Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

DC Fans Market: $14.5B Valuation with 7.82% CAGR

DC Fans

DC Fans Market: $14.5B Valuation with 7.82% CAGR

DC Fans by Application (Residential, Commercial, Industrial, Other), by Types (220-762mm, 763-1219mm, 1220-3000mm, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 11, 2026|Base Year : 2025|Pages : 126

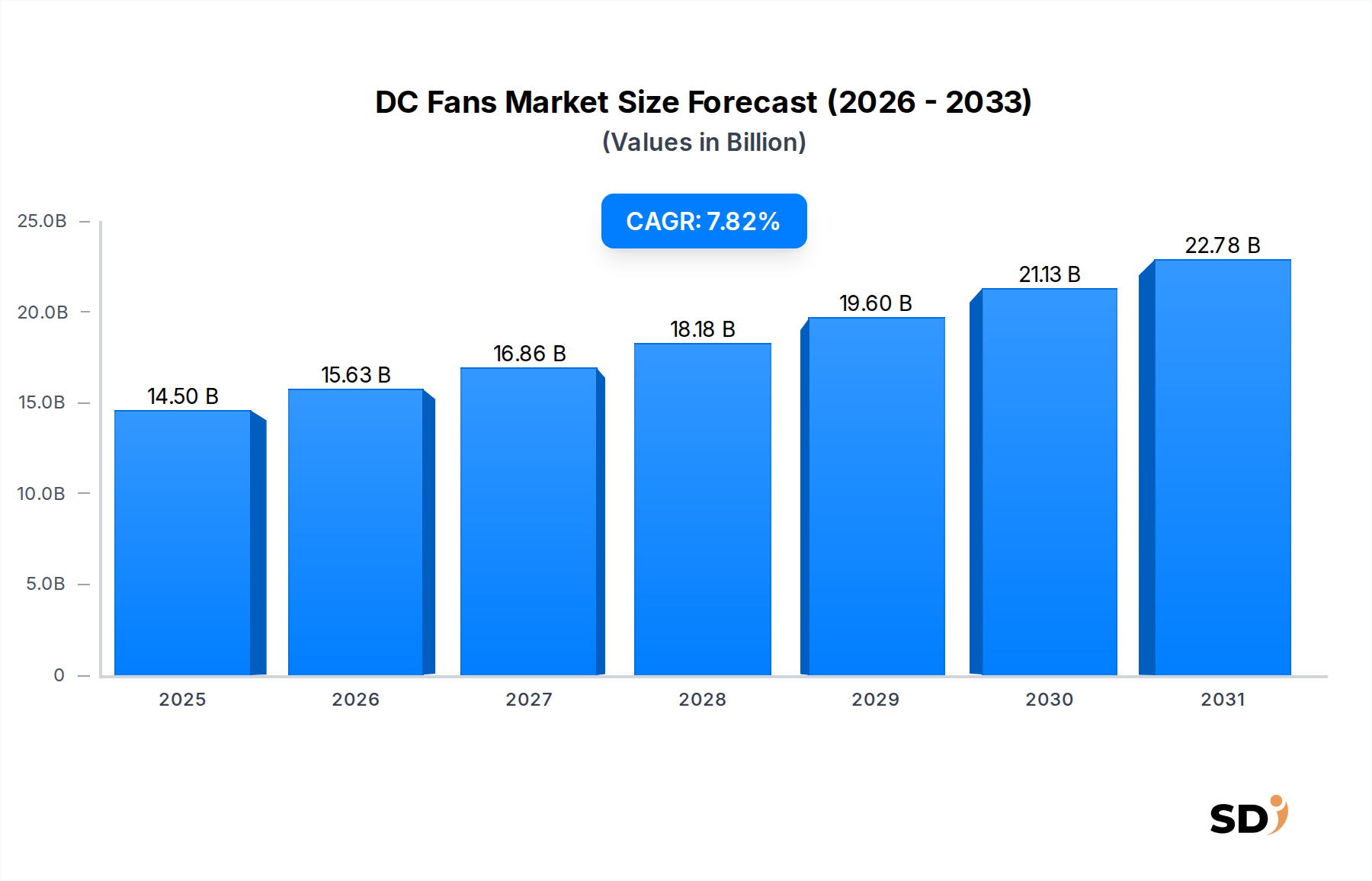

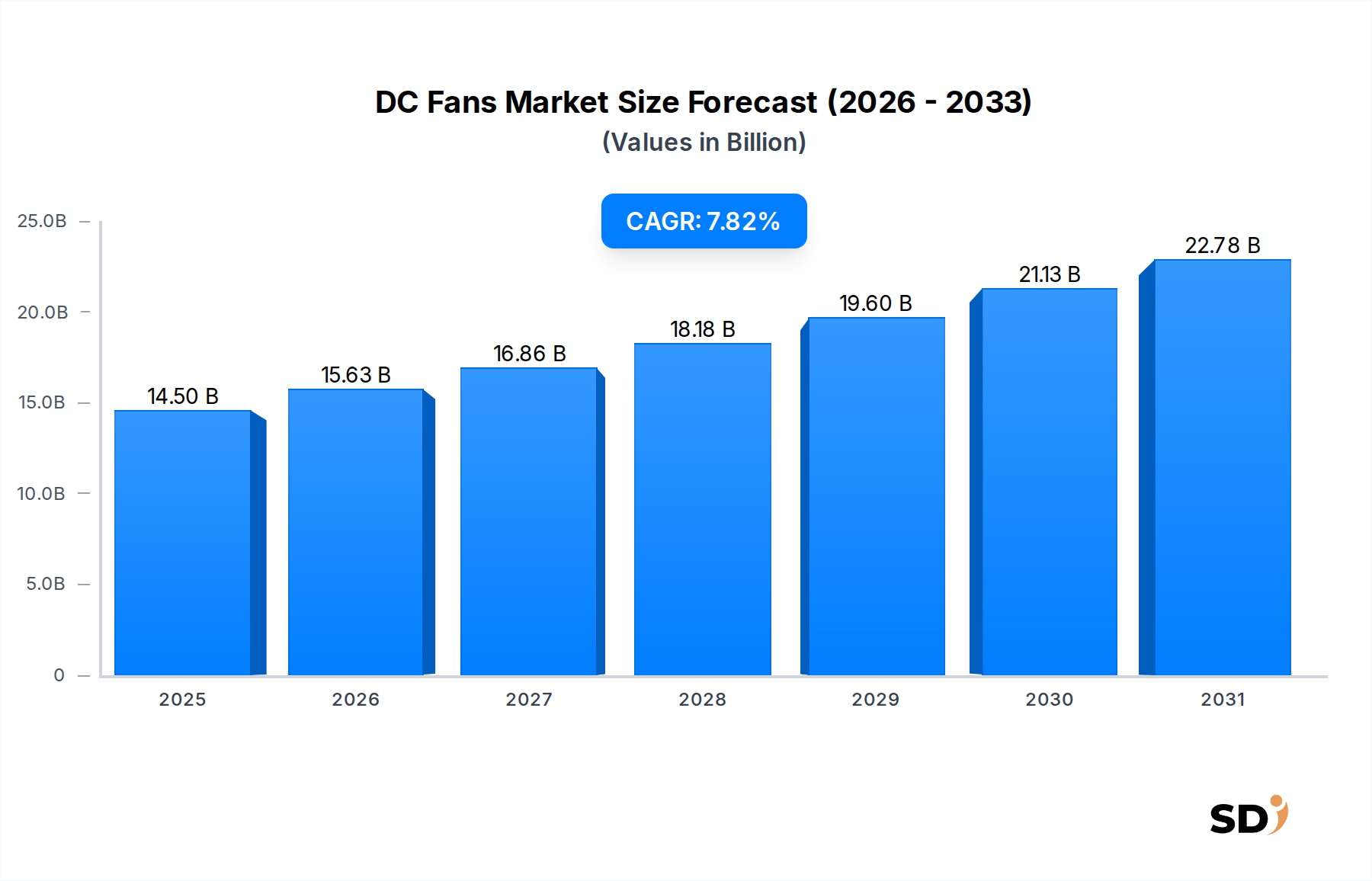

The Global DC Fans Market is currently valued at an estimated $14,500.75 million in 2024, exhibiting robust expansion driven by escalating demand across diverse end-use sectors. Projections indicate a substantial growth trajectory, forecasting the market to reach approximately $30,779.6 million by 2034, propelled by a compound annual growth rate (CAGR) of 7.82% over the forecast period. This significant growth is underpinned by several critical demand drivers and macro-economic tailwinds. Foremost among these is the pervasive trend of miniaturization and increasing power density in electronic devices, necessitating efficient and compact cooling solutions. The rapid proliferation of data centers and cloud computing infrastructure globally represents another pivotal accelerator, with these facilities requiring vast arrays of reliable and energy-efficient DC fans for optimal server performance and longevity. Furthermore, the burgeoning electric vehicle (EV) sector, coupled with advancements in automotive electronics, is fueling demand for specialized DC fans for battery cooling, cabin ventilation, and onboard system thermal management.

DC Fans Market Size (In Billion)

25.0B

20.0B

15.0B

10.0B

5.0B

0

14.50 B

2025

15.63 B

2026

16.86 B

2027

18.18 B

2028

19.60 B

2029

21.13 B

2030

22.78 B

2031

Technological advancements in fan design, material science, and motor control—particularly within the Brushless DC Motors Market—are enhancing the efficiency, reducing noise levels, and extending the lifespan of DC fans, thereby expanding their applicability. Regulatory mandates for energy efficiency across industrial and commercial sectors further stimulate the adoption of high-performance DC fan systems over conventional AC alternatives due to their superior power conversion efficiency and precise speed control capabilities. The increasing sophistication of industrial automation and robotics also contributes significantly to market growth, as these advanced systems rely on dependable cooling solutions to maintain operational integrity in demanding environments. Geographically, Asia Pacific is anticipated to maintain its dominance and register the fastest growth, largely due to its robust manufacturing base for electronics and burgeoning industrial sector. The overall outlook for the DC Fans Market remains highly optimistic, characterized by continuous innovation in smart fan technologies, integration with IoT ecosystems for predictive maintenance, and a sustained focus on energy conservation, positioning DC fans as indispensable components in the evolving digital and industrial landscapes."

