Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Dipping Sonar by Application (Military and Defense, Others), by Types (Low Frequency Sonar, Mid-frequency Sonar), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 16, 2026|Base Year : 2025|Pages : 74

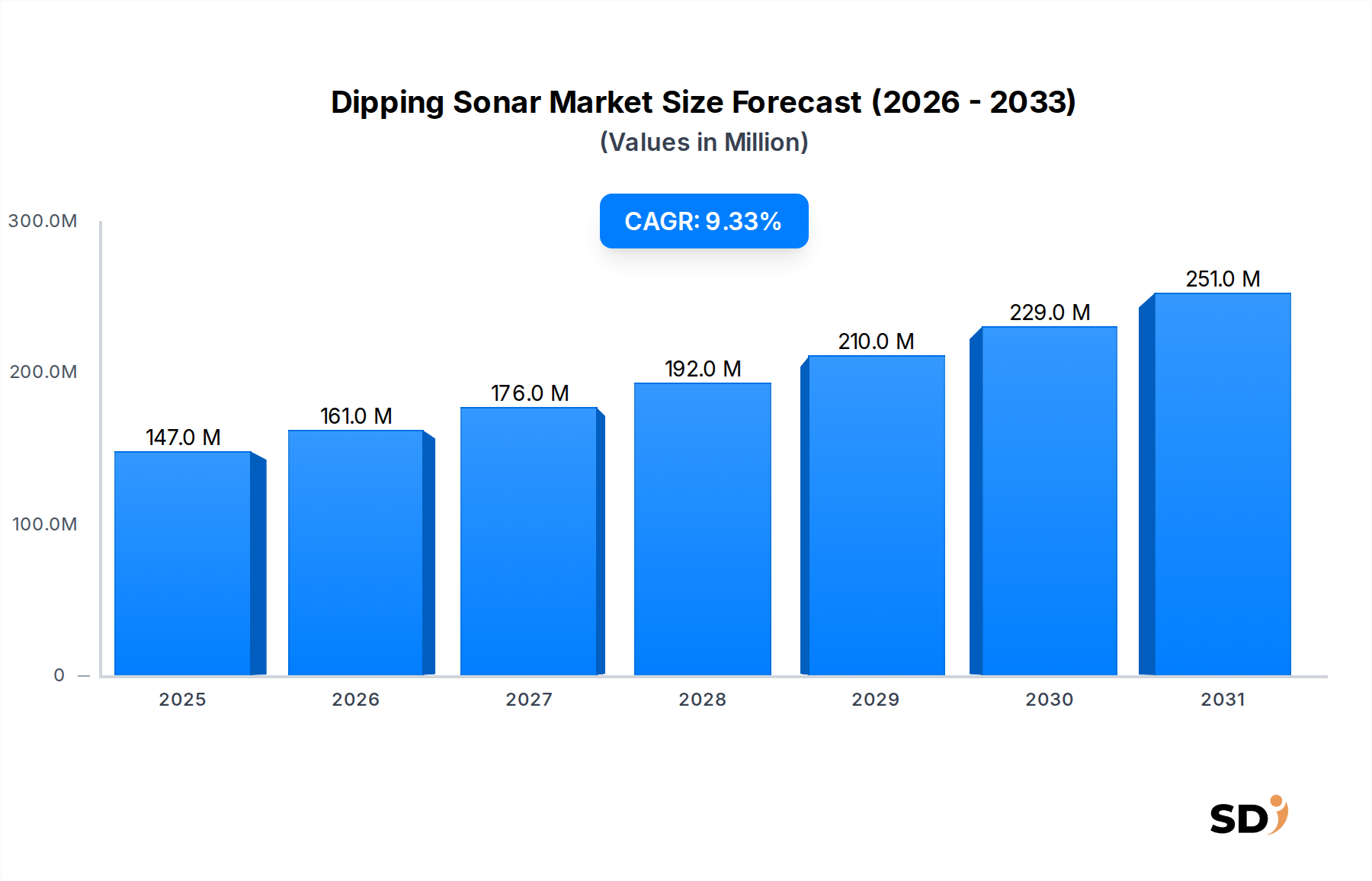

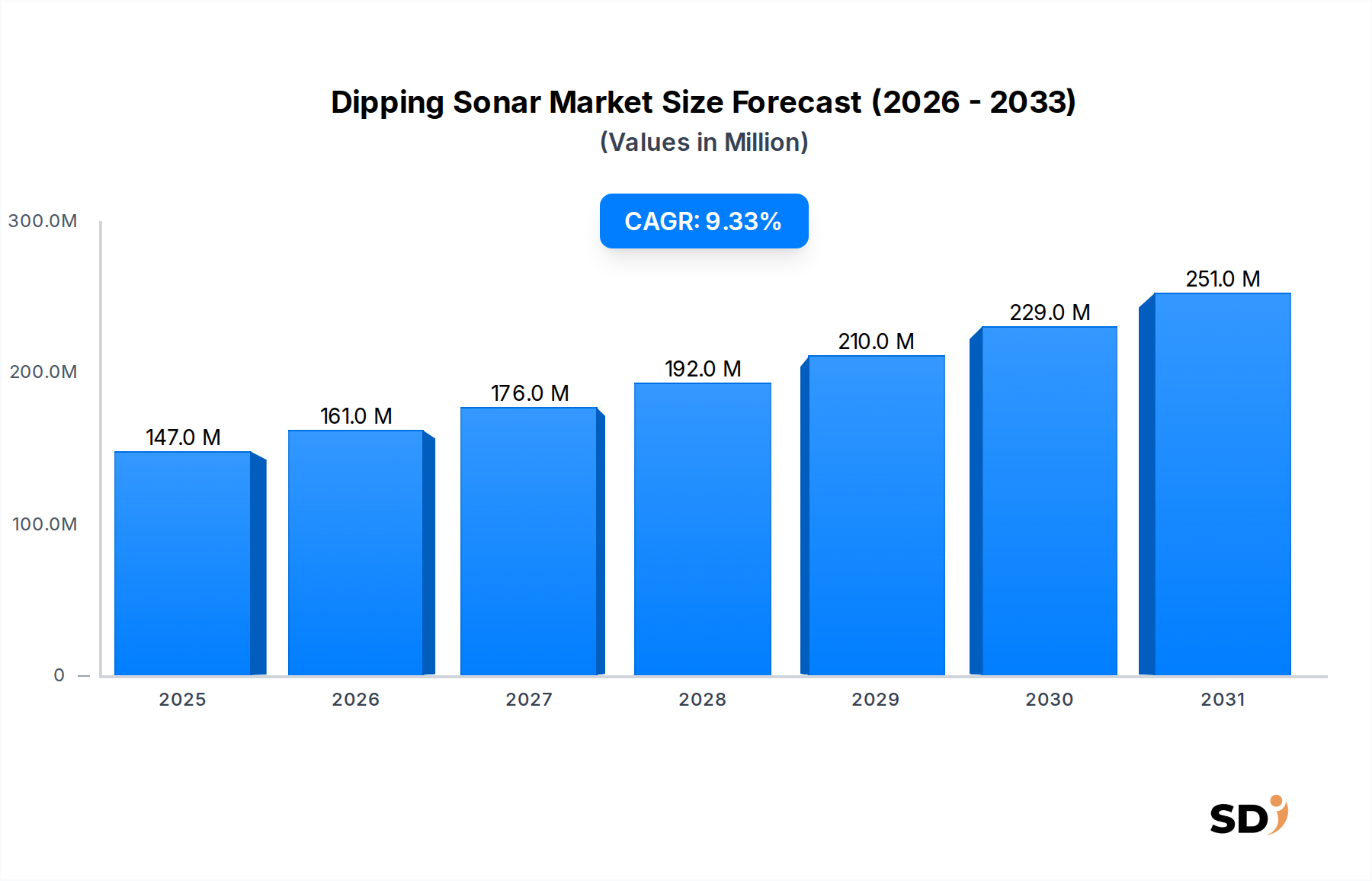

The Dipping Sonar Market is poised for robust expansion, driven primarily by escalating global naval modernization programs and the imperative for enhanced Anti-Submarine Warfare (ASW) capabilities. Valued at an estimated $147 million in 2026, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.3%, reaching approximately $249.46 million by 2032. This trajectory is underpinned by geopolitical instabilities, fostering increased defense expenditures among major and emerging naval powers. The inherent mobility and rapid deployment capabilities of dipping sonars make them indispensable assets for intelligence, surveillance, and reconnaissance (ISR) missions, particularly in contested littoral zones and deep-sea environments.

