Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Accommodating Intraocular Lens Market: $4.1B by 2026, 5.4% CAGR

Accommodating Intraocular Lens

Accommodating Intraocular Lens Market: $4.1B by 2026, 5.4% CAGR

Accommodating Intraocular Lens by Product Type (Single-Piece, Multi-Piece), by Material (Hydrophobic Acrylic, Hydrophilic Acrylic, Polymethyl Methacrylate, Silicone Lenses, Others), by End-User (Hospitals, Ophthalmic Clinics, Ambulatory Surgery Centers, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 110

Key Insights into the Accommodating Intraocular Lens Market

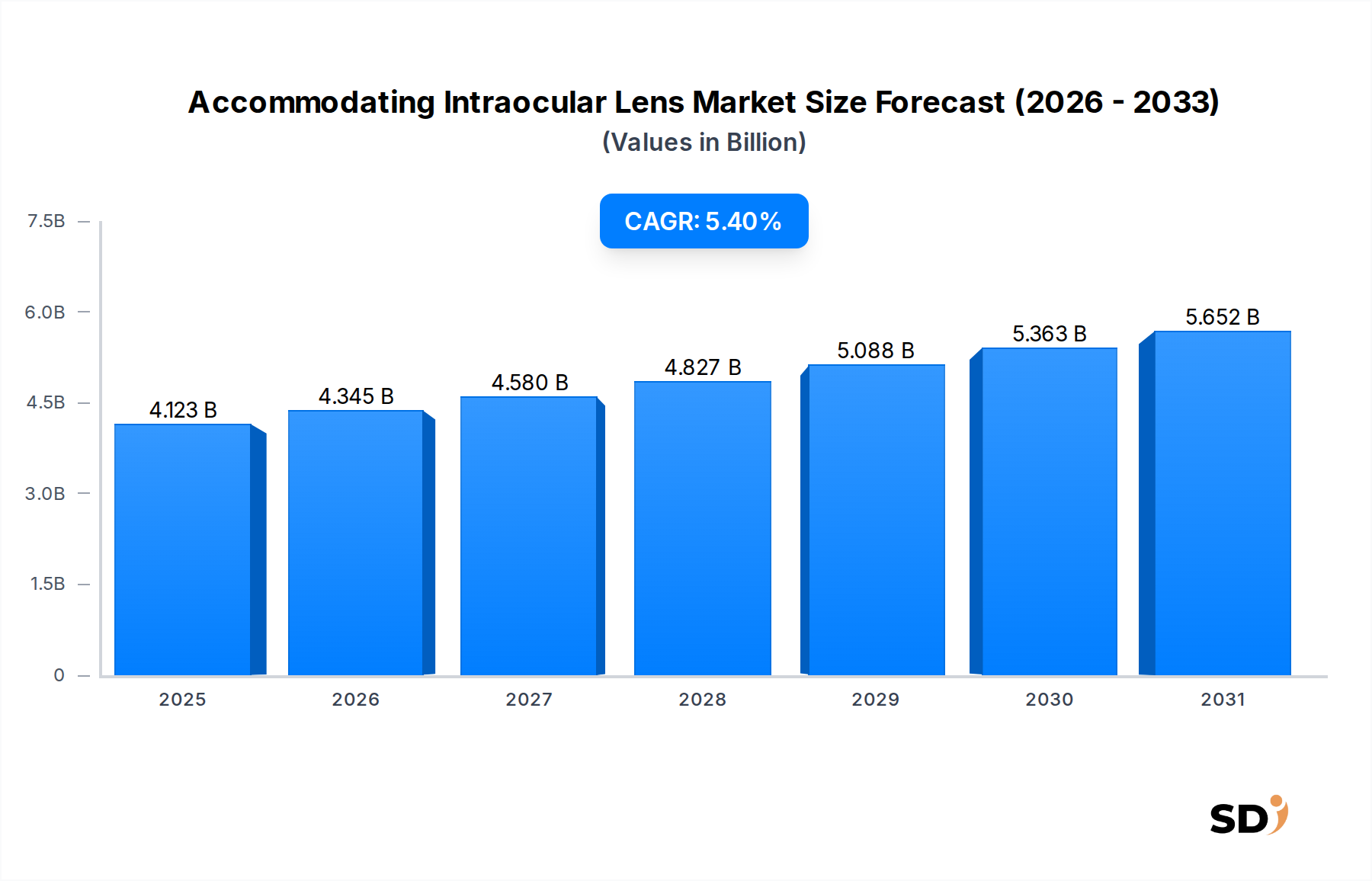

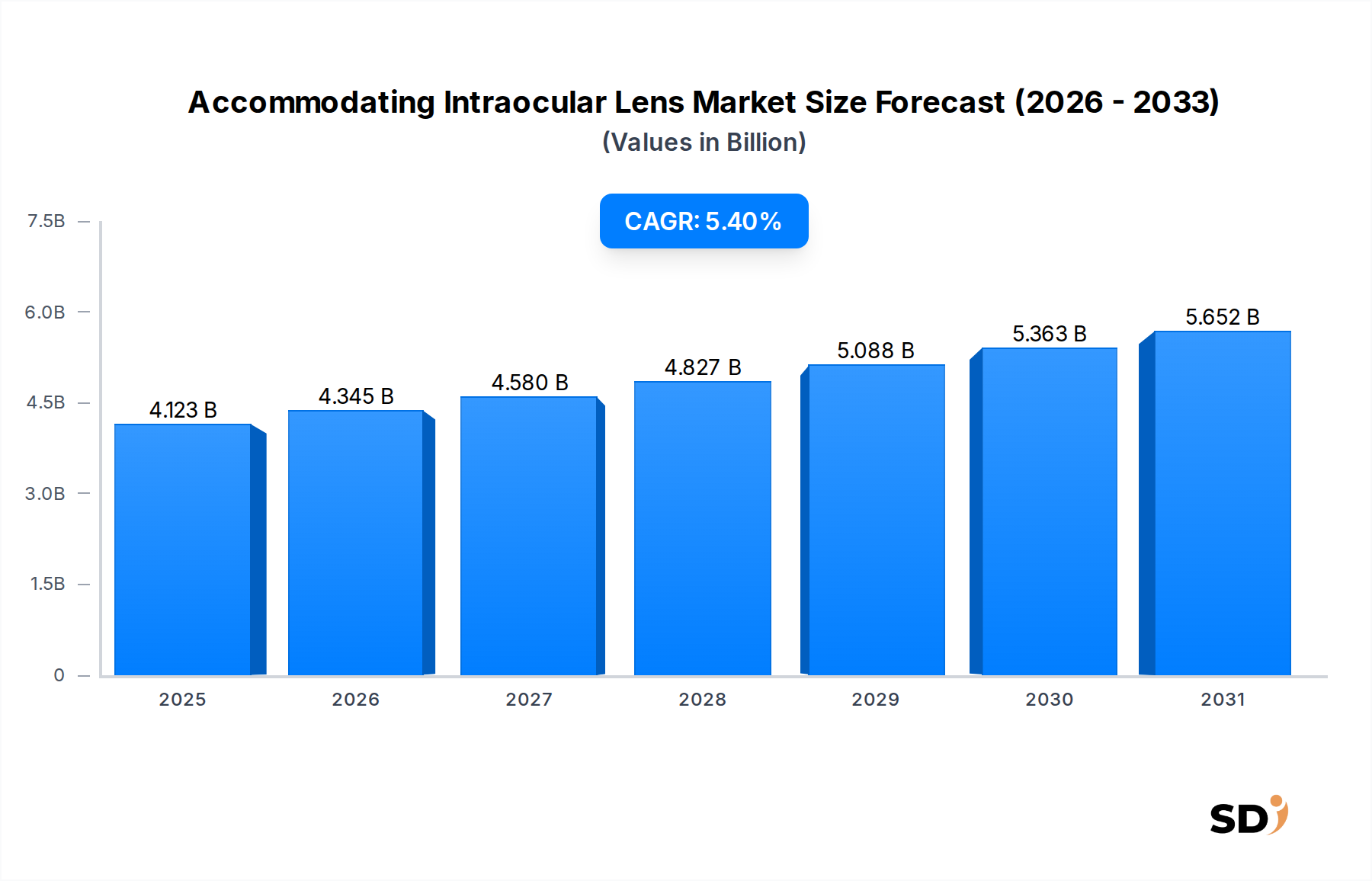

The Accommodating Intraocular Lens Market is experiencing robust expansion, primarily driven by the escalating global prevalence of presbyopia and cataracts, coupled with significant advancements in ophthalmic surgical techniques. In 2023, the market was valued at an estimated $4122.7 million. Projections indicate a substantial growth trajectory, with the market expected to reach approximately $5971.8 million by 2030, advancing at a compound annual growth rate (CAGR) of 5.4% over the forecast period. This growth underscores the increasing patient desire for spectacle independence and the continuous innovation within the ophthalmic sector.

Accommodating Intraocular Lens Market Size (In Billion)

7.5B

6.0B

4.5B

3.0B

1.5B

0

4.123 B

2025

4.345 B

2026

4.580 B

2027

4.827 B

2028

5.088 B

2029

5.363 B

2030

5.652 B

2031

A key demand driver for accommodating intraocular lenses (A-IOLs) is the aging global demographic. As the population aged 60 and above expands, so does the incidence of age-related vision impairments, particularly cataracts and presbyopia, creating a persistent and growing demand for advanced vision correction solutions. Technological leaps in lens design, material science, and surgical instrumentation are further propelling market expansion. The development of A-IOLs offering enhanced range of vision and reduced post-operative complications is significantly contributing to their adoption. Furthermore, the shift towards personalized medicine and the increasing availability of sophisticated diagnostic tools enable ophthalmologists to offer tailored A-IOL solutions, optimizing patient outcomes. The Premium Intraocular Lens Market, encompassing A-IOLs, multifocal IOLs, and toric IOLs, is benefiting from this trend, as patients are increasingly willing to invest in superior visual acuity and quality of life.

