Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Digital Accessibility Software: $1.25B Market Outlook by 2034

Digital Accessibility Software

Digital Accessibility Software: $1.25B Market Outlook by 2034

Digital Accessibility Software by Application (Large Enterprises, SMEs), by Types (Color Contrast Checker Software, Website Accessibility Software), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 11, 2026|Base Year : 2025|Pages : 87

Key Insights into Digital Accessibility Software Market

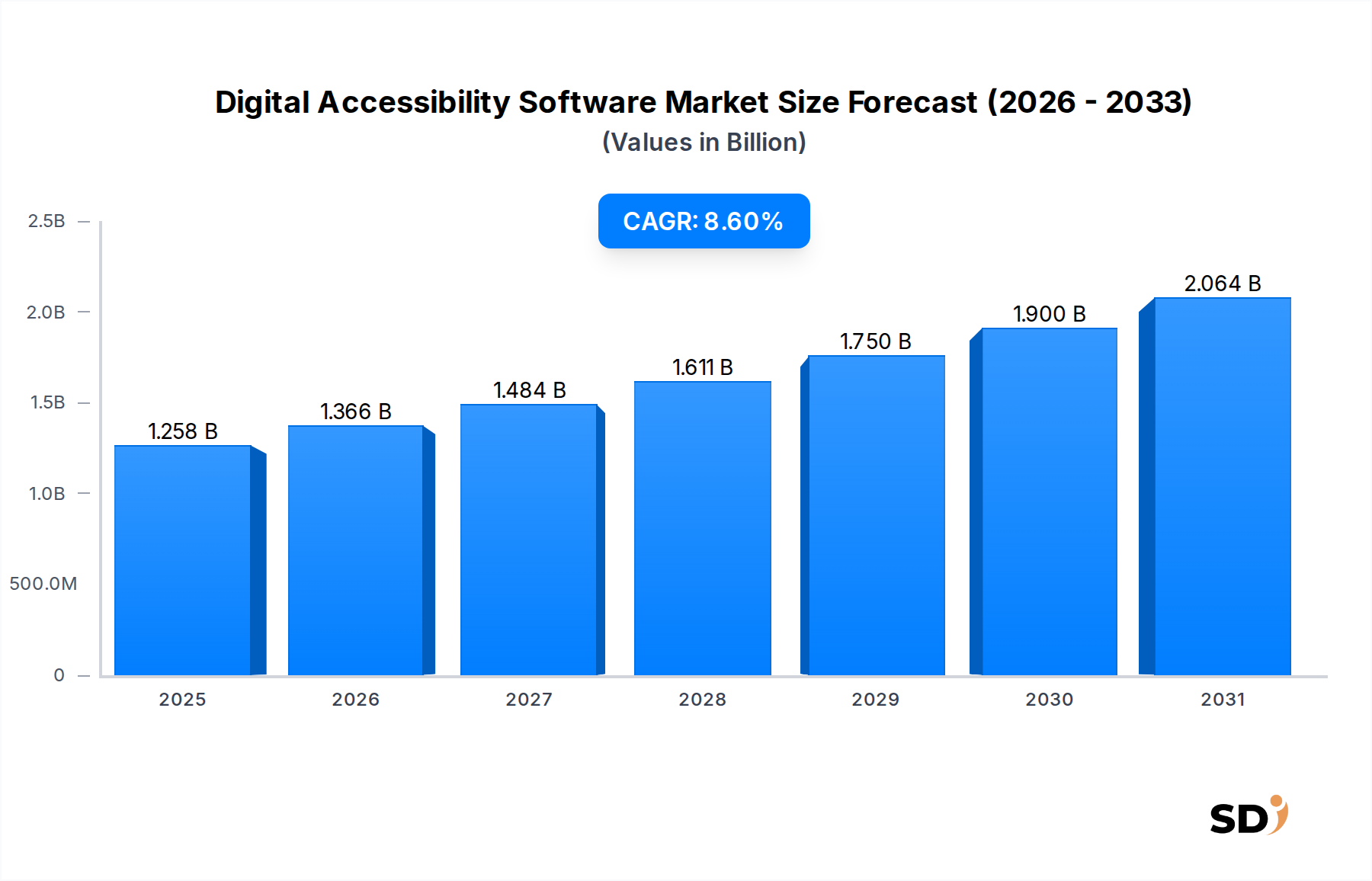

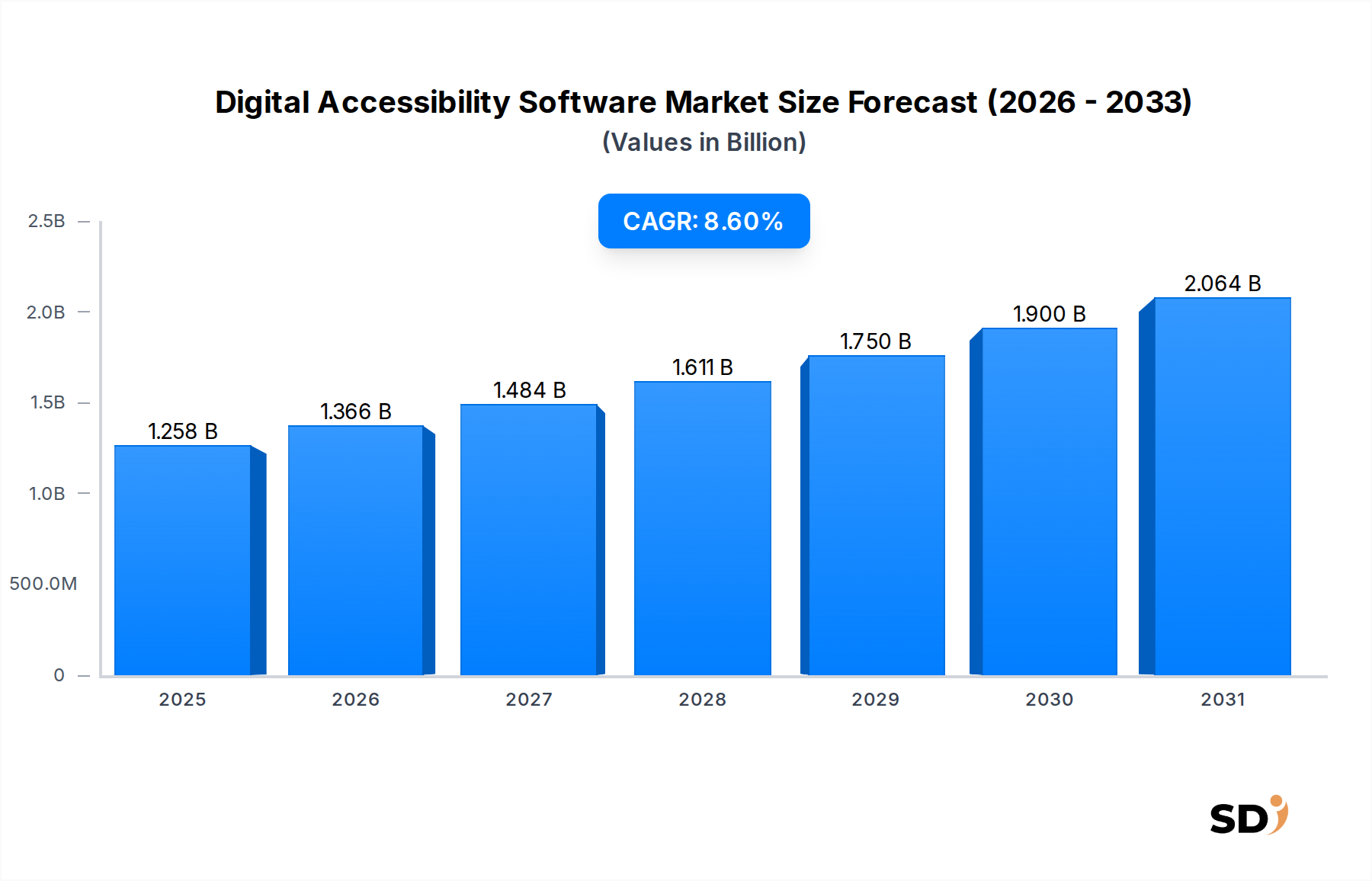

The Digital Accessibility Software Market is poised for substantial expansion, projected to reach a valuation of $1258 million by 2034, demonstrating a robust Compound Annual Growth Rate (CAGR) of 8.6%. This growth trajectory is fundamentally driven by a confluence of stringent regulatory mandates, escalating societal demand for digital inclusion, and rapid technological advancements, particularly in artificial intelligence and machine learning. Enterprises globally are increasingly prioritizing digital accessibility not merely as a compliance obligation but as a strategic imperative to expand market reach and enhance brand reputation. The evolving legislative landscape, exemplified by updates to standards like WCAG (Web Content Accessibility Guidelines) and regional acts such as the Americans with Disabilities Act (ADA) and the European Accessibility Act (EAA), creates a foundational demand for sophisticated Digital Accessibility Software Market solutions.

