Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

4C Superfast Charging Battery Cells by Type (Ternary Lithium Batteries, Lithium Iron Phosphate (LFP) Batteries), by Battery Capacity (Below 2000 mAh, 2000-4000 mAh, Above 4000 mAh), by Application (Electric Vehicles (EVs), Energy Storage Systems (ESS), Others), by End-Use (Residential, Commercial), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 144

Key Insights for 4C Superfast Charging Battery Cells Market

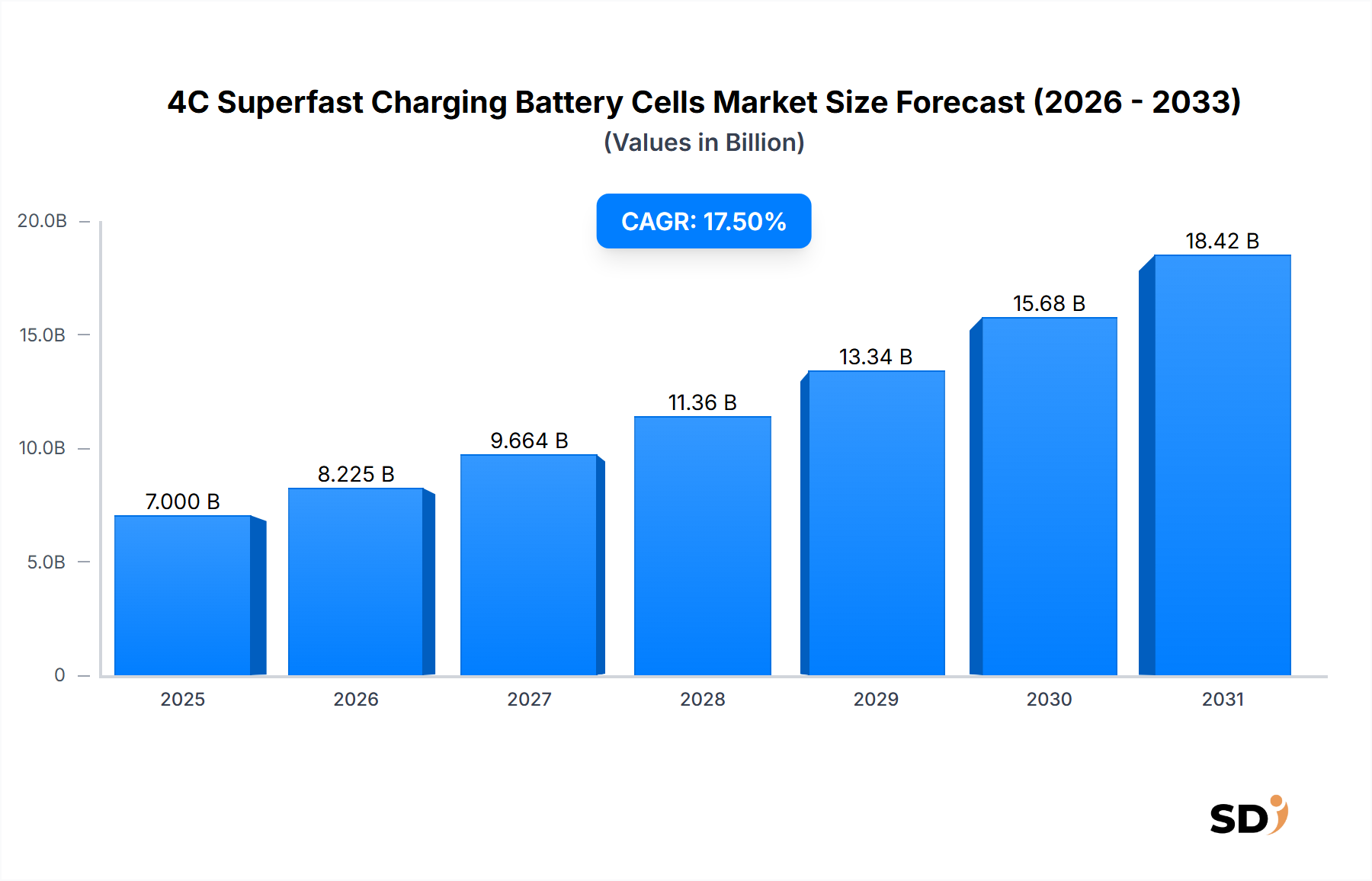

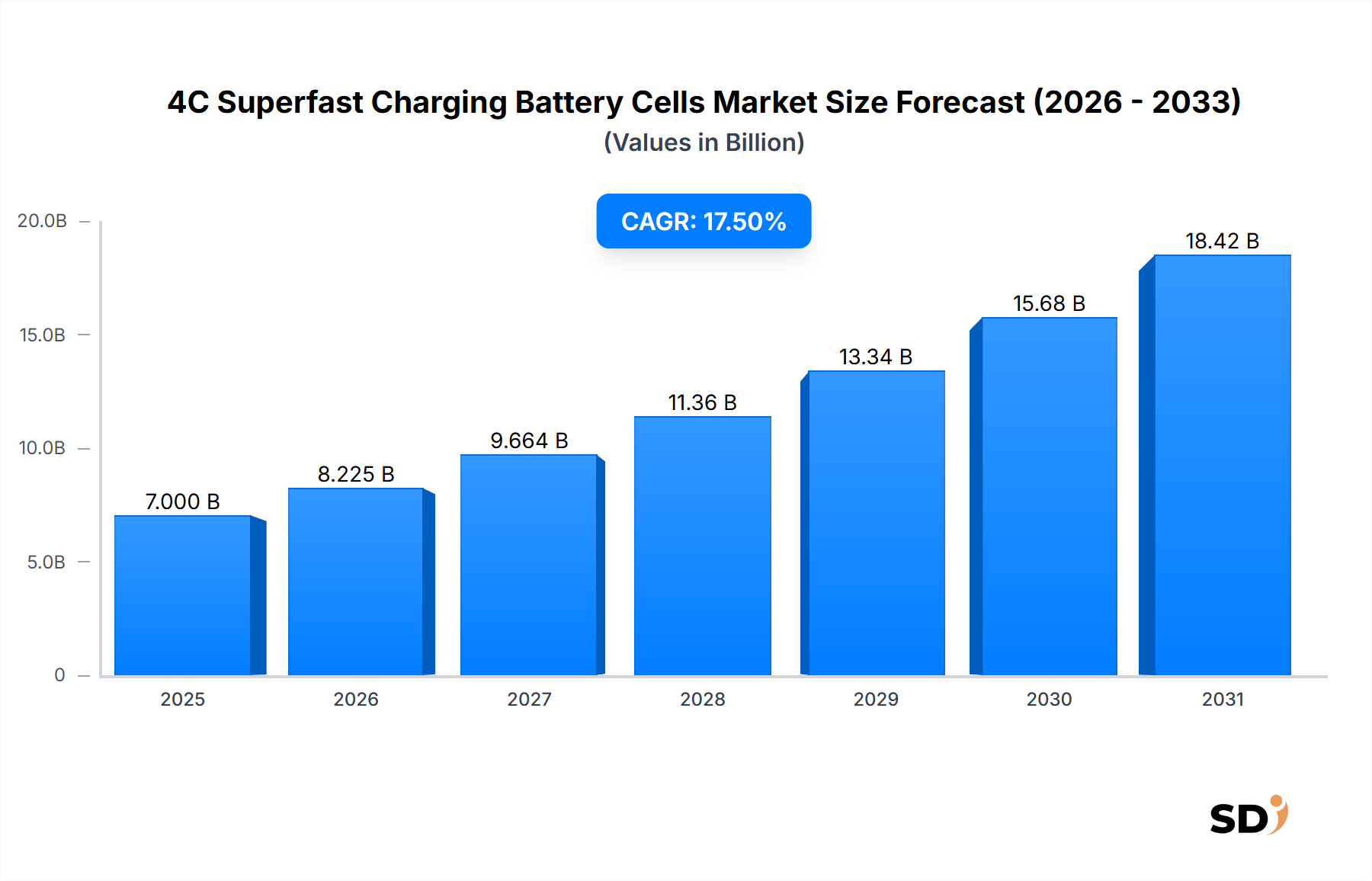

The global 4C Superfast Charging Battery Cells Market, valued at approximately $7 billion in 2023, is poised for robust expansion, projected to reach an estimated $42.525 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 17.5% during the forecast period. This remarkable growth trajectory is fundamentally driven by the escalating demand for rapid charging solutions across diverse applications, particularly in the burgeoning electric vehicle (EV) sector. Consumers and industries alike are increasingly prioritizing efficiency and convenience, making 4C charging capabilities a critical differentiator. The imperative to mitigate range anxiety in Electric Vehicle Battery Market applications, coupled with the need for faster turnaround times in commercial and logistics fleets, acts as a significant catalyst for market expansion. Furthermore, the integration of renewable energy sources necessitates sophisticated Energy Storage Systems Market, where quick charging and discharging cycles enhance grid stability and operational flexibility.

4C Superfast Charging Battery Cells Market Size (In Billion)

20.0B

15.0B

10.0B

5.0B

0

7.000 B

2025

8.225 B

2026

9.664 B

2027

11.36 B

2028

13.34 B

2029

15.68 B

2030

18.42 B

2031

Macroeconomic tailwinds, including aggressive governmental policies promoting electric mobility and substantial investments in smart grid infrastructure, are creating a fertile ground for the 4C Superfast Charging Battery Cells Market. For instance, regulatory mandates aiming to phase out internal combustion engine vehicles by specific deadlines across North America and Europe are directly fueling the demand for advanced battery technologies. Innovations in battery chemistry, such as high-nickel Ternary Lithium Battery Market compositions and advancements in Lithium Iron Phosphate (LFP) Battery Market architectures, are crucial in achieving higher charging rates while maintaining safety and longevity. Research and development efforts are continuously pushing the boundaries of material science, focusing on novel electrode materials, enhanced electrolyte formulations, and robust Battery Management Systems Market that can safely handle the thermal and electrical stresses associated with 4C charging.