Macroeconomic tailwinds such as improving healthcare infrastructure in emerging economies, rising disposable incomes, and increasing awareness about advanced ophthalmic treatments are also playing a crucial role. These factors are broadening patient access to specialized eye care and premium surgical options. The continuous research and development efforts by key market players to overcome current limitations of A-IOLs, such as the pseudo-accommodative effect or limited focal range, are vital for sustained market growth. The focus on developing truly accommodating lenses with dynamic optical power adjustment capabilities represents the next frontier, promising to further revolutionize the Ophthalmology Devices Market. The Accommodating Intraocular Lens Market is set for continued innovation and strong patient uptake, driven by both demographic imperatives and technological advancements.

The Dominance of Single-Piece Accommodating Intraocular Lenses in Accommodating Intraocular Lens Market

Within the broader Accommodating Intraocular Lens Market, the Single-Piece Intraocular Lens Market segment is currently estimated to hold a dominant share, primarily due to its widespread adoption, manufacturing efficiency, and well-established surgical protocols. Single-piece IOLs are typically designed with integrated haptics, allowing for easier insertion through smaller incisions and often reducing the risk of complications associated with haptic-optic disjunction or misplacement. This design simplicity contributes to lower manufacturing costs compared to their multi-piece counterparts, making them an attractive option for both manufacturers and healthcare providers, especially in high-volume cataract surgery centers. The preference for single-piece designs is particularly pronounced in procedures involving pre-loaded injection systems, which streamline the surgical process and minimize human error. These attributes have cemented the position of the Single-Piece Intraocular Lens Market as the primary revenue generator within the A-IOL landscape.

The key players in the Accommodating Intraocular Lens Market, including Alcon Laboratories, Inc., Johnson & Johnson Vision Care, Inc., and Bausch & Lomb Incorporated, have heavily invested in developing and refining single-piece accommodating designs. These companies leverage their extensive distribution networks and clinical research capabilities to promote the benefits of these lenses. While true accommodative properties remain a research frontier, current single-piece A-IOLs often employ advanced optical designs, such as extended depth of focus (EDOF) features, to provide a wider range of functional vision, thus minimizing the need for spectacles for various tasks. This pseudo-accommodative effect has been a significant driver for their market acceptance.

