noise Attenuation

5.2.6. Others

5.3. Market Analysis, Insights and Forecast - by Vehicle Type

5.3.1. Passenger Vehicles

5.3.2. Commercial Vehicles

5.3.3. Others

5.4. Market Analysis, Insights and Forecast - by End User

5.4.1. Automotive OEMs

5.4.2. Tier-1 Automotive Suppliers

5.4.3. Automotive Aftermarket Service Providers

5.4.4. Research & Development Organizations

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Product Type

6.1.1. Acoustic Panels

6.1.2. Acoustic Insulation Materials

6.1.3. Acoustic Liners

6.1.4. Sound Absorbing Metamaterials

6.2. Market Analysis, Insights and Forecast - by Application

6.2.1. Cabin Noise Reduction

6.2.2. Engine Noise Control

6.2.3. Powertrain Noise Management

6.2.4. Road Noise Reduction

6.2.5. Tire Noise Attenuation

6.2.6. Others

6.3. Market Analysis, Insights and Forecast - by Vehicle Type

6.3.1. Passenger Vehicles

6.3.2. Commercial Vehicles

6.3.3. Others

6.4. Market Analysis, Insights and Forecast - by End User

6.4.1. Automotive OEMs

6.4.2. Tier-1 Automotive Suppliers

6.4.3. Automotive Aftermarket Service Providers

6.4.4. Research & Development Organizations

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Product Type

7.1.1. Acoustic Panels

7.1.2. Acoustic Insulation Materials

7.1.3. Acoustic Liners

7.1.4. Sound Absorbing Metamaterials

7.2. Market Analysis, Insights and Forecast - by Application

7.2.1. Cabin Noise Reduction

7.2.2. Engine Noise Control

7.2.3. Powertrain Noise Management

7.2.4. Road Noise Reduction

7.2.5. Tire Noise Attenuation

7.2.6. Others

7.3. Market Analysis, Insights and Forecast - by Vehicle Type

7.3.1. Passenger Vehicles

7.3.2. Commercial Vehicles

7.3.3. Others

7.4. Market Analysis, Insights and Forecast - by End User

7.4.1. Automotive OEMs

7.4.2. Tier-1 Automotive Suppliers

7.4.3. Automotive Aftermarket Service Providers

7.4.4. Research & Development Organizations

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Product Type

8.1.1. Acoustic Panels

8.1.2. Acoustic Insulation Materials

8.1.3. Acoustic Liners

8.1.4. Sound Absorbing Metamaterials

8.2. Market Analysis, Insights and Forecast - by Application

8.2.1. Cabin Noise Reduction

8.2.2. Engine Noise Control

8.2.3. Powertrain Noise Management

8.2.4. Road Noise Reduction

8.2.5. Tire Noise Attenuation

8.2.6. Others

8.3. Market Analysis, Insights and Forecast - by Vehicle Type

8.3.1. Passenger Vehicles

8.3.2. Commercial Vehicles

8.3.3. Others

8.4. Market Analysis, Insights and Forecast - by End User

8.4.1. Automotive OEMs

8.4.2. Tier-1 Automotive Suppliers

8.4.3. Automotive Aftermarket Service Providers

8.4.4. Research & Development Organizations

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Product Type

9.1.1. Acoustic Panels

9.1.2. Acoustic Insulation Materials

9.1.3. Acoustic Liners

9.1.4. Sound Absorbing Metamaterials

9.2. Market Analysis, Insights and Forecast - by Application

9.2.1. Cabin Noise Reduction

9.2.2. Engine Noise Control

9.2.3. Powertrain Noise Management

9.2.4. Road Noise Reduction

9.2.5. Tire Noise Attenuation

9.2.6. Others

9.3. Market Analysis, Insights and Forecast - by Vehicle Type

9.3.1. Passenger Vehicles

9.3.2. Commercial Vehicles

9.3.3. Others

9.4. Market Analysis, Insights and Forecast - by End User

9.4.1. Automotive OEMs

9.4.2. Tier-1 Automotive Suppliers

9.4.3. Automotive Aftermarket Service Providers

9.4.4. Research & Development Organizations

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Product Type

10.1.1. Acoustic Panels

10.1.2. Acoustic Insulation Materials

10.1.3. Acoustic Liners

10.1.4. Sound Absorbing Metamaterials

10.2. Market Analysis, Insights and Forecast - by Application

10.2.1. Cabin Noise Reduction

10.2.2. Engine Noise Control

