1. What is the projected valuation and growth rate for the Cold Cereal Food market?

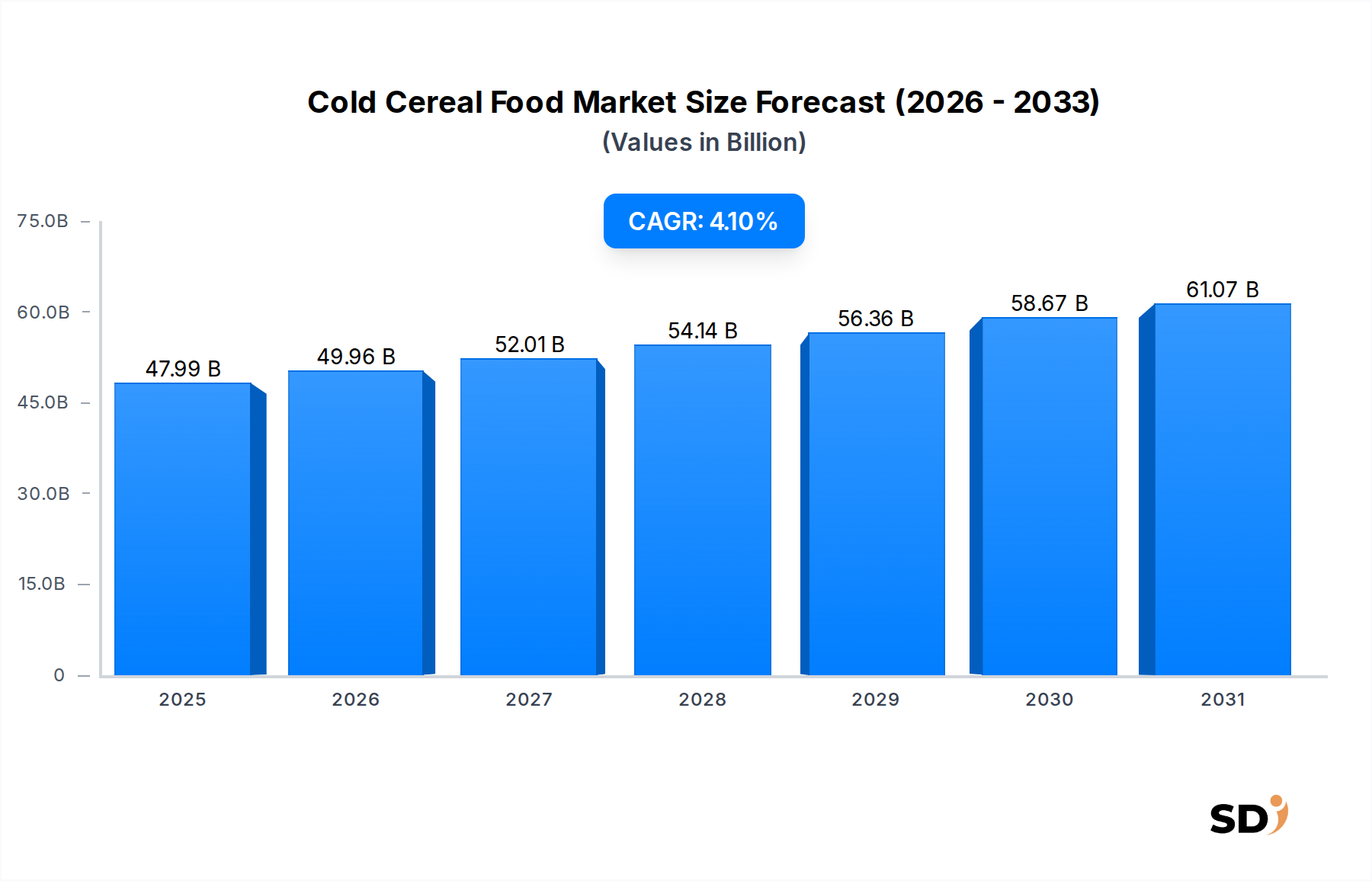

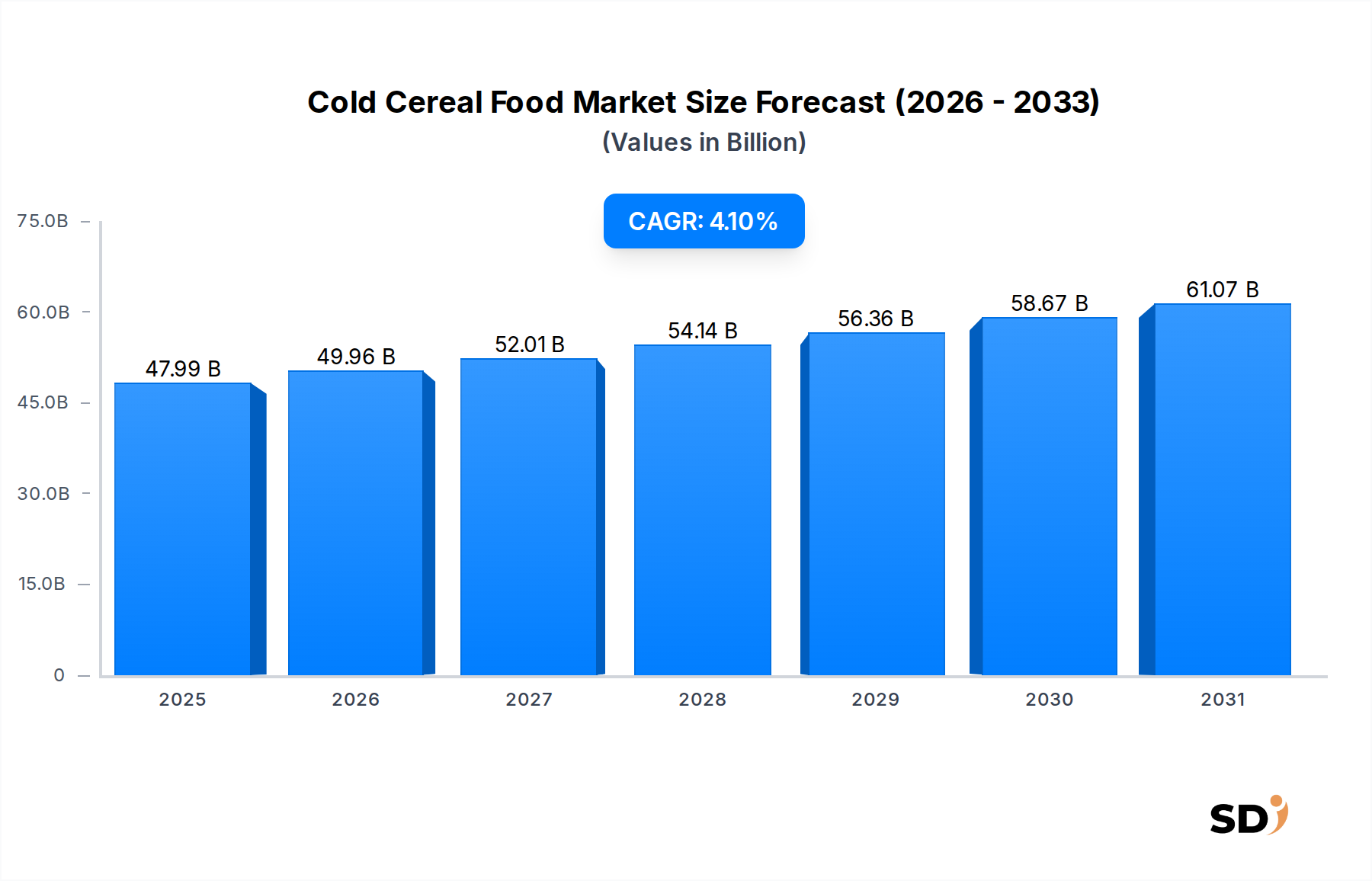

The Cold Cereal Food market is valued at $47.99 billion in 2025. It is projected to expand at a Compound Annual Growth Rate (CAGR) of 4.1% from the base year 2025.

