Automotive Refrigerants by Refrigerant Type (R-134a, R-1234yf, R-744 (CO₂ Refrigerant), R-152a, Others), by System Type (Conventional Automotive Air Conditioning Systems, Heat Pump HVAC Systems, Integrated Thermal Management Systems), by Application (Cabin Air Conditioning Systems, Heat Pump Systems, Battery Thermal Management, Power Electronics Cooling, Commercial Vehicle Climate Control, Others), by Sales Channel (OEM, Aftermarket), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Rest of Europe), by Middle East & Africa (GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 93

Sadashiv Parab

Research Analyst

About Sector Data Insights

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Key Insights into the Automotive Refrigerants Market

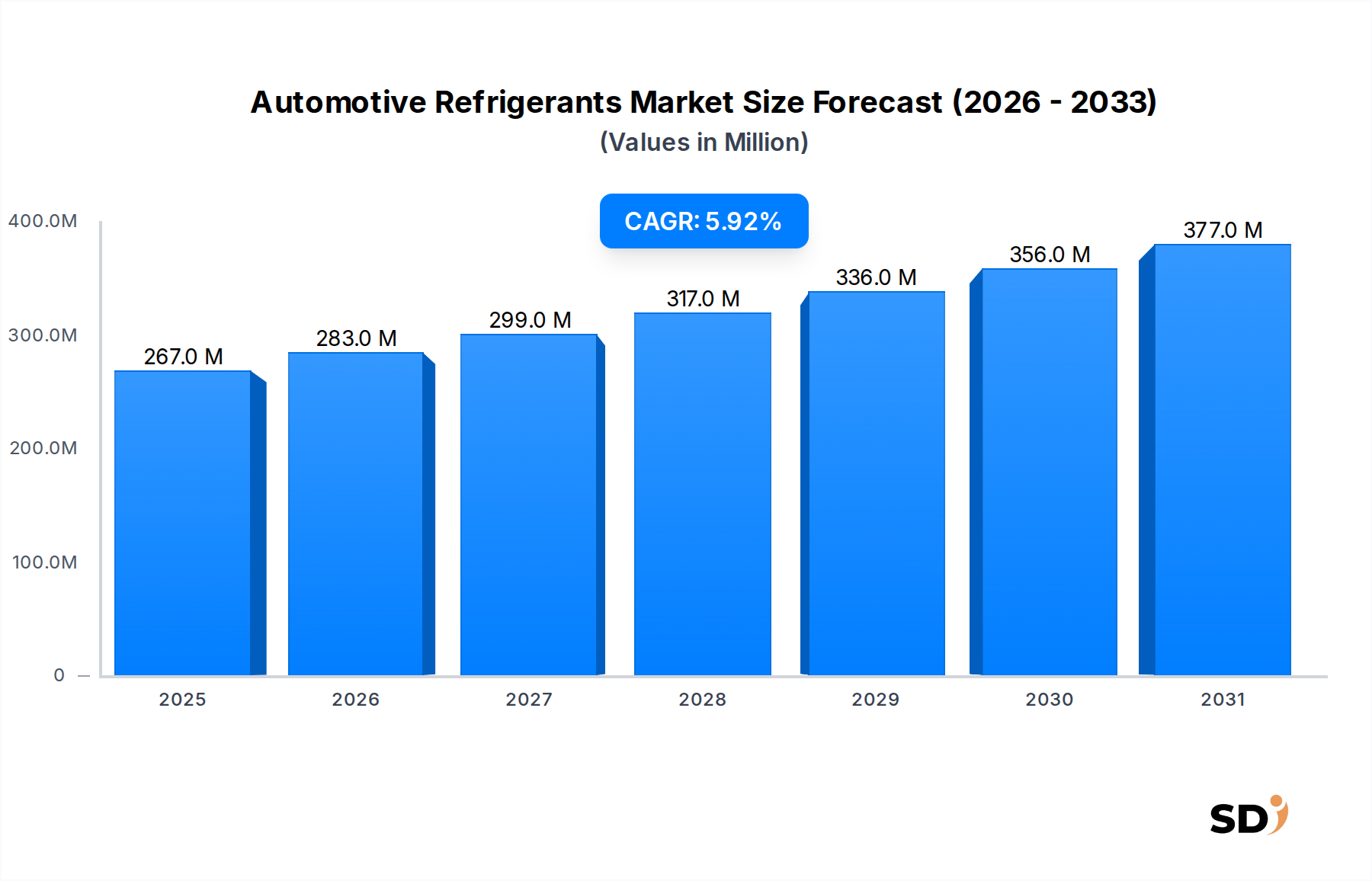

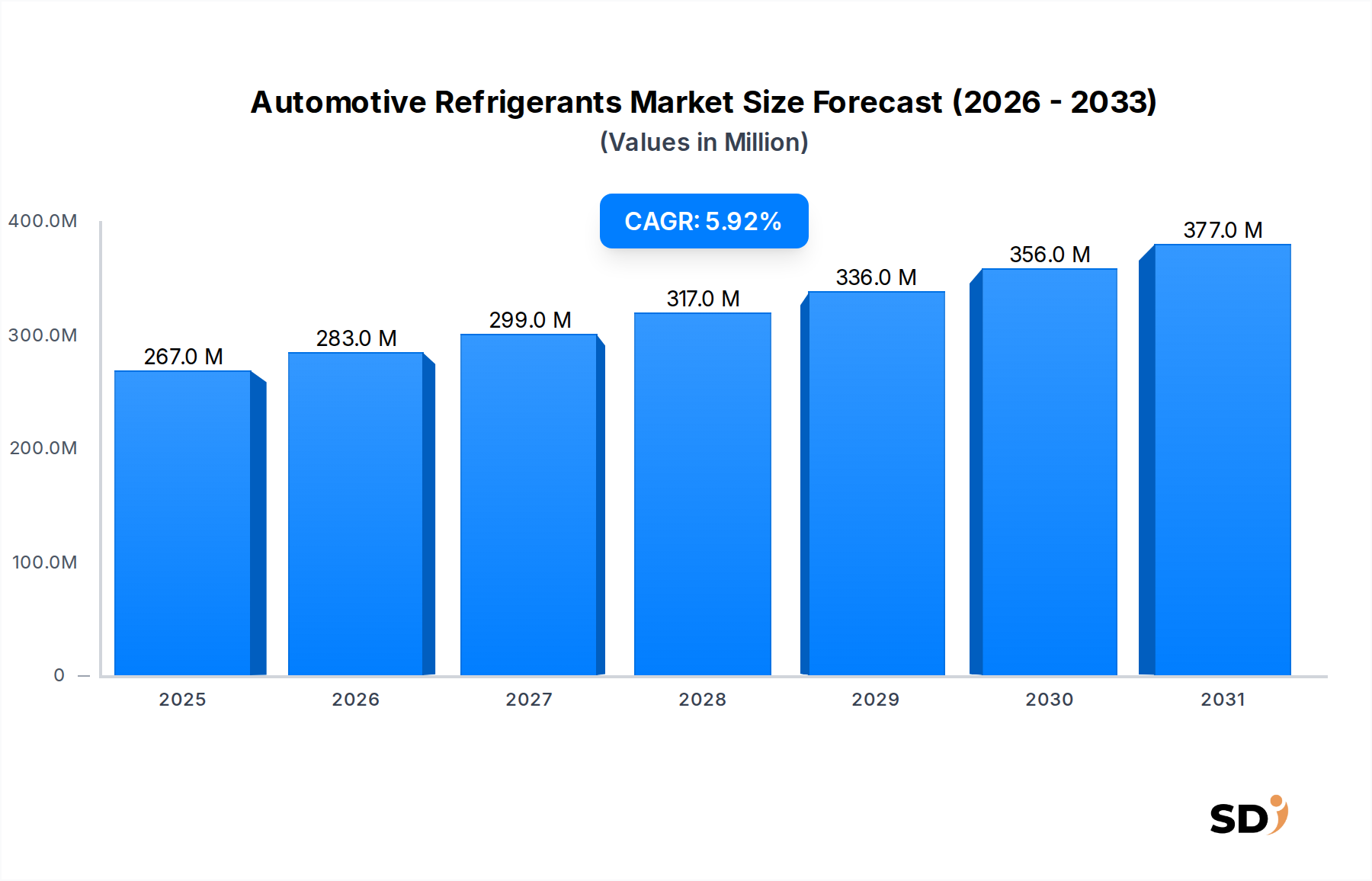

The Automotive Refrigerants Market, a critical component of the broader Automotive Climate Control Market, is currently valued at $267 million in 2026. Projections indicate a robust expansion, with the market expected to reach approximately $421.18 million by 2034, advancing at a Compound Annual Growth Rate (CAGR) of 5.9% during the forecast period. This growth trajectory is primarily underpinned by stringent global environmental regulations mandating the adoption of refrigerants with lower Global Warming Potential (GWP), alongside the accelerating electrification of the automotive industry.

Automotive Refrigerants Market Size (In Million)

400.0M

300.0M

200.0M

100.0M

0

267.0 M

2025

283.0 M

2026

299.0 M

2027

317.0 M

2028

336.0 M

2029

356.0 M

2030

377.0 M

2031

Key demand drivers include the escalating production of conventional vehicles in emerging economies and the surging demand for Electric Vehicle Thermal Management Market solutions. The latter is particularly impactful, as battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs) require sophisticated thermal management systems for optimal battery performance, cabin comfort, and power electronics cooling. This segment demands specialized refrigerants and system designs, diverging from traditional internal combustion engine (ICE) vehicle requirements.

