Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Direct Laser Writers Market: 5.3% CAGR & Key Regional Shares

Direct Laser Writers

Direct Laser Writers Market: 5.3% CAGR & Key Regional Shares

Direct Laser Writers by Application (Industrial, Laboratory, Others), by Types (Desktop, Vertical), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 16, 2026|Base Year : 2025|Pages : 90

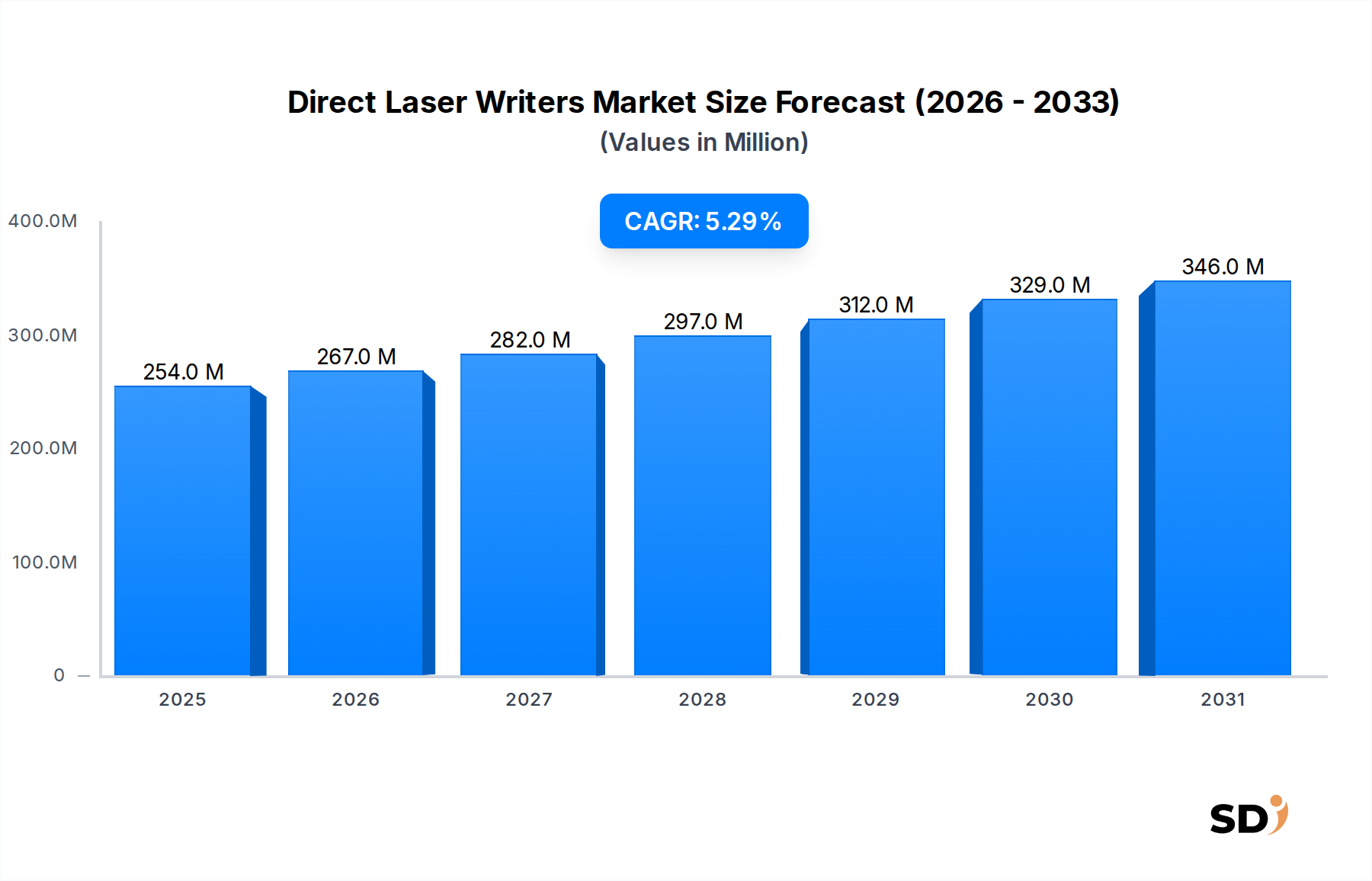

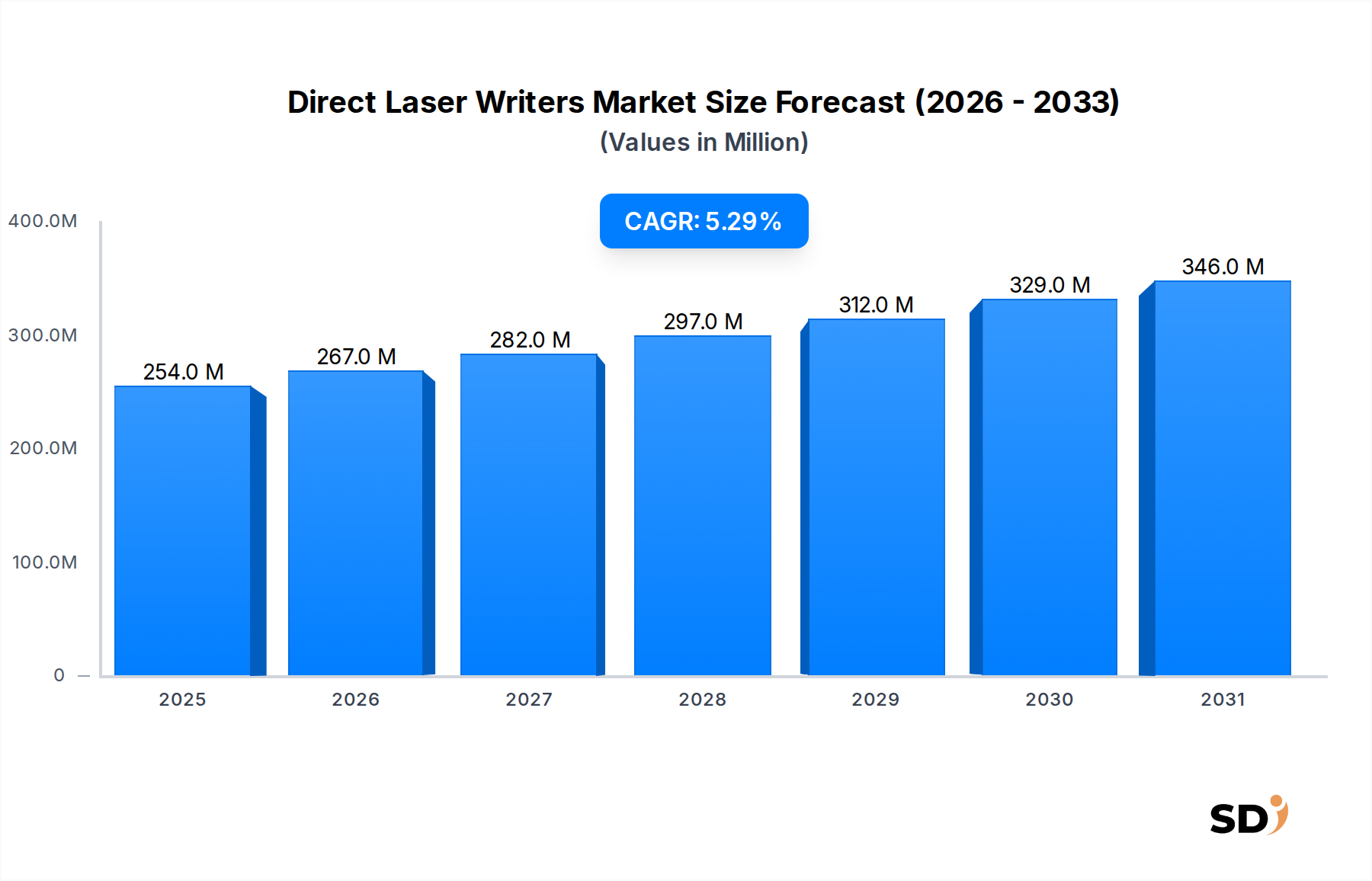

The Direct Laser Writers Market is witnessing robust expansion driven by an escalating demand for high-precision patterning and additive manufacturing across various advanced technology sectors. Valued at an estimated $254 million in 2023, the market is poised for significant growth, projected to reach approximately $364.5 million by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 5.3% over the forecast period. This trajectory is primarily fueled by rapid advancements in microelectronics, photonics, and biomedical research, where the capability to create intricate 2D and 3D structures at micro- and nano-scales is paramount. The miniaturization trend in electronic components and the increasing complexity of optical devices are key demand catalysts, reinforcing the indispensability of direct laser writing technologies. Furthermore, the burgeoning requirement for rapid prototyping and custom fabrication in academic and industrial laboratories significantly contributes to market expansion, notably impacting the Research & Development Market.

