1. バンカー・地下シェルターの建設プロジェクトは、環境への影響と持続可能性にどのように対処していますか?

建設には主に鉄筋コンクリートや構造用鋼などの耐久性のある素材が使用され、寿命の長さと交換サイクルの短縮に貢献しています。初期建設には環境負荷がありますが、シェルターは極端な事象に対応できるように設計されており、設置後の長期的な現場への影響は最小限に抑えられることが多いです。

+1 2315155523

Sector Data Insights(SDI)は、高品質でデータ駆動型のシンジケート調査レポート、業界分析、競合インテリジェンス、およびアドバイザリーソリューションの提供に注力する、専門的なマーケットインテリジェンスおよび戦略的コンサルティング企業です。Sector Data Insightsは、特にライフサイエンス、分析機器、および関連するハイテク分野における分析の卓越性に強く重点を置いており、メーカー、投資家、サービスプロバイダー、研究者、および意思決定者が、戦略的成長、イノベーション、および市場のリーダーシップのための実用的な洞察を得られるように支援します。

SDIは、ラボおよび分析技術における深いドメインの専門知識と高度な分析を組み合わせて、包括的な市場評価、技術トレンド分析、ベンダーシェアデータ、投資インテリジェンス、サプライチェーンの洞察、および将来を見据えた予測を提供します。私たちの調査は、ライフサイエンス、半導体・電子機器、消費財、材料・化学、建設・製造、飲食料品、エネルギー・電力、自動車・輸送、ICT・メディア、航空宇宙・防衛、BFSIなどの業界にわたる複雑なグローバル市場をナビゲートする組織をサポートしています。

