Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Corn Flake Market: Trends Driving Growth & 2033 Outlook

Corn Flake

Corn Flake Market: Trends Driving Growth & 2033 Outlook

Corn Flake by Application (Online Sales, Offline Sales), by Types (Organic Corn Flakes, Conventional Corn Flakes), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 7, 2026|Base Year : 2025|Pages : 97

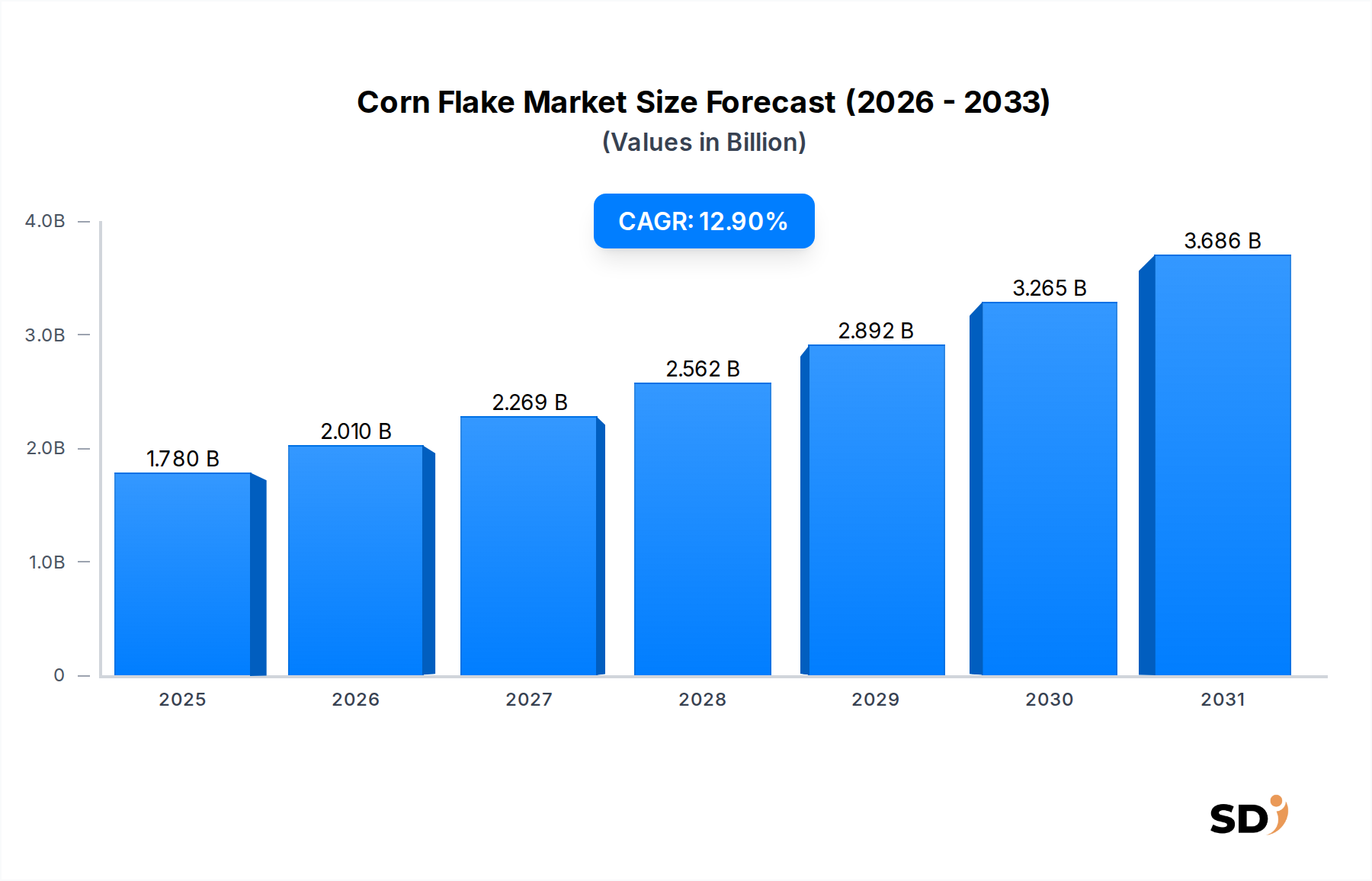

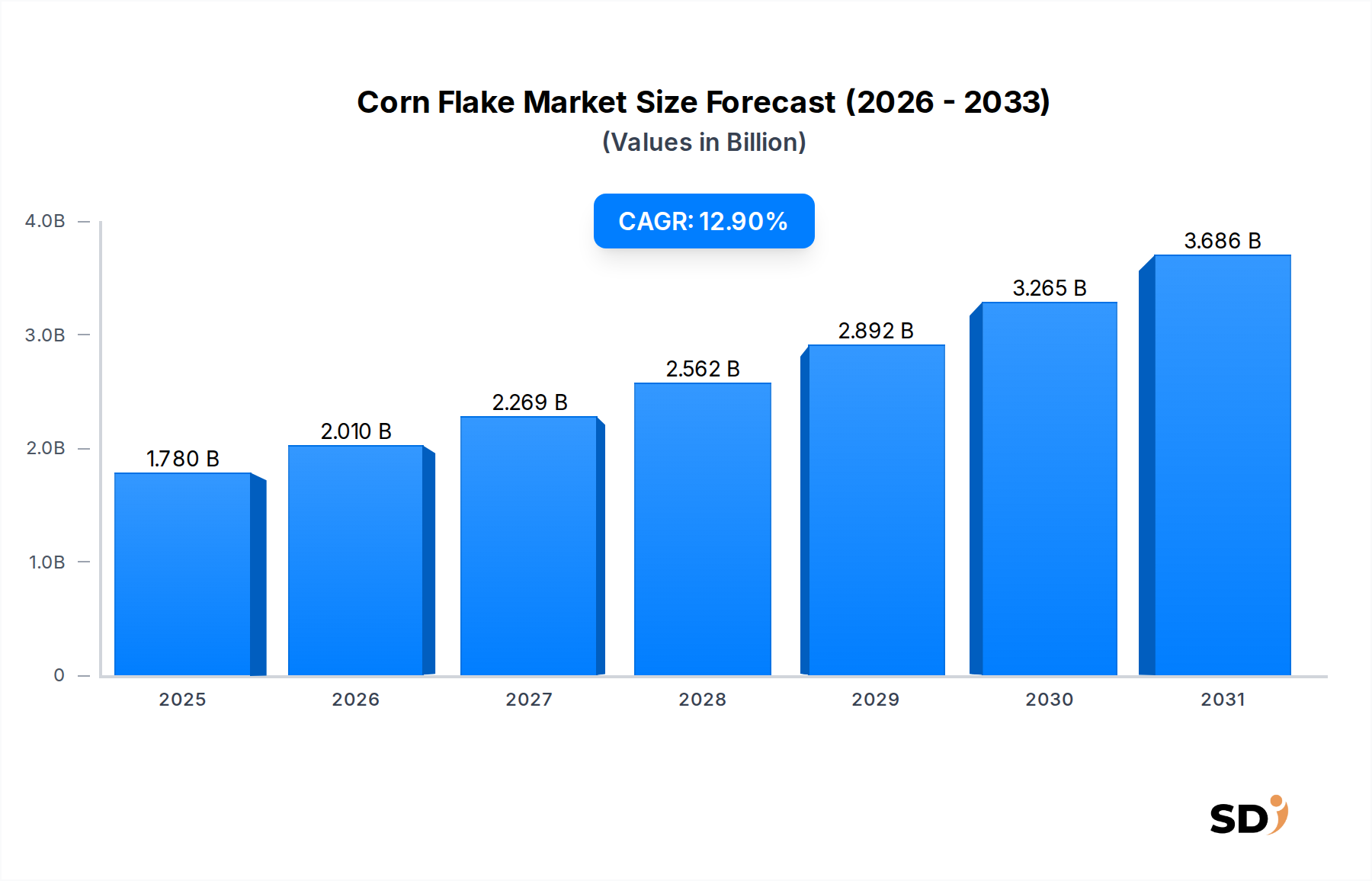

The global Corn Flake Market exhibited a valuation of $1.78 billion in 2024, and is projected to expand significantly at a robust Compound Annual Growth Rate (CAGR) of 12.9% over the forecast period. This substantial growth is primarily fueled by evolving consumer preferences towards convenient and ready-to-eat breakfast options, coupled with an increasing awareness regarding the nutritional benefits of fortified cereals. The market's trajectory is also bolstered by aggressive marketing strategies from key players and the continuous introduction of new flavors and variants catering to diverse palates.

Corn Flake Market Size (In Billion)

4.0B

3.0B

2.0B

1.0B

0

1.780 B

2025

2.010 B

2026

2.269 B

2027

2.562 B

2028

2.892 B

2029

3.265 B

2030

3.686 B

2031

Macro tailwinds such as rapid urbanization, changing dietary habits, and the rising disposable incomes in emerging economies are pivotal in accelerating market expansion. The increasing demand for a quick and nutritious start to the day, especially among working professionals and children, positions corn flakes as a staple breakfast item. Furthermore, the penetration of organized retail and the burgeoning e-commerce sector are enhancing product accessibility, contributing to higher sales volumes. The Online Food Retail Market has become a critical channel, enabling wider reach and consumer convenience, particularly in metropolitan areas. Innovations in packaging, which extend shelf life and offer single-serve options, also play a crucial role in attracting modern consumers. The Breakfast Cereal Market as a whole is experiencing innovation, with corn flakes maintaining a prominent position due to their versatility and perceived health benefits. Looking forward, the Corn Flake Market is expected to witness sustained growth, driven by product diversification, strategic partnerships, and geographic expansion into untapped regions. The integration of functional ingredients and a focus on sustainable sourcing are also emerging as key trends, poised to shape the market's future landscape and maintain its aggressive growth trajectory.