The market outlook for 4C Superfast Charging Battery Cells is exceptionally positive, characterized by an intense competitive landscape driving continuous innovation. Key players are investing heavily in expanding manufacturing capacities and forging strategic partnerships with automotive OEMs and energy developers to integrate their cutting-edge solutions. The increasing sophistication of the Fast Charging Technology Market is not merely about speed but also about optimizing battery health and cycle life, addressing a critical concern for end-users. As the cost of battery production continues to decline through economies of scale and improved manufacturing processes, the adoption of 4C superfast charging capabilities is expected to permeate beyond premium segments into mass-market applications, further accelerating market growth. The ongoing global transition towards sustainable energy solutions solidifies the long-term prospects of this dynamic market, underscoring its pivotal role in the future of electric mobility and grid-scale energy storage.

Dominant Application Segment in 4C Superfast Charging Battery Cells Market

The Electric Vehicles (EVs) application segment stands as the unequivocal dominant force within the 4C Superfast Charging Battery Cells Market, commanding the largest revenue share and exhibiting a trajectory of sustained growth. This segment's preeminence is directly attributable to the global automotive industry's aggressive pivot towards electrification, spurred by escalating environmental concerns, stringent emissions regulations, and compelling governmental incentives. The ability of 4C battery cells to rapidly replenish an EV's charge significantly addresses one of the primary barriers to EV adoption: range anxiety and long charging times. For an average EV, a 4C charging rate can mean adding hundreds of kilometers of range in merely 10-15 minutes, thereby paralleling the refueling experience of conventional gasoline vehicles. This transformative capability is especially critical for commercial EV fleets, ride-sharing services, and high-utilization private vehicles where downtime directly impacts operational efficiency and profitability. The demand for such swift charging is particularly pronounced in the premium and performance EV segments, where users expect cutting-edge technology and unparalleled convenience.

Key players in the 4C Superfast Charging Battery Cells Market, such as Contemporary Amperex Technology Co. Ltd., LG Energy Solution Ltd., and Samsung SDI Co., Ltd., are heavily invested in developing and supplying these advanced cells to major automotive OEMs. These manufacturers are not only focusing on increasing the charging speed but also on optimizing the energy density and cycle life under rigorous fast-charging conditions. For instance, the ongoing advancements in electrode materials, particularly in the Anode Material Market and Cathode Material Market, are central to enabling higher current densities without compromising battery integrity. The integration of sophisticated thermal management systems and advanced Battery Management Systems Market algorithms is also paramount to ensure safe and efficient operation during high-rate charging events. The rapid expansion of charging infrastructure, particularly ultra-fast charging stations along major highways and urban centers, further reinforces the dominance of the EV segment by making 4C charging a practical reality for a growing number of drivers.

While the Electric Vehicle Battery Market is the primary driver, advancements in battery technology also benefit other segments, such as the Energy Storage Systems Market, which demands high power delivery capabilities. However, the sheer volume and continuous innovation cycles within the automotive industry mean that the EV application segment will likely continue to consolidate its lead. The shift towards next-generation EV platforms specifically designed to accommodate 4C charging, coupled with consumer preferences for vehicles offering superior charging performance, will further entrench this segment's dominance. This segment also benefits from the diverse battery chemistries being optimized for fast charging, including both the Ternary Lithium Battery Market, known for its high energy density, and the Lithium Iron Phosphate (LFP) Battery Market, valued for its cost-effectiveness and safety profile. The combined effect of technological push, consumer pull, and regulatory support ensures that the EV application remains the cornerstone of the 4C Superfast Charging Battery Cells Market's growth over the forecast period.

The 4C Superfast Charging Battery Cells Market is shaped by a confluence of compelling drivers and inherent constraints. A primary driver is the accelerating global adoption of Electric Vehicles (EVs). With countries enacting ambitious policies, such as the European Union's proposed ban on new internal combustion engine car sales from 2035, the demand for efficient and rapid EV charging solutions has surged. This legislative push, coupled with consumer preference for convenience, directly fuels the Electric Vehicle Battery Market and necessitates faster charging capabilities to alleviate range anxiety and minimize vehicle downtime. Data indicates a year-over-year increase in global EV sales by over 30% in recent periods, underscoring this trend.

Another significant driver is the expansion of the Energy Storage Systems Market. As renewable energy sources like solar and wind become more prevalent, the need for efficient grid-scale storage solutions that can quickly absorb and release power becomes critical. 4C charging capabilities are highly advantageous here, enabling faster energy cycling for grid stabilization, peak shaving, and demand response services, which are crucial for a resilient and sustainable power infrastructure. This demand is further amplified by significant investments in smart grid technologies, with global smart grid spending projected to exceed $70 billion annually by 2028.