バンカー・地下シェルター

バンカー・地下シェルターResearch Analyst

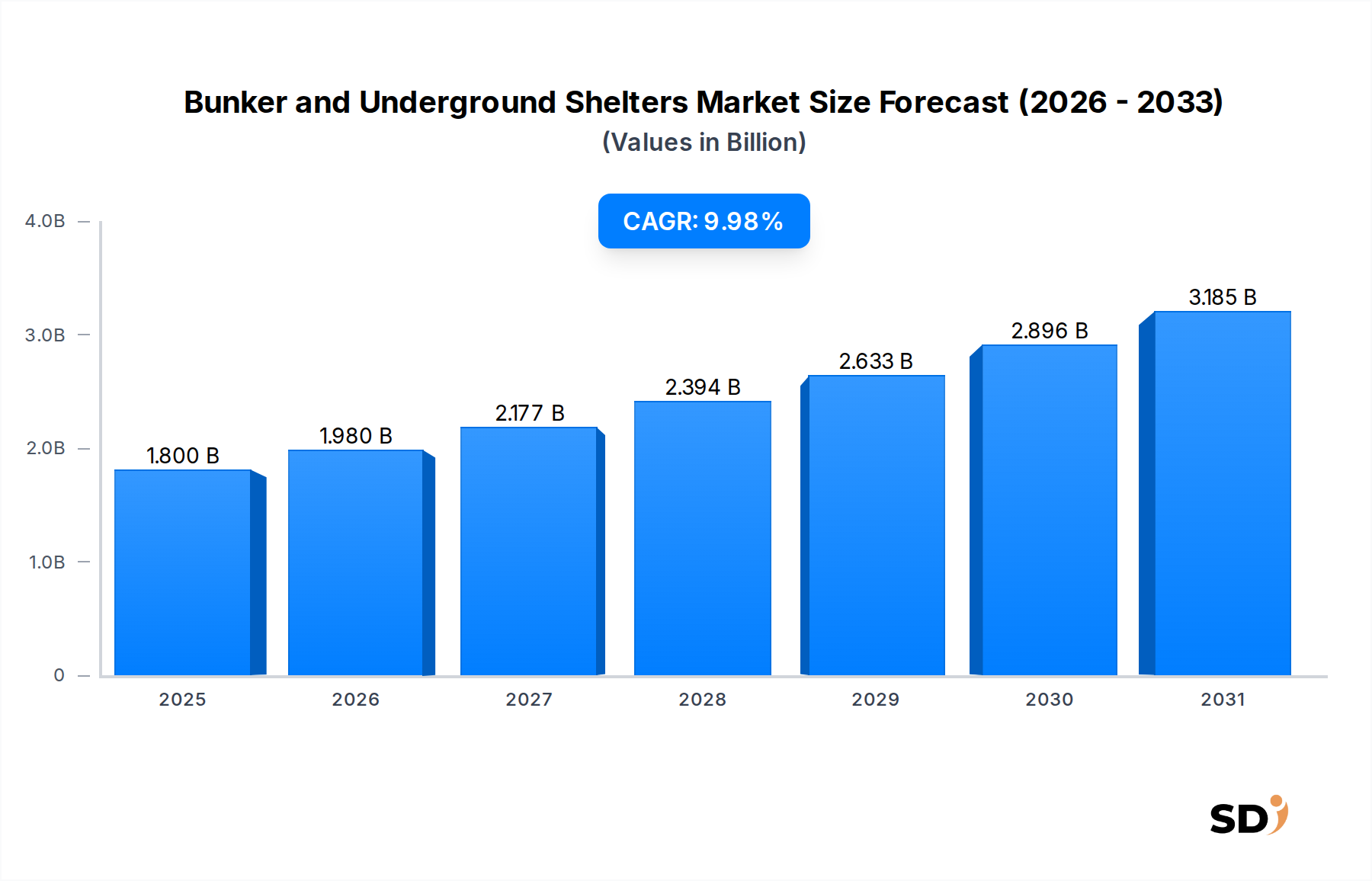

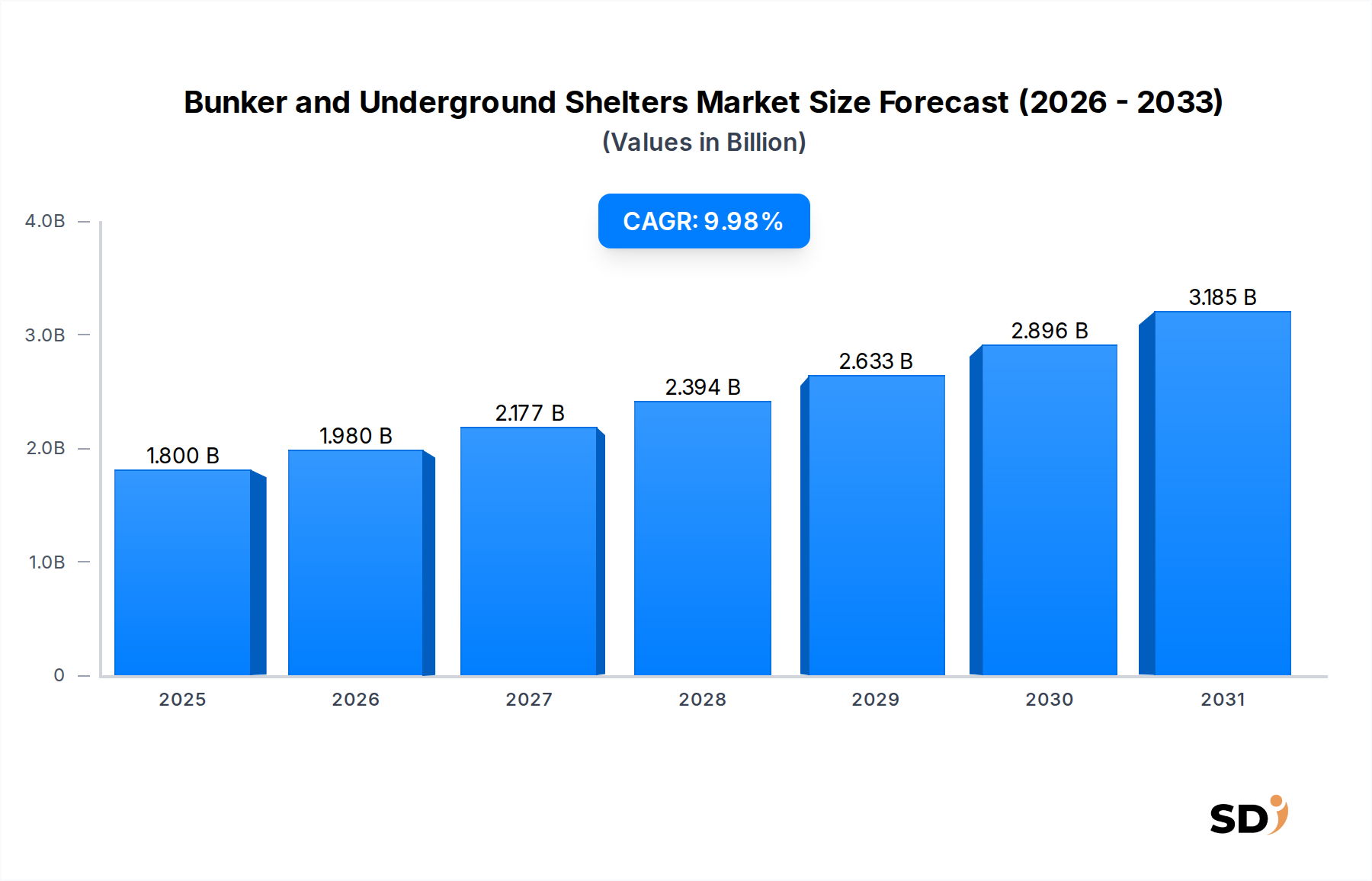

世界の地下シェルターおよび地下避難所市場は、地政学的不安の高まり、異常気象イベントの増加、および個人および地域社会の安全への重視の高まりに後押しされ、堅調な拡大を経験しています。2024年には18億ドルと推定される市場は、予測期間中に9.98%の年平均成長率(CAGR)を達成すると予測されており、著しい成長を遂げる見込みです。この軌跡は、個人宅から政府・防衛機関に至るまで、多様なエンドユーザーセグメントで保護インフラへの需要が大幅に増加していることを示しています。

主な需要ドライバーには、世界的な安全保障上の懸念の高まり、気候変動に起因する自然災害、およびレジリエンスと自己充足性への社会的な再重視が含まれます。このセクターで見られる消費者中心のトレンドは、純粋に機能的で実用的な構造物から、より統合された、技術的に高度で快適な居住環境への移行を強調しています。先進複合材料や高密度ポリエチレン(HDPE)などの素材におけるイノベーションは、シェルターの耐久性、建設効率、およびコスト効率を高めています。市場は、洗練された空気ろ過システム市場の技術や統合されたセキュリティシステム市場などの補助システムの進歩からも恩恵を受けており、これらは長期的な居住性と保護のために不可欠です。潜在的な脅威に関する一般の認識の高まりと、裕福な個人の間で可処分所得が増加していることは、カスタムメイドでハイエンドな地下シェルターソリューションへの投資を促進しています。さらに、民間の取り組みと公的助言の両方によって推進される防災市場(Disaster Preparedness Market)でのトレンドの高まりは、市場成長のための肥沃な土壌を 生み出しています。モジュラーおよび半恒久的な設置への戦略的拡大は、特に迅速な展開または適応性のあるソリューションを必要とするアプリケーションのアクセス可能性を広げています。地下シェルターおよび地下避難所市場の長期的な見通しは、継続的なイノベーション、多様化された製品提供、および進化する脅威の状況に対する安全性とセキュリティへの根強い根本的な需要によって特徴づけられる、例外的に前向きなものです。継続的な地政学的な状況と、自然災害の頻度および強度の増加が組み合わさることで、これらの重要なインフラストラクチャの市場はその上昇軌道を継続することが保証され、より広範な安全保障産業における重要なセグメントとなっています。

民間シェルター市場セグメントは、より広範な地下シェルターおよび地下避難所市場において最大かつ最もダイナミックな構成要素であり、世界的に支配的な収益シェアを

The Global Bunker and Underground Shelters Market is experiencing robust expansion, propelled by escalating geopolitical instabilities, an uptick in extreme weather events, and a growing emphasis on personal and communal safety. Valued at an estimated $1.8 billion (約2,700億円) in 2024, the market is poised for significant growth, projected to achieve a Compound Annual Growth Rate (CAGR) of 9.98% over the forecast period. This trajectory underscores a substantial increase in demand for protective infrastructure across diverse end-user segments, from individual households to government and defense organizations.