Digital Accessibility Software Market Size (In Billion)

2.5B

2.0B

1.5B

1.0B

500.0M

0

1.258 B

2025

1.366 B

2026

1.484 B

2027

1.611 B

2028

1.750 B

2029

1.900 B

2030

2.064 B

2031

Macro tailwinds, including the accelerated Digital Transformation Market across industries and the pervasive shift towards remote work models, further amplify the need for inclusive digital experiences. The inherent global nature of online platforms necessitates solutions that cater to a diverse user base, encompassing individuals with visual, auditory, cognitive, and motor impairments. Furthermore, the increasing adoption of cloud-based delivery models, underpinning the Software as a Service (SaaS) Market, provides scalability and flexibility for businesses of all sizes to implement and manage accessibility initiatives efficiently. Innovations in areas such as automated accessibility testing, AI-powered remediation tools, and real-time user feedback mechanisms are continually enhancing the efficacy and scope of available software, positioning the Digital Accessibility Software Market for sustained, long-term growth. The focus remains on not only identifying accessibility barriers but also providing actionable insights and automated corrections to foster genuinely inclusive digital environments.

Website Accessibility Software Segment in Digital Accessibility Software Market

The Website Accessibility Software Market segment currently holds a dominant share within the broader Digital Accessibility Software Market, primarily driven by the universal need for web-based content and applications to be accessible to all users, including those with disabilities. This segment encompasses a range of solutions designed to identify, report, and remediate accessibility issues on websites and web applications, ensuring compliance with international standards such as WCAG 2.1 and various national regulations. Its dominance stems from the critical role websites play as primary touchpoints for businesses, governments, and educational institutions in interacting with their target audiences. Any failure to comply with accessibility standards not only risks legal penalties but also alienates a significant portion of the population, impacting potential revenue and brand perception.

Key players in the Website Accessibility Software Market include prominent names like Siteimprove, UserWay, Level Access, and accessiBe, each offering varied approaches from automated overlays to comprehensive auditing and remediation platforms. The continuous evolution of web technologies, coupled with the dynamic nature of website content, necessitates ongoing monitoring and updates, thereby ensuring a sustained demand for these software solutions. Furthermore, the increasing complexity of modern websites, often integrated with a vast array of third-party plugins and dynamic content, requires sophisticated tools capable of accurately assessing and correcting accessibility flaws. The integration capabilities of these software platforms with various Content Management System (CMS) Market solutions, e-commerce platforms, and development environments are crucial for seamless implementation and ongoing maintenance, making them an indispensable component of the digital infrastructure. As organizations continue to expand their digital footprints and enhance user engagement through online channels, the imperative to ensure web accessibility will only intensify, solidifying the Website Accessibility Software Market's leading position within the Digital Accessibility Software Market and driving continuous innovation in automated testing, AI-driven remediation, and personalized user experiences. This segment’s growth is further fueled by the widespread understanding that an accessible website not only serves a social good but also improves SEO, expands customer base, and mitigates legal risks.

Regulatory Compliance and Innovation Driving Digital Accessibility Software Market

The Digital Accessibility Software Market's robust expansion is primarily fueled by two critical factors: escalating regulatory pressures and continuous technological innovation. Regulatory compliance stands as a significant driver, with various global and regional mandates compelling organizations to ensure their digital assets are accessible. For instance, the European Accessibility Act (EAA), effective June 2025, will directly impact a broad range of products and services, forcing companies operating within the EU to adopt compliant solutions or face penalties. Similarly, in the United States, interpretations of the Americans with Disabilities Act (ADA) continue to drive lawsuits related to inaccessible websites and digital platforms, creating a strong impetus for investment in Digital Accessibility Software Market tools to mitigate legal risk. These regulations ensure a baseline demand and continuously push for higher standards, directly translating into increased adoption rates for accessibility software.

Complementing regulatory mandates, technological innovation, particularly within the Artificial Intelligence (AI) Software Market, is a potent accelerator. Advanced AI and machine learning algorithms are revolutionizing accessibility solutions by enabling automated detection of complex accessibility issues, generating alternative text for images, and even dynamically adapting interfaces to suit individual user needs. This significantly reduces the manual effort and expertise previously required for accessibility audits and remediation. Furthermore, the enhanced integration capabilities of Digital Accessibility Software Market solutions with other essential business applications and the rise of the Assistive Technology Market provide a seamless and comprehensive approach to digital inclusion. These innovations not only simplify compliance but also open new avenues for personalized and effective accessibility experiences, moving beyond mere regulatory checkboxes to genuinely inclusive design. The convergence of these drivers creates a dynamic market environment where demand is both legally enforced and technologically empowered, fostering rapid evolution and adoption.