Direct Laser Writers Market Size (In Million)

400.0M

300.0M

200.0M

100.0M

0

254.0 M

2025

267.0 M

2026

282.0 M

2027

297.0 M

2028

312.0 M

2029

329.0 M

2030

346.0 M

2031

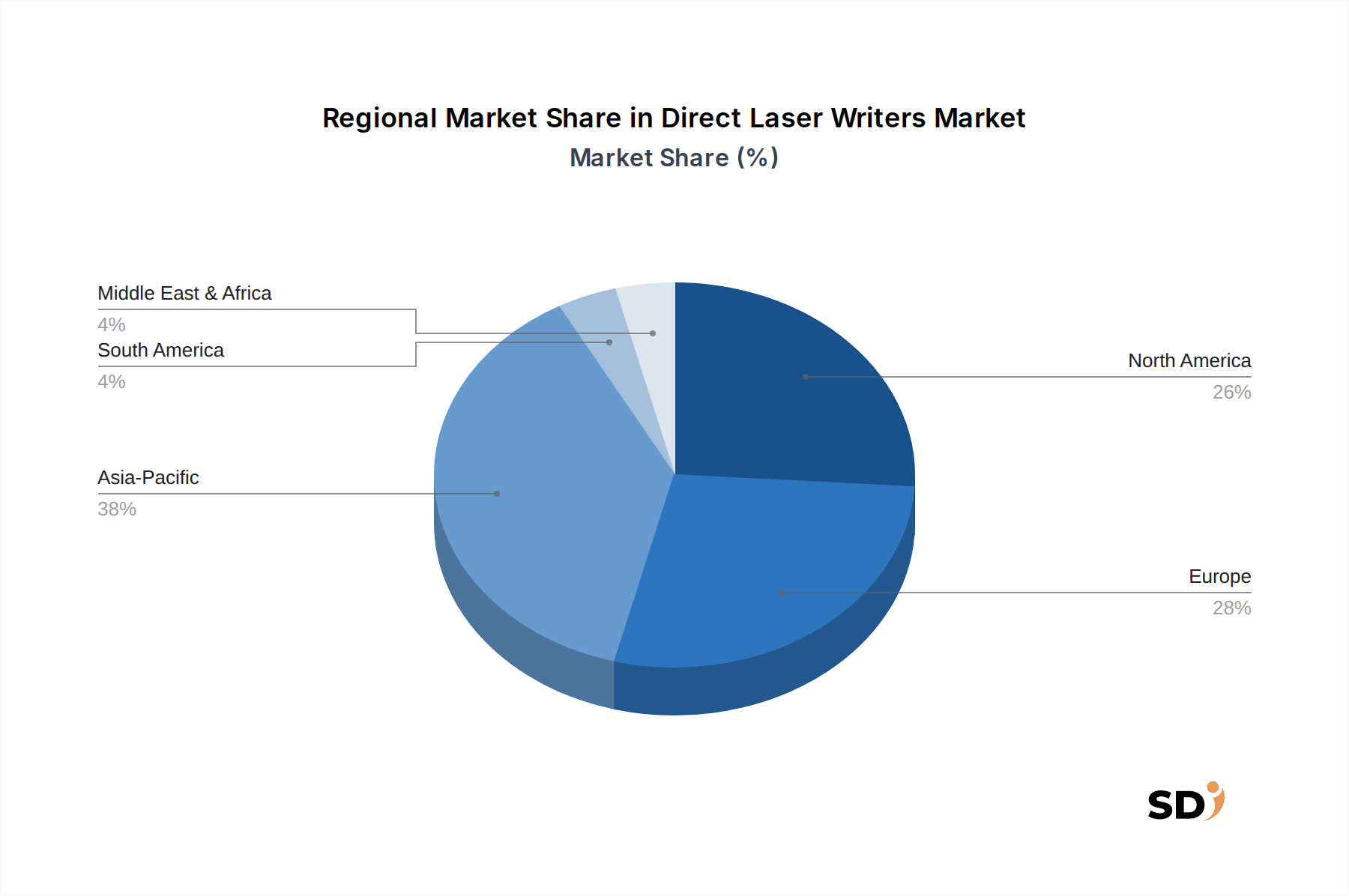

Technological breakthroughs, particularly in areas like two-photon polymerization and multi-wavelength laser systems, are enhancing the capabilities and accessibility of direct laser writers, enabling superior resolution and wider material compatibility. This evolution directly supports the growth in specialized applications and the overall Microfabrication Equipment Market. Geographically, Asia Pacific is anticipated to maintain its dominance, largely due to extensive investments in semiconductor manufacturing and advanced R&D facilities, particularly in countries like China, Japan, and South Korea. Europe and North America also represent significant markets, characterized by strong innovation ecosystems and established advanced manufacturing bases. Despite the high initial capital investment associated with these sophisticated systems, the long-term benefits of precision, flexibility, and accelerated development cycles underscore their value proposition. The market is also benefiting from increased funding in scientific research and the expansion of the Additive Manufacturing Market into micron-scale applications, further solidifying the strategic importance of direct laser writers in the modern industrial landscape. The competitive landscape is marked by continuous innovation, with leading players focusing on improving system throughput, automation, and user-friendliness to cater to a broader spectrum of research and industrial applications.

