Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

CXL Memory Expander Controller: Market Growth & Data Analysis

CXL Memory Expander Controller

CXL Memory Expander Controller: Market Growth & Data Analysis

CXL Memory Expander Controller by Application (Computers, Data Centers, Artificial Intelligence, Others), by Types (DDR4, DDR5), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 8, 2026|Base Year : 2025|Pages : 92

Key Insights for CXL Memory Expander Controller Market

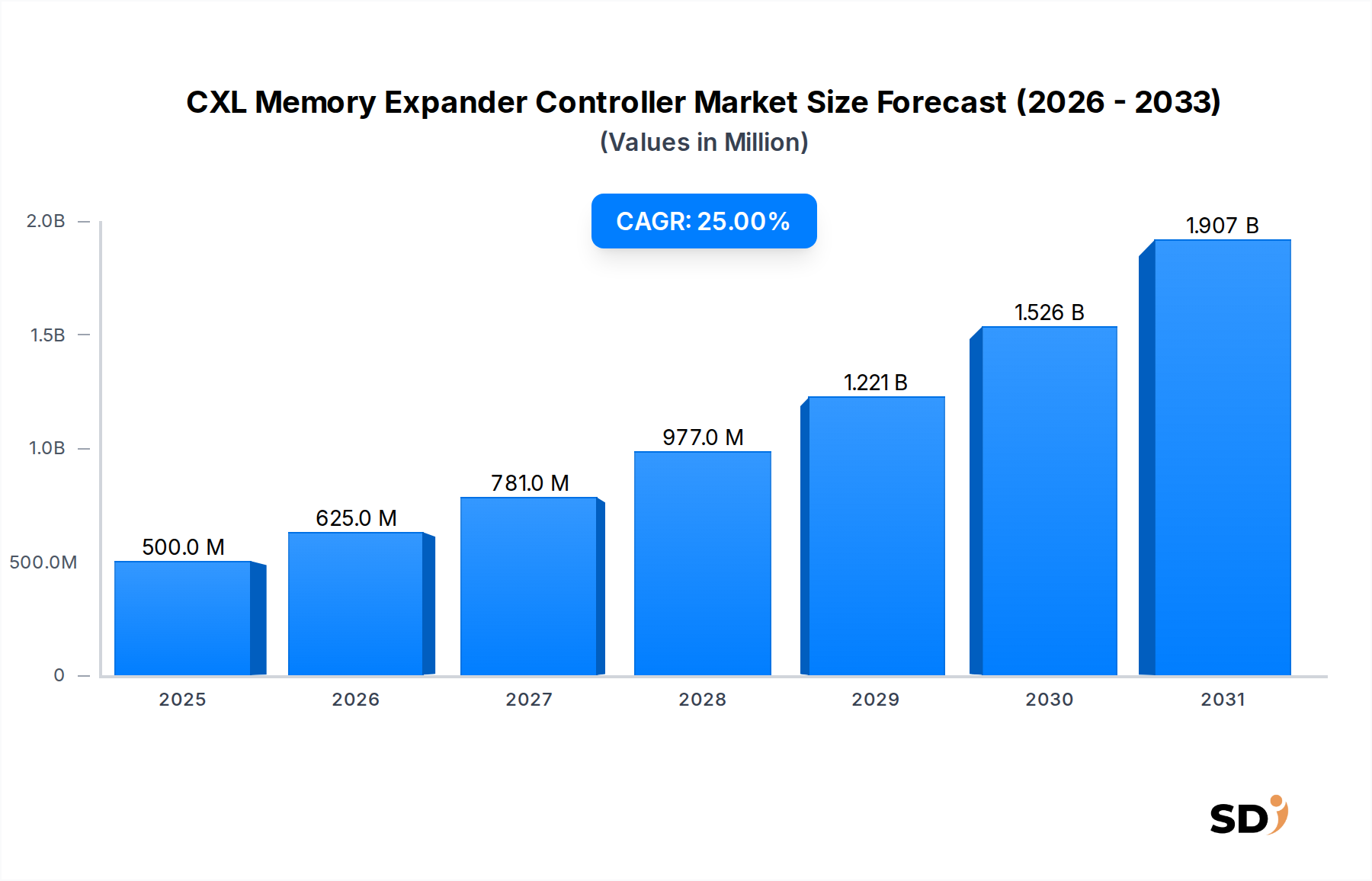

The CXL Memory Expander Controller Market is positioned for robust expansion, driven by the escalating demand for advanced memory solutions capable of addressing the complexities of modern data-intensive workloads. Valued at an estimated USD 500 million in 2025, the market is projected to reach USD 3,725.29 million by 2034, exhibiting an impressive Compound Annual Growth Rate (CAGR) of 25% over the forecast period. This significant growth trajectory is primarily propelled by the architectural paradigm shift towards memory disaggregation and pooling, critical for optimizing resource utilization in high-performance computing (HPC) and Artificial Intelligence Market applications. The inherent advantages of CXL controllers, such as increased memory bandwidth, lower latency, and expanded capacity, are becoming indispensable for server and data center environments struggling with traditional memory scaling limitations. Macro tailwinds include the rapid proliferation of digital transformation initiatives, the persistent demand for faster data processing, and the continuous evolution of server processor architectures that increasingly support CXL. The increasing adoption of the Cloud Computing Market also plays a pivotal role, as hyperscale operators seek innovative ways to improve operational efficiency and deliver superior performance to their vast client bases. Furthermore, the strategic evolution of the PCIe Interconnect Market, which forms the foundational layer for CXL, ensures a robust and high-bandwidth pathway for memory expansion. The market outlook remains exceptionally positive, as CXL technology matures, standards become more universally adopted, and an increasingly diverse ecosystem of hardware and software vendors emerge to support its deployment across various end-use segments, including the burgeoning Enterprise Storage Market. Innovation in controller design, coupled with advancements in the underlying DRAM Module Market, will further solidify the market's upward momentum.

CXL Memory Expander Controller Market Size (In Million)

