1. メガネ用セルロースアセテート市場の主な製品タイプは何ですか?

市場は主にセルロースアセテートシートとセルロースアセテートブロックにセグメント化されています。これらはさまざまなアイウェア用途のために加工され、その他の特殊な製品タイプが残りの製品群を構成しています。

+1 2315155523

Sector Data Insights(SDI)は、高品質でデータ駆動型のシンジケート調査レポート、業界分析、競合インテリジェンス、およびアドバイザリーソリューションの提供に注力する、専門的なマーケットインテリジェンスおよび戦略的コンサルティング企業です。Sector Data Insightsは、特にライフサイエンス、分析機器、および関連するハイテク分野における分析の卓越性に強く重点を置いており、メーカー、投資家、サービスプロバイダー、研究者、および意思決定者が、戦略的成長、イノベーション、および市場のリーダーシップのための実用的な洞察を得られるように支援します。

SDIは、ラボおよび分析技術における深いドメインの専門知識と高度な分析を組み合わせて、包括的な市場評価、技術トレンド分析、ベンダーシェアデータ、投資インテリジェンス、サプライチェーンの洞察、および将来を見据えた予測を提供します。私たちの調査は、ライフサイエンス、半導体・電子機器、消費財、材料・化学、建設・製造、飲食料品、エネルギー・電力、自動車・輸送、ICT・メディア、航空宇宙・防衛、BFSIなどの業界にわたる複雑なグローバル市場をナビゲートする組織をサポートしています。