Macro tailwinds such as increasing disposable incomes in developing regions, leading to higher vehicle ownership and demand for comfort features, further bolster market expansion. Additionally, technological advancements in automotive air conditioning systems, focusing on improved efficiency and reduced refrigerant leakage, are contributing to market dynamism. The transition away from high-GWP refrigerants like R-134a towards alternatives such as R-1234yf and R-744 (CO₂) represents a significant shift. While the R-134a Refrigerant Market still holds a substantial installed base, the R-1234yf Refrigerant Market is experiencing rapid growth, driven by regulatory compliance and OEM mandates. This evolving landscape necessitates continuous innovation from refrigerant manufacturers and system integrators to meet both environmental directives and consumer expectations for performance and reliability in the Automotive Refrigerants Market.

Cabin Air Conditioning Systems Dominance in the Automotive Refrigerants Market

The application segment of Cabin Air Conditioning Systems stands as the dominant force within the Automotive Refrigerants Market, commanding the largest revenue share. This segment’s supremacy is rooted in its universal presence across nearly all classes of passenger and commercial vehicles, where it serves as a fundamental comfort and safety feature. The sheer volume of vehicles produced globally, each equipped with a cabin air conditioning system, intrinsically links the demand for refrigerants to automotive manufacturing cycles. As global automotive production continues its upward trend, particularly in Asia Pacific nations like China and India, the demand for refrigerants for initial fill (OEM channel) in cabin air conditioning systems remains consistently high. Furthermore, the extensive installed base of vehicles worldwide fuels a substantial aftermarket segment for refrigerant top-ups and replacements, ensuring sustained demand for the Automotive Aftermarket.