2.0B

1.5B

1.0B

500.0M

0

500.0 M

2025

625.0 M

2026

781.0 M

2027

977.0 M

2028

1.221 B

2029

1.526 B

2030

1.907 B

2031

Data Center Applications Dominating the CXL Memory Expander Controller Market

The Data Center Infrastructure Market stands as the predominant application segment within the CXL Memory Expander Controller Market, projected to maintain its leading revenue share throughout the forecast period. This dominance is intrinsically linked to CXL's core value proposition, which directly addresses the scaling, efficiency, and performance challenges endemic to modern data centers. Hyperscale cloud providers, colocation facilities, and large-scale enterprise data centers are at the forefront of CXL adoption, driven by their insatiable demand for enhanced computational capabilities and optimized memory resource management. The growth of Artificial Intelligence Market workloads, machine learning, and big data analytics within these environments necessitates memory architectures that can transcend traditional DIMM slot limitations, providing both massive capacity expansion and the flexibility of memory pooling and tiering. CXL Memory Expander Controllers enable servers to access and share memory resources across multiple CPUs, GPUs, and specialized accelerators, significantly improving total cost of ownership (TCO) and operational efficiency. Key players in the CXL Memory Expander Controller Market, such as Astera Labs and Montage Technology, are intensely focused on developing and delivering solutions specifically optimized for server-grade applications, including robust error correction, advanced memory management, and secure communication protocols vital for mission-critical data center operations. The segment's market share is not merely consolidating but is actively expanding, propelled by the relentless pace of data generation and processing requirements across industries. The transition from legacy memory systems to CXL-enabled server platforms represents a fundamental shift in how data centers provision and utilize memory, impacting not only the immediate CXL controller demand but also influencing trends in the DDR4 Memory Market and especially the higher-bandwidth DDR5 Memory Market, as newer CXL implementations predominantly leverage the latest DDR5 DRAM for optimal performance. This continuous innovation and strategic investment by data center operators solidify the segment's dominant position and ensure its sustained growth as CXL technology becomes a standard component of next-generation server architectures.

