Corn Hybrids Market: What Drives 5.56% CAGR Growth?

corn hybrids

Corn Hybrids Market: What Drives 5.56% CAGR Growth?

corn hybrids by Application (Farmland, Greenhouse, Others), by Types (GMOs Seeds, non-GMOs Seeds), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 7, 2026|Base Year : 2025|Pages : 119

Atul Bhusare

Research Associate

About Sector Data Insights

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

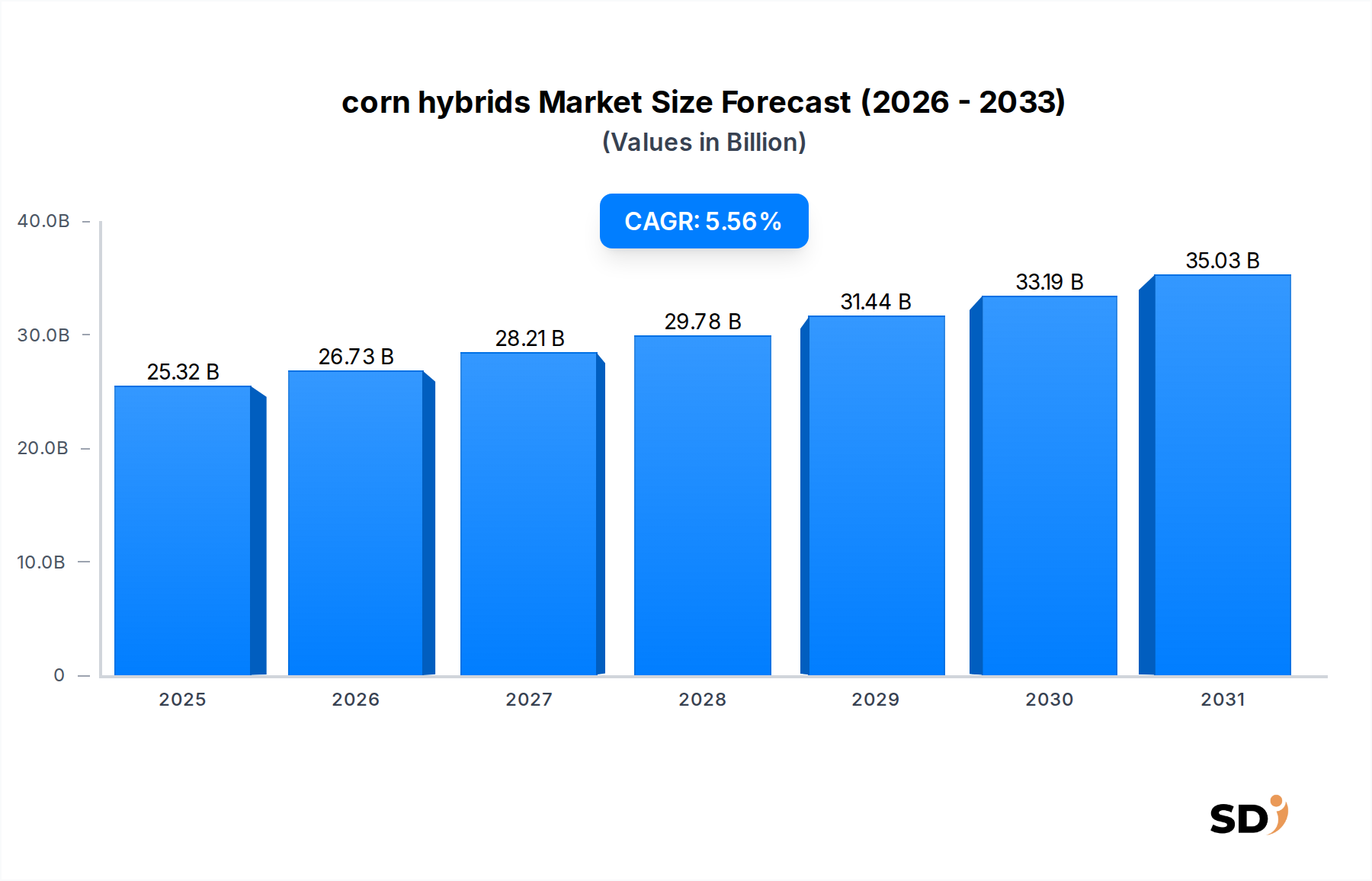

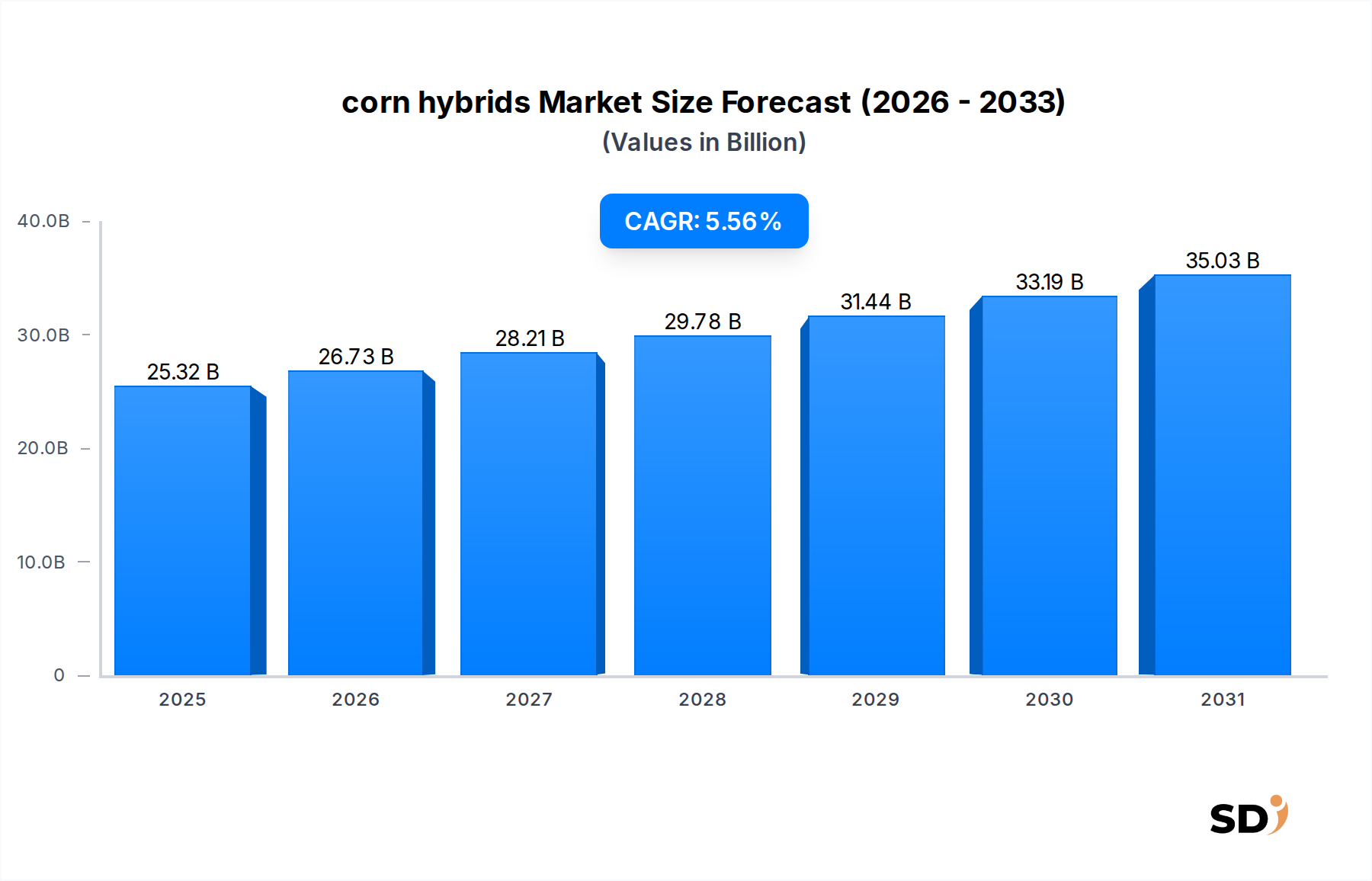

The global corn hybrids Market is experiencing robust expansion, propelled by escalating global food and feed demands, advancements in agricultural biotechnology, and the imperative for climate-resilient crop varieties. Valued at $25.32 billion in 2025, the market is projected to reach approximately $41.16 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 5.56% over the forecast period. This significant growth underscores the critical role of advanced corn genetics in enhancing agricultural productivity and food security worldwide. Key demand drivers include the continuous need for higher yields to feed a growing population, improved resistance traits against evolving pests and diseases, and enhanced tolerance to abiotic stresses such as drought and heat.

corn hybrids Market Size (In Billion)

40.0B

30.0B

20.0B

10.0B

0

25.32 B

2025

26.73 B

2026

28.21 B

2027

29.78 B

2028

31.44 B

2029

33.19 B

2030

35.03 B

2031

Technological innovations, particularly in genetic engineering and molecular breeding, are central to the market's trajectory. These innovations enable the development of corn hybrids with stacked traits, offering multiple benefits like herbicide tolerance, insect resistance, and improved nutritional profiles. The adoption of these advanced seeds is particularly pronounced in major corn-producing regions like North America and South America, where large-scale commercial farming benefits significantly from enhanced productivity and reduced input costs. Furthermore, the increasing integration of digital agriculture and Precision Agriculture Market solutions is optimizing planting, monitoring, and harvesting processes, further boosting the efficacy of corn hybrids. While the GMO Seeds Market remains a dominant force, there is also a notable, albeit smaller, segment