The dominance of Cabin Air Conditioning Systems is also influenced by evolving consumer expectations. Modern vehicle buyers prioritize enhanced climate control capabilities, quick cooling times, and efficient defrosting, which directly translates to a need for high-performance refrigerants and robust Automotive HVAC Systems Market. The transition to new refrigerant types, specifically R-1234yf, has been largely driven by regulatory pushes aimed at reducing the environmental footprint of automotive air conditioning, particularly in this primary application. While the capital investment for R-1234yf systems is higher, the long-term environmental benefits and regulatory compliance make it an inevitable choice for OEMs, thus solidifying the growth of the R-1234yf Refrigerant Market within this application.

Beyond traditional comfort, cabin air conditioning systems are increasingly integrated into broader thermal management strategies. For electric vehicles, while the primary focus shifts to battery thermal management and power electronics cooling, cabin heating and cooling still consume a significant portion of the vehicle's energy budget. This integration requires refrigerants that can efficiently operate across a wider range of temperatures and pressures, contributing to the development of more complex and integrated thermal management systems. The continued innovation in compressor technology, heat exchangers, and refrigerant circuits within cabin air conditioning systems ensures their enduring dominance and influence on the overall Automotive Refrigerants Market, driving demand for both traditional and next-generation refrigerants as vehicles become more sophisticated and environmentally conscious. The ongoing need for maintenance and repair services further bolsters the aftermarket's role in this segment, ensuring a continuous cycle of demand.

Key Regulatory Drivers and Cost Constraints in the Automotive Refrigerants Market

The Automotive Refrigerants Market is profoundly shaped by a dual dynamic of stringent environmental regulations acting as primary growth drivers and significant cost differentials posing persistent constraints. A major driver is the global legislative push for refrigerants with lower Global Warming Potential (GWP), exemplified by the European Union's F-Gas Regulation and the U.S. EPA's Significant New Alternatives Policy (SNAP) program. These regulations have led to the phase-down of high-GWP refrigerants, notably R-134a, which has a GWP of 1,430. This regulatory pressure has accelerated the adoption of ultra-low GWP alternatives such as R-1234yf (GWP of 1), particularly in new vehicle platforms. For instance, the EU’s Mobile Air Conditioning (MAC) Directive required all new vehicle types approved after 2011 and all new vehicles sold after 2017 to use a refrigerant with a GWP below 150, directly fueling the expansion of the R-1234yf Refrigerant Market.

Another significant driver is the rapid global expansion of the Electric Vehicle Thermal Management Market. EVs require sophisticated thermal management for batteries, power electronics, and cabin conditioning to optimize range and performance. These systems often employ more efficient and sometimes different refrigerant cycles, including heat pump systems for heating, which necessitates specific refrigerant properties. The proliferation of EVs is projected to increase demand for specialized refrigerants and Refrigeration Components Market solutions tailored for these advanced thermal architectures.

Conversely, a key constraint impeding market growth is the substantially higher cost of next-generation refrigerants compared to legacy options. R-1234yf, for instance, can be 8-10 times more expensive per kilogram than R-134a. This price disparity translates into higher manufacturing costs for OEMs and increased repair expenses for consumers, potentially slowing adoption in cost-sensitive regions or vehicle segments. Furthermore, the investment required for retrofitting existing service infrastructure and training technicians for handling new refrigerants also represents a significant cost barrier, particularly for the Automotive Aftermarket. Supply chain complexities and the limited number of manufacturers for these specialized fluorochemicals also contribute to price volatility and supply security concerns, presenting ongoing challenges for the Automotive Refrigerants Market.

Competitive Ecosystem of Automotive Refrigerants Market

The competitive landscape of the Automotive Refrigerants Market is characterized by a mix of established chemical giants, specialized refrigerant manufacturers, and automotive component suppliers. These entities vie for market share through product innovation, strategic partnerships, and global distribution networks.

Honeywell International Inc.: A prominent global player offering a broad portfolio of refrigerants, including Solstice® yf (R-1234yf), positioning itself at the forefront of low-GWP solutions. Its strategic focus includes expanding production capacity and collaborating with OEMs to meet evolving regulatory demands.

Oz-Chill: Specializes in environmentally friendly refrigerants, focusing on natural and low-GWP alternatives for various applications, including automotive, catering to niche segments demanding sustainable solutions.

HELLA GmbH & Co. KGaA: A significant supplier of automotive components, including advanced thermal management systems and associated hardware, supporting the integration and efficient use of refrigerants in vehicle climate control.

DuPont: Historically a major producer of refrigerants, though its fluorochemicals business, including refrigerants, was spun off to Chemours. Its legacy in chemical innovation continues to influence related material markets.

Mexichem: Now Orbia Advance Corporation, it is a key producer of fluorinated products, including hydrofluoric acid, a crucial precursor for many refrigerants. This upstream integration provides a competitive advantage in the Fluorochemicals Market.

The Chemours Company: A leading global producer of fluorochemicals and refrigerants, including Opteon™ YF (R-1234yf) and Opteon™ XP series. The company is actively investing in R&D for next-generation, sustainable refrigerant solutions.

Daikin Industries, Ltd.: A global leader in air conditioning and chemical manufacturing, offering a range of fluorochemicals and refrigerants for automotive and other applications. Daikin focuses on energy-efficient and environmentally responsible solutions.

Arkema S.A.: A specialty materials company that produces fluorogases, including refrigerants. Arkema's strategy involves expanding its sustainable solutions portfolio and strengthening its position in high-performance polymers for automotive applications.

