Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Distributed Ammonia Cracking System by Application (Ship, Automobile, Hydrogen Generation Plant, Others), by Types (Catalyst Reactor, Membrane Reactor), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 16, 2026|Base Year : 2025|Pages : 90

Key Insights into the Distributed Ammonia Cracking System Market

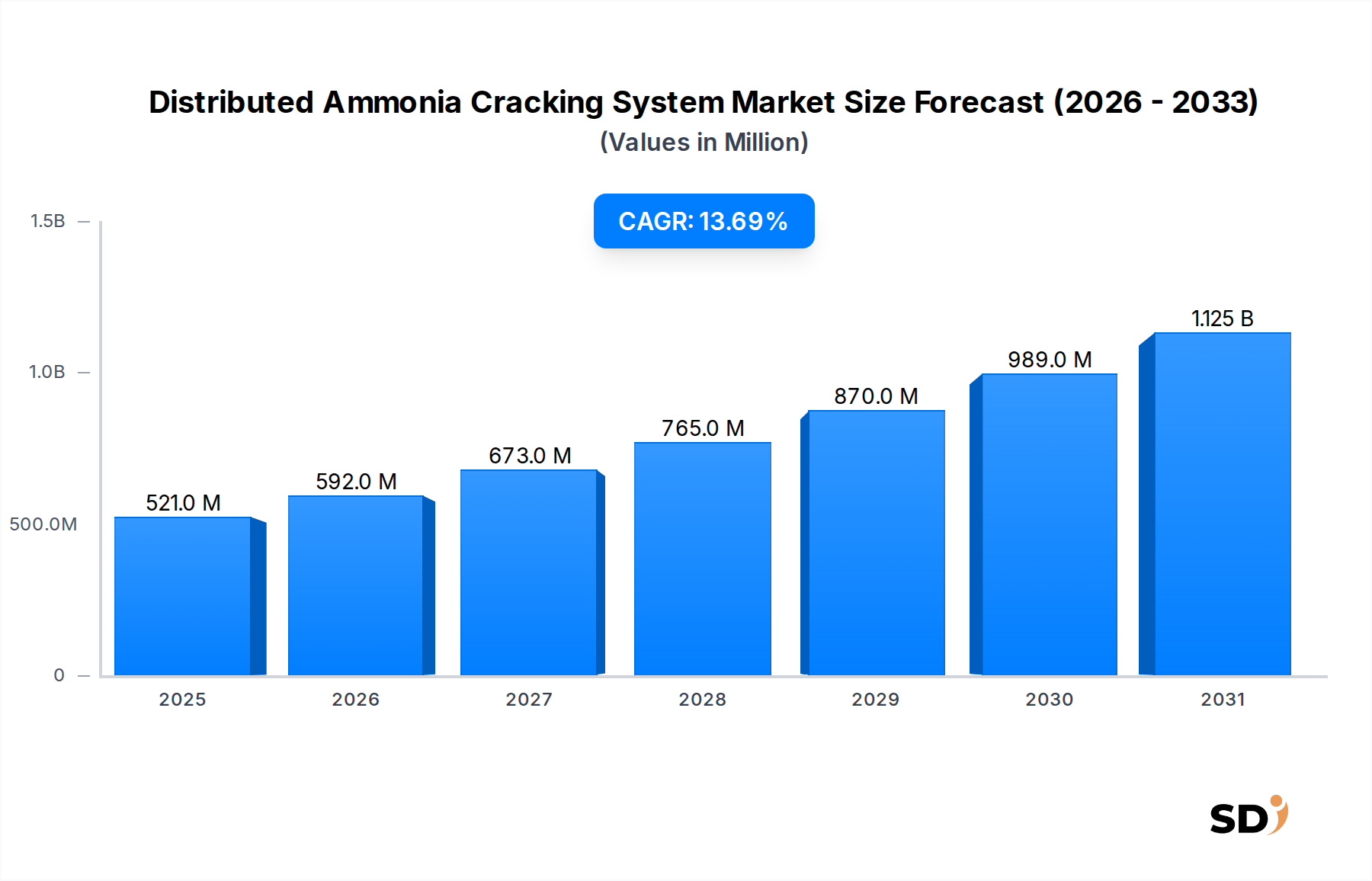

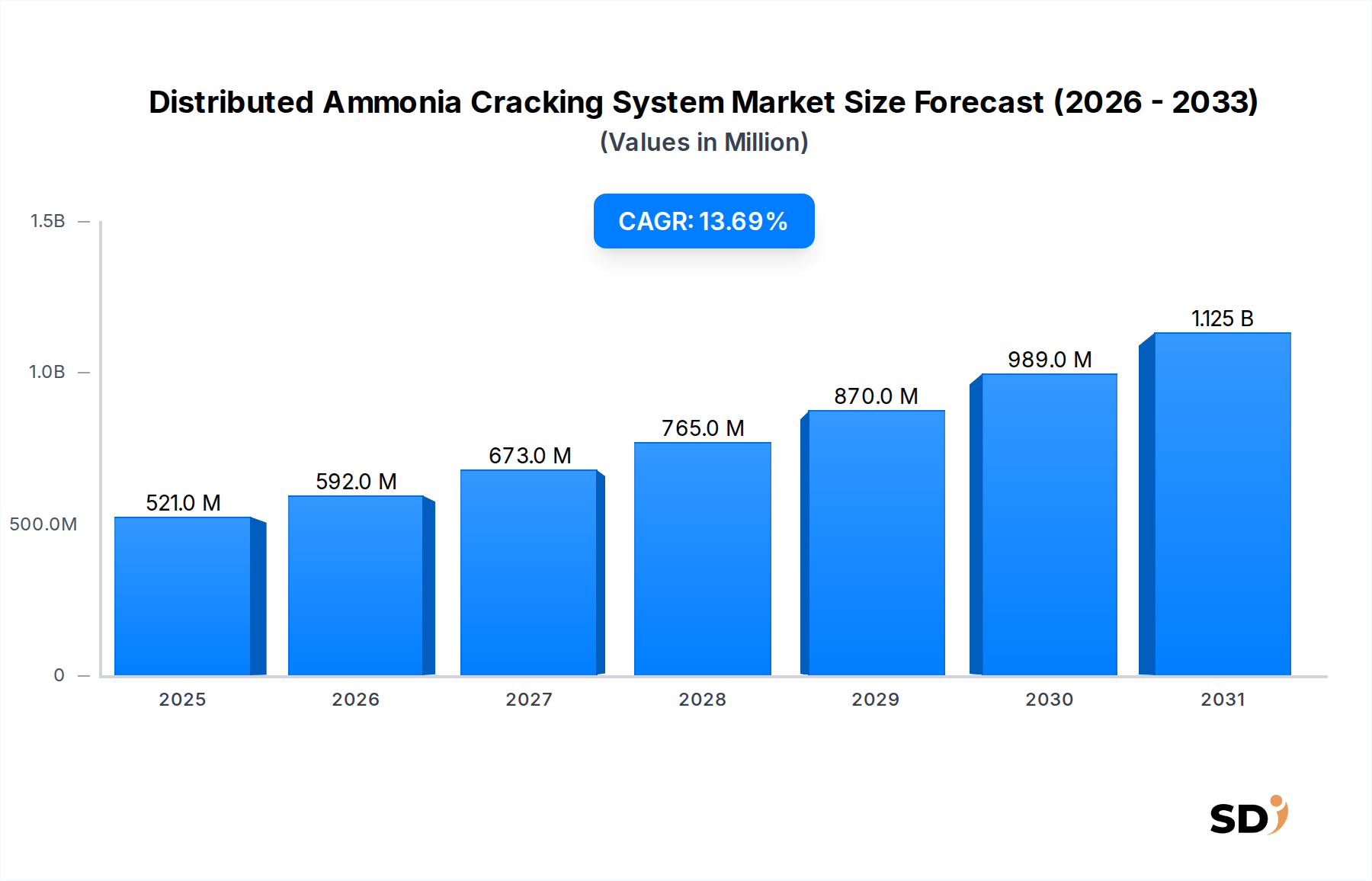

The Distributed Ammonia Cracking System Market is experiencing robust expansion, driven by the escalating global demand for clean hydrogen and the critical role of ammonia as an efficient hydrogen carrier. Valued at $520.6 million in 2024, the market is projected to reach $1,884.2 million by 2034, demonstrating an impressive Compound Annual Growth Rate (CAGR) of 13.7% over the forecast period. This significant growth trajectory is underpinned by macro tailwinds such as ambitious decarbonization goals, advancements in cracking technology, and strategic investments in hydrogen infrastructure.