dedicated to the Non-GMO Seeds Market, driven by specific consumer preferences and regulatory landscapes, particularly in parts of Europe. The sustained investment in research and development by leading seed companies is crucial for overcoming emerging agricultural challenges and unlocking new growth opportunities within the corn hybrids Market, including expansion into previously underutilized arable land and enhancing sustainable farming practices.

Dominant Segment Analysis in corn hybrids Market

Within the broader corn hybrids Market, the "GMOs Seeds" segment, under the Types categorization, stands as the unequivocal dominant force by revenue share and adoption rate. This segment's preeminence is largely attributable to its capacity to deliver superior agronomic benefits, addressing critical challenges faced by modern agriculture. Genetically modified corn hybrids are engineered to possess traits such as herbicide tolerance (e.g., Roundup Ready technology) and insect resistance (e.g., Bt corn), which significantly reduce the need for manual weeding and the application of chemical insecticides. These advantages translate directly into higher yields, lower operational costs for farmers, and improved crop consistency, particularly in large-scale commercial farming operations.

The widespread adoption of GMOs seeds is particularly evident in regions with expansive agricultural land and progressive agricultural policies, such as North America and South America. In the United States, for instance, a vast majority of corn planted annually comprises genetically modified varieties, reflecting the economic benefits and operational efficiencies they provide. Major players like Monsanto (now part of Bayer), Syngenta, Dupont (now Corteva Agriscience), and Dow (now Corteva Agriscience) have invested heavily in the research, development, and commercialization of these advanced hybrid varieties, creating a highly competitive and innovation-driven GMO Seeds Market. These companies continuously introduce new stacked traits, combining multiple genetic enhancements into a single seed, thereby offering comprehensive solutions against a spectrum of biotic and abiotic stresses. This strategy not only solidifies their market leadership but also drives the overall growth of the corn hybrids Market.

