1. 環境規制は銅スクラップ市場にどのように影響しますか?

特に廃棄物管理と材料リサイクルに関する環境規制は、銅スクラップ市場に大きな影響を与えます。コンプライアンスは、湿式製錬や乾式製錬などの処理技術への需要を促進し、持続可能な材料回収を保証します。より厳しい基準は、処理コストを増加させ、世界中のスクラップの流れに影響を与える可能性があります。

+1 2315155523

Sector Data Insights(SDI)は、高品質でデータ駆動型のシンジケート調査レポート、業界分析、競合インテリジェンス、およびアドバイザリーソリューションの提供に注力する、専門的なマーケットインテリジェンスおよび戦略的コンサルティング企業です。Sector Data Insightsは、特にライフサイエンス、分析機器、および関連するハイテク分野における分析の卓越性に強く重点を置いており、メーカー、投資家、サービスプロバイダー、研究者、および意思決定者が、戦略的成長、イノベーション、および市場のリーダーシップのための実用的な洞察を得られるように支援します。

SDIは、ラボおよび分析技術における深いドメインの専門知識と高度な分析を組み合わせて、包括的な市場評価、技術トレンド分析、ベンダーシェアデータ、投資インテリジェンス、サプライチェーンの洞察、および将来を見据えた予測を提供します。私たちの調査は、ライフサイエンス、半導体・電子機器、消費財、材料・化学、建設・製造、飲食料品、エネルギー・電力、自動車・輸送、ICT・メディア、航空宇宙・防衛、BFSIなどの業界にわたる複雑なグローバル市場をナビゲートする組織をサポートしています。