Distributed Ammonia Cracking System Market Size (In Million)

1.5B

1.0B

500.0M

0

521.0 M

2025

592.0 M

2026

673.0 M

2027

765.0 M

2028

870.0 M

2029

989.0 M

2030

1.125 B

2031

Key demand drivers include the inherent advantages of ammonia in terms of storage and transportation density compared to compressed or liquefied hydrogen, making it an economically viable option for long-distance hydrogen supply chains. The imperative to reduce carbon emissions across various sectors, including heavy industry, power generation, and transportation, further fuels the adoption of distributed cracking solutions. As the world pivots towards a hydrogen economy, distributed ammonia crackers enable on-demand, localized hydrogen production, minimizing the complexities and costs associated with centralized hydrogen distribution.

Technological innovations, particularly in catalyst efficiency and reactor design, are enhancing the economic viability and operational performance of these systems. Furthermore, supportive government policies and funding initiatives aimed at accelerating the Energy Transition Market are creating a fertile ground for market expansion. The Hydrogen Generation Plant Market stands as a crucial application area, leveraging distributed cracking systems for decentralized hydrogen supply. Moreover, emerging applications in the Marine Fuel Market and heavy-duty transport are expected to contribute significantly to market growth as ammonia-to-hydrogen conversion becomes more mainstream. The outlook for the Distributed Ammonia Cracking System Market remains overwhelmingly positive, reflecting its pivotal role in enabling a sustainable, hydrogen-powered future.

The Dominant Catalyst Reactor Segment in the Distributed Ammonia Cracking System Market

Within the Distributed Ammonia Cracking System Market, the Catalyst Reactor segment currently holds the largest revenue share and is anticipated to maintain its dominance throughout the forecast period. This leadership is primarily attributed to the maturity, reliability, and established efficiency of catalytic cracking technologies. Traditional catalyst reactors, employing noble metals or transition metal-based catalysts, have been extensively researched and optimized for ammonia decomposition, offering predictable performance and relatively lower capital expenditure compared to more nascent alternatives.

Key players in the Distributed Ammonia Cracking System Market, such as Johnson Matthey, Topsoe, and Toyo Engineering, have significant expertise in catalyst development and reactor engineering, contributing to the segment's stronghold. These companies continuously innovate to improve catalyst longevity, reduce energy consumption, and enhance reaction kinetics, further solidifying the Catalyst Reactor Market position. The widespread availability of proven catalyst materials and design methodologies also reduces the technological risk for early adopters, facilitating broader market penetration.

While the Membrane Reactor Market represents a promising technological advancement offering potential for higher hydrogen purity and improved energy integration, it is still in earlier stages of commercialization. Membrane reactors leverage selective membranes to separate hydrogen in situ, driving the reaction equilibrium forward and potentially reducing operating temperatures. However, challenges related to membrane durability, poisoning, and scalability need to be fully addressed before they can significantly displace conventional catalyst reactors. For the immediate future, the cost-effectiveness, robust operational history, and continuous incremental improvements in catalyst technology ensure that the Catalyst Reactor segment will remain the cornerstone of distributed ammonia cracking, even as membrane technology progresses and gains traction in niche or specialized applications.

Key Market Drivers & Constraints in the Distributed Ammonia Cracking System Market

The Distributed Ammonia Cracking System Market is influenced by a complex interplay of drivers and constraints, each significantly shaping its growth trajectory and adoption rates.

One primary driver is the increasing recognition of ammonia as a superior hydrogen carrier. Ammonia boasts a volumetric hydrogen density of 108 kg H2/m³, which is significantly higher than liquid hydrogen (71 kg H2/m³) and compressed hydrogen (39 kg H2/m³ at 700 bar). This makes ammonia transport more economically viable over long distances, positioning distributed cracking systems at the demand point as a practical solution for global hydrogen supply chains. The Green Hydrogen Market expansion is intrinsically linked, as distributed cracking enables the utilization of green ammonia produced from renewable sources to deliver clean hydrogen.

Another significant driver is the global push for decarbonization and energy independence. Governments worldwide are implementing stringent emissions reduction targets, spurring investment in low-carbon technologies. For example, the European Union's ambitious hydrogen strategy targets 40 GW of electrolyzer capacity by 2030, requiring efficient methods for hydrogen delivery, for which distributed ammonia cracking is highly suitable. This policy support fosters technological development and market uptake.