10.2.3. Powertrain Noise Management

10.2.4. Road Noise Reduction

10.2.5. Tire Noise Attenuation

10.2.6. Others

10.3. Market Analysis, Insights and Forecast - by Vehicle Type

10.3.1. Passenger Vehicles

10.3.2. Commercial Vehicles

10.3.3. Others

10.4. Market Analysis, Insights and Forecast - by End User

10.4.1. Automotive OEMs

10.4.2. Tier-1 Automotive Suppliers

10.4.3. Automotive Aftermarket Service Providers

10.4.4. Research & Development Organizations

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Applied Metamaterials

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Merford

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Lios

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Metacoustic

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Product Type 2025 & 2033

Figure 3: Revenue Share (%), by Product Type 2025 & 2033

Figure 4: Revenue (million), by Application 2025 & 2033

Figure 5: Revenue Share (%), by Application 2025 & 2033

Figure 6: Revenue (million), by Vehicle Type 2025 & 2033

Figure 7: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 8: Revenue (million), by End User 2025 & 2033

Figure 9: Revenue Share (%), by End User 2025 & 2033

Figure 10: Revenue (million), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (million), by Product Type 2025 & 2033

Figure 13: Revenue Share (%), by Product Type 2025 & 2033

Figure 14: Revenue (million), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (million), by Vehicle Type 2025 & 2033

Figure 17: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 18: Revenue (million), by End User 2025 & 2033

Figure 19: Revenue Share (%), by End User 2025 & 2033

Figure 20: Revenue (million), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (million), by Product Type 2025 & 2033

Figure 23: Revenue Share (%), by Product Type 2025 & 2033

Figure 24: Revenue (million), by Application 2025 & 2033

Figure 25: Revenue Share (%), by Application 2025 & 2033

Figure 26: Revenue (million), by Vehicle Type 2025 & 2033

Figure 27: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 28: Revenue (million), by End User 2025 & 2033

Figure 29: Revenue Share (%), by End User 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (million), by Product Type 2025 & 2033

Figure 33: Revenue Share (%), by Product Type 2025 & 2033

Figure 34: Revenue (million), by Application 2025 & 2033

Figure 35: Revenue Share (%), by Application 2025 & 2033

Figure 36: Revenue (million), by Vehicle Type 2025 & 2033

Figure 37: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 38: Revenue (million), by End User 2025 & 2033

Figure 39: Revenue Share (%), by End User 2025 & 2033

Figure 40: Revenue (million), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (million), by Product Type 2025 & 2033

Figure 43: Revenue Share (%), by Product Type 2025 & 2033

Figure 44: Revenue (million), by Application 2025 & 2033

Figure 45: Revenue Share (%), by Application 2025 & 2033

Figure 46: Revenue (million), by Vehicle Type 2025 & 2033

Figure 47: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 48: Revenue (million), by End User 2025 & 2033

Figure 49: Revenue Share (%), by End User 2025 & 2033

Figure 50: Revenue (million), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Product Type 2020 & 2033

Table 2: Revenue million Forecast, by Application 2020 & 2033

Table 3: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 4: Revenue million Forecast, by End User 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Revenue million Forecast, by Product Type 2020 & 2033

Table 7: Revenue million Forecast, by Application 2020 & 2033

Table 8: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 9: Revenue million Forecast, by End User 2020 & 2033