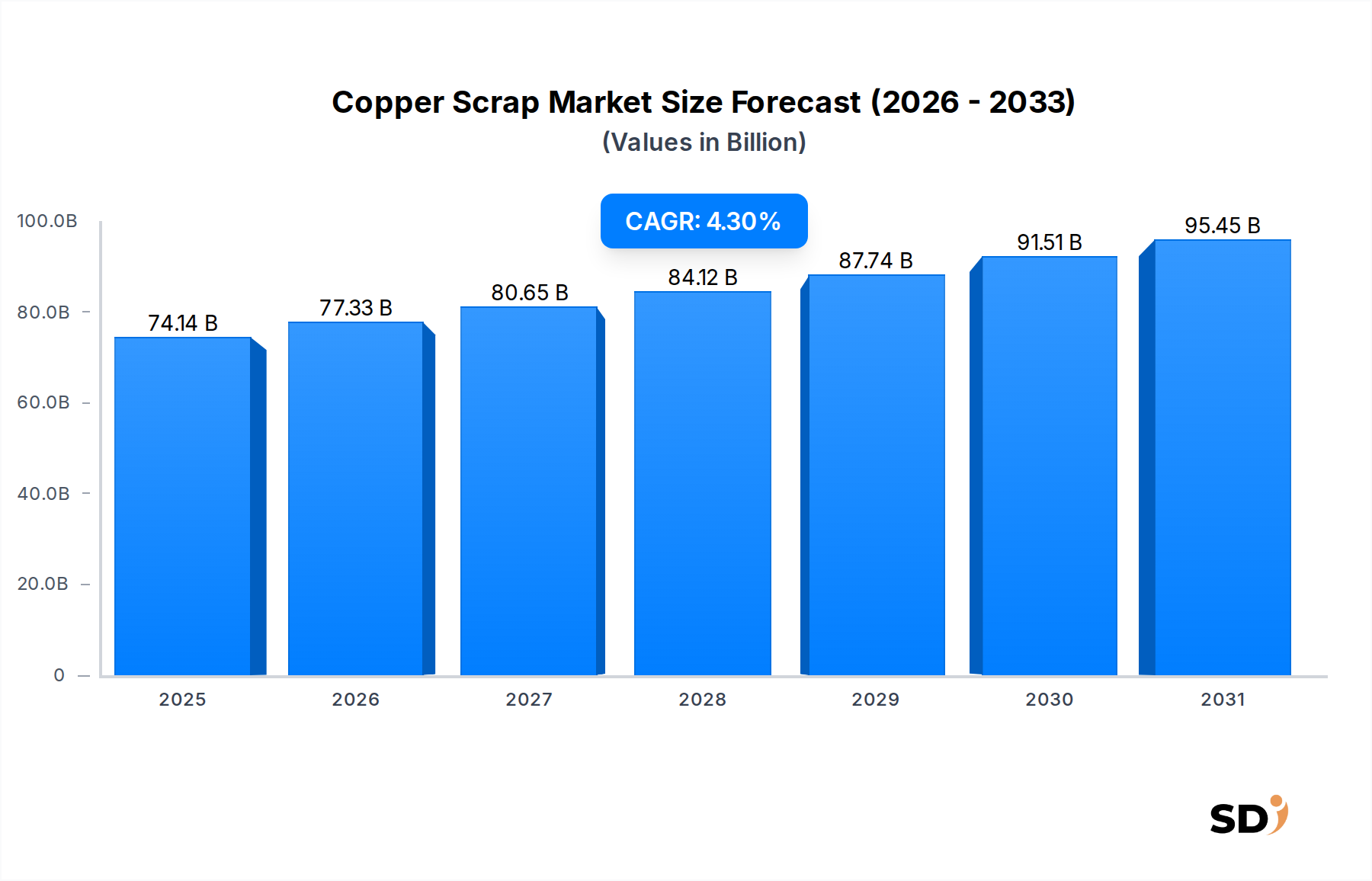

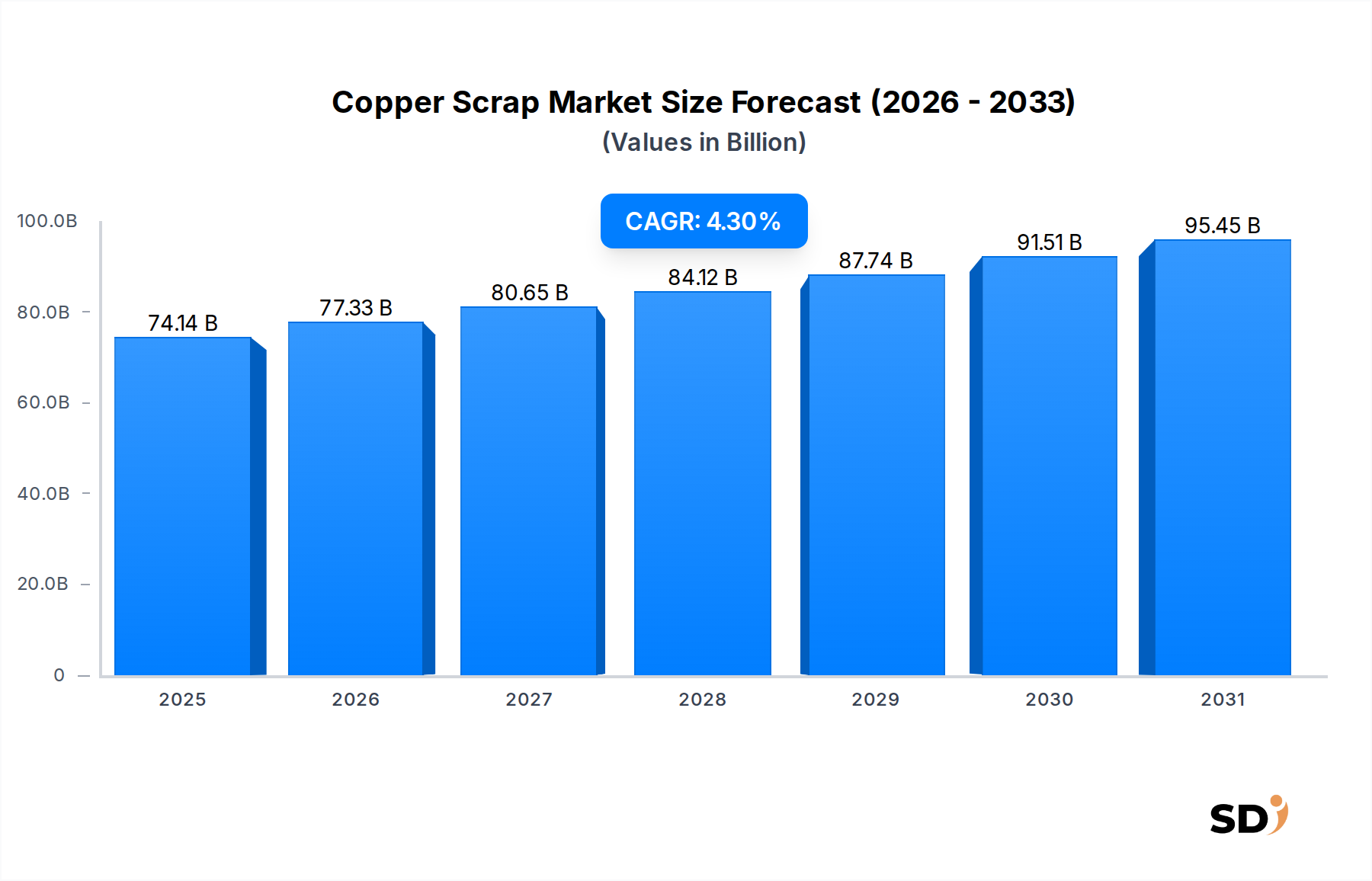

世界の銅スクラップ市場は、予測期間終了までに741億4,000万ドル(約1,112兆円)の評価額を達成し、4.3%の複合年間成長率(CAGR)で成長すると予測されています。この成長軌道は、産業需要を満たし、循環型経済の原則を推進する上で、リサイクル銅が果たす極めて重要な役割を強調しています。この市場の拡大の主な要因には、特に急成長する電気・電子市場および堅調な建設市場内での、様々な最終用途産業における銅の需要の高まりが含まれます。世界経済が持続可能な材料調達を目指す中、新品の銅生産に代わる費用対効果が高く環境に優しい代替手段を提供する、古銅および新銅スクラップへの依存が intensifies します。

機械的および溶金法を含むスクラップ処理における技術的進歩は、回収率をさらに最適化し、リサイクル銅の品質を向上させ、それによってその競争力を高めています。一次銅抽出と比較してエネルギー消費と温室効果ガス排出量を大幅に削減するリサイクルの固有の効率性は、銅スクラップ市場を、より広範な金属リサイクル市場の重要な構成要素として位置づけています。さらに、地政学的な変動や一次金属市場におけるサプライチェーンの脆弱性は、国内および地域的なスクラップサプライチェーンの戦略的重要性 を高めています。電気自動車および再生可能エネルギーインフラストラクチャでの銅の採用の増加は、高純度のリサイクル銅に対する持続的な需要を保証する、重要なマクロ経済の追い風です。成熟した産業基盤と確立されたリサイクルインフラストラクチャを持つ国は、このトレンドから恩恵を受ける一方、開発途上国は収集および処理能力に急速に投資しています。長期的な見通しは、継続的な都市化、工業化、および資源効率に対する世界的なコミットメントによって、依然としてポジティブであり、銅スクラップ市場を多様な製造セクターにとって重要なリソースストリームとしています。

使用済み製品および寿命を終えた製品を表す「旧スクラップ」セグメントは、銅スクラップ市場内で支配的なカテゴリーであり、 substantial な収益シェアを占めています。この優位性は、銅含有製品の寿命と様々なセクターから廃棄される材料の広範な入手可能性に intrinsically linked しています。旧スクラップの供給源には、廃止された電気配線、配管、自動車部品、および時代遅れの産業機械が含まれます。これらの成熟したアプリケーションからのリサイクルストリームに入る材料の sheer volume は、処理業者に安定した large volume の供給を保証します。このセグメント内で operating する主要プレイヤーは、しばしば extensive な収集ネットワーク、 advanced sorting technologies、および解体会社、廃棄物管理会社、その他のスクラップ発生業者との確立された関係を保有しています。