While concerns regarding environmental impact and consumer acceptance persist in certain regions, the economic incentives for farmers, coupled with scientific validation of safety and efficacy, continue to fuel the dominance of GMO corn hybrids. The segment's share is expected to remain substantial, driven by ongoing R&D in areas like drought tolerance, nitrogen use efficiency, and improved nutritional content. This continuous innovation ensures that GMOs Seeds will continue to dictate the technological trajectory and economic landscape of the corn hybrids Market, despite the niche but growing demand for the Non-GMO Seeds Market in specific consumer segments and regulatory environments. The Farmland Application Market heavily relies on these advanced seed types for optimal productivity.

Key Market Drivers & Constraints in corn hybrids Market

The corn hybrids Market is significantly influenced by a confluence of potent drivers and discernible constraints. A primary driver is the escalating global demand for food, feed, and industrial applications, directly linked to a projected global population increase. For instance, the demand for meat and dairy products, which heavily relies on corn as animal feed, is estimated to grow by 1.5% annually in certain developing economies, compelling farmers to seek higher-yielding corn varieties. This translates into a sustained impetus for advanced corn hybrids offering enhanced productivity and nutritional value. Furthermore, the expanding Biofuel Feedstock Market, particularly for ethanol production, represents a significant industrial demand driver for corn. The U.S. ethanol industry alone consumes over 40% of the domestic corn crop, thereby tying the demand for corn hybrids directly to energy policy and fossil fuel price dynamics. Advancements in Agricultural Biotechnology Market are another pivotal driver, enabling the development of genetically engineered corn hybrids with improved disease resistance (e.g., against Fusarium ear rot, reducing yield losses by up to 20% in affected areas) and enhanced herbicide tolerance, which streamlines weed management and reduces labor costs.

Conversely, the corn hybrids Market faces several significant constraints. Stringent regulatory frameworks and public perception issues, particularly concerning genetically modified organisms (GMOs), present a notable impediment. For example, several European Union countries maintain strict import and cultivation restrictions on GMO crops, significantly limiting the penetration of certain corn hybrids. This divergent regulatory landscape fragments the market and restricts the global scalability of some products, fostering a segmented Non-GMO Seeds Market in these regions. Another constraint is the evolving pest resistance to existing GMO traits, such as certain insect populations developing tolerance to Bt corn, necessitating continuous research and development for new trait stacks. This R&D investment is substantial, impacting the cost structure for seed developers. Finally, the volatile pricing of agricultural commodities, including corn itself, and the associated high input costs for farmers (fertilizers, Crop Protection Market products) can influence planting decisions and adoption rates of premium-priced hybrid seeds, thereby restraining market growth, especially in regions with limited financial resources.

Competitive Ecosystem of corn hybrids Market

The competitive landscape of the corn hybrids Market is characterized by intense innovation, strategic collaborations, and a strong focus on proprietary genetic traits. Key players are continuously investing in R&D to develop superior hybrids that offer higher yields, enhanced disease and pest resistance, and improved stress tolerance.

Dupont: A global leader in agricultural sciences, known for its Pioneer brand of seeds, which offers a wide range of corn hybrids optimized for various growing conditions and end-uses, emphasizing high-performance genetics and sustainable solutions.

Syngenta: A major agribusiness company providing diverse crop solutions, including corn seeds with advanced traits for insect control and herbicide tolerance, alongside a strong portfolio in crop protection products.

Monsanto: Now a subsidiary of Bayer AG, it remains a historical pioneer in genetic engineering for corn, renowned for its Roundup Ready and Bt corn technologies, which have revolutionized corn cultivation globally.

Bayer: A life science company with a comprehensive portfolio in agriculture, including seeds and traits, crop protection, and digital farming tools, heavily focused on integrated solutions for corn production.

KWS: A German-based independent seed company specializing in plant breeding, offering a broad selection of high-performance corn hybrids tailored for specific regional climates and agricultural practices, with a strong emphasis on European markets.

Dow: Now part of Corteva Agriscience, it has been a significant player in the seed industry, contributing advanced corn genetics and trait technologies aimed at enhancing productivity and resilience.

Origin Agritech: A China-based company focused on agricultural biotechnology, specializing in corn seed breeding and genetic modification, aiming to improve domestic food security and farmer profitability in China.

DLF: A global seed company, primarily known for forage and turf seeds, but also involved in field crops including corn, focusing on developing robust varieties suitable for diverse agricultural systems.

Land O'Lakes: A farmer-owned cooperative, offering a range of agricultural inputs including corn seeds through its WinField United brand, focusing on agronomic expertise and tailored solutions for growers.

Limagrain: A French international agricultural co-operative group, active in field seeds (including corn), vegetable seeds, and cereal products, known for its commitment to plant breeding and innovation.

Pacific Seeds: An Australian company with a strong focus on tropical and subtropical crops, offering corn hybrids adapted to challenging environmental conditions in the Asia-Pacific region.

Zemun Polje: A Serbian agricultural institute engaged in research, breeding, and production of field crops, including corn hybrids, contributing to agricultural development in the Balkan region.

DeKalb Genetics: A brand under Monsanto/Bayer, recognized for its yellow corn varieties and ongoing innovation in corn seed technology, maintaining a strong presence in key corn-growing areas.

Seminis: Another brand under Monsanto/Bayer, primarily known for vegetable seeds, but also contributing to the broader seed genetics pool that can indirectly influence field crop breeding.

