1. Who are the leading companies in the Data Center Ethernet Switch market?

Cisco, Arista Networks, Dell, Juniper Networks, and Huawei are prominent players. These companies compete for market share in a sector valued at $17.78 billion by 2025.

+1 2315155523

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

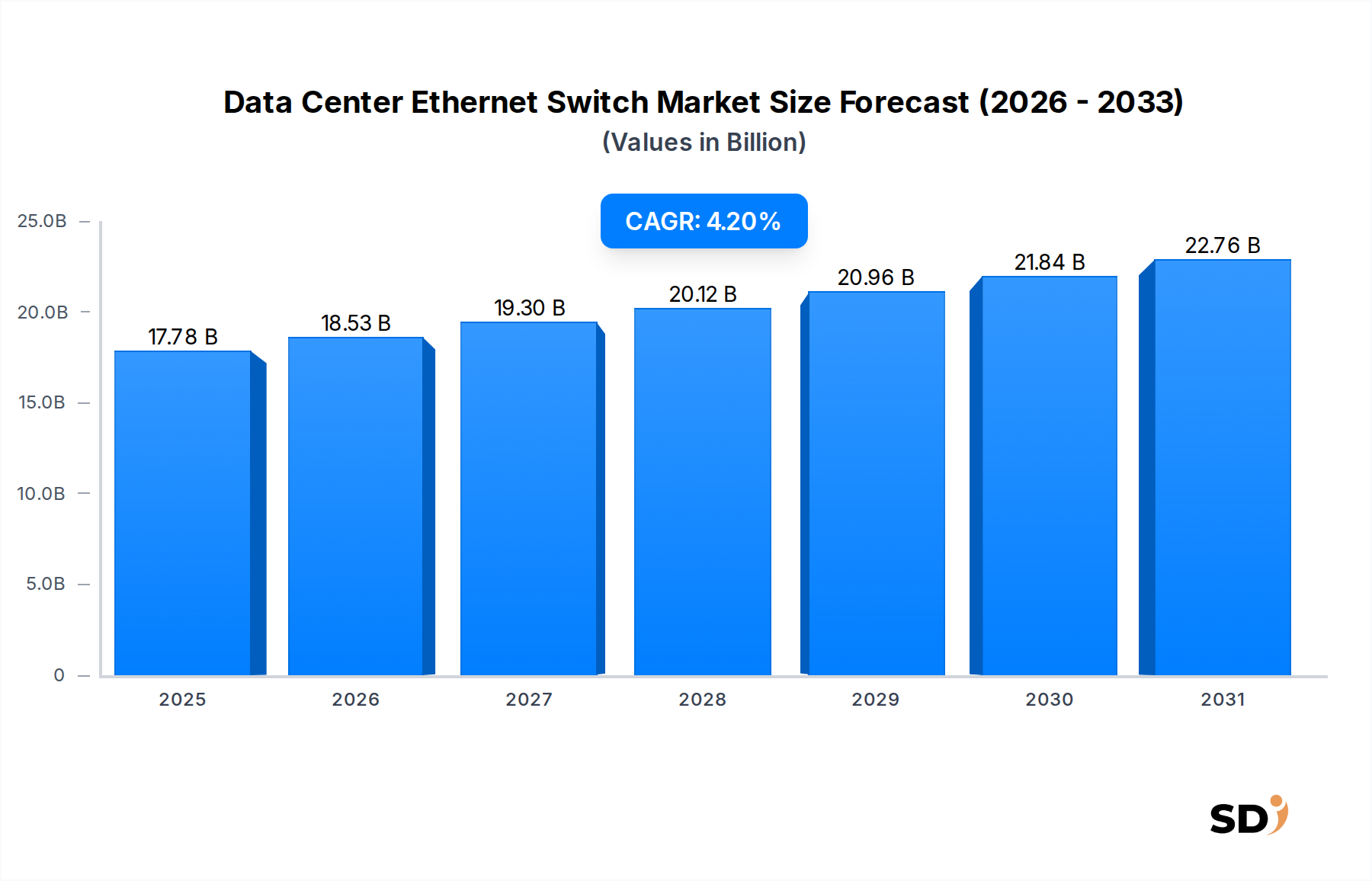

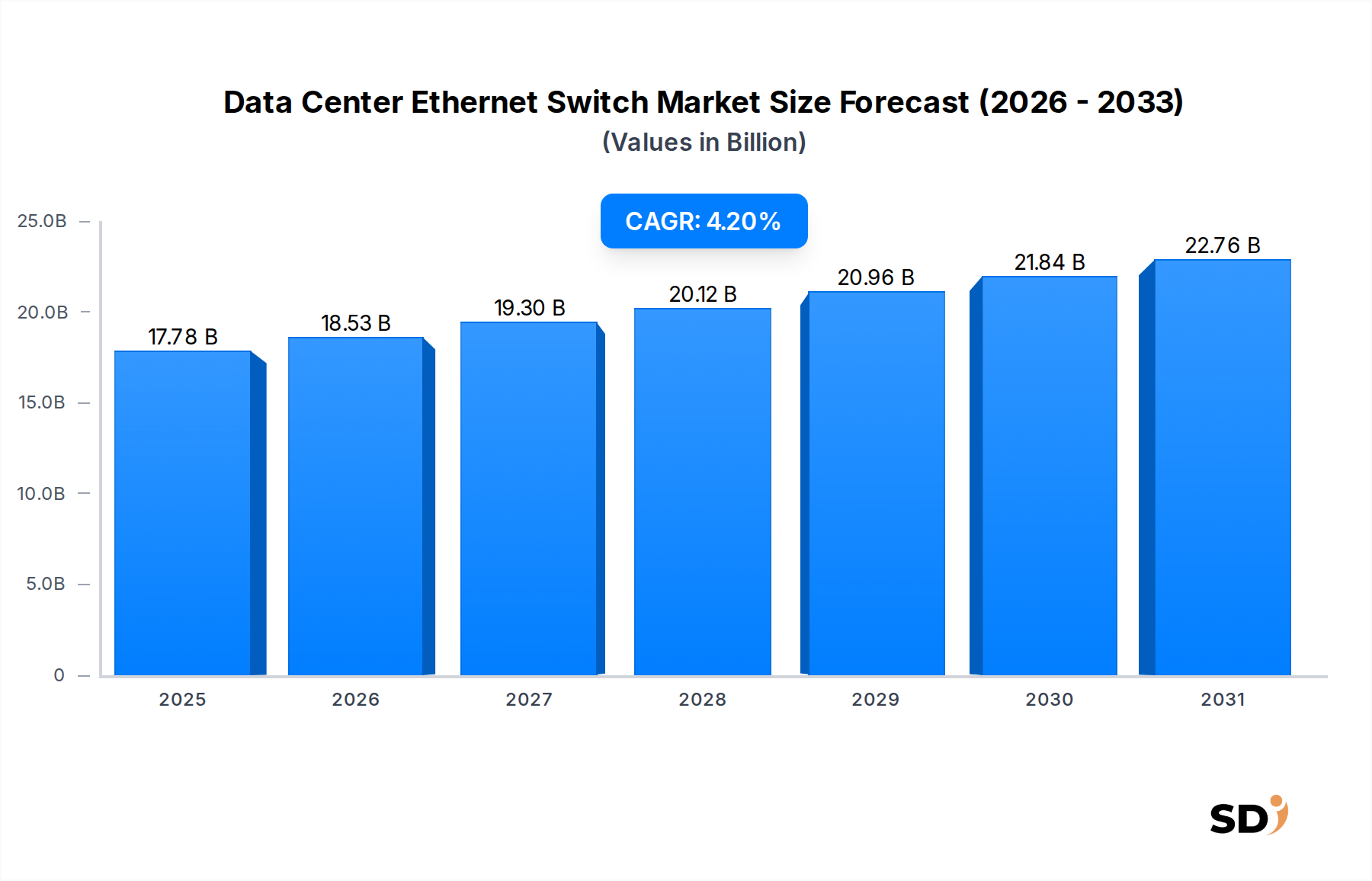

The Global Data Center Ethernet Switch Market, a critical component of modern digital infrastructure, was valued at approximately $17.78 billion in 2025. Projections indicate a robust expansion, with the market expected to reach an estimated $25.79 billion by 2034, advancing at a Compound Annual Growth Rate (CAGR) of 4.2% during the forecast period. This growth trajectory is fundamentally driven by the escalating demand for high-speed, low-latency data processing and transmission capabilities within data centers worldwide. Key demand drivers include the pervasive adoption of cloud computing, the explosion of data traffic fueled by emerging technologies like Artificial Intelligence (AI) and Machine Learning (ML), and the continuous digital transformation initiatives undertaken by enterprises across various sectors. The proliferation of hyperscale data centers, edge computing deployments, and the relentless need for greater network bandwidth are primary macro tailwinds. The market’s segmentation by type, encompassing 25 GbE, 100 GbE, 200/400 GbE, and other advanced speeds, highlights an ongoing transition towards higher throughput solutions to accommodate intensive workloads. Applications span critical sectors such as Internet services, government, telecommunications, and finance, each demanding resilient and performant networking