旧スクラップカテゴリー内では、No.1 Copper Market(裸、コーティングなし、合金化されていない銅線およびケーブル、パイプ、および固体)および Insulated Copper Wire Scrap Market のようなサブセグメントは、 particularly valuable です。No.1 Copper は、その high purity のため、 premium prices を獲得し、製錬業者および精製業者によって direct melting または alloy production に highly sought after されています。Insulated Copper Wire Scrap Market の処理は、 more complex ですが、 special machinery を使用して断熱材から銅を分離し、全体的な旧スクラップ供給に significant volume を貢献しています。旧スクラップセグメントの市場シェアは、主に都市および産業解体からの廃棄物の continuous generation と、世界的な urban mining initiatives への increasing focus の combination により、dominant のままであると予想されます。New Scrap セグメント(製造廃棄物)は、 higher purity と lower contamination を提供しますが、その volume は製造 output に directly tied されており、 vast reservoir of old scrap よりも less consistent です。旧スクラップの収集および処理セクター内での consolidation は、より広範な地域でのリーチを拡大し、処理効率を向上させるために、より大きなプレーヤーが smaller, regional 企業を買収するにつれて observed されています。この strategic consolidation は、integrated recyclers および primary copper producers に raw material の stable supply を確保することを目的としており、これらは environmental regulations および cost objectives を満たすために secondary raw materials への依存を increasing しています。建設市場の成長も、古い構造物が廃止されるにつれて、旧スクラップの将来的な入手可能性と directly correlates しています。