Table 10: Revenue million Forecast, by Country 2020 & 2033

Table 11: Revenue (million) Forecast, by Application 2020 & 2033

Table 12: Revenue (million) Forecast, by Application 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue million Forecast, by Product Type 2020 & 2033

Table 15: Revenue million Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 17: Revenue million Forecast, by End User 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue million Forecast, by Product Type 2020 & 2033

Table 23: Revenue million Forecast, by Application 2020 & 2033

Table 24: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 25: Revenue million Forecast, by End User 2020 & 2033

Table 26: Revenue million Forecast, by Country 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue (million) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Revenue (million) Forecast, by Application 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue million Forecast, by Product Type 2020 & 2033

Table 37: Revenue million Forecast, by Application 2020 & 2033

Table 38: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 39: Revenue million Forecast, by End User 2020 & 2033

Table 40: Revenue million Forecast, by Country 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Table 47: Revenue million Forecast, by Product Type 2020 & 2033

Table 48: Revenue million Forecast, by Application 2020 & 2033

Table 49: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 50: Revenue million Forecast, by End User 2020 & 2033

Table 51: Revenue million Forecast, by Country 2020 & 2033

Table 52: Revenue (million) Forecast, by Application 2020 & 2033

Table 53: Revenue (million) Forecast, by Application 2020 & 2033

Table 54: Revenue (million) Forecast, by Application 2020 & 2033

Table 55: Revenue (million) Forecast, by Application 2020 & 2033

Table 56: Revenue (million) Forecast, by Application 2020 & 2033

Table 57: Revenue (million) Forecast, by Application 2020 & 2033

Table 58: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research forms the cornerstone of this report, accounting for approximately 75% of the total research effort. This extensive phase involves direct engagement with key stakeholders across the value chain of the acoustic metamaterials for automotive market. We employ a structured approach, conducting in-depth interviews, expert panels, and detailed surveys. The insights gathered are critical for validating secondary data, understanding market dynamics, identifying emerging trends, and capturing nuanced perspectives on technological advancements and adoption rates.

Secondary research constitutes approximately 25% of our overall methodology and serves as a foundational layer for market understanding and initial data validation. This phase involves a rigorous review of published data, industry reports, and financial filings to establish baseline market parameters, identify competitive landscapes, and track technological innovations. Our approach emphasizes credible and authoritative sources to ensure data integrity.

Key sources utilized include:

Financial Databases: Bloomberg, Factiva, Hoovers, PitchBook for company profiles, financial performance, and investment trends.

Government & Regulatory Bodies: Publications from governmental agencies focusing on transportation, environmental regulations, and materials science. Examples include reports from the U.S. Department of Transportation (www.transportation.gov) and the European Environment Agency (www.eea.europa.eu).

Trade Associations & Industry Organizations: Data, standards, and reports from recognized industry bodies relevant to automotive and acoustics. Examples include SAE International (www.sae.org), ISO (International Organization for Standardization) for acoustic measurement standards (www.iso.org), European Acoustics Association (EAA) (euracoustics.org), and Automotive Industry Action Group (AIAG) (www.aiag.org).

Company Annual Reports and Investor Presentations: Direct filings and communications from public and private companies active in the market.

Academic Research and Journals: Peer-reviewed publications on acoustic metamaterials, material science, and automotive NVH.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies leverage a sophisticated combination of top-down and bottom-up approaches, coupled with multi-level data triangulation to ensure robust estimations. This integrated strategy allows for a comprehensive assessment of the market from both macro and micro perspectives.

Bottom-Up Approach: This method involves aggregating market size estimations from granular levels. Key metrics and variables used for bottom-up calculation include:

New Vehicle Production Volumes (segmented by Passenger Vehicles and Commercial Vehicles)

Average Metamaterial Content (volume/area/weight) per vehicle, by specific application area (e.g., cabin, engine bay, wheel wells).

Average Selling Price (ASP) of Acoustic Metamaterial solutions per unit (e.g., per panel, per kg, per m²).

Penetration Rate of Acoustic Metamaterials in various vehicle segments (e.g., luxury, premium, mid-range, and electric vehicles).