Competitive Ecosystem of Digital Accessibility Software Market

The Digital Accessibility Software Market features a diverse landscape of vendors offering a wide array of solutions, from comprehensive platforms to specialized tools. The competitive environment is characterized by continuous innovation aimed at simplifying compliance, enhancing user experience, and integrating seamlessly with existing digital infrastructures.

Siteimprove: A leading provider of comprehensive digital presence optimization software, offering robust solutions for web accessibility, analytics, SEO, and content quality management, enabling organizations to manage and optimize their digital assets from a unified platform.

ChromeLens: Focuses on browser-based accessibility testing and development tools, providing developers and content creators with immediate feedback on accessibility issues directly within their workflow, streamlining the remediation process.

Monsido: Specializes in website intelligence, offering tools for website governance, quality assurance, and accessibility. Their platform helps organizations maintain high standards for content, SEO, and legal compliance across their digital properties.

UserWay: Known for its AI-powered accessibility widget and auditing solutions, UserWay aims to simplify website accessibility for businesses through automated remediation and a user-friendly interface, reducing the complexity of compliance.

Level Access: A long-standing player offering comprehensive accessibility solutions, including audits, training, and software. They provide expert guidance and technology to help organizations achieve and maintain digital accessibility across all platforms.

DubBot: Delivers website quality assurance and accessibility monitoring, helping universities and public sector entities identify and resolve issues related to broken links, misspellings, and accessibility standards violations.

Crownpeak DQM: Provides digital quality management solutions, including accessibility monitoring and remediation, ensuring that digital content adheres to brand guidelines, legal requirements, and accessibility standards.

accessiBe: Offers an AI-powered, fully automated web accessibility solution designed to make websites compliant with ADA and WCAG, focusing on ease of integration and real-time accessibility adjustments.

Silktide: Specializes in website quality and accessibility auditing, providing tools that help organizations identify and fix issues across large and complex websites, ensuring a consistent and accessible user experience.

EqualWeb: Provides an AI-powered web accessibility solution that leverages machine learning to automatically scan, analyze, and remediate website accessibility issues, ensuring compliance with global standards.

UsableNet AQA: Offers a full suite of accessibility services, including automated and manual audits, user testing, and ongoing monitoring, providing comprehensive support for organizations navigating accessibility compliance.

WAVE API: A tool and API from WebAIM that helps developers and designers check web content for accessibility issues by providing visual feedback on potential problems directly on the web page, facilitating rapid identification and correction.

Recent Developments & Milestones in Digital Accessibility Software Market

The Digital Accessibility Software Market is dynamic, marked by continuous advancements and strategic collaborations aimed at enhancing inclusivity and compliance.

March 2024: Several leading accessibility software providers launched new AI-driven features, including enhanced image description generators and automated captioning services for video content, significantly improving the efficiency of content remediation.

February 2024: A major player in the Digital Accessibility Software Market announced a strategic partnership with a global Enterprise Software Market vendor to integrate accessibility checks directly into their enterprise resource planning (ERP) and customer relationship management (CRM) platforms, ensuring accessibility at the foundational software layer.

November 2023: A Series B funding round successfully closed for a specialized Color Contrast Checker Software Market developer, raising $30 million to further innovate automated design system integration and real-time accessibility feedback for designers.

September 2023: New regulatory guidelines for public sector websites in several European nations, aligning with the European Accessibility Act, led to a surge in demand for comprehensive Digital Accessibility Software Market solutions offering multi-language support and compliance reporting capabilities.

July 2023: An emerging vendor introduced a new Cloud Computing Market-based accessibility platform specifically tailored for Small and Medium-sized Enterprises (SMEs), offering tiered pricing and simplified deployment to broaden market penetration.

May 2023: Industry consortia published updated best practices for integrating Digital Accessibility Software Market tools within continuous integration/continuous delivery (CI/CD) pipelines, emphasizing a 'shift-left' approach to accessibility in software development.