いくつかのマクロ経済の追い風と進化するサプライチェーンのダイナミクスが、銅スクラップ市場を significant に形成しています。主要なドライバーは、特に 自動車市場 および電気・電子市場における、 global electrification trend の加速です。電気自動車(EV)生産の rapid expansion は、従来の車両よりも substantial に多くの銅を必要とし、 primary および secondary 銅資源の両方に対する需要の増加に directly translates します。例えば、EVは、内燃機関(ICE)車両の20 kgと比較して、最大83 kgの銅を含めることができます。これにより、 primary サプライを supplement するために銅スクラップに対する powerful pull が生まれます。同様に、ソーラーパネルや風力タービンを含む再生可能エネルギーインフラストラクチャは、銅を highly copper-intensive であり、 gigawatt-scale プロジェクトが substantial な long-term demand を driving しています。

もう一つの重要な要因は、 decarbonization および resource efficiency に対する global imperative です。銅のリサイクルは、 virgin copper mining および smelting と比較して、 significantly less energy(最大85-90% less)を消費し、 fewer CO2 emissions を生成します。この environmental advantage は、 carbon footprint を削減し、 stringent environmental regulations を遵守することを目指す産業にとって、リサイクル銅を preferred material にしています。Primary copper mining および concentrate supply chains に associated する volatility および geopolitical risks は、 robust Copper Scrap Market の strategic importance を further elevates します。Major mining regions または trade disputes における disruption は、リサイクルソースへの demand を rapidly shift させ、価格を安定させ、 manufacturing sectors の supply continuity を保証することができます。さらに、 global manufacturing の expansion 、 particularly in developing economies 、 continuously generates new scrap (製造副産物)と feeds the pipeline for old scrap (最終製品)を、銅スクラップ市場のための supply and demand の self-reinforcing cycle を作成します。Brass Market の sustained growth 、 significant consumer of copper scrap 、 also underpins demand.

銅スクラップ市場は、 large, integrated global players から specialized regional recyclers まで、 diverse competitive landscape を特徴としています。Strategic capabilities は、 efficient collection networks 、 advanced processing technologies 、および wire rod mills 、 brass mills 、 ingots makers のような downstream consumers との strong customer relationships を中心に展開されることが often です。

過去2〜3年間の銅スクラップ市場における投資および資金調達活動は、主に processing capacity の拡大、 technological capabilities の向上、および robust supply chains の確保に centered してきました。Major M&A activities では、 larger recycling conglomerates が smaller, regional players を買収し、 collection networks を統合し、 economies of scale を達成しています。これらの strategic moves は、 critical raw material flows を control し、 market penetration を向上させることを目的としており、 particularly in regions with burgeoning industrial output and increasing scrap generation 。Companies はまた、 advanced sorting and separation technologies 、 particularly for mixed metal streams and complex materials like Insulated Copper Wire Scrap Market 、 to maximize recovery rates and purity に heavily investing しています。例えば、 sensor-based sorting 、 artificial intelligence (AI) driven material identification 、および robotic systems における innovations は significant capital を attracting しています。

さらに、 Hydrometallurgical Processing Market および Pyrometallurgical Processing Market facilities の開発および scaling に向けた investment の notable uptick が見られます。これらの technologies は、 lower-grade scrap および complex alloys からの superior purity yields を提供し、 electrical and electronics market および automotive market の demanding applications に required される high-spec copper を生産するために crucial です。Venture funding rounds は、 high-tech sectors よりも less frequent ですが、 difficult-to-recycle materials のための novel solutions を提供する startup や、 blockchain または IoT を使用して supply chain transparency および traceability を改善する startup を increasingly targeting しています。Scrap processors と primary copper producers の間の strategic partnerships が形成されており、後者は sustainability targets を満たし、 volatile raw material costs を緩和するために、 their production に more recycled content を統合することを目指しています。電子廃棄物(e-waste)からの high-purity copper recovery および processing に焦点を当てた sub-segments が、 materials に関する high copper content および environmental regulations によって driving され、 most capital を attracting しています。これらの investments は、 copper scrap market における rising demand を満たすために crucial です。