Application Dominance in Direct Laser Writers Market

The Application segment, particularly the industrial category, stands as the single largest and most influential segment by revenue share within the Direct Laser Writers Market. Its dominance is a direct reflection of the widespread and critical need for high-precision, direct patterning, and micro-fabrication capabilities across a myriad of industrial sectors, including semiconductors, microelectromechanical systems (MEMS), photonics, and advanced materials. Direct laser writers provide unparalleled advantages in these applications by enabling the creation of intricate 2D and 3D structures with sub-micron resolution, which is often unattainable with conventional lithography techniques for specific use cases. This includes the direct fabrication of waveguides, diffractive optical elements, microfluidic channels, and customized micro-components for various industrial systems.

The demand from the Industrial Lasers Market, which encompasses a broader spectrum of laser-based manufacturing processes, frequently intersects with direct laser writing technology as industries seek greater precision and flexibility. Companies operating within the industrial segment of the Direct Laser Writers Market often provide robust, high-throughput systems designed for continuous operation and integration into existing manufacturing lines. Key players like Nanoscribe and Heidelberg Instruments have made significant inroads by offering solutions tailored for industrial-scale production and prototyping in areas such as advanced packaging, display manufacturing, and bespoke sensor fabrication. The ability of direct laser writers to facilitate rapid iteration and customization without the need for masks or complex tooling makes them invaluable for agile manufacturing environments. Furthermore, the increasing adoption of micro-optics in consumer electronics and automotive applications, alongside the escalating complexity of MEMS devices, continues to drive demand in the industrial segment.

While the laboratory segment also constitutes a significant portion, primarily serving academic research and early-stage development, the sheer volume and continuous operational demands of industrial applications ensure its leading revenue share. The industrial segment's share is further consolidating as technological advancements in automation, software integration, and improved material processing capabilities make direct laser writing more accessible and cost-effective for large-scale industrial deployment. This consolidation is also supported by the increasing crossover of technologies, where innovations initially developed for laboratory research quickly find their way into industrial production processes, underscoring the dynamic interplay between fundamental research and applied manufacturing within the Direct Laser Writers Market. The imperative for miniaturization and enhanced performance across diverse industrial products ensures that the industrial application segment will continue to be the primary revenue driver and innovation hub for the foreseeable future.

Driving Forces & Constraints in Direct Laser Writers Market

The Direct Laser Writers Market is significantly influenced by a confluence of technological drivers and inherent constraints. One primary driving force is the persistent trend of miniaturization in electronics and photonics. For instance, the demand for semiconductor devices with feature sizes below 100 nm necessitates advanced patterning techniques, which direct laser writers can often provide for specific applications, particularly in rapid prototyping and maskless lithography, complementing the broader Microlithography Equipment Market. This is further evidenced by the continuous push towards higher transistor densities and more complex integrated photonic circuits, driving significant investment in high-resolution fabrication tools. The expansion of the Research & Development Market is another critical driver; academic and corporate research institutions are increasingly adopting direct laser writers for fundamental material science studies, advanced device prototyping, and bio-engineering applications. This includes the development of meta-materials, microfluidic devices, and scaffolding for tissue engineering, where the precision and versatility of direct laser writing are indispensable. This has led to a notable uptick in academic publications utilizing direct laser writing, indicating widespread adoption in advanced research settings.

Another significant impetus comes from the burgeoning Additive Manufacturing Market, specifically its extension into micro- and nano-scale 3D printing. Direct laser writers, particularly those utilizing two-photon polymerization, allow for the creation of intricate 3D microstructures, opening new avenues for product design and functionality in fields like micro-optics and biomedical implants. Furthermore, the increasing complexity of optical components, such as free-form micro-lenses and photonic crystals, requires manufacturing methods that offer both precision and flexibility, driving demand from the Optical Components Market for customizable fabrication tools. On the constraint side, the high initial capital expenditure for direct laser writer systems remains a significant barrier, particularly for smaller research groups or emerging companies. A typical high-end system can cost upwards of $500,000 to $1 million, limiting accessibility. Moreover, the reliance on specialized materials, such as specific Photopolymer Resins Market offerings, can limit application breadth and introduce supply chain vulnerabilities or cost fluctuations. The complexity of operating these advanced systems also necessitates highly skilled personnel, adding to operational costs and potentially slowing adoption in regions with limited technical expertise. These factors collectively shape the market dynamics, balancing technological promise against practical implementation challenges.