Conversely, a major constraint is the energy intensity of the ammonia cracking process. The endothermic reaction typically requires temperatures between 400°C and 800°C, demanding substantial energy input. While technological advancements are reducing this requirement, it still represents a significant operational cost. The Catalyst Material Market is also a point of concern, as the long-term stability and cost of catalysts, particularly those based on noble metals like ruthenium, can impact system economics. Catalyst degradation and poisoning by unreacted ammonia or other impurities necessitate regular replacement, adding to operational expenses. Furthermore, the nascent stage of broad infrastructure development for ammonia handling and transport for fuel applications presents a barrier, requiring significant upfront capital investment to scale.

Competitive Ecosystem of Distributed Ammonia Cracking System Market

The competitive landscape of the Distributed Ammonia Cracking System Market is characterized by a mix of established industrial players, specialized technology firms, and innovative startups, all vying for market share in the burgeoning hydrogen economy. These companies are focused on developing more efficient, cost-effective, and scalable ammonia cracking solutions.

Reaction Engines: A company renowned for its SABRE engine technology, it is also exploring ammonia cracking for aerospace applications, aiming to leverage its expertise in high-temperature thermal management systems for efficient hydrogen release.

AFC Energy: Primarily focused on alkaline fuel cell technology, AFC Energy is also working on integrated solutions that combine ammonia cracking with fuel cells to provide zero-emission power generation, particularly for off-grid and marine applications.

H2SITE: Specializes in integrated membrane reactors for on-site hydrogen production from various feedstocks, including ammonia. Their technology aims to achieve high-purity hydrogen separation and enhanced cracking efficiency in a single unit.

Johnson Matthey: A global leader in sustainable technologies, Johnson Matthey offers advanced catalysts and process technologies for ammonia synthesis and decomposition. Their focus is on developing highly efficient and durable catalysts crucial for distributed cracking systems.

Topsoe: Known for its catalytic solutions and process technologies, Topsoe is a significant player in the ammonia value chain, providing catalysts and technologies for large-scale ammonia production and cracking, with an increasing focus on smaller, distributed units.

Metacon: A clean hydrogen and heat provider, Metacon develops and supplies energy systems based on proprietary technologies, including reformers for hydrogen production from various hydrocarbons and potentially from ammonia.

KIER (Korea Institute of Energy Research): As a leading research institution, KIER is actively involved in R&D for advanced hydrogen production and utilization technologies, including high-efficiency ammonia cracking systems and associated infrastructure.

KAPSOM: Focuses on providing solutions for hydrogen production, including systems for ammonia cracking. Their offerings aim to support industrial applications and contribute to the transition to green hydrogen.

AMOGY: A developer of ammonia-to-power solutions, AMOGY integrates ammonia cracking technology with Fuel Cell Technology Market to produce electricity, particularly targeting heavy-duty transportation and marine sectors.

Toyo Engineering: A global engineering firm, Toyo Engineering possesses extensive experience in designing and constructing large-scale chemical plants, including ammonia facilities, and is expanding its expertise to encompass distributed cracking solutions for hydrogen supply.

Recent Developments & Milestones in Distributed Ammonia Cracking System Market

Recent developments in the Distributed Ammonia Cracking System Market underscore a growing momentum towards commercialization and technological refinement:

January 2024: Several research consortia, backed by European grants, announced pilot projects in Northern Europe focused on demonstrating the viability of ammonia cracking for localized Hydrogen Generation Plant Market applications, aiming to de-risk technology deployment.

November 2023: A leading catalyst manufacturer reported a breakthrough in ruthenium-based catalysts, achieving 20% higher activity at lower temperatures, promising reduced energy consumption for distributed cracking systems.

August 2023: Investment funds allocated $50 million towards a startup specializing in modular ammonia cracking units designed for small to medium-scale industrial hydrogen supply, emphasizing scalability and rapid deployment.

June 2023: A collaboration between a major shipping company and an energy technology firm commenced testing of an ammonia-powered tugboat, incorporating an on-board distributed ammonia cracking system to fuel its engines, signifying progress in the Marine Fuel Market.

April 2023: Asian nations, particularly Japan and South Korea, intensified their strategic alliances with Middle Eastern Ammonia Production Market hubs to secure long-term green ammonia supplies, laying the groundwork for future distributed cracking infrastructure.

February 2023: A North American clean energy firm unveiled plans for a network of ammonia bunkering stations equipped with cracking technology, facilitating the use of ammonia as a maritime fuel and fostering a robust supply chain.

