1. アスファルテン阻害剤の主要な価格動向とコストドライバーは何ですか?

アスファルテン阻害剤の価格設定は、主に原材料コストと、特にバイオベースの高度な製剤に必要とされる多額の研究開発投資によって影響を受けます。HalliburtonやBaker Hughesなどの主要企業が名を連ねる競争環境も、さまざまな製品タイプにわたる市場価格戦略を決定します。

+1 2315155523

Sector Data Insights(SDI)は、高品質でデータ駆動型のシンジケート調査レポート、業界分析、競合インテリジェンス、およびアドバイザリーソリューションの提供に注力する、専門的なマーケットインテリジェンスおよび戦略的コンサルティング企業です。Sector Data Insightsは、特にライフサイエンス、分析機器、および関連するハイテク分野における分析の卓越性に強く重点を置いており、メーカー、投資家、サービスプロバイダー、研究者、および意思決定者が、戦略的成長、イノベーション、および市場のリーダーシップのための実用的な洞察を得られるように支援します。

SDIは、ラボおよび分析技術における深いドメインの専門知識と高度な分析を組み合わせて、包括的な市場評価、技術トレンド分析、ベンダーシェアデータ、投資インテリジェンス、サプライチェーンの洞察、および将来を見据えた予測を提供します。私たちの調査は、ライフサイエンス、半導体・電子機器、消費財、材料・化学、建設・製造、飲食料品、エネルギー・電力、自動車・輸送、ICT・メディア、航空宇宙・防衛、BFSIなどの業界にわたる複雑なグローバル市場をナビゲートする組織をサポートしています。