In contrast, the Multi-Piece Intraocular Lens Market, though smaller, caters to specific clinical needs where the independent positioning of haptics and optic offers certain surgical advantages, particularly in cases requiring precise centration or where sulcus fixation is preferred. However, the complexities involved in their manufacturing and insertion typically result in a higher cost profile and a more niche application. While the Single-Piece Intraocular Lens Market is expected to maintain its leadership, ongoing innovation in both segments will continue to address diverse patient requirements. The drive towards enhancing the range of vision, reducing dysphotopsia, and improving long-term stability remains a central theme for all players in the Accommodating Intraocular Lens Market, with single-piece designs continually evolving to meet these demands effectively and efficiently.

Advancements in Surgical Techniques Driving the Accommodating Intraocular Lens Market

The Accommodating Intraocular Lens Market is significantly propelled by several key drivers and advancements, primarily anchored in demographic shifts and technological innovation. A paramount driver is the global aging population; individuals over 65 years are the demographic most affected by cataracts and presbyopia, the primary indications for A-IOL implantation. The World Health Organization estimates that the number of people aged 60 years and older will double by 2050, directly correlating to an increased incidence of these conditions and, consequently, a higher demand for solutions within the Cataract Surgery Devices Market.

Technological breakthroughs in A-IOL design represent another crucial driver. Modern A-IOLs are engineered with sophisticated optics that provide an extended range of vision, attempting to mimic the eye's natural accommodation. This involves material innovations, particularly in the Hydrophobic Acrylic Materials Market, which allow for greater flexibility and biocompatibility. Furthermore, the increasing adoption of minimally invasive surgical techniques, such as femtosecond laser-assisted cataract surgery (FLACS), enhances precision and reduces recovery times. This increased surgical efficacy and predictability contribute to greater patient confidence and willingness to opt for premium IOLs. For instance, FLACS improves capsulorhexis consistency, which is vital for optimal A-IOL performance.

Patient preference for spectacle independence is also a powerful market accelerator. There is a growing willingness among cataract patients to pay for premium options that reduce or eliminate their reliance on glasses for near, intermediate, and distance vision. This preference fuels the expansion of the Accommodating Intraocular Lens Market. Conversely, a significant restraint is the high cost of A-IOLs compared to conventional monofocal IOLs. This often translates into out-of-pocket expenses for patients, as many healthcare systems and insurance providers offer limited reimbursement for premium IOLs, thus potentially limiting access in cost-sensitive markets. The complex learning curve associated with advanced surgical techniques for optimal A-IOL placement and the need for meticulous patient selection also pose challenges, requiring extensive surgeon training and experience to achieve satisfactory outcomes.

Competitive Ecosystem of Accommodating Intraocular Lens Market

The Accommodating Intraocular Lens Market is characterized by a concentrated competitive landscape featuring a blend of large multinational corporations and specialized ophthalmic device manufacturers. These entities are engaged in continuous research and development to enhance lens design, material science, and surgical delivery systems.

Alcon Laboratories, Inc.: A global leader in eye care, Alcon offers a broad portfolio of IOLs, including advanced technology lenses like A-IOLs, and is a significant player in the Premium Intraocular Lens Market. Its strong R&D pipeline focuses on improving visual outcomes and patient satisfaction.

Bausch & Lomb Incorporated: A well-established name in ophthalmology, Bausch & Lomb provides a comprehensive range of IOLs and surgical devices. The company emphasizes innovation in lens materials and designs to address diverse patient needs and expand its market presence.

Johnson & Johnson Vision Care, Inc.: Through its Vision division, Johnson & Johnson offers a wide array of ophthalmic products, including advanced IOLs. The company leverages its extensive global reach and strong research capabilities to drive product development and market penetration.

Carl Zeiss Meditec AG: Renowned for its precision optics and medical technology, Carl Zeiss Meditec offers high-quality IOLs and diagnostic equipment. The company focuses on integrated solutions that enhance surgical efficiency and patient results.

Rayner Intraocular Lenses Limited: A pioneer in IOL manufacturing, Rayner boasts a long history of innovation, including the first IOL implantation. The company continues to develop advanced IOLs with a focus on optical performance and surgeon preferences.

STAAR Surgical Company: Specializing in implantable collamer lenses (ICLs), STAAR Surgical also participates in the broader refractive and cataract surgery market. Its expertise in biocompatible materials influences its strategic direction within the IOL space.

Santen Pharmaceutical Co., Ltd. : A global pharmaceutical company focused on ophthalmology, Santen Pharmaceutical is expanding its presence in the device segment, aiming to provide comprehensive eye care solutions, including IOLs.

Lenstec, Inc.: Known for its unique IOL designs, Lenstec focuses on delivering predictable visual outcomes. The company's technology aims to provide a continuous range of vision, contributing to the advancements in A-IOLs.

VSY Biotechnology GmbH: This company is an R&D and manufacturing firm specializing in ophthalmic medical devices. VSY Biotechnology develops IOLs utilizing advanced materials and designs to improve visual acuity and patient experience.

HumanOptics: A German manufacturer of high-quality IOLs, HumanOptics is known for its customized solutions and advanced lens technologies. The company emphasizes precision and patient-specific designs.

Biotech Visioncare: An Indian-based company, Biotech Visioncare is a significant manufacturer of IOLs, offering a range of products including those designed for advanced vision correction in emerging markets.

Omni Lens Pvt Ltd: Another prominent Indian IOL manufacturer, Omni Lens focuses on providing affordable and high-quality intraocular lenses to a wide patient base.

Aurolab: As a unit of Aravind Eye Care System, Aurolab produces a vast array of ophthalmic consumables, including IOLs, aiming to make eye care affordable and accessible globally.

SAV-IOL: A Swiss company, SAV-IOL specializes in the design and manufacture of innovative IOLs, with a strong focus on advanced optical concepts for improved visual function.