infrastructure. The substantial expansion within the Cloud Data Center Market, for instance, directly correlates with the increased deployment of advanced Ethernet switches capable of handling multi-tenant environments and dynamic resource allocation. Similarly, the evolution of the Telecommunications Infrastructure Market, particularly with the rollout of 5G networks and associated edge computing paradigms, necessitates upgraded switching fabrics to manage distributed data loads efficiently. Geographically, while North America and Europe continue to be significant revenue contributors due to established digital ecosystems, the Asia Pacific region is poised for accelerated growth, propelled by rapid data center construction and digital initiatives. The competitive landscape is characterized by innovation in silicon, software-defined networking, and energy efficiency, as vendors strive to deliver scalable and sustainable solutions amidst evolving network architectures.

Within the Data Center Ethernet Switch Market, the 100 GbE segment currently holds a significant revenue share, representing a critical sweet spot for performance, cost-effectiveness, and widespread adoption. This dominance stems from its ability to meet the escalating bandwidth requirements of modern data centers, particularly those supporting hyperscale cloud environments, large enterprises, and internet service providers. The transition from lower speed interfaces, such as those found in the 25 GbE Ethernet Switch Market, to 100 GbE has been a defining trend over recent years, driven by the increasing density of virtual machines, containerized applications, and the general surge in east-west traffic within data center fabrics. Many organizations found 10 