Dominant Conventional Corn Flakes Segment in the Corn Flake Market

The Conventional Corn Flakes segment currently holds the dominant share within the Corn Flake Market, primarily due to its widespread availability, established consumer base, and competitive pricing strategy. This segment encompasses standard corn flake products that do not carry specific organic certifications or cater to specialized dietary needs like gluten-free. Its dominance is rooted in decades of strong brand presence and extensive distribution networks, particularly through offline retail channels such as supermarkets, hypermarkets, and convenience stores, which represent a significant portion of the Packaged Food Market. The familiarity and affordability of conventional corn flakes make them a go-to choice for a broad demographic, including budget-conscious consumers and large families.

Major players like Kellogg Company and Nestlé have long championed conventional corn flakes, investing heavily in marketing and product development to maintain their market leadership. These companies leverage economies of scale in raw material sourcing, such as corn and Corn Starch Market supplies, and efficient Food Processing Equipment Market operations to keep production costs low, allowing for attractive price points. While the Organic Food Market and Gluten-Free Food Market are experiencing rapid growth, their combined share still lags behind that of conventional variants due to higher production costs and a more niche consumer base. The accessibility of conventional corn flakes across diverse socioeconomic strata, particularly in developing regions where price sensitivity is higher, further solidifies its leading position. The segment also benefits from a long history of consumer trust and consistent quality. Although the Organic Corn Flakes segment is growing faster due to increasing health consciousness and demand for natural products, Conventional Corn Flakes are expected to maintain their majority share throughout the forecast period. This is largely due to continued innovation in fortification (vitamins, minerals), flavor enhancements, and packaging design, ensuring they remain relevant and appealing to the mass market while offering a reliable and economical breakfast solution. Strategic promotions and expanded reach into tier-2 and tier-3 cities in emerging markets will also contribute to sustaining the dominance of conventional offerings.

Strategic Growth Drivers & Constraints in the Corn Flake Market

The Corn Flake Market's expansion is underpinned by several strategic drivers, primarily the burgeoning demand for Convenience Food Market products. With increasingly busy lifestyles globally, consumers are prioritizing ready-to-eat breakfast options, driving consistent demand for corn flakes. Data indicates that over 70% of urban households in developed economies consume breakfast cereals regularly due to time constraints. Additionally, rising health consciousness and the demand for fortified foods are significant drivers. Many manufacturers are enriching corn flakes with essential vitamins and minerals, addressing nutritional gaps and appealing to health-aware consumers. This trend is evident in a 15% year-over-year increase in product launches featuring nutritional claims over the past three years. The expansion of retail infrastructure, especially in emerging markets, further enhances product accessibility. The proliferation of supermarkets, hypermarkets, and the robust growth of the Online Food Retail Market contribute to wider product reach, translating to a 10-15% annual increase in distribution points across Asia Pacific.

Conversely, the market faces notable constraints. Volatility in raw material prices, particularly corn, sugar, and packaging materials, presents a significant challenge. Fluctuations in the global Corn Starch Market can directly impact production costs and, consequently, profit margins. For instance, a 20% surge in corn prices can elevate manufacturing costs by 5-7%. Intense competition from alternative breakfast options, such as oats, muesli, breakfast bars, and traditional breakfast foods, also constrains market growth. Consumers have a wide array of choices, and aggressive marketing by competitors can divert market share. The entry of private label brands offering similar products at lower price points further intensifies competition and exerts downward pressure on average selling prices. Moreover, the Breakfast Cereal Market is subject to stringent food safety regulations and evolving dietary guidelines, requiring continuous investment in research and development to ensure compliance and maintain consumer trust.

Competitive Ecosystem of the Corn Flake Market

The Corn Flake Market is characterized by a mix of well-established multinational corporations and emerging regional players, all vying for market share through product innovation, strategic acquisitions, and extensive distribution networks. The competitive landscape is dynamic, with companies focusing on expanding their product portfolios to include organic, gluten-free, and fortified variants to cater to diverse consumer preferences.

Kellogg Company: A global leader in the Breakfast Cereal Market, Kellogg Company has a dominant presence in the Corn Flake Market, leveraging its iconic brand recognition and vast distribution network to maintain its market leadership and continually innovate with new flavors and nutritional profiles.

Bagrrys: An Indian brand, Bagrrys focuses on health-conscious consumers, offering a range of breakfast cereals including corn flakes, with an emphasis on natural ingredients and nutritional value, expanding its footprint in the Asia Pacific region.

Nestlé: A diversified food and beverage giant, Nestlé competes in the Corn Flake Market with its own line of cereals, often emphasizing convenience and fortified options, backed by its global brand strength and extensive retail presence.