Eagle Optics: With a focus on quality and innovation, Eagle Optics offers a variety of IOLs catering to different patient needs and surgical techniques.

SIFI Medtech: Part of the SIFI group, SIFI Medtech is dedicated to ophthalmic devices, including a range of IOLs designed to enhance vision and improve patient quality of life.

Physiol: A Belgian company with a strong focus on innovation in IOLs, Physiol develops and manufactures a range of advanced lenses, including those aimed at providing extended depth of focus and accommodative properties.

Recent Developments & Milestones in Accommodating Intraocular Lens Market

The Accommodating Intraocular Lens Market is continually evolving through strategic initiatives, product innovations, and regulatory advancements aimed at improving patient outcomes and expanding market reach.

March 2024: A leading player in the Accommodating Intraocular Lens Market announced the commencement of a Phase III clinical trial for a novel A-IOL design, intended to provide a greater range of continuous vision with reduced incidence of glare and halos, building on prior successes in the Premium Intraocular Lens Market.

January 2024: A major ophthalmic company received FDA approval for its new single-piece extended depth of focus (EDOF) IOL, which features enhanced material properties derived from advancements in the Hydrophobic Acrylic Materials Market, targeting presbyopic cataract patients seeking minimized spectacle dependence.

November 2023: A significant partnership was forged between an A-IOL manufacturer and a prominent academic research institution to explore gene therapy applications that could potentially enhance the ciliary muscle function, thereby improving the long-term accommodative amplitude of implanted lenses.

September 2023: An industry report highlighted a 15% increase in the adoption of femtosecond laser-assisted cataract surgery for A-IOL implantation across North America over the past year, indicating growing surgeon confidence in precision surgical techniques within the Cataract Surgery Devices Market.

July 2023: A European company launched its latest multi-piece accommodating IOL, specifically engineered for challenging cases where precise customization of haptic placement is crucial for optimal visual outcomes, thereby contributing to the Multi-Piece Intraocular Lens Market.

May 2023: New clinical data was presented demonstrating superior intermediate vision for patients implanted with a next-generation A-IOL compared to conventional monofocal IOLs, reinforcing the value proposition of premium lenses in the Accommodating Intraocular Lens Market.

February 2023: Regulatory authorities in Japan approved an advanced A-IOL, signifying an expansion into the Asia Pacific region for a key market player and broadening treatment options for patients in the rapidly growing Ophthalmic Clinics Market.

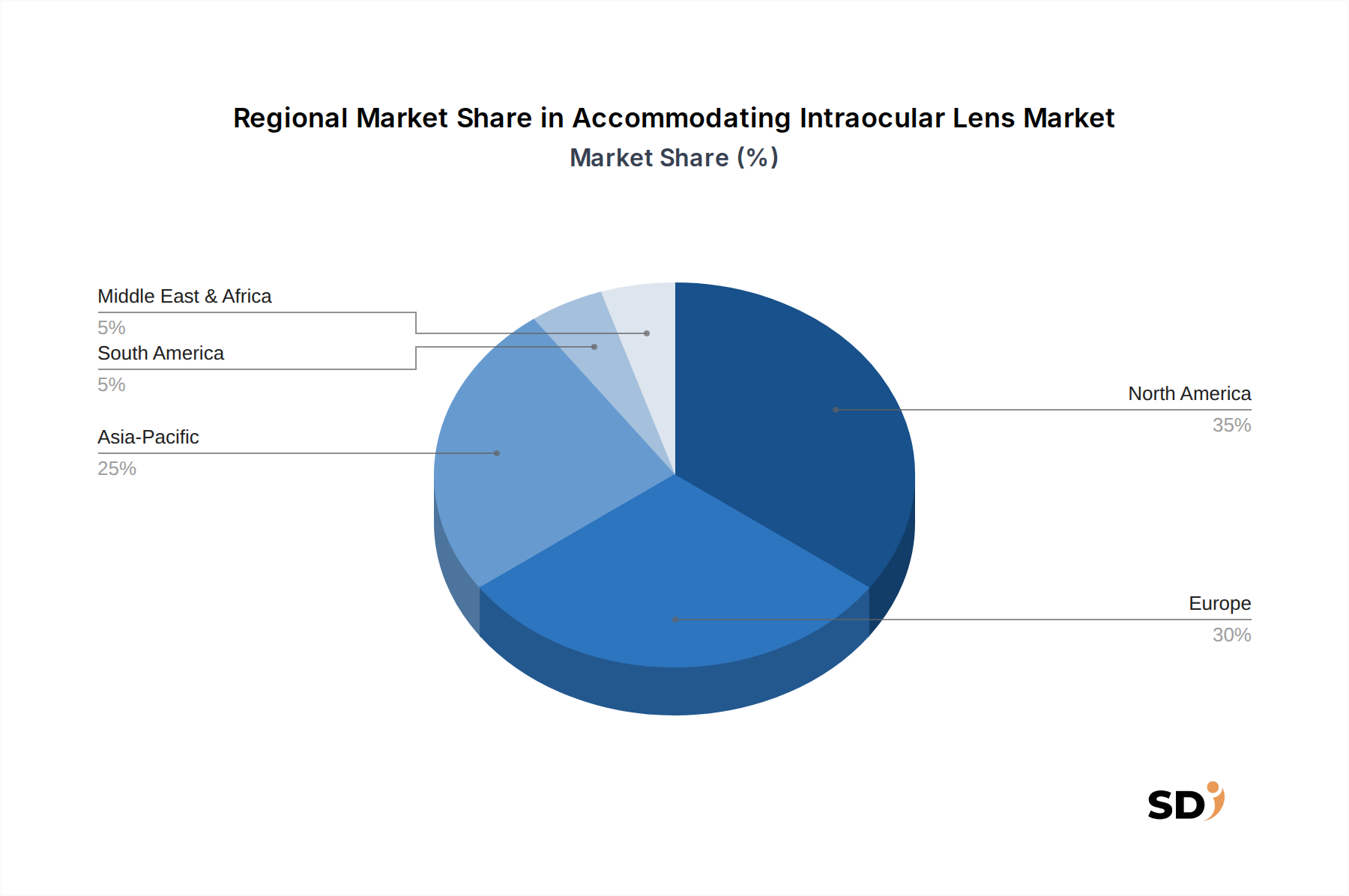

Regional Market Breakdown for Accommodating Intraocular Lens Market

The Accommodating Intraocular Lens Market exhibits distinct regional dynamics, influenced by healthcare infrastructure, demographic trends, and economic factors. While the market is experiencing a global CAGR of 5.4%, regional growth rates and market shares vary significantly.