メガネ用セルロースアセテート

メガネ用セルロースアセテートSenior Analyst

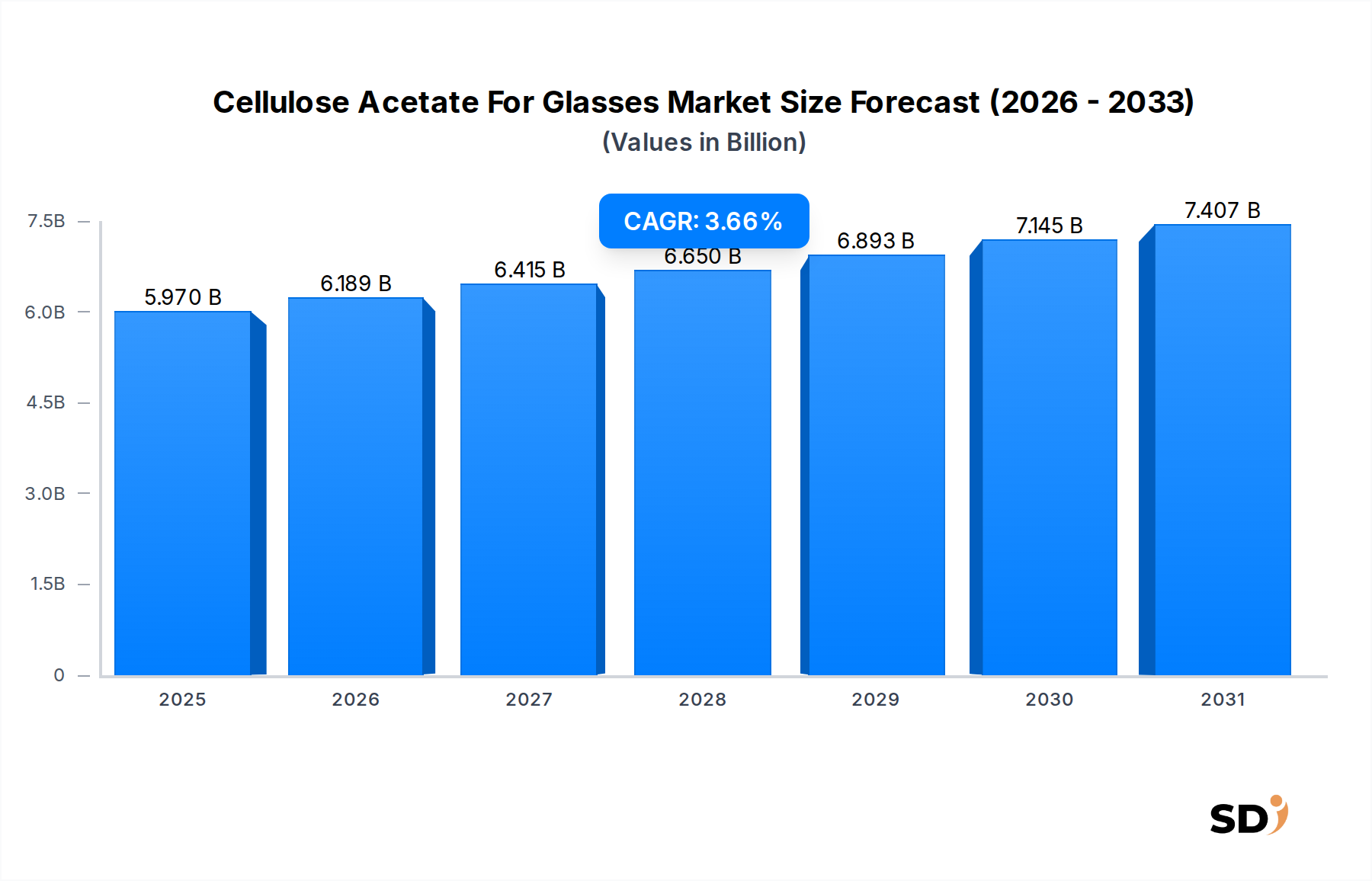

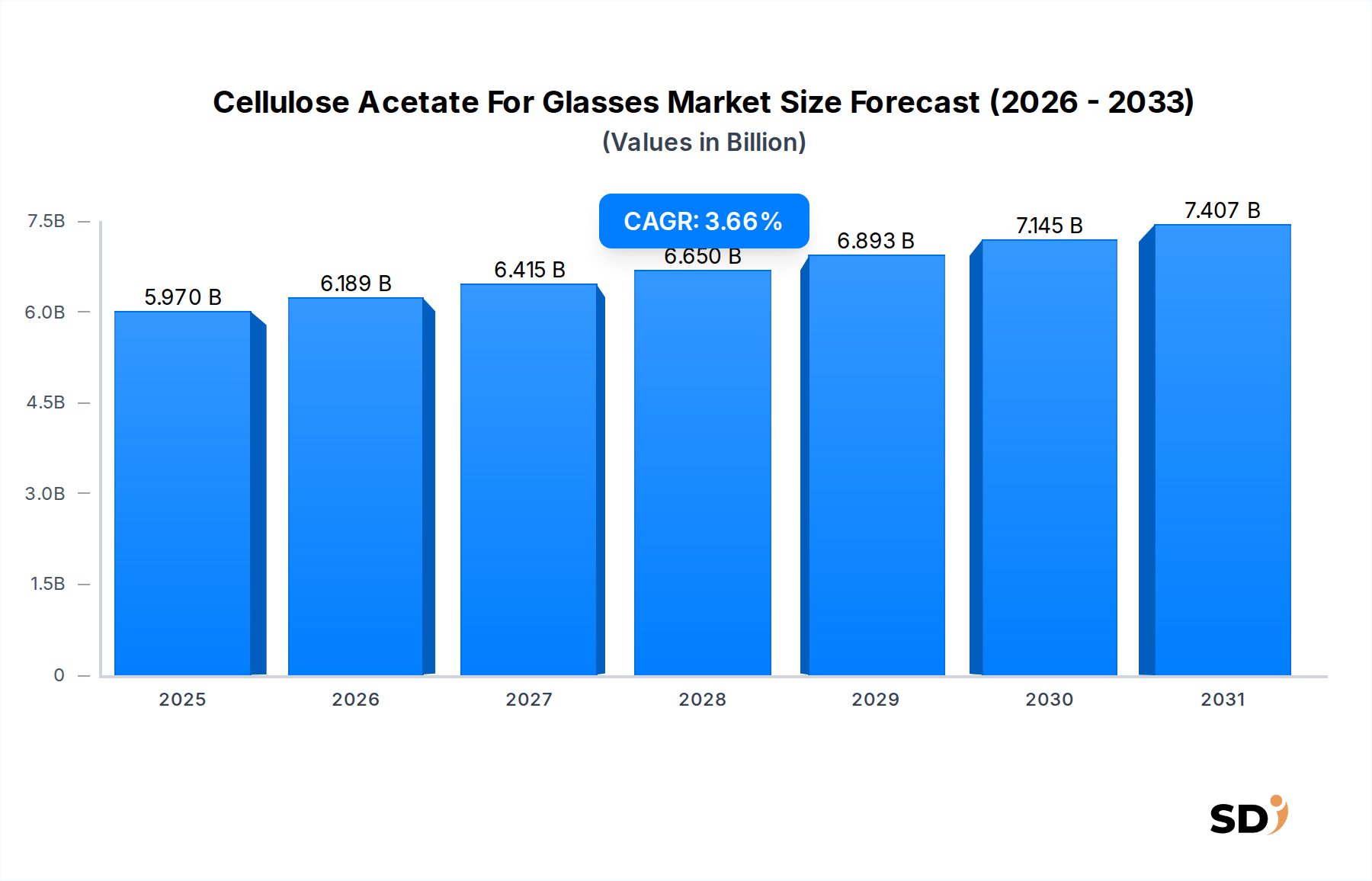

The global Cellulose Acetate For Glasses Market was valued at an estimated $5.97 billion in 2024, and it is projected to expand at a Compound Annual Growth Rate (CAGR) of 3.66% from 2024 to 2032. This consistent growth is primarily driven by cellulose acetate's unique combination of aesthetic versatility, excellent processability, and increasing demand for sustainable materials in the eyewear industry. As a bio-based polymer derived from cellulose, it offers a compelling alternative to petroleum-based plastics, aligning with evolving consumer preferences for environmentally responsible products. The material's inherent characteristics, such as its lightweight nature, durability, and hypoallergenic properties, make it a preferred choice for various frame types, including optical eyeglasses, sunglasses, and fashion eyewear.

The market's expansion is further propelled by macro tailwinds such as rising disposable incomes in emerging economies, the growing influence of fashion and luxury trends on eyewear choices, and the increasing prevalence of vision correction needs globally. The customization potential of cellulose acetate, allowing for a wide array of colors, patterns, and finishes, significantly contributes to its dominance, particularly in the premium and mid-range segments. The integration of advanced manufacturing techniques also plays a crucial role in enhancing product quality and design capabilities.