Conversely, the market faces several inherent constraints. Firstly, the elevated cost of advanced raw materials poses a significant hurdle. High-performance battery cells often rely on specific cathode materials, such as nickel-rich formulations, or specialized anode materials, like silicon-graphite composites, which are more expensive and subject to price volatility in the global Cathode Material Market and Anode Material Market. This directly impacts the overall manufacturing cost of 4C cells, potentially hindering broader market penetration. Secondly, safety concerns associated with rapid charging are critical. Charging at 4C rates generates substantial heat, increasing the risk of thermal runaway. While Battery Management Systems Market are continually improving, ensuring robust safety protocols without compromising charging speed or battery longevity remains a complex engineering challenge. Finally, the existing charging infrastructure requires substantial upgrades to support widespread 4C charging. This involves significant investments in higher-capacity grid connections and specialized charging hardware, which can be a slow and capital-intensive process, limiting the immediate scalability of the Fast Charging Technology Market.

Competitive Ecosystem of 4C Superfast Charging Battery Cells Market

The 4C Superfast Charging Battery Cells Market is characterized by intense competition among a concentrated group of global leaders, primarily based in Asia, alongside a growing number of innovators. These companies are continually pushing the boundaries of battery chemistry, cell design, and manufacturing processes to achieve higher charging rates, improved energy density, and enhanced safety, impacting the broader Lithium-ion Battery Market.

Contemporary Amperex Technology Co. Ltd.: A global leader in battery manufacturing, known for extensive R&D in fast-charging technologies and a wide portfolio of cells, particularly strong in the Electric Vehicle Battery Market.

BYD Company Limited: An integrated technology company with significant capabilities in both EV manufacturing and battery production, increasingly exploring rapid charging capabilities with technologies like its Blade Battery.

LG Energy Solution Ltd.: A prominent global battery manufacturer supplying a broad range of lithium-ion cells for EVs and Energy Storage Systems Market, continuously innovating in material science for faster charging.

Samsung SDI Co., Ltd.: A leading provider of high-performance battery solutions, actively engaged in developing next-generation materials and designs enabling superfast charging for automotive and mobile applications.

SK On Co., Ltd.: A rapidly growing battery manufacturer focusing on advanced Ternary Lithium Battery Market technologies, investing heavily in global production and enhancing charging performance for automotive partners.

Panasonic Holdings Corporation: A long-standing player known for its collaboration with major EV manufacturers and ongoing efforts to refine cell technology for improved energy density, safety, and charging speeds.

Prime Planet Energy & Solutions: A joint venture between Toyota and Panasonic, dedicated to high-performance automotive batteries, with a focus on advanced chemistries for future EVs.

China Aviation Lithium Battery Co., Ltd. (CALB): A significant Chinese battery manufacturer with a strong focus on LFP and high-nickel ternary batteries, expanding market share with solutions for various EV and ESS applications.

Gotion High-Tech Co., Ltd.: A technology-driven company specializing in power battery R&D and manufacturing, providing both Lithium Iron Phosphate (LFP) Battery Market and ternary solutions, with developments in increasing charging rates.

EVE Energy Co., Ltd.: A diversified battery manufacturer with advancements in both cylindrical and prismatic cell formats, conducive to fast charging for consumer electronics to power batteries for EVs.

SVOLT Energy Technology Co., Ltd.: A newer entrant focusing on advanced chemistries and innovative cell designs, with a strong emphasis on achieving superfast charging performance.

Sunwoda Electronic Co., Ltd.: A comprehensive energy solution provider active in various battery segments, continuously developing Fast Charging Technology Market capabilities across its product lines.

Farasis Energy, Inc.: A global developer of soft-pack pouch power batteries for electric vehicles, specializing in high-energy density NMC cells and actively enhancing their fast-charging performance.

The 4C Superfast Charging Battery Cells Market has witnessed a flurry of strategic activities and technological advancements aimed at enhancing performance and broadening application scope. These developments underscore the industry's commitment to overcoming technical hurdles and meeting growing demand.

October 2023: Several leading battery manufacturers, including Contemporary Amperex Technology Co. Ltd. and LG Energy Solution Ltd., announced breakthroughs in advanced electrolyte formulations, enabling more stable ion transport at high charging rates for 4C battery cells.

August 2023: A major European automotive OEM unveiled its next-generation EV platform, explicitly designed to integrate 4C superfast charging capabilities, signaling a growing industry trend towards native support for ultra-rapid power delivery.

June 2023: Investments in the Cathode Material Market saw a significant boost, with several material suppliers announcing expanded production capacities for high-nickel and manganese-rich cathode materials crucial for high-performance and fast-charging Lithium-ion Battery Market cells.

April 2023: Collaborative pilot projects between energy companies and battery manufacturers were initiated in North America to deploy specialized charging infrastructure capable of delivering the power required for widespread 4C superfast charging.

February 2023: New patents were filed focusing on enhanced Battery Management Systems Market algorithms, specifically designed to monitor and optimize cell health during 4C charging cycles, minimizing degradation and maximizing safety.