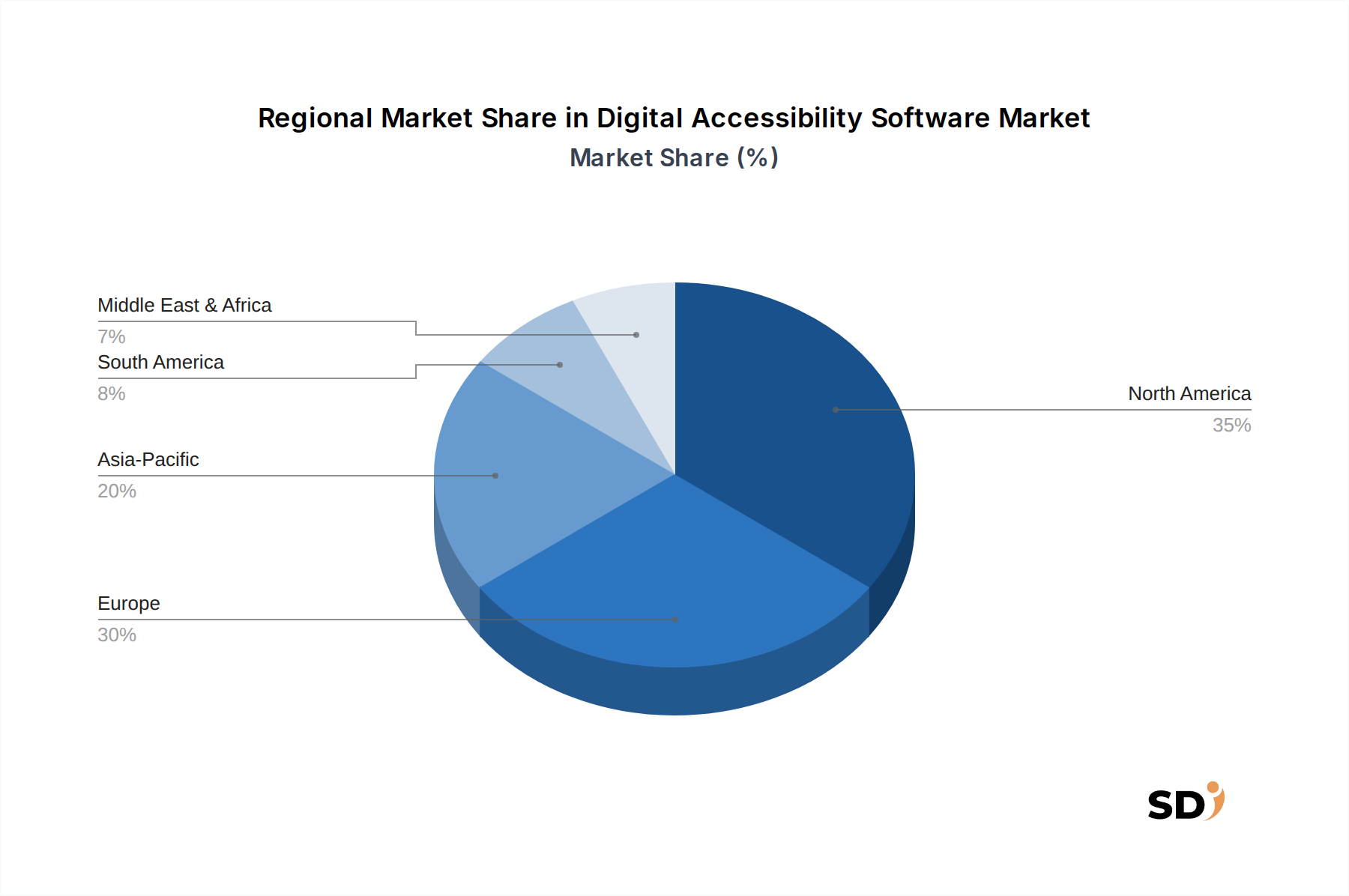

Regional Market Breakdown for Digital Accessibility Software Market

The Digital Accessibility Software Market exhibits diverse growth patterns and adoption rates across various global regions, driven by distinct regulatory landscapes, digital maturity, and economic conditions.

North America holds a significant revenue share in the Digital Accessibility Software Market, largely propelled by stringent legislation such as the Americans with Disabilities Act (ADA) and Section 508 of the Rehabilitation Act. The region, particularly the United States, is characterized by a high degree of digital adoption and a litigious environment that mandates robust accessibility solutions across public and private sectors. With an estimated regional CAGR of 7.9%, North America remains a mature yet expanding market, driven by continuous updates to digital platforms and increasing corporate emphasis on Diversity, Equity, and Inclusion (DEI) initiatives.

Europe represents another substantial market, fueled by the comprehensive European Accessibility Act (EAA), which mandates accessibility for a broad range of products and services. Countries like the United Kingdom, Germany, and France are at the forefront of adoption, with governmental bodies and large corporations leading the charge. Europe is expected to register a CAGR of 8.3%, with the primary demand driver being the harmonization of accessibility standards across member states and increasing public awareness of digital rights. The need for comprehensive solutions that integrate with the Enterprise Software Market is pronounced here.

Asia Pacific is projected to be the fastest-growing region in the Digital Accessibility Software Market, with an anticipated CAGR exceeding 9.5%. This rapid growth is attributed to surging digital transformation initiatives, increasing internet penetration, and a rising awareness of digital inclusion in populous nations like China, India, and Japan. While regulatory frameworks are still evolving in many parts of the region, the expanding digital economy and the growing consumer base are strong incentives for businesses to adopt accessibility software. The rising demand from the SME Software Market is particularly noticeable.

