Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

AMR for Semiconductor Market Evolution & 2034 Growth Outlook

AMR for Semiconductor

AMR for Semiconductor Market Evolution & 2034 Growth Outlook

AMR for Semiconductor by Offering (Hardware, Software & Services), by Mode of Operation (Fully Autonomous, Semi-Autonomous), by Type (Picking Robots, Inventory Robots, Self-driving Forklifts, Others), by Application (Picking & Sorting, Transportation, Inventory Management, Assembly, Others), by End User (Logistics & Warehousing, Retail and E-commerce, Pharmaceuticals and Healthcare, Automotive, Aerospace and Defense, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 116

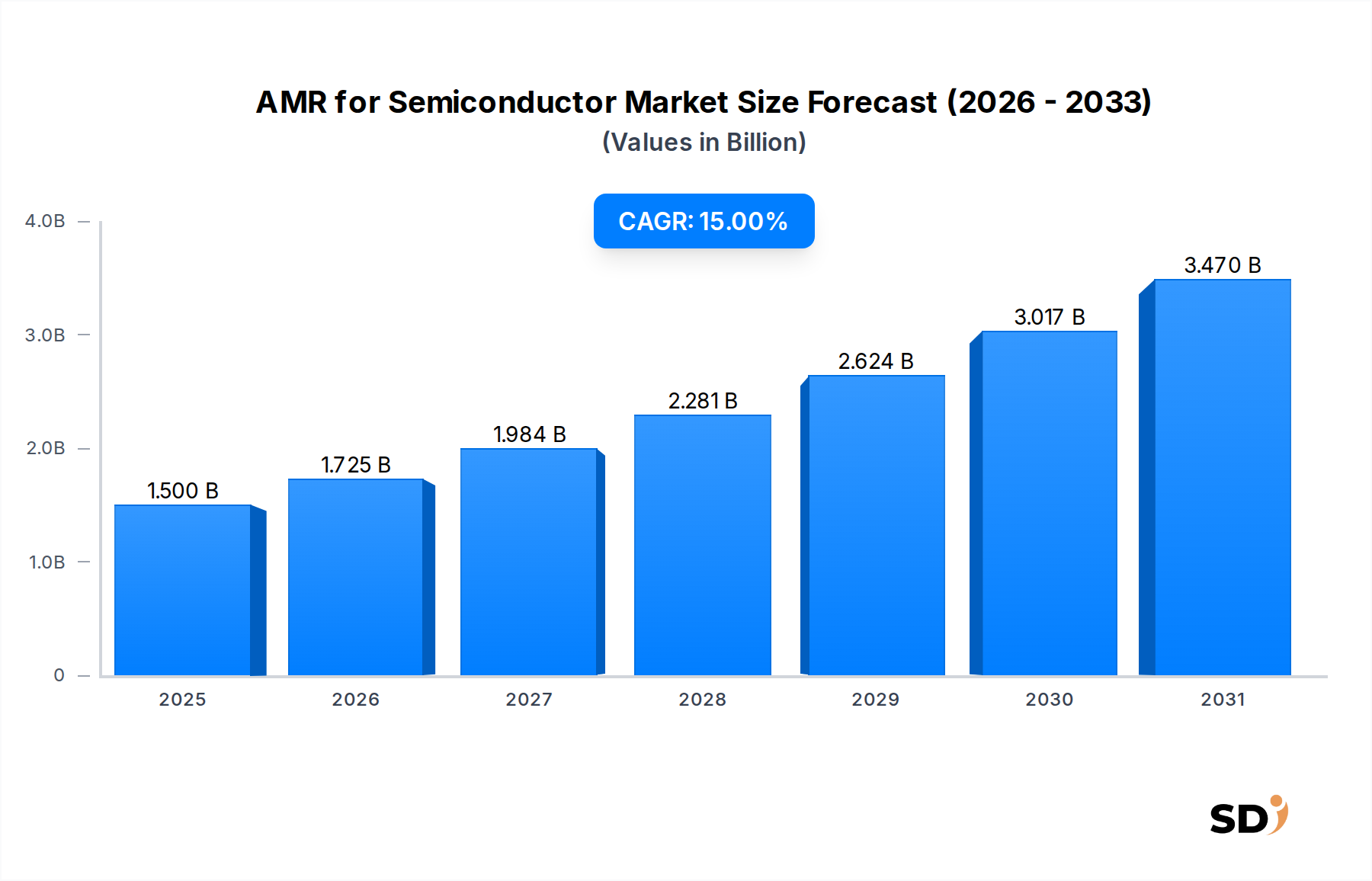

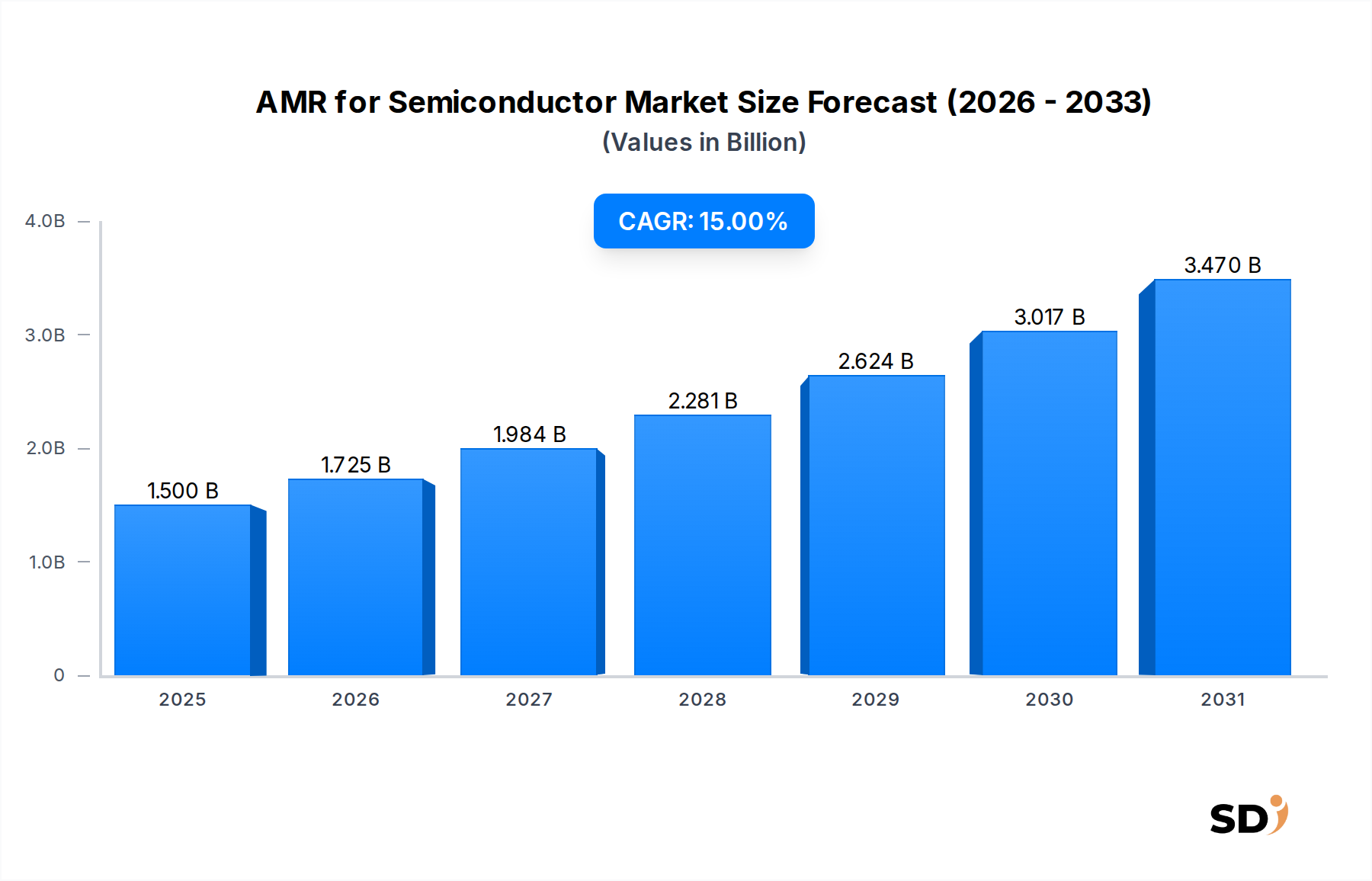

The Global AMR for Semiconductor Market is experiencing a robust growth trajectory, driven by the escalating demand for advanced automation within semiconductor fabrication plants (fabs). Valued at an estimated $1.5 billion in 2025, the market is projected to expand significantly, reaching approximately $5.277 billion by 2034, exhibiting a compelling Compound Annual Growth Rate (CAGR) of 15% from 2026 to 2034. This aggressive growth is underpinned by several critical demand drivers and macro tailwinds impacting the semiconductor industry globally.

AMR for Semiconductor Market Size (In Billion)

4.0B

3.0B

2.0B

1.0B

0

1.500 B

2025

1.725 B

2026

1.984 B

2027

2.281 B

2028

2.624 B

2029

3.017 B

2030

3.470 B

2031

At its core, the adoption of Autonomous Mobile Robots (AMRs) in semiconductor manufacturing is fueled by the imperative for unparalleled precision, stringent cleanroom compatibility, and enhanced operational efficiency. Semiconductor fabs operate under exceptionally demanding conditions, requiring ISO Class 1-5 cleanroom environments where human presence can introduce critical contamination. AMRs mitigate this risk, ensuring pristine manufacturing conditions for delicate wafers and high-value components. Furthermore, the persistent global labor shortage in skilled manufacturing roles, coupled with rising labor costs, incentivizes fabs to invest in intelligent automation solutions that can operate 24/7 without fatigue or error. AMRs excel in repetitive material handling tasks, such as wafer transport between processing stages, inventory management within storage areas, and automated delivery of chemicals or reticles, thereby optimizing throughput and reducing cycle times.

Macro tailwinds are significantly propelling this market forward. The insatiable global demand for semiconductors, driven by advancements in Artificial Intelligence (AI), the Internet of Things (IoT), 5G technology, and the automotive sector, necessitates increased chip production capacity. Government initiatives, such as the CHIPS Act in the United States and the EU Chips Act, are catalyzing massive investments in new fab construction and expansion, directly translating into greater demand for sophisticated automation technologies like AMRs. The ongoing push for Industry 4.0 integration across manufacturing sectors further accelerates the adoption of connected and data-driven AMR systems. The Artificial Intelligence in Manufacturing Market is particularly benefiting from this integration, as AI and machine learning algorithms are crucial for optimizing AMR navigation, path planning, and predictive maintenance. This strategic push for resilience and efficiency within the semiconductor supply chain also provides significant momentum to the broader Logistics Automation Market, of which AMRs are an integral, high-value component within semiconductor operations.

Dominant Offering Segment in AMR for Semiconductor Market