Orbia Advance Corporation: A global producer of specialty chemicals, including fluorochemicals. Its vertical integration from raw materials to finished products, such as refrigerants, strengthens its supply chain and market presence.

Dongyue Group Limited: A major Chinese chemical enterprise with a significant presence in fluorosilicon materials and refrigerants, catering to the domestic and international Automotive Refrigerants Market.

Sinochem Holdings Corporation: A diversified Chinese state-owned enterprise involved in chemicals, including fluorochemicals and refrigerants, with a strong focus on domestic market supply and export.

Zhejiang Juhua Co., Ltd.: A leading Chinese fluorochemicals producer, manufacturing various refrigerants and fluoropolymers, playing a crucial role in meeting the demand from Asian automotive manufacturers.

Linde plc: A global industrial gases and engineering company that also supplies specialty gases, including refrigerants, to various industries. Linde's strength lies in its extensive distribution network and technical support capabilities.

Others: This category encompasses smaller regional players, distributors, and companies providing specialized services and components that contribute to the overall ecosystem of the Automotive Refrigerants Market.

Recent Developments & Milestones in Automotive Refrigerants Market

The Automotive Refrigerants Market has witnessed several strategic developments reflecting the industry's shift towards sustainability and efficiency.

Q4 2023: Leading refrigerant manufacturers announced significant investments in expanding R-1234yf production capacities globally, primarily driven by increasing OEM adoption rates in North America and Europe to meet stringent environmental regulations. This expansion aims to alleviate supply concerns and stabilize pricing for the R-1234yf Refrigerant Market.

Q3 2023: Major automotive OEMs in Europe introduced new vehicle models featuring advanced heat pump systems utilizing R-744 (CO₂) refrigerants, particularly in premium electric vehicle segments. This marks a growing trend toward natural refrigerants for enhanced energy efficiency in both heating and cooling functions.

Q2 2023: A significant partnership was forged between a global chemical company and a prominent automotive thermal system supplier to co-develop next-generation, ultra-low GWP refrigerant blends specifically designed for integrated thermal management systems in future hybrid and electric vehicle platforms.

Q1 2023: Regulatory bodies in several Asian countries initiated discussions and proposed timelines for the phase-down of R-134a in new vehicles, signaling a future shift in the R-134a Refrigerant Market in these rapidly growing automotive regions and fostering opportunities for alternative refrigerants.

Q4 2022: Advancements in material science led to the introduction of new hose and seal technologies compatible with R-1234yf, addressing previous concerns regarding system integrity and refrigerant leakage in the Automotive HVAC Systems Market. These innovations enhance the reliability and longevity of refrigerant circuits.

Q3 2022: Research consortia involving universities and industry players published findings on the viability and safety of R-152a as an ultra-low GWP alternative, contingent on further system design modifications to mitigate its flammability characteristics for widespread automotive adoption.