Latin America and Middle East & Africa are emerging markets, currently holding smaller shares but demonstrating promising growth potential. In Latin America, countries such as Brazil and Mexico are witnessing increased legislative efforts and a growing digital population. The Middle East & Africa region, particularly the GCC countries, is investing heavily in smart city initiatives and digital infrastructure, which inherently drives the need for accessibility solutions. The primary demand driver in these regions is nascent regulatory development coupled with increasing digital literacy and the expanding reach of global technology firms.

Investment & Funding Activity in Digital Accessibility Software Market

Investment and funding activity within the Digital Accessibility Software Market have seen a notable uptick over the past 2-3 years, reflecting the market's growing strategic importance and the imperative for innovation. Venture capital firms and private equity funds are increasingly targeting companies that offer scalable, AI-driven, and Cloud Computing Market-based solutions. A key trend observed is the acquisition of smaller, specialized accessibility tools by larger Enterprise Software Market players, aiming to integrate accessibility features directly into their core product offerings rather than relying solely on third-party integrations. This M&A activity underscores a shift towards embedding accessibility from the design phase, rather than treating it as an afterthought.

For example, late 2023 saw a significant Series C funding round for a company specializing in automated WCAG compliance testing, raising $50 million to expand its AI capabilities and global footprint. This highlights investor confidence in the growth potential of AI-powered solutions that can significantly reduce the cost and complexity of accessibility audits. Strategic partnerships are also prevalent, with accessibility software vendors collaborating with web development agencies, design studios, and digital marketing firms to offer comprehensive digital inclusion services. Sub-segments attracting the most capital include those focused on real-time remediation, AI-driven content analysis (especially for rich media), and platforms offering robust reporting and analytics for compliance. The drive to enhance the User Experience (UX) Software Market through accessibility is a strong motivator for these investments, positioning these solutions as critical components of broader digital transformation strategies.

Export, Trade Flow & Tariff Impact on Digital Accessibility Software Market

For the Digital Accessibility Software Market, traditional concepts of "export" and "tariff impact" are largely redefined by the nature of software, especially those delivered via the Software as a Service (SaaS) Market model. Instead of physical goods, the trade flows involve licenses, subscriptions, and intellectual property. Major exporting nations are typically those with advanced technological infrastructures and robust software development ecosystems, such as the United States, certain European nations (e.g., Ireland, Germany), and increasingly, Israel and India. These countries develop and provide accessibility software solutions to a global clientele, often leveraging cloud infrastructure for seamless delivery.

Importing nations are essentially any country where businesses and organizations require digital accessibility solutions. The "trade corridors" are predominantly digital, facilitated by global internet connectivity. Tariffs, in the conventional sense, have minimal direct impact on the cost of Digital Accessibility Software Market licenses. However, non-tariff barriers are highly significant. Data localization laws, such as GDPR in Europe or specific data residency requirements in China and Russia, can act as de facto barriers, necessitating vendors to host data centers within specific jurisdictions. This impacts cross-border volume by requiring additional infrastructure investment or limiting market access for some providers. Furthermore, varying national accessibility standards and certifications (e.g., Section 508 vs. EN 301 549) require software to be adaptable to multiple regulatory environments, adding complexity to market entry and cross-border service provision. Recent discussions around digital service taxes and cross-border data transfer regulations have introduced new layers of complexity, potentially impacting the operational costs and market strategies for global Digital Accessibility Software Market providers, though direct quantifiable impact on volume remains fluid.

Digital Accessibility Software Segmentation

1. Application

1.1. Large Enterprises

1.2. SMEs

2. Types

2.1. Color Contrast Checker Software

2.2. Website Accessibility Software

Digital Accessibility Software Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Digital Accessibility Software REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 8.6% from 2020-2034

Segmentation

By Application

Large Enterprises

SMEs

By Types

Color Contrast Checker Software

Website Accessibility Software

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Large Enterprises

5.1.2. SMEs

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Color Contrast Checker Software

5.2.2. Website Accessibility Software

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Large Enterprises

6.1.2. SMEs

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Color Contrast Checker Software

6.2.2. Website Accessibility Software

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Large Enterprises

7.1.2. SMEs

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Color Contrast Checker Software

7.2.2. Website Accessibility Software

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Large Enterprises

8.1.2. SMEs

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Color Contrast Checker Software

8.2.2. Website Accessibility Software

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Large Enterprises

9.1.2. SMEs

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Color Contrast Checker Software