Patanjali: An Indian consumer goods company, Patanjali has entered the market with an emphasis on Ayurvedic principles and natural ingredients, appealing to consumers seeking traditional and health-oriented food products.

Barbara's Bakery: Known for its natural and organic products, Barbara's Bakery offers corn flakes that cater to the Organic Food Market and health-conscious consumers, with a focus on simple, wholesome ingredients and non-GMO certifications.

Erewhon: Specializing in organic and natural foods, Erewhon provides premium corn flake options that align with the growing demand for clean-label and minimally processed breakfast cereals.

Dr. Schär: A leading brand in the Gluten-Free Food Market, Dr. Schär offers specialized gluten-free corn flakes, catering to consumers with celiac disease or gluten sensitivities, expanding the market's reach to specific dietary needs.

Consenza: Another prominent player in the gluten-free segment, Consenza provides a range of gluten-free corn flakes, addressing the increasing demand for allergen-friendly breakfast solutions with a focus on taste and quality.

Recent Developments & Milestones in the Corn Flake Market

Recent developments in the Corn Flake Market highlight a strategic shift towards product diversification, sustainable practices, and enhanced consumer engagement to capitalize on evolving dietary trends and expand market reach.

May 2026: A leading player launched a new line of corn flakes fortified with probiotics and additional dietary fiber, targeting the growing segment of consumers focused on gut health and digestive wellness, signaling a move beyond basic nutritional fortification.

February 2026: Several manufacturers initiated partnerships with sustainable agriculture programs to source corn from farms employing environmentally friendly practices, responding to increasing consumer demand for transparency and eco-conscious Packaged Food Market products.

November 2025: A major regional brand expanded its distribution network by securing significant shelf space in leading hypermarket chains across Southeast Asia, aiming to capture a larger share of the rapidly growing Breakfast Cereal Market in the region.

August 2025: Innovative packaging solutions, including recyclable and compostable materials, were introduced by key players for their corn flake products, demonstrating a commitment to reducing environmental footprint and appealing to eco-conscious consumers.

April 2025: A prominent brand in the Gluten-Free Food Market category unveiled a new marketing campaign emphasizing the benefits of a gluten-free lifestyle, alongside new flavor variants for its gluten-free corn flakes, aiming to broaden its appeal beyond specific dietary restrictions.

January 2025: The market saw an increase in mergers and acquisitions activity among smaller, specialized brands focusing on Organic Food Market products, as larger conglomerates sought to integrate niche health-focused portfolios into their mainstream offerings.