The 'Industrial' application segment is identified as the single largest by revenue share within the broader DC Fans Market, exhibiting sustained growth and commanding a significant portion of the total market valuation. This dominance is primarily attributed to the critical and varied requirements for precise thermal management in industrial machinery, control panels, manufacturing processes, and specialized equipment. DC fans are integral to maintaining optimal operating temperatures for sensitive electronics and mechanical components in factory automation systems, power generation equipment, telecommunication infrastructure, and medical devices. The demand stems from the necessity to ensure operational reliability, prevent overheating-induced failures, and extend the lifespan of high-value industrial assets.

Within the industrial sphere, sectors such as manufacturing, energy, and heavy machinery frequently deploy large-scale DC fan solutions, including those in the 1220-3000mm 'Types' segment, to manage heat dissipation effectively. The increasing adoption of advanced robotics and smart manufacturing initiatives, integral to the Industrial Automation Market, further solidifies the 'Industrial' segment's leading position. These applications demand high-performance, robust, and often customized DC fans that can withstand harsh operating conditions, including exposure to dust, vibrations, and extreme temperatures, while delivering consistent airflow and static pressure. Key players such as Delta, Ebmpapst, and Nidec Corporation are prominent in this segment, offering a comprehensive portfolio of industrial-grade DC fans engineered for reliability and energy efficiency.

Moreover, the evolution of industrial IoT (IIoT) and the proliferation of advanced sensor technologies are driving the integration of 'smart' DC fans capable of dynamic speed control based on real-time temperature data, further enhancing energy efficiency and predictive maintenance capabilities. This trend aligns with the broader demand for sustainable and intelligent manufacturing processes. The high upfront investment in industrial machinery and the associated costs of downtime due to thermal issues underscore the importance of reliable cooling, thereby reinforcing the market dominance of the 'Industrial' application segment. Its share is not only growing but also consolidating, as manufacturers continuously innovate to meet increasingly stringent performance and efficiency standards demanded by modern industrial applications, including those within the Power Electronics Market where precise temperature regulation is paramount for component stability and operational safety. This segment's consistent need for robust, high-performance cooling solutions ensures its enduring leadership in the DC Fans Market."

The trajectory of the DC Fans Market is significantly shaped by several compelling drivers, each contributing to its expansive growth. A primary driver is the accelerating trend of miniaturization and power density increases in electronic components. As devices, from smartphones to servers, become smaller yet more powerful, they generate more heat in confined spaces. This necessitates highly efficient, compact DC fans capable of dissipating heat effectively without increasing the device footprint or energy consumption. For instance, the robust expansion of the Consumer Electronics Market, particularly in high-performance laptops, gaming consoles, and smart home devices, directly correlates with the demand for advanced DC fan solutions that offer optimal thermal management in increasingly compact designs.

Secondly, the global expansion of data centers and cloud computing infrastructure is a monumental driver. Data centers are energy-intensive facilities that rely heavily on sophisticated cooling systems to maintain the operational integrity of thousands of servers. DC fans are preferred for their energy efficiency, precise control, and longer lifespan compared to AC alternatives in these critical environments. The continuous growth of data traffic and cloud services translates directly into a persistent demand for high-capacity, fault-tolerant DC fans, significantly boosting the Data Center Cooling Market. Industry reports indicate that global data center IP traffic is projected to double every few years, directly amplifying the need for efficient cooling solutions.

Thirdly, stringent energy efficiency regulations and sustainability initiatives globally are fostering the adoption of DC fans. With increasing emphasis on reducing carbon footprints and operational costs, industries are transitioning from less efficient AC fans to Electronically Commutated (EC) DC fans. These fans offer superior energy savings, precise speed control, and reduced noise levels, aligning with green building standards and industrial efficiency mandates. This regulatory push is observed across various sectors, including the HVAC Systems Market, where DC fans are increasingly integrated into air handling units and ventilation systems for enhanced performance and lower energy consumption.

Finally, the rapid advancements in the Automotive Electronics Market, particularly with the proliferation of Electric Vehicles (EVs), present a significant growth impetus. EVs demand dedicated thermal management systems for their battery packs, power electronics, and cabin climate control, where DC fans offer the necessary precision, efficiency, and reliability in challenging automotive environments. As global EV adoption rates continue to climb, so too does the demand for specialized DC fans, often designed to meet rigorous automotive industry standards for vibration, temperature, and lifespan."

The DC Fans Market features a dynamic competitive landscape, characterized by a mix of established global players and specialized regional manufacturers, all vying for market share through product innovation, strategic partnerships, and expanded distribution networks. Key companies are constantly developing more efficient, quieter, and smarter fan solutions to meet the evolving demands of diverse end-use applications.

YS Tech: A prominent manufacturer known for its wide range of cooling fans and blowers, specializing in thermal solutions for IT, telecom, and industrial applications, with a focus on high-performance and reliable products.

Nidec Corporation: A global leader in motor manufacturing, Nidec offers an extensive portfolio of DC fans and blowers, leveraging its core motor technology expertise to deliver highly efficient and compact cooling solutions across various industries, including automotive and consumer electronics.

Pelonis Technologies: Specializes in custom-engineered thermal management solutions, including DC fans, blowers, and heaters, catering to medical, industrial, and defense sectors with a strong emphasis on quality and tailored performance.

Hidria: An international group recognized for its development and production of high-tech solutions for automotive, industrial, and building technologies, including advanced motor components and ventilation systems incorporating DC fan technology.

Mechatronics Fan Group: A provider of high-quality AC and DC axial and centrifugal fans, known for offering customized thermal solutions for demanding industrial, medical, and telecommunications equipment, with a focus on long-life and robust designs.