銅スクラップ市場における最近の動向は、 sustainability 、 technological advancement 、および growing industrial demand を満たすための strategic expansion への commitment を強調しています。

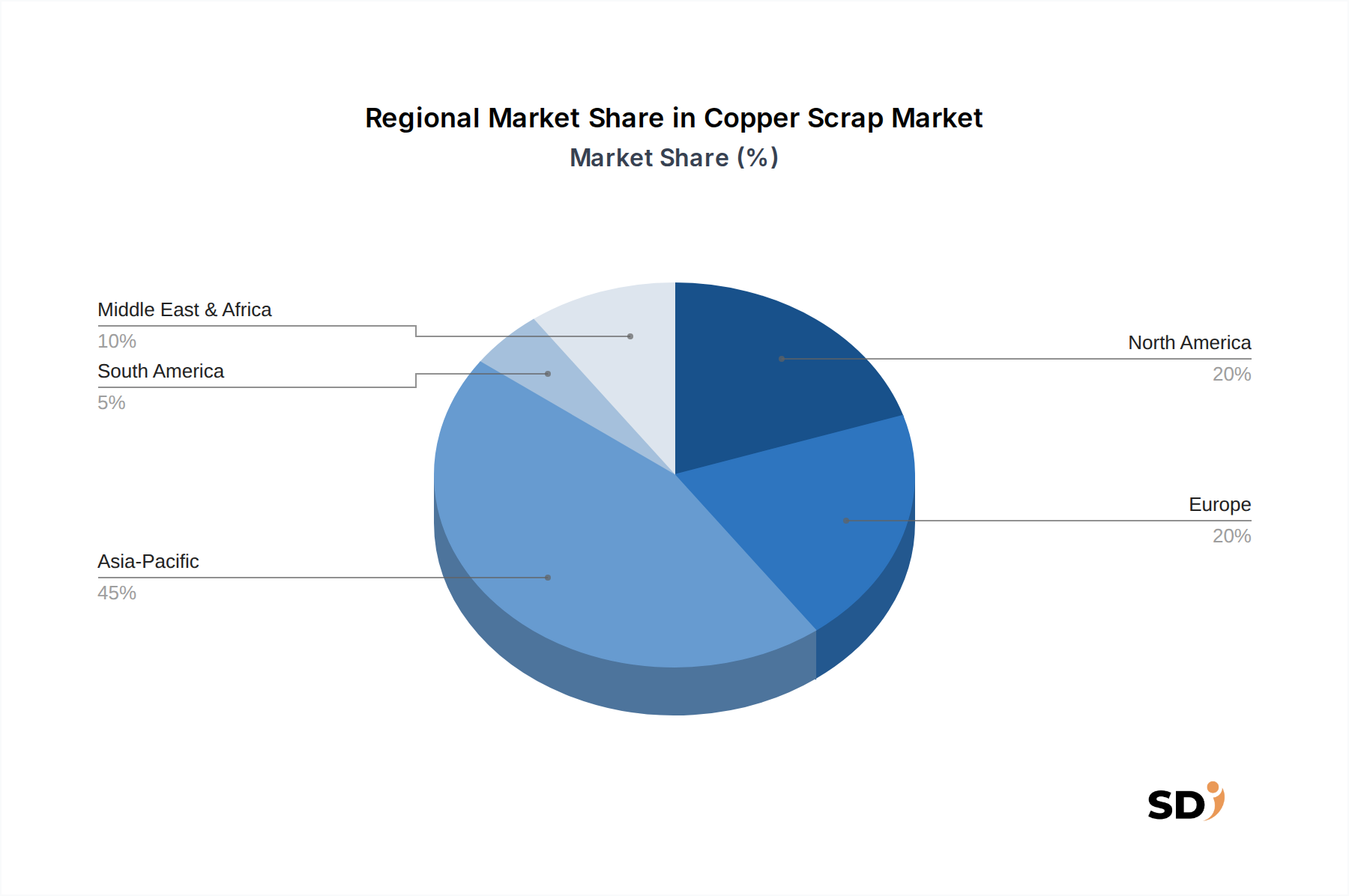

Metals Recycling Market capabilities を強化することを目指しています。Electrical and Electronics Market は、 minimum of 30% recycled copper content の使用を stated commitment とする new product line を発表し、 downstream industries が sustainable materials を demand する increasing trend を示しています。Pyrometallurgical Processing Market techniques を実証する pilot facility を launch し、 higher efficiency and lower emissions を達成しました。Brass Market および other alloy production sectors からの strong pull を示しています。Automotive Market manufacturer と metals recycling company の間で、 end-of-life vehicle components のための closed-loop recycling program を確立し、 copper scrap の steady stream を保証するために締結されました。銅スクラップ市場は、 varying industrialization levels 、 regulatory frameworks 、および recycling infrastructures によって driving され、 key global regions を横断して distinct characteristics を示しています。Asia Pacific 、 particularly China and India 、は volume の面で市場を支配しており、 fastest-growing region としても projected されています。この成長は、 massive industrial expansion 、 rapid urbanization 、および particularly in the Electrical and Electronics Market and Building and Construction Market における burgeoning manufacturing base によって fuel されています。Exact regional CAGRs は provided されていませんが、 infrastructure development 、 consumer electronics 、および renewable energy projects のための these economies における immense demand は、 imported および domestically generated copper scrap の両方に対する high intake を保証しています。Asia Pacific における primary demand driver は、 copper を fundamental input として requiring industrial output の sheer scale であり、 improving scrap collection and processing capabilities と coupled されています。

Europe は、 robust recycling infrastructure および stringent environmental regulations を持つ mature Copper Scrap Market を represent しています。The region boasts advanced Metals Recycling Market technologies 、 including sophisticated Hydrometallurgical Processing Market and Pyrometallurgical Processing Market facilities 、 allowing for high-purity recovery of copper 。Europe's demand は、 Automotive Market および various industrial machinery applications を含む established manufacturing sectors 、 along with a strong emphasis on circular economy principles and reducing reliance on virgin materials 、によって driving されています。Growth は Asia Pacific よりも slower であるかもしれませんが、 high-quality, sustainably sourced copper scrap への focus は strong のままです。

North America もまた、 well-established collection networks および processing capabilities を持つ mature market を構成しています。Demand は primarily driven by its significant industrial base 、 including the construction and transportation sectors 、および domestic sourcing of raw materials への growing emphasis 。The region benefits from strong regulatory support for recycling および technological investments to enhance recovery 。While facing competition from imported scrap 、 North America's robust end-use industries 、 such as the Building and Construction Market 、 ensure consistent demand 。Middle East & Africa および South America regions は、 varying levels of recycling infrastructure を持つ emerging markets を represent しています。These regions における growth は、 industrialization および infrastructure development projects と increasingly tied されており、 copper scrap の generation および consumption の両方の rise につながっていますが、 more developed regions よりも lower base からです。These regions は、 rising local demand を満たすために their scrap collection and processing capacities を improving することに actively investing しています。