Looking forward, the Cellulose Acetate For Glasses Market is anticipated to reach approximately $7.96 billion by 2032, underpinned by continuous innovation in material science, which focuses on improving the material's performance characteristics like strength and scratch resistance, as well as enhancing its sustainable attributes through greener processing methods and recycled content integration. Key segments, such as Cellulose Acetate Sheets, continue to be pivotal, reflecting the market's reliance on traditional, high-quality manufacturing processes. The robust competitive landscape, comprising both established chemical manufacturers and specialized material suppliers, ensures a steady supply chain and continuous product development to meet the dynamic demands of global eyewear manufacturers and optical brands. This market's trajectory is firmly set towards innovation, sustainability, and aesthetic excellence.

Within the Cellulose Acetate For Glasses Market, the "Cellulose Acetate Sheets" segment stands out as the single largest contributor to revenue share, dominating the product landscape. This segment's pre-eminence is attributable to several intrinsic advantages and historical manufacturing preferences within the eyewear industry. Cellulose acetate sheets provide unparalleled aesthetic versatility, allowing designers to create intricate patterns, vibrant colorations, and rich textures that are difficult to replicate with other materials. The layered structure of the sheets enables depth and uniqueness in designs, which is a critical factor for the aesthetic-driven Luxury Eyewear Market and overall fashion eyewear.