Competitive Ecosystem of Direct Laser Writers Market

The Direct Laser Writers Market is characterized by a concentrated competitive landscape featuring specialized manufacturers focusing on high-precision micro- and nano-fabrication solutions.

Nanoscribe: A German company renowned for its 3D microfabrication systems based on two-photon polymerization, enabling the creation of complex 3D structures with sub-micrometer resolution for applications in micro-optics, photonics, and medical technology.

Heidelberg Instruments: A leading provider of high-resolution maskless lithography systems and direct-write tools, offering versatile solutions for research and industrial applications in microelectronics, MEMS, and photonics.

Raith: Specializes in nanofabrication instruments, including electron beam lithography systems and focused ion beam systems, often integrated with direct laser writing capabilities for advanced material processing and prototyping.

KLOE: A French manufacturer providing mask aligners and direct write lithography systems, focusing on robust and high-throughput solutions for research and industrial production of micro-components.

Durham Magneto Optics: Focuses on direct laser writing solutions for magnetic materials, specializing in tools that enable the creation of custom magnetic structures for advanced data storage and spintronics research.

SVG Optronics: A Chinese company involved in developing and manufacturing high-precision optical components and systems, including direct laser writing equipment primarily for the production of diffractive optical elements and micro-optics.

Recent Developments & Milestones in Direct Laser Writers Market

June 2024: Leading research institutions announce breakthroughs in multi-material direct laser writing, enabling the simultaneous patterning of different polymers and metals with high precision, signaling new potential for the Additive Manufacturing Market.

March 2024: Nanoscribe launches a new generation of its 3D microfabrication system, featuring enhanced resolution, faster writing speeds, and an expanded material library, further solidifying its position in the Microlithography Equipment Market.

December 2023: Collaborations between direct laser writer manufacturers and Photopolymer Resins Market suppliers lead to the development of novel biocompatible resins, broadening application scope in biomedical and life sciences research.

August 2023: Heidelberg Instruments introduces an advanced software suite for its direct laser writing systems, integrating AI-driven optimization algorithms for improved patterning accuracy and reduced fabrication times, enhancing efficiency for the Industrial Lasers Market.

May 2023: Several universities in North America report significant increases in grant funding specifically allocated for the acquisition of direct laser writing equipment, indicating robust growth in the Research & Development Market.

February 2023: A major manufacturer unveils a compact, high-throughput Desktop Laser Writers Market system, targeting academic labs and small-scale prototyping, making the technology more accessible to a wider user base.

Regional Market Breakdown for Direct Laser Writers Market

The Direct Laser Writers Market exhibits distinct regional dynamics, influenced by varying levels of industrialization, research investment, and technological adoption. Asia Pacific is currently the dominant region and is projected to experience the fastest growth, primarily driven by robust investments in semiconductor manufacturing, advanced electronics, and photonics industries in countries such as China, South Korea, Japan, and Taiwan. These nations are major hubs for the Precision Manufacturing Market, creating a consistent demand for high-precision micro-fabrication tools to produce components for consumer electronics, automotive, and telecommunications sectors. The region's extensive network of research institutions also contributes significantly to the Research & Development Market, fostering innovation and the adoption of cutting-edge direct laser writing technologies.

North America represents a mature yet dynamic market, characterized by strong governmental and private sector funding in advanced research and development, particularly in biotechnology, aerospace, and defense. The United States, in particular, showcases high adoption rates of direct laser writers for fundamental science and highly specialized industrial applications. The presence of numerous leading technology companies and research universities ensures a steady demand, although the growth rate might be marginally lower compared to the rapidly expanding Asian markets. Similarly, Europe holds a substantial share of the Direct Laser Writers Market, fueled by strong innovation ecosystems in Germany, the UK, and France. European countries are leaders in areas such as automotive, medical devices, and industrial machinery, necessitating precise manufacturing capabilities. The region benefits from significant public and private investments in photonics and micro-optics research, further bolstering the demand for Microlithography Equipment Market solutions.