Advanta: A global seed company with a focus on diverse field crops including corn, known for developing hybrids that perform well under varied climatic conditions, particularly in emerging markets.

Sakata: A Japanese company specializing in vegetable and flower seeds, with a growing presence in field crops, aiming to provide high-quality genetic material for sustainable agriculture.

Mycogen Seeds: A brand under Dow (now Corteva Agriscience), offering advanced corn hybrids featuring proprietary traits for insect protection and weed control.

Winfield Solutions: Part of the Land O'Lakes system, providing crop protection products, seed, and other agricultural services, distributing various corn hybrid brands and offering agronomic advice.

LG Seeds: A brand offering corn, soybean, and alfalfa seeds, known for local service and regionally adapted genetics, focusing on providing farmers with tailored seed solutions.

Recent Developments & Milestones in corn hybrids Market

February 2026: A major seed developer announced the commercial launch of a new corn hybrid designed with enhanced drought tolerance, capable of sustaining 15-20% higher yields under moderate water stress conditions, targeting the Farmland Application Market in arid regions.

November 2025: Regulatory approval was granted in a key Asia Pacific market for a stacked-trait corn hybrid incorporating both insect resistance and herbicide tolerance, paving the way for its widespread adoption and boosting the local GMO Seeds Market.

August 2025: A prominent agricultural biotechnology firm entered into a strategic partnership with a drone technology company to integrate AI-powered phenotyping into their corn breeding programs, aiming to accelerate the development of superior corn hybrids.

April 2024: Breakthrough research published by a university consortium detailed the identification of novel genetic markers linked to improved nitrogen use efficiency in corn, promising future hybrids that require less synthetic fertilizer, which is crucial for the Crop Protection Market and overall sustainability.

January 2024: A leading seed producer unveiled its next-generation corn hybrid portfolio, emphasizing resistance to prevalent corn diseases such as tar spot and Southern rust, addressing significant yield loss concerns for farmers.

October 2023: An international collaboration was established to develop Specialty Corn Market hybrids, focusing on varieties with enhanced nutritional profiles for human consumption and specialized industrial uses, beyond conventional feed and ethanol.

June 2023: Several seed companies reported significant investments in expanding their seed production and processing facilities in South America, anticipating robust demand for corn hybrids driven by the expanding Biofuel Feedstock Market and increased agricultural exports from the region.