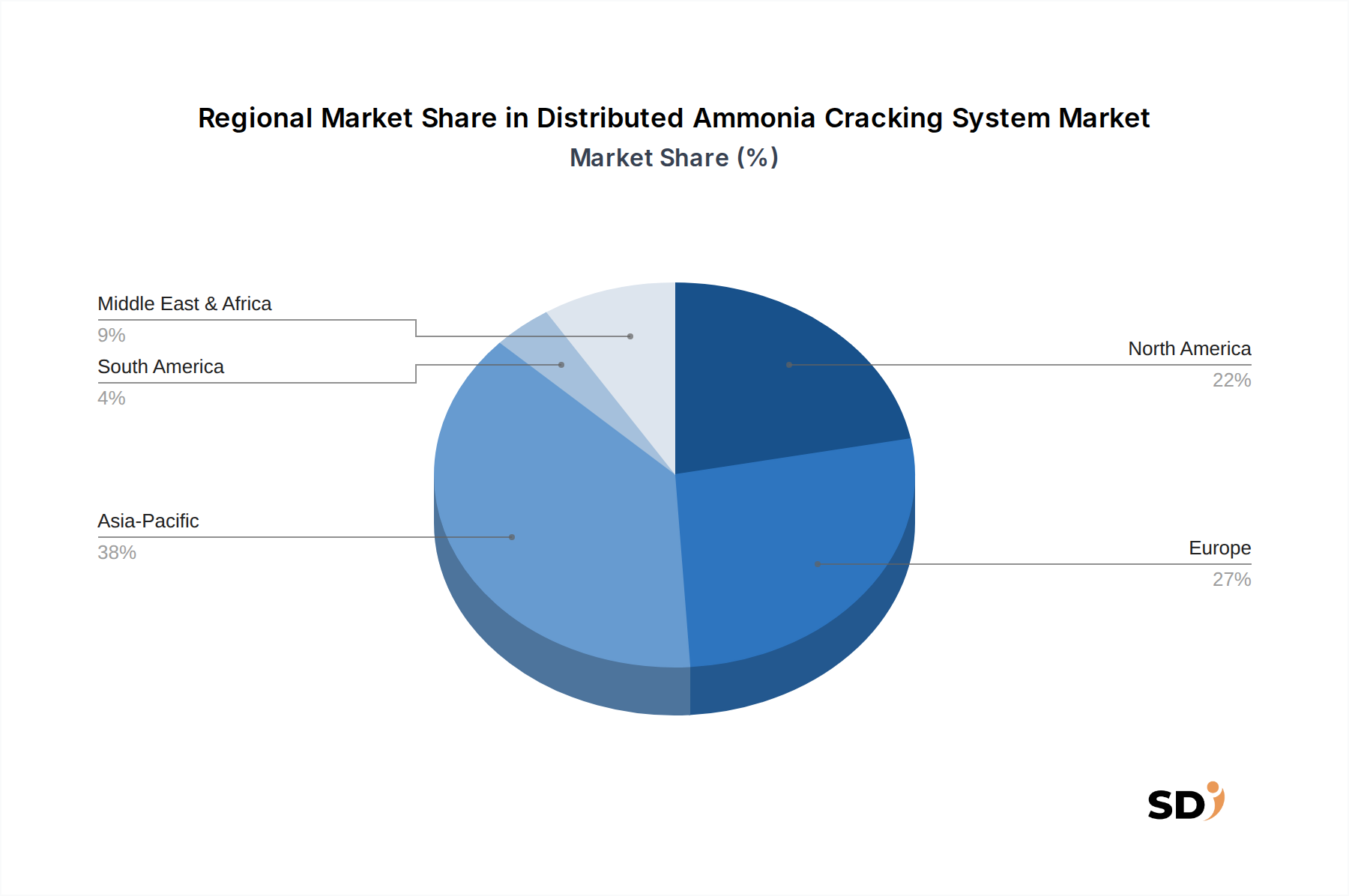

Regional Market Breakdown for Distributed Ammonia Cracking System Market

The global Distributed Ammonia Cracking System Market exhibits diverse growth patterns and drivers across key regions, reflecting varying energy policies, industrial landscapes, and hydrogen economy development stages.

Asia Pacific is anticipated to be the fastest-growing region, registering a projected CAGR of over 15% through 2034. This growth is fueled by massive industrialization, high energy demand, and ambitious national hydrogen strategies, particularly in countries like China, India, and Japan. These nations are heavily investing in hydrogen production and infrastructure, viewing distributed ammonia cracking as a crucial pathway to diversify energy sources and reduce reliance on fossil fuels. The robust Hydrogen Generation Plant Market in the region is a key demand driver.