The dominance of cellulose acetate sheets is further reinforced by the traditional methods of eyewear frame manufacturing. Techniques such as CNC machining, hand polishing, and lamination processing are ideally suited for working with sheets, enabling high levels of customization and artisan craftsmanship. This appeals to brands focused on quality and bespoke design, distinguishing their products in a competitive market. Key players like Mazzucchelli (イタリアのアイウェア素材メーカー、高品質セルロースアセテートシートの主要プロデューサー) and La/Es (イタリアのアイウェア素材メーカー、ファッション性の高いセルロースアセテートシートを提供) are renowned globally for their mastery in producing high-quality cellulose acetate sheets, offering a vast palette of colors and designs that set industry trends. JIMEI (中国のアイウェア素材メーカー、多様な色やデザインのセルロースアセテートシート・ブロックを供給) and other manufacturers also contribute significantly to this segment's robust supply.

While other forms like Cellulose Acetate Blocks Market exist, offering similar aesthetic benefits, sheets remain the primary choice due to their direct applicability in cutting and forming operations for a broader range of frame designs. The continuous innovation in sheet manufacturing, focusing on improved material properties such as enhanced flexibility, reduced weight, and increased resistance to warping, ensures that this segment maintains its leading position. Its share is not merely consolidating but rather growing, driven by the escalating demand for unique, high-quality, and customizable eyewear, particularly in fashion-forward regions. The ability to integrate advanced multi-layer designs and incorporate sustainable variants further solidifies the Cellulose Acetate Sheets Market's role as the foundational product type in the global Cellulose Acetate For Glasses Market, often differentiating premium products from mass-produced alternatives. This widespread adoption underscores the segment's critical role in shaping both product design and manufacturing methodologies.

Aesthetic Versatility and Design Freedom: A primary driver for the Cellulose Acetate For Glasses Market is the material's unparalleled aesthetic flexibility. Cellulose acetate allows for the creation of frames with a vast array of colors, patterns, and finishes, from transparent and vibrant hues to deep tortoiseshell and marble effects. This design freedom is crucial for eyewear manufacturers to cater to constantly evolving fashion trends and consumer demand for personalized and distinctive products. The ability to produce unique color combinations and complex patterns directly contributes to the growth of both the Optical Eyeglass Market and the Sunglass Market as fashion accessories. This design advantage helps justify premium pricing, particularly in the Luxury Eyewear Market, where distinctiveness is a key purchasing factor.

Sustainability and Biocompatibility: The bio-based nature of cellulose acetate positions it favorably amidst growing environmental consciousness. Derived from renewable resources like wood pulp, cellulose acetate is biodegradable under certain conditions, offering a more sustainable alternative to petroleum-based plastics. Furthermore, its hypoallergenic properties make it highly biocompatible, reducing the risk of skin irritation for wearers. This health and environmental benefit is a significant driver, with consumers increasingly prioritizing eco-friendly and safe products. The push towards sustainable materials is also influencing the broader Bioplastics Market, of which cellulose acetate is a key component.

Growth in Eyewear Demand and Fashion Integration: The increasing global prevalence of vision impairments, coupled with the rising adoption of eyewear as a fashion statement, significantly fuels market demand. As disposable incomes rise in emerging economies, consumers are more willing to invest in multiple pairs of glasses for different occasions, or to align with specific fashion trends. The convergence of eyewear with lifestyle and fashion industries has amplified the demand for high-quality, aesthetically pleasing materials like cellulose acetate. This trend benefits the entire Eyewear Manufacturing Market, as brands seek materials that offer both functional performance and stylistic appeal.