NMB Technologies: A subsidiary of MinebeaMitsumi Inc., NMB Technologies is a major global supplier of miniature ball bearings, motors, and cooling fans, delivering precision-engineered DC fans for various applications including data centers and consumer devices.

Allied Electronics: As a major distributor of industrial electronic components, Allied Electronics provides a broad selection of DC fans from various manufacturers, serving as a critical supply channel for businesses seeking readily available thermal management solutions.

Oriental Motor: A leading manufacturer of motion control systems and fractional horsepower motors, Oriental Motor offers a range of cooling fans and accessories that integrate seamlessly with their broader automation product lines, focusing on industrial reliability.

ADDA Corp: Known for its comprehensive range of DC axial fans and blowers, ADDA Corp serves diverse industries from computing to home appliances, emphasizing cost-effectiveness and mass-production capabilities.

Sinwan Fans: A manufacturer with a focus on cooling fans for various electronic applications, providing solutions tailored for PC, server, and other general electronics cooling needs.

Ebmpapst: A global market leader in fans and motors, Ebmpapst specializes in energy-efficient EC (Electronically Commutated) DC fans and blower solutions for HVAC, refrigeration, and industrial applications, renowned for their advanced aerodynamics and quiet operation.

COPPUS: Primarily known for its industrial ventilation and portable cooling equipment, COPPUS offers robust fans suitable for challenging industrial environments, often employing powerful DC motor technology for demanding air movement.

Crown Electronics: A supplier of various electronic components, including DC fans, catering to a range of industries with a focus on offering reliable and cost-effective cooling solutions.

Comair Rotron: A long-standing manufacturer of AC and DC axial fans, blowers, and specialty cooling products, Comair Rotron provides thermal management solutions for demanding military, aerospace, and industrial applications.

Marsh Electronics: A distributor of electronic components, Marsh Electronics supplies DC fans from numerous manufacturers, supporting OEMs and end-users with a wide selection of cooling solutions.

Humidin & Casilica: This entity likely specializes in environmental control solutions, potentially integrating DC fans within their dehumidification and air quality management systems.

Sofasco: An ISO-certified manufacturer of AC and DC fans and accessories, Sofasco provides cooling solutions for diverse applications, including industrial, telecom, and medical, with an emphasis on quality and performance.

Delta: A global provider of power and thermal management solutions, Delta is a major player in the DC fan market, offering a vast array of high-performance and energy-efficient fans and blowers for IT, industrial, and automotive applications.

Sunon: A leading brand in cooling fan and thermal module solutions, Sunon is known for its innovative designs, compact form factors, and quiet operation, serving the consumer electronics, IT, and automotive industries.

Sanju International Electric Machinery: Focuses on manufacturing various fan products, likely including DC fans, catering to general industrial and commercial ventilation needs."

"## Recent Developments & Milestones in the DC Fans Market

Recent years have seen continuous innovation and strategic initiatives shaping the DC Fans Market, driven by evolving demands for efficiency, connectivity, and environmental sustainability. These developments underscore the dynamic nature of the industry and its commitment to meeting the thermal management challenges of modern electronics and industrial systems.

January 2024: Leading manufacturers introduced next-generation smart DC fans integrating advanced sensor technology and predictive analytics capabilities. These fans are designed for proactive thermal management, communicating real-time performance data to prevent system overheating in critical applications like data centers.

October 2023: A major component supplier launched a new series of ultra-thin DC micro fans specifically engineered for compact, high-performance computing devices and augmented reality (AR) headsets, addressing the persistent demand for miniaturization in the Consumer Electronics Market.

August 2023: Several industry players announced collaborations aimed at developing DC fans with enhanced acoustic performance, specifically targeting noise reduction for residential and commercial HVAC Systems Market applications without compromising airflow.

May 2023: Developments in sustainable manufacturing processes for DC fan components gained traction, with companies investing in recyclable materials for fan housings and blades, aligning with broader corporate sustainability goals and circular economy principles.

February 2023: Advancements in Brushless DC Motors Market technology led to the introduction of DC fans with significantly improved energy efficiency ratios, capable of reducing power consumption by up to 20% compared to previous generations, appealing to energy-conscious industrial clients.

November 2022: A strategic partnership was formed between a DC fan manufacturer and a specialized provider of Artificial Intelligence (AI) solutions to optimize fan speed control algorithms, leading to more adaptive and responsive cooling in dynamic operational environments.

July 2022: New product lines featuring ruggedized DC fans were unveiled, specifically designed to withstand extreme temperatures, dust, and vibration, targeting the growing demands of outdoor telecom equipment and industrial automation systems."