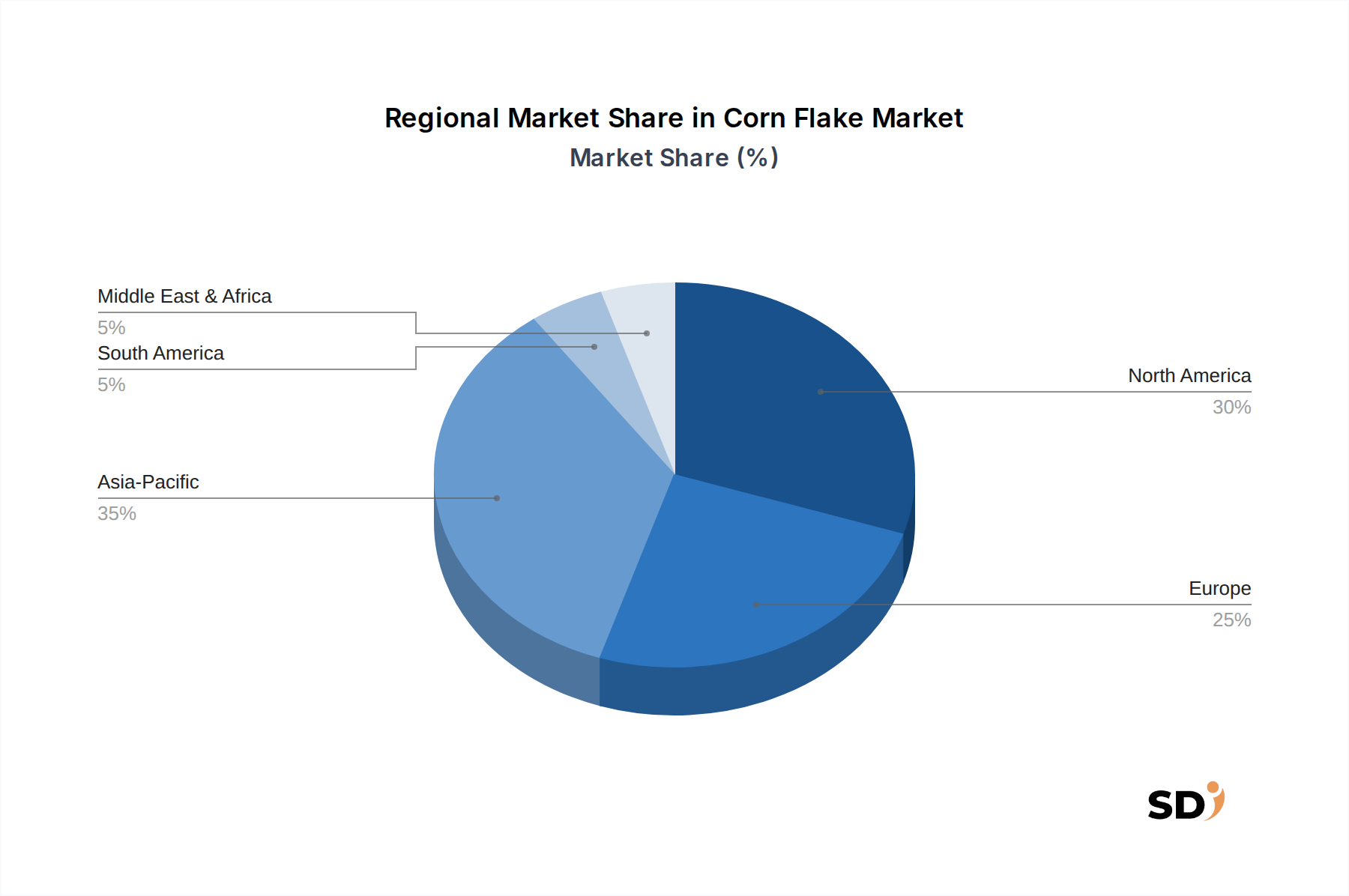

Regional Market Breakdown for the Corn Flake Market

The global Corn Flake Market demonstrates varied growth dynamics across key regions, influenced by consumer preferences, economic development, and cultural dietary habits. Asia Pacific currently represents the fastest-growing region, driven by rapid urbanization, increasing disposable incomes, and the growing adoption of Western breakfast habits. Countries like China and India are experiencing significant demand, with a regional CAGR projected to exceed 15.0% over the forecast period, primarily due to expanding distribution channels and aggressive marketing by international players. The rising awareness regarding health benefits and the convenience factor of Packaged Food Market items, especially among the young population, are key demand drivers in this region.

North America, while a mature market, holds a substantial revenue share in the Corn Flake Market, propelled by established brand loyalty and continuous product innovation, particularly in the Gluten-Free Food Market and Organic Food Market segments. The region's consumers, highly attuned to health trends, are consistently driving demand for fortified and specialized corn flake variants. Europe also commands a significant market share, characterized by a preference for premium and organic breakfast cereals. Countries such as the UK and Germany are leading contributors, with strong emphasis on product quality and sustainable sourcing. The demand driver here is primarily consumer demand for natural ingredients and ethical production, coupled with convenient breakfast solutions.

The Middle East & Africa (MEA) region is emerging as a promising market, albeit with a smaller current share, exhibiting a robust growth trajectory fueled by increasing Westernization of diets and a burgeoning youth population. The expansion of modern retail formats and Online Food Retail Market penetration are making corn flakes more accessible across countries like the UAE and Saudi Arabia. Latin America also contributes to the global market, with Brazil and Mexico being key markets. The primary demand driver in Latin America is the growing middle class and the increasing adoption of convenient, ready-to-eat foods as lifestyles evolve. While North America and Europe remain foundational, Asia Pacific is undeniably the engine of future growth for the Corn Flake Market.

Customer Segmentation & Buying Behavior in the Corn Flake Market

Customer segmentation in the Corn Flake Market is increasingly nuanced, reflecting a divergence in consumer priorities across various demographics. The primary segments include: traditional family households, which prioritize value and convenience; health-conscious individuals, who seek fortified, organic, or gluten-free options; and children, for whom taste and appealing packaging are key drivers. Price sensitivity remains a significant factor for a large portion of the market, particularly in developing economies, where conventional corn flakes are preferred due to their affordability. However, a growing segment is willing to pay a premium for products that align with specific dietary needs or ethical considerations, such as the Organic Food Market or Gluten-Free Food Market consumers.

Purchasing criteria have shifted from mere sustenance to include nutritional value, ingredient transparency, and brand reputation. Consumers are actively scrutinizing labels for sugar content, artificial additives, and allergen information. Procurement channels have also evolved; while offline sales through supermarkets and hypermarkets remain dominant, the Online Food Retail Market has witnessed substantial growth, particularly post-pandemic. This channel appeals to consumers seeking convenience, home delivery, and wider product selection. Notably, there's a shift towards personalized nutrition, with some buyers showing preference for brands that offer customization or cater to niche dietary requirements. Loyalty programs and subscription models are also influencing buying behaviors, particularly within the digital space. The increasing influence of social media and health influencers plays a role in shaping preferences, leading to cyclical demand shifts towards specific product attributes or brands.