Constraints: Cost Competitiveness and Manufacturing Complexity: One significant constraint impacting the Cellulose Acetate For Glasses Market is its relatively higher cost compared to other common frame materials such as TR90 or nylon. While its premium quality justifies the cost for mid-range and luxury segments, this price point can limit its penetration into the mass-market or economy categories where cost-efficiency is paramount. Additionally, the manufacturing processes for cellulose acetate, especially sheet cutting and forming for intricate designs, can be more labor-intensive and require specialized machinery compared to injection molding of other plastics. This can contribute to higher production costs and longer lead times, potentially impacting scalability for some manufacturers. These factors necessitate careful material selection based on target market and desired product attributes.

The Cellulose Acetate For Glasses Market is characterized by a mix of large chemical manufacturers supplying raw materials and specialized sheet producers, alongside major eyewear brands that integrate these materials into their product lines. The competitive landscape is dynamic, with innovation in sustainable and performance-enhanced grades being a key differentiator.

The provided dataset did not contain specific recent developments or milestone events for the Cellulose Acetate For Glasses Market. However, the industry generally exhibits ongoing efforts and trends that can be considered significant:

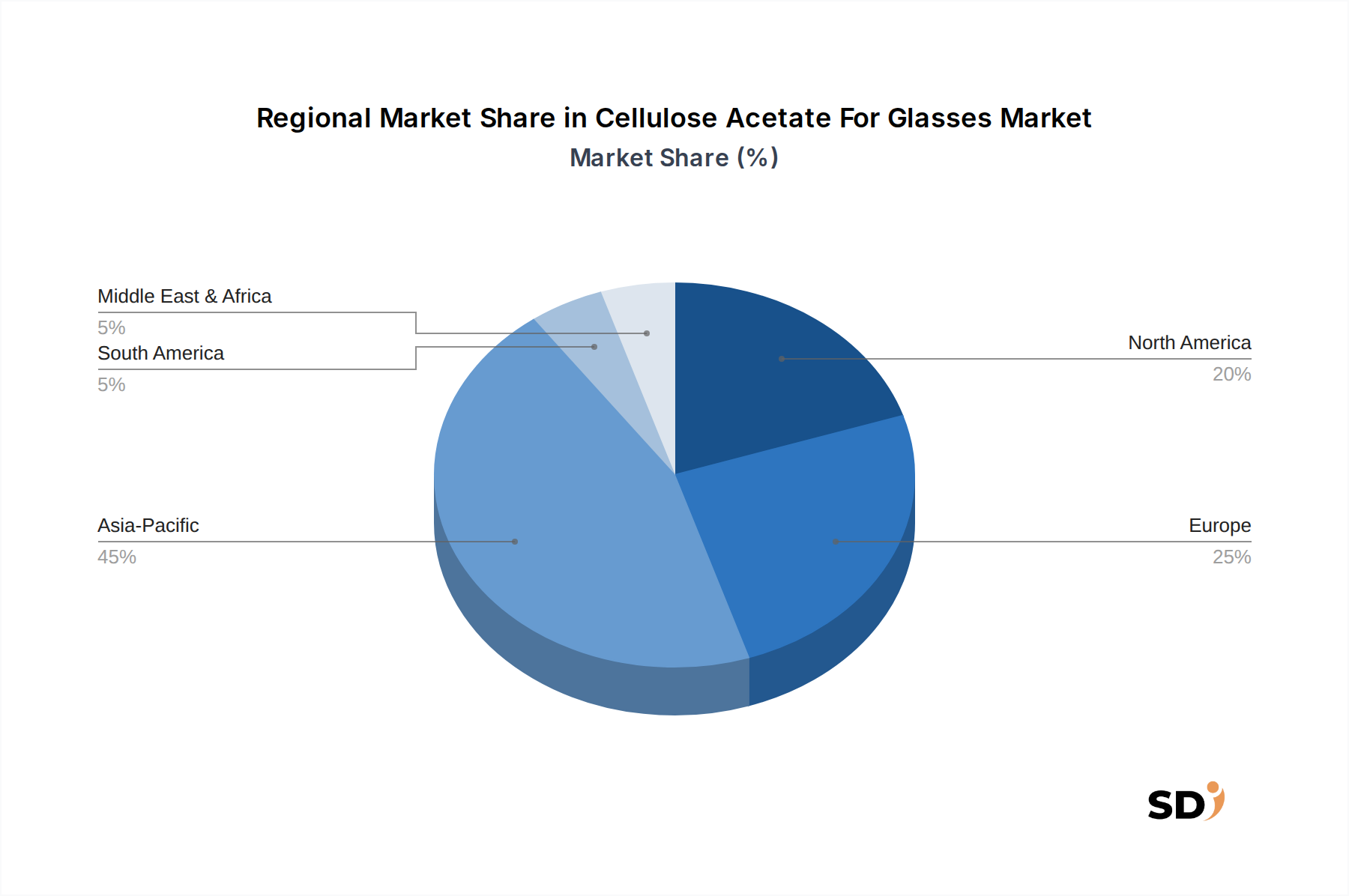

The global Cellulose Acetate For Glasses Market exhibits distinct regional dynamics driven by varying consumer preferences, economic conditions, and manufacturing landscapes. While specific regional CAGR and revenue share data were not provided in the dataset, a qualitative assessment reveals key trends across major geographies.

Asia Pacific is anticipated to be the fastest-growing region in the Cellulose Acetate For Glasses Market. This growth is propelled by a burgeoning middle class, increasing disposable incomes, and a strong fashion-conscious consumer base, particularly in countries like China, India, and ASEAN nations. Furthermore, Asia Pacific serves as a major manufacturing hub for eyewear, fostering a robust supply chain for cellulose acetate materials. The region's large population and rising prevalence of vision-related issues also contribute significantly to the demand for both optical and sunglass frames.