"## Regional Market Breakdown for DC Fans Market

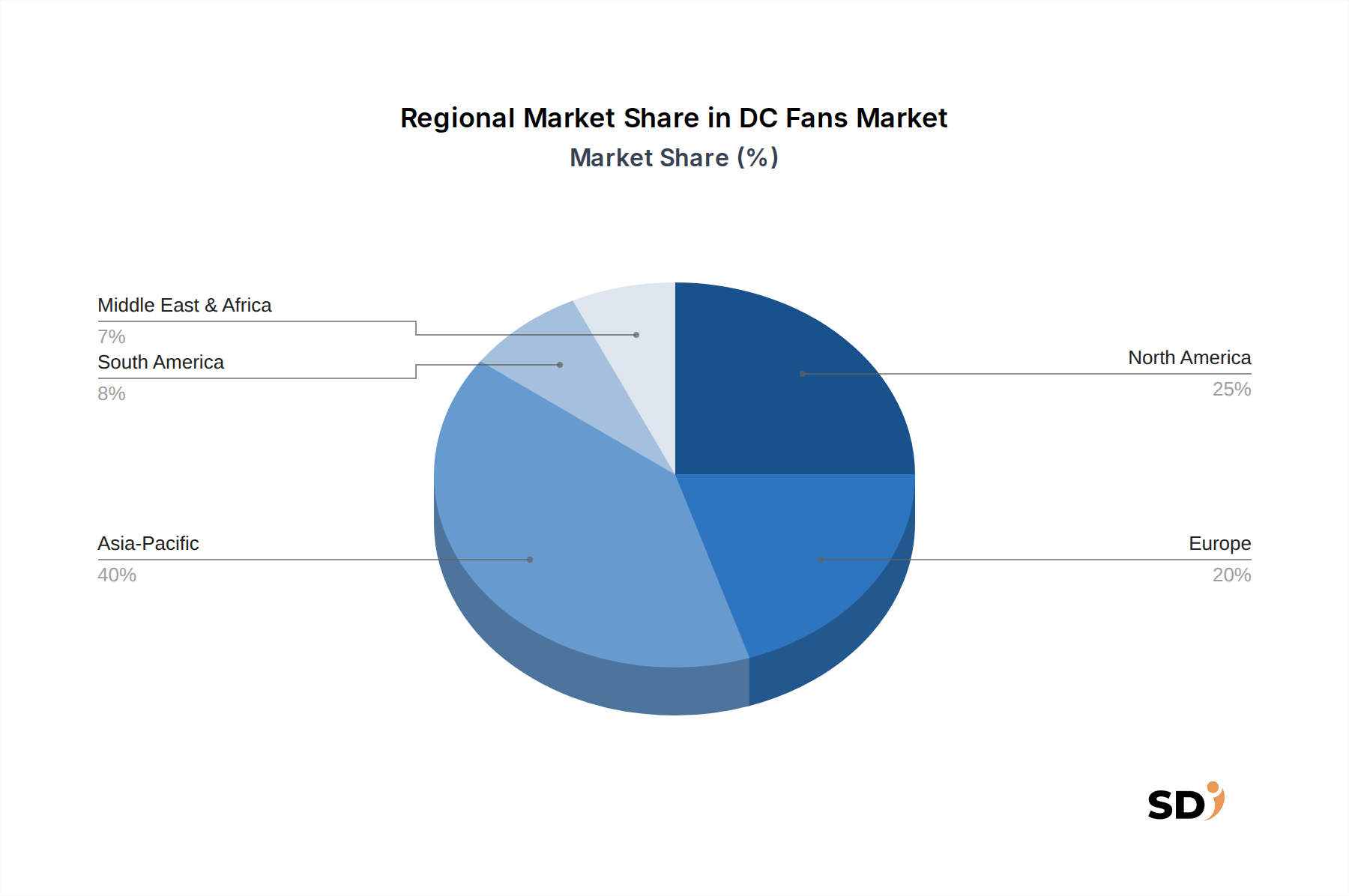

The Global DC Fans Market exhibits a heterogeneous regional distribution, with distinct growth drivers and market dynamics across key geographical areas. Analyzing these regional contributions provides critical insights into the global market's structure and future trajectory.

Asia Pacific currently stands as the dominant region in the DC Fans Market and is projected to register the fastest growth over the forecast period. This preeminence is primarily fueled by the region's robust electronics manufacturing base, particularly in countries like China, South Korea, Japan, and Taiwan, which are major producers of consumer electronics, automotive components, and IT hardware. Furthermore, the rapid expansion of data centers, driven by burgeoning digital transformation and cloud adoption in economies such as China and India, significantly contributes to demand within the Data Center Cooling Market. Industrialization and urbanization across emerging economies also bolster the need for DC fans in industrial automation and commercial infrastructure projects. The availability of low-cost labor and raw materials further enhances the competitive advantage of manufacturers in this region.

North America holds a substantial share of the DC Fans Market, characterized by a mature technology infrastructure and high adoption rates of advanced cooling solutions. The region's demand is largely driven by its extensive network of hyperscale data centers, robust automotive industry (including a strong push for EVs), and significant investments in industrial automation and advanced manufacturing. Strict energy efficiency regulations also promote the adoption of high-performance DC fans, with innovation often centered on smart and integrated thermal management systems. The presence of key technology developers and early adopters fuels continuous market evolution.

Europe represents a significant market, distinguished by a strong emphasis on energy efficiency, environmental regulations, and advanced engineering. Countries like Germany, France, and the UK are at the forefront of adopting high-efficiency DC fan technologies, particularly within the HVAC Systems Market and renewable energy sectors. The region's mature industrial base and focus on precision engineering, including advanced medical devices and industrial machinery, necessitate reliable and quiet DC fan solutions. Innovation in compact and low-noise fan designs is a key regional driver.