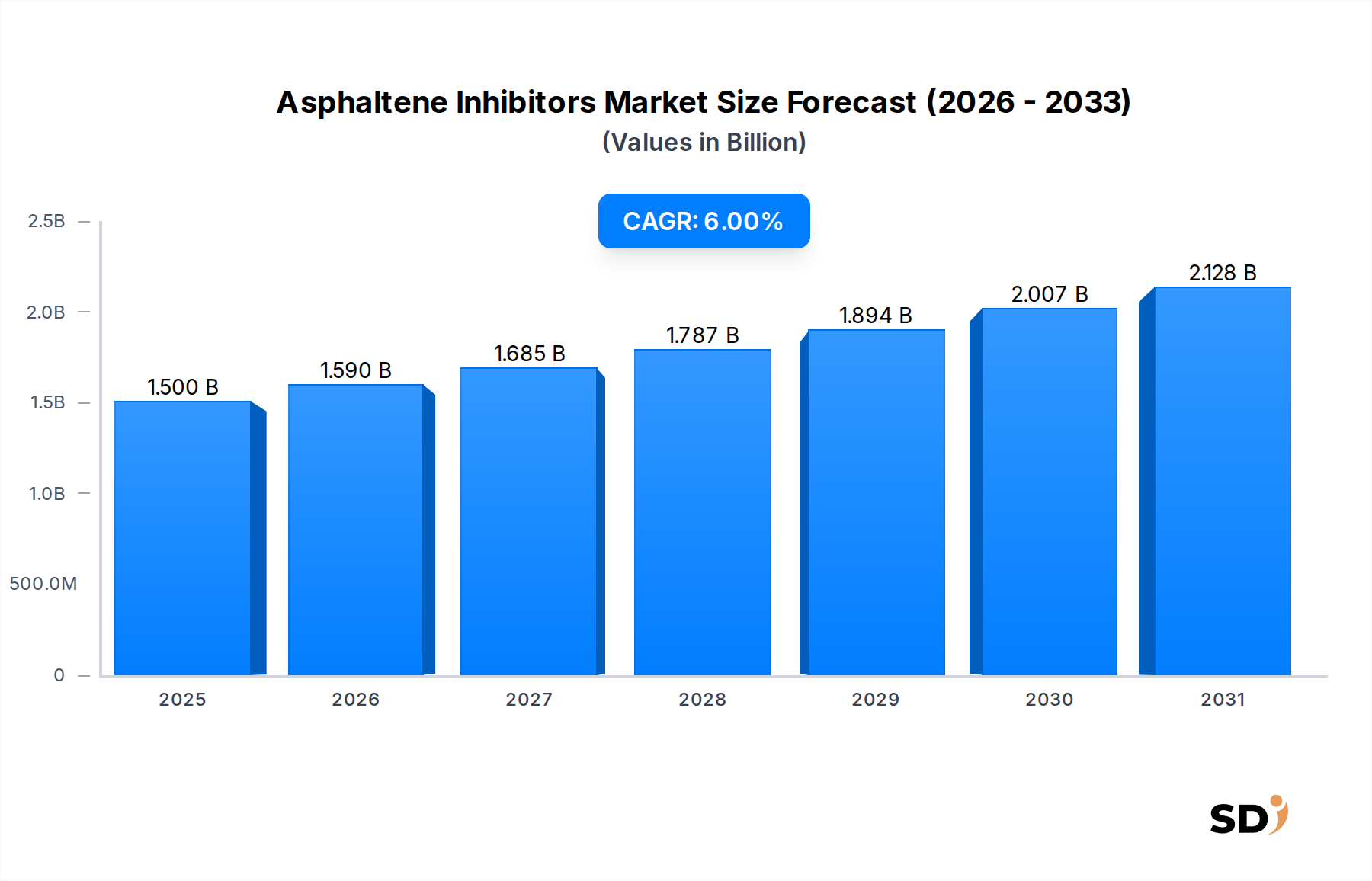

The global Asphaltene Inhibitors Market was valued at an estimated USD 1.5 billion (約2,250億円) in the base year 2025, and is projected to expand significantly, demonstrating a robust Compound Annual Growth Rate (CAGR) of 6% through the forecast period. This growth trajectory underscores the critical role of asphaltene inhibitors in ensuring operational efficiency and asset integrity across the upstream, midstream, and downstream sectors of the oil and gas industry. The market's expansion is fundamentally driven by the increasing global demand for energy, which necessitates intensified exploration and production activities in challenging environments such as deepwater, ultra-deepwater, and mature oilfields where asphaltene deposition is more prevalent. The complexity of modern crude oil compositions, particularly heavier crude grades and unconventional resources, exacerbates asphaltene precipitation issues, thereby creating a sustained demand for effective inhibition solutions.

Technological advancements in inhibitor chemistry, including the development of more potent, environmentally benign, and cost-effective formulations, are further catalyzing market growth. Innovations such as bio-based inhibitors and multi-functional chemical packages are addressing both performance and sustainability mandates. Macro tailwinds, including the continued investment in oil and gas infrastructure in emerging economies, coupled with significant expenditures in enhanced oil recovery (EOR) projects, where flow assurance is paramount, are bolstering the Asphaltene Inhibitors Market. The imperative to minimize production downtime, reduce maintenance costs, and extend the lifespan of critical infrastructure components like pipelines and processing equipment directly fuels the adoption of these specialized chemicals. The demand for various formulations, including liquid and emulsion-based inhibitors, is driven by their application versatility. Furthermore, the broader Oilfield Chemicals Market and Production Chemicals Market segments are intertwined, indicating a holistic approach to wellbore and pipeline management. The outlook for the Asphaltene Inhibitors Market remains positive, underpinned by an unwavering global energy demand and the continuous operational challenges posed by asphaltene deposition, ensuring sustained innovation and investment in this crucial segment of the Specialty Chemicals Market.

The End-User Industry segment, specifically Oil & Gas Operators, unequivocally holds the largest revenue share within the global Asphaltene Inhibitors Market. This dominance is attributable to several intrinsic factors related to the core business operations and inherent challenges faced by these entities. Oil & Gas Operators are at the forefront of exploration, drilling, production, and initial processing of crude oil and natural gas. Asphaltene deposition poses a significant threat across all these stages, leading to severe operational disruptions, reduced production efficiency, increased maintenance costs, and potential safety hazards. Consequently, the proactive and reactive application of asphaltene inhibitors becomes an indispensable part of their operational strategy.