Dipping Sonar Market Size (In Million)

300.0M

200.0M

100.0M

0

147.0 M

2025

161.0 M

2026

176.0 M

2027

192.0 M

2028

210.0 M

2029

229.0 M

2030

251.0 M

2031

The demand landscape is significantly shaped by the continuous innovation in acoustic processing and transducer technologies, which are enhancing detection ranges, target classification accuracy, and operational endurance. The integration of dipping sonar systems with advanced platforms, including naval helicopters, Uncrewed Surface Vessels (USVs), and Uncrewed Underwater Vehicles (UUVs), is a pivotal demand driver. These systems offer critical advantages in time-sensitive operations, such as search and rescue, mine countermeasures (MCM), and rapid environmental assessment. Macroeconomic tailwinds include increasing investment in defense research and development, particularly in advanced materials science for transducer design and Artificial Intelligence (AI) for real-time data analysis. The expanding global Military and Defense Electronics Market serves as a foundational growth accelerator for dipping sonar systems.

Further market impetus stems from the growing adoption of modular and open-architecture designs, facilitating easier integration and upgrades, thereby extending the operational lifespan and cost-effectiveness of these sophisticated systems. The outlook for the Dipping Sonar Market remains highly positive, with significant opportunities emerging from technological convergence, platform diversification, and the strategic importance of underwater domain awareness. The market is also benefiting from developments in the Acoustic Sensor Market, leading to more sensitive and versatile sonar arrays.

Military and Defense Application Dominance in Dipping Sonar Market

The Military and Defense segment unequivocally represents the largest revenue share within the Dipping Sonar Market, a dominance rooted in its critical application across various naval operations. Dipping sonars are fundamental tools in Anti-Submarine Warfare (ASW), providing airborne and surface platforms with the capability to detect, track, and classify subsurface threats, including conventional and nuclear submarines. The ongoing expansion and modernization of submarine fleets globally, particularly by nations in the Asia-Pacific region and the heightened naval activities in geopolitical hotspots, directly fuel the demand for advanced ASW solutions. Consequently, defense budgets allocated for such strategic capabilities remain substantial, ensuring a consistent procurement pipeline for dipping sonar systems. For instance, global defense expenditure surged by 9.0% in 2023, with a significant portion directed towards naval assets and underwater domain awareness technologies.

Within this military context, both Low Frequency Sonar Market and Mid-frequency Sonar Market technologies play distinct yet complementary roles. Low-frequency systems are preferred for long-range detection in deep ocean environments, owing to their ability to propagate over greater distances with less attenuation. Conversely, mid-frequency sonars offer superior resolution and classification capabilities, making them ideal for target localization and detailed reconnaissance, especially in challenging coastal and shallow-water conditions. The convergence of these capabilities within multi-frequency dipping sonar systems is a growing trend, offering operators greater operational flexibility. Major defense contractors, including L3Harris Technologies and Thales Group, are key players in this segment, leveraging decades of expertise in integrating these complex systems onto diverse platforms.

The demand for dipping sonars is also expanding beyond traditional helicopter deployments to include Uncrewed Surface Vessels (USVs) and Uncrewed Underwater Vehicles (UUVs), thereby merging with the rapidly evolving Underwater Robotics Market. These autonomous platforms offer prolonged endurance, reduced risk to personnel, and the ability to operate in contested zones, making them highly attractive for future naval strategies. The military and defense segment's dominance is expected to consolidate further, driven by continued technological advancements, such as enhanced signal processing, AI-driven data interpretation, and miniaturization. The Active Sonar Systems Market remains central to these applications, providing the necessary energy for detection, while advancements in the Passive Sonar Systems Market are also enhancing the overall operational picture through silent listening capabilities. This sustained investment ensures its position as the primary revenue generator within the Dipping Sonar Market.

Key Market Drivers in Dipping Sonar Market

The Dipping Sonar Market is propelled by several critical drivers, each underscored by quantifiable trends and strategic imperatives.

Escalating Naval Modernization Programs: Global naval powers are engaged in extensive modernization efforts to counter evolving maritime threats. Nations such as China, India, and the United States are significantly expanding and upgrading their naval fleets, including frigates, destroyers, and maritime patrol aircraft, each requiring advanced ASW capabilities. For example, the U.S. Navy's fiscal year 2024 budget requested over $29 billion for shipbuilding and existing ship upgrades, a portion of which is directly allocated to enhanced sonar systems. This trend is a primary catalyst for the Marine Technology Market generally, and specifically for advanced ASW solutions.