Middle East & Africa (MEA) and South America are emerging markets for DC fans, experiencing considerable growth, albeit from a smaller base. Growth in MEA is driven by infrastructure development, investment in IT and telecom sectors, and industrial diversification initiatives, particularly in the GCC countries. South America's market expansion is linked to industrialization, urbanization, and increasing foreign investment in manufacturing and data infrastructure. While these regions typically have higher price sensitivity, the growing need for reliable cooling in new commercial and industrial installations is steadily increasing demand for cost-effective and durable DC fan solutions."

The DC Fans Market's supply chain is a complex network, highly dependent on the availability and price stability of key raw materials and sophisticated components. Upstream dependencies include various metals, plastics, and electronic sub-components, each subject to its own market dynamics and geopolitical influences.

Key raw materials critical to DC fan manufacturing include copper for motor windings, various polymer resins (such as PBT, PC, and ABS) for fan blades and housings, and rare earth elements like neodymium and samarium-cobalt for permanent magnets in Brushless DC Motors Market. The price of copper, often traded on global commodity exchanges, has historically shown significant volatility. For example, periods of strong global economic growth or supply disruptions can lead to sharp increases in the Copper Wire Market, directly impacting the manufacturing cost of DC motors and, by extension, DC fans. Similarly, the availability and pricing of rare earth magnets, predominantly sourced from a few geographical regions, pose a significant sourcing risk due to potential geopolitical tensions or export restrictions. Price trends for these magnets have also shown periods of sharp increases in response to demand surges from the electric vehicle and renewable energy sectors.

Beyond raw materials, the supply chain is heavily reliant on the consistent availability of semiconductor devices, including motor drivers and control ICs. The global semiconductor shortage experienced from 2020 to 2022 demonstrated the vulnerability of this dependency, leading to production delays, increased lead times, and inflated component costs for DC fan manufacturers. This highlighted the necessity for diversified sourcing strategies and closer collaboration with semiconductor suppliers.

Overall, the supply chain for the DC Fans Market has historically been susceptible to disruptions from natural disasters, trade policy shifts, and global health crises, such as the COVID-19 pandemic. These events have led to factory closures, port congestion, and increased logistics costs, all of which trickle down to affect manufacturing schedules and final product pricing. Manufacturers are increasingly focusing on supply chain resilience through strategies like dual-sourcing, regionalization of production, and closer inventory management to mitigate future risks and ensure continuous product availability in the face of fluctuating raw material prices and potential component shortages."

The DC Fans Market serves a diverse range of end-users, each with distinct purchasing criteria and procurement strategies. Understanding these customer segments and their evolving buying behaviors is crucial for manufacturers to tailor product offerings and market approaches effectively.

Original Equipment Manufacturers (OEMs) form the largest customer segment. This includes manufacturers of consumer electronics, automotive components, industrial machinery, and telecommunication infrastructure. For OEMs, key purchasing criteria revolve around performance metrics (airflow, static pressure), energy efficiency, reliability, physical dimensions (compactness), and acoustics (noise levels). Price sensitivity is high, particularly in the Consumer Electronics Market where cost-efficiency is paramount for competitive product pricing. OEMs typically procure DC fans in large volumes directly from manufacturers or through authorized distributors, often requiring customization or specific certifications to integrate seamlessly into their proprietary systems.

System Integrators (SIs) and Contractors constitute another significant segment, particularly in sectors such as Data Center Cooling Market and HVAC Systems Market. SIs focus on overall system performance, ease of integration, and long-term maintenance. Their purchasing decisions are driven by factors like fan lifespan, availability of smart features (PWM control, alarm signals), and compliance with industry standards. They may also value bundled solutions and technical support from fan manufacturers. Procurement for this segment often involves project-based purchasing, with considerations for lead times and scalability.

Aftermarket and Replacement Buyers represent a continuous demand stream, encompassing repair services, maintenance departments, and individual consumers replacing faulty fans. For this segment, immediate availability, compatibility with existing systems, and cost-effectiveness are primary drivers. They typically source through distributors, online retailers, or local electronic component suppliers.

Recent cycles have shown notable shifts in buyer preference across all segments. There is an increasing demand for smarter, connected DC fans capable of real-time monitoring and dynamic speed adjustments, driven by the broader trend towards IoT and Industry 4.0. Energy efficiency remains a paramount concern, pushing demand for Electronically Commutated (EC) DC fans. Furthermore, lower acoustic noise is becoming a critical differentiating factor, especially in consumer devices, medical equipment, and office environments. Sustainability considerations, including the use of recyclable materials and adherence to environmental regulations, are also starting to influence procurement decisions, particularly among larger corporate buyers seeking to enhance their environmental, social, and governance (ESG) profiles.

"## Application Segment Dominance in the DC Fans Market

"## Key Market Drivers for the DC Fans Market

"## Competitive Ecosystem of the DC Fans Market

"## Supply Chain & Raw Material Dynamics for DC Fans Market

"## Customer Segmentation & Buying Behavior in DC Fans Market

DC Fans Segmentation

1. Application

1.1. Residential

1.2. Commercial

1.3. Industrial

1.4. Other

2. Types

2.1. 220-762mm

2.2. 763-1219mm

2.3. 1220-3000mm

2.4. Other

DC Fans Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

DC Fans REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 7.82% from 2020-2034