The high investment associated with exploration and production (E&P) activities, particularly in challenging environments like deepwater, ultra-deepwater, and unconventional reservoirs, necessitates robust flow assurance solutions. Asphaltene inhibitors are critical for maintaining the integrity and flow in wellbores, subsea flowlines, and processing facilities. Without effective inhibition, operators face risks of plug formation, equipment damage, and premature asset abandonment. The substantial volume of crude oil and gas handled by these operators globally translates into a massive cumulative requirement for asphaltene inhibitor chemicals. This demand is further amplified by the increasing complexity and heavier nature of crudes being extracted, which inherently contain higher asphaltene content. The imperative for maximizing hydrocarbon recovery and ensuring uninterrupted flow from the reservoir to the refinery gate directly drives the consumption of these specialized chemicals by Oil & Gas Operators. Companies like Halliburton, Baker Hughes, Schlumberger, and Ecolab are prominent players in providing comprehensive chemical solutions, including asphaltene inhibitors, directly to these operators, often integrating these services within broader flow assurance or production optimization contracts. The segment's share is expected to remain dominant, driven by ongoing global upstream activities and the continuous need for optimized production and transport of hydrocarbons. The integration of asphaltene inhibitors with other specialized chemicals, such as those found in the Flow Assurance Chemicals Market, further solidifies its critical role for Oil & Gas Operators. As new fields are developed and existing ones mature, the need for effective asphaltene management only intensifies, ensuring sustained growth in this crucial end-user segment of the Asphaltene Inhibitors Market.

The Asphaltene Inhibitors Market is fundamentally propelled by several critical factors intrinsic to the global energy landscape and operational demands within the hydrocarbon industry. One primary driver is the escalating global demand for energy, which compels increased exploration and production efforts, particularly in challenging and complex reservoirs. The exploitation of deeper oil wells, ultra-deepwater resources, and unconventional shale plays inherently involves crude oil with higher asphaltene content and more complex compositions, leading to increased precipitation issues. This necessitates a greater reliance on advanced asphaltene inhibitors to ensure continuous flow and operational integrity.

Secondly, the aging infrastructure of existing oil and gas fields significantly contributes to the demand. As fields mature, changes in pressure, temperature, and crude composition can trigger asphaltene deposition, reducing pipeline efficiency and increasing maintenance costs. Operators are increasingly deploying inhibitors as part of proactive maintenance strategies to extend the operational life of pipelines and processing equipment. Thirdly, the growing emphasis on Enhanced Oil Recovery (EOR) techniques, such as gas injection or chemical flooding, often alters reservoir fluid properties, making asphaltene precipitation more likely. The success of EOR projects heavily depends on effective flow assurance, thereby boosting the demand for specialized asphaltene inhibitors that can perform under diverse and often harsh reservoir conditions. Lastly, the economic imperative to minimize production downtime and optimize operational expenditures drives the adoption of inhibitors. Uncontrolled asphaltene deposition can lead to costly shutdowns, equipment damage, and significant production losses. The financial benefits derived from preventing these issues, combined with the continuous innovation in the broader Oilfield Chemicals Market, underscore the indispensable value proposition of asphaltene inhibitors, driving steady growth across the Asphaltene Inhibitors Market. The demand for these products is also closely linked to activity in the Crude Oil Production Market and the overall increase in crude production globally.

Within the Asphaltene Inhibitors Market, a diverse range of companies operate, from multinational conglomerates offering integrated solutions to specialized chemical producers. The competitive landscape is characterized by continuous innovation in chemical formulations and strategic service offerings:

The Asphaltene Inhibitors Market is characterized by continuous research and development aimed at improving efficacy, environmental profile, and cost-effectiveness. Key strategic activities and innovations reflect the dynamic nature of this specialized chemical sector:

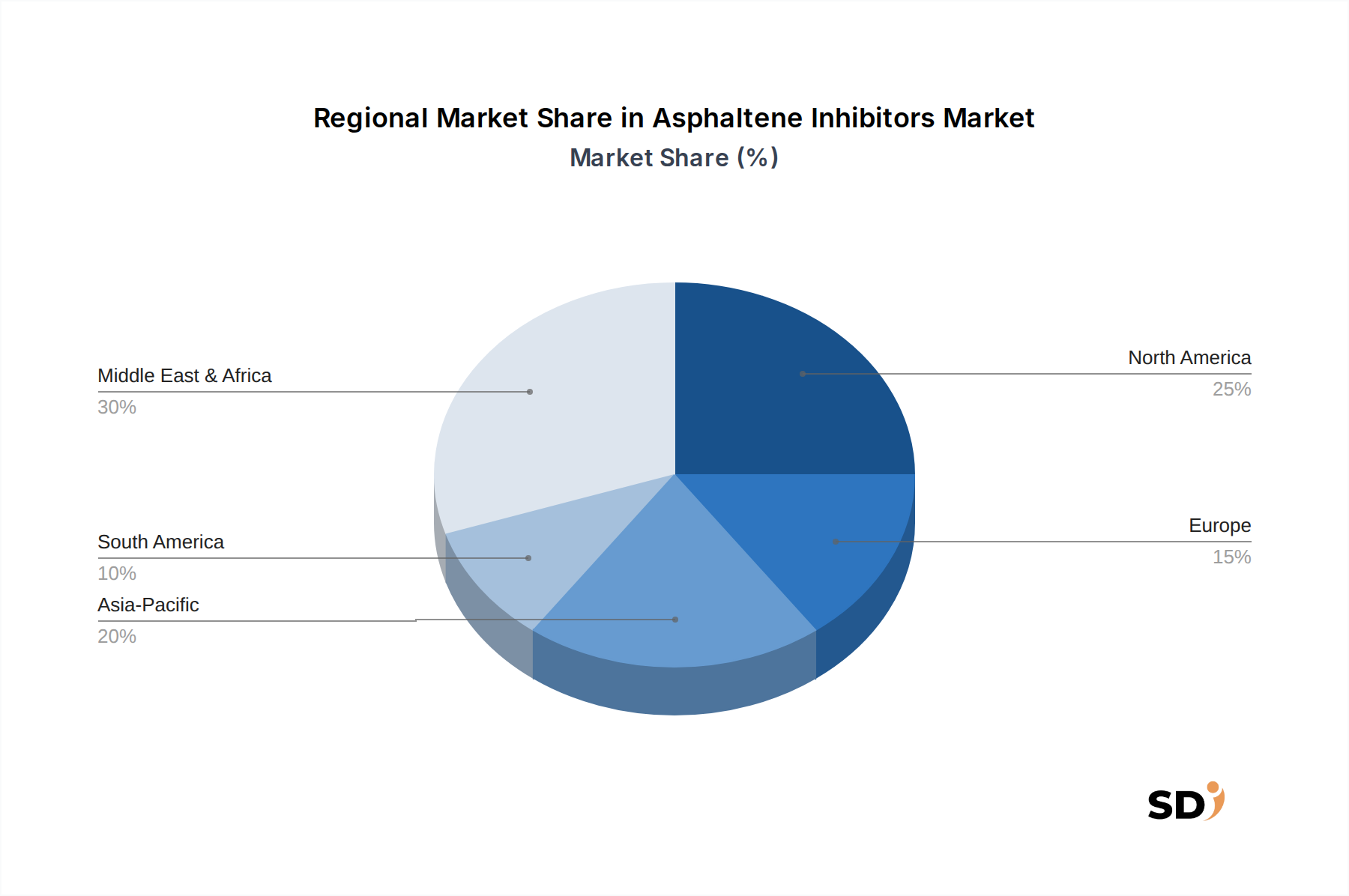

The global Asphaltene Inhibitors Market exhibits significant regional disparities influenced by varying levels of oil and gas production, crude oil characteristics, and regulatory frameworks. North America, encompassing the United States, Canada, and Mexico, represents a substantial market share. This region's dominance is driven by extensive conventional and unconventional oil and gas production, coupled with significant investment in offshore exploration and mature asset management. The demand for asphaltene inhibitors in North America is robust, primarily to manage complex crude compositions and maintain flow assurance in its vast pipeline network and processing facilities.

The Middle East & Africa region, particularly the GCC countries, is projected to be among the fastest-growing markets. This growth is spurred by large-scale upstream investments, the exploitation of heavy and sour crude reserves, and the continuous expansion of production capacities. Countries like Saudi Arabia and the UAE, with their massive oil production, are significant consumers of asphaltene inhibitors to ensure uninterrupted operations. Similarly, the Asia Pacific market, led by China, India, and ASEAN countries, is experiencing rapid growth due to increasing energy demand, new exploration activities, and the development of challenging offshore fields. These regions are witnessing substantial infrastructure development in the Crude Oil Production Market.

Europe, including the UK, Germany, and Norway, represents a mature but stable market. While new exploration activities might be more constrained, the focus on maximizing recovery from mature fields in the North Sea and extending the life of existing infrastructure drives a consistent demand for asphaltene inhibitors. The stringent environmental regulations in Europe also push for the adoption of more eco-friendly and high-performance inhibitor formulations. Latin America, with Brazil and Argentina as key contributors, shows steady growth, driven by deepwater exploration activities and the need to manage heavy oil production challenges. Each region's unique crude characteristics and operational environments dictate specific requirements for asphaltene inhibitor formulations and application strategies within the Asphaltene Inhibitors Market, contributing to the overall dynamics of the Specialty Chemicals Market.