November 2022: Researchers demonstrated a novel silicon-anode material that significantly improved the energy density and Fast Charging Technology Market performance of experimental cells, indicating future advancements for the Anode Material Market.

September 2022: Asian battery producers announced strategic partnerships with mining companies to secure long-term supplies of critical raw materials, aiming to mitigate supply chain risks for the burgeoning Electric Vehicle Battery Market.

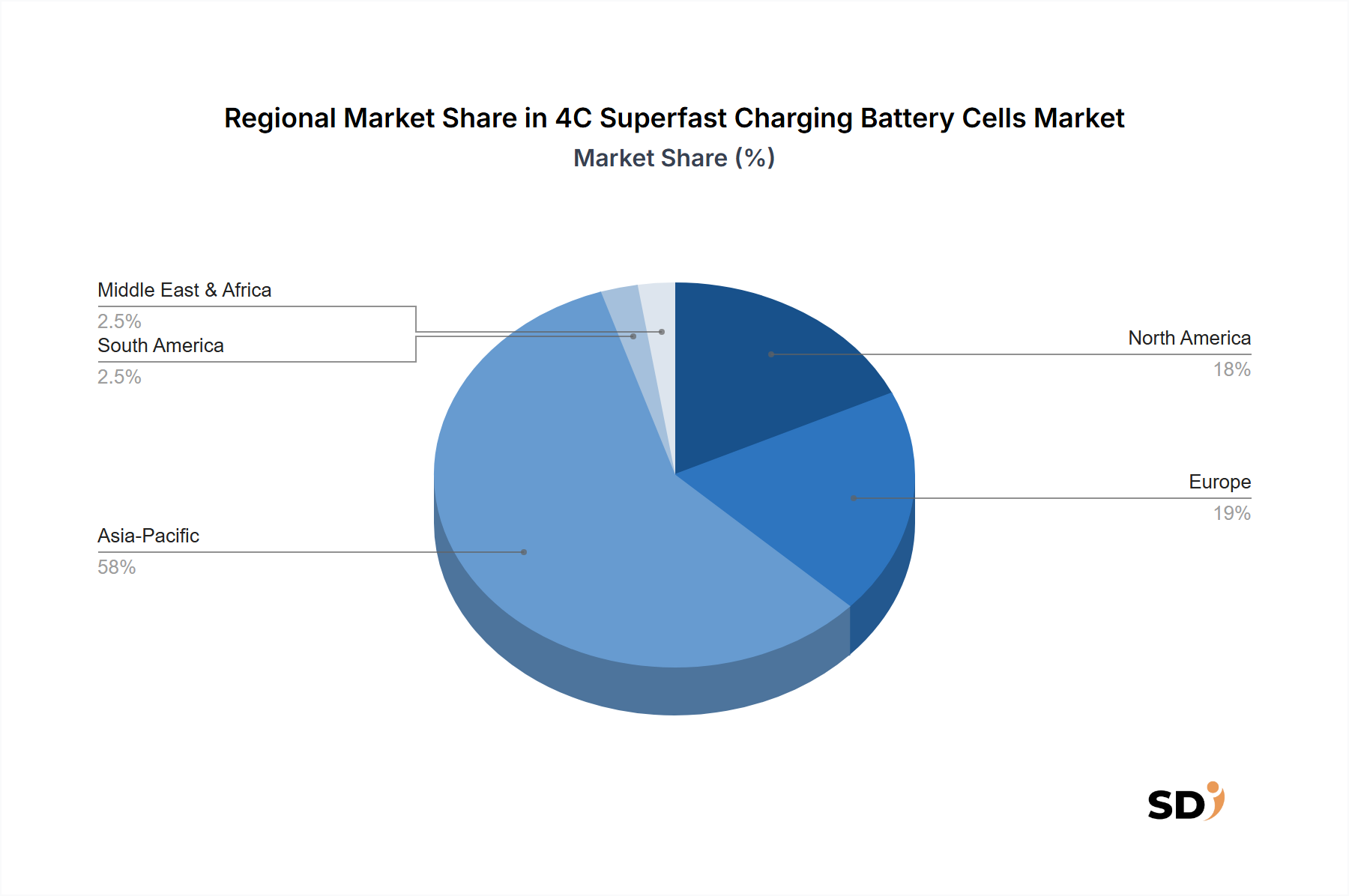

Regional Market Breakdown for 4C Superfast Charging Battery Cells Market

The global 4C Superfast Charging Battery Cells Market exhibits significant regional variations in growth, adoption rates, and underlying demand drivers. Asia Pacific currently dominates the market, primarily propelled by the robust expansion of the Electric Vehicle Battery Market in China and South Korea, which are also major hubs for battery manufacturing. China, in particular, benefits from extensive government subsidies, a large domestic EV market, and a highly developed battery supply chain, including key players in the Ternary Lithium Battery Market and Lithium Iron Phosphate (LFP) Battery Market. The region is projected to maintain its leading market share, with a high CAGR driven by continuous technological advancements and increasing investments in new battery production facilities. This dominance is further supported by the substantial presence of raw material processing facilities and a skilled labor force, cementing its position as a global leader in the Lithium-ion Battery Market.