In contrast, the Middle East & Africa and South America currently hold smaller shares but are emerging markets with considerable potential. Growth in these regions is largely driven by increasing investment in scientific research infrastructure, particularly in countries like Israel and Brazil, aiming to diversify their economies and build local high-tech capabilities. While the immediate demand might be concentrated in academic and governmental research institutions, the long-term outlook suggests gradual expansion as industrial sectors in these regions mature and adopt more advanced manufacturing processes. The global competitive landscape thus underscores a continued geographic diversification, albeit with established markets maintaining their leadership in innovation and high-value applications.

Supply Chain & Raw Material Dynamics for Direct Laser Writers Market

The Direct Laser Writers Market is intricately linked to a complex supply chain, with several critical upstream dependencies that influence cost, availability, and overall market stability. Key components include high-precision laser sources (e.g., femtosecond or picosecond lasers), advanced Optical Components Market such as objective lenses, mirrors, and beam shapers, as well as highly precise motion stages and sophisticated control electronics. The sourcing of these specialized components often involves a limited number of niche suppliers, creating potential single-source risks and vulnerability to geopolitical disruptions or trade restrictions. For instance, the global semiconductor shortage experienced in recent years significantly impacted the availability and cost of control electronics, indirectly affecting the production timelines and pricing of direct laser writing systems.

Raw material inputs are also crucial, particularly the specialized Photopolymer Resins Market. These resins, often acrylate or epoxy-based, are precisely formulated for specific wavelengths and curing properties, enabling the creation of fine structures. Price volatility in base chemicals used to produce these resins, or disruptions in their manufacturing processes, can directly influence the operational costs for end-users. While the volume of resin consumed per device is small, their specialized nature and the need for high purity make them a critical, non-substitutable input. Furthermore, high-quality optical-grade glass and specialized coatings for lenses and mirrors are essential, and their availability can be influenced by global supply dynamics for precision materials. The supply chain for the Direct Laser Writers Market, therefore, demands robust risk management strategies, including diversified sourcing and strategic inventory management, to mitigate the impact of potential disruptions on manufacturing schedules and market pricing.

Technology Innovation Trajectory in Direct Laser Writers Market

Innovation is a cornerstone of the Direct Laser Writers Market, constantly pushing the boundaries of resolution, speed, and application versatility. One of the most disruptive emerging technologies is Two-Photon Polymerization (2PP). This technique utilizes ultra-short pulsed lasers to initiate polymerization in a small, localized volume within a photoresist, enabling true three-dimensional micro- and nano-fabrication. 2PP systems, such as those offered by Nanoscribe, are rapidly gaining traction in the Research & Development Market for creating intricate structures like photonic crystals, micro-optics, and biomedical scaffolds with resolutions down to tens of nanometers. Adoption timelines for 2PP are accelerating, with significant R&D investment from both academic institutions and industry players, as it offers unprecedented design freedom for complex 3D geometries. It reinforces incumbent business models by expanding their capabilities into advanced 3D Additive Manufacturing Market applications that were previously unachievable.

Another significant innovation is the integration of Artificial Intelligence (AI) and Machine Learning (ML) for process optimization and automation. AI algorithms are being developed to predict optimal laser parameters for different materials and geometries, significantly reducing trial-and-error time and improving fabrication yield. ML models can also enhance the precision of positioning stages and compensate for environmental fluctuations, leading to more consistent and reliable patterning. This technology is still in its early to mid-adoption phase, with R&D focused on developing robust, user-friendly software interfaces. AI/ML integration primarily reinforces existing business models by making Direct Laser Writers more efficient, accessible, and less reliant on highly specialized human expertise, thus potentially broadening the user base to a more diverse set of applications, including the Desktop Laser Writers Market.

Finally, hybrid additive/subtractive manufacturing approaches are emerging as a powerful innovation. This involves combining direct laser writing with techniques like focused ion beam (FIB) milling or atomic layer deposition (ALD) within a single workflow. For instance, a direct laser writer might create a 3D polymer scaffold, which is then functionalized or reinforced with metal layers using ALD, or selectively modified using FIB. This allows for the fabrication of multi-material devices with tailored electrical, optical, and mechanical properties. These hybrid systems are in a nascent stage of adoption, requiring substantial R&D investment to integrate disparate technologies seamlessly. They pose a potential threat to specialized single-process manufacturers by offering a more comprehensive fabrication solution, but also reinforce the overall Microfabrication Equipment Market by expanding the capabilities and complexity of deployable micro- and nano-devices.