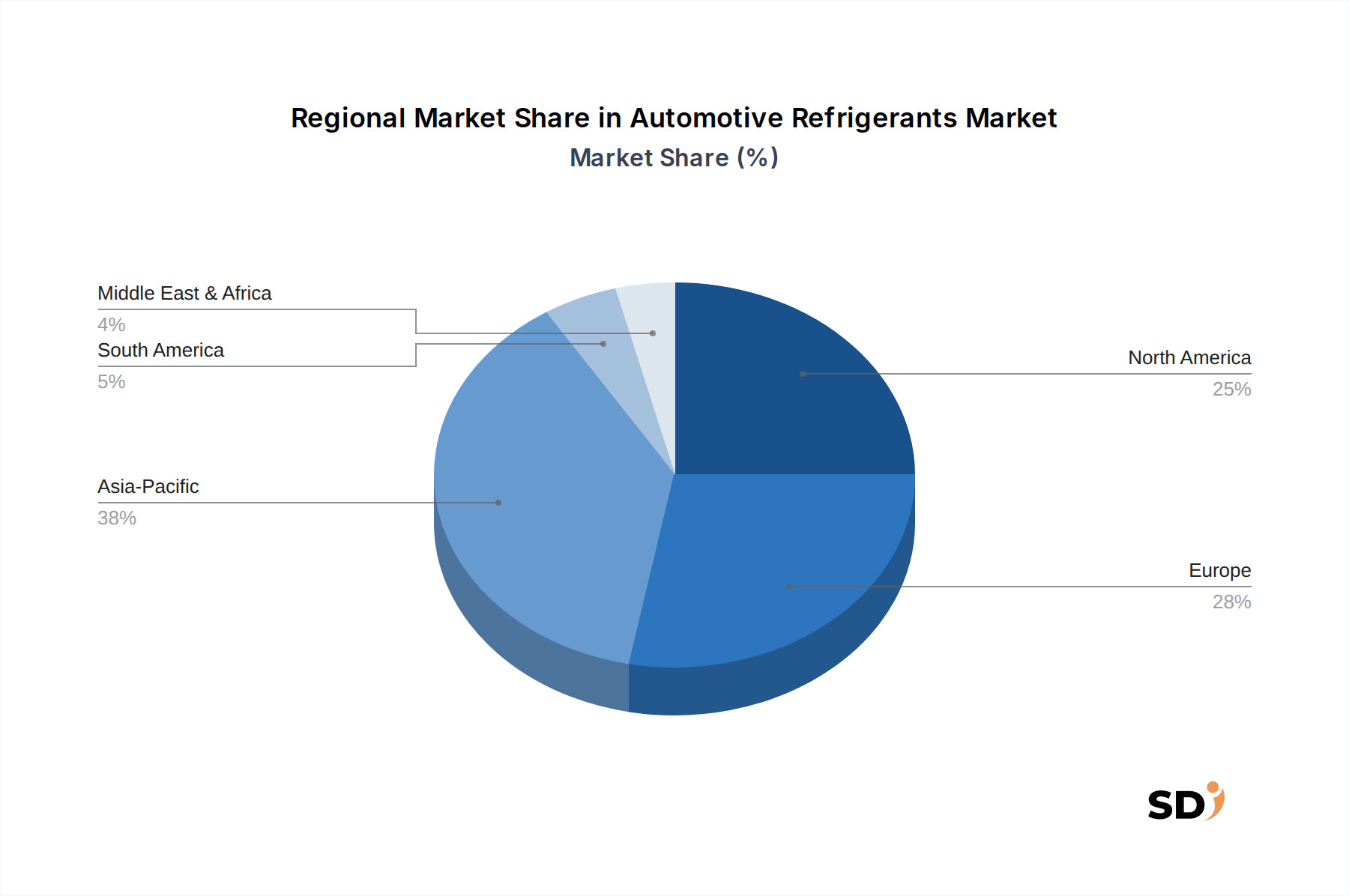

Regional Market Breakdown for Automotive Refrigerants Market

Geographically, the Automotive Refrigerants Market exhibits diverse growth patterns influenced by regional regulatory frameworks, vehicle production volumes, and consumer demand. While specific regional CAGRs are not provided, an analysis of underlying market dynamics allows for a comprehensive breakdown of key regions.

Asia Pacific currently represents the largest and fastest-growing region in the Automotive Refrigerants Market. Driven by booming automotive production in countries like China, India, and Japan, this region accounts for a substantial share of refrigerant consumption, primarily for initial OEM fill. The increasing adoption of advanced air conditioning systems and a gradual shift towards low-GWP refrigerants, spurred by domestic regulations and export requirements, propel its growth. The expanding Electric Vehicle Thermal Management Market in countries like China is also a significant demand driver, requiring advanced refrigerant solutions.

Europe is a mature but highly dynamic market, characterized by stringent environmental regulations, particularly the EU F-Gas Regulation. This has led to an early and widespread adoption of R-1234yf in new vehicles, making it a leading region for the R-1234yf Refrigerant Market. Europe also shows increasing interest in natural refrigerants like R-744 (CO₂) for certain high-efficiency applications, especially in premium and electric vehicles. The emphasis on fuel efficiency and reduced emissions drives continuous innovation in Automotive HVAC Systems Market.

North America holds a significant share, predominantly driven by a large vehicle parc and the implementation of EPA SNAP rules. The region has seen a robust transition to R-1234yf in new vehicles, with a substantial Automotive Aftermarket for both R-134a and R-1234yf. The demand for comfort in varied climate zones across the United States and Canada ensures consistent uptake of automotive refrigerants. The ongoing evolution of light-duty and commercial vehicle fleets further underpins demand.

South America and the Middle East & Africa (MEA) regions are emerging markets with considerable growth potential. While the R-134a Refrigerant Market still dominates due to lower costs and less stringent regulations compared to developed markets, there is a gradual shift towards modern refrigerant technologies as vehicle fleets are modernized and global automotive standards trickle down. Increasing vehicle ownership and demand for basic Automotive Climate Control Market comfort are primary demand drivers in these regions, signaling future opportunities for low-GWP refrigerants and advanced thermal solutions.

Pricing Dynamics & Margin Pressure in Automotive Refrigerants Market

The pricing dynamics in the Automotive Refrigerants Market are complex, influenced by raw material costs, regulatory mandates, manufacturing complexities, and competitive intensity. The transition from R-134a to R-1234yf has introduced a significant price disparity. R-1234yf, being a newer, patented, and more complex molecule to produce, commands a substantially higher average selling price (ASP), often 8 to 10 times that of R-134a per kilogram. This directly impacts the cost structure for OEMs and the Automotive Aftermarket, where technicians must absorb higher material costs for service and repairs.

Margin structures across the value chain are experiencing pressure. Refrigerant manufacturers face high R&D and capital expenditure for new production facilities, particularly for R-1234yf, necessitating higher ASPs to ensure profitability. Distributors and automotive parts suppliers, on the other hand, navigate increased inventory costs and the need for specialized equipment to handle different refrigerant types. OEMs are absorbing some of these higher costs in vehicle manufacturing to meet regulatory compliance, which can put pressure on vehicle profit margins or necessitate price increases for consumers.

Key cost levers primarily include the price volatility of feedstock chemicals, especially fluorochemicals. Hydrofluoric acid, a crucial raw material for many fluorinated refrigerants, is susceptible to commodity cycles and supply chain disruptions, directly impacting production costs. Energy costs associated with complex chemical synthesis also play a significant role. Competitive intensity among the limited number of R-1234yf producers (primarily Honeywell and Chemours) can influence pricing, though demand driven by regulatory mandates currently provides these companies with strong pricing power. For the R-134a Refrigerant Market, margin pressure is intense due to its mature status, widespread availability, and numerous producers, leading to commoditization.

Supply Chain & Raw Material Dynamics for Automotive Refrigerants Market

The Automotive Refrigerants Market's supply chain is intricate and highly dependent on the global Fluorochemicals Market. The primary upstream dependency lies in the availability and pricing of key intermediates, notably anhydrous hydrogen fluoride (AHF) or hydrofluoric acid. This critical raw material is essential for the synthesis of most fluorinated refrigerants, including R-134a and R-1234yf. Other vital inputs include chlorine, methane, and various catalysts, all subject to global commodity market fluctuations.