The supply chain for the Asphaltene Inhibitors Market is intricate, primarily revolving around the availability and pricing of various specialized organic chemicals. Upstream dependencies include the petrochemical industry, which provides the foundational building blocks for synthetic inhibitors. Key raw materials often include various amines (e.g., polyamines), polycarboxylates, aromatic solvents, and a range of surfactants. The production of these intermediates is highly susceptible to the volatility of crude oil and natural gas prices, which directly impacts the cost of petrochemical feedstocks. Consequently, manufacturers in the Asphaltene Inhibitors Market face inherent sourcing risks related to price fluctuations and potential supply disruptions.

Price trends for key inputs like aromatic solvents (e.g., toluene, xylene) and amine derivatives have shown periods of significant volatility, often influenced by geopolitical events, refinery outages, or shifts in global demand for other petrochemical end-products. For instance, a surge in demand for plastics can divert precursor chemicals away from inhibitor production, impacting supply and driving up costs. Historical disruptions, such as those caused by natural disasters or global pandemics, have highlighted vulnerabilities in logistics and raw material procurement, leading to extended lead times and increased operational costs for inhibitor manufacturers. The ongoing shift towards more sustainable and bio-based inhibitors is also introducing new raw material streams, such as derivatives from plant oils or biomass, which come with their own unique supply chain considerations and price dynamics. The efficiency of the global transportation network also plays a crucial role in delivering these specialized chemicals from production facilities to oilfields and refineries worldwide. Managing these supply chain complexities is vital for maintaining competitiveness and ensuring consistent product availability within the Asphaltene Inhibitors Market.

The Asphaltene Inhibitors Market operates within a complex web of national and international regulatory frameworks and industry standards, primarily driven by environmental protection, worker safety, and operational efficiency mandates. Key geographies, including North America, Europe, and increasingly Asia Pacific, have established guidelines that significantly influence the formulation, application, and disposal of these chemicals. In Europe, the REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulation is paramount, requiring extensive data on chemical properties, hazards, and risks. This necessitates manufacturers to ensure their asphaltene inhibitor formulations comply with strict substance registration and authorization processes, influencing product development towards safer and less persistent chemistries. The European Union's directives on environmental protection, such as the Water Framework Directive, also impact the permissible discharge levels of chemicals in offshore operations.

In the United States, the Environmental Protection Agency (EPA) and various state-level environmental agencies regulate chemical use and discharge, particularly for offshore drilling under the National Pollutant Discharge Elimination System (NPDES) permits. The Occupational Safety and Health Administration (OSHA) sets standards for worker safety during handling and application. Recent policy changes often lean towards promoting biodegradable and low-toxicity chemicals, pushing R&D towards green chemistry solutions within the Specialty Chemicals Market. Industry bodies like NACE International (now AMPP) provide technical standards and recommended practices for corrosion and flow assurance management, including the selection and application of asphaltene inhibitors, which are often adopted globally. Emerging markets in Asia Pacific and the Middle East are also strengthening their regulatory oversight, often drawing inspiration from established Western frameworks, leading to a global trend towards more environmentally conscious and transparent chemical management. These evolving policies and standards directly impact product innovation, market entry barriers, and the operational costs for companies in the Asphaltene Inhibitors Market, while also fostering the growth of the Oilfield Chemicals Market and Production Chemicals Market with more sustainable offerings.

日本のアスファルテン阻害剤市場は、世界のエネルギー需要の増加というマクロトレンドに支えられつつも、国内の石油・ガス生産活動の特性に合わせた独自の成長軌道を描いています。日本のエネルギー市場は、化石燃料への依存度が高い一方で、再生可能エネルギーへの移行も進んでおり、石油・ガス部門は依然として重要な役割を担っています。特に、国内での埋蔵量が限られているため、既存油田の維持管理や、海外での探鉱・開発プロジェクトにおける操業効率の確保が、アスファルテン阻害剤の需要を牽引しています。市場規模としては、グローバル市場に比べて限定的であると推定されますが、高度な技術が求められる特殊化学品分野として、着実な成長が見込まれます。