Direct Laser Writers Segmentation

1. Application

1.1. Industrial

1.2. Laboratory

1.3. Others

2. Types

2.1. Desktop

2.2. Vertical

Direct Laser Writers Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Direct Laser Writers REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 5.3% from 2020-2034

Segmentation

By Application

Industrial

Laboratory

Others

By Types

Desktop

Vertical

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Industrial

5.1.2. Laboratory

5.1.3. Others

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Desktop

5.2.2. Vertical

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Industrial

6.1.2. Laboratory

6.1.3. Others

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Desktop

6.2.2. Vertical

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Industrial

7.1.2. Laboratory

7.1.3. Others

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Desktop

7.2.2. Vertical

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Industrial

8.1.2. Laboratory

8.1.3. Others

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Desktop

8.2.2. Vertical

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Industrial

9.1.2. Laboratory

9.1.3. Others

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Desktop

9.2.2. Vertical

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Industrial

10.1.2. Laboratory

10.1.3. Others

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Desktop

10.2.2. Vertical

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Nanoscribe

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Heidelberg Instruments

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Raith

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. KLOE

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Durham Magneto Optics

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. SVG Optronics

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (million), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (million), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (million), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (million), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (million), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (million), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (million), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (million), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (million), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (million), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (million), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Revenue million Forecast, by Types 2020 & 2033

Table 3: Revenue million Forecast, by Region 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Types 2020 & 2033

Table 6: Revenue million Forecast, by Country 2020 & 2033

Table 7: Revenue (million) Forecast, by Application 2020 & 2033

Table 8: Revenue (million) Forecast, by Application 2020 & 2033

Table 9: Revenue (million) Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Application 2020 & 2033

Table 11: Revenue million Forecast, by Types 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Types 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Revenue (million) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue million Forecast, by Application 2020 & 2033

Table 29: Revenue million Forecast, by Types 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue million Forecast, by Application 2020 & 2033

Table 38: Revenue million Forecast, by Types 2020 & 2033

Table 39: Revenue million Forecast, by Country 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our robust primary research methodology forms the cornerstone of our market analysis, accounting for 70-80% of our total research effort. We engage with a diverse array of industry experts and stakeholders through in-depth interviews, discussions, and surveys. This direct engagement provides invaluable qualitative and quantitative insights, validating secondary findings and uncovering nascent market trends. Our primary respondents are strategically identified across the entire value chain of the Direct Laser Writers market.

Key participant types in our primary interviews include:

Direct Laser Writer Manufacturers: Companies specializing in the design, production, and sale of direct laser writing systems.

Semiconductor Fabrication Firms: Major end-users leveraging direct laser writers for lithography and patterning processes.

Academic & Industrial Research Laboratories: Institutions utilizing direct laser writers for advanced materials science, nanotechnology, and fundamental research.

Advanced Material Processing & Micro-fabrication Companies: Businesses employing these systems for precision manufacturing beyond traditional semiconductor applications.

Distributors & System Integrators: Channel partners responsible for sales, service, and integration of direct laser writing solutions.

Our interviewees hold critical positions, ensuring insights from decision-makers and technical experts. These include:

Director of Product Development (OEMs): Providing perspectives on technological advancements, product roadmaps, and competitive strategies.

Head of Process Engineering (Industrial End-users): Offering insights into application requirements, operational challenges, and ROI considerations.

Principal Research Scientist (Laboratory End-users): Sharing views on cutting-edge research needs, system capabilities, and future research directions.

Global Sourcing/Procurement Manager: Detailing purchasing criteria, supplier relationships, and market pricing dynamics.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Director of Product Development (OEMs)

30%

Head of Process Engineering (Industrial End-users)

25%

Principal Research Scientist (Laboratory End-users)

25%

Global Sourcing/Procurement Manager

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Direct Laser Writer Manufacturers

30%

Semiconductor Fabrication Firms

25%

Academic & Industrial Research Laboratories

20%

Advanced Material Processing & Micro-fabrication Companies

15%

Distributors & System Integrators

10%

Secondary Research & Industry Benchmarking

The remaining 20-30% of our research is dedicated to comprehensive secondary research and industry benchmarking. This phase provides foundational data, market landscapes, and validation points for primary insights. We meticulously gather data from reputable, publicly available sources, ensuring neutrality and accuracy. Our firm strictly avoids utilizing data from other market research websites to maintain originality and integrity.

Key sources leveraged include:

Government & Regulatory Bodies: Official reports, statistical data, and policy documents from agencies relevant to technology, trade, and manufacturing.

Public company annual reports (10-K, 20-F), investor presentations, and earnings call transcripts.

Subscription databases such as Bloomberg, Factiva, Hoovers, and PitchBook for financial data, competitive intelligence, and M&A activities.