Top-Down Approach: This method estimates the overall market size based on macro-economic factors, industry growth drivers, and total addressable market analyses. We consider factors such as global automotive production trends, NVH solution spending by OEMs, and regulatory pressures for quiet vehicle interiors.

Multi-Level Data Triangulation: Data from both primary and secondary sources, and from top-down and bottom-up analyses, are cross-referenced and validated at various stages. This iterative process helps in identifying discrepancies, refining assumptions, and converging on the most accurate market figures.

Data Accuracy & Quality Check

Maintaining the highest standards of data accuracy and reliability is paramount to our research. We guarantee an estimated data accuracy level of 88% for all market figures presented in this report. Our quality control process is rigorous and multi-faceted:

Validation: All quantitative data points derived from secondary research are validated through primary interviews with industry experts. Conversely, insights from primary interviews are cross-verified with available secondary data.

Forecasting Models: Our proprietary forecasting models incorporate multiple variables and statistical techniques (e.g., regression analysis, time-series analysis) to project market trends and future growth accurately.

Expert Review: The entire research output undergoes a thorough review by senior analysts and domain experts to ensure consistency, logical coherence, and alignment with industry realities.

Up-to-Date Information: Every report is dynamically updated up to the date of purchase, ensuring that clients receive the most current market intelligence, reflecting the latest industry developments, economic shifts, and technological advancements. This includes incorporating recent mergers, acquisitions, product launches, and regulatory changes impacting the acoustic metamaterials for automotive market.

Frequently Asked Questions

1. How do consumer preferences impact the Acoustic Metamaterials for Automotive market?

Consumer demand for quieter, more comfortable vehicle cabins and enhanced driving experiences drives market growth. This preference influences OEM decisions to integrate advanced noise reduction solutions, including metamaterials, in new vehicle models. The focus is on reducing cabin noise and improving overall acoustic comfort.

2. Which region leads the Acoustic Metamaterials for Automotive market, and why?

Asia-Pacific is estimated to be the dominant region for Acoustic Metamaterials for Automotive. This leadership is primarily due to the region's high volume of automotive manufacturing, particularly in countries like China, Japan, and South Korea, coupled with increasing adoption of advanced materials in vehicles to meet consumer expectations and emerging regulations.

3. What are the key pricing trends and cost structure dynamics in Acoustic Metamaterials for Automotive?

Pricing in the acoustic metamaterials market for automotive applications is influenced by R&D costs, material sophistication, and production scale. While initial costs for novel metamaterials can be higher, increasing adoption, particularly in segments like Passenger Vehicles, is expected to drive down unit costs through economies of scale. Cost-efficiency in material sourcing is a continuous focus for suppliers.

4. How does raw material sourcing affect the Acoustic Metamaterials for Automotive supply chain?

Raw material sourcing for acoustic metamaterials depends on the specific product type, such as Acoustic Panels or Sound Absorbing Metamaterials. The supply chain involves specialized material providers, with companies like Applied Metamaterials focusing on advanced material composition. Reliability in sourcing ensures consistent production for Automotive OEMs and Tier-1 Automotive Suppliers.

5. Who are the primary end-users driving demand for Acoustic Metamaterials for Automotive?

Automotive OEMs and Tier-1 Automotive Suppliers are the primary end-users, accounting for significant demand. They integrate these materials into Passenger Vehicles and Commercial Vehicles for applications like Cabin Noise Reduction and Engine Noise Control. The Automotive Aftermarket Service Providers also contribute to downstream demand for replacement or upgrade solutions.

6. What are the significant challenges impacting the Acoustic Metamaterials for Automotive market?

A key challenge involves the integration complexity of new materials into existing automotive manufacturing processes. Cost-effectiveness at mass production scales can also be a restraint, especially for advanced Sound Absorbing Metamaterials. Ensuring consistent material performance across diverse vehicle types and environmental conditions is another technical hurdle.