North America holds a substantial share of the Accommodating Intraocular Lens Market. The region, particularly the United States, benefits from a well-established healthcare system, high patient awareness, and strong adoption of advanced medical technologies. High disposable incomes and favorable reimbursement policies for premium IOLs also contribute to its dominance. North America shows a mature market, with a strong emphasis on technological innovation and a high concentration of key market players. The demand here is driven by the aging Baby Boomer population seeking spectacle independence post-cataract surgery.

Europe represents another significant market segment for accommodating IOLs. Countries like Germany, France, and the UK are major contributors, characterized by advanced healthcare systems and a high standard of ophthalmic care. The market in Europe is driven by similar factors to North America, including an aging population and increasing demand for premium vision solutions. However, the varying reimbursement landscapes across different European countries can influence market penetration and pricing strategies for the Premium Intraocular Lens Market.

Asia Pacific is projected to be the fastest-growing region in the Accommodating Intraocular Lens Market over the forecast period. This rapid growth is attributable to several factors: a vast and rapidly aging population, particularly in countries like China and India, increasing healthcare expenditure, and a growing middle class with rising disposable incomes. The expansion of Ophthalmic Clinics Market and Ambulatory Surgery Centers Market in this region, coupled with improving access to advanced eye care, fuels the adoption of A-IOLs. Governments and private entities are investing heavily in upgrading healthcare infrastructure, leading to a surge in cataract surgeries and the subsequent demand for sophisticated IOLs.

The Middle East & Africa (MEA) region is an emerging market for accommodating IOLs. While smaller in market share compared to the established regions, MEA is expected to exhibit steady growth. This growth is driven by increasing healthcare tourism, rising awareness about advanced ophthalmic treatments, and significant investments in healthcare infrastructure, particularly in the GCC countries. The expanding network of specialized ophthalmic centers and rising prevalence of cataracts due to demographic and environmental factors will underpin growth in this region.

Pricing Dynamics & Margin Pressure in Accommodating Intraocular Lens Market

The pricing dynamics in the Accommodating Intraocular Lens Market are complex, influenced by innovation, competitive intensity, and the premium nature of the technology. Average Selling Prices (ASPs) for A-IOLs are significantly higher than those for standard monofocal IOLs, reflecting the advanced R&D, sophisticated manufacturing processes, and the value proposition of spectacle independence. This positions A-IOLs firmly within the Premium Intraocular Lens Market segment. However, competitive pressures among key players, coupled with the entry of new market participants, exert a downward pressure on pricing, especially for older or less differentiated A-IOL models. Early market entrants could command substantial premiums, but as technologies mature and alternatives emerge, price points tend to stabilize or gradually decrease.

Margin structures across the value chain are generally healthy but are subject to various cost levers. R&D expenditure constitutes a substantial portion, as continuous innovation is critical to staying competitive. Manufacturing costs are influenced by the complexity of lens design, precision molding, and the specialized nature of raw materials. The Hydrophobic Acrylic Materials Market, for instance, supplies high-quality polymers that contribute significantly to the COGS. Regulatory approval processes, clinical trials, and extensive marketing efforts also add to the overall cost structure. These factors mean that while the gross margins for A-IOLs can be attractive, the net margins are often moderated by the high operational overheads.

Margin pressure is further exacerbated by the fragmented reimbursement landscape. In many regions, the premium component of A-IOLs is not fully covered by public or private insurance, requiring patients to bear a significant out-of-pocket expense. This creates a ceiling on ASPs that the market can sustain, especially in cost-sensitive economies. Furthermore, as the Cataract Surgery Devices Market matures, volume-based procurement agreements by large hospital groups or governmental bodies can lead to price concessions. Companies manage these pressures by diversifying their product portfolios, focusing on incremental innovations that justify premium pricing, and optimizing their supply chains to control raw material and manufacturing costs. Strategic partnerships and direct-to-consumer educational initiatives also help in maintaining pricing power by emphasizing the long-term benefits of A-IOLs.

Supply Chain & Raw Material Dynamics for Accommodating Intraocular Lens Market

The Accommodating Intraocular Lens Market is heavily reliant on a specialized and intricate supply chain, primarily centered around high-purity optical polymers and precision manufacturing. Upstream dependencies are significant, with a limited number of specialized suppliers providing the advanced materials required for IOL fabrication. The core components of A-IOLs are typically made from biocompatible synthetic polymers, predominantly acrylics (both hydrophobic and hydrophilic) and silicone. The Hydrophobic Acrylic Materials Market is a critical segment, as these materials offer excellent optical clarity, high refractive index, and long-term biocompatibility, crucial for the longevity and performance of implanted lenses. Silicone-based lenses, while offering good flexibility, face competition from acrylics due to concerns over potential posterior capsular opacification (PCO) rates, influencing the dynamics within the Silicone Lenses Market.

Sourcing risks are notable due to this specialization. Any disruption to the supply of these high-grade monomers and polymers can severely impact IOL production. Geopolitical tensions, trade restrictions, and natural disasters in key manufacturing regions for these chemical precursors can lead to supply shortages and price volatility. For instance, the global events of 2020-2022 demonstrated how disruptions in international logistics and manufacturing capacities significantly affected the availability of various medical device components, including those for ophthalmic devices.

Price volatility of key inputs is another critical factor. The cost of raw polymers is subject to fluctuations in the petrochemical industry, energy prices, and global supply-demand dynamics. While IOLs are high-value medical devices, sustained increases in raw material costs can erode manufacturer margins or necessitate price adjustments, potentially impacting market accessibility. Manufacturers mitigate these risks through strategic long-term contracts with suppliers, diversification of sourcing channels where possible, and investing in vertical integration for critical components.