9.2.2. Website Accessibility Software

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Large Enterprises

10.1.2. SMEs

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Color Contrast Checker Software

10.2.2. Website Accessibility Software

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Siteimprove

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. ChromeLens

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Monsido

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. UserWay

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Level Access

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. DubBot

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Crownpeak DQM

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. accessiBe

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Silktide

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. EqualWeb

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. UsableNet AQA

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. WAVE API

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Application 2025 & 2033

Figure 3: Revenue Share (%), by Application 2025 & 2033

Figure 4: Revenue (million), by Types 2025 & 2033

Figure 5: Revenue Share (%), by Types 2025 & 2033

Figure 6: Revenue (million), by Country 2025 & 2033

Figure 7: Revenue Share (%), by Country 2025 & 2033

Figure 8: Revenue (million), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (million), by Types 2025 & 2033

Figure 11: Revenue Share (%), by Types 2025 & 2033

Figure 12: Revenue (million), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (million), by Application 2025 & 2033

Figure 15: Revenue Share (%), by Application 2025 & 2033

Figure 16: Revenue (million), by Types 2025 & 2033

Figure 17: Revenue Share (%), by Types 2025 & 2033

Figure 18: Revenue (million), by Country 2025 & 2033

Figure 19: Revenue Share (%), by Country 2025 & 2033

Figure 20: Revenue (million), by Application 2025 & 2033

Figure 21: Revenue Share (%), by Application 2025 & 2033

Figure 22: Revenue (million), by Types 2025 & 2033

Figure 23: Revenue Share (%), by Types 2025 & 2033

Figure 24: Revenue (million), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (million), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (million), by Types 2025 & 2033

Figure 29: Revenue Share (%), by Types 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Revenue million Forecast, by Types 2020 & 2033

Table 3: Revenue million Forecast, by Region 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Types 2020 & 2033

Table 6: Revenue million Forecast, by Country 2020 & 2033

Table 7: Revenue (million) Forecast, by Application 2020 & 2033

Table 8: Revenue (million) Forecast, by Application 2020 & 2033

Table 9: Revenue (million) Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Application 2020 & 2033

Table 11: Revenue million Forecast, by Types 2020 & 2033

Table 12: Revenue million Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue (million) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Types 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue (million) Forecast, by Application 2020 & 2033

Table 23: Revenue (million) Forecast, by Application 2020 & 2033

Table 24: Revenue (million) Forecast, by Application 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Revenue (million) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue million Forecast, by Application 2020 & 2033

Table 29: Revenue million Forecast, by Types 2020 & 2033

Table 30: Revenue million Forecast, by Country 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue (million) Forecast, by Application 2020 & 2033

Table 37: Revenue million Forecast, by Application 2020 & 2033

Table 38: Revenue million Forecast, by Types 2020 & 2033

Table 39: Revenue million Forecast, by Country 2020 & 2033

Table 40: Revenue (million) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

The comprehensive methodology employed for the "Digital Accessibility Software Market" report ensures a robust and accurate market forecast from 2026 to 2034. Our approach integrates rigorous primary and secondary research techniques, sophisticated demand modeling, and multi-level data triangulation to deliver high-fidelity insights.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP of Product Management (Software Vendors)

30%

Chief Digital Officer (Large Enterprises)

25%

Accessibility Lead/Specialist

25%

Head of Software Development / CTO

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Digital Accessibility Software Vendors

35%

Large Enterprises (End-Users)

25%

Accessibility Consulting Firms

15%

Web Development/Design Agencies

15%

SMEs (End-Users)

10%

Primary Research

Primary research constitutes the cornerstone of our analysis, accounting for approximately 75% of the overall research effort. This phase involves extensive, in-depth interviews and discussions with key stakeholders across the digital accessibility software value chain. Our interview strategy is designed to capture qualitative and quantitative insights directly from industry experts, validating secondary data, and uncovering emerging trends and market dynamics specific to Digital Accessibility Software. Key participants include:

Company Types: Digital Accessibility Software Vendors, Web Development/Design Agencies, Accessibility Consulting Firms, Large Enterprise IT Departments, and SaaS Platform Providers (integrating accessibility features).

Stakeholders Interviewed: VP of Product Management (Digital Accessibility Software Vendors), Chief Digital Officer (Large Enterprises), Accessibility Lead/Specialist (Accessibility Consulting Firms, Enterprises), and Head of Software Development / CTO (Software Vendors, Web Development Agencies).

These discussions provide critical insights into product roadmaps, technology adoption rates, pricing strategies, competitive landscapes, regulatory compliance challenges, and end-user requirements across different applications (Large Enterprises, SMEs) and geographies.