Key demand drivers include heightened global security concerns, climate change-induced natural disasters, and a renewed societal focus on resilience and self-sufficiency. The consumer-centric trends observed within this sector highlight a shift from purely functional, utilitarian structures to more integrated, technologically advanced, and comfortable living environments. Innovations in materials, such as advanced composite materials and high-density polyethylene (HDPE), are enhancing shelter durability, construction efficiency, and cost-effectiveness. The market is also benefiting from advancements in ancillary systems, including sophisticated Air Filtration Systems Market technologies and integrated Security Systems Market, which are crucial for long-term habitability and protection. The increasing public awareness regarding potential threats, coupled with a growing disposable income among affluent individuals, is fueling investments in customized and high-end bunker solutions. Furthermore, a rising trend in the Disaster Preparedness Market, driven by both private initiatives and public advisories, is creating a fertile ground for market growth. The strategic expansion into modular and semi-permanent installations is broadening accessibility, particularly for applications requiring rapid deployment or adaptable solutions. The long-term outlook for the Bunker and Underground Shelters Market remains exceptionally positive, characterized by continuous innovation, diversified product offerings, and a persistent underlying demand for safety and security against an evolving threat landscape. The ongoing geopolitical climate, combined with increasing frequency and intensity of natural disasters, ensures that the market for these critical infrastructures will continue its upward trajectory, making it a pivotal segment within the broader safety and security industry.