The CXL Memory Expander Controller Market is profoundly influenced by a confluence of powerful drivers and notable constraints. A primary driver is the exponential growth in data generation and the increasing demand for processing capabilities from advanced applications such as Artificial Intelligence Market and High-Performance Computing (HPC). Enterprises are struggling with memory bottlenecks in existing server architectures, necessitating solutions that offer superior memory bandwidth and capacity beyond traditional DIMM limitations. The drive towards memory disaggregation and pooling in the Data Center Infrastructure Market further accelerates CXL adoption, as it allows for more efficient allocation and utilization of memory resources, reducing overall system costs and improving scalability. This architectural shift is also supported by advancements in the PCIe Interconnect Market, which provides the high-speed, low-latency foundation for CXL protocol communication, ensuring seamless integration and robust performance. Furthermore, the imperative for memory expansion is magnified by the proliferation of the Cloud Computing Market, where hyperscalers are continuously seeking to optimize server configurations for maximum performance and efficiency per watt. These factors combined create a compelling environment for the CXL Memory Expander Controller Market's rapid growth.

Conversely, significant constraints exist. The initial complexity and relatively nascent stage of the CXL ecosystem present integration challenges for system designers and IT professionals. Interoperability between different vendor solutions and generations of CXL controllers and devices is a concern, requiring robust standardization and extensive validation efforts. Moreover, the cost premium associated with new CXL-enabled hardware compared to traditional memory configurations can be a barrier for budget-sensitive organizations, particularly for widespread adoption outside of mission-critical or performance-intensive applications. While the DDR5 Memory Market is poised to benefit from CXL, the slower transition from the established DDR4 Memory Market still represents a segment that needs to be addressed for broader market penetration. Additionally, the reliance on a sophisticated supply chain, including the specialized manufacturing of the DRAM Module Market components, means that disruptions can impact the availability and pricing of CXL solutions. Overcoming these constraints will be crucial for the CXL Memory Expander Controller Market to achieve its full potential.

Competitive Ecosystem of CXL Memory Expander Controller Market

The competitive landscape of the CXL Memory Expander Controller Market is characterized by innovation-driven companies focusing on delivering high-performance, low-latency memory expansion solutions.

Astera Labs: A leading innovator in connectivity solutions for data-centric systems, Astera Labs is a key player in the CXL ecosystem, offering a portfolio of CXL-based products designed to unlock the full potential of memory and compute resources in data centers and cloud infrastructure. Their solutions are pivotal for enabling memory pooling, tiering, and expansion.

Microchip: A prominent provider of smart, connected, and secure embedded control solutions, Microchip has entered the CXL Memory Expander Controller Market with products aimed at facilitating the adoption of CXL technology, offering robust controllers that support advanced memory architectures and system scalability.

Montage Technology: Specializing in high-performance, low-power IC solutions for cloud computing and data center applications, Montage Technology is a significant contributor to the CXL controller segment, providing integral components that enable memory expansion and improve system efficiency in next-generation servers.

BIWIN: Known for its expertise in flash memory and DRAM products, BIWIN is expanding its portfolio to include CXL-compatible solutions, aiming to leverage its memory market experience to offer integrated CXL memory expander modules and controllers that meet the evolving demands of enterprise and data center clients.

Recent Developments & Milestones in CXL Memory Expander Controller Market

Recent developments underscore the rapid maturation and increasing industry acceptance of CXL technology within the CXL Memory Expander Controller Market:

October 2025: A major semiconductor firm announced the successful validation of its CXL Memory Expander Controller with a leading cloud service provider's next-generation server platform, signaling readiness for broader commercial deployment and significantly de-risking adoption for hyperscale customers.

August 2025: A prominent CXL IP provider secured substantial Series C funding, indicating strong investor confidence in the long-term potential of memory disaggregation and pooling technologies, specifically targeting growth in the Data Center Infrastructure Market.

June 2025: The CXL Consortium released a new specification update, focusing on enhanced security features and improved compatibility with emerging memory types, further solidifying the standard's robustness and expanding its addressable applications.