+1 2315155523

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Cold Cereal Food

Cold Cereal FoodResearch Associate

The Global Cold Cereal Food Market is currently valued at an impressive $47.99 billion in 2025, demonstrating its significant footprint within the broader Packaged Food Market. This market is projected to expand robustly, registering a Compound Annual Growth Rate (CAGR) of 4.1% through 2032, to reach an estimated valuation of $63.73 billion. The sustained growth is underpinned by several macro-economic and consumer-centric drivers. A primary demand catalyst is the increasing consumer preference for convenient, ready-to-eat breakfast options, aligning with modern, fast-paced lifestyles. Urbanization trends and rising disposable incomes, particularly in emerging economies, further fuel this demand, positioning cold cereals as an accessible and versatile dietary staple.

Key market drivers include ongoing product innovation, focusing on enhanced nutritional profiles and diversified flavor offerings. Manufacturers are strategically reformulating products to incorporate functional ingredients, reduce sugar content, and introduce plant-based or gluten-free alternatives, catering to an increasingly health-conscious consumer base. The proliferation of specialized diets and a greater emphasis on wellness have propelled the growth of segments such as the Organic Food Market within cold cereals. Furthermore, the expansion of modern retail channels, including hypermarkets, supermarkets, and the burgeoning Online Retail Market, ensures wider product accessibility and consumer reach. Promotional activities and aggressive marketing strategies by key players also contribute significantly to market expansion, fostering brand loyalty and driving new product adoption. Despite challenges such as competition from other Breakfast Food Market alternatives and concerns regarding sugar content, the Cold Cereal Food Market exhibits a resilient growth trajectory, leveraging convenience and ongoing innovation to meet evolving consumer demands globally." , "## Supermarkets & Hypermarkets Dominance in the Cold Cereal Food Market

The distribution landscape of the Cold Cereal Food Market is largely dominated by the Supermarkets & Hypermarkets segment, which currently accounts for the lion's share of revenue. This segment’s supremacy is attributed to several critical factors that align perfectly with consumer purchasing behaviors for staple food items like cold cereals. Supermarkets and hypermarkets offer an unparalleled breadth of product choice, presenting consumers with an extensive array of brands, product types (e.g., Flaked Cereals, Granola Cereals, Muesli Cereals), ingredient profiles (wheat-based, corn-based, oat-based), and flavor varieties from numerous manufacturers. This 'one-stop-shop' convenience allows consumers to fulfill their entire grocery list, including cold cereals, efficiently under a single roof. The sheer scale and footprint of these retail formats provide optimal visibility and accessibility for cereal brands, acting as crucial touchpoints for broad consumer engagement.

Moreover, the competitive pricing strategies, frequent promotional offers, and loyalty programs employed by supermarkets and hypermarkets significantly influence consumer purchasing decisions. These outlets are adept at leveraging merchandising techniques, strategic shelf placement, and in-store advertisements to promote cold cereal products, thereby stimulating impulse purchases and driving sales volumes. The established supply chain infrastructure and robust logistics networks of major supermarket chains ensure consistent product availability across diverse geographic locations, minimizing stockouts and enhancing consumer satisfaction. While the Online Retail Market is growing rapidly and specialty stores cater to niche demands, supermarkets and hypermarkets continue to serve as the primary channel for bulk purchasing and everyday grocery needs for the majority of global consumers. The convenience of physically inspecting products, comparing options, and integrating cereal purchases into a larger shopping trip reinforces the dominant position of this segment. Consequently, manufacturers heavily invest in maintaining strong relationships with these retailers, ensuring prime shelf space and participation in promotional campaigns to capture and consolidate their market share within the highly competitive Cold Cereal Food Market." , "## Key Market Drivers & Constraints in Cold Cereal Food Market