Heightened Anti-Submarine Warfare (ASW) Imperatives: The proliferation of quieter and more advanced submarines by various state and non-state actors has amplified the need for sophisticated ASW technologies. Dipping sonars provide a crucial mobile and rapid-response ASW capability, essential for protecting high-value naval assets and sea lanes. The number of active submarines globally is projected to exceed 500 units by 2030, necessitating a proportional increase in detection and tracking capabilities. This persistent threat environment is a foundational driver.

Integration with Uncrewed Platforms: The rapid development and deployment of Uncrewed Surface Vessels (USVs) and Uncrewed Underwater Vehicles (UUVs) are creating new demand vectors for compact, high-performance dipping sonar systems. These platforms extend the reach and endurance of ASW operations while reducing human risk. The global Underwater Robotics Market is forecast to grow at a CAGR of 15.8% from 2023 to 2030, with dipping sonar integration being a key enabling technology for their ASW roles. Miniaturized dipping sonars are crucial for these emerging platforms.

Advancements in Transducer and Signal Processing Technologies: Continuous innovation in materials science, particularly in the Piezoelectric Materials Market, and digital signal processing, has led to significant improvements in sonar performance. New transducer designs offer greater sensitivity and bandwidth, while AI/ML algorithms enhance target classification and reduce false alarms. This technological push is allowing dipping sonars to operate effectively in increasingly complex acoustic environments, further solidifying their strategic value.

Competitive Ecosystem of Dipping Sonar Market

The Dipping Sonar Market is characterized by a concentrated competitive landscape dominated by a few major defense contractors and specialized technology firms. These entities leverage extensive R&D capabilities, long-standing relationships with defense ministries, and comprehensive product portfolios.

L3Harris Technologies: A leading provider of advanced defense and commercial technologies, L3Harris offers a range of dipping sonar solutions known for their robust performance and integration capabilities, particularly for naval helicopters and maritime patrol aircraft, focusing on advanced Anti-Submarine Warfare (ASW) and Intelligence, Surveillance, and Reconnaissance (ISR) applications.

Thales Group: A global technology leader for the aerospace, defense, security, and transportation markets, Thales provides state-of-the-art dipping sonar systems that are integral to numerous international naval programs. Their offerings often feature multi-frequency capabilities and advanced signal processing to enhance detection and classification in diverse operational environments.

Armelsan: A Turkish defense technology company, Armelsan specializes in underwater acoustic systems, including dipping sonars. The company is actively developing indigenous solutions to meet the growing demands of the Turkish Navy and other regional defense forces, focusing on competitive performance and localized support.

SAES: Sociedad Anónima de Electrónica Submarina (SAES) is a Spanish company with extensive expertise in underwater acoustics and sonars. They provide advanced dipping sonar systems for both military and civilian applications, with a strong emphasis on acoustic signal intelligence, mine countermeasures, and environmental monitoring solutions.

Recent Developments & Milestones in Dipping Sonar Market

Recent activities within the Dipping Sonar Market underscore its dynamic nature, driven by technological advancements and evolving defense requirements.

March 2024: L3Harris Technologies announced the receipt of a significant contract to supply next-generation dipping sonar systems for a major international naval helicopter program, emphasizing enhanced deep-water detection and active target classification capabilities. This further solidifies the position of Active Sonar Systems Market players.

January 2024: Thales Group unveiled a new compact dipping sonar prototype specifically designed for integration with Uncrewed Surface Vessels (USVs), aiming to expand the operational envelope of autonomous platforms in ASW and ISR missions. This innovation directly impacts the Underwater Robotics Market.

November 2023: Armelsan successfully completed extensive sea trials for its domestically developed dipping sonar system, achieving significant milestones in range and accuracy, signaling increased self-reliance in naval defense technology for its target markets.

August 2023: SAES announced a strategic partnership with a leading European research institute to co-develop advanced signal processing algorithms for existing dipping sonar systems, focusing on improving the detection of ultra-quiet submarines and enhancing multi-static sonar operations.

June 2023: A major defense procurement agency issued a global Request for Information (RFI) for next-generation Acoustic Sensor Market technologies to upgrade existing helicopter-borne dipping sonar fleets, highlighting the ongoing demand for performance enhancements.

April 2023: Several defense primes explored new manufacturing techniques for sonar transducers using novel compounds from the Piezoelectric Materials Market, aiming to improve acoustic sensitivity and power efficiency for both Low Frequency Sonar Market and Mid-frequency Sonar Market applications.