April 2025: A strategic partnership was forged between a leading server OEM and a CXL Memory Expander Controller manufacturer to jointly develop optimized server designs featuring integrated CXL memory expansion capabilities, aiming to accelerate time-to-market for enterprise solutions.

January 2025: Early performance benchmarks of CXL-enabled servers showcased significant improvements in memory capacity and bandwidth for Artificial Intelligence Market workloads, demonstrating the tangible benefits of CXL controllers in demanding computational environments.

November 2024: Several major memory module manufacturers announced plans to launch CXL-compatible DDR5 Memory Market modules with integrated expander logic, indicating a robust ecosystem development supporting the controller market.

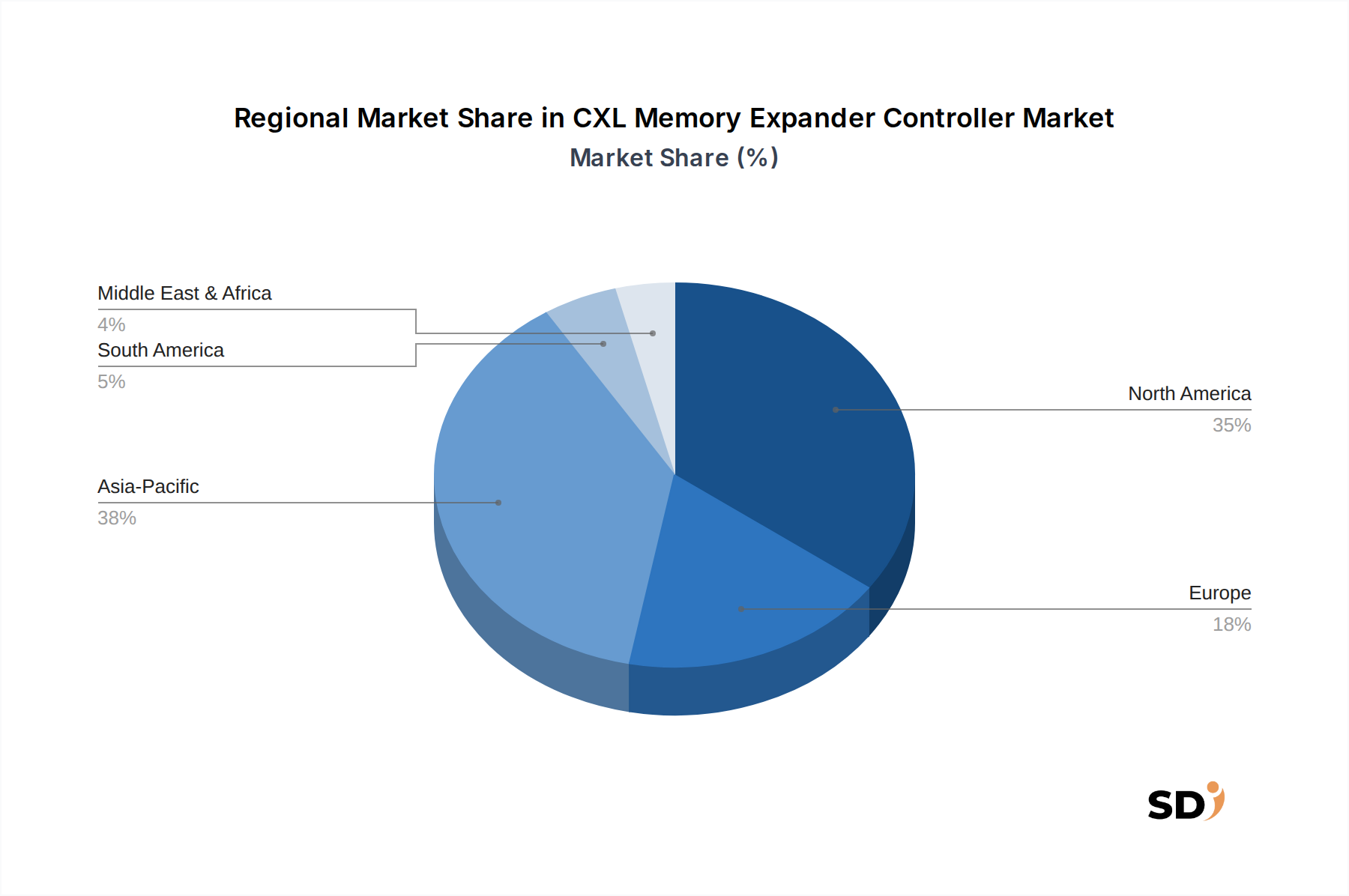

Regional Market Breakdown for CXL Memory Expander Controller Market

The global CXL Memory Expander Controller Market exhibits varied adoption rates and growth trajectories across different geographical regions, primarily influenced by technological infrastructure, data center investments, and the presence of key industry players. North America is anticipated to hold a significant revenue share and experience a high CAGR due to its robust technological ecosystem, early adoption of advanced data center architectures, and the strong presence of hyperscale Cloud Computing Market providers and leading Semiconductor Industry Market companies. The region's extensive R&D investments in AI and HPC drive the demand for sophisticated memory solutions, with the United States at the forefront of this innovation.

Asia Pacific, particularly China, Japan, and South Korea, is projected to be the fastest-growing region in the CXL Memory Expander Controller Market. This growth is fueled by massive investments in data center infrastructure, rapid digitalization across industries, and the burgeoning Artificial Intelligence Market and 5G network rollouts. Countries like China and India are seeing exponential growth in data consumption and storage, necessitating advanced memory solutions. The region also hosts a significant portion of the global electronics manufacturing base, fostering strong local innovation and competitive pricing.