Europe holds a significant revenue share, driven by aggressive decarbonization targets and strong regulatory support for Green Hydrogen Market initiatives. Countries like Germany, France, and the UK are pioneering demonstration projects and investing in the entire hydrogen value chain, including ammonia imports and distributed cracking. The region's focus on sustainable transport and industrial feedstock conversion provides a strong impetus for market development, with a projected CAGR of approximately 12%.

North America is a mature yet rapidly evolving market, characterized by substantial R&D investments and a focus on energy independence. The United States and Canada are exploring diverse pathways to hydrogen production, with distributed ammonia cracking gaining traction for applications in heavy-duty transport, industrial processes, and grid balancing. Government incentives and corporate commitments to net-zero emissions are expected to drive consistent growth, with a CAGR around 11.5%.

The Middle East & Africa region is emerging as a critical player, primarily due to its potential as a hub for large-scale Ammonia Production Market (especially green ammonia) for export. Countries in the GCC are leveraging abundant renewable energy resources to produce green ammonia, which will be transported globally and cracked at demand centers. While local adoption of distributed cracking is still developing, the region's role as a future supplier significantly influences global market dynamics, showing strong nascent growth.

Export, Trade Flow & Tariff Impact on Distributed Ammonia Cracking System Market

The Distributed Ammonia Cracking System Market is profoundly influenced by global trade flows, particularly concerning ammonia as a hydrogen carrier. Major trade corridors are emerging from regions with abundant renewable energy resources (e.g., Middle East, Australia, South America) to demand centers in Asia and Europe, where hydrogen consumption is high. Leading exporting nations for green and blue ammonia, such as Saudi Arabia, Australia, and the United States, are establishing partnerships to supply importing nations like Japan, South Korea, and Germany.

Tariff and non-tariff barriers, while currently nascent specifically for hydrogen-ready ammonia cracking components, are becoming increasingly relevant as the hydrogen economy matures. Carbon border adjustment mechanisms (CBAMs) proposed by regions like the EU could incentivize the use of low-carbon Ammonia Production Market and subsequent cracking technologies. Conversely, overly protective tariffs on advanced reactor components or catalysts could hinder the cost-effective global deployment of distributed cracking systems. For instance, trade agreements facilitating the cross-border movement of Catalyst Reactor Market components or specialized membranes could accelerate market growth. Recent geopolitical events have also highlighted the imperative for energy security, prompting regions to diversify their hydrogen supply chains, sometimes through trade routes that bypass traditional energy suppliers, impacting the strategic siting of distributed cracking facilities and the associated trade in ammonia.

Pricing Dynamics & Margin Pressure in Distributed Ammonia Cracking System Market

The pricing dynamics within the Distributed Ammonia Cracking System Market are complex, influenced by technology maturity, scale of deployment, and the broader hydrogen market. Average Selling Price (ASP) trends for cracking systems are initially high, reflecting the novelty and custom engineering involved in early installations. However, as modularity increases and manufacturing scales, ASPs are expected to gradually decline, driven by economies of scale and competitive pressures.

Margin structures across the value chain are currently robust for technology developers and specialized engineering firms, given the high value-add of their proprietary designs and catalysts. However, as the market matures, increased competition and standardization will likely exert downward pressure on these margins. Key cost levers include the capital expenditure (CapEx) for the reactor system itself, which can range from a few hundred thousand to several million dollars depending on capacity, and the operational expenditure (OpEx), predominantly influenced by energy input and Catalyst Material Market costs. Energy consumption for the endothermic cracking reaction is a significant OpEx component, and innovations aimed at heat integration or lower operating temperatures directly impact system economics.

Competitive intensity from alternative on-site hydrogen production methods, such as natural gas reforming with carbon capture or direct electrolysis, also affects pricing power. Companies offering integrated solutions that combine cracking with hydrogen purification or Fuel Cell Technology Market applications may command higher ASPs due to added value. The price volatility of ammonia, often linked to natural gas prices for conventional ammonia, also introduces a variable cost component. For green ammonia, the cost of renewable electricity is the primary driver. Navigating these cost levers and pricing pressures will be critical for sustaining profitability in the evolving Distributed Ammonia Cracking System Market.