Pricing Dynamics & Margin Pressure in the Corn Flake Market

Pricing dynamics in the Corn Flake Market are complex, influenced by a confluence of raw material costs, competitive intensity, brand equity, and consumer demand elasticity. The average selling price (ASP) of corn flakes varies significantly between conventional, organic, and specialty (e.g., gluten-free) variants. Conventional corn flakes typically command lower ASPs due to economies of scale in production and fierce competition. However, the Organic Food Market and Gluten-Free Food Market segments exhibit higher ASPs, reflecting the premium associated with specialized ingredients and production processes. Raw material costs, predominantly corn, sugar, and packaging materials, exert substantial margin pressure. Fluctuations in the global Corn Starch Market or sugar commodity prices directly impact manufacturers' cost of goods sold (COGS). For example, a 10% increase in corn prices can lead to a 3-5% reduction in gross margins for standard products if price increases cannot be passed directly to consumers.

Margin structures across the value chain are segmented. Manufacturers typically operate with moderate to high gross margins, which are then compressed by significant investments in marketing, distribution, and research & development. Retailers, particularly large supermarket chains and the Online Food Retail Market platforms, often negotiate favorable terms, leading to thinner margins for manufacturers at the wholesale level. Private label brands, offering similar products at a 15-20% lower ASP, intensify competitive intensity and exert downward pressure on branded product pricing. Key cost levers include optimizing the Food Processing Equipment Market for efficiency, strategic sourcing of raw materials to mitigate commodity price volatility, and streamlining logistics. The proliferation of promotional activities and discounts, particularly during holiday seasons or to clear inventory, further impacts pricing power and overall profitability, often leading to a challenging environment for maintaining consistent margins in the Breakfast Cereal Market.

Corn Flake Segmentation

1. Application

1.1. Online Sales

1.2. Offline Sales

2. Types

2.1. Organic Corn Flakes

2.2. Conventional Corn Flakes

Corn Flake Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Corn Flake REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 12.9% from 2020-2034

Segmentation

By Application

Online Sales

Offline Sales

By Types

Organic Corn Flakes

Conventional Corn Flakes

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Online Sales

5.1.2. Offline Sales

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Organic Corn Flakes

5.2.2. Conventional Corn Flakes

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Online Sales

6.1.2. Offline Sales

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Organic Corn Flakes

6.2.2. Conventional Corn Flakes

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Online Sales

7.1.2. Offline Sales

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Organic Corn Flakes

7.2.2. Conventional Corn Flakes

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Online Sales

8.1.2. Offline Sales

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Organic Corn Flakes

8.2.2. Conventional Corn Flakes

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Online Sales

9.1.2. Offline Sales

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Organic Corn Flakes

9.2.2. Conventional Corn Flakes

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Online Sales

10.1.2. Offline Sales

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Organic Corn Flakes

10.2.2. Conventional Corn Flakes

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Kellogg Company

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Bagrrys

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Nestlé

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Patanjali

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Barbara's Bakery

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Erewhon

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Dr. Schär

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Consenza

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Application 2025 & 2033

Figure 4: Volume (K), by Application 2025 & 2033

Figure 5: Revenue Share (%), by Application 2025 & 2033

Figure 6: Volume Share (%), by Application 2025 & 2033

Figure 7: Revenue (billion), by Types 2025 & 2033

Figure 8: Volume (K), by Types 2025 & 2033

Figure 9: Revenue Share (%), by Types 2025 & 2033

Figure 10: Volume Share (%), by Types 2025 & 2033

Figure 11: Revenue (billion), by Country 2025 & 2033

Figure 12: Volume (K), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Volume Share (%), by Country 2025 & 2033

Figure 15: Revenue (billion), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (billion), by Types 2025 & 2033

Figure 20: Volume (K), by Types 2025 & 2033

Figure 21: Revenue Share (%), by Types 2025 & 2033

Figure 22: Volume Share (%), by Types 2025 & 2033

Figure 23: Revenue (billion), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (billion), by Application 2025 & 2033

Figure 28: Volume (K), by Application 2025 & 2033

Figure 29: Revenue Share (%), by Application 2025 & 2033

Figure 30: Volume Share (%), by Application 2025 & 2033

Figure 31: Revenue (billion), by Types 2025 & 2033

Figure 32: Volume (K), by Types 2025 & 2033

Figure 33: Revenue Share (%), by Types 2025 & 2033

Figure 34: Volume Share (%), by Types 2025 & 2033

Figure 35: Revenue (billion), by Country 2025 & 2033

Figure 36: Volume (K), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Volume Share (%), by Country 2025 & 2033

Figure 39: Revenue (billion), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (billion), by Types 2025 & 2033

Figure 44: Volume (K), by Types 2025 & 2033

Figure 45: Revenue Share (%), by Types 2025 & 2033

Figure 46: Volume Share (%), by Types 2025 & 2033

Figure 47: Revenue (billion), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (billion), by Application 2025 & 2033