国内市場において、大手総合化学メーカーや、石油・ガス産業向けの特殊化学品を提供する企業が主要なプレイヤーとして活動しています。例えば、API(American Petroleum Institute)規格に準拠した製品を提供するグローバル企業や、日本国内での事業展開を持つ化学品メーカーが、日本の石油・ガスオペレーターや海外に展開する日本の企業に対して、アスファルテン阻害剤や関連するフローアシュランス(流動性確保)ソリューションを提供しています。これらの企業は、日本の厳しい品質基準や環境規制に対応した製品開発に注力しています。

日本市場におけるアスファルテン阻害剤の利用は、特定の規制や標準に直接関連しています。石油・ガス探査・生産活動においては、APIの標準や、業界団体による推奨事項(例: NACE International / AMPPの技術基準)が、化学薬品の選定や使用方法に影響を与えます。また、化学物質全般に関しては、化審法(化学物質の審査及び製造等の規制に関する法律)や安衛法(労働安全衛生法)といった国内法規制が、製品の安全性、環境への影響、および取り扱い方法に適用されます。これらの法規制は、製品のライフサイクル全体にわたって、環境負荷の低減と作業者の安全確保を重視する傾向にあります。

流通チャネルとしては、主要な石油・ガスオペレーターやエンジニアリング会社が、化学品メーカーや石油・ガスサービス会社から直接購入するケースが一般的です。また、専門商社や代理店を通じて、小規模なオペレーターや海外プロジェクトへの供給が行われることもあります。日本の消費者は、製品の性能だけでなく、安全性、環境への配慮、そしてサプライヤーの信頼性を重視する傾向があります。これは、アスファルテン阻害剤の選定においても、技術的な有効性はもちろんのこと、環境規制への適合性や、長期的な操業安定性への貢献度といった観点から評価されることを意味します。

為替レートの変動は、原材料の輸入コストや、海外でのプロジェクトにおける事業採算性に影響を与える可能性があります。例えば、1.5兆円規模(USD 1.5 billion)と推定されるグローバル市場の成長率6%を基準に、日本市場の動向を分析する際には、円安・円高といった為替変動リスクも考慮する必要があります。市場調査レポートにおける具体的な円換算額は、経済動向や調査時点の為替レートによって変動するため、最新の市場データや専門家の分析を参照することが重要です。

| 項目 | 詳細 |

|---|---|

| 調査期間 | 2020-2034 |

| 基準年 | 2025 |

| 推定年 | 2026 |

| 予測期間 | 2026-2034 |

| 過去の期間 | 2020-2025 |

| 成長率 | 2020年から2034年までのCAGR 6% |

| セグメンテーション |

|

当社の厳格な調査手法は、多層的アプローチと包括的な品質保証を組み合わせ、すべての市場分析において正確性、精度、信頼性を確保します。

当社の調査方法論は、一次調査に重点を置いており、データ収集および検証作業全体の約75%を占めます。このアプローチにより、当社の調査結果は、リアルタイムの市場動向、専門家の意見、および主要な業界関係者からの直接的な専有的な洞察に基づいています。バリューチェーン全体にわたる多様なステークホルダーとの広範かつ構造化されたインタビューを実施し、主に電話およびオンラインビデオ会議プラットフォームを通じて実施し、可能かつ必要な場合は対面会議で補完します。

一次調査インタビューは、現在の市場トレンド、競合環境、技術的進歩、価格戦略、需要ドライバー、規制の影響、および満たされていない市場ニーズに関する定性的および定量的データを収集するように設計されています。インタビューの対象となる主要な参加者は次のとおりです。

アスファルテンインヒビターのバリューチェーンにおける非常に特定の企業タイプ:

インタビューされた特定の役職/ステークホルダー:

この強力な一次エンゲージメントは、重要な第一線の視点を提供し、特定されたすべてのセグメントおよび地域(北米、南米、ヨーロッパ、中東・アフリカ、アジア太平洋)で二次情報源を通じて収集されたデータを検証および豊かにします。

| Stakeholder Role | Interview Share (%) |

|---|---|

| フローアシュアランスエンジニア/生産化学者 | 30% |

| 調達マネージャー(化学品・サービス) | 25% |

| 研究開発ディレクター/シニア処方科学者 | 25% |

| パイプラインインテグリティマネージャー/アセットマネージャー | 20% |

| Company Type | Representation (%) |

|---|---|

| 特殊化学品メーカー | 35% |

| 川上石油・ガスオペレーター | 25% |

| 川中パイプライン・貯蔵オペレーター | 15% |

| 川下精製所・石油化学プラント | 15% |

| 油田サービス会社 | 10% |

二次調査は、当社の方法論の残りの25%を形成し、一次検証の基盤層として機能し、包括的な市場インテリジェンスを提供します。アスファルテンインヒビター市場の全体像を構築するために、幅広い信頼できる専有的な情報源を活用しています。当社の二次調査の取り組みは、データの整合性と関連性を確保するために綿密に行われています。