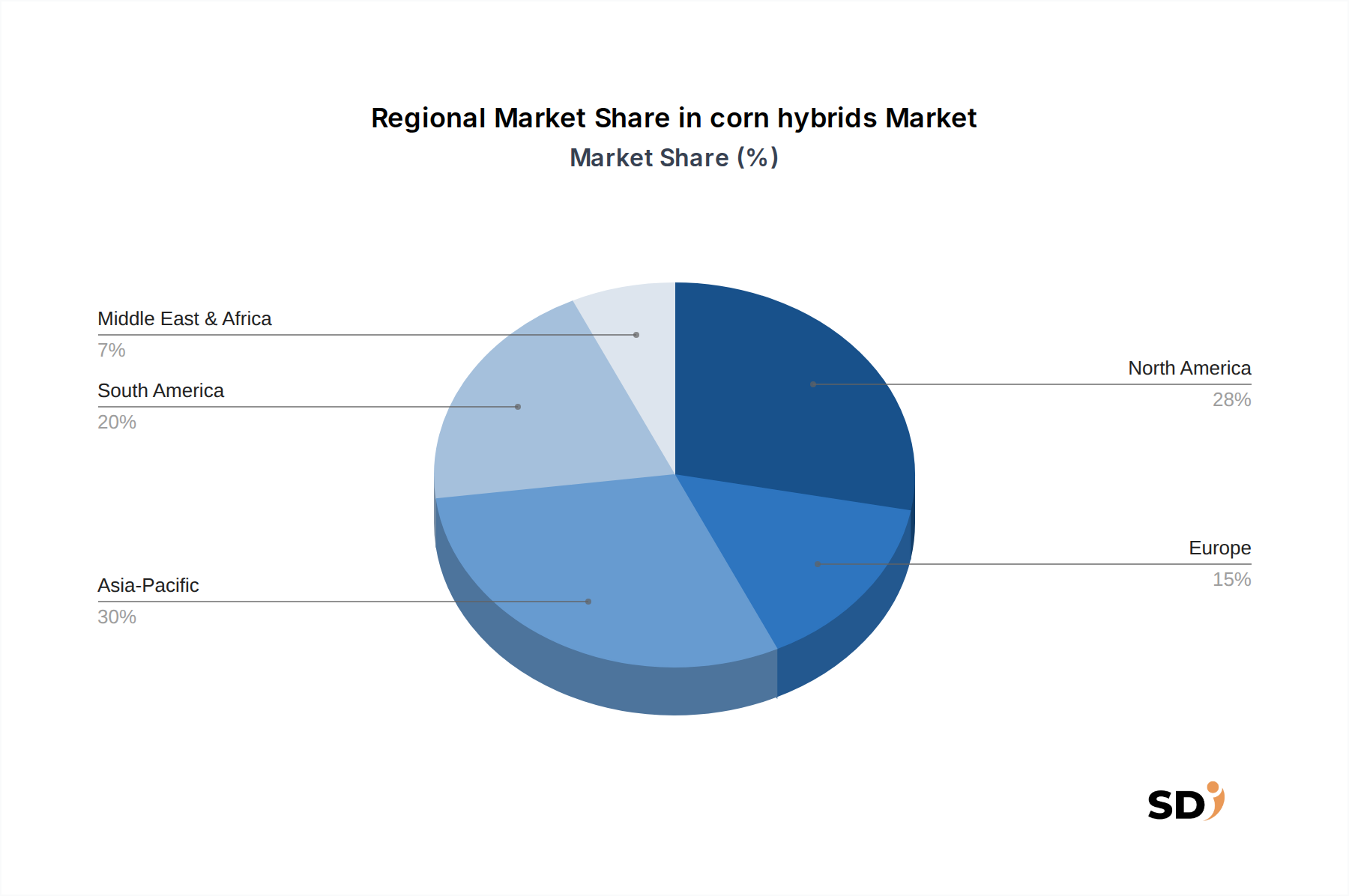

Regional Market Breakdown for corn hybrids Market

Geographically, the corn hybrids Market demonstrates varied growth dynamics and adoption patterns across different regions, influenced by agricultural practices, regulatory environments, and economic factors. North America currently holds the largest revenue share, primarily driven by the United States, which is a global leader in corn production and adoption of advanced genetic technologies. The region’s mature agricultural infrastructure, extensive Farmland Application Market, and high farmer acceptance of genetically modified corn hybrids contribute to a stable and substantial market. With a projected CAGR of approximately 4.8%, North America continues to see innovation in stacked traits and digital agriculture integration.

Asia Pacific emerges as the fastest-growing region, anticipated to register a CAGR exceeding 7.0% over the forecast period. This growth is fueled by increasing populations, rising demand for feed for expanding livestock industries, and a gradual shift towards modern farming techniques in countries like China, India, and ASEAN nations. While some regulatory hurdles exist for GMOs, the imperative for food security and yield improvement is driving significant investment in high-performing corn hybrids. The large acreage dedicated to corn cultivation and the rising income levels of farmers are key demand drivers in this region, increasingly embracing the Hybrid Seeds Market.

South America is another high-growth region for corn hybrids, with Brazil and Argentina being major contributors. The vast agricultural lands, favorable climatic conditions, and the significant role of corn in the Biofuel Feedstock Market and export-oriented agriculture bolster demand. The region is expected to demonstrate a CAGR of around 6.2%, propelled by continuous expansion of cultivated areas and the adoption of advanced seed technologies to maximize output and efficiency. Companies are actively expanding their presence and product portfolios here.

Europe, in contrast, exhibits a more modest growth rate, primarily due to stringent regulations and strong public opposition to genetically modified crops, which limits the penetration of the GMO Seeds Market. The focus in many European countries leans towards the Non-GMO Seeds Market and Specialty Corn Market, alongside conventional breeding for resilience and specific end-use quality. While there are pockets of growth for conventional hybrids, the overall regional CAGR is lower, estimated at about 3.5%, making it a more mature and slower-growing segment within the global corn hybrids Market. The demand here is often driven by specific silage corn or food-grade corn requirements.

Technology Innovation Trajectory in corn hybrids Market

The corn hybrids Market is at the forefront of agricultural innovation, with several disruptive technologies poised to reshape its future. One of the most impactful emerging technologies is gene editing, particularly CRISPR-Cas9. Unlike traditional genetic modification, gene editing allows for precise, targeted alterations to a plant's DNA without introducing foreign genetic material. This technology promises accelerated breeding cycles for desirable traits like enhanced nutrient uptake, improved photosynthesis efficiency, and even intrinsic disease resistance, potentially bypassing some regulatory hurdles associated with traditional GMOs. Adoption timelines are expected to shorten considerably, with initial commercial products focusing on quality traits rather than input traits, emerging within the next 3-5 years. R&D investment is significant, with both large agricultural firms and numerous biotech startups actively exploring gene-edited corn varieties. This could challenge incumbent business models by enabling smaller players to develop novel traits more efficiently, fostering a more diverse Agricultural Biotechnology Market.

Another critical innovation trajectory involves the integration of artificial intelligence (AI) and machine learning (ML) into breeding programs. AI algorithms can analyze vast datasets of genomic, phenotypic, and environmental data to predict optimal hybrid crosses, identify key genetic markers, and simulate crop performance under various conditions. This significantly enhances the efficiency and speed of developing new corn hybrids, reducing the time from discovery to market. AI also plays a crucial role in Precision Agriculture Market applications, optimizing planting density, fertilizer application, and irrigation, thereby maximizing the genetic potential of the hybrids in the field. Adoption of AI in breeding is already ongoing in advanced R&D centers, with broader commercial impact expected within 5-7 years. It reinforces incumbent models by enhancing their existing R&D capabilities but also allows for more tailored solutions, moving towards hyper-localized hybrid recommendations.

Finally, advanced sensor technologies and remote sensing (e.g., drone-based imaging) are transforming how hybrids are evaluated and managed. These technologies provide real-time, high-resolution data on plant health, growth rates, and stress levels across vast acreages. This allows breeders to make more informed selections and farmers to optimize the performance of specific corn hybrids. While these technologies primarily reinforce incumbent business models by providing better tools for existing products, they also pave the way for entirely new service offerings centered around data-driven agronomic advice, potentially disrupting traditional distribution channels for the Hybrid Seeds Market.

Supply Chain & Raw Material Dynamics for corn hybrids Market

The supply chain for the corn hybrids Market is complex, stretching from upstream genetic research and parent seed multiplication to downstream distribution to farmers. Upstream dependencies are highly concentrated, revolving around a few global agricultural biotechnology giants that hold proprietary genetic traits and intellectual property (IP). Key "raw materials" in this context include the foundational parent lines, which undergo extensive breeding and selection processes. Sourcing risks are significant, primarily stemming from biological vulnerabilities: an unforeseen disease outbreak in a parent seed production field could jeopardize the supply of specific hybrids for an entire season. Furthermore, the limited number of companies with extensive IP portfolios creates potential concentration risks, where disruptions at one major player could have cascading effects on the wider Hybrid Seeds Market.