Historically, supply chain disruptions have manifested as extended lead times for IOL components, delays in product launches, and increased production costs. Companies in the Accommodating Intraocular Lens Market must maintain robust inventory management systems and contingency plans to ensure a steady supply of materials. Furthermore, stringent quality control and regulatory requirements for medical-grade materials add another layer of complexity and cost to the supply chain, ensuring that only the highest quality and safest inputs are used in the manufacturing of these sensitive ophthalmic implants.

Accommodating Intraocular Lens Segmentation

1. Product Type

1.1. Single-Piece

1.2. Multi-Piece

2. Material

2.1. Hydrophobic Acrylic

2.2. Hydrophilic Acrylic

2.3. Polymethyl Methacrylate

2.4. Silicone Lenses

2.5. Others

3. End-User

3.1. Hospitals

3.2. Ophthalmic Clinics

3.3. Ambulatory Surgery Centers

3.4. Others

Accommodating Intraocular Lens Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Accommodating Intraocular Lens REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 5.4% from 2020-2034

Segmentation

By Product Type

Single-Piece

Multi-Piece

By Material

Hydrophobic Acrylic

Hydrophilic Acrylic

Polymethyl Methacrylate

Silicone Lenses

Others

By End-User

Hospitals

Ophthalmic Clinics

Ambulatory Surgery Centers

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Type

5.1.1. Single-Piece

5.1.2. Multi-Piece

5.2. Market Analysis, Insights and Forecast - by Material

5.2.1. Hydrophobic Acrylic

5.2.2. Hydrophilic Acrylic

5.2.3. Polymethyl Methacrylate

5.2.4. Silicone Lenses

5.2.5. Others

5.3. Market Analysis, Insights and Forecast - by End-User

5.3.1. Hospitals

5.3.2. Ophthalmic Clinics

5.3.3. Ambulatory Surgery Centers

5.3.4. Others

5.4. Market Analysis, Insights and Forecast - by Region

5.4.1. North America

5.4.2. South America

5.4.3. Europe

5.4.4. Middle East & Africa

5.4.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Product Type

6.1.1. Single-Piece

6.1.2. Multi-Piece

6.2. Market Analysis, Insights and Forecast - by Material

6.2.1. Hydrophobic Acrylic

6.2.2. Hydrophilic Acrylic

6.2.3. Polymethyl Methacrylate

6.2.4. Silicone Lenses

6.2.5. Others

6.3. Market Analysis, Insights and Forecast - by End-User

6.3.1. Hospitals

6.3.2. Ophthalmic Clinics

6.3.3. Ambulatory Surgery Centers

6.3.4. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Product Type

7.1.1. Single-Piece

7.1.2. Multi-Piece

7.2. Market Analysis, Insights and Forecast - by Material

7.2.1. Hydrophobic Acrylic

7.2.2. Hydrophilic Acrylic

7.2.3. Polymethyl Methacrylate

7.2.4. Silicone Lenses

7.2.5. Others

7.3. Market Analysis, Insights and Forecast - by End-User

7.3.1. Hospitals

7.3.2. Ophthalmic Clinics

7.3.3. Ambulatory Surgery Centers

7.3.4. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Product Type

8.1.1. Single-Piece

8.1.2. Multi-Piece

8.2. Market Analysis, Insights and Forecast - by Material

8.2.1. Hydrophobic Acrylic

8.2.2. Hydrophilic Acrylic

8.2.3. Polymethyl Methacrylate

8.2.4. Silicone Lenses

8.2.5. Others

8.3. Market Analysis, Insights and Forecast - by End-User

8.3.1. Hospitals

8.3.2. Ophthalmic Clinics

8.3.3. Ambulatory Surgery Centers

8.3.4. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Product Type

9.1.1. Single-Piece

9.1.2. Multi-Piece

9.2. Market Analysis, Insights and Forecast - by Material

9.2.1. Hydrophobic Acrylic

9.2.2. Hydrophilic Acrylic

9.2.3. Polymethyl Methacrylate

9.2.4. Silicone Lenses

9.2.5. Others

9.3. Market Analysis, Insights and Forecast - by End-User

9.3.1. Hospitals

9.3.2. Ophthalmic Clinics

9.3.3. Ambulatory Surgery Centers

9.3.4. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Product Type

10.1.1. Single-Piece

10.1.2. Multi-Piece

10.2. Market Analysis, Insights and Forecast - by Material

10.2.1. Hydrophobic Acrylic

10.2.2. Hydrophilic Acrylic

10.2.3. Polymethyl Methacrylate

10.2.4. Silicone Lenses

10.2.5. Others

10.3. Market Analysis, Insights and Forecast - by End-User

10.3.1. Hospitals

10.3.2. Ophthalmic Clinics

10.3.3. Ambulatory Surgery Centers

10.3.4. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Alcon Laboratories Inc.

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Bausch & Lomb Incorporated

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Johnson & Johnson Vision Care Inc.

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Carl Zeiss Meditec AG

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Rayner Intraocular Lenses Limited

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. STAAR Surgical Company

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Santen Pharmaceutical Co. Ltd.

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Lenstec Inc.