GbE insufficient for server uplinks and aggregate links, making 25 GbE and subsequently 100 GbE the logical progression for efficiency and scale. The maturity of the 100 GbE ecosystem, including a broad range of transceivers, cables, and switch ASICs, has contributed to its lower per-gigabit cost compared to newer, higher-speed alternatives. Key players such as Cisco, Arista Networks, and Juniper Networks have invested heavily in optimizing their 100 GbE product portfolios, offering robust, feature-rich switches that integrate with existing network architectures while providing a clear upgrade path. These offerings often include advanced telemetry, automation capabilities, and deep buffering, crucial for handling unpredictable traffic patterns in virtualized and cloud-native environments. While the market is increasingly seeing the emergence and adoption of solutions within the 400 GbE Ethernet Switch Market, especially in core and spine layers of hyperscale data centers, 100 GbE continues to dominate the leaf and access layers due to its balanced performance profile and established cost efficiency. The share of the 100 GbE segment is stabilizing as higher-speed technologies gain traction, but its entrenched position in numerous operational data centers globally ensures its continued significance throughout the forecast period. Its robust feature set and proven reliability make it the current workhorse for the majority of data center interconnects, facilitating the vast flow of digital information underpinning the global economy. This segment's enduring appeal lies in its optimal balance of high throughput, operational stability, and economic viability, making it a foundational element for scalable data center designs.