Within the multifaceted AMR for Semiconductor Market, the "Hardware" sub-segment of the Offering category is firmly established as the dominant force by revenue share. This segment encompasses the physical robot units themselves, including their chassis, integrated navigation systems (e.g., LiDAR, cameras), highly specialized manipulators or end-effectors designed for delicate wafer handling (such as EFEM interfaces or FOUP/SMIF carriers), advanced power systems, and the construction using cleanroom-compatible materials. The very nature of semiconductor manufacturing dictates that these hardware components are engineered to the highest standards of precision, reliability, and environmental resilience.

Several factors contribute to Hardware's preeminence. Firstly, the initial capital expenditure associated with procuring these specialized robots is substantial. Unlike general-purpose industrial robots, AMRs for semiconductor applications must adhere to stringent cleanroom standards, often requiring bespoke materials, sealed components, and specialized lubrication to prevent particulate generation. Secondly, the complexity involved in engineering robots capable of micron-level positioning and precise interaction with high-value wafers and sophisticated Semiconductor Manufacturing Equipment Market components commands a significant premium. The mechanical design, including advanced actuators and highly accurate motion control systems, represents a considerable portion of the overall cost.

While the "Software & Services" segment is rapidly evolving and gaining traction, driven by advancements in fleet management systems, AI/ML-powered navigation, predictive analytics, and integration services, the foundational investment in the physical robot unit remains paramount. The ongoing evolution of the Industrial Robotics Market continually introduces more capable hardware platforms, but the specific adaptations for the semiconductor environment differentiate these offerings. The requirement for specialized components means that the Robotics Components Market is a crucial upstream supplier, providing the high-performance sensors, motors, and controllers necessary for these advanced systems. Furthermore, the market for Automated Guided Vehicle Market is closely intertwined here, with many AMRs effectively serving as advanced AGVs in a semiconductor context, albeit with enhanced autonomy and intelligence. The sophistication of these hardware platforms ensures their continued dominance in revenue generation, despite the increasing value proposition of the software and service layers that enable their intelligent operation.

Key Market Drivers & Constraints in AMR for Semiconductor Market

The AMR for Semiconductor Market is shaped by a unique combination of compelling growth drivers and significant operational constraints, each with quantifiable impacts on adoption and market dynamics.

Market Drivers:

Stringent Cleanroom Protocols and Contamination Control: Semiconductor manufacturing demands environments ranging from ISO Class 1 to Class 5 cleanrooms. Human operators are a primary source of particulate contamination, which can critically impair yields and product quality. AMRs virtually eliminate human-induced contamination in these controlled environments. This direct impact on yield improvement is a non-negotiable factor, quantified by reduced defect rates in wafer processing, which can save millions in a single fab's output.

Increased Global Demand for Semiconductor Products: The burgeoning Semiconductor Manufacturing Equipment Market is witnessing unprecedented growth, driven by the pervasive digitalization of industries, advancements in AI, IoT, and the rapid expansion of electric vehicles. This surge necessitates expanded and more efficient fab capacities, with global chip sales projected to grow by double-digit percentages in coming years. Such expansion directly translates into a heightened need for automated material handling solutions, as AMRs contribute to a substantial increase in wafer starts per month (WSPM) through optimized logistics.