Price volatility of key inputs directly impacts the cost structure of corn hybrids. While the seed itself is the primary product, its successful cultivation by farmers relies on other crucial agricultural inputs. Fertilizers (e.g., urea, phosphate, potash) and Crop Protection Market products (herbicides, insecticides, fungicides) are significant expenses. Geopolitical events, energy price fluctuations, and trade policies can cause sharp increases in fertilizer costs, for instance, with natural gas prices directly impacting nitrogen fertilizer production. Historically, spikes in global energy prices or disruptions in mining operations for phosphates have led to increased production costs for farmers, subsequently influencing their willingness to invest in premium corn hybrids. Similarly, the availability and pricing of raw materials for crop protection chemicals can affect integrated seed+chemical solutions offered by major players.

Supply chain disruptions have historically impacted the corn hybrids Market in various ways. Severe weather events in key seed production regions (e.g., droughts in North America, floods in South America) can reduce the yield of parent seeds, leading to shortages and delayed availability of certain hybrids. Trade disputes and export restrictions on agricultural inputs or finished seeds can also fragment the market, forcing companies to re-evaluate their global production and distribution networks. The COVID-19 pandemic, for example, highlighted fragilities in logistics and labor availability, causing temporary disruptions in seed movement and planting schedules. Effective supply chain management, including diversified production locations and robust inventory strategies, is paramount for mitigating these risks and ensuring stable delivery within the corn hybrids Market.

corn hybrids Segmentation

1. Application

1.1. Farmland

1.2. Greenhouse

1.3. Others

2. Types

2.1. GMOs Seeds

2.2. non-GMOs Seeds

corn hybrids Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

corn hybrids REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 5.56% from 2020-2034

Segmentation

By Application

Farmland

Greenhouse

Others

By Types

GMOs Seeds

non-GMOs Seeds

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Farmland

5.1.2. Greenhouse

5.1.3. Others

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. GMOs Seeds

5.2.2. non-GMOs Seeds

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Farmland

6.1.2. Greenhouse

6.1.3. Others

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. GMOs Seeds

6.2.2. non-GMOs Seeds

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Farmland

7.1.2. Greenhouse

7.1.3. Others

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. GMOs Seeds

7.2.2. non-GMOs Seeds

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Farmland

8.1.2. Greenhouse

8.1.3. Others

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. GMOs Seeds

8.2.2. non-GMOs Seeds

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Farmland

9.1.2. Greenhouse

9.1.3. Others

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. GMOs Seeds

9.2.2. non-GMOs Seeds

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Farmland

10.1.2. Greenhouse

10.1.3. Others

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. GMOs Seeds

10.2.2. non-GMOs Seeds

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Dupont

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Syngenta

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Monsanto

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Bayer

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. KWS

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Dow

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Origin Agritech

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. DLF

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Land O'Lakes

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Limagrain

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Pacific Seeds

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Zemun Polje

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. DeKalb Genetics

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.1.14. Seminis

11.1.14.1. Company Overview

11.1.14.2. Products

11.1.14.3. Company Financials

11.1.14.4. SWOT Analysis

11.1.15. Advanta

11.1.15.1. Company Overview

11.1.15.2. Products

11.1.15.3. Company Financials

11.1.15.4. SWOT Analysis

11.1.16. Sakata

11.1.16.1. Company Overview

11.1.16.2. Products

11.1.16.3. Company Financials

11.1.16.4. SWOT Analysis

11.1.17. Mycogen Seeds

11.1.17.1. Company Overview

11.1.17.2. Products

11.1.17.3. Company Financials

11.1.17.4. SWOT Analysis

11.1.18. Winfield Solutions

11.1.18.1. Company Overview

11.1.18.2. Products

11.1.18.3. Company Financials

11.1.18.4. SWOT Analysis

11.1.19. LG Seeds

11.1.19.1. Company Overview

11.1.19.2. Products

11.1.19.3. Company Financials

11.1.19.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Application 2025 & 2033

Figure 4: Volume (K), by Application 2025 & 2033

Figure 5: Revenue Share (%), by Application 2025 & 2033

Figure 6: Volume Share (%), by Application 2025 & 2033

Figure 7: Revenue (billion), by Types 2025 & 2033

Figure 8: Volume (K), by Types 2025 & 2033

Figure 9: Revenue Share (%), by Types 2025 & 2033

Figure 10: Volume Share (%), by Types 2025 & 2033

Figure 11: Revenue (billion), by Country 2025 & 2033

Figure 12: Volume (K), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Volume Share (%), by Country 2025 & 2033

Figure 15: Revenue (billion), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (billion), by Types 2025 & 2033

Figure 20: Volume (K), by Types 2025 & 2033

Figure 21: Revenue Share (%), by Types 2025 & 2033

Figure 22: Volume Share (%), by Types 2025 & 2033

Figure 23: Revenue (billion), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (billion), by Application 2025 & 2033

Figure 28: Volume (K), by Application 2025 & 2033

Figure 29: Revenue Share (%), by Application 2025 & 2033

Figure 30: Volume Share (%), by Application 2025 & 2033

Figure 31: Revenue (billion), by Types 2025 & 2033

Figure 32: Volume (K), by Types 2025 & 2033

Figure 33: Revenue Share (%), by Types 2025 & 2033

Figure 34: Volume Share (%), by Types 2025 & 2033

Figure 35: Revenue (billion), by Country 2025 & 2033

Figure 36: Volume (K), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Volume Share (%), by Country 2025 & 2033