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. VSY Biotechnology GmbH

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. HumanOptics

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Biotech Visioncare

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Omni Lens Pvt Ltd

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. Aurolab

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.1.14. SAV-IOL

11.1.14.1. Company Overview

11.1.14.2. Products

11.1.14.3. Company Financials

11.1.14.4. SWOT Analysis

11.1.15. Eagle Optics

11.1.15.1. Company Overview

11.1.15.2. Products

11.1.15.3. Company Financials

11.1.15.4. SWOT Analysis

11.1.16. SIFI Medtech

11.1.16.1. Company Overview

11.1.16.2. Products

11.1.16.3. Company Financials

11.1.16.4. SWOT Analysis

11.1.17. Physiol

11.1.17.1. Company Overview

11.1.17.2. Products

11.1.17.3. Company Financials

11.1.17.4. SWOT Analysis

11.1.18. Others

11.1.18.1. Company Overview

11.1.18.2. Products

11.1.18.3. Company Financials

11.1.18.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Product Type 2025 & 2033

Figure 3: Revenue Share (%), by Product Type 2025 & 2033

Figure 4: Revenue (million), by Material 2025 & 2033

Figure 5: Revenue Share (%), by Material 2025 & 2033

Figure 6: Revenue (million), by End-User 2025 & 2033

Figure 7: Revenue Share (%), by End-User 2025 & 2033

Figure 8: Revenue (million), by Country 2025 & 2033

Figure 9: Revenue Share (%), by Country 2025 & 2033

Figure 10: Revenue (million), by Product Type 2025 & 2033

Figure 11: Revenue Share (%), by Product Type 2025 & 2033

Figure 12: Revenue (million), by Material 2025 & 2033

Figure 13: Revenue Share (%), by Material 2025 & 2033

Figure 14: Revenue (million), by End-User 2025 & 2033

Figure 15: Revenue Share (%), by End-User 2025 & 2033

Figure 16: Revenue (million), by Country 2025 & 2033

Figure 17: Revenue Share (%), by Country 2025 & 2033

Figure 18: Revenue (million), by Product Type 2025 & 2033

Figure 19: Revenue Share (%), by Product Type 2025 & 2033

Figure 20: Revenue (million), by Material 2025 & 2033

Figure 21: Revenue Share (%), by Material 2025 & 2033

Figure 22: Revenue (million), by End-User 2025 & 2033

Figure 23: Revenue Share (%), by End-User 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Product Type 2025 & 2033

Figure 27: Revenue Share (%), by Product Type 2025 & 2033

Figure 28: Revenue (million), by Material 2025 & 2033

Figure 29: Revenue Share (%), by Material 2025 & 2033

Figure 30: Revenue (million), by End-User 2025 & 2033

Figure 31: Revenue Share (%), by End-User 2025 & 2033

Figure 32: Revenue (million), by Country 2025 & 2033

Figure 33: Revenue Share (%), by Country 2025 & 2033

Figure 34: Revenue (million), by Product Type 2025 & 2033

Figure 35: Revenue Share (%), by Product Type 2025 & 2033

Figure 36: Revenue (million), by Material 2025 & 2033

Figure 37: Revenue Share (%), by Material 2025 & 2033

Figure 38: Revenue (million), by End-User 2025 & 2033

Figure 39: Revenue Share (%), by End-User 2025 & 2033

Figure 40: Revenue (million), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Product Type 2020 & 2033

Table 2: Revenue million Forecast, by Material 2020 & 2033

Table 3: Revenue million Forecast, by End-User 2020 & 2033

Table 4: Revenue million Forecast, by Region 2020 & 2033

Table 5: Revenue million Forecast, by Product Type 2020 & 2033

Table 6: Revenue million Forecast, by Material 2020 & 2033

Table 7: Revenue million Forecast, by End-User 2020 & 2033

Table 8: Revenue million Forecast, by Country 2020 & 2033

Table 9: Revenue (million) Forecast, by Application 2020 & 2033

Table 10: Revenue (million) Forecast, by Application 2020 & 2033

Table 11: Revenue (million) Forecast, by Application 2020 & 2033

Table 12: Revenue million Forecast, by Product Type 2020 & 2033

Table 13: Revenue million Forecast, by Material 2020 & 2033

Table 14: Revenue million Forecast, by End-User 2020 & 2033

Table 15: Revenue million Forecast, by Country 2020 & 2033

Table 16: Revenue (million) Forecast, by Application 2020 & 2033

Table 17: Revenue (million) Forecast, by Application 2020 & 2033

Table 18: Revenue (million) Forecast, by Application 2020 & 2033

Table 19: Revenue million Forecast, by Product Type 2020 & 2033

Table 20: Revenue million Forecast, by Material 2020 & 2033

Table 21: Revenue million Forecast, by End-User 2020 & 2033

Table 22: Revenue million Forecast, by Country 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Revenue (million) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue (million) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Revenue (million) Forecast, by Application 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue million Forecast, by Product Type 2020 & 2033

Table 33: Revenue million Forecast, by Material 2020 & 2033

Table 34: Revenue million Forecast, by End-User 2020 & 2033

Table 35: Revenue million Forecast, by Country 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue (million) Forecast, by Application 2020 & 2033

Table 38: Revenue (million) Forecast, by Application 2020 & 2033

Table 39: Revenue (million) Forecast, by Application 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue million Forecast, by Product Type 2020 & 2033

Table 43: Revenue million Forecast, by Material 2020 & 2033

Table 44: Revenue million Forecast, by End-User 2020 & 2033

Table 45: Revenue million Forecast, by Country 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Table 47: Revenue (million) Forecast, by Application 2020 & 2033

Table 48: Revenue (million) Forecast, by Application 2020 & 2033

Table 49: Revenue (million) Forecast, by Application 2020 & 2033

Table 50: Revenue (million) Forecast, by Application 2020 & 2033

Table 51: Revenue (million) Forecast, by Application 2020 & 2033

Table 52: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology forms the cornerstone of our market intelligence, accounting for 75% of our total research efforts. This robust approach involves direct engagement with key stakeholders across the value chain to gather proprietary, real-time insights into market dynamics, competitive landscapes, product adoption rates, pricing trends, and regional specific nuances.