The Cold Cereal Food Market's trajectory is shaped by a complex interplay of demand-side drivers and supply-side constraints, necessitating strategic responses from market participants. A primary driver is the accelerating consumer demand for convenience-oriented breakfast solutions. With global urban populations experiencing increasingly hectic schedules, ready-to-eat cold cereals offer a time-efficient and accessible morning meal. This trend is quantified by a consistent year-over-year increase in convenience food sales across developed and developing economies, with breakfast foods being a significant contributor. Another pivotal driver is the growing health and wellness consciousness among consumers. This has led to a surge in demand for fortified cereals, products with lower sugar content, whole grains, and functional ingredients. For instance, the Organic Food Market segment within cold cereals has shown a significant growth rate, reflecting consumer willingness to pay a premium for perceived healthier options. Product innovation, including new flavor profiles and ingredient diversification (e.g., plant-based protein cereals), also serves as a crucial driver, attracting new demographics and stimulating repeat purchases.

Conversely, the market faces notable constraints. Intense competition from alternative breakfast options poses a significant challenge. Consumers are increasingly diversifying their breakfast choices, opting for protein-rich yogurts, breakfast bars, smoothies, or hot breakfast meals, which can fragment the traditional cold cereal consumer base. Furthermore, persistent consumer concerns regarding sugar content in many conventional cold cereals act as a restraint. Public health campaigns and dietary guidelines advocating for reduced sugar intake compel manufacturers to reformulate products, incurring R&D and production costs. Lastly, volatility in raw material prices presents a supply-side constraint. The price fluctuations of key ingredients like wheat, corn, oats, and sugar, heavily influenced by global Grain Market dynamics, climate events, and geopolitical factors, directly impact production costs and profit margins for cereal manufacturers, adding an element of unpredictability to the Cold Cereal Food Market." , "## Competitive Ecosystem of Cold Cereal Food Market

The Cold Cereal Food Market is characterized by a highly competitive landscape dominated by several multinational food corporations and a growing number of specialized regional players. These companies leverage extensive distribution networks, aggressive marketing strategies, and continuous product innovation to maintain and expand their market share:

The Cold Cereal Food Market continues to evolve with strategic initiatives aimed at capturing consumer attention and addressing changing dietary trends. Key developments highlight a focus on health, sustainability, and market expansion:

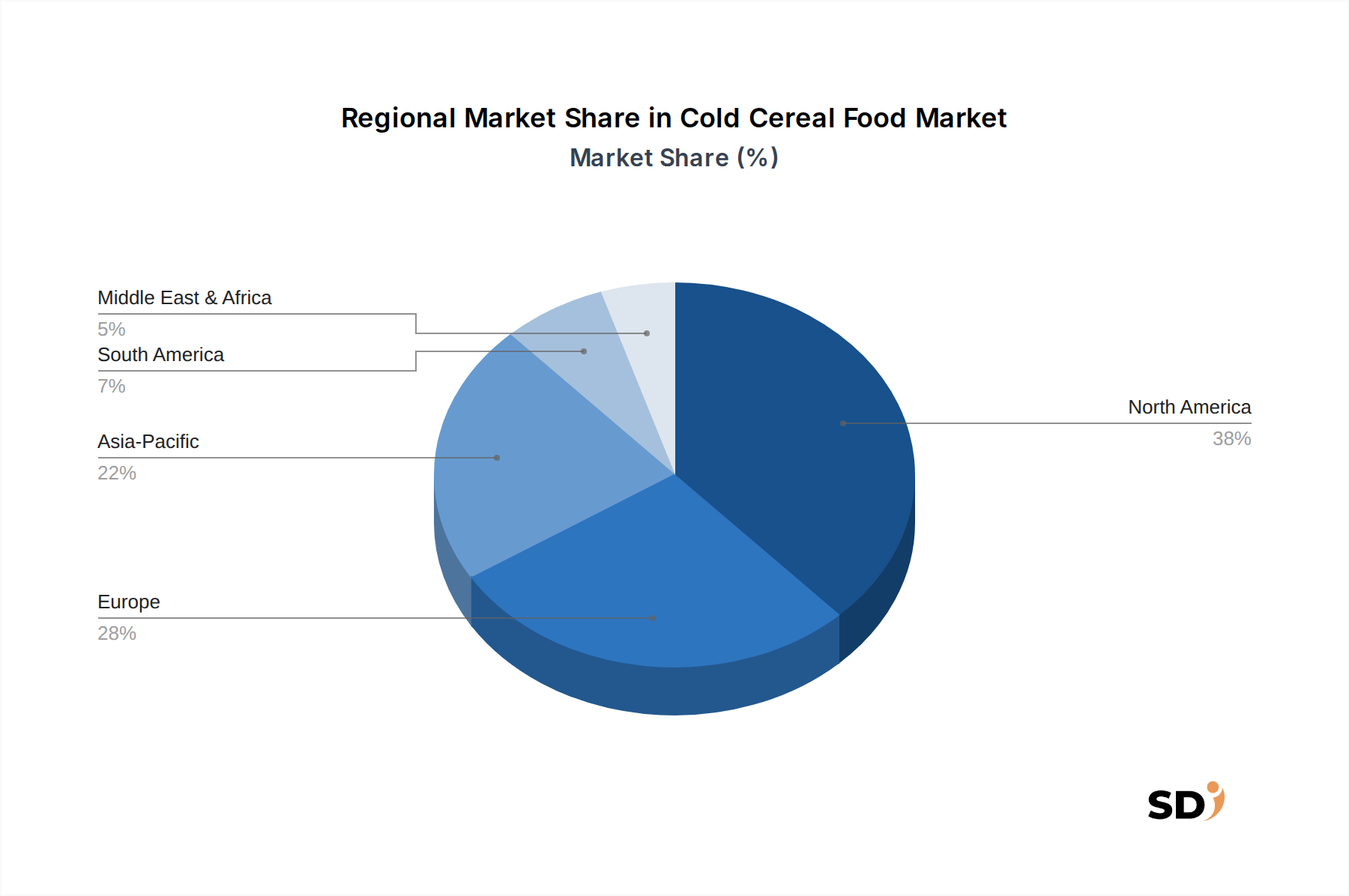

The Cold Cereal Food Market exhibits distinct growth patterns and consumption dynamics across its key geographical regions, reflecting diverse cultural preferences, economic conditions, and retail infrastructures. North America holds the largest revenue share in the global market. The United States and Canada, driven by established breakfast routines, high disposable incomes, and the strong presence of major cereal manufacturers, represent a mature yet significant market. Convenience remains a primary driver, with robust demand for a wide variety of cold cereal options, including those catering to specific dietary needs or premium segments like the Granola Cereals Market. Europe also represents a substantial market, characterized by stable demand in countries like the UK, Germany, and France, with a growing emphasis on organic and healthy options, contributing to the expansion of the Organic Food Market.

Asia Pacific is projected to be the fastest-growing region in the Cold Cereal Food Market, driven by rapidly increasing urbanization, rising disposable incomes, and a gradual shift towards Western-style breakfast habits. Countries such as China, India, and ASEAN nations are witnessing a surge in demand for convenient food products, presenting significant opportunities for market penetration. Manufacturers are tailoring products to local tastes and preferences, contributing to higher regional CAGRs. Latin America, particularly Brazil and Argentina, demonstrates moderate growth, influenced by improving economic conditions and increased consumer awareness of packaged breakfast solutions. The Middle East & Africa region, while smaller in absolute terms, is also experiencing notable growth, primarily due to expanding retail infrastructure and changing lifestyles. Demand in these regions is heavily influenced by the adoption of modern retail formats, including the growth of the Online Retail Market, which facilitates wider product accessibility and consumer engagement, fostering an upward trajectory for the Cold Cereal Food Market globally." , "## Supply Chain & Raw Material Dynamics for Cold Cereal Food Market