Segmentation

By Application

Residential

Commercial

Industrial

Other

By Types

220-762mm

763-1219mm

1220-3000mm

Other

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Residential

5.1.2. Commercial

5.1.3. Industrial

5.1.4. Other

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. 220-762mm

5.2.2. 763-1219mm

5.2.3. 1220-3000mm

5.2.4. Other

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Residential

6.1.2. Commercial

6.1.3. Industrial

6.1.4. Other

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. 220-762mm

6.2.2. 763-1219mm

6.2.3. 1220-3000mm

6.2.4. Other

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Residential

7.1.2. Commercial

7.1.3. Industrial

7.1.4. Other

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. 220-762mm

7.2.2. 763-1219mm

7.2.3. 1220-3000mm

7.2.4. Other

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Residential

8.1.2. Commercial

8.1.3. Industrial

8.1.4. Other

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. 220-762mm

8.2.2. 763-1219mm

8.2.3. 1220-3000mm

8.2.4. Other

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Residential

9.1.2. Commercial

9.1.3. Industrial

9.1.4. Other

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. 220-762mm

9.2.2. 763-1219mm

9.2.3. 1220-3000mm

9.2.4. Other

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Residential

10.1.2. Commercial

10.1.3. Industrial

10.1.4. Other

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. 220-762mm

10.2.2. 763-1219mm

10.2.3. 1220-3000mm

10.2.4. Other

11. Competitive Analysis

11.1. Company Profiles

11.1.1. YS Tech

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Nidec Corporation

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Pelonis Technologies

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Hidria

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Mechatronics Fan Group

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. NMB Technologies

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Allied Electronics

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Oriental Motor

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. ADDA Corp

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Sinwan Fans

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Ebmpapst

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. COPPUS

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. Crown Electronics

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.1.14. Comair Rotron

11.1.14.1. Company Overview

11.1.14.2. Products

11.1.14.3. Company Financials

11.1.14.4. SWOT Analysis

11.1.15. Marsh Electronics

11.1.15.1. Company Overview

11.1.15.2. Products

11.1.15.3. Company Financials

11.1.15.4. SWOT Analysis

11.1.16. Humidin & Casilica

11.1.16.1. Company Overview

11.1.16.2. Products

11.1.16.3. Company Financials

11.1.16.4. SWOT Analysis

11.1.17. Sofasco

11.1.17.1. Company Overview

11.1.17.2. Products

11.1.17.3. Company Financials

11.1.17.4. SWOT Analysis

11.1.18. Delta

11.1.18.1. Company Overview

11.1.18.2. Products

11.1.18.3. Company Financials

11.1.18.4. SWOT Analysis

11.1.19. Sunon

11.1.19.1. Company Overview

11.1.19.2. Products

11.1.19.3. Company Financials

11.1.19.4. SWOT Analysis

11.1.20. Sanju International Electric Machinery

11.1.20.1. Company Overview

11.1.20.2. Products

11.1.20.3. Company Financials

11.1.20.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (million), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (million), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (million), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (million), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (million), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (million), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (million), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (million), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (million), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (million), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (million), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Revenue million Forecast, by Types 2020 & 2033

Table 3: Revenue million Forecast, by Region 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Types 2020 & 2033

Table 6: Revenue million Forecast, by Country 2020 & 2033

Table 7: Revenue (million) Forecast, by Application 2020 & 2033

Table 8: Revenue (million) Forecast, by Application 2020 & 2033

Table 9: Revenue (million) Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Application 2020 & 2033

Table 11: Revenue million Forecast, by Types 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Types 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Revenue (million) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue million Forecast, by Application 2020 & 2033

Table 29: Revenue million Forecast, by Types 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue million Forecast, by Application 2020 & 2033

Table 38: Revenue million Forecast, by Types 2020 & 2033

Table 39: Revenue million Forecast, by Country 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our robust research methodology places a significant emphasis on primary research, comprising approximately 75% of our total market insights. This approach ensures deep qualitative and quantitative understanding, drawing directly from key market participants across the value chain. Our extensive network of industry contacts allows for comprehensive data validation and the capture of nuanced market dynamics.

Targeted Stakeholders Interviewed:

VP of Engineering / R&D Director (Fan Manufacturers, OEM Integrators)

Head of Procurement / Supply Chain Manager (OEM Integrators, Large Distributors)

Product Line Manager / Business Development Manager (Fan Manufacturers, Component Suppliers)

Facilities Manager / Operations Director (Large Residential/Commercial/Industrial End-Users)

Company Types Engaged:

DC Fan Manufacturers (e.g., producing axial, centrifugal, or cross-flow fans for various applications)

OEM Integrators (e.g., manufacturers of HVAC systems, automotive electronics, data center servers, industrial machinery that embed DC fans)

Component Suppliers (e.g., motor manufacturers, bearing suppliers, controller board providers specific to DC fans)

Specialized Distributors and Wholesalers (e.g., focused on industrial components, electronic parts, or HVAC supplies)

Large-Scale End-Use Application Operators (e.g., Data Center operators, industrial automation firms, commercial building management groups)

Interviews are conducted through structured questionnaires, in-depth discussions, and qualitative surveys, meticulously designed to elicit critical insights on market trends, competitive landscape, technological advancements, pricing strategies, and future outlook specific to the DC Fans market across its defined applications, types, and geographies.

Secondary Research & Industry Benchmarking

Complementing our primary research, the remaining ~25% of our market insights are derived from rigorous secondary research. This phase involves extensive data collection from credible, publicly available sources to establish a foundational understanding and corroborate primary findings. Our strategy deliberately excludes data from other market research websites to ensure originality and mitigate potential biases.