The Data Center Ethernet Switch Market is experiencing significant impetus from several critical factors, primarily centered around the exponential growth of data and the evolving demands of digital infrastructure. A principal driver is the relentless expansion of the Cloud Data Center Market. Hyperscale cloud providers are continuously building and expanding their global footprints to support a burgeoning array of services, from SaaS applications to AI training platforms. This expansion directly translates into a soaring demand for high-port-density, high-speed Ethernet switches capable of handling massive inter-server communication. For instance, the volume of data traffic within hyperscale data centers is projected to grow by double-digit percentages annually, mandating the deployment of 200/400 GbE switches to maintain operational efficiency and user experience. Another significant driver is the proliferation of Artificial Intelligence (AI) and Machine Learning (ML) workloads. These computationally intensive tasks require ultra-low latency and high-bandwidth networking to facilitate rapid data exchange between GPUs and other accelerators. The architecture of AI/ML clusters often necessitates specialized Ethernet switches that can support lossless communication and efficient congestion management, driving innovation and demand for advanced switch fabrics. Furthermore, the global rollout of 5G technology and the subsequent rise of edge computing are profoundly influencing the Telecommunications Infrastructure Market and, by extension, the demand for data center Ethernet switches. Edge data centers require compact, powerful, and reliable switches to process data closer to the source, reducing latency for applications such as autonomous vehicles, industrial IoT, and real-time streaming. This shift decentralizes data processing, creating new pockets of demand for robust switching solutions outside traditional centralized data centers. Finally, ongoing enterprise digital transformation initiatives, including the adoption of hybrid cloud strategies and the modernization of legacy IT infrastructure, continue to fuel investments in advanced Ethernet switches. Enterprises are upgrading their networks to support virtualized environments, software-defined networking, and enhanced security postures, all of which necessitate high-performance and agile switching hardware.

The Data Center Ethernet Switch Market is characterized by intense competition among a diverse set of global and regional players, driving continuous innovation in speed, density, power efficiency, and software capabilities. Each company vies for market share by leveraging distinct strengths in hardware design, software features, and ecosystem integration.

The Data Center Ethernet Switch Market is dynamic, with ongoing innovations and strategic moves shaping its future trajectory.