Europe is anticipated to be one of the fastest-growing regions for 4C Superfast Charging Battery Cells, driven by ambitious decarbonization targets and stringent emission regulations. Countries like Germany, France, and the UK are witnessing accelerated EV adoption rates, supported by attractive incentives and significant investments in charging infrastructure. The region's focus on renewable energy integration also fuels the demand for the Energy Storage Systems Market, where 4C cells can enhance grid flexibility. The demand driver here is predominantly policy-driven electrification mandates and a strong consumer appetite for sustainable transportation solutions.

North America is also experiencing substantial growth, largely attributed to increasing consumer adoption of EVs and supportive governmental policies, such as the Inflation Reduction Act in the United States, which offers tax credits for domestically produced electric vehicles and batteries. Significant investments in public and private charging networks are underway to support the proliferation of faster charging capabilities. The primary demand driver for North America is the shifting consumer preference towards electric mobility, coupled with strategic investments in localized battery manufacturing and the Fast Charging Technology Market.

The Middle East & Africa and South America regions, while currently holding smaller market shares, are poised for emerging growth. In the Middle East & Africa, growing interest in renewable energy projects and smart city initiatives in GCC countries are creating nascent demand for advanced energy storage solutions. In South America, the development of local EV markets and expanding charging infrastructure, albeit from a lower base, are expected to contribute to future market expansion. The demand driver in these regions is nascent EV adoption and increasing urbanization, alongside diversification efforts in energy sectors.

Supply Chain & Raw Material Dynamics for 4C Superfast Charging Battery Cells Market

The supply chain for the 4C Superfast Charging Battery Cells Market is complex and globally interdependent, characterized by significant upstream dependencies and inherent sourcing risks. Key raw materials include lithium, nickel, cobalt, and manganese for the Cathode Material Market, particularly for Ternary Lithium Battery Market chemistries. For Lithium Iron Phosphate (LFP) Battery Market cells, iron and phosphate are crucial. The Anode Material Market primarily relies on graphite, with a growing interest in silicon-based composites for enhanced performance. Electrolytes, separators, and binders constitute other vital components.

Sourcing risks are substantial due to the concentrated geographical distribution of these critical minerals. For instance, a significant portion of the world's cobalt originates from the Democratic Republic of Congo, while lithium is largely mined in Australia, Chile, and Argentina. Nickel production is dominated by Indonesia and Russia. This concentration creates geopolitical vulnerabilities and susceptibility to supply disruptions, as seen during recent global events. Price volatility for these raw materials is a constant challenge, driven by supply-demand imbalances, geopolitical tensions, and speculative trading. For example, lithium prices experienced unprecedented spikes in 2021-2022 before stabilizing, directly impacting battery production costs.

Disruptions in the raw material supply chain can significantly affect the manufacturing output and pricing strategies within the 4C Superfast Charging Battery Cells Market. Shortages or sudden price increases for critical inputs can lead to higher battery cell costs, potentially slowing the adoption rate of Electric Vehicle Battery Market and Energy Storage Systems Market. To mitigate these risks, market participants are increasingly pursuing diversified sourcing strategies, including direct investments in mining operations, long-term supply agreements, and exploring recycling technologies to recover valuable materials. The ongoing efforts to develop new battery chemistries that reduce reliance on scarce or high-cost materials (e.g., cobalt-free solutions) also represent a strategic response to these supply chain pressures, aiming to build a more resilient and sustainable Lithium-ion Battery Market ecosystem.

The pricing dynamics within the 4C Superfast Charging Battery Cells Market are subject to a delicate balance of technological innovation, raw material costs, and intense competitive pressures. Historically, average selling prices (ASPs) for lithium-ion battery cells have demonstrated a downward trend due to economies of scale, advancements in manufacturing processes, and continuous improvements in energy density per unit cost. However, the specialized nature and higher performance requirements of 4C superfast charging cells often command a premium, at least in the initial stages of market penetration.

Margin structures across the value chain, from raw material suppliers to cell manufacturers and ultimately to EV OEMs or ESS integrators, are under constant pressure. Battery manufacturers face the challenge of absorbing volatile raw material costs, particularly for inputs like lithium, nickel, and cobalt, which are critical for high-performance cells in the Cathode Material Market and Anode Material Market. These commodity cycles can significantly erode profitability if not effectively managed through hedging strategies or long-term procurement contracts. The competitive intensity within the Fast Charging Technology Market further exacerbates margin pressure, as companies strive to offer innovative solutions at competitive price points to gain market share in the Electric Vehicle Battery Market.

Key cost levers include optimizing raw material utilization, enhancing manufacturing efficiency through automation and advanced production techniques, and investing in R&D to develop more cost-effective yet high-performing battery chemistries. The ability to vertically integrate certain aspects of the supply chain, or establish strong strategic partnerships, can also provide a competitive edge in managing costs. As the market matures and production scales up, cost reductions are anticipated, making 4C superfast charging more accessible. However, the continuous drive for higher energy density, faster charging rates, and improved safety features will likely ensure that R&D expenditure remains a significant component of the overall cost structure, impacting long-term margin potential across the broader Lithium-ion Battery Market.