Figure 39: Revenue (billion), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (billion), by Types 2025 & 2033

Figure 44: Volume (K), by Types 2025 & 2033

Figure 45: Revenue Share (%), by Types 2025 & 2033

Figure 46: Volume Share (%), by Types 2025 & 2033

Figure 47: Revenue (billion), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (billion), by Application 2025 & 2033

Figure 52: Volume (K), by Application 2025 & 2033

Figure 53: Revenue Share (%), by Application 2025 & 2033

Figure 54: Volume Share (%), by Application 2025 & 2033

Figure 55: Revenue (billion), by Types 2025 & 2033

Figure 56: Volume (K), by Types 2025 & 2033

Figure 57: Revenue Share (%), by Types 2025 & 2033

Figure 58: Volume Share (%), by Types 2025 & 2033

Figure 59: Revenue (billion), by Country 2025 & 2033

Figure 60: Volume (K), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

Figure 62: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Application 2020 & 2033

Table 2: Volume K Forecast, by Application 2020 & 2033

Table 3: Revenue billion Forecast, by Types 2020 & 2033

Table 4: Volume K Forecast, by Types 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Volume K Forecast, by Region 2020 & 2033

Table 7: Revenue billion Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue billion Forecast, by Types 2020 & 2033

Table 10: Volume K Forecast, by Types 2020 & 2033

Table 11: Revenue billion Forecast, by Country 2020 & 2033

Table 12: Volume K Forecast, by Country 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Volume (K) Forecast, by Application 2020 & 2033

Table 15: Revenue (billion) Forecast, by Application 2020 & 2033

Table 16: Volume (K) Forecast, by Application 2020 & 2033

Table 17: Revenue (billion) Forecast, by Application 2020 & 2033

Table 18: Volume (K) Forecast, by Application 2020 & 2033

Table 19: Revenue billion Forecast, by Application 2020 & 2033

Table 20: Volume K Forecast, by Application 2020 & 2033

Table 21: Revenue billion Forecast, by Types 2020 & 2033

Table 22: Volume K Forecast, by Types 2020 & 2033

Table 23: Revenue billion Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue billion Forecast, by Application 2020 & 2033

Table 32: Volume K Forecast, by Application 2020 & 2033

Table 33: Revenue billion Forecast, by Types 2020 & 2033

Table 34: Volume K Forecast, by Types 2020 & 2033

Table 35: Revenue billion Forecast, by Country 2020 & 2033

Table 36: Volume K Forecast, by Country 2020 & 2033

Table 37: Revenue (billion) Forecast, by Application 2020 & 2033

Table 38: Volume (K) Forecast, by Application 2020 & 2033

Table 39: Revenue (billion) Forecast, by Application 2020 & 2033

Table 40: Volume (K) Forecast, by Application 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Volume (K) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Volume (K) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Volume (K) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue billion Forecast, by Application 2020 & 2033

Table 56: Volume K Forecast, by Application 2020 & 2033

Table 57: Revenue billion Forecast, by Types 2020 & 2033

Table 58: Volume K Forecast, by Types 2020 & 2033

Table 59: Revenue billion Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (billion) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (billion) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (billion) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (billion) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue billion Forecast, by Application 2020 & 2033

Table 74: Volume K Forecast, by Application 2020 & 2033

Table 75: Revenue billion Forecast, by Types 2020 & 2033

Table 76: Volume K Forecast, by Types 2020 & 2033

Table 77: Revenue billion Forecast, by Country 2020 & 2033

Table 78: Volume K Forecast, by Country 2020 & 2033

Table 79: Revenue (billion) Forecast, by Application 2020 & 2033

Table 80: Volume (K) Forecast, by Application 2020 & 2033

Table 81: Revenue (billion) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue (billion) Forecast, by Application 2020 & 2033

Table 84: Volume (K) Forecast, by Application 2020 & 2033

Table 85: Revenue (billion) Forecast, by Application 2020 & 2033

Table 86: Volume (K) Forecast, by Application 2020 & 2033

Table 87: Revenue (billion) Forecast, by Application 2020 & 2033

Table 88: Volume (K) Forecast, by Application 2020 & 2033

Table 89: Revenue (billion) Forecast, by Application 2020 & 2033

Table 90: Volume (K) Forecast, by Application 2020 & 2033

Table 91: Revenue (billion) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research approach is the cornerstone of our market estimations, contributing approximately 75% of the total research effort. This extensive engagement ensures real-time insights and validation of secondary findings. We conduct in-depth, semi-structured interviews and discussions with a wide array of industry participants across the corn hybrids value chain. Our outreach spans multiple regions, including North America, South America, Europe, Asia Pacific, and MEA, capturing diverse market dynamics and perspectives. Every data point and insight gathered through primary interviews undergoes rigorous cross-validation to enhance accuracy and reliability. This direct interaction with industry experts allows us to understand current market trends, technological advancements, competitive landscapes, pricing strategies, supply chain nuances, and future outlooks directly from key opinion leaders.

Key stakeholders interviewed for this report include:

Head of R&D, Seed Development (e.g., at major seed breeders or agricultural biotechnology firms)

VP of Sales/Marketing, Crop Science Division (e.g., at global seed producers or regional distributors)

Farm Manager/Agronomist (at large-scale commercial corn farms or agricultural cooperatives)

Procurement Director, Agricultural Inputs (e.g., at major food processing companies or livestock feed manufacturers)

Companies engaged during the primary research phase broadly represent the following segments:

Secondary research accounts for approximately 25% of our overall methodology, providing foundational data, market landscapes, and validation points for our primary findings. This phase involves extensive data collection from credible and authoritative sources, ensuring comprehensive market intelligence. We meticulously cross-reference information from multiple sources to eliminate discrepancies and establish a robust factual basis. Our research is updated to the date of purchase, reflecting the latest market developments and data.