Technology innovation は、 Copper Scrap Market の evolution における critical enabler であり、 particularly in maximizing resource recovery and enhancing material purity 。Two of the most disruptive emerging technologies は、 advanced sensor-based sorting systems および sophisticated Hydrometallurgical Processing Market methods です。Advanced sensor-based sorting 、 often incorporating near-infrared (NIR), X-ray transmission (XRT), and artificial intelligence (AI)-driven visual recognition 、 is revolutionizing scrap classification 。These systems can precisely identify and separate various copper alloys and grades 、 including different types of Insulated Copper Wire Scrap Market 、 at high throughput rates 。This significantly reduces manual sorting labor 、 improves material purity 、 and ultimately increases the value of the recycled product 。Adoption timelines for these technologies are accelerating 、 with major recycling facilities globally investing in upgrades 。R&D investments are substantial 、 focusing on improving sensor accuracy for complex mixtures および developing AI algorithms that can adapt to diverse scrap compositions 。This innovation threatens incumbent business models reliant on less efficient, labor-intensive manual sorting 、 while reinforcing those that embrace high-tech automation to achieve superior material specifications 。

Concurrently 、 Hydrometallurgical Processing Market is gaining traction as a highly efficient and environmentally cleaner alternative to traditional Pyrometallurgical Processing Market for certain copper scrap streams 。Hydrometallurgical processes involve using aqueous solutions to leach copper from scrap 、 followed by solvent extraction and electrowinning to produce high-purity copper cathode 、 often exceeding 99.99% purity 。This technology is particularly valuable for processing lower-grade copper scrap 、 complex alloys 、 and electronic waste 、 which may contain impurities detrimental to direct melting in pyrometallurgical furnaces 。The adoption timeline for large-scale hydrometallurgical plants is longer due to capital intensity and process complexity 、 but smaller, modular systems are emerging 。R&D is focused on developing more selective and environmentally benign leaching agents 、 optimizing energy consumption 、 and reducing effluent generation 。While not replacing pyrometallurgy entirely 、 hydrometallurgy offers a complementary pathway that reinforces circular economy principles by unlocking value from challenging secondary resources 、 potentially threatening traditional smelting operations for certain feedstocks while creating new opportunities for specialized refiners 。The high-purity output from these methods is crucial for the demanding requirements of the Electrical and Electronics Market 。