4C Superfast Charging Battery Cells Segmentation

1. Type

1.1. Ternary Lithium Batteries

1.2. Lithium Iron Phosphate (LFP) Batteries

2. Battery Capacity

2.1. Below 2000 mAh

2.2. 2000-4000 mAh

2.3. Above 4000 mAh

3. Application

3.1. Electric Vehicles (EVs)

3.2. Energy Storage Systems (ESS)

3.3. Others

4. End-Use

4.1. Residential

4.2. Commercial

4C Superfast Charging Battery Cells Segmentation By Geography

Table 96: Volume K Forecast, by Battery Capacity 2020 & 2033

Table 97: Revenue billion Forecast, by Application 2020 & 2033

Table 98: Volume K Forecast, by Application 2020 & 2033

Table 99: Revenue billion Forecast, by End-Use 2020 & 2033

Table 100: Volume K Forecast, by End-Use 2020 & 2033

Table 101: Revenue billion Forecast, by Country 2020 & 2033

Table 102: Volume K Forecast, by Country 2020 & 2033

Table 103: Revenue (billion) Forecast, by Application 2020 & 2033

Table 104: Volume (K) Forecast, by Application 2020 & 2033

Table 105: Revenue (billion) Forecast, by Application 2020 & 2033

Table 106: Volume (K) Forecast, by Application 2020 & 2033

Table 107: Revenue (billion) Forecast, by Application 2020 & 2033

Table 108: Volume (K) Forecast, by Application 2020 & 2033

Table 109: Revenue (billion) Forecast, by Application 2020 & 2033

Table 110: Volume (K) Forecast, by Application 2020 & 2033

Table 111: Revenue (billion) Forecast, by Application 2020 & 2033

Table 112: Volume (K) Forecast, by Application 2020 & 2033

Table 113: Revenue (billion) Forecast, by Application 2020 & 2033

Table 114: Volume (K) Forecast, by Application 2020 & 2033

Table 115: Revenue (billion) Forecast, by Application 2020 & 2033

Table 116: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is the cornerstone of our market intelligence, accounting for 70-80% of our total research efforts. This approach is designed to capture nuanced insights, validate secondary findings, and uncover latent market dynamics directly from industry experts. We conduct extensive qualitative and quantitative interviews, utilizing structured and semi-structured questionnaires to ensure comprehensive data collection. This direct engagement provides unparalleled depth into market trends, competitive landscapes, technological advancements, pricing strategies, and regional specificities relevant to 4C Superfast Charging Battery Cells.

Key stakeholders targeted for primary interviews include:

VP/Director of Battery Technology & R&D (at cell manufacturers and automotive OEMs)

Head of Product Management (across battery cells, EV platforms, and ESS solutions)

Senior Supply Chain & Procurement Manager (focused on critical battery components and raw materials)

Senior Power Electronics/Charging Systems Engineer (specializing in fast-charging infrastructure and battery integration)

These interviews span a diverse range of companies across the value chain, ensuring a holistic market perspective:

Battery Cell Manufacturers (e.g., producers of Ternary Lithium and LFP 4C cells)

Electric Vehicle (EV) Original Equipment Manufacturers (OEMs) (integrating 4C cells into their vehicles)

Energy Storage System (ESS) Integrators & Developers (deploying 4C cells for grid-scale or residential storage)

Raw Material & Component Suppliers (e.g., cathode/anode material producers for 4C optimized chemistries)

Battery Management System (BMS) & Charging Infrastructure Providers (enabling and optimizing 4C charging capabilities)

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP/Director of Battery Technology & R&D

30%

Head of Product Management (Batteries/EVs/ESS)

25%

Senior Supply Chain & Procurement Manager

25%

Senior Power Electronics/Charging Systems Engineer

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Battery Cell Manufacturers

35%

Electric Vehicle (EV) OEMs

25%

Energy Storage System (ESS) Integrators

15%

Raw Material & Component Suppliers

15%

BMS & Charging Infrastructure Providers

10%

Secondary Research & Industry Benchmarking

Secondary research forms 20-30% of our methodology, serving as a critical foundation for initial market sizing, trend identification, and data validation. We meticulously gather data from reputable, verifiable sources, ensuring robust industry benchmarking. Our firm explicitly avoids data from other market research websites to maintain the highest standard of originality and integrity.

Key secondary data sources include:

Financial Databases: Bloomberg, Factiva, Hoovers, and PitchBook, providing company financial performance, investment trends, and strategic developments.

Government Publications: Official statistics, policy documents, and energy reports from national and international government bodies (e.g., U.S. Department of Energy .Gov, European Commission .Gov).