Labor Shortages and Escalating Labor Costs: The global semiconductor industry faces a significant deficit of skilled technicians and engineers. This shortage, coupled with rising labor costs, drives the imperative for automation. AMRs can reduce the reliance on human operators for repetitive, mundane, and ergonomically challenging tasks, allowing personnel to be reallocated to higher-value activities like process monitoring and complex problem-solving. This addresses operational expenditure concerns by optimizing workforce deployment.

Demand for Enhanced Operational Efficiency and Throughput: AMRs enable continuous 24/7 operation, consistent speed, and dynamic path optimization within fabs. This leads to significantly higher wafer throughput and reduced cycle times. For instance, optimized AMR routes can cut material travel times by 10-20%, directly enhancing overall equipment effectiveness (OEE) and production output, a critical metric in high-volume manufacturing.

Market Constraints:

High Initial Investment Costs: The specialized design, robust engineering, and mandatory cleanroom compatibility of AMRs for semiconductor applications lead to substantial upfront capital expenditure. A single cleanroom-rated AMR system can cost significantly more than a general industrial AMR, posing a barrier, particularly for smaller foundries or new entrants, impacting their initial return on investment calculations.

Integration Complexity with Legacy Systems: Many existing semiconductor fabs rely on a diverse array of legacy, often proprietary, material handling systems (e.g., Overhead Hoist Transport systems - OHTs, or older conveyor lines). Integrating new, intelligent AMRs into these established, and sometimes closed, ecosystems presents considerable technical challenges, requiring extensive customization and substantial engineering effort for seamless interoperability.

Safety Concerns and Regulatory Compliance: Ensuring the seamless and safe co-existence of AMRs with human operators and other automated equipment within a dynamic fab environment is paramount. This necessitates advanced safety features, robust collision avoidance systems, and adherence to evolving industry safety standards (e.g., SEMI S2/S8). The complexity of certifying AMRs for human-robot collaborative environments adds to the deployment timeline and cost, particularly in the context of the Industrial Sensors Market used for detection and navigation.

Competitive Ecosystem of AMR for Semiconductor Market

The AMR for Semiconductor Market is characterized by a mix of established industrial automation giants and specialized robotics firms, all vying to meet the stringent demands of semiconductor manufacturing:

Körber AG: A global technology group offering integrated supply chain solutions, including advanced automation and software, Körber aims to optimize material flow and logistics within high-tech production environments such as semiconductor fabs.

ABB: A leader in industrial automation and robotics, ABB provides a comprehensive range of robotic solutions that can be adapted for the precise material handling, assembly, and cleanroom applications critical to the semiconductor sector.

Yaskawa Electric Corporation: A prominent manufacturer of industrial robots and motion control systems, Yaskawa offers high-precision robot arms and controllers that are well-suited for the delicate wafer handling, inspection, and assembly tasks required in semiconductor production processes.

Stäubli: Known for its precision mechatronics and advanced robotics, Stäubli provides high-performance industrial robots, including specialized versions designed for stringent cleanroom environments, catering directly to the unique requirements of semiconductor fabrication.

KUKA AG: A leading global supplier of intelligent automation solutions, KUKA manufactures a broad portfolio of industrial robots and automated systems that are customizable for material transport, processing, and quality control within advanced manufacturing facilities.

Conveyco: Specializes in integrating material handling systems and comprehensive supply chain solutions, leveraging various automation technologies to enhance logistics efficiency and operational throughput for manufacturing clients.

Epson Robots: Focuses on compact, high-precision industrial robots, particularly SCARA and 6-axis robots, which are highly suitable for intricate and cleanroom-compatible tasks often found in the assembly, packaging, and testing stages of semiconductor manufacturing.

Aethon: A pioneer in autonomous mobile robots primarily for logistics and healthcare, Aethon's TUG robots are designed for automated material delivery, a core capability that is transferable and adaptable for intra-fab logistics for materials and work-in-progress (WIP).

Blue Ocean Robotics: This company develops and commercializes professional service robots, often through spin-out ventures, addressing diverse industry needs including those requiring automated internal logistics and specialized handling capabilities.

Recent Developments & Milestones in AMR for Semiconductor Market

Recent innovations and strategic movements underscore the dynamic evolution of the AMR for Semiconductor Market, driving enhanced capabilities and broader adoption:

Q3 2023: Leading AMR providers introduced new generations of cleanroom-certified autonomous mobile robots, featuring significantly enhanced payload capacities and advanced navigation algorithms, specifically engineered to optimize 300mm wafer handling and FOUP transport in next-generation fabs.

Q1 2024: Several major semiconductor manufacturers announced strategic partnerships with automation specialists to integrate cutting-edge, AI-driven Autonomous Mobile Robot Software Market for real-time optimization of material flow, predictive maintenance, and dynamic routing across their global production facilities.

Q2 2024: Industry consortia, comprising key players from the Semiconductor Manufacturing Equipment Market and leading fab operators, published updated standardization guidelines for AMR communication protocols and safety features. This initiative aims to accelerate seamless integration and foster wider adoption within both existing infrastructure and new fab constructions.

Q4 2024: Breakthroughs in battery technology led to the commercial introduction of AMRs offering significantly extended operational hours and faster charging cycles. These advancements directly address the critical uptime requirements and continuous operation demands of high-volume semiconductor manufacturing environments.

Q1 2025: Companies showcased next-generation AMRs equipped with highly advanced vision systems and deep machine learning capabilities. These systems enable more flexible and precise handling of diverse cassette types, reticles, and specialty materials, thereby expanding the reach and sophistication of Artificial Intelligence in Manufacturing Market applications within semiconductor fabs.