Secondary Research & Industry Benchmarking

Secondary research contributes approximately 25% to our research methodology and serves as the foundational layer for market understanding and segmentation. This phase involves a comprehensive review of published information from credible sources, allowing for preliminary market sizing, identification of key players, and understanding of market drivers and restraints. Our sources include:

Proprietary and Subscription Databases: Financial databases such as Bloomberg, Factiva, Hoovers, and PitchBook are utilized to gather company financials, investment trends, and strategic developments.

Government & Regulatory Bodies: Official publications from government agencies (e.g., U.S. Department of Justice on ADA compliance [https://www.ada.gov/], European Union Accessibility Act guidelines) provide critical regulatory context and compliance drivers.

Industry Associations & Organizations: Reports and statistics from globally recognized bodies such as the World Wide Web Consortium (W3C) [https://www.w3.org/], International Association of Accessibility Professionals (IAAP) [https://www.accessibilityassociation.org/], and the European Disability Forum (EDF) [https://www.edf-feph.org/] offer valuable industry benchmarks, best practices, and technological standards (e.g., WCAG guidelines). We strictly avoid data from other market research websites to maintain originality and integrity.

This robust secondary research provides a holistic view of the market's historical performance, current landscape, and future growth potential.

Demand Modeling & Market Estimation

Our market estimation leverages a combination of top-down and bottom-up methodologies, complemented by multi-level data triangulation to ensure maximum accuracy.

Top-Down Approach: This involves analyzing macroeconomic factors, overall digital transformation trends, and total addressable market estimations for digital services, which are then cascaded down to specific market segments for digital accessibility software.

Bottom-Up Approach: This detailed approach builds the market size from the ground up by aggregating granular data points. Key metrics and variables used for bottom-up calculation include:

The estimated number of active websites and digital platforms across Large Enterprises and SMEs requiring accessibility compliance.

Average annual recurring revenue (ARR) or license fees for different digital accessibility software types (Color Contrast Checker Software, Website Accessibility Software) per user or per website/platform.

Penetration rates of digital accessibility software within the target enterprise segments (Large Enterprises, SMEs) across various geographies.

The impact of evolving compliance mandates and their regional adoption rates (e.g., WCAG 2.1 AA/AAA adoption).

Multi-level data triangulation involves cross-referencing findings from primary interviews with secondary data and both top-down and bottom-up market sizing models. This iterative process helps in reconciling discrepancies, refining assumptions, and strengthening the validity of our forecasts across all segments and regions (North America, South America, Europe, Middle East & Africa, Asia Pacific).

Data Accuracy & Quality Check

We are committed to delivering highly reliable market intelligence. Our rigorous quality control processes guarantee an estimated data accuracy level of 85-90%. Every data point, trend, and forecast undergoes multiple layers of validation by experienced analysts.

Furthermore, to ensure the utmost relevance, every report is updated dynamically up to the date of purchase, incorporating the latest industry developments, technological advancements, and shifts in the competitive landscape. This commitment ensures that our clients receive the most current and actionable insights for their strategic decision-making.

Frequently Asked Questions

1. What are the primary 'raw materials' for Digital Accessibility Software?

For software, primary inputs include skilled human capital (developers, UX designers), data for testing and AI models, and cloud infrastructure services. The supply chain focuses on talent acquisition, robust data privacy, and secure, reliable hosting platforms.

2. Which region leads the Digital Accessibility Software market, and why?

North America is projected to lead due to stringent regulatory frameworks like the ADA and Section 508. High digital adoption rates and a strong emphasis on corporate social responsibility also drive significant demand.

3. How are technological innovations impacting Digital Accessibility Software?

Innovations include AI and machine learning for automated accessibility testing and remediation, and improved integration with existing web development workflows. Advanced tools now offer real-time compliance monitoring and user-specific adaptive interfaces, enhancing usability for diverse needs.

4. What are the pricing trends for Digital Accessibility Software?

Pricing typically follows a SaaS subscription model, varying by feature set, usage volume, and enterprise size. Cost structures are dominated by R&D, continuous updates, and customer support, reflecting ongoing efforts to meet evolving accessibility standards.

5. How did the pandemic affect Digital Accessibility Software market growth?

The pandemic accelerated digital transformation across industries, increasing the necessity for accessible online platforms. This led to sustained growth, reinforcing the long-term structural shift towards mandatory digital inclusion and remote work accessibility solutions.

6. Which industries are the main end-users for Digital Accessibility Software?

Key end-user industries include large enterprises and SMEs across sectors like e-commerce, government, education, and healthcare. Downstream demand is driven by legal compliance requirements and a desire to expand user bases through inclusive digital experiences.