The Civilian Shelters Market segment stands as the largest and most dynamic component within the broader Bunker and Underground Shelters Market, holding a dominant revenue share globally. This supremacy is primarily attributed to a confluence of factors including increasing individual and family concerns over safety, heightened geopolitical tensions, and a perceived increase in the frequency and severity of natural disasters. While historically niche, the demand for civilian shelters has surged as homeowners and private entities seek resilient solutions against a wide array of threats, ranging from economic collapse and civil unrest to nuclear incidents and extreme weather events. This consumer-driven growth is clearly reflected in the expanding Residential Construction Market, where considerations for safety and resilience are increasingly integrated into high-value property developments.

The Civilian Shelters Market encompasses a wide spectrum of products, from compact backyard bunkers designed for short-term survival to elaborate, self-sufficient underground estates capable of sustaining inhabitants for extended periods. Key players within this segment include companies like Atlas Survival Shelters, Rising S Company, and Ultimate Bunker, which specialize in designing and constructing bespoke solutions tailored to individual client specifications. These companies often leverage advanced materials such as Reinforced Concrete Market and Structural Steel Market for robust structural integrity, alongside cutting-edge life support and communication systems. The demand within this segment is not only for basic protection but also for comfort, amenities, and advanced technological integration, reflecting a sophisticated consumer base. Customization options, including ergonomic layouts, advanced climate control, and entertainment systems, are becoming standard offerings, blurring the lines between survival infrastructure and luxury living spaces. The market share of civilian shelters is not only growing but also consolidating as leading manufacturers expand their geographical reach and diversify their product portfolios to cater to different budget points and threat profiles. The segment is also experiencing innovation driven by the High-Density Polyethylene Market, offering more flexible and corrosion-resistant alternatives for certain applications. The underlying psychological drivers – a desire for control, security, and peace of mind – will continue to fuel the expansion and consolidation of the Civilian Shelters Market as it evolves to meet complex consumer needs and adapt to emerging global challenges.

The Bunker and Underground Shelters Market is primarily driven by two critical macro-environmental factors: escalating geopolitical instability and the intensifying impacts of climate change. Geopolitical tensions, manifesting as regional conflicts, cyber warfare threats, and nuclear proliferation concerns, have significantly amplified the perceived need for robust protective infrastructure. For instance, recent global events and geopolitical shifts have led to a 20-30% increase in inquiries for private bunkers in specific high-net-worth demographics over the past three years. This surge in demand is directly correlated with a heightened sense of vulnerability among individuals and governmental bodies, driving investments in both Civilian Shelters Market and Military & Defense Shelters Market. Government and municipalities, as well as military and defense organizations, are consequently increasing their strategic expenditures on hardened facilities, impacting the Government Infrastructure Market.

Concurrently, the escalating frequency and severity of natural disasters attributable to climate change serve as another potent driver. Data from international meteorological organizations indicates a substantial rise in extreme weather events, including hurricanes, tornadoes, and floods, over the last decade. This has translated into a growing imperative for disaster-resilient structures. For example, coastal regions prone to severe weather have witnessed a 15% year-over-year increase in demand for underground shelters designed to withstand high-impact events and prolonged outages. These shelters often integrate advanced Air Filtration Systems Market and redundant power systems to ensure habitability during crises. While the initial investment in these structures can be substantial, the perceived long-term benefits in terms of safety, asset protection, and continuity of operations outweigh the costs for many end-users. Regulatory frameworks in certain regions are also beginning to mandate or incentivize the construction of resilient infrastructure, further stimulating market growth. The high initial capital expenditure, however, remains a significant constraint, particularly for individual households or smaller entities, limiting broader market penetration despite the undeniable need.

The competitive landscape of the Bunker and Underground Shelters Market is characterized by a mix of specialized manufacturers offering bespoke solutions and larger construction firms with dedicated defense or security divisions. Innovation in material science, survivability systems, and customization capabilities are key differentiators.