Europe represents a mature but highly significant market for cellulose acetate in eyewear. Characterized by a strong tradition of luxury and high-fashion brands, Europe demands premium materials with sophisticated aesthetics and high-quality craftsmanship. Countries like Italy, France, and Germany are leaders in eyewear design and manufacturing, driving consistent demand for cellulose acetate sheets. The focus here is on innovative designs, sustainable production, and maintaining a high standard of material quality, often leading to partnerships with specialized Cellulose Acetate Sheets Market suppliers.

North America holds a substantial share of the Cellulose Acetate For Glasses Market, driven by high consumer spending, a strong influence of fashion trends, and a developed retail infrastructure. The United States, in particular, demonstrates robust demand for diverse eyewear styles, from functional to high-fashion. Innovation in eyewear design and a consumer base willing to invest in premium and branded products are key demand drivers in this region. The market here is stable, with consistent demand for both Optical Eyeglass Market and Sunglass Market frames made from cellulose acetate.

Middle East & Africa and South America represent emerging markets with considerable growth potential. While currently smaller in terms of market share, these regions are experiencing increasing urbanization, improving economic conditions, and growing awareness of eyewear as both a necessity and a fashion accessory. Demand is gradually picking up, particularly in urban centers and for established international brands. As purchasing power rises, so does the appetite for aesthetically pleasing and high-quality materials like cellulose acetate. These regions are likely to witness accelerated growth as economic development continues and fashion trends become more globalized.

The Cellulose Acetate For Glasses Market is influenced by a diverse array of regulatory frameworks and policy initiatives, primarily centered around material safety, environmental sustainability, and product quality standards. These regulations vary by region but generally aim to ensure consumer safety and promote responsible manufacturing practices.

In Europe, the REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) regulation is paramount. It governs the manufacturing and import of chemical substances, including cellulose acetate and its precursor chemicals, ensuring that substances are safely managed. Eyewear products must also comply with the CE Mark requirements, which indicate conformity with EU health, safety, and environmental protection standards. Furthermore, the EU's focus on circular economy initiatives and waste reduction promotes the use of bio-based and biodegradable materials like cellulose acetate, and encourages responsible end-of-life management for products, indirectly supporting the Bioplastics Market. Policies promoting sustainable forest management, which is critical for Cellulose Pulp Market sourcing, also impact the upstream supply chain.