Sourcing risks are significant, stemming from the concentrated nature of AHF production and geopolitical factors affecting its supply. A disruption in the supply of AHF from major producing regions can ripple through the entire refrigerant value chain, impacting production schedules and increasing costs. For instance, temporary plant closures or export restrictions in key raw material producing countries have historically led to price spikes and supply shortages for downstream refrigerant manufacturers.

Price volatility of these key inputs directly affects the profitability of refrigerant producers. When AHF prices rise, it increases the cost of manufacturing refrigerants, which is then often passed down to OEMs and the Automotive Aftermarket. This can lead to increased prices for consumers and margin compression for component suppliers in the Refrigeration Components Market. The increasing demand for R-1234yf further stresses this supply chain, as its manufacturing process requires specific feedstocks and sophisticated production capabilities that are less widely available than those for R-134a.

Moreover, the transition to new refrigerants like R-1234yf has necessitated significant investments in new production facilities and specialized logistics for handling and distribution. This has created a bifurcated supply chain where R-134a is widely available, while R-1234yf supply is more controlled and concentrated among fewer players. Supply chain disruptions, such as those experienced during the COVID-19 pandemic or due to extreme weather events, have highlighted vulnerabilities, leading to longer lead times and elevated freight costs for all types of refrigerants in the Automotive Refrigerants Market.

Automotive Refrigerants Segmentation

1. Refrigerant Type

1.1. R-134a

1.2. R-1234yf

1.3. R-744 (CO₂ Refrigerant)

1.4. R-152a

1.5. Others

2. System Type

2.1. Conventional Automotive Air Conditioning Systems

2.2. Heat Pump HVAC Systems

2.3. Integrated Thermal Management Systems

3. Application

3.1. Cabin Air Conditioning Systems

3.2. Heat Pump Systems

3.3. Battery Thermal Management

3.4. Power Electronics Cooling

3.5. Commercial Vehicle Climate Control

3.6. Others

4. Sales Channel

4.1. OEM

4.2. Aftermarket

Automotive Refrigerants Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Rest of Europe

4. Middle East & Africa

4.1. GCC

4.2. North Africa

4.3. South Africa

4.4. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. Rest of Asia Pacific

Automotive Refrigerants REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 5.9% from 2020-2034

Segmentation

By Refrigerant Type

R-134a

R-1234yf

R-744 (CO₂ Refrigerant)