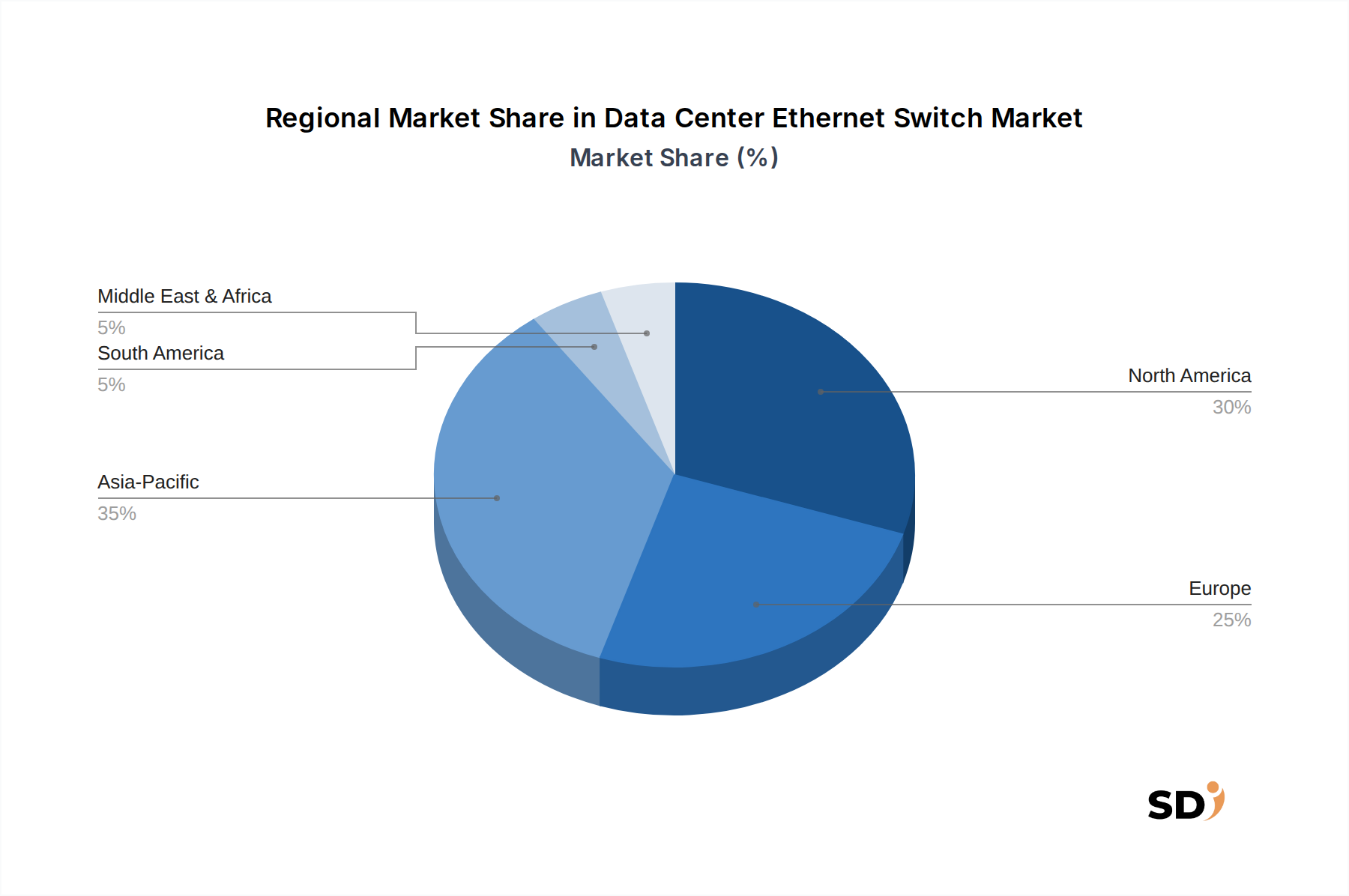

Geographically, the Data Center Ethernet Switch Market exhibits varied growth patterns and demand drivers across major regions. While detailed regional CAGR and revenue shares are dynamic, an analysis of the primary demand influencers provides a clear picture of the landscape.

North America continues to be a dominant market, largely due to the presence of hyperscale cloud providers (e.g., Google, Amazon, Microsoft) and a mature enterprise IT sector. This region is a leader in adopting advanced technologies like 400 GbE and is characterized by significant investment in AI/ML infrastructure. Demand is driven by the continuous expansion and modernization of existing data centers, as well as robust R&D in networking innovation. It is often an early adopter of new switching technologies, setting trends for global deployment.

Asia Pacific is recognized as the fastest-growing region in the Data Center Ethernet Switch Market. Nations like China, India, Japan, and South Korea are experiencing unprecedented growth in digital transformation, internet penetration, and mobile data consumption. This surge drives massive investments in new data center builds and the expansion of the Telecommunications Infrastructure Market, particularly for 5G deployments. The Cloud Data Center Market is also expanding rapidly across the region, fueling demand for high-density, energy-efficient switches. Government initiatives promoting digitalization further accelerate market growth.

Europe represents a mature yet steadily growing market. Demand is spurred by stringent data localization regulations, a strong focus on data privacy (e.g., GDPR), and increasing adoption of hybrid cloud strategies by enterprises. Countries like Germany, the UK, and France are investing in upgrading their data center infrastructure to meet escalating digital service demands. The emphasis on sustainable data center operations also drives demand for power-efficient Ethernet switches across the Network Equipment Market in this region.

Middle East & Africa (MEA), while smaller in absolute terms, is an emerging market demonstrating rapid growth. Countries within the GCC (e.g., UAE, Saudi Arabia) are making substantial investments in digital infrastructure, smart city initiatives, and economic diversification away from oil. This translates into new data center constructions and a growing need for advanced Ethernet switches to support nascent cloud services and robust telecommunications networks. Africa, in particular, is witnessing increasing internet penetration and mobile data usage, promising future growth opportunities for the Network Equipment Market.