Figure 52: Volume (K), by Application 2025 & 2033

Figure 53: Revenue Share (%), by Application 2025 & 2033

Figure 54: Volume Share (%), by Application 2025 & 2033

Figure 55: Revenue (billion), by Types 2025 & 2033

Figure 56: Volume (K), by Types 2025 & 2033

Figure 57: Revenue Share (%), by Types 2025 & 2033

Figure 58: Volume Share (%), by Types 2025 & 2033

Figure 59: Revenue (billion), by Country 2025 & 2033

Figure 60: Volume (K), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

Figure 62: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Application 2020 & 2033

Table 2: Volume K Forecast, by Application 2020 & 2033

Table 3: Revenue billion Forecast, by Types 2020 & 2033

Table 4: Volume K Forecast, by Types 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Volume K Forecast, by Region 2020 & 2033

Table 7: Revenue billion Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue billion Forecast, by Types 2020 & 2033

Table 10: Volume K Forecast, by Types 2020 & 2033

Table 11: Revenue billion Forecast, by Country 2020 & 2033

Table 12: Volume K Forecast, by Country 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Volume (K) Forecast, by Application 2020 & 2033

Table 15: Revenue (billion) Forecast, by Application 2020 & 2033

Table 16: Volume (K) Forecast, by Application 2020 & 2033

Table 17: Revenue (billion) Forecast, by Application 2020 & 2033

Table 18: Volume (K) Forecast, by Application 2020 & 2033

Table 19: Revenue billion Forecast, by Application 2020 & 2033

Table 20: Volume K Forecast, by Application 2020 & 2033

Table 21: Revenue billion Forecast, by Types 2020 & 2033

Table 22: Volume K Forecast, by Types 2020 & 2033

Table 23: Revenue billion Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue billion Forecast, by Application 2020 & 2033

Table 32: Volume K Forecast, by Application 2020 & 2033

Table 33: Revenue billion Forecast, by Types 2020 & 2033

Table 34: Volume K Forecast, by Types 2020 & 2033

Table 35: Revenue billion Forecast, by Country 2020 & 2033

Table 36: Volume K Forecast, by Country 2020 & 2033

Table 37: Revenue (billion) Forecast, by Application 2020 & 2033

Table 38: Volume (K) Forecast, by Application 2020 & 2033

Table 39: Revenue (billion) Forecast, by Application 2020 & 2033

Table 40: Volume (K) Forecast, by Application 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Volume (K) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Volume (K) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Volume (K) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue billion Forecast, by Application 2020 & 2033

Table 56: Volume K Forecast, by Application 2020 & 2033

Table 57: Revenue billion Forecast, by Types 2020 & 2033

Table 58: Volume K Forecast, by Types 2020 & 2033

Table 59: Revenue billion Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (billion) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (billion) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (billion) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (billion) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue billion Forecast, by Application 2020 & 2033

Table 74: Volume K Forecast, by Application 2020 & 2033

Table 75: Revenue billion Forecast, by Types 2020 & 2033

Table 76: Volume K Forecast, by Types 2020 & 2033

Table 77: Revenue billion Forecast, by Country 2020 & 2033

Table 78: Volume K Forecast, by Country 2020 & 2033

Table 79: Revenue (billion) Forecast, by Application 2020 & 2033

Table 80: Volume (K) Forecast, by Application 2020 & 2033

Table 81: Revenue (billion) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue (billion) Forecast, by Application 2020 & 2033

Table 84: Volume (K) Forecast, by Application 2020 & 2033

Table 85: Revenue (billion) Forecast, by Application 2020 & 2033

Table 86: Volume (K) Forecast, by Application 2020 & 2033

Table 87: Revenue (billion) Forecast, by Application 2020 & 2033

Table 88: Volume (K) Forecast, by Application 2020 & 2033

Table 89: Revenue (billion) Forecast, by Application 2020 & 2033

Table 90: Volume (K) Forecast, by Application 2020 & 2033

Table 91: Revenue (billion) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology forms the cornerstone of our market estimations, contributing approximately 75% of the total research effort. This robust approach ensures a granular understanding of market dynamics, competitive landscapes, and emerging trends directly from industry participants. We engage with a diverse set of stakeholders across the value chain through structured interviews, telephonic surveys, and validated questionnaires. This direct interaction allows us to gather qualitative insights and quantitatively validate secondary data points, ensuring a comprehensive and current market perspective. The report is updated up to the date of purchase, reflecting the latest market intelligence derived from ongoing primary interactions.

Secondary research accounts for approximately 25% of our overall methodology, providing foundational data, market landscapes, and validation points for our primary findings. This phase involves extensive data mining from credible and authoritative sources, prioritizing governmental, organizational, and industry-specific publications over general market research reports. Our approach to secondary data collection includes, but is not limited to, the following:

Financial Databases: Leveraging premium subscription databases such as Bloomberg, Factiva, Hoovers, and PitchBook for company financials, investment trends, and competitive intelligence.