In North America, particularly the United States, the FDA (Food and Drug Administration) may have oversight on certain eyewear classified as medical devices (e.g., prescription spectacles), focusing on material biocompatibility and safety for prolonged skin contact. While general fashion eyewear is less strictly regulated than medical devices, manufacturers adhere to voluntary industry standards and consumer protection laws regarding material composition and labeling. Environmental regulations, such as those related to sustainable manufacturing and waste management, also play a role, encouraging the adoption of greener materials and processes.

Globally, standards organizations like the International Organization for Standardization (ISO) establish benchmarks for optical properties, mechanical strength, and chemical resistance of eyewear materials, which cellulose acetate must meet. There's a growing trend towards regulatory incentives for bio-based materials and biodegradable polymers, which could further boost the Cellulose Acetate For Glasses Market. Recent policy changes often lean towards promoting sustainable sourcing and manufacturing, pushing companies to demonstrate the environmental credentials of their products throughout the value chain. This shift creates both compliance challenges and market opportunities for cellulose acetate producers and eyewear manufacturers who can demonstrate robust sustainability practices.

The Cellulose Acetate For Glasses Market is at the forefront of several technological innovations, primarily focused on enhancing material properties, improving manufacturing efficiency, and bolstering sustainability credentials. These advancements threaten traditional methods in some areas while reinforcing incumbent business models in others.

One significant area of innovation is Advanced Material Compounding and Functionalization. Researchers and manufacturers are developing new grades of cellulose acetate with enhanced performance characteristics. This includes incorporating additives to improve flexibility, increase impact resistance (reducing brittleness), enhance scratch resistance, and provide better UV protection without compromising the material's aesthetic appeal or biocompatibility. For instance, new formulations might offer lighter weight or improved thermal stability, making the material more versatile for various frame designs and manufacturing processes. These innovations extend the functional lifespan of frames and improve wearer comfort, reinforcing the material's position in the premium eyewear segment. Adoption timelines for these improved grades are relatively swift, often seen within 2-3 years of lab development, as the Specialty Chemicals Market suppliers race to offer competitive solutions. R&D investments are high as companies like Celanese and Eastman focus on proprietary formulations to gain a competitive edge.

Another disruptive technology involves Precision Manufacturing and Automation. While traditional sheet cutting and forming remain prevalent, there's increasing adoption of advanced CNC machining and robotic automation in the production of cellulose acetate frames. This allows for intricate designs, higher precision, reduced material waste, and faster production cycles, especially for complex geometries that were previously difficult to achieve. Furthermore, the potential for 3D Printing with Cellulose Acetate is an emerging area. While direct 3D printing of pure cellulose acetate is still nascent due to challenges in melt processability, advancements in composite materials and binder jetting techniques are showing promise for rapid prototyping and bespoke frame production. If commercially viable, 3D printing could drastically shorten design-to-market cycles and enable unparalleled customization, potentially disrupting the Eyewear Manufacturing Market by offering on-demand production. However, widespread adoption is likely 5-10 years away, requiring significant R&D investment to overcome material processing hurdles and scale production for mass markets. These technologies aim to lower costs and increase efficiency, reinforcing the long-term viability of cellulose acetate as a primary eyewear material while also opening avenues for entirely new business models focused on personalized eyewear manufacturing.