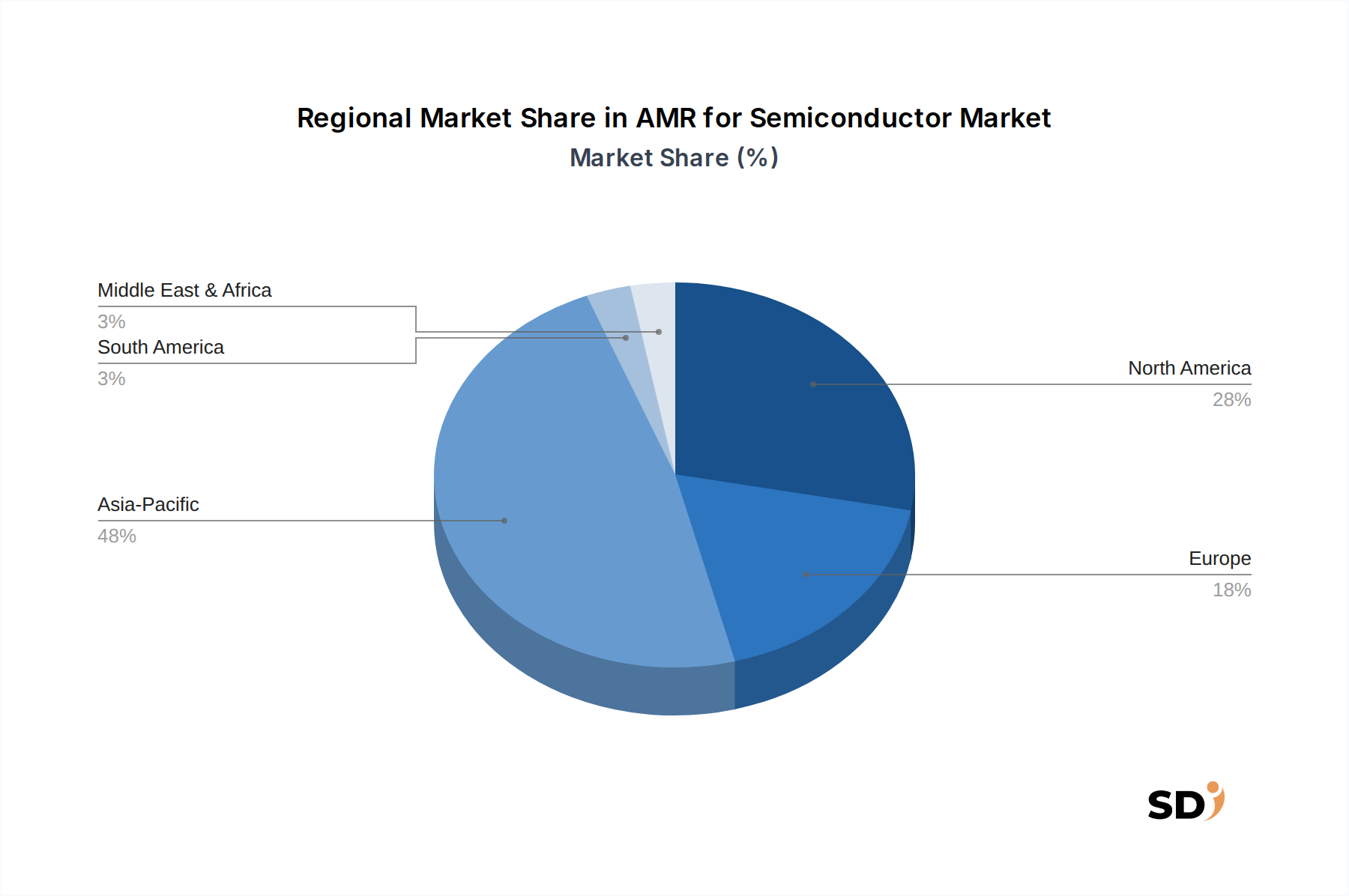

Regional Market Breakdown for AMR for Semiconductor Market

The global AMR for Semiconductor Market exhibits distinct regional dynamics, largely influenced by the concentration of semiconductor manufacturing, investment in new fabs, and technological adoption rates. While a precise regional CAGR for this specialized niche requires granular data, general trends within the broader semiconductor and automation industries provide a clear outlook.

Asia Pacific is anticipated to hold the largest revenue share and likely demonstrate the highest growth in the AMR for Semiconductor Market. This dominance is driven by the region's unparalleled concentration of semiconductor manufacturing giants in Taiwan, South Korea, China, and Japan, coupled with substantial investments in new fab construction and expansion. Countries like China and India are also rapidly building domestic semiconductor capabilities, fueling demand for advanced automation. The primary demand driver in this region is the sheer volume of high-capacity manufacturing and the strategic push for domestic chip production, significantly impacting the Semiconductor Manufacturing Equipment Market landscape.

North America commands a significant market share, characterized by its focus on advanced node manufacturing and reshoring initiatives, such as the CHIPS Act. The region's emphasis on high-tech innovation and automation to offset rising labor costs ensures a strong adoption rate of AMRs in existing and upcoming fabs. The primary demand driver here is strategic investments in advanced manufacturing capabilities, aiming to reduce supply chain dependencies and maintain technological leadership.

Europe represents a growing market for AMR in semiconductors, propelled by initiatives like the EU Chips Act and a strong focus on sustainable, highly automated manufacturing processes. The region's robust R&D ecosystem and presence of specialized equipment manufacturers contribute to innovation in this space. The strongest demand driver in Europe is the emphasis on high-value, specialized chip production and enhancing regional self-sufficiency in critical technologies.

Middle East & Africa (MEA), while currently holding a smaller revenue share, is an emerging market with substantial growth potential. New investments in technology infrastructure and efforts towards economic diversification are laying the groundwork for future fab projects. The primary demand driver is greenfield investments in technology-intensive industries and national strategies to establish advanced manufacturing capabilities, though this growth occurs from a relatively smaller base.

Pricing Dynamics & Margin Pressure in AMR for Semiconductor Market

The pricing dynamics in the AMR for Semiconductor Market are complex, influenced by high specialization, stringent performance requirements, and a demanding customer base. Average Selling Prices (ASPs) for AMRs in this sector are generally higher compared to general industrial AMRs, primarily due to the necessity for cleanroom compatibility (ISO Class 1-5), extreme precision in motion and positioning, and customized end-effectors for delicate wafer or FOUP handling. These bespoke requirements mean that off-the-shelf solutions are rare, leading to premium pricing for highly engineered systems.

Margin structures across the value chain reflect this specialization. Hardware manufacturers typically achieve healthy initial margins, which can fluctuate based on the volume of specialized component procurement from the Robotics Components Market and the intensity of R&D investment. However, as technology matures and competitive intensity grows, particularly with new entrants from regions like Asia, there's a predictable downward pressure on ASPs for more commoditized AMR functionalities. Conversely, the "Software & Services" sub-segment within the offering often yields higher, more recurring margins through subscription models for Autonomous Mobile Robot Software Market, long-term maintenance contracts, and periodic software updates.

Key cost levers include the expense of advanced navigation sensors (a significant component of the Industrial Sensors Market), specialized materials for cleanroom environments, high-precision actuators, and the significant R&D investment required to meet evolving semiconductor manufacturing standards. Competitive intensity from both established Industrial Robotics Market players expanding into AMRs and specialized AMR startups is steadily increasing. This heightens pressure on pricing power, pushing manufacturers to innovate and differentiate through superior performance, reliability, and advanced features like AI-driven predictive maintenance or enhanced collaborative safety. Semiconductor manufacturers, while prioritizing performance, are also increasingly focused on the total cost of ownership (TCO), necessitating solutions that offer clear ROI through yield improvements and operational efficiency, further influencing pricing strategies.

Customer Segmentation & Buying Behavior in AMR for Semiconductor Market

Customer segmentation in the AMR for Semiconductor Market is primarily defined by the different operational entities within the semiconductor value chain, each with unique purchasing criteria and behavioral patterns.

End-User Segments:

Integrated Device Manufacturers (IDMs): These are large corporations that design, manufacture, and sell semiconductors (e.g., Intel, Samsung, Micron). They demand highly sophisticated, integrated AMR solutions for their high-volume, vertically integrated fabs, often involving long-term strategic partnerships and multi-year procurement cycles.

Foundries: Companies that exclusively manufacture chips for other companies (e.g., TSMC, UMC, GlobalFoundries). Their focus is intensely on efficiency, throughput, and flexibility to serve diverse clients. AMRs are critical for optimizing material flow in their high-mix, high-volume production environments.