Sources leveraged include:

Government Publications & Regulatory Bodies: U.S. Department of Agriculture (USDA) reports on acreage, yields, and seed use (https://www.usda.gov/), European Commission agricultural data, national statistics agencies like Statistics Canada, Brazil's IBGE, and India's Ministry of Agriculture. These provide crucial data on planted areas, crop production, and government policies related to agricultural inputs.

Industry Associations: International Seed Federation (ISF) publications and statistics (https://www.worldseed.org/) for global seed trade and innovation, American Seed Trade Association (ASTA) market insights (https://www.betterseed.org/) for North American trends, and European Seed Association (ESA) reports (https://www.euroseeds.eu/) for European market dynamics. These sources offer valuable insights into industry best practices, regulatory challenges, and technological advancements.

Financial Databases: Bloomberg Terminals, Factiva, Hoovers, and PitchBook for company financials, investor presentations, annual reports, and competitive intelligence of key market players in the corn hybrids sector. These platforms provide a deep dive into the financial performance, strategic initiatives, and M&A activities of seed companies.

Academic Research & Scientific Journals: Peer-reviewed studies on corn genetics, biotechnology, sustainable agriculture practices, and crop yield optimization to inform technological advancements and future market potential.

We strictly avoid data from other market research websites to maintain the independence and integrity of our findings.

Demand Modeling & Market Estimation

Our market estimation framework employs a robust combination of top-down and bottom-up approaches, integrated with multi-level data triangulation to ensure maximum accuracy and reliability.

Bottom-Up Approach: This method involves segmenting the market at its most granular level, estimating demand and revenue for each segment, and then aggregating these figures to derive the total market size.

Specific variables used for bottom-up calculation in the corn hybrids market include:

Total Corn Planted Area (by region/country, in hectares/acres) - sourced from government agricultural departments.

Average Seed Usage Rate (seeds per hectare/acre, differentiated by GMO/non-GMO and specific hybrid types) - derived from primary interviews and agricultural extension reports.

Average Price per 1,000 Seeds/Seed Bag (varying by hybrid type, trait package, and regional market dynamics) - validated through primary interviews with distributors and farmers.

Market Share of Key Seed Producers (analyzed by specific hybrid segments, application, and geography) - informed by company reports and industry expert consensus.

Top-Down Approach: We start with the broader agricultural input market or the global corn market value and then disaggregate these figures down to the specific corn hybrids segment based on relevant market drivers, penetration rates, and industry expert insights.

Multi-Level Data Triangulation: Data derived from primary interviews, secondary sources, and our quantitative models are constantly cross-referenced and validated. This iterative process helps in reconciling discrepancies, strengthening estimates, and building confidence in the final market figures.

Data Accuracy & Quality Check

We are committed to delivering highly accurate and reliable market intelligence. Our stringent data quality control processes guarantee an estimated data accuracy level of 85-90%. This is achieved through:

Expert Validation: All market figures, forecasts, and qualitative insights are thoroughly reviewed and validated by a panel of internal senior analysts and external industry experts familiar with the corn hybrids market.

Source Verification: Every piece of data, whether primary or secondary, is traced back to its original source to ensure authenticity and credibility. Data from .gov, .org, and trade association sources are prioritized for their authoritative nature.

Quantitative Modeling & Scenario Analysis: Our in-house quantitative models are used to forecast market trends, incorporating various economic indicators, technological advancements, and regulatory changes pertinent to the agricultural sector. Sensitivity and scenario analyses are conducted to understand the impact of different variables (e.g., climate change, policy shifts, input costs) on market outcomes.

Continuous Updates: Our reports are dynamically updated up to the date of purchase, ensuring that clients receive the most current and relevant market information available. This real-time update mechanism incorporates the latest industry news, company developments, and regulatory announcements affecting the global corn hybrids market.

Frequently Asked Questions

1. What recent developments impact the corn hybrids market?

Major players like Bayer, Dupont, and Syngenta consistently invest in R&D to improve yield and disease resistance. While specific recent launches aren't detailed, innovation in GMOs and non-GMOs seeds is a constant driver across the industry.

2. Which end-user industries primarily drive demand for corn hybrids?

The primary demand for corn hybrids stems from farmland applications, crucial for large-scale crop production aimed at food, feed, and industrial uses. Greenhouse usage represents a smaller segment, with the overall market valued at $25.32 billion in 2025.

3. How has the corn hybrids market recovered post-pandemic?

The market for corn hybrids demonstrated resilience through the pandemic, maintaining a steady growth trajectory due to essential global food and feed demands. Structural shifts include an increased focus by companies like Monsanto and KWS on developing resilient varieties to ensure food security.

4. What are the current pricing trends for corn hybrids?

Pricing for corn hybrids is influenced by input costs, R&D investments, and demand for specific traits like pest resistance or drought tolerance. Premium GMOs seeds typically command higher prices than non-GMOs seeds due to their advanced genetic modifications and performance benefits.

5. Why is the corn hybrids market experiencing significant growth?

The market is driven by increasing global food and feed demand, coupled with the need for higher yield and improved crop protection. Innovation from companies like Dupont and KWS in new GMOs and non-GMOs varieties contributes to the 5.56% CAGR.

6. How does the regulatory environment impact the corn hybrids market?

Regulations surrounding GMOs seeds significantly influence market access and product development in various regions. Strict approval processes, particularly in Europe, can impact the speed and cost of bringing new hybrid varieties to market for companies like Dow and Origin Agritech.