Recent innovations and strategic movements within the Bunker and Underground Shelters Market reflect an industry adapting to evolving global threats and consumer demands.

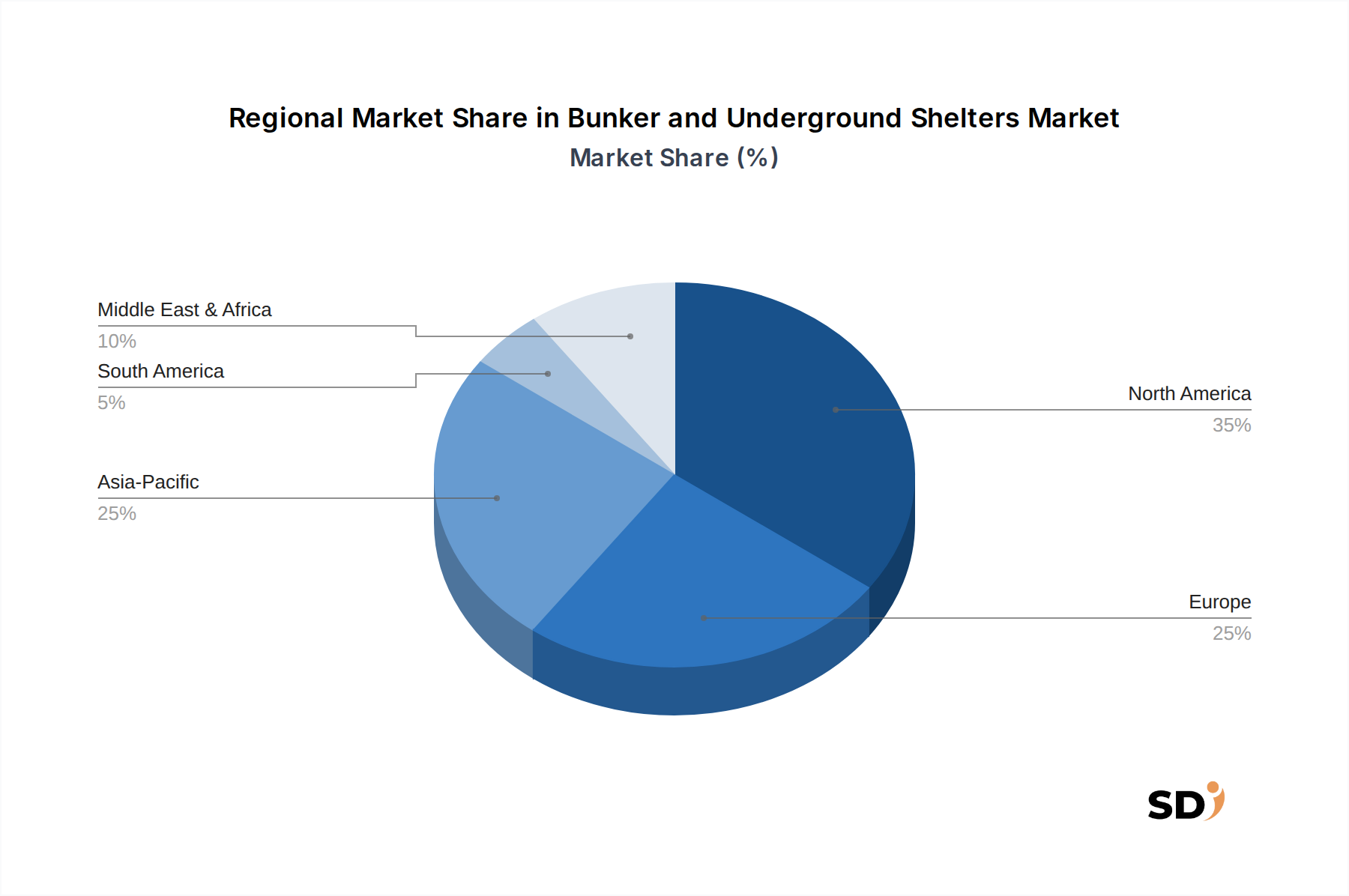

Geographic analysis reveals diverse growth trajectories and demand drivers within the global Bunker and Underground Shelters Market. North America, particularly the United States, holds a significant revenue share and is currently the most mature market. This maturity is driven by a well-established culture of preparedness, a high concentration of high-net-worth individuals, and strong governmental investment in national security infrastructure, including the Military & Defense Shelters Market. Demand in North America is consistently strong for both individual households and federal installations, fueled by concerns over natural disasters and a proactive stance on disaster preparedness.