Key Databases & Sources Leveraged:

Financial Databases: Bloomberg, Factiva, Hoovers, PitchBook for company financials, investment trends, and competitive intelligence.

Government Publications: Official statistics, energy consumption reports, manufacturing output data from country-specific .Gov websites (e.g., U.S. Department of Energy, EU statistical offices).

Non-Profit Organizations & Academic Journals: Research papers, whitepapers, and reports from recognized .org institutions focusing on electronics, HVAC, and industrial engineering.

Industry & Trade Associations: Reports, standards, and statistical data from globally recognized bodies relevant to the DC fan market. Examples include:

ASHRAE: American Society of Heating, Refrigerating and Air-Conditioning Engineers (for HVAC and building systems standards).

AMCA International: Air Movement and Control Association International (specifically for air movement and control equipment, including fans).

IEC: International Electrotechnical Commission (for international standards concerning electrical, electronic and related technologies).

IEEE: Institute of Electrical and Electronics Engineers (for advancements in electrical engineering, electronics, and related technologies).

Data collected is rigorously cross-referenced, synthesized, and analyzed to construct a comprehensive market landscape and identify key industry benchmarks.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies employ a hybrid approach, integrating both top-down and bottom-up analyses alongside multi-level data triangulation to ensure robustness and accuracy.

Top-down Approach: This involves assessing the overall market size based on macroeconomic indicators (e.g., GDP growth, industrial production indices, construction spending), relevant industry-level trends (e.g., growth in data center deployments, smart home adoption, industrial automation investments), and regional economic outlooks. The total addressable market for DC fans is then disaggregated by application, type, and geography.

Bottom-up Approach: This granular approach involves aggregating micro-level data points to build the market size from its constituent parts. This includes:

Unit Shipments by Type & Application: Calculating the number of DC fans shipped annually for each specific type (e.g., 220-762mm, 763-1219mm, etc.) across various applications (residential, commercial, industrial, other) and regions.

Average Selling Price (ASP): Determining the weighted average selling price for different fan types, considering variations based on size, performance, features (e.g., smart controls), and end-use application segments.

Installed Base & Replacement Cycles: Estimating the existing installed base of equipment utilizing DC fans (e.g., HVAC units, servers, machinery) and factoring in typical replacement cycles to project future demand.

Production Capacities & Utilization Rates: Analyzing the manufacturing capacities and utilization rates of leading DC fan manufacturers and their suppliers to gauge supply-side potential and constraints.

Multi-level data triangulation, involving comparison and validation of data points from various primary and secondary sources, is continuously applied throughout the demand modeling process. Sophisticated statistical and econometric models are utilized for forecasting, taking into account historical trends, market drivers, restraints, opportunities, and the competitive landscape. Our reports are meticulously updated up to the date of purchase to reflect the latest market conditions and emerging trends, ensuring the most current insights for our clients.

Data Accuracy & Quality Check

Ensuring the highest level of data integrity and analytical rigor is paramount. We guarantee an estimated data accuracy level of 85-90% for our market estimations. This high standard is achieved through a multi-stage validation and quality control process:

Validation: All data points, market sizes, and forecasts undergo stringent validation against multiple independent sources, expert opinions, and historical trends. Any discrepancies are investigated and resolved through further primary research or re-evaluation of assumptions.

Peer Review: The entire research process, including methodology design, data collection, analysis, and report drafting, is subjected to internal peer review by senior analysts to identify and correct potential errors or biases.

Quality Control: Our robust quality control mechanism involves cross-checking calculations, logical consistency, and coherence of market narratives. This iterative process ensures that all findings are robust, reliable, and actionable for strategic decision-making.

Frequently Asked Questions

1. How has the DC fans market responded to post-pandemic shifts and long-term trends?

The DC fans market saw increased demand post-pandemic due to accelerated digital transformation and data center expansion. This has driven a long-term structural shift towards energy-efficient and compact fan solutions, contributing to a 7.82% CAGR.

2. What disruptive technologies or emerging substitutes impact the DC fan market?

While direct substitutes are limited for many critical applications, passive cooling advancements and liquid cooling solutions offer alternative thermal management in specific niches. Miniaturization trends and integrated cooling modules also influence DC fan design and functionality from key players like Nidec Corporation.

3. What are the primary challenges or supply-chain risks facing the DC fans market?

Key challenges include fluctuating raw material costs, notably for components like copper and specialized magnets, alongside ongoing global supply chain disruptions. Geopolitical factors also influence trade and production for major manufacturers such as Delta and Ebmpapst.

4. Which key segments drive demand for DC fans?

Significant demand originates from industrial and commercial applications, particularly for cooling electronics in machinery, data centers, and HVAC systems. The market includes various fan types, from 220-762mm for consumer devices to over 1220mm for heavy industrial equipment.

5. How do export-import dynamics influence the global DC fans market?

Asia-Pacific, as a major manufacturing hub, largely drives global DC fan exports to meet demand in regions like North America and Europe. International trade policies and tariffs significantly impact pricing and supply chain efficiency for components and finished products.

6. Why is the DC fans market experiencing robust growth drivers?

Growth at a 7.82% CAGR is driven by the expanding consumer electronics sector, surging data center construction, and the increasing adoption of IoT devices requiring advanced thermal solutions. The market is projected to reach $14.5 billion by 2034, fueled by these consistent technological advancements.