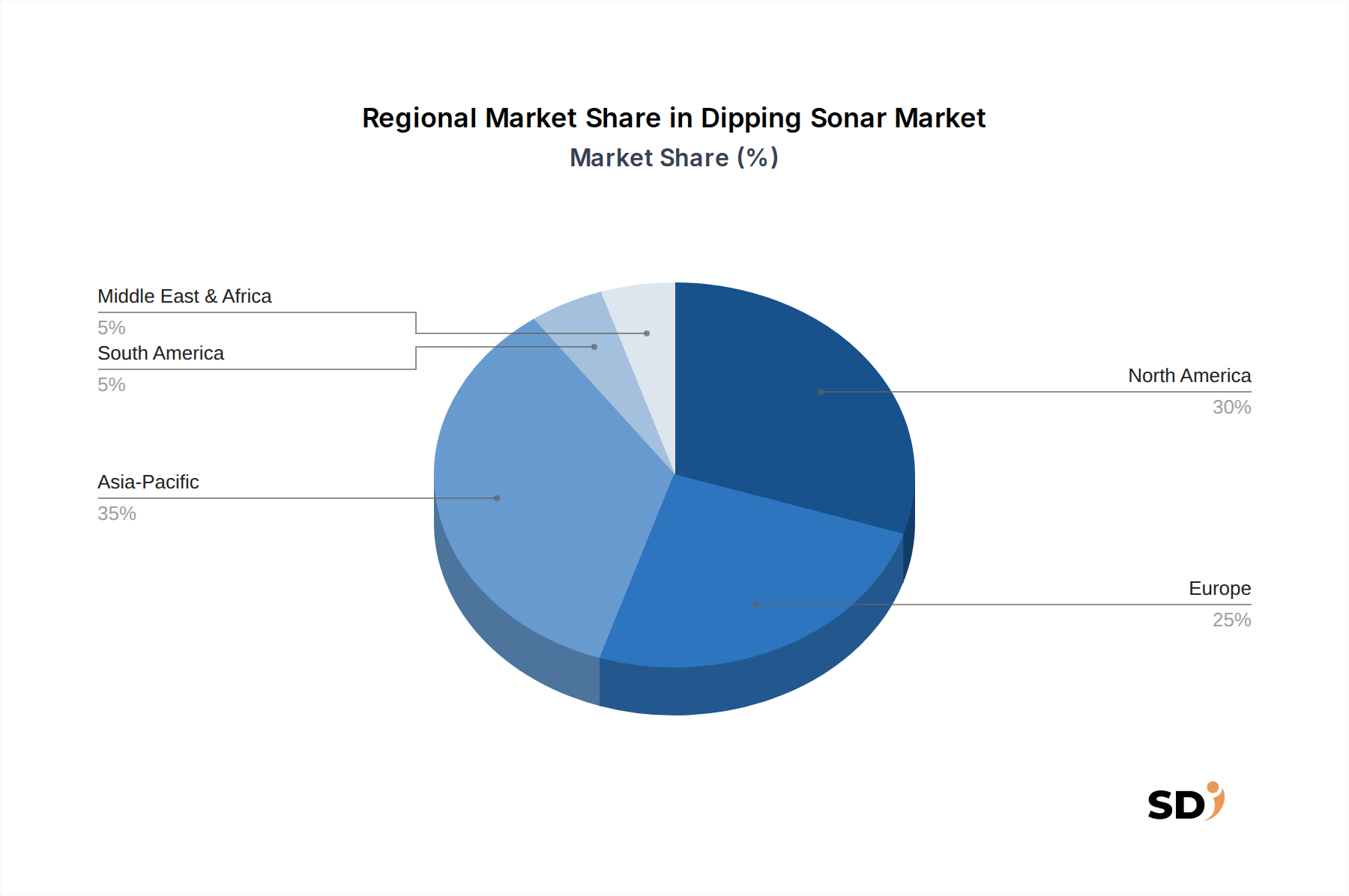

Regional Market Breakdown for Dipping Sonar Market

The Dipping Sonar Market exhibits distinct regional dynamics, influenced by geopolitical factors, defense spending priorities, and technological adoption rates.

North America holds the largest revenue share in the Dipping Sonar Market, primarily driven by significant defense budgets in the United States and Canada. The region is a hub for advanced research and development in ASW technologies, with continuous investment in upgrading existing fleets and integrating new dipping sonar systems onto state-of-the-art platforms. The primary demand driver is the imperative for maintaining technological superiority in naval warfare and enhancing homeland security, alongside substantial R&D expenditure. The robust Military and Defense Electronics Market in the U.S. also contributes significantly.