Europe, while demonstrating steady growth, presents a more fragmented market due to varying geopolitical landscapes and national defense strategies. Countries like Russia and parts of Eastern Europe show robust demand for strategic shelters, reflecting historical contexts and ongoing security concerns. Western Europe exhibits a growing interest in private bunkers driven by increasing geopolitical anxieties and a surge in the Disaster Preparedness Market, particularly amongst affluent populations. The region is witnessing a gradual shift towards advanced Security Systems Market integrations within these structures. The Middle East & Africa region is emerging as a significant growth area, primarily driven by persistent geopolitical instability, regional conflicts, and substantial defense spending. Nations within the GCC (Gulf Cooperation Council) are investing heavily in secure infrastructure, boosting demand for both military and commercial & industrial shelters. This region is projected to be one of the faster-growing segments due to ongoing modernization efforts and a strategic focus on national security. Asia Pacific, spearheaded by China, India, and South Korea, is experiencing considerable growth, becoming a crucial growth engine. This is attributed to rapid economic development, increasing disposable incomes, a growing awareness of natural disaster risks, and, in some areas, escalating regional tensions. The Residential Construction Market in these nations is increasingly seeing integrated safety solutions. While specific regional CAGRs are not disclosed, the Middle East & Africa, alongside parts of Asia Pacific, are poised for accelerated growth, reflecting dynamic threat landscapes and increasing economic capacities to invest in high-value protective solutions.

The Bunker and Underground Shelters Market is characterized by highly variable pricing dynamics, largely influenced by customization levels, material costs, and the sophistication of integrated systems. Average selling prices for entry-level, basic shelters can range from $40,000 (約600万円) to $150,000 (約2,250万円), while bespoke, luxury underground complexes can command prices well into the multi-million dollar range, often exceeding $10 million (約15億円) for comprehensive solutions. Margin structures across the value chain differ significantly. Manufacturers of pre-fabricated modules or standardized components typically operate with more predictable margins, often in the 15-25% range, due to economies of scale in material procurement, such as for the Reinforced Concrete Market or Structural Steel Market. However, custom builders and full-service integrators, particularly those catering to the high-net-worth individual market, can achieve significantly higher project-specific margins, sometimes exceeding 40-50%, reflecting the high value placed on unique design, specialized engineering, and discretion.

Key cost levers include raw material prices, primarily steel, concrete, and high-density polyethylene (HDPE) which is integral to the High-Density Polyethylene Market, labor costs for specialized construction, and the expense of advanced life support, Air Filtration Systems Market, and Security Systems Market. Fluctuations in global commodity cycles directly impact the cost of inputs like steel, creating margin pressure for manufacturers who may absorb these costs to maintain competitive pricing or pass them on to consumers, particularly in projects with long lead times. Competitive intensity, while not as pronounced as in mass-market construction, does exert downward pressure on pricing for standardized offerings. Niche players differentiate through specialization, proprietary technology, or exceptional customer service, enabling them to command premium prices. The increasing demand for turn-key solutions that include installation, maintenance, and long-term support also allows providers to capture higher value and sustain healthier margins throughout the product lifecycle, moving beyond just the initial sale to a service-oriented model.

Customer segmentation in the Bunker and Underground Shelters Market is highly stratified, reflecting diverse motivations, purchasing criteria, and price sensitivities. The primary end-user segments include individual households, government & municipalities, military & defense organizations, corporates, and NGOs & disaster relief agencies.

Individual Households (High-Net-Worth & Preparedness Enthusiasts): This segment, a major driver of the Civilian Shelters Market, is characterized by a strong desire for personal and family safety, privacy, and long-term self-sufficiency. Purchasing criteria often prioritize durability, advanced life support systems (e.g., sophisticated Air Filtration Systems Market), and comprehensive Security Systems Market. Price sensitivity varies significantly; ultra-high-net-worth individuals exhibit low price sensitivity, often seeking custom, luxurious, and technologically advanced solutions, whereas preparedness enthusiasts may opt for more cost-effective, modular, or DIY-friendly options. Procurement channels for this segment are typically direct from specialized builders and manufacturers, with personalized consultations being paramount.