Europe demonstrates a steady growth trajectory, driven by stringent data sovereignty regulations, increasing digitalization, and strong academic and industrial research in HPC. Countries like Germany, the UK, and France are investing in advanced computing facilities, requiring efficient memory expansion solutions. While adoption may be slightly more conservative than North America, the emphasis on energy efficiency and sustainable data centers provides a unique demand driver for CXL technology.

The Middle East & Africa (MEA) region represents an emerging market for CXL memory expander controllers. While starting from a smaller base, significant infrastructure investments, particularly in the GCC countries, coupled with initiatives to diversify economies through technology, are expected to fuel future demand. The need for localized data centers and cloud services will create opportunities for CXL deployments, though the initial growth might be slower compared to the more mature markets.

Pricing dynamics within the CXL Memory Expander Controller Market are currently characterized by premium average selling prices (ASPs), reflective of the technology's novelty, complexity, and the significant research and development investments required. As an early-stage market, specialized CXL controllers, particularly those supporting the DDR5 Memory Market, command higher prices due to advanced intellectual property, specialized manufacturing processes, and limited initial volume. The value chain for CXL controllers typically involves ASIC design houses, IP licensors, and semiconductor foundries, each contributing to the final cost. Margin structures are initially robust for pioneers, but are expected to experience pressure as the market matures and competitive intensity increases. Key cost levers include the cost of underlying silicon, packaging, and the integration of sophisticated firmware and software stacks for memory management. The cyclical nature of the broader Semiconductor Industry Market and fluctuations in the raw material costs for the DRAM Module Market can also indirectly influence CXL controller pricing, especially for solutions that integrate memory directly. As more vendors enter the Enterprise Storage Market and the Data Center Infrastructure Market with CXL-enabled products, economies of scale will gradually drive down component costs, leading to a more competitive pricing environment. This will necessitate manufacturers to optimize their design-for-cost strategies and innovate on performance-per-dollar metrics to maintain market share and profitability.