Academic Journals & White Papers: Peer-reviewed research, technical articles, and scholarly publications on laser technology, micro-fabrication, and advanced materials.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodology employs a robust combination of top-down and bottom-up approaches, complemented by multi-level data triangulation to ensure comprehensive coverage and accuracy.

Bottom-Up Approach: This method begins at the granular level, aggregating detailed data points to build the total market size.

Annual unit shipments of Direct Laser Writers (segmented by type: Desktop, Vertical) are estimated based on production capacities, sales data from manufacturers, and observed demand from end-user industries across various regions.

Average Selling Price (ASP) per unit, segmented by type (Desktop, Vertical), application (Industrial, Laboratory), and regional variations, is meticulously tracked and projected.

Projected capital expenditure (CapEx) in the semiconductor, microelectronics, and advanced materials sectors provides a crucial indicator of future investments in direct laser writing technology.

Growth rate of R&D spending in relevant academic and industrial laboratories directly correlates with the demand for advanced laboratory-grade laser writers.

Top-Down Approach: We estimate the overall market size by analyzing macroeconomic indicators, industry growth rates, and broad technology adoption trends, then breaking it down by segment (application, type, region).

Data Triangulation: All market figures are subjected to a rigorous triangulation process, cross-referencing data points from primary interviews, secondary sources, and our proprietary demand models. This iterative validation strengthens the robustness of our estimates.

The forecast for 2026-2034 considers technological advancements, economic cycles, regulatory impacts, and competitive landscape shifts. The market is segmented comprehensively by Application (Industrial, Laboratory, Others), by Types (Desktop, Vertical), and across key geographic regions including North America, South America, Europe, Middle East & Africa, and Asia Pacific.

Data Accuracy & Quality Check

Our unwavering commitment to data quality ensures that all market estimations adhere to the highest standards. We guarantee an estimated data accuracy level of 85-90%, a testament to our meticulous research processes and analytical rigor.

Key aspects of our quality control include:

Expert Validation: All market figures, trends, and forecasts are reviewed and validated by a panel of internal senior analysts and external industry experts.

Iterative Process: Research findings are continuously updated and refined throughout the report generation cycle, incorporating the latest market developments and feedback.

Proprietary Models: We utilize sophisticated econometric and statistical models, developed in-house, to process raw data and generate robust forecasts.

Report Freshness: Every report is updated up to the date of purchase, ensuring that clients receive the most current and relevant market intelligence available. This commitment reflects our agile research approach and responsiveness to market dynamics.

Frequently Asked Questions

1. What is the investment landscape for Direct Laser Writers technology?

The Direct Laser Writers market is characterized by specialized industrial and laboratory applications. Investment activity typically focuses on R&D for enhanced precision and speed, rather than broad venture capital funding rounds. Companies like Nanoscribe and Heidelberg Instruments often drive innovation through internal funding and strategic partnerships.

2. How do raw material sourcing and supply chain impact Direct Laser Writers production?

Direct Laser Writers rely on precise optical components, laser sources, and high-quality materials for their fabrication systems. The supply chain involves a global network of specialized component manufacturers. Any disruptions in sourcing critical parts, such as those used by Raith or KLOE, can affect lead times and production costs.

3. Which region dominates the Direct Laser Writers market and why?

Asia-Pacific currently holds the largest share, estimated at 38%, due to its robust manufacturing sector, advanced electronics production, and extensive academic research in nanotechnology. Key contributors include China, Japan, and South Korea, driving demand for precision writing technologies.

4. Where are the fastest-growing opportunities for Direct Laser Writers technology?

Emerging economies within Asia-Pacific and parts of Europe are showing accelerated growth in Direct Laser Writers adoption. Increased governmental investment in scientific research, industrial automation, and semiconductor fabrication in these regions creates new opportunities. This supports the market's overall 5.3% CAGR.

5. How did the pandemic affect the Direct Laser Writers market and what are long-term shifts?

The Direct Laser Writers market experienced initial supply chain disruptions and project delays during the pandemic. However, long-term demand remains strong due to increasing needs for miniaturization and precision in industries like semiconductors and medical devices. The market's 5.3% CAGR reflects its resilience and ongoing technological relevance.

6. What are the primary challenges or supply-chain risks for Direct Laser Writers?

Key challenges include the high capital cost of the equipment, which requires substantial investment from end-users, and the necessity for highly skilled operators. Supply chain risks involve sourcing specialized components, such as high-power lasers and precision optics, from a limited number of global suppliers like those supporting SVG Optronics or Durham Magneto Optics.