Government & Municipalities: These entities focus on public safety, civil defense, and critical infrastructure protection. Their purchasing criteria are driven by strict regulatory compliance, resilience standards, and capacity requirements for communal or strategic assets. Price sensitivity is moderate, balanced against the need for robust, long-lasting solutions, often incorporating significant Reinforced Concrete Market and Structural Steel Market components. Procurement is typically through competitive bidding processes, involving detailed specifications and compliance audits.

Military & Defense Organizations: This segment demands the highest levels of protection against a spectrum of threats, including conventional attacks, WMDs, and EMPs. Purchasing criteria are non-negotiable on survivability, operational continuity, and secure communication capabilities. Price sensitivity is generally low, given the strategic importance of these installations. Procurement occurs through specialized defense contractors and government procurement agencies, with stringent security clearances and classified project execution.

Corporates & NGOs: Corporates seek business continuity, data protection, and executive safety, particularly for essential personnel. NGOs and disaster relief agencies focus on rapid deployment, modularity, and humanitarian aid distribution centers in disaster-prone regions. Price sensitivity is moderate, balancing functionality with budget constraints. Procurement involves standard B2B channels and strategic partnerships with suppliers. A notable shift in buyer preference is the increasing demand for integrated, smart-shelter technologies across all segments, allowing for remote monitoring, automated climate control, and advanced communication, moving beyond mere physical protection to comprehensive, intelligent resilience platforms. Furthermore, the growth of the Disaster Preparedness Market is seeing increased demand for semi-permanent modular shelter systems for rapid deployment.

日本の地下シェルターおよび地下避難所市場は、そのユニークな地政学的な位置、自然災害への脆弱性、および技術革新への強い志向によって特徴づけられます。市場規模は、急速に変化する世界情勢や気候変動による災害リスクへの懸念の高まりを反映し、着実に拡大しています。個人の安全意識の高まりは、特に富裕層や防災意識の高い層の間で、民間シェルターへの投資を促進しています。公的機関や地方自治体も、国民保護の観点から、災害時の避難施設や重要インフラの保護のために地下シェルターの設置を検討する動きが見られます。日本国内に拠点を置く、あるいは日本で事業を展開している企業としては、地質調査や建設技術に強みを持つゼネコンや、安全・防災関連のソリューションを提供する企業が市場に関与する可能性があります。具体的にこの分野で先行する日本企業は特定されていませんが、建築基準法や建築基準法に基づく建築確認、消防法、そして災害対策基本法などが、安全基準や設置要件に影響を与える可能性があります。また、近年では、省令で定める設備基準を満たすことが求められる場合など、個別の製品や設備に関連する規制も考慮されることがあります。流通チャネルとしては、専門の建設業者やセキュリティコンサルタントを介した直接販売が主流ですが、企業や自治体向けの入札やコンペティションも重要なチャネルとなります。消費者の行動パターンとしては、単なる避難場所としてだけでなく、長期的な居住性、快適性、および最新の通信・監視システムといった付加価値を求める傾向があります。日本の住宅事情や土地利用の制約を考慮すると、モジュラー式やコンパクトな地下シェルター、あるいは既存建物の地下空間を活用したソリューションが、今後さらに注目される可能性があります。円滑な地下空間の確保や、地震、台風、津波といった複合的な災害への対応能力が、製品開発における重要な要素となるでしょう。市場の成長は、こうした国内固有のニーズとグローバルな安全保障トレンドの融合によって、今後も継続すると予想されます。現時点での正確な市場規模(円建て)や成長率は公表されていませんが、防災意識の高まりとともに、潜在的な市場ポテンシャルは大きいと考えられます。

| 項目 | 詳細 |

|---|---|

| 調査期間 | 2020-2034 |

| 基準年 | 2025 |

| 推定年 | 2026 |

| 予測期間 | 2026-2034 |

| 過去の期間 | 2020-2025 |

| 成長率 | 2020年から2034年までのCAGR 9.98% |

| セグメンテーション |

|

当社の厳格な調査手法は、多層的アプローチと包括的な品質保証を組み合わせ、すべての市場分析において正確性、精度、信頼性を確保します。

当社の調査手法は、一次調査に重点を置いており、総データ収集活動の約75%を占めています。このアプローチにより、バリューチェーン全体にわたる業界の実務家および主要なステークホルダーから、最も最新かつ詳細なインサイトを直接得ることができます。私たちは、半構造化された質問票を使用して、市場インテリジェンスを特定し、二次的な発見を検証するために、主に電話およびウェブベースのプラットフォームを介して、広範な定性的および定量的インタビューを実施します。一次回答者は、バンカーおよび地下シェルター市場における専門知識と影響力に基づいて戦略的に特定されます。