The Data Center Ethernet Switch Market is at the forefront of technological innovation, driven by the insatiable demand for higher bandwidth, lower latency, and greater intelligence in network operations. Several disruptive emerging technologies are shaping the future landscape.

One pivotal area is Co-Packaged Optics (CPO) and its broader implication for silicon photonics. As Ethernet speeds push beyond 400 GbE towards 800 GbE and 1.6 TbE, traditional pluggable optical transceivers face limitations in power consumption, signal integrity, and port density. CPO integrates optical transceivers directly into the same package as the switch ASIC, drastically reducing electrical trace lengths and power consumption while enabling much higher port densities. R&D investments in CPO are substantial, led by major silicon vendors and cloud hyperscalers, with widespread adoption expected within the next 3-5 years for top-of-rack and spine switches in cutting-edge data centers. This innovation threatens incumbent discrete Optical Transceiver Market manufacturers in the long run but reinforces the position of integrated component suppliers and switch vendors capable of complex chip integration.

Another transformative technology is AI/ML Integration for Network Automation and Optimization. This involves embedding AI algorithms directly into network devices or leveraging AI-driven platforms for predictive analytics, anomaly detection, and automated network management. These intelligent networks can dynamically optimize traffic flows, identify security threats in real-time, and even self-heal, significantly reducing operational expenditure and improving network reliability. Adoption is already underway, particularly in hyperscale and large enterprise environments, with R&D focused on refining AI models for network telemetry and control. This trend reinforces incumbent vendors who can integrate sophisticated software capabilities with their hardware, while also creating opportunities for AI-focused networking startups.

Finally, Disaggregated Networking and Open Ethernet continues to gain traction. This approach separates network hardware (white-box switches) from network operating systems (NOS), allowing greater flexibility, choice, and often, lower cost. While not entirely new, its maturity and the emergence of robust open-source and commercial NOS options are making it more viable for a wider range of data centers. Adoption timelines vary; hyperscalers have been early adopters, while enterprises are cautiously exploring. This model threatens traditional vertically integrated business models but fosters innovation and competition, empowering network operators with greater control over their infrastructure. It leverages a robust ecosystem of ODMs and software developers, moving some value creation from proprietary hardware to open software and system integration.

The Data Center Ethernet Switch Market is intricately linked to global supply chains and trade flows, with significant manufacturing and consumption centers dictating patterns of export and import. Major trade corridors for these critical networking components primarily connect Asian manufacturing hubs with consumption markets in North America and Europe.

Leading exporting nations for raw components and finished switches include China, Taiwan, and other Southeast Asian countries, which serve as global manufacturing bases for semiconductor chips, PCBs, and assembled networking equipment. The United States, while a major consumer, also exports high-value intellectual property, design expertise, and specialized networking hardware, particularly to regions requiring advanced data center infrastructure. Key importing nations are generally those with developed digital economies and significant data center investments, such as the United States, Germany, the United Kingdom, Japan, and increasingly, emerging economies in Asia Pacific and the Middle East seeking to bolster their digital infrastructure.

Recent geopolitical tensions and trade policies have had a tangible impact on the Data Center Ethernet Switch Market. The US-China trade disputes, for instance, led to tariffs on a wide range of goods, including networking equipment and critical components like optical transceivers. These tariffs, which at their peak added 15-25% to the cost of certain imported goods, directly affected pricing strategies for vendors and increased procurement costs for data center operators. While some manufacturers absorbed these costs, others passed them on to customers, potentially slowing down infrastructure upgrades. Non-tariff barriers, such as export controls on specific technologies or security concerns related to certain vendors, have also influenced trade flows, prompting some regions to diversify their supply chains or favor domestic or allied-country suppliers within the Network Equipment Market.