Asia Pacific is identified as the fastest-growing region, experiencing a robust CAGR that surpasses the global average. This growth is propelled by escalating naval arms races, territorial disputes, and widespread naval modernization programs across countries like China, India, Japan, and South Korea. These nations are heavily investing in expanding their submarine and surface fleets, directly increasing the demand for advanced dipping sonar systems to bolster their ASW capabilities. The region's focus on maritime domain awareness in contested waters is a key demand driver.

Europe represents a mature but steadily growing market. Countries such as the UK, France, Germany, and Italy are engaged in naval fleet upgrades and collaborative defense initiatives, driving demand for modern dipping sonars. Geopolitical tensions, particularly in Eastern Europe, necessitate sustained investment in ASW. The region benefits from a strong domestic defense industrial base and collaborative R&D efforts within the Marine Technology Market, aiming to counter emerging threats and support NATO operations.

Middle East & Africa shows nascent but increasing interest in dipping sonar systems. Growing defense budgets in nations like Saudi Arabia, UAE, Turkey, and Israel, coupled with regional security concerns, are fostering procurement of advanced naval technologies. The demand is primarily driven by the need for coastal defense, maritime security, and limited ASW capabilities against potential regional threats. This region relies heavily on imports from established global defense contractors.

Pricing Dynamics & Margin Pressure in Dipping Sonar Market

The pricing dynamics within the Dipping Sonar Market are complex, characterized by high average selling prices (ASPs) and significant margin pressures shaped by specialized technology, extensive R&D, and the unique defense procurement lifecycle. ASPs for advanced dipping sonar systems typically range from several million to tens of millions of dollars per unit, depending on capabilities, integration requirements, and customization. These high prices reflect the substantial investment in fundamental research, sophisticated materials from the Piezoelectric Materials Market, precision engineering, and rigorous testing required to meet stringent military specifications. The inherent complexity of underwater acoustics and the need for robust performance in challenging marine environments also contribute to elevated costs.

Margin structures across the value chain are generally healthy for prime contractors, given the oligopolistic nature of the market. However, these margins are constantly under pressure from rising raw material costs, particularly for rare earth elements and specialized alloys used in transducers and electronic components. The Acoustic Sensor Market segment, which supplies critical components, also faces its own supply chain and cost pressures. Intense competitive bidding during defense procurement cycles, coupled with long lead times and high initial capital expenditures for R&D, can compress margins for even the largest players. Furthermore, customers increasingly demand modular, open-architecture systems that reduce through-life costs and facilitate future upgrades, adding pressure on manufacturers to innovate while controlling expenses.

Key cost levers include the cost of specialized labor (acoustic engineers, software developers), intellectual property licensing, and the highly regulated certification processes. The shift towards smaller, more compact dipping sonars for Uncrewed Surface Vessels (USVs) and Uncrewed Underwater Vehicles (UUVs) may introduce new competitive tiers and potentially slightly lower ASPs for certain product categories, but the overall high-value nature of the market is expected to persist due to the strategic importance and performance demands of Military and Defense Electronics Market applications. This sustained demand keeps the Active Sonar Systems Market and Passive Sonar Systems Market highly valuable.

Investment & Funding Activity in Dipping Sonar Market

Investment and funding activity within the Dipping Sonar Market has primarily revolved around strategic acquisitions, government-backed R&D grants, and partnerships aimed at enhancing capabilities, particularly for Anti-Submarine Warfare (ASW) and autonomous platforms. Over the past 2-3 years, M&A activity has largely focused on consolidation among prime defense contractors seeking to expand their technology portfolios or market reach. For instance, larger players often acquire specialized Acoustic Sensor Market or signal processing firms to integrate cutting-edge components and software into their existing sonar offerings, strengthening their position in the Marine Technology Market.

Venture funding, while less prevalent than in other tech sectors, is increasingly directed towards startups pioneering advanced data analytics, Artificial Intelligence (AI), and Machine Learning (ML) solutions for sonar data interpretation. These investments aim to reduce operator workload, improve target classification accuracy, and enable autonomous decision-making for platforms operating in the Underwater Robotics Market. Companies developing novel Piezoelectric Materials Market for next-generation transducers, offering improved efficiency and bandwidth for both Low Frequency Sonar Market and Mid-frequency Sonar Market applications, also attract targeted funding.