Industry Associations & Regulatory Bodies: Publications, whitepapers, and reports from leading industry organizations and standard-setting bodies:

International Electrotechnical Commission (IEC) .org (for battery safety and performance standards)

Global Battery Alliance (GBA) .org (focused on sustainable battery value chains)

The European Association for Storage of Energy (EASE) .org (advocating for energy storage solutions)

SAE International .org (for automotive engineering and charging standards)

Corporate Filings & Annual Reports: Publicly available disclosures from key market players.

Academic Research & Scientific Journals: Peer-reviewed studies on battery technology advancements and material science.

All data is systematically reviewed and updated up to the date of purchase, ensuring the report reflects the most current market conditions and developments.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies employ a robust combination of top-down and bottom-up approaches, triangulated across multiple levels to ensure accuracy and consistency. This multi-layered validation process mitigates potential biases and provides a comprehensive view of the market's trajectory from 2026-2034.

Top-Down Approach: This involves analyzing macro-economic indicators, industry-wide growth forecasts for EVs and ESS, and regulatory landscapes to estimate the total addressable market for battery cells. This global or regional estimate is then disaggregated based on the projected penetration of 4C superfast charging technology.

Bottom-Up Approach: This method meticulously builds market size by aggregating detailed data points from the ground up. Key metrics and variables used for the 4C Superfast Charging Battery Cells market include:

Annual Production/Sales Volume of 4C-enabled EVs and ESS Units: Segmented by vehicle type (passenger, commercial) and ESS scale (residential, utility-scale) across all regions.

Average Battery Pack Capacity (kWh) per Unit: The typical energy capacity of battery packs utilizing 4C superfast charging cells for both EV and ESS applications.

Penetration Rate of 4C Technology: The projected adoption rate of 4C superfast charging battery cells within the broader EV and ESS battery markets, influenced by technological maturity, cost-effectiveness, and consumer demand.

Average Selling Price (ASP) per kWh for 4C Cells: The pricing dynamics of 4C cells, considering variations by chemistry (Ternary Lithium, LFP), capacity (Below 2000 mAh, 2000-4000 mAh, Above 4000 mAh), and regional market conditions.

These granular estimates are then aggregated to project market size by type, capacity, application, end-use, and all specified geographic regions.

Data Accuracy & Quality Check

Our commitment to data integrity ensures an estimated data accuracy level of 85-90%. This rigorous standard is maintained through a multi-stage quality assurance process:

Multi-Level Data Triangulation: Data points are cross-verified using inputs from primary interviews, diverse secondary sources, and quantitative modeling results. Any discrepancies are investigated and reconciled through further research.

Expert Panel Review: Our internal team of seasoned analysts, along with external industry experts, critically reviews all data, assumptions, and forecasts to challenge methodologies and refine conclusions.

Iterative Refinement: The entire research process is iterative. Initial findings are continually validated and refined as new information emerges, ensuring the report's conclusions are robust and reflective of current market realities.

Quantitative and Qualitative Consistency: We ensure that quantitative market figures align logically with qualitative market drivers, challenges, and trends identified throughout the research. This holistic approach guarantees a coherent and reliable market narrative.

Frequently Asked Questions

1. What technological innovations are driving the 4C Superfast Charging Battery Cells market?

Innovations focus on improving energy density, safety, and cycle life for rapid charging applications. Developments in both Ternary Lithium and Lithium Iron Phosphate (LFP) battery chemistries are key to enhancing 4C performance. Leading companies like Contemporary Amperex Technology Co. Ltd. are investing heavily in these advancements.

2. What are the main challenges impacting the 4C Superfast Charging Battery Cells supply chain?

Challenges include sourcing critical raw materials like lithium and nickel, ensuring cost-effective manufacturing processes, and managing thermal runaway risks during rapid charging. Geopolitical factors can also influence global supply chain stability for key components.

3. How are consumer preferences influencing the adoption of 4C Superfast Charging Battery Cells?

Consumer demand for quicker charging times in Electric Vehicles (EVs) and reliable power for Energy Storage Systems (ESS) is a primary driver. The convenience of reducing charging duration directly impacts purchase decisions, especially for high-capacity applications above 4000 mAh.

4. What sustainability factors are relevant to 4C Superfast Charging Battery Cells production and use?

Sustainability efforts focus on ethical raw material sourcing, reducing carbon footprints in manufacturing, and developing battery recycling programs. The environmental impact of end-of-life battery management is a critical consideration for producers like Samsung SDI Co., Ltd. and Panasonic Holdings Corporation.

5. Which regions dominate the export and import of 4C Superfast Charging Battery Cells components?

Asia-Pacific, particularly China, South Korea, and Japan, are major exporters of battery cells and components due to strong manufacturing bases. Europe and North America are significant importers, driven by their expanding EV and ESS markets, holding an estimated combined 37% market share.

6. What is the projected growth for the 4C Superfast Charging Battery Cells market through 2033?

The 4C Superfast Charging Battery Cells market was valued at $7 billion in 2023. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 17.5% through 2033, driven by increasing applications in Electric Vehicles and Energy Storage Systems.