日本の銅スクラップ市場は、成熟した産業基盤、先進的なリサイクル技術、そして循環型経済への強いコミットメントに支えられ、世界の市場において重要な位置を占めています。市場規模は、経済産業省の金属資源統計年報などから示唆されるように、年間約100万トン以上の銅スクラップが流通していると推定され、その価値は数百億円規模に達すると考えられます。この市場は、一次銅の調達リスク軽減、資源の有効活用、および環境負荷低減の観点から、経済産業省をはじめとする政府機関によって戦略的に重要視されています。特に、電気自動車(EV)の普及、再生可能エネルギーインフラの拡大、そして老朽化したインフラの更新といったトレンドは、高純度銅スクラップへの需要を継続的に押し上げています。国内の主要企業としては、金属リサイクルの大手であるパンパシフィックリサイクリング株式会社(旧:パンパシフィック・メタリスティック・リサイクル)や、大手総合商社である阪和興業株式会社が、スクラップの収集、加工、および国内外への販売において重要な役割を担っています。これらの企業は、高度な選別・加工技術を駆使し、国内外の需要家へ高品質な銅スクラップを供給しています。日本の規制・基準フレームワークにおいては、金属スクラップの品質や取引に関するJIS(日本産業規格)の適用や、廃棄物処理法に基づく適正な処理が求められます。また、リサイクル材の利用促進は、環境省が推進する「3R(リデュース、リユース、リサイクル)」政策とも連動しています。流通チャネルにおいては、専門の金属スクラップ商社やリサイクル事業者が、発生源(建設現場、解体業者、工場など)からスクラップを回収し、精錬業者や加工業者へと供給する中間流通を担っています。消費者の行動パターンとしては、環境意識の高まりから、リサイクル材を使用した製品への関心が増加していますが、価格競争力も依然として重要な要素です。銅スクラップの価格は、国際的な銅価格の動向や、国内の供給・需要バランス、さらには為替レート(USD/JPY)に大きく影響されます。例えば、USD 1.20 billion(約1,800億円)の市場規模が報告される場合、日本国内の関連市場もそれに呼応して変動すると考えられます。将来的に、都市鉱山からの回収技術の高度化や、電子機器廃棄物(E-waste)からの銅回収促進が、国内市場のさらなる発展に寄与すると見込まれます。

| 項目 | 詳細 |

|---|---|

| 調査期間 | 2020-2034 |

| 基準年 | 2025 |

| 推定年 | 2026 |

| 予測期間 | 2026-2034 |

| 過去の期間 | 2020-2025 |

| 成長率 | 2020年から2034年までのCAGR 4.3% |

| セグメンテーション |

|

当社の厳格な調査手法は、多層的アプローチと包括的な品質保証を組み合わせ、すべての市場分析において正確性、精度、信頼性を確保します。

「銅スクラップ:スクラップタイプ別、ソース別、加工技術別、用途別、最終用途別、地域別予測 2026-2034」レポートの市場調査は、主に一次調査によって実施されており、全体的な労力の約75%を占めています。この徹底的な関与により、リアルタイムの洞察、二次調査結果の検証、および業界参加者からの市場ダイナミクスの深い理解が保証されます。私たちは、バリューチェーン全体にわたる主要なステークホルダーに対し、さまざまな地域にわたる構造化された詳細なインタビューと定性調査を実施し、多様な視点と微妙な市場インテリジェンスを捉えています。