Outsourced Semiconductor Assembly and Test (OSAT) Providers: Companies specializing in the assembly, packaging, and testing phases of semiconductor manufacturing (e.g., ASE Technology Holding, Amkor). While cleanroom requirements may be slightly less stringent than front-end fabs, they heavily rely on AMRs for efficient material handling between different assembly and test process steps.

Semiconductor Manufacturing Equipment Manufacturers: These companies may utilize AMRs within their own internal assembly lines or testing facilities before shipping equipment to fabs, emphasizing precision material movement for their components.

Purchasing Criteria:

Customer buying behavior is dominated by technical performance and operational reliability. Key criteria include:

Cleanroom Compatibility: An absolute necessity, with AMRs required to meet specific ISO Class standards (e.g., ISO Class 1-5) to prevent contamination.

Precision and Repeatability: Crucial for delicate wafer handling and exact positioning within process tools, measured in microns.

Payload Capacity and Type: The ability to handle specific wafer sizes (e.g., 300mm), FOUPs, reticles, or chemical containers.

Integration Capabilities: Seamless interface with existing Manufacturing Execution Systems (MES), SCADA, and other fab automation systems is paramount for optimized material flow, often requiring robust Autonomous Mobile Robot Software Market interfaces.

Safety and Reliability: Essential for protecting high-value assets and ensuring continuous uptime, as downtime in a fab can cost millions per hour.

Total Cost of Ownership (TCO): While initial cost is considered, ROI derived from yield improvements, throughput gains, and reduced labor needs is prioritized, especially given the high value of products.

Procurement Channel & Shifts:

Procurement primarily occurs directly from AMR manufacturers or through highly specialized system integrators with deep expertise in semiconductor fab automation. There is an observable shift towards modular, scalable, and easily reconfigurable AMRs to adapt to the rapidly changing production demands and technology nodes. Additionally, a growing preference exists for solutions that offer advanced data analytics and AI-driven predictive maintenance, contributing to the broader trends seen in the Warehouse Automation Market but adapted for the unique precision of semiconductor manufacturing.

AMR for Semiconductor Segmentation

1. Offering

1.1. Hardware

1.2. Software & Services

2. Mode of Operation

2.1. Fully Autonomous

2.2. Semi-Autonomous

3. Type

3.1. Picking Robots

3.2. Inventory Robots

3.3. Self-driving Forklifts

3.4. Others

4. Application

4.1. Picking & Sorting

4.2. Transportation

4.3. Inventory Management

4.4. Assembly

4.5. Others

5. End User

5.1. Logistics & Warehousing

5.2. Retail and E-commerce

5.3. Pharmaceuticals and Healthcare

5.4. Automotive

5.5. Aerospace and Defense

5.6. Others

AMR for Semiconductor Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

AMR for Semiconductor REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 15% from 2020-2034