使用される主要な情報源は次のとおりです。

この包括的な二次分析は、市場規模、過去のトレンド、技術的進歩、競合環境分析、および一次調査結果の検証の特定に役立ちます。研究の独自性と信頼性を維持するために、市場調査ウェブサイトからのデータは厳密に避けています。

当社の市場推定方法論は、トップダウンアプローチとボトムアップアプローチの堅牢な組み合わせを採用し、マルチレベルデータトライアンギュレーションによって補強され、最高レベルの正確性と信頼性を確保します。この二重アプローチにより、異なる視点からの市場数値を相互検証できます。

ボトムアップアプローチ: 最小限の識別可能な市場セグメントからのデータを集計することにより、市場規模を綿密に計算します。これには以下が含まれます。

トップダウンアプローチ: 同時に、マクロ経済要因、石油・ガス、化学品、エネルギーセクターの全体的な成長率、地域エネルギー需要予測、および世界的な規制トレンドを分析することにより、市場全体の規模を推定します。これにより、より広範な視点が提供され、集計されたボトムアップ数値が検証されます。

マルチレベルデータトライアンギュレーションは、一次インタビュー、さまざまな二次情報源、および当社の内部専有データベースからのデータポイントの比較と調整を伴います。この厳密な相互検証プロセスにより、不一致が最小限に抑えられ、市場予測への信頼が高まります。市場規模、シェア、および予測を含むすべての定量的データは、購入時点まで一貫して更新され、最新の市場状況とインテリジェンスを反映しています。

非常に信頼性の高い市場インテリジェンスを提供するという当社のコミットメントは、厳格なデータ精度および品質管理対策に裏打ちされています。市場レポートでは、通常85%から90%の推定データ精度レベルを保証します。これは、いくつかの反復段階を通じて達成されます。

この多面的なアプローチにより、当社の市場推定および予測は、正確であるだけでなく、堅牢、信頼性があり、戦略的意思決定に役立つものとなります。

アスファルテン阻害剤の価格設定は、主に原材料コストと、特にバイオベースの高度な製剤に必要とされる多額の研究開発投資によって影響を受けます。HalliburtonやBaker Hughesなどの主要企業が名を連ねる競争環境も、さまざまな製品タイプにわたる市場価格戦略を決定します。

アスファルテン阻害剤の国際貿易は、世界的な石油・ガス探査・生産活動と密接に連動しています。主要な化学企業は、広範な原油抽出が行われている地域に特殊な阻害剤製剤を輸出し、世界中の多様な操業環境における流動性の確保を保証しています。

アスファルテン阻害剤市場は、特に非在来型および深海油田における世界的な石油・ガス探査の増加、および流動性確保の重要性の高まりによって牽引されています。市場は、年平均成長率6%に後押しされ、2025年までに15億ドルに達すると予測されています。

市場に影響を与える重大な課題には、効果的で環境規制に準拠した阻害剤の開発に伴う高額な研究開発費用、および上流支出に直接影響を与える原油価格の固有の変動性があります。サプライチェーンのリスクには、特殊化学品の調達と遠隔地の操業サイトへのロジスティクスも含まれます。

主要な製品タイプには、それぞれ特定のアスファルテン緩和要件に対応するように製剤化された分散剤、溶剤、界面活性剤が含まれます。主なエンドユーザーセグメントは、石油・ガス事業者、パイプライン事業者、製油所であり、これらの阻害剤を炭化水素の生産および処理のさまざまな段階で統合しています。

パンデミック後、市場はE&P支出の削減により当初は低迷しましたが、世界的な石油需要の急増に伴い、操業効率と流動性確保への重点が再認識されたことにより、力強い回復を遂げました。長期的な構造的変化には、より持続可能なバイオベース阻害剤への移行や、高度な液体製剤の開発が含まれます。