Key aspects of our primary research include:

Interview Targets: We conduct in-depth interviews with a carefully selected pool of industry experts, including:

VP of Sales & Marketing (IOL Manufacturers)

Head of Ophthalmology Department (Hospitals/Clinics)

Director of Procurement/Supply Chain (Hospitals/ASCs)

Key Opinion Leader (KOL) Cataract Surgeon

Company Types Interviewed: Our outreach extends to a diverse set of organizations integral to the Accommodating Intraocular Lens market, such as:

Accommodating IOL Manufacturers

Ophthalmic Device Distributors

Large Hospital Chains with dedicated Ophthalmology Departments

Specialized Ophthalmic Clinic Networks

Ambulatory Surgical Centers (ASCs) focused on Ophthalmic Surgeries

Engagement Strategy: Interviews are conducted through various channels, including telephonic discussions, virtual meetings, and sometimes face-to-face interactions at industry conferences, ensuring comprehensive data collection.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP of Sales & Marketing (IOL Manufacturers)

30%

Head of Ophthalmology Department (Hospitals/Clinics)

25%

Director of Procurement/Supply Chain (Hospitals/ASCs)

25%

Key Opinion Leader (KOL) Cataract Surgeon

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Accommodating IOL Manufacturers

35%

Ophthalmic Device Distributors

20%

Large Hospital Chains (Ophthalmology Depts)

15%

Specialized Ophthalmic Clinic Networks

15%

Ambulatory Surgical Centers (Ophthalmic)

15%

Secondary Research & Industry Benchmarking

Comprising 25% of our research methodology, secondary research provides the foundational data and validates primary findings. This phase involves a meticulous review of a wide array of published information from credible and authoritative sources.

Our secondary research leverages:

Standard Financial Databases: Access to premium databases such as Bloomberg, Factiva, Hoovers, and PitchBook provides critical corporate financials, competitive intelligence, and investment trends.

Government & Regulatory Bodies: Data from national and international regulatory bodies and governmental health departments offers insights into market approvals, public health statistics, and policy frameworks. Examples include reports from the U.S. Food and Drug Administration (FDA) and national health ministries.

Industry Associations & Trade Bodies: Publications, journals, and reports from recognized industry associations are crucial for understanding market standards, technological advancements, and advocacy efforts. Key organizations include:

American Academy of Ophthalmology (AAO)

European Society of Cataract and Refractive Surgeons (ESCRS)

AdvaMed (Advanced Medical Technology Association)

Company Publications: Annual reports, investor presentations, product whitepapers, and press releases of leading market players offer direct insights into their strategies, financial performance, and product pipelines.

Academic & Scientific Publications: Peer-reviewed journals and research papers provide a deeper understanding of clinical trials, technological advancements, and emerging trends in ophthalmology.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies employ a robust combination of top-down and bottom-up approaches, further validated through multi-level data triangulation to ensure accuracy and reliability.

Top-Down Approach: We initiate market sizing by analyzing macro-level indicators such as global and regional healthcare expenditure on ophthalmic procedures, prevalence rates of cataract and presbyopia, and general economic indicators. This broad market value is then progressively segmented down to the specific Accommodating Intraocular Lens market, broken down by product type, material, end-user, and geography.

Bottom-Up Approach: This granular approach involves aggregating market estimates based on specific operational metrics:

Number of cataract surgeries performed annually by region/country.

Average selling price (ASP) of Accommodating IOLs, differentiated by product type (Single-Piece, Multi-Piece) and material (Hydrophobic Acrylic, Hydrophilic Acrylic, Polymethyl Methacrylate, Silicone Lenses, Others).

Market penetration rate of Accommodating IOLs within the total IOL market, considering competition from standard monofocal IOLs and other premium IOLs.

Incidence and prevalence rates of age-related presbyopia and cataracts in target demographic segments.

Data Triangulation: All market estimates are subjected to multi-level data triangulation, cross-referencing findings from primary interviews, secondary research, and internal proprietary databases to eliminate discrepancies and enhance statistical validity.

Forecasting Model: Our forecasting model integrates historical growth rates, anticipated technological advancements (e.g., next-generation IOLs, surgical techniques), new product launches, regulatory changes, and key macroeconomic factors to project market trends from 2026 to 2034.

Data Accuracy & Quality Check

Ensuring the highest level of data integrity is paramount. We guarantee an estimated data accuracy level of 85-90% for our market insights and forecasts.

Key components of our quality assurance process include:

Rigorous Cross-Validation: Every data point and market estimate undergoes stringent cross-validation against multiple independent sources, both primary and secondary, through our multi-level triangulation process.

Analyst Review: All collected data and derived insights are meticulously reviewed by senior market research analysts with deep domain expertise in the ophthalmic devices sector.

Dynamic Updating: Our research framework is designed for continuous updates. This ensures that the market report reflects the most current market dynamics, technological advancements, regulatory changes, and competitive landscape up to the date of purchase, providing clients with timely and relevant intelligence.

Frequently Asked Questions

1. Who are the leading companies in the Accommodating Intraocular Lens market?

Key players include Alcon Laboratories, Inc., Bausch & Lomb Incorporated, and Johnson & Johnson Vision Care, Inc. Other significant firms are Carl Zeiss Meditec AG and Rayner Intraocular Lenses Limited, indicating a competitive landscape with several established manufacturers.

2. What are the primary barriers to entry in the Accommodating Intraocular Lens market?

Entry barriers are substantial due to high R&D costs, stringent regulatory approval processes for medical devices, and the need for specialized manufacturing capabilities. Established companies benefit from strong brand recognition and extensive clinical validation.

3. Which region exhibits the fastest growth in the Accommodating Intraocular Lens market?

While specific regional growth rates are not detailed, Asia Pacific is generally considered an emerging market with significant growth opportunities. North America and Europe currently hold substantial market shares due to advanced healthcare infrastructure and an aging population.

4. What are the international trade dynamics for Accommodating Intraocular Lenses?

The global presence of major manufacturers like Alcon and Johnson & Johnson Vision Care suggests significant international trade flows for these devices. Production often occurs in established manufacturing hubs, followed by global distribution to ophthalmic clinics and hospitals worldwide.

5. What are the key product segments in the Accommodating Intraocular Lens market?

The market is segmented by product type into Single-Piece and Multi-Piece lenses. Material types include Hydrophobic Acrylic, Hydrophilic Acrylic, and Silicone Lenses. These segments address varied patient needs and surgical approaches.

6. Which end-user segments drive demand for Accommodating Intraocular Lenses?

Demand is primarily driven by Hospitals and Ophthalmic Clinics. Ambulatory Surgery Centers also represent a significant end-user segment. These facilities cater to patients requiring cataract surgery and refractive lens exchange procedures.