Distributed Ammonia Cracking System Segmentation

1. Application

1.1. Ship

1.2. Automobile

1.3. Hydrogen Generation Plant

1.4. Others

2. Types

2.1. Catalyst Reactor

2.2. Membrane Reactor

Distributed Ammonia Cracking System Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Distributed Ammonia Cracking System REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 13.7% from 2020-2034

Segmentation

By Application

Ship

Automobile

Hydrogen Generation Plant

Others

By Types

Catalyst Reactor

Membrane Reactor

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Ship

5.1.2. Automobile

5.1.3. Hydrogen Generation Plant

5.1.4. Others

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Catalyst Reactor

5.2.2. Membrane Reactor

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Ship

6.1.2. Automobile

6.1.3. Hydrogen Generation Plant

6.1.4. Others

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Catalyst Reactor

6.2.2. Membrane Reactor

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Ship

7.1.2. Automobile

7.1.3. Hydrogen Generation Plant

7.1.4. Others

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Catalyst Reactor

7.2.2. Membrane Reactor

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Ship

8.1.2. Automobile

8.1.3. Hydrogen Generation Plant

8.1.4. Others

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Catalyst Reactor

8.2.2. Membrane Reactor

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Ship

9.1.2. Automobile

9.1.3. Hydrogen Generation Plant

9.1.4. Others

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Catalyst Reactor

9.2.2. Membrane Reactor

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Ship

10.1.2. Automobile

10.1.3. Hydrogen Generation Plant

10.1.4. Others

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Catalyst Reactor

10.2.2. Membrane Reactor

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Reaction Engines

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. AFC Energy

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. H2SITE

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Johnson Matthey

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Topsoe

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Metacon

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. KIER

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. KAPSOM

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. AMOGY

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Toyo Engineering

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (million), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (million), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (million), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (million), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (million), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (million), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (million), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (million), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (million), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (million), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (million), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Revenue million Forecast, by Types 2020 & 2033

Table 3: Revenue million Forecast, by Region 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Types 2020 & 2033

Table 6: Revenue million Forecast, by Country 2020 & 2033

Table 7: Revenue (million) Forecast, by Application 2020 & 2033

Table 8: Revenue (million) Forecast, by Application 2020 & 2033

Table 9: Revenue (million) Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Application 2020 & 2033

Table 11: Revenue million Forecast, by Types 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Types 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Revenue (million) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue million Forecast, by Application 2020 & 2033

Table 29: Revenue million Forecast, by Types 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue million Forecast, by Application 2020 & 2033

Table 38: Revenue million Forecast, by Types 2020 & 2033

Table 39: Revenue million Forecast, by Country 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is designed to capture granular, real-time insights directly from key stakeholders across the value chain of the distributed ammonia cracking system market. This comprehensive approach ensures that our analysis is grounded in industry realities and future projections from those actively shaping the market.

Approach: We employ a structured interview process, engaging with industry experts through in-depth discussions, telephone interviews, and virtual consultations. This iterative process allows for validation of initial hypotheses and exploration of emergent trends.

Research Split: Primary research constitutes approximately 75% of our total research effort, focusing on qualitative and quantitative data collection to inform market sizing, competitive analysis, and strategic recommendations.

Targeted Companies for Interviews: Our outreach targets a diverse range of organizations critical to the distributed ammonia cracking ecosystem:

Marine & Automotive OEM R&D Divisions (e.g., departments exploring alternative fuel systems for ships and automobiles)

Industrial Gas & Chemical Suppliers (e.g., major players in ammonia production and distribution logistics)

Key Stakeholder Job Titles: Interviews are conducted with individuals holding strategic and technical roles, ensuring deep dives into market dynamics:

Director of Hydrogen Technology & Innovation

Chief Product Officer, Distributed Energy Systems

Head of R&D, Catalysis & Materials Science

VP of Strategic Partnerships, Alternative Fuels

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Director of Hydrogen Technology & Innovation

30%

Chief Product Officer, Distributed Energy Systems

25%

Head of R&D, Catalysis & Materials Science

25%

VP of Strategic Partnerships, Alternative Fuels

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Ammonia Cracking System Manufacturers

30%

Advanced Material & Catalyst Developers

20%

Hydrogen Fueling Infrastructure Providers

15%

Marine & Automotive OEM R&D Divisions

25%

Industrial Gas & Chemical Suppliers

10%

Secondary Research & Industry Benchmarking

Secondary research forms the foundational layer of our market analysis, providing a broad understanding of the market landscape, technological advancements, regulatory frameworks, and macroeconomic factors. This phase constitutes approximately 25% of our total research effort.

Data Sources: We meticulously gather data from a diverse array of credible and authoritative sources:

Government Publications & Reports: Official documents from energy ministries, environmental agencies, and national statistics offices globally, such as the U.S. Department of Energy, European Commission, and national hydrogen strategies.