Segmentation

By Offering

Hardware

Software & Services

By Mode of Operation

Fully Autonomous

Semi-Autonomous

By Type

Picking Robots

Inventory Robots

Self-driving Forklifts

Others

By Application

Picking & Sorting

Transportation

Inventory Management

Assembly

Others

By End User

Logistics & Warehousing

Retail and E-commerce

Pharmaceuticals and Healthcare

Automotive

Aerospace and Defense

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Offering

5.1.1. Hardware

5.1.2. Software & Services

5.2. Market Analysis, Insights and Forecast - by Mode of Operation

5.2.1. Fully Autonomous

5.2.2. Semi-Autonomous

5.3. Market Analysis, Insights and Forecast - by Type

5.3.1. Picking Robots

5.3.2. Inventory Robots

5.3.3. Self-driving Forklifts

5.3.4. Others

5.4. Market Analysis, Insights and Forecast - by Application

5.4.1. Picking & Sorting

5.4.2. Transportation

5.4.3. Inventory Management

5.4.4. Assembly

5.4.5. Others

5.5. Market Analysis, Insights and Forecast - by End User

5.5.1. Logistics & Warehousing

5.5.2. Retail and E-commerce

5.5.3. Pharmaceuticals and Healthcare

5.5.4. Automotive

5.5.5. Aerospace and Defense

5.5.6. Others

5.6. Market Analysis, Insights and Forecast - by Region

5.6.1. North America

5.6.2. South America

5.6.3. Europe

5.6.4. Middle East & Africa

5.6.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Offering

6.1.1. Hardware

6.1.2. Software & Services

6.2. Market Analysis, Insights and Forecast - by Mode of Operation

6.2.1. Fully Autonomous

6.2.2. Semi-Autonomous

6.3. Market Analysis, Insights and Forecast - by Type

6.3.1. Picking Robots

6.3.2. Inventory Robots

6.3.3. Self-driving Forklifts

6.3.4. Others

6.4. Market Analysis, Insights and Forecast - by Application

6.4.1. Picking & Sorting

6.4.2. Transportation

6.4.3. Inventory Management

6.4.4. Assembly

6.4.5. Others

6.5. Market Analysis, Insights and Forecast - by End User

6.5.1. Logistics & Warehousing

6.5.2. Retail and E-commerce

6.5.3. Pharmaceuticals and Healthcare

6.5.4. Automotive

6.5.5. Aerospace and Defense

6.5.6. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Offering

7.1.1. Hardware

7.1.2. Software & Services

7.2. Market Analysis, Insights and Forecast - by Mode of Operation

7.2.1. Fully Autonomous

7.2.2. Semi-Autonomous

7.3. Market Analysis, Insights and Forecast - by Type

7.3.1. Picking Robots

7.3.2. Inventory Robots

7.3.3. Self-driving Forklifts

7.3.4. Others

7.4. Market Analysis, Insights and Forecast - by Application

7.4.1. Picking & Sorting

7.4.2. Transportation

7.4.3. Inventory Management

7.4.4. Assembly

7.4.5. Others

7.5. Market Analysis, Insights and Forecast - by End User

7.5.1. Logistics & Warehousing

7.5.2. Retail and E-commerce

7.5.3. Pharmaceuticals and Healthcare

7.5.4. Automotive

7.5.5. Aerospace and Defense

7.5.6. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Offering

8.1.1. Hardware

8.1.2. Software & Services

8.2. Market Analysis, Insights and Forecast - by Mode of Operation

8.2.1. Fully Autonomous

8.2.2. Semi-Autonomous

8.3. Market Analysis, Insights and Forecast - by Type

8.3.1. Picking Robots

8.3.2. Inventory Robots

8.3.3. Self-driving Forklifts

8.3.4. Others

8.4. Market Analysis, Insights and Forecast - by Application

8.4.1. Picking & Sorting

8.4.2. Transportation

8.4.3. Inventory Management

8.4.4. Assembly

8.4.5. Others

8.5. Market Analysis, Insights and Forecast - by End User

8.5.1. Logistics & Warehousing

8.5.2. Retail and E-commerce

8.5.3. Pharmaceuticals and Healthcare

8.5.4. Automotive

8.5.5. Aerospace and Defense

8.5.6. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Offering

9.1.1. Hardware

9.1.2. Software & Services

9.2. Market Analysis, Insights and Forecast - by Mode of Operation

9.2.1. Fully Autonomous

9.2.2. Semi-Autonomous

9.3. Market Analysis, Insights and Forecast - by Type

9.3.1. Picking Robots

9.3.2. Inventory Robots

9.3.3. Self-driving Forklifts

9.3.4. Others

9.4. Market Analysis, Insights and Forecast - by Application

9.4.1. Picking & Sorting

9.4.2. Transportation

9.4.3. Inventory Management

9.4.4. Assembly

9.4.5. Others

9.5. Market Analysis, Insights and Forecast - by End User

9.5.1. Logistics & Warehousing

9.5.2. Retail and E-commerce

9.5.3. Pharmaceuticals and Healthcare

9.5.4. Automotive

9.5.5. Aerospace and Defense

9.5.6. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Offering

10.1.1. Hardware

10.1.2. Software & Services

10.2. Market Analysis, Insights and Forecast - by Mode of Operation

10.2.1. Fully Autonomous

10.2.2. Semi-Autonomous

10.3. Market Analysis, Insights and Forecast - by Type

10.3.1. Picking Robots

10.3.2. Inventory Robots

10.3.3. Self-driving Forklifts

10.3.4. Others

10.4. Market Analysis, Insights and Forecast - by Application

10.4.1. Picking & Sorting

10.4.2. Transportation

10.4.3. Inventory Management

10.4.4. Assembly

10.4.5. Others

10.5. Market Analysis, Insights and Forecast - by End User

10.5.1. Logistics & Warehousing

10.5.2. Retail and E-commerce

10.5.3. Pharmaceuticals and Healthcare

10.5.4. Automotive

10.5.5. Aerospace and Defense

10.5.6. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Körber AG

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. ABB

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Yaskawa Electric Corporation

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Stäubli

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. KUKA AG

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Conveyco

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Epson Robots

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Aethon

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Blue Ocean Robotics

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Others

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Offering 2025 & 2033

Figure 4: Volume (K), by Offering 2025 & 2033

Figure 5: Revenue Share (%), by Offering 2025 & 2033

Figure 6: Volume Share (%), by Offering 2025 & 2033

Figure 7: Revenue (billion), by Mode of Operation 2025 & 2033

Figure 8: Volume (K), by Mode of Operation 2025 & 2033

Figure 9: Revenue Share (%), by Mode of Operation 2025 & 2033

Figure 10: Volume Share (%), by Mode of Operation 2025 & 2033

Figure 11: Revenue (billion), by Type 2025 & 2033

Figure 12: Volume (K), by Type 2025 & 2033

Figure 13: Revenue Share (%), by Type 2025 & 2033

Figure 14: Volume Share (%), by Type 2025 & 2033

Figure 15: Revenue (billion), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (billion), by End User 2025 & 2033

Figure 20: Volume (K), by End User 2025 & 2033

Figure 21: Revenue Share (%), by End User 2025 & 2033

Figure 22: Volume Share (%), by End User 2025 & 2033

Figure 23: Revenue (billion), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (billion), by Offering 2025 & 2033

Figure 28: Volume (K), by Offering 2025 & 2033

Figure 29: Revenue Share (%), by Offering 2025 & 2033

Figure 30: Volume Share (%), by Offering 2025 & 2033

Figure 31: Revenue (billion), by Mode of Operation 2025 & 2033

Figure 32: Volume (K), by Mode of Operation 2025 & 2033

Figure 33: Revenue Share (%), by Mode of Operation 2025 & 2033

Figure 34: Volume Share (%), by Mode of Operation 2025 & 2033

Figure 35: Revenue (billion), by Type 2025 & 2033

Figure 36: Volume (K), by Type 2025 & 2033

Figure 37: Revenue Share (%), by Type 2025 & 2033

Figure 38: Volume Share (%), by Type 2025 & 2033

Figure 39: Revenue (billion), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (billion), by End User 2025 & 2033

Figure 44: Volume (K), by End User 2025 & 2033

Figure 45: Revenue Share (%), by End User 2025 & 2033

Figure 46: Volume Share (%), by End User 2025 & 2033

Figure 47: Revenue (billion), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (billion), by Offering 2025 & 2033