Strategic partnerships are common, often involving collaboration between defense contractors, academic institutions, and government research labs. These alliances typically focus on specific R&D challenges, such as developing quieter sonar systems, enhancing multi-static sonar capabilities, or integrating dipping sonars with uncrewed systems for extended maritime surveillance. Significant capital is being channeled into sub-segments that promise to deliver enhanced stealth detection, real-time environmental adaptive processing, and miniaturization for diverse platform integration, reflecting a concerted effort to maintain technological superiority in the Military and Defense Electronics Market.

Dipping Sonar Segmentation

1. Application

1.1. Military and Defense

1.2. Others

2. Types

2.1. Low Frequency Sonar

2.2. Mid-frequency Sonar

Dipping Sonar Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Dipping Sonar REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 9.3% from 2020-2034

Segmentation

By Application

Military and Defense

Others

By Types

Low Frequency Sonar

Mid-frequency Sonar

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Military and Defense

5.1.2. Others

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Low Frequency Sonar

5.2.2. Mid-frequency Sonar

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Military and Defense

6.1.2. Others

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Low Frequency Sonar

6.2.2. Mid-frequency Sonar

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Military and Defense

7.1.2. Others

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Low Frequency Sonar

7.2.2. Mid-frequency Sonar

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Military and Defense

8.1.2. Others

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Low Frequency Sonar

8.2.2. Mid-frequency Sonar

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Military and Defense

9.1.2. Others

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Low Frequency Sonar

9.2.2. Mid-frequency Sonar

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Military and Defense

10.1.2. Others

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Low Frequency Sonar

10.2.2. Mid-frequency Sonar

11. Competitive Analysis

11.1. Company Profiles

11.1.1. L3Harris Technologies

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Thales Group

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Armelsan

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. SAES

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (million), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (million), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (million), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (million), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (million), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (million), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (million), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (million), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (million), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (million), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (million), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Revenue million Forecast, by Types 2020 & 2033

Table 3: Revenue million Forecast, by Region 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Types 2020 & 2033

Table 6: Revenue million Forecast, by Country 2020 & 2033

Table 7: Revenue (million) Forecast, by Application 2020 & 2033

Table 8: Revenue (million) Forecast, by Application 2020 & 2033

Table 9: Revenue (million) Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Application 2020 & 2033

Table 11: Revenue million Forecast, by Types 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Types 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Revenue (million) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue million Forecast, by Application 2020 & 2033

Table 29: Revenue million Forecast, by Types 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue million Forecast, by Application 2020 & 2033

Table 38: Revenue million Forecast, by Types 2020 & 2033

Table 39: Revenue million Forecast, by Country 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research efforts are paramount, constituting approximately 75% of our total research methodology. This direct engagement ensures the collection of real-time, granular data, capturing nuanced market dynamics, emerging trends, and stakeholder sentiments crucial for the "Dipping Sonar" market. We conduct extensive interviews with key opinion leaders (KOLs) across the value chain.

Company Types Interviewed:

Dipping Sonar System Original Equipment Manufacturers (OEMs)

Governmental and Private Maritime R&D Institutions

Naval Vessel Maintenance & Upgrade Service Providers

Key Stakeholder Job Titles:

Director of Naval Systems Procurement (Military & Defense)

Chief Engineer, Anti-Submarine Warfare (ASW) Systems

Program Manager, Maritime Surveillance Technologies

Head of Acoustic Research & Development

Our interviews are typically conducted via telephone or virtual meetings, utilizing a structured questionnaire designed to elicit qualitative insights and validate quantitative findings. Each report is updated up to the date of purchase, ensuring our primary data reflects the most current market realities.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Director of Naval Systems Procurement (Military & Defense)

30%

Chief Engineer, Anti-Submarine Warfare (ASW) Systems

25%

Program Manager, Maritime Surveillance Technologies

25%

Head of Acoustic Research & Development

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Dipping Sonar System Original Equipment Manufacturers (OEMs)

Governmental and Private Maritime R&D Institutions

10%

Naval Vessel Maintenance & Upgrade Service Providers

10%

Secondary Research & Industry Benchmarking

Secondary research underpins our primary efforts, accounting for approximately 25% of the total research. This phase involves a rigorous review of published data and industry reports to establish a foundational understanding of the "Dipping Sonar" market. We leverage a diverse array of credible sources, avoiding market research websites to maintain independent analysis.