Government & Regulatory Bodies: Accessing official statistics, food consumption data, trade policies, and health guidelines from national and international government agencies.

Examples include the U.S. Department of Agriculture (USDA) (nass.usda.gov), Eurostat (ec.europa.eu/eurostat) for agricultural production and consumption data.

Regulatory insights from the Food and Drug Administration (FDA) (FDA.gov) in North America, and the European Food Safety Authority (EFSA) (EFSA.europa.eu) for food safety standards in Europe.

Industry Associations & Trade Publications: Reviewing reports, newsletters, and statistical data published by relevant trade associations to understand industry trends, consumption patterns, and technological advancements.

Key associations include the Codex Alimentarius Commission (fao.org/codex) for international food standards and the Organic Trade Association (ota.com) for organic product market insights.

Company Annual Reports & Investor Presentations: Analyzing publicly available financial statements, annual reports, and investor presentations of key market players to gather sales figures, strategic initiatives, and segment performance.

Academic Research & White Papers: Consulting peer-reviewed journals and academic studies for deep dives into consumer behavior, nutritional trends, and processing technologies related to breakfast cereals.

Demand Modeling & Market Estimation

Our market estimation framework employs a rigorous combination of top-down and bottom-up methodologies, complemented by multi-level data triangulation, to ensure the highest possible accuracy. The market sizing for "Corn Flake by Application, by Types, by Region" is derived through a systematic process:

Bottom-Up Approach: This involves aggregating specific segment data points. For the Corn Flake market, key variables considered include:

Regional Per Capita Cereal Consumption (kg/year): Derived from national food balance sheets and household consumption surveys.

Average Retail Price per Kilogram of Corn Flakes (USD/kg): Collected through retail audits and e-commerce price aggregators, segmented by type (organic/conventional) and region.

Number of Households by Income Bracket: Utilized to understand purchasing power and penetration of premium (organic) vs. conventional products.

E-commerce Penetration Rate for Groceries: Essential for estimating the online sales application segment across different regions.

Top-Down Approach: This approach starts with the broader global or regional breakfast cereal market size and progressively narrows down to the specific corn flake segment, further bifurcating by type and application. Macroeconomic indicators, population demographics, urbanization trends, and disposable income growth rates are integrated into this model.

Data Triangulation: All market figures are subjected to multi-level data triangulation. This involves cross-referencing estimates derived from various sources (primary interviews, secondary data, internal databases, and statistical models) and methodologies (top-down, bottom-up). Any discrepancies are critically analyzed and resolved through further expert consultation and data verification.

Data Accuracy & Quality Check

Our commitment to data integrity ensures an estimated data accuracy level of 85-90%. This high level of precision is maintained through a meticulous quality check process that spans the entire research lifecycle. Each data point, whether qualitative insight or quantitative metric, undergoes rigorous validation against multiple independent sources. A dedicated team of analysts scrutinizes the consistency, reliability, and relevance of collected information. Furthermore, market forecasts are developed using advanced statistical models, incorporating historical growth patterns, economic indicators, and projected consumer trends. These models are continuously refined and stress-tested with various sensitivity analyses to account for potential market volatilities and unforeseen disruptors, ensuring the robustness and foresight of our projections from 2026 to 2034.

Frequently Asked Questions

1. Who are the key competitors in the global Corn Flake market?

The global Corn Flake market features major players like Kellogg Company, Nestlé, and Patanjali. The competitive landscape includes both established international brands and regional manufacturers such as Bagrrys and Barbara's Bakery.

2. What are the primary demand drivers for Corn Flake products?

Demand for Corn Flake products is primarily driven by direct consumer consumption as a breakfast cereal. Segmentation includes both online and offline sales channels, reflecting diverse consumer purchasing habits and retail accessibility.

3. Which region exhibits the highest growth potential for Corn Flakes?

Asia Pacific is anticipated to be a region with high growth potential, driven by rising disposable incomes and changing dietary preferences. Emerging opportunities also exist within developing economies in South America and the Middle East & Africa as product awareness increases.

4. What is the projected market size and growth rate for Corn Flakes by 2033?

The Corn Flake market was valued at $1.78 billion in 2024 and is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.9%. This growth trajectory suggests a significant increase in market valuation by 2033.

5. What raw materials are crucial for Corn Flake production?

The primary raw material for Corn Flake production is corn. Supply chain considerations involve sourcing quality corn, processing, and distribution networks for both conventional and organic variants, impacting overall production costs and availability.

6. How have post-pandemic consumer trends impacted the Corn Flake market?

Post-pandemic, there has been a sustained focus on health and convenience, benefiting the breakfast cereal category. The market has observed structural shifts towards increased online sales adoption and a growing interest in organic product types like Organic Corn Flakes.