Figure 52: Volume (K), by Offering 2025 & 2033

Figure 53: Revenue Share (%), by Offering 2025 & 2033

Figure 54: Volume Share (%), by Offering 2025 & 2033

Figure 55: Revenue (billion), by Mode of Operation 2025 & 2033

Figure 56: Volume (K), by Mode of Operation 2025 & 2033

Figure 57: Revenue Share (%), by Mode of Operation 2025 & 2033

Figure 58: Volume Share (%), by Mode of Operation 2025 & 2033

Figure 59: Revenue (billion), by Type 2025 & 2033

Figure 60: Volume (K), by Type 2025 & 2033

Figure 61: Revenue Share (%), by Type 2025 & 2033

Figure 62: Volume Share (%), by Type 2025 & 2033

Figure 63: Revenue (billion), by Application 2025 & 2033

Figure 64: Volume (K), by Application 2025 & 2033

Figure 65: Revenue Share (%), by Application 2025 & 2033

Figure 66: Volume Share (%), by Application 2025 & 2033

Figure 67: Revenue (billion), by End User 2025 & 2033

Figure 68: Volume (K), by End User 2025 & 2033

Figure 69: Revenue Share (%), by End User 2025 & 2033

Figure 70: Volume Share (%), by End User 2025 & 2033

Figure 71: Revenue (billion), by Country 2025 & 2033

Figure 72: Volume (K), by Country 2025 & 2033

Figure 73: Revenue Share (%), by Country 2025 & 2033

Figure 74: Volume Share (%), by Country 2025 & 2033

Figure 75: Revenue (billion), by Offering 2025 & 2033

Figure 76: Volume (K), by Offering 2025 & 2033

Figure 77: Revenue Share (%), by Offering 2025 & 2033

Figure 78: Volume Share (%), by Offering 2025 & 2033

Figure 79: Revenue (billion), by Mode of Operation 2025 & 2033

Figure 80: Volume (K), by Mode of Operation 2025 & 2033

Figure 81: Revenue Share (%), by Mode of Operation 2025 & 2033

Figure 82: Volume Share (%), by Mode of Operation 2025 & 2033

Figure 83: Revenue (billion), by Type 2025 & 2033

Figure 84: Volume (K), by Type 2025 & 2033

Figure 85: Revenue Share (%), by Type 2025 & 2033

Figure 86: Volume Share (%), by Type 2025 & 2033

Figure 87: Revenue (billion), by Application 2025 & 2033

Figure 88: Volume (K), by Application 2025 & 2033

Figure 89: Revenue Share (%), by Application 2025 & 2033

Figure 90: Volume Share (%), by Application 2025 & 2033

Figure 91: Revenue (billion), by End User 2025 & 2033

Figure 92: Volume (K), by End User 2025 & 2033

Figure 93: Revenue Share (%), by End User 2025 & 2033

Figure 94: Volume Share (%), by End User 2025 & 2033

Figure 95: Revenue (billion), by Country 2025 & 2033

Figure 96: Volume (K), by Country 2025 & 2033

Figure 97: Revenue Share (%), by Country 2025 & 2033

Figure 98: Volume Share (%), by Country 2025 & 2033

Figure 99: Revenue (billion), by Offering 2025 & 2033

Figure 100: Volume (K), by Offering 2025 & 2033

Figure 101: Revenue Share (%), by Offering 2025 & 2033

Figure 102: Volume Share (%), by Offering 2025 & 2033

Figure 103: Revenue (billion), by Mode of Operation 2025 & 2033

Figure 104: Volume (K), by Mode of Operation 2025 & 2033

Figure 105: Revenue Share (%), by Mode of Operation 2025 & 2033

Figure 106: Volume Share (%), by Mode of Operation 2025 & 2033

Figure 107: Revenue (billion), by Type 2025 & 2033

Figure 108: Volume (K), by Type 2025 & 2033

Figure 109: Revenue Share (%), by Type 2025 & 2033

Figure 110: Volume Share (%), by Type 2025 & 2033

Figure 111: Revenue (billion), by Application 2025 & 2033

Figure 112: Volume (K), by Application 2025 & 2033

Figure 113: Revenue Share (%), by Application 2025 & 2033

Figure 114: Volume Share (%), by Application 2025 & 2033

Figure 115: Revenue (billion), by End User 2025 & 2033

Figure 116: Volume (K), by End User 2025 & 2033

Figure 117: Revenue Share (%), by End User 2025 & 2033

Figure 118: Volume Share (%), by End User 2025 & 2033

Figure 119: Revenue (billion), by Country 2025 & 2033

Figure 120: Volume (K), by Country 2025 & 2033

Figure 121: Revenue Share (%), by Country 2025 & 2033

Figure 122: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Offering 2020 & 2033

Table 2: Volume K Forecast, by Offering 2020 & 2033

Table 3: Revenue billion Forecast, by Mode of Operation 2020 & 2033

Table 4: Volume K Forecast, by Mode of Operation 2020 & 2033

Table 5: Revenue billion Forecast, by Type 2020 & 2033

Table 6: Volume K Forecast, by Type 2020 & 2033

Table 7: Revenue billion Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue billion Forecast, by End User 2020 & 2033

Table 10: Volume K Forecast, by End User 2020 & 2033

Table 11: Revenue billion Forecast, by Region 2020 & 2033

Table 12: Volume K Forecast, by Region 2020 & 2033

Table 13: Revenue billion Forecast, by Offering 2020 & 2033

Table 14: Volume K Forecast, by Offering 2020 & 2033

Table 15: Revenue billion Forecast, by Mode of Operation 2020 & 2033

Table 16: Volume K Forecast, by Mode of Operation 2020 & 2033

Table 17: Revenue billion Forecast, by Type 2020 & 2033

Table 18: Volume K Forecast, by Type 2020 & 2033

Table 19: Revenue billion Forecast, by Application 2020 & 2033

Table 20: Volume K Forecast, by Application 2020 & 2033

Table 21: Revenue billion Forecast, by End User 2020 & 2033

Table 22: Volume K Forecast, by End User 2020 & 2033

Table 23: Revenue billion Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue billion Forecast, by Offering 2020 & 2033

Table 32: Volume K Forecast, by Offering 2020 & 2033

Table 33: Revenue billion Forecast, by Mode of Operation 2020 & 2033

Table 34: Volume K Forecast, by Mode of Operation 2020 & 2033

Table 35: Revenue billion Forecast, by Type 2020 & 2033

Table 36: Volume K Forecast, by Type 2020 & 2033

Table 37: Revenue billion Forecast, by Application 2020 & 2033

Table 38: Volume K Forecast, by Application 2020 & 2033

Table 39: Revenue billion Forecast, by End User 2020 & 2033

Table 40: Volume K Forecast, by End User 2020 & 2033

Table 41: Revenue billion Forecast, by Country 2020 & 2033

Table 42: Volume K Forecast, by Country 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue billion Forecast, by Offering 2020 & 2033

Table 50: Volume K Forecast, by Offering 2020 & 2033

Table 51: Revenue billion Forecast, by Mode of Operation 2020 & 2033

Table 52: Volume K Forecast, by Mode of Operation 2020 & 2033

Table 53: Revenue billion Forecast, by Type 2020 & 2033

Table 54: Volume K Forecast, by Type 2020 & 2033

Table 55: Revenue billion Forecast, by Application 2020 & 2033

Table 56: Volume K Forecast, by Application 2020 & 2033

Table 57: Revenue billion Forecast, by End User 2020 & 2033

Table 58: Volume K Forecast, by End User 2020 & 2033

Table 59: Revenue billion Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (billion) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (billion) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (billion) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (billion) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue (billion) Forecast, by Application 2020 & 2033

Table 74: Volume (K) Forecast, by Application 2020 & 2033

Table 75: Revenue (billion) Forecast, by Application 2020 & 2033

Table 76: Volume (K) Forecast, by Application 2020 & 2033

Table 77: Revenue (billion) Forecast, by Application 2020 & 2033

Table 78: Volume (K) Forecast, by Application 2020 & 2033

Table 79: Revenue billion Forecast, by Offering 2020 & 2033

Table 80: Volume K Forecast, by Offering 2020 & 2033

Table 81: Revenue billion Forecast, by Mode of Operation 2020 & 2033

Table 82: Volume K Forecast, by Mode of Operation 2020 & 2033

Table 83: Revenue billion Forecast, by Type 2020 & 2033

Table 84: Volume K Forecast, by Type 2020 & 2033

Table 85: Revenue billion Forecast, by Application 2020 & 2033

Table 86: Volume K Forecast, by Application 2020 & 2033

Table 87: Revenue billion Forecast, by End User 2020 & 2033

Table 88: Volume K Forecast, by End User 2020 & 2033

Table 89: Revenue billion Forecast, by Country 2020 & 2033

Table 90: Volume K Forecast, by Country 2020 & 2033

Table 91: Revenue (billion) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Table 93: Revenue (billion) Forecast, by Application 2020 & 2033