インタビューされた主要なステークホルダーは次のとおりです。

市場エコシステムに不可欠な、多様な企業と協力し、包括的な視点を確保しています。

これらのインタビューは、レポートの範囲で言及されている主要な地域を網羅しており、市場のトレンド、競合状況、技術的進歩、規制環境に関するグローバルな視点を提供します。

| Stakeholder Role | Interview Share (%) |

|---|---|

| 最高技術責任者/設計責任者 | 30% |

| 政府販売担当/防衛契約マネージャー | 30% |

| オペレーション/調達ディレクター | 25% |

| セキュリティ&レジリエンスコンサルタント | 15% |

| Company Type | Representation (%) |

|---|---|

| 特殊バンカー建設会社 | 30% |

| プレハブシェルターメーカー | 25% |

| セキュリティ&弾道材料サプライヤー | 25% |

| 地下インフラエンジニアリング会社 | 20% |

調査の残りの25%は、堅牢な二次データ収集と業界ベンチマーキングに充てられています。このフェーズでは、基礎データ、市場トレンド、競合インテリジェンスが提供され、一次調査の範囲と方向性の形成に役立ちます。当社のアナリストは、独自性と客観性を維持するために、他の市場調査ウェブサイトを避け、さまざまな信頼できる情報源から注意深くデータを収集します。

主要な二次情報源は次のとおりです。

すべてのデータは体系的にカタログ化され、クロスチェックされ、一貫性と正確性が確保されています。各レポートは購入日まで更新され、最新の市場ダイナミクスと利用可能な情報を反映しています。

当社の市場推定は、堅牢で検証済みの市場規模を確保するために、トップダウンとボトムアップの両方の方法論を組み合わせたデュアルアプローチを活用しています。この多層的なデータ三角測量アプローチは、一次インタビューからの定性的なインサイトと、二次情報源からの定量的なデータを統合しています。

ボトムアップアプローチ:この方法では、詳細なデータを集計して市場規模を推定します。計算に使用される主要な変数は次のとおりです。

トップダウンアプローチ:この方法では、より広範な市場または経済指標から開始し、特定の市場セグメントに絞り込みます。マクロ経済要因、地政学的安定性指数、地域GDP成長率、防衛支出トレンド、人口密度を分析して全体的な市場規模を導き出し、それを以下に分解します。

両方のアプローチは、反復的なデータ三角測量を通じて調整され、最終的な市場規模と予測に到達します。

当社は、非常に信頼性の高い市場インテリジェンスを提供することにコミットしています。85〜90%の推定データ精度レベルを保証します。この高い精度レベルは、厳格な多段階検証プロセスを通じて達成されます。

建設には主に鉄筋コンクリートや構造用鋼などの耐久性のある素材が使用され、寿命の長さと交換サイクルの短縮に貢献しています。初期建設には環境負荷がありますが、シェルターは極端な事象に対応できるように設計されており、設置後の長期的な現場への影響は最小限に抑えられることが多いです。

市場は、一般市民用シェルターや軍事・防衛用シェルターを含む「シェルターの種類」と、主に個人世帯、政府・自治体、軍事・防衛組織を含む「エンドユーザー」によってセグメント化されています。個人世帯と政府機関が主要なエンドユーザーを占めています。

物理的な保護というその特定の機能性を考慮すると、市場には直接的な破壊的代替手段は限られています。イノベーションは、耐久性を高めるための複合材料、迅速な設置のためのモジュラー設計、シェルターの機能を改善するための高度な空気ろ過システムに焦点を当てています。

主要な参入障壁には、専門的な建設のための高い資本投資、厳格な安全基準、および高度なエンジニアリング専門知識の必要性が含まれます。Atlas Survival SheltersやRising S Companyのような確立された企業は、ブランドの評判と複雑な地下プロジェクトにおける経験から恩恵を受けています。

特定の地域別成長率は提供されていませんが、アジア太平洋地域は、人口の多さと災害対策への意識の高まりから、新興の機会として特定されています。北米とヨーロッパは、持続的な需要を反映して、それぞれ約35%と25%の大きな市場シェアを占めています。

市場は、地政学的不安の高まり、自然災害の頻度の増加、および個人および国家の安全保障への関心の高まりによって牽引されています。2033年までのCAGR 9.98%と予測される、個人世帯、政府、軍事組織向けの堅牢な保護ソリューションの需要が拡大しています。