Investment & Funding Activity in CXL Memory Expander Controller Market

Investment and funding activity within the CXL Memory Expander Controller Market has been robust over the past 2-3 years, reflecting strong industry confidence in the technology's disruptive potential. Venture Capital (VC) firms have shown keen interest in startups specializing in CXL IP, controller design, and validation tools, providing significant capital to accelerate product development and market penetration. Several Series A and B funding rounds have been announced, primarily supporting companies focused on delivering CXL 1.1 and CXL 2.0 compliant controllers and related hardware for the Data Center Infrastructure Market. Strategic partnerships have also been a prominent feature, with major server OEMs and CPU manufacturers collaborating with CXL controller developers to integrate this technology into their next-generation platforms. This includes joint efforts to optimize CXL memory expanders for Artificial Intelligence Market and High-Performance Computing applications, aiming to create comprehensive, performant solutions. Mergers and acquisitions (M&A) activity, while not yet at a high volume, is anticipated to increase as larger Semiconductor Industry Market players look to acquire specialized CXL expertise or consolidate market share. The primary sub-segments attracting the most capital are those enabling memory pooling and tiering, particularly for the DDR5 Memory Market, and solutions designed to enhance the performance and efficiency of the Cloud Computing Market. Investment is also flowing into companies developing CXL-based solutions for the Enterprise Storage Market, recognizing the protocol's potential to revolutionize how data is accessed and managed across hybrid memory-storage hierarchies. This sustained investment underscores the strategic importance of CXL in shaping future data center architectures and memory ecosystems.

CXL Memory Expander Controller Segmentation

1. Application

1.1. Computers

1.2. Data Centers

1.3. Artificial Intelligence

1.4. Others

2. Types

2.1. DDR4

2.2. DDR5

CXL Memory Expander Controller Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

CXL Memory Expander Controller REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 25% from 2020-2034

Segmentation

By Application

Computers

Data Centers

Artificial Intelligence

Others

By Types

DDR4

DDR5

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Computers

5.1.2. Data Centers

5.1.3. Artificial Intelligence

5.1.4. Others

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. DDR4

5.2.2. DDR5

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Computers

6.1.2. Data Centers

6.1.3. Artificial Intelligence

6.1.4. Others

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. DDR4

6.2.2. DDR5

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Computers

7.1.2. Data Centers

7.1.3. Artificial Intelligence

7.1.4. Others

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. DDR4

7.2.2. DDR5

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Computers

8.1.2. Data Centers

8.1.3. Artificial Intelligence

8.1.4. Others

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. DDR4

8.2.2. DDR5

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Computers

9.1.2. Data Centers

9.1.3. Artificial Intelligence

9.1.4. Others

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. DDR4

9.2.2. DDR5

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Computers

10.1.2. Data Centers

10.1.3. Artificial Intelligence

10.1.4. Others

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. DDR4

10.2.2. DDR5

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Astera Labs

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Microchip

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Montage Technology

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. BIWIN

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (million), by Application 2025 & 2033

Figure 4: Volume (K), by Application 2025 & 2033

Figure 5: Revenue Share (%), by Application 2025 & 2033

Figure 6: Volume Share (%), by Application 2025 & 2033

Figure 7: Revenue (million), by Types 2025 & 2033

Figure 8: Volume (K), by Types 2025 & 2033

Figure 9: Revenue Share (%), by Types 2025 & 2033

Figure 10: Volume Share (%), by Types 2025 & 2033

Figure 11: Revenue (million), by Country 2025 & 2033

Figure 12: Volume (K), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Volume Share (%), by Country 2025 & 2033

Figure 15: Revenue (million), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (million), by Types 2025 & 2033

Figure 20: Volume (K), by Types 2025 & 2033

Figure 21: Revenue Share (%), by Types 2025 & 2033

Figure 22: Volume Share (%), by Types 2025 & 2033

Figure 23: Revenue (million), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (million), by Application 2025 & 2033

Figure 28: Volume (K), by Application 2025 & 2033

Figure 29: Revenue Share (%), by Application 2025 & 2033

Figure 30: Volume Share (%), by Application 2025 & 2033

Figure 31: Revenue (million), by Types 2025 & 2033

Figure 32: Volume (K), by Types 2025 & 2033

Figure 33: Revenue Share (%), by Types 2025 & 2033

Figure 34: Volume Share (%), by Types 2025 & 2033

Figure 35: Revenue (million), by Country 2025 & 2033

Figure 36: Volume (K), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Volume Share (%), by Country 2025 & 2033

Figure 39: Revenue (million), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (million), by Types 2025 & 2033