In response to these challenges, there has been a noticeable trend towards supply chain de-risking and regionalization. Companies are exploring manufacturing in countries like Vietnam, India, or Mexico to mitigate tariff impacts and enhance resilience. This strategic shift aims to reduce reliance on single manufacturing geographies, although it often entails higher initial setup costs and necessitates new logistics infrastructure. The long-term impact of these trade dynamics could reshape the global manufacturing footprint for the Optical Transceiver Market and the broader Network Equipment Market, fostering greater regional self-sufficiency but potentially increasing overall costs due to reduced economies of scale.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Our robust primary research methodology forms the cornerstone of this report, accounting for 70-80% of the total research effort. This extensive engagement ensures real-time insights and validates secondary findings directly from industry experts. Our interviews are conducted globally across key regions to capture diverse perspectives and localized market dynamics.

Key Stakeholders Interviewed:

Target Companies for Primary Interviews:

The primary research process involves structured telephonic and in-person interviews, complemented by detailed questionnaires, enabling deep dives into market trends, technology adoption patterns, competitive landscape, pricing dynamics, and future growth projections.

| Stakeholder Role | Interview Share (%) |

|---|---|

| VP of Network Architecture/Engineering | 30% |

| Data Center Operations Manager | 25% |

| Head of Infrastructure Procurement | 25% |

| Principal Network Engineer | 20% |

| Company Type | Representation (%) |

|---|---|

| Ethernet Switch Manufacturers | 25% |

| Hyperscale Cloud Service Providers | 25% |

| Colocation Data Center Operators | 20% |

| Large Enterprise IT Departments | 15% |

| Network Infrastructure Integrators & VARs | 15% |

The remaining 20-30% of our research is dedicated to comprehensive secondary research and industry benchmarking, providing foundational data and corroborating primary findings. This rigorous approach involves the systematic review and analysis of a multitude of credible sources.

It is crucial to note that data from other market research websites is strictly excluded to maintain the originality and integrity of our findings.

Our market sizing and forecasting methodology employs a robust blend of top-down and bottom-up approaches, rigorously triangulated across multiple data points to ensure accuracy. This multi-level data triangulation considers various market facets, including value chain analysis, supply-side capacity, and demand-side consumption patterns.

Bottom-Up Market Sizing Variables:

Top-Down Validation: The bottom-up calculations are then validated against macroeconomic indicators, overall IT infrastructure spending trends, global data traffic growth, major vendor revenue reports for the data center networking segment, and regional economic forecasts. This dual approach provides a comprehensive and balanced market size estimate.

All market values are estimated in USD Million unless otherwise specified. The forecast period extends from 2026 to 2034, projecting market dynamics based on identified growth drivers, restraints, opportunities, and challenges across various applications, types, and geographies.

Our commitment to data integrity is paramount. We guarantee an estimated data accuracy level of 85-90% for all quantitative figures presented in this report. This high level of accuracy is achieved through a multi-stage validation process.

Furthermore, our reports are dynamic documents. Every report is meticulously updated up to the date of purchase, ensuring that clients receive the most current and relevant market intelligence, reflecting the latest industry developments and data points for the Data Center Ethernet Switch market.

Cisco, Arista Networks, Dell, Juniper Networks, and Huawei are prominent players. These companies compete for market share in a sector valued at $17.78 billion by 2025.

With a projected market size of $17.78 billion by 2025 and a 4.2% CAGR, significant investment potential exists. Focus areas include next-generation 200/400 GbE switches and solutions for Internet and Telecommunications applications.

Enterprises prioritize high-speed switches like 100 GbE and 200/400 GbE to support growing data demands and cloud adoption. Decisions are driven by scaling infrastructure for applications in finance and telecommunications.

The acceleration of digital transformation and remote work post-pandemic has intensified demand for robust data center infrastructure. This drives increased adoption of advanced Ethernet switches to handle expanded network traffic and cloud services.

Key application segments include Internet, Government, Telecommunications, and Finance. These sectors require high-performance networking to manage vast data volumes and critical operations efficiently.

The emergence of 200/400 GbE switches is a key disruptor, pushing higher performance and density. These advancements enable data centers to manage increasingly demanding workloads and future-proof their network architectures.