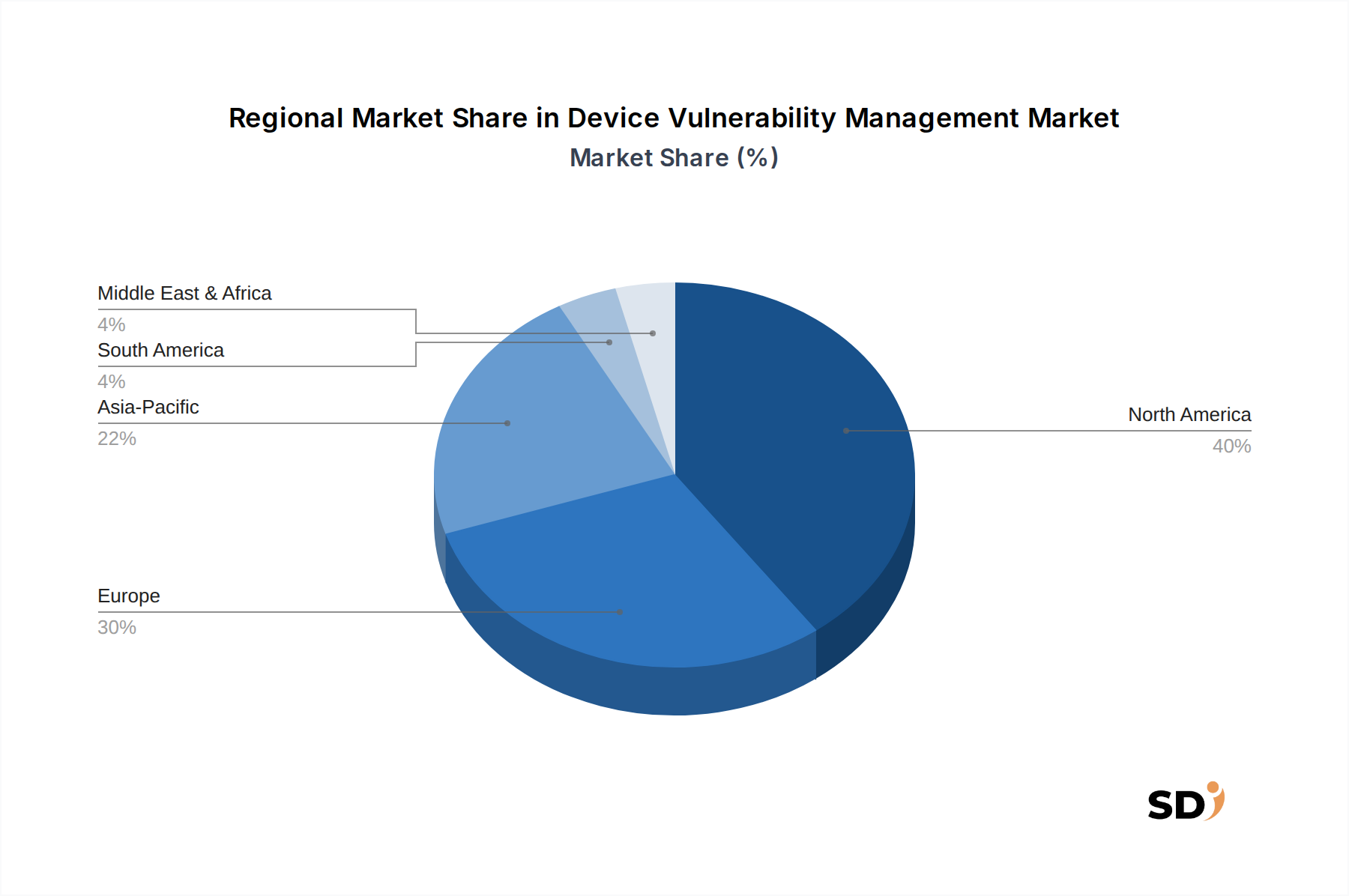

Regional Market Breakdown for Device Vulnerability Management Market

The Device Vulnerability Management Market exhibits distinct characteristics across key global regions, each driven by unique regulatory environments, technological adoption rates, and threat landscapes.

North America holds the largest revenue share in the Device Vulnerability Management Market, primarily due to the presence of a mature cybersecurity infrastructure, stringent regulatory compliance mandates (e.g., HIPAA, SOX, NIST), and a high concentration of large enterprises with complex IT environments. The region benefits from early adoption of advanced security technologies and significant investments in digital transformation initiatives. The market here is expected to continue its robust growth, supported by a strong innovation ecosystem and a proactive stance against escalating cyber threats. The demand for Endpoint Security Market solutions is particularly high in this region.

Europe represents a substantial segment of the market, driven by comprehensive data protection regulations such as GDPR and the NIS2 Directive, which compel organizations to implement robust vulnerability management practices. Countries like the UK, Germany, and France are at the forefront of adoption, with considerable investment in both solutions and Security Services Market offerings. While mature, the market continues to expand steadily as businesses modernize their IT infrastructure and address evolving compliance requirements. The need for Patch Management Software Market solutions is acutely felt across European industries.

Asia Pacific (APAC) is projected to be the fastest-growing region in the Device Vulnerability Management Market, exhibiting the highest CAGR. This rapid expansion is fueled by accelerated digitalization across countries like China, India, and Japan, increasing internet penetration, and the booming adoption of industrial IoT. The region faces a rapidly expanding threat landscape, prompting enterprises to allocate more resources towards cybersecurity. Government initiatives promoting digital economies and smart cities further drive the demand for device vulnerability management solutions, particularly those addressing the nuances of the Cloud Security Market and rapidly expanding IT infrastructures.

Middle East & Africa (MEA) and South America are emerging markets, currently holding smaller market shares but demonstrating promising growth potential. In MEA, regions like the GCC are investing heavily in digital infrastructure and smart initiatives, leading to increased awareness and adoption of cybersecurity measures. Similarly, in South America, growing digitalization and rising cybercrime rates are pushing organizations to adopt more proactive security strategies. Both regions are characterized by a growing appetite for managed security services, particularly within the SMB Cybersecurity Market, as businesses seek to enhance their security posture without significant in-house investments. Overall, while North America and Europe maintain leading positions, APAC's rapid ascent underscores the global imperative for comprehensive device vulnerability management.