Trade Associations & Industry Bodies: Reports, whitepapers, and statistical data from recognized industry groups that provide market-specific insights. Examples include:

Company Filings & Financial Databases: Leveraging robust financial intelligence platforms for public company data, annual reports, investor presentations, and competitive intelligence. Our standard resources include: Bloomberg, Factiva, Hoovers, and PitchBook.

Academic Research & Scientific Journals: Peer-reviewed publications offering insights into material science, chemical engineering, and advanced reactor design pertinent to ammonia cracking.

Exclusion of Market Research Websites: To maintain the highest integrity and originality of our data, we explicitly exclude data from other market research websites.

Up-to-Date Information: All secondary data and market intelligence are continually updated up to the date of the report purchase, ensuring the most current market view.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies integrate both top-down and bottom-up approaches, triangulated across multiple data points to ensure robust and reliable estimates.

Bottom-Up Approach: This method involves estimating market size by aggregating data from granular segments. Key variables utilized for this approach include:

Annual production capacity (in kg H2/day equivalent) of distributed ammonia crackers by type (catalyst/membrane).

Average selling price (ASP) per unit capacity of ammonia cracking systems across different applications (ship, automobile, hydrogen generation plant).

Number of ammonia-fueled vessels or heavy-duty vehicles projected for deployment, coupled with their specific hydrogen demand.

Top-Down Approach: This involves assessing the overall market from a macro perspective, utilizing global and regional hydrogen demand projections, and then segmenting down to the distributed ammonia cracking market based on adoption rates, technological feasibility, and policy support.

Multi-Level Data Triangulation: Our estimates are rigorously cross-referenced using data from primary interviews, diverse secondary sources, and proprietary statistical models. This triangulation minimizes potential biases and maximizes the accuracy of our forecasts across applications (Ship, Automobile, Hydrogen Generation Plant, Others), types (Catalyst Reactor, Membrane Reactor), and global regions.

Data Accuracy & Quality Check

Ensuring the highest level of data integrity and reliability is paramount to our research process.

Accuracy Guarantee: We guarantee an estimated data accuracy level of 85-90% for our market figures and forecasts.

Validation: All data points, assumptions, and models undergo a stringent validation process by senior analysts and domain experts. This involves comparing findings against historical trends, industry benchmarks, and expert consensus.

Iterative Refinement: Our methodology includes an iterative refinement loop where initial findings from secondary research are validated and enriched through primary interviews. Any discrepancies are investigated and reconciled through further data collection or expert consultation.

Market Dynamics Integration: The model continuously incorporates dynamic market factors such as technological advancements, regulatory changes, competitive landscape shifts, and evolving end-user preferences to provide a forward-looking and adaptive market view.

Frequently Asked Questions

1. What are the primary barriers to entry in the Distributed Ammonia Cracking System market?

Significant R&D investment and specialized catalyst/membrane technologies form key entry barriers. Companies like Johnson Matthey and Topsoe leverage established expertise, protecting market positions through proprietary innovations.

2. How do international trade flows impact the Distributed Ammonia Cracking System market?

International trade of Distributed Ammonia Cracking Systems is primarily influenced by regional hydrogen demand and manufacturing capabilities. Countries with advanced industrial bases, like Germany and Japan, often export specialized components to regions adopting green hydrogen infrastructure.

3. What raw material and supply chain considerations affect ammonia cracking systems?

The primary operational 'raw material' is ammonia itself, sourced globally. For system manufacturing, critical components include specialized catalysts, advanced alloys for reactors, and membrane materials, requiring robust supply chain management.

4. Which disruptive technologies could impact the Distributed Ammonia Cracking System sector?

Direct hydrogen storage solutions, such as compressed or liquid hydrogen, and alternative hydrogen carriers pose competitive alternatives. Advancements in direct ammonia fuel cells that bypass cracking also present an emerging substitute technology.

5. Who are the leading companies in the Distributed Ammonia Cracking System market?

Key players shaping the Distributed Ammonia Cracking System market include Johnson Matthey, Topsoe, H2SITE, and AMOGY. Competition focuses on system efficiency, scalability for various applications like hydrogen generation plants, and cost reduction.

6. Why is the Asia-Pacific region dominant in the Distributed Ammonia Cracking System market?

Asia-Pacific is projected to be the dominant region, driven by extensive industrialization and significant green hydrogen investments. Countries like China and Japan are making substantial progress in adopting advanced hydrogen technologies and infrastructure development.