The supply chain of the Cold Cereal Food Market is intricate, characterized by upstream dependencies on agricultural commodities and downstream reliance on efficient manufacturing and distribution networks. Key raw materials include major grains such as wheat, corn, oats, and rice, alongside sweeteners (sugar, corn syrup), flavorings, fortifying agents (vitamins, minerals), and packaging materials. Sourcing risks are significant, primarily stemming from the inherent volatility of the global Grain Market. Agricultural output is highly susceptible to climatic conditions, including droughts, floods, and unseasonable weather patterns, which can drastically impact crop yields and, consequently, raw material prices. Geopolitical tensions and trade policies also play a crucial role, influencing the availability and cost of imported grains and other ingredients.

Price volatility of key inputs is a perennial challenge. For instance, global wheat prices can fluctuate significantly based on harvest reports from major producing regions, impacting the cost of wheat-based cereals. Similarly, sugar prices are subject to global supply-demand dynamics and regulatory interventions. Historically, disruptions such as the COVID-19 pandemic highlighted vulnerabilities, leading to increased freight costs, labor shortages, and logistical bottlenecks, which affected the timely delivery of raw materials and finished products. Manufacturers in the Cold Cereal Food Market mitigate these risks through diversified sourcing strategies, long-term contracts with suppliers, and hedging against commodity price fluctuations. Investment in sustainable agriculture practices is also gaining traction, aiming to secure future supply and appeal to environmentally conscious consumers within the broader Packaged Food Market. The efficiency and resilience of this supply chain are critical to ensuring consistent product availability and managing production costs." , "## Regulatory & Policy Landscape Shaping Cold Cereal Food Market

The Cold Cereal Food Market operates within a complex web of regulatory frameworks and policy initiatives designed to ensure food safety, consumer protection, and fair trade practices across key geographies. Major regulatory bodies such as the Food and Drug Administration (FDA) in the United States, the European Food Safety Authority (EFSA) in Europe, and national food safety agencies in Asia Pacific, set stringent standards for ingredient sourcing, manufacturing processes, labeling, and marketing. These regulations directly impact product formulation, requiring adherence to permitted additive lists, maximum residue limits for pesticides, and hygiene protocols in facilities, often supported by the Food Processing Equipment Market.

Labeling requirements are particularly critical, mandating clear disclosure of nutritional information, allergen declarations, and ingredient lists. Recent policy changes in several regions have focused on clearer front-of-pack labeling for high-sugar, high-salt, or high-fat products, influencing consumer choices and prompting manufacturers to reformulate. For instance, initiatives to reduce sugar content in breakfast cereals, driven by public health concerns about obesity and diabetes, have led to a noticeable trend of product innovation in the Breakfast Food Market. Marketing to children is another heavily scrutinized area, with many countries implementing restrictions on advertising unhealthy food products to minors. Furthermore, the growth of the Organic Food Market segment within cereals necessitates compliance with specific organic certification standards, which vary by country but generally require adherence to non-GMO, chemical-pesticide-free, and sustainable farming practices. Ongoing monitoring of these evolving regulatory landscapes is crucial for manufacturers to ensure compliance, avoid penalties, and maintain consumer trust in the Cold Cereal Food Market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Our market research methodology for the "Cold Cereal Food by Product Type (Flaked Cereals, Granola Cereals, Muesli Cereals, Puffed Cereals, Shredded Cereals, Bran Cereals, Others), by Ingredient Type (Wheat-Based Cereals, Corn-Based Cereals, Oat-Based Cereals, Rice-Based Cereals, Barley-Based Cereals, Multigrain Cereals, Others), by Nature (Conventional, Organic), by Flavor (Plain/Original, Chocolate, Honey, Fruit-Based, Vanilla, Cinnamon, Others), by Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Specialty Stores, Online Retail/E-Commerce, Wholesale Clubs, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034" report is built on a robust, multi-faceted approach designed to deliver highly accurate and actionable market insights. It strategically blends extensive primary research with rigorous secondary analysis, leveraging advanced analytical techniques to forecast market trends and opportunities.