Data Sources:

Governmental defense spending reports (e.g., U.S. Department of Defense Budgets, UK Ministry of Defence gov.uk)

Company annual reports, investor presentations, and financial disclosures retrieved from Bloomberg, Factiva, Hoovers, and PitchBook.

Patent databases and technical whitepapers.

This phase also involves benchmarking against industry best practices and global market trends to contextualize our findings.

Demand Modeling & Market Estimation

Our market size estimation for "Dipping Sonar" employs a robust combination of top-down and bottom-up methodologies, enhanced by multi-level data triangulation to ensure accuracy and reliability.

Bottom-up Market Sizing Variables:

Number of active naval platforms (helicopters, frigates, patrol vessels) equipped or slated for ASW dipping sonar integration.

Average unit price of Low-Frequency Sonar and Mid-Frequency Sonar systems, differentiated by application (Military & Defense, Others) and region.

Annual procurement budgets and R&D spending specifically allocated for Anti-Submarine Warfare (ASW) sensor systems by key military powers.

Installed base replacement cycles and upgrade schedules for existing sonar assets.

The top-down approach involves segmenting the broader global defense and maritime electronics market, then applying specific growth rates and penetration factors for dipping sonar. Multi-level data triangulation involves comparing and cross-referencing data points derived from primary interviews, secondary sources, and internal statistical models. This iterative process helps resolve discrepancies and refine estimates across all defined segments: Application (Military and Defense, Others), Types (Low Frequency Sonar, Mid-frequency Sonar), and regions (North America, South America, Europe, Middle East & Africa, Asia Pacific).

Data Accuracy & Quality Check

We are committed to delivering market intelligence with a guaranteed estimated data accuracy level of 85-90%. This high standard is maintained through a rigorous, multi-stage validation process. All primary data points are cross-verified with multiple sources where possible. Quantitative data is subjected to statistical analysis to identify outliers and anomalies. Qualitative insights are interpreted within the context of prevailing industry trends and expert consensus. Our proprietary quality control framework involves:

Source Verification: Ensuring the credibility and relevance of all primary and secondary data sources.

Methodological Review: Peer review of sampling strategies, questionnaire design, and analytical models.

Expert Panel Validation: Select insights and market forecasts are presented to an independent panel of industry experts for validation and feedback.

Continuous Updates: As part of our commitment to delivering the most current insights, every report is updated up to the date of purchase, incorporating any new developments or data shifts in the "Dipping Sonar" market.

This comprehensive approach allows us to present a nuanced, accurate, and forward-looking analysis of the global Dipping Sonar market.

Frequently Asked Questions

1. Which industries are the primary end-users for Dipping Sonar technology?

Dipping Sonar technology is primarily utilized by the military and defense sector for anti-submarine warfare (ASW) and maritime surveillance operations. Downstream demand is driven by global naval modernization programs and geopolitical tensions requiring enhanced underwater detection capabilities.

2. What is the current state of investment activity in the Dipping Sonar market?

Investment in Dipping Sonar technology is primarily driven by government defense budgets and strategic procurement by leading manufacturers like L3Harris Technologies and Thales Group. Venture capital interest is limited, with most funding directed towards established defense contractors and R&D through public grants.

3. What disruptive technologies or substitutes are emerging in the Dipping Sonar market?

While direct substitutes for active dipping sonar are limited, advancements in passive acoustic systems, autonomous underwater vehicles (AUVs) with integrated sensors, and multi-static sonar networks represent emerging capabilities. These technologies aim to enhance stealth and expand detection ranges.

4. Have there been notable recent developments or M&A activities in Dipping Sonar?

Major players such as L3Harris Technologies and Thales Group continuously invest in R&D to improve sonar performance, signal processing, and operational efficiency. While specific recent M&A deals were not detailed, product launches focus on integrating AI/ML for data analysis and enhancing interoperability across naval platforms.

5. What is the projected market size and CAGR for Dipping Sonar through 2033?

The Dipping Sonar market was valued at $147 million, with a projected Compound Annual Growth Rate (CAGR) of 9.3%. This growth is anticipated to continue through 2033, driven by ongoing naval defense spending and technological upgrades.

6. How do export-import dynamics influence the global Dipping Sonar market?

International trade flows are highly regulated due to the strategic military nature of Dipping Sonar technology. Export licenses and intergovernmental agreements dictate the supply chain, with key manufacturers like Armelsan and SAES serving both domestic and allied international markets under strict controls.