R-152a

Others

By System Type

Conventional Automotive Air Conditioning Systems

Heat Pump HVAC Systems

Integrated Thermal Management Systems

By Application

Cabin Air Conditioning Systems

Heat Pump Systems

Battery Thermal Management

Power Electronics Cooling

Commercial Vehicle Climate Control

Others

By Sales Channel

OEM

Aftermarket

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Rest of Europe

Middle East & Africa

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Refrigerant Type

5.1.1. R-134a

5.1.2. R-1234yf

5.1.3. R-744 (CO₂ Refrigerant)

5.1.4. R-152a

5.1.5. Others

5.2. Market Analysis, Insights and Forecast - by System Type

5.2.1. Conventional Automotive Air Conditioning Systems

5.2.2. Heat Pump HVAC Systems

5.2.3. Integrated Thermal Management Systems

5.3. Market Analysis, Insights and Forecast - by Application

5.3.1. Cabin Air Conditioning Systems

5.3.2. Heat Pump Systems

5.3.3. Battery Thermal Management

5.3.4. Power Electronics Cooling

5.3.5. Commercial Vehicle Climate Control

5.3.6. Others

5.4. Market Analysis, Insights and Forecast - by Sales Channel

5.4.1. OEM

5.4.2. Aftermarket

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Refrigerant Type

6.1.1. R-134a

6.1.2. R-1234yf

6.1.3. R-744 (CO₂ Refrigerant)

6.1.4. R-152a

6.1.5. Others

6.2. Market Analysis, Insights and Forecast - by System Type

6.2.1. Conventional Automotive Air Conditioning Systems

6.2.2. Heat Pump HVAC Systems

6.2.3. Integrated Thermal Management Systems

6.3. Market Analysis, Insights and Forecast - by Application

6.3.1. Cabin Air Conditioning Systems

6.3.2. Heat Pump Systems

6.3.3. Battery Thermal Management

6.3.4. Power Electronics Cooling

6.3.5. Commercial Vehicle Climate Control

6.3.6. Others

6.4. Market Analysis, Insights and Forecast - by Sales Channel

6.4.1. OEM

6.4.2. Aftermarket

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Refrigerant Type

7.1.1. R-134a

7.1.2. R-1234yf

7.1.3. R-744 (CO₂ Refrigerant)

7.1.4. R-152a

7.1.5. Others

7.2. Market Analysis, Insights and Forecast - by System Type

7.2.1. Conventional Automotive Air Conditioning Systems

7.2.2. Heat Pump HVAC Systems

7.2.3. Integrated Thermal Management Systems

7.3. Market Analysis, Insights and Forecast - by Application

7.3.1. Cabin Air Conditioning Systems

7.3.2. Heat Pump Systems

7.3.3. Battery Thermal Management

7.3.4. Power Electronics Cooling

7.3.5. Commercial Vehicle Climate Control

7.3.6. Others

7.4. Market Analysis, Insights and Forecast - by Sales Channel

7.4.1. OEM

7.4.2. Aftermarket

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Refrigerant Type

8.1.1. R-134a

8.1.2. R-1234yf

8.1.3. R-744 (CO₂ Refrigerant)

8.1.4. R-152a

8.1.5. Others

8.2. Market Analysis, Insights and Forecast - by System Type

8.2.1. Conventional Automotive Air Conditioning Systems

8.2.2. Heat Pump HVAC Systems

8.2.3. Integrated Thermal Management Systems

8.3. Market Analysis, Insights and Forecast - by Application

8.3.1. Cabin Air Conditioning Systems

8.3.2. Heat Pump Systems

8.3.3. Battery Thermal Management

8.3.4. Power Electronics Cooling

8.3.5. Commercial Vehicle Climate Control

8.3.6. Others

8.4. Market Analysis, Insights and Forecast - by Sales Channel

8.4.1. OEM

8.4.2. Aftermarket

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Refrigerant Type

9.1.1. R-134a

9.1.2. R-1234yf

9.1.3. R-744 (CO₂ Refrigerant)

9.1.4. R-152a

9.1.5. Others

9.2. Market Analysis, Insights and Forecast - by System Type

9.2.1. Conventional Automotive Air Conditioning Systems

9.2.2. Heat Pump HVAC Systems

9.2.3. Integrated Thermal Management Systems

9.3. Market Analysis, Insights and Forecast - by Application

9.3.1. Cabin Air Conditioning Systems

9.3.2. Heat Pump Systems

9.3.3. Battery Thermal Management

9.3.4. Power Electronics Cooling

9.3.5. Commercial Vehicle Climate Control

9.3.6. Others

9.4. Market Analysis, Insights and Forecast - by Sales Channel

9.4.1. OEM

9.4.2. Aftermarket

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Refrigerant Type

10.1.1. R-134a

10.1.2. R-1234yf

10.1.3. R-744 (CO₂ Refrigerant)

10.1.4. R-152a

10.1.5. Others

10.2. Market Analysis, Insights and Forecast - by System Type

10.2.1. Conventional Automotive Air Conditioning Systems

10.2.2. Heat Pump HVAC Systems

10.2.3. Integrated Thermal Management Systems

10.3. Market Analysis, Insights and Forecast - by Application

10.3.1. Cabin Air Conditioning Systems

10.3.2. Heat Pump Systems

10.3.3. Battery Thermal Management

10.3.4. Power Electronics Cooling

10.3.5. Commercial Vehicle Climate Control

10.3.6. Others

10.4. Market Analysis, Insights and Forecast - by Sales Channel

10.4.1. OEM

10.4.2. Aftermarket

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Honeywell International Inc.

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Oz-Chill

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. HELLA GmbH & Co. KGaA

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. DuPont

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Mexichem

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. The Chemours Company

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Daikin Industries Ltd.

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Arkema S.A.

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Orbia Advance Corporation

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Dongyue Group Limited

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Sinochem Holdings Corporation

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Zhejiang Juhua Co. Ltd.

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. Linde plc

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.1.14. Others

11.1.14.1. Company Overview

11.1.14.2. Products

11.1.14.3. Company Financials

11.1.14.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Refrigerant Type 2025 & 2033

Figure 3: Revenue Share (%), by Refrigerant Type 2025 & 2033

Figure 4: Revenue (million), by System Type 2025 & 2033

Figure 5: Revenue Share (%), by System Type 2025 & 2033

Figure 6: Revenue (million), by Application 2025 & 2033

Figure 7: Revenue Share (%), by Application 2025 & 2033

Figure 8: Revenue (million), by Sales Channel 2025 & 2033

Figure 50: Revenue (million), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Refrigerant Type 2020 & 2033

Table 2: Revenue million Forecast, by System Type 2020 & 2033

Table 3: Revenue million Forecast, by Application 2020 & 2033

Table 4: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Revenue million Forecast, by Refrigerant Type 2020 & 2033

Table 7: Revenue million Forecast, by System Type 2020 & 2033

Table 8: Revenue million Forecast, by Application 2020 & 2033

Table 9: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 10: Revenue million Forecast, by Country 2020 & 2033

Table 11: Revenue (million) Forecast, by Application 2020 & 2033

Table 12: Revenue (million) Forecast, by Application 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue million Forecast, by Refrigerant Type 2020 & 2033

Table 15: Revenue million Forecast, by System Type 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue million Forecast, by Refrigerant Type 2020 & 2033

Table 23: Revenue million Forecast, by System Type 2020 & 2033

Table 24: Revenue million Forecast, by Application 2020 & 2033

Table 25: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 26: Revenue million Forecast, by Country 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue (million) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Revenue (million) Forecast, by Application 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue million Forecast, by Refrigerant Type 2020 & 2033

Table 35: Revenue million Forecast, by System Type 2020 & 2033

Table 36: Revenue million Forecast, by Application 2020 & 2033

Table 37: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 38: Revenue million Forecast, by Country 2020 & 2033

Table 39: Revenue (million) Forecast, by Application 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue million Forecast, by Refrigerant Type 2020 & 2033

Table 44: Revenue million Forecast, by System Type 2020 & 2033

Table 45: Revenue million Forecast, by Application 2020 & 2033

Table 46: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 47: Revenue million Forecast, by Country 2020 & 2033

Table 48: Revenue (million) Forecast, by Application 2020 & 2033

Table 49: Revenue (million) Forecast, by Application 2020 & 2033

Table 50: Revenue (million) Forecast, by Application 2020 & 2033

Table 51: Revenue (million) Forecast, by Application 2020 & 2033

Table 52: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our robust methodology prioritizes primary research, constituting 75% of the overall data collection effort. This extensive engagement ensures direct insights from industry thought leaders, offering a granular, real-time perspective on market dynamics, technological shifts, and emerging opportunities. Our primary research strategy involves in-depth, semi-structured interviews and discussions conducted across diverse geographic regions and key segments of the automotive refrigerant value chain.