Table 94: Volume (K) Forecast, by Application 2020 & 2033

Table 95: Revenue (billion) Forecast, by Application 2020 & 2033

Table 96: Volume (K) Forecast, by Application 2020 & 2033

Table 97: Revenue (billion) Forecast, by Application 2020 & 2033

Table 98: Volume (K) Forecast, by Application 2020 & 2033

Table 99: Revenue (billion) Forecast, by Application 2020 & 2033

Table 100: Volume (K) Forecast, by Application 2020 & 2033

Table 101: Revenue (billion) Forecast, by Application 2020 & 2033

Table 102: Volume (K) Forecast, by Application 2020 & 2033

Table 103: Revenue billion Forecast, by Offering 2020 & 2033

Table 104: Volume K Forecast, by Offering 2020 & 2033

Table 105: Revenue billion Forecast, by Mode of Operation 2020 & 2033

Table 106: Volume K Forecast, by Mode of Operation 2020 & 2033

Table 107: Revenue billion Forecast, by Type 2020 & 2033

Table 108: Volume K Forecast, by Type 2020 & 2033

Table 109: Revenue billion Forecast, by Application 2020 & 2033

Table 110: Volume K Forecast, by Application 2020 & 2033

Table 111: Revenue billion Forecast, by End User 2020 & 2033

Table 112: Volume K Forecast, by End User 2020 & 2033

Table 113: Revenue billion Forecast, by Country 2020 & 2033

Table 114: Volume K Forecast, by Country 2020 & 2033

Table 115: Revenue (billion) Forecast, by Application 2020 & 2033

Table 116: Volume (K) Forecast, by Application 2020 & 2033

Table 117: Revenue (billion) Forecast, by Application 2020 & 2033

Table 118: Volume (K) Forecast, by Application 2020 & 2033

Table 119: Revenue (billion) Forecast, by Application 2020 & 2033

Table 120: Volume (K) Forecast, by Application 2020 & 2033

Table 121: Revenue (billion) Forecast, by Application 2020 & 2033

Table 122: Volume (K) Forecast, by Application 2020 & 2033

Table 123: Revenue (billion) Forecast, by Application 2020 & 2033

Table 124: Volume (K) Forecast, by Application 2020 & 2033

Table 125: Revenue (billion) Forecast, by Application 2020 & 2033

Table 126: Volume (K) Forecast, by Application 2020 & 2033

Table 127: Revenue (billion) Forecast, by Application 2020 & 2033

Table 128: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Our comprehensive market research methodology employs a rigorous, multi-layered approach to ensure the highest fidelity and actionable insights for the Autonomous Mobile Robots (AMR) for Semiconductor market. This robust framework integrates both primary and secondary research techniques, underpinned by sophisticated analytical models and exhaustive data validation processes, delivering an estimated data accuracy level of 85-90%. Our commitment ensures that every report is meticulously updated with the latest market intelligence up to the date of purchase.

Primary Research

Primary research forms the cornerstone of our analysis, comprising 70-80% (typically 75%) of our total research effort. This critical phase involves direct engagement with key industry stakeholders across the value chain, conducted through in-depth interviews, surveys, and expert consultations. This allows us to gather first-hand, qualitative, and quantitative insights into market dynamics, emerging trends, competitive landscapes, pricing strategies, and technological advancements.

Our primary interviews specifically target a diverse range of participants from the AMR for Semiconductor ecosystem, including:

Key Company Types Interviewed:

Autonomous Mobile Robot (AMR) Manufacturers

Semiconductor Component Suppliers (e.g., chip manufacturers providing components for AMRs)

System Integrators specializing in industrial automation and robotics

Major End-Users in Logistics & Warehousing, Automotive, and E-commerce adopting AMRs

Specific Stakeholders Interviewed:

VP of Robotics & Automation

Head of Supply Chain Optimization

Director of Operations Technology

Chief Technology Officer (CTO) in industrial automation firms

Secondary Research & Industry Benchmarking

The remaining 20-30% (typically 25%) of our research effort is dedicated to extensive secondary research. This phase involves a thorough review of published data, industry reports, company filings, and proprietary databases. We leverage a wide array of credible sources to build a foundational understanding of the market, identify key players, and cross-reference primary insights.

Government & Organizational Publications: Official reports from national statistical offices, Department of Commerce (.Gov), and other relevant government bodies. (e.g., NIST, USPTO)

Company Websites & Annual Reports: Investor presentations, financial statements, and product literature of public and private companies.

We strictly avoid using data from other market research websites to maintain the originality and integrity of our findings.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies are robust, incorporating both top-down and bottom-up approaches, followed by multi-level data triangulation. This ensures a holistic and accurate estimation of the market's current size and future potential.

Bottom-Up Approach: This method involves segmenting the market by its smallest components and aggregating them to derive the total market size. For the AMR for Semiconductor market, this includes:

Number of AMR unit shipments (segmented by type: Picking Robots, Self-driving Forklifts, etc.)

Average Selling Price (ASP) per AMR unit (differentiated by Offering: Hardware, Software & Services components)

Software & Services revenue per deployed AMR unit (considering recurring subscriptions, maintenance, and customization)

End-user industry penetration rates and expansion plans within specific applications (e.g., Picking & Sorting, Inventory Management)

Top-Down Approach: This approach begins with the total addressable market and then segments it down based on relevant factors such as end-user adoption, geographical distribution, and technological readiness. Macroeconomic indicators, industry growth rates, and regulatory frameworks are also considered.

Multi-Level Data Triangulation: All data points derived from primary and secondary research, along with the top-down and bottom-up models, are cross-referenced and validated across multiple levels. This iterative process helps in minimizing discrepancies, identifying outliers, and arriving at a highly reliable and consistent market estimate.

Data Accuracy & Quality Check

Maintaining the highest standards of data accuracy and quality is paramount to our research integrity. Our internal quality assurance protocols include:

Expert Validation: Insights and estimates are continually reviewed and validated by our panel of senior industry experts.

Statistical Analysis: Advanced statistical tools and techniques are employed to analyze raw data, identify trends, and extrapolate forecasts.

Peer Review: All research findings and methodologies undergo rigorous internal peer review to ensure objectivity and methodological soundness.

Regular Updates: As a standard practice, our market data, forecasts, and competitive landscapes are updated continually, ensuring that clients receive the most current and relevant information available at the time of purchase.

Frequently Asked Questions

1. What supply chain considerations impact AMR for Semiconductor manufacturing?

Manufacturing AMRs for semiconductor facilities relies on stable access to advanced sensors, high-precision robotics components, and specialized electronic control systems. Geopolitical shifts and raw material availability for microchips can affect production costs and lead times, as seen with recent global supply chain disruptions.

2. What are the primary barriers to entry in the AMR for Semiconductor market?

High R&D costs for specialized robotics, stringent safety standards for semiconductor cleanrooms, and the need for seamless integration with existing fab automation systems represent significant barriers. Established players like ABB and KUKA AG leverage their expertise and proprietary software to maintain competitive moats.

3. Have there been recent notable innovations or M&A in AMR for Semiconductor?

While specific recent deals are not detailed, the market sees continuous product development focused on enhanced navigation, AI-driven picking, and collaborative robotic solutions. Companies such as Körber AG and Yaskawa Electric Corporation consistently update their AMR platforms to meet evolving semiconductor manufacturing demands.

4. How did the pandemic impact the AMR for Semiconductor market, and what are the long-term shifts?

The pandemic accelerated automation adoption in semiconductor fabs to mitigate labor shortages and improve operational resilience. Long-term structural shifts include increased investment in fully autonomous systems and a greater reliance on advanced robotics for supply chain stability, contributing to a projected 15% CAGR.

5. Which region dominates the AMR for Semiconductor market, and why?

Asia-Pacific is expected to dominate the AMR for Semiconductor market, accounting for approximately 48% of the share, due to its high concentration of semiconductor manufacturing facilities and rapid investment in factory automation. Countries like China, Japan, and South Korea are key drivers of this regional leadership.

6. What are the key growth drivers for the AMR for Semiconductor market?

Increasing demand for semiconductors, the need for enhanced operational efficiency and precision in fabs, and the rising adoption of Industry 4.0 technologies are primary growth drivers. The market is propelled by applications such as transportation and inventory management within these specialized environments.