インタビューされた主要なステークホルダーは以下の通りです。

包括的な市場カバレッジを確保するため、銅スクラップエコシステムに不可欠なさまざまな企業タイプを代表する断面から参加者を戦略的に選定しています。

| Stakeholder Role | Interview Share (%) |

|---|---|

| サプライチェーンディレクター/調達責任者 | 35% |

| リサイクルオペレーションマネージャー/プラントディレクター | 30% |

| 営業・トレーディング担当副社長/シニアトレーダー | 25% |

| サステナビリティ&ESGリーダー/資材調達スペシャリスト | 10% |

| Company Type | Representation (%) |

|---|---|

| 銅スクラップ収集・加工施設 | 30% |

| 二次銅製錬所・精錬所 | 20% |

| ワイヤーロッドミル・真鍮ミル | 25% |

| 銅合金・鋳造メーカー | 15% |

| 商品トレーダー・産業スクラップブローカー | 10% |

一次調査を補完する二次調査は、方法論の約25%を占めます。この段階は、市場の基礎理解を確立し、主要なトレンド、技術的進歩、規制環境、競合ダイナミクスを特定するために不可欠です。私たちの手法には、他の市場調査ウェブサイトからのデータに依存することなく、さまざまな信頼できる公開および独自の情報源からの綿密なデータ収集が含まれます。

情報源は以下の通りです。

*.govソース)。*.orgソース)。私たちの市場規模および予測手法は、トップダウンアプローチとボトムアップアプローチの堅牢な組み合わせを活用し、複数のレベルで三角測量して、精度と包括的なカバレッジを保証します。トップダウンアプローチは、マクロ経済指標、産業生産、およびグローバルな銅消費トレンドに基づいて総市場規模を推定し、それをスクラップタイプ、ソース、技術、用途、最終用途、および地域別に細分化します。ボトムアップアプローチは、個々の企業能力、地域生産、消費統計などの詳細なデータポイントから市場推定を収集し、それを総市場に拡大します。

ボトムアップ市場規模の計算に使用される特定の指標および変数は以下の通りです。

複数レベルのデータ三角測量は、一次調査と二次調査からの結果を相互参照し、仮定を検証し、矛盾を解消して、各セグメントおよびサブセグメントの最も正確で信頼性の高い市場推定値に到達することを含みます。

私たちは、非常に信頼性が高く、実行可能な市場インテリジェンスを提供することにコミットしています。私たちの方法論には、調査プロセス全体にわたる厳格なデータ精度および品質チェックが含まれており、88%の推定精度レベルを保証します。すべてのデータポイント、仮定、および市場予測は、以下を通じて厳密な検証を受けます。

さらに、最新の市場インテリジェンスを提供するという私たちのコミットメントは、すべてのレポートが購入日まで綿密に更新され、グローバルな銅スクラップ市場に影響を与える最新の市場動向、規制変更、および経済的シフトを反映していることを意味します。

特に廃棄物管理と材料リサイクルに関する環境規制は、銅スクラップ市場に大きな影響を与えます。コンプライアンスは、湿式製錬や乾式製錬などの処理技術への需要を促進し、持続可能な材料回収を保証します。より厳しい基準は、処理コストを増加させ、世界中のスクラップの流れに影響を与える可能性があります。

銅スクラップの価格は、世界の銅需要、供給の入手可能性、および電気・電子機器などの分野からの製造出力によって影響されます。コスト構造には、収集、選別、処理が含まれ、機械的処理などの処理技術が最終製品の品質と価値に影響を与えます。市場規模は現在741億4000万ドルであり、全体的な評価額を反映しています。

銅スクラップ市場のパンデミック後の回復は、特に建築・建設および自動車分野における産業活動の再開によって牽引されています。長期的な構造的変化には、循環経済原則への注目の高まりとリサイクルインフラの強化が含まれ、市場の4.3%のCAGR予測をサポートしています。旧スクラップと新スクラップの両方の需要は進化し続けています。

世界の銅スクラップ市場の主要企業には、Glencore、Sims Limited、Kuusakoski Group、Steel Dynamicsなどが含まれます。これらの企業は大量のスクラップ材料を管理し、さまざまな処理技術や最終用途にわたって事業を展開しています。彼らの競争戦略は、しばしばグローバルな調達ネットワークと高度なリサイクル能力を含んでいます。

銅スクラップは主に線材ミル、真鍮ミル、インゴットメーカーで使用されます。主要な最終用途セグメントには、電気・電子機器、建築・建設、産業用機械・設備、自動車が含まれます。No.1銅や被覆銅線スクラップなどの特定のスクラップタイプは、さまざまな用途要件に対応しています。

銅スクラップの調達課題には、解体からの旧スクラップや製造副産物からの新スクラップを含む多様な発生源の管理が含まれます。サプライチェーンの考慮事項には、収集のロジスティクス、No.2銅や銅ソリッドなどのスクラップタイプに基づく等級付け、および世界中の処理施設への効率的な輸送が含まれます。