Key participants in our primary research include:

Company Types Interviewed:

Automotive Original Equipment Manufacturers (OEMs) specializing in vehicle thermal management systems.

Major Global Refrigerant Manufacturers and Chemical Suppliers.

Tier 1 and Tier 2 Automotive HVAC and Thermal Management System Suppliers.

Large-scale Automotive Aftermarket Parts Distributors and Service Network Operators.

Automotive HVAC/Thermal Management System Suppliers

30%

Automotive Aftermarket Parts Distributors

15%

Specialty Component Manufacturers

10%

Secondary Research & Industry Benchmarking

Complementing our primary research, secondary data collection forms the remaining 25% of our methodology. This phase is crucial for establishing a foundational understanding of the market, validating primary findings, and providing historical context and overarching industry trends. Our researchers meticulously gather information from a wide array of credible and authoritative sources.

Our secondary research leverages:

Proprietary and Commercial Financial Databases: Bloomberg Terminal, Factiva, Hoovers, and PitchBook.

Government Publications & Data Repositories: Official reports and statistics from government bodies.

Non-Governmental Organizations (NGOs) & Research Institutions: Data, whitepapers, and studies.

Trade Associations & Industry Bodies: Publications, annual reports, and technical standards.

Globally Recognized Industry Associations & Regulatory Bodies:

SAE International (Society of Automotive Engineers) https://www.sae.org/ - For automotive engineering standards and best practices, particularly related to HVAC and thermal systems.

U.S. Environmental Protection Agency (EPA) https://www.epa.gov/ - For regulations pertaining to refrigerants, F-gases, and environmental impact in North America.

European Commission / European Environment Agency (EEA) https://ec.europa.eu/ - For F-Gas regulations, environmental policies, and automotive industry directives in Europe.

International Institute of Refrigeration (IIR) https://www.iifiir.org/ - For scientific and technical information on refrigeration and associated technologies.

Demand Modeling & Market Estimation

Our market estimation process employs a rigorous combination of top-down and bottom-up methodologies, meticulously triangulated across multiple data points to ensure the highest degree of accuracy and reliability.

Top-Down Approach: This involves starting with the total available market at a macro level (e.g., global automotive production, total refrigerant consumption across all sectors) and then segmenting it down to the specific market for automotive refrigerants based on relevant market share, penetration rates, and application specifics.

Bottom-Up Approach: This involves building the market size by aggregating data from the smallest identifiable units upwards. For the automotive refrigerants market, key metrics and variables used for bottom-up calculation include:

New Vehicle Production Volumes (segmented by region, vehicle type - ICE, EV, Hybrid).

Average Refrigerant Charge per Vehicle (differentiated by refrigerant type, system type, and vehicle class).

Aftermarket Recharge and Replacement Frequency/Volumes (derived from vehicle parc, average vehicle age, and service intervals).

Average Price per Kilogram of Refrigerant (by type, region, and sales channel - OEM vs. Aftermarket).

Multi-Level Data Triangulation: All gathered primary and secondary data, along with top-down and bottom-up estimates, are cross-referenced and validated through a multi-stage triangulation process. This includes comparing findings from different sources, verifying assumptions with industry experts, and using statistical models to reconcile discrepancies, ensuring a cohesive and robust market picture.

Data Accuracy & Quality Check

We are committed to delivering the highest quality market intelligence. Our stringent data validation processes ensure an estimated data accuracy level of 85-90%. Every data point, trend, and forecast undergoes multiple layers of verification by senior analysts before inclusion in the final report. Furthermore, our commitment to real-time market insights means that every report is meticulously updated with the latest available data and market developments up to the date of purchase, providing clients with the most current and actionable intelligence for their strategic decision-making.

Frequently Asked Questions

1. What are the primary barriers to entry in the Automotive Refrigerants market?

Entry barriers include high R&D costs for new refrigerants like R-1234yf, stringent regulatory approvals, and established intellectual property by key players such as Honeywell International Inc. and The Chemours Company. Supply chain control and manufacturing expertise also create significant moats.

2. How do raw material sourcing and supply chain considerations impact the Automotive Refrigerants industry?

The industry relies on specialized chemical precursors, making supply chains susceptible to raw material price volatility and availability. Manufacturers like Daikin Industries, Ltd. manage complex global supply networks to ensure consistent production and distribution of refrigerants like R-134a and R-1234yf.

3. Which factors influence export-import dynamics for Automotive Refrigerants globally?

International trade flows are shaped by regional regulations governing refrigerant use, such as HFC phase-downs, and manufacturing hubs in Asia-Pacific and Europe. The demand for next-generation refrigerants like R-1234yf, produced by companies like Arkema S.A., drives significant cross-border movement.

4. What disruptive technologies and emerging substitutes are impacting Automotive Refrigerants?

R-744 (CO₂ Refrigerant) and R-152a are emerging as lower GWP alternatives, challenging traditional R-134a dominance. Advancements in heat pump HVAC systems and battery thermal management for EVs also necessitate new refrigerant formulations, potentially displacing older technologies.

5. What is the projected market size and CAGR for Automotive Refrigerants through 2033?

The Automotive Refrigerants market is valued at $267 million. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.9% through 2033, driven by regulatory shifts and demand for efficient thermal management.

6. How are technological innovations and R&D trends shaping the Automotive Refrigerants industry?

R&D focuses on ultra-low GWP refrigerants and optimizing blends for EV applications, including battery thermal management and integrated thermal management systems. Companies like DuPont and Dongyue Group Limited are investing in research to develop more energy-efficient and environmentally compliant solutions.