| Stakeholder Role | Interview Share (%) |

|---|---|

| VP of Sales & Marketing (Cereal Division) | 30% |

| Senior Product Category Manager (Retail Grocery) | 30% |

| R&D Director (Food Science & Nutrition) | 20% |

| Supply Chain Director (Food Manufacturing & Logistics) | 20% |

| Company Type | Representation (%) |

|---|---|

| Large-Scale Cereal Manufacturers | 35% |

| Specialty/Organic Cereal Producers | 25% |

| Major Grain & Ingredient Processors | 15% |

| National Food Distributors | 15% |

| Online Grocery Retailers | 10% |

Primary research forms the cornerstone of our market estimation, accounting for 70-80% (typically 75%) of our overall research effort. This involves conducting in-depth, structured interviews and surveys with key opinion leaders, industry experts, and stakeholders across the cold cereal food value chain. Our objective is to gather first-hand intelligence, validate secondary findings, and uncover nuanced market dynamics often missed by quantitative data alone. Participant selection is meticulous, ensuring representation across various regions and market segments.

Key participants in our primary research interviews include:

Company Types:

Job Titles/Stakeholders:

Complementing our primary efforts, secondary research constitutes 20-30% (typically 25%) of our data collection. This phase involves a comprehensive review of existing market intelligence, industry reports, company filings, and statistical databases. Our secondary research is updated up to the date of purchase, ensuring the most current market information is integrated.

Key sources for secondary research include:

This robust secondary analysis helps in understanding the competitive landscape, market trends, technological advancements, and regulatory frameworks impacting the cold cereal market.

Our market sizing and forecasting methodologies employ a rigorous combination of top-down and bottom-up approaches, further strengthened by multi-level data triangulation. This ensures that market estimates are consistent, reliable, and reflect real-world dynamics from multiple perspectives.

Top-Down Approach: Global or regional market sizes are estimated using macroeconomic indicators, demographic trends, and overall food consumption patterns, then disaggregated down to specific product types, ingredients, flavors, and distribution channels.

Bottom-Up Approach: This method involves aggregating market size estimates from granular levels. Key metrics and variables used for bottom-up calculation in the cold cereal market include:

Data Triangulation: Outputs from both top-down and bottom-up approaches are cross-validated with primary interview data, historical market trends, and expert insights to resolve discrepancies and refine estimates. Advanced statistical and econometric models (e.g., regression analysis, time-series forecasting) are utilized to project future market growth.

Our commitment to data integrity is paramount. We guarantee an estimated data accuracy level of 85-90%. This high level of accuracy is achieved through several layers of validation:

The Cold Cereal Food market is valued at $47.99 billion in 2025. It is projected to expand at a Compound Annual Growth Rate (CAGR) of 4.1% from the base year 2025.

Innovation in the Cold Cereal Food market focuses on ingredient diversification, such as new multigrain or organic formulations, and processing advancements to enhance texture and shelf-life. Companies explore fortified cereals and plant-based ingredients to meet evolving consumer demands.

Demand for Cold Cereal Food is primarily driven by household consumers across various demographics seeking convenient and quick breakfast options. Growth is also observed among health-conscious individuals opting for organic or specialized ingredient types.

International trade in Cold Cereal Food is influenced by regional production capabilities and consumer preferences, leading to significant export-import flows between major economic blocs. Leading companies like Kellanova and General Mills maintain global supply chains to serve diverse markets.

Emerging substitutes for Cold Cereal Food include convenient breakfast alternatives like protein bars, yogurt, and ready-to-drink meal replacements. Innovations in on-the-go breakfast solutions present a competitive landscape for traditional cereal products.

The Cold Cereal Food market is segmented by Product Type (e.g., Flaked, Granola), Ingredient Type (e.g., Wheat-Based, Oat-Based), Nature (Conventional, Organic), Flavor, and Distribution Channel. Supermarkets & Hypermarkets remain a dominant distribution channel.