日本のセルロースアセテート眼鏡市場は、世界市場の成長トレンドに沿いつつも、独自の特性を持っています。市場規模は、眼鏡全体の普及率とファッションアイテムとしての需要の高まりを背景に、安定した成長が見込まれます。高齢化社会における視力矯正ニーズの増加や、若年層におけるファッションアイウェアとしての需要が市場を牽引しています。国内では、セルロースアセテートシートが眼鏡フレーム製造における主要な素材として位置づけられており、その多様な色合い、模様、質感は、日本の精密な職人技と融合し、高品質な眼鏡製造を支えています。特に、鯖江市に代表される眼鏡産業集積地では、高度な加工技術とデザイン力が強みとなっており、国内外のブランドに素材や製品を供給しています。 主要な国内企業としては、セルロースアセテートの原料供給に関わる化学メーカーや、眼鏡フレーム用素材を製造・供給する専門メーカーが挙げられます。具体的には、ダイセル(Daicel)のような日本の化学大手は、セルロースアセテートの主要サプライヤーとして、高品質な素材を提供しています。また、多様なデザインと色調のセルロースアセテートシートを製造する企業も、日本の眼鏡メーカーやOEM/ODMサプライヤーにとって重要なパートナーとなっています。 規制面では、眼鏡フレームは一般的に「雑貨」として扱われることが多いですが、人体への安全性(アレルギー反応の有無など)や、素材の表示に関する自主規制や業界基準が影響します。また、環境意識の高まりから、持続可能な素材調達やリサイクル素材の利用を推奨する動きが、間接的にセルロースアセテートのようなバイオベース素材の利用を後押しする可能性があります。 流通チャネルとしては、大手眼鏡チェーン店、百貨店内ブランドショップ、眼鏡専門店、そして近年ではオンラインストアが主要な販売経路となっています。消費者の行動パターンとしては、品質、デザイン、ブランドイメージを重視する傾向が強く、特に高価格帯の製品では、素材の希少性や職人技へのこだわりが購買決定に大きく影響します。また、機能性(UVカット、ブルーライトカットなど)とデザイン性を両立させた製品への関心も高まっています。為替レートによっては、輸入素材のコスト変動が国内価格に影響を与える可能性もあります。

| 項目 | 詳細 |

|---|---|

| 調査期間 | 2020-2034 |

| 基準年 | 2025 |

| 推定年 | 2026 |

| 予測期間 | 2026-2034 |

| 過去の期間 | 2020-2025 |

| 成長率 | 2020年から2034年までのCAGR 3.66% |

| セグメンテーション |

|

当社の厳格な調査手法は、多層的アプローチと包括的な品質保証を組み合わせ、すべての市場分析において正確性、精度、信頼性を確保します。

市場情報に関する正確性、信頼性、および国際基準の遵守を保証する包括的な検証ロジック。

500以上のデータソースを相互検証

200人以上の業界スペシャリストによる検証

NAICS, SIC, ISIC, TRBC規格

市場の追跡と継続的な更新

市場は主にセルロースアセテートシートとセルロースアセテートブロックにセグメント化されています。これらはさまざまなアイウェア用途のために加工され、その他の特殊な製品タイプが残りの製品群を構成しています。

需要は主にアイウェアメーカー、オプティカルブランド、ラグジュアリーアイウェアブランドによって牽引されています。これらのユーザーは、オプティカルグラス、サングラス、リーディンググラス、ファッションアイウェアに素材を使用しており、下流の素材加工に影響を与えています。

入力データには、最近のM&A活動または製品発売に関する情報は記載されていません。しかし、Celanese、Daicel、Solvayなどの主要企業は、アイウェア用途における製品性能と持続可能性を向上させるために、常に素材科学の革新を続けています。

メガネ用セルロースアセテートの国際貿易フローは、地域的な製造業の集積と世界的なアイウェア需要によって牽引されています。原材料生産または加工能力が強い国は、アイウェアの組み立てと消費率が高い地域に輸出しています。

障壁には、射出成形やCNC加工などの特殊な製造プロセスに対する多額の資本投資、アイウェア用途に対する厳格な品質要件、MazzucchelliとLuxotticaなどの主要アイウェアブランドとの間の確立されたサプライヤー関係が含まれます。

アジア太平洋地域は、特に中国におけるセルロースアセテート生産とアイウェア組立の両方の堅調な製造基盤により、 significantな市場シェアを占めると予測されています。この地域は、アイウェア製品の巨大な消費者市場からも恩恵を受けています。