Figure 44: Volume (K), by Types 2025 & 2033

Figure 45: Revenue Share (%), by Types 2025 & 2033

Figure 46: Volume Share (%), by Types 2025 & 2033

Figure 47: Revenue (million), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (million), by Application 2025 & 2033

Figure 52: Volume (K), by Application 2025 & 2033

Figure 53: Revenue Share (%), by Application 2025 & 2033

Figure 54: Volume Share (%), by Application 2025 & 2033

Figure 55: Revenue (million), by Types 2025 & 2033

Figure 56: Volume (K), by Types 2025 & 2033

Figure 57: Revenue Share (%), by Types 2025 & 2033

Figure 58: Volume Share (%), by Types 2025 & 2033

Figure 59: Revenue (million), by Country 2025 & 2033

Figure 60: Volume (K), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

Figure 62: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Volume K Forecast, by Application 2020 & 2033

Table 3: Revenue million Forecast, by Types 2020 & 2033

Table 4: Volume K Forecast, by Types 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Volume K Forecast, by Region 2020 & 2033

Table 7: Revenue million Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue million Forecast, by Types 2020 & 2033

Table 10: Volume K Forecast, by Types 2020 & 2033

Table 11: Revenue million Forecast, by Country 2020 & 2033

Table 12: Volume K Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Volume (K) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Volume (K) Forecast, by Application 2020 & 2033

Table 17: Revenue (million) Forecast, by Application 2020 & 2033

Table 18: Volume (K) Forecast, by Application 2020 & 2033

Table 19: Revenue million Forecast, by Application 2020 & 2033

Table 20: Volume K Forecast, by Application 2020 & 2033

Table 21: Revenue million Forecast, by Types 2020 & 2033

Table 22: Volume K Forecast, by Types 2020 & 2033

Table 23: Revenue million Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue million Forecast, by Application 2020 & 2033

Table 32: Volume K Forecast, by Application 2020 & 2033

Table 33: Revenue million Forecast, by Types 2020 & 2033

Table 34: Volume K Forecast, by Types 2020 & 2033

Table 35: Revenue million Forecast, by Country 2020 & 2033

Table 36: Volume K Forecast, by Country 2020 & 2033

Table 37: Revenue (million) Forecast, by Application 2020 & 2033

Table 38: Volume (K) Forecast, by Application 2020 & 2033

Table 39: Revenue (million) Forecast, by Application 2020 & 2033

Table 40: Volume (K) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Volume (K) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (million) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue (million) Forecast, by Application 2020 & 2033

Table 50: Volume (K) Forecast, by Application 2020 & 2033

Table 51: Revenue (million) Forecast, by Application 2020 & 2033

Table 52: Volume (K) Forecast, by Application 2020 & 2033

Table 53: Revenue (million) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue million Forecast, by Application 2020 & 2033

Table 56: Volume K Forecast, by Application 2020 & 2033

Table 57: Revenue million Forecast, by Types 2020 & 2033

Table 58: Volume K Forecast, by Types 2020 & 2033

Table 59: Revenue million Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (million) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (million) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (million) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (million) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (million) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (million) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue million Forecast, by Application 2020 & 2033

Table 74: Volume K Forecast, by Application 2020 & 2033

Table 75: Revenue million Forecast, by Types 2020 & 2033

Table 76: Volume K Forecast, by Types 2020 & 2033

Table 77: Revenue million Forecast, by Country 2020 & 2033

Table 78: Volume K Forecast, by Country 2020 & 2033

Table 79: Revenue (million) Forecast, by Application 2020 & 2033

Table 80: Volume (K) Forecast, by Application 2020 & 2033

Table 81: Revenue (million) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue (million) Forecast, by Application 2020 & 2033

Table 84: Volume (K) Forecast, by Application 2020 & 2033

Table 85: Revenue (million) Forecast, by Application 2020 & 2033

Table 86: Volume (K) Forecast, by Application 2020 & 2033

Table 87: Revenue (million) Forecast, by Application 2020 & 2033

Table 88: Volume (K) Forecast, by Application 2020 & 2033

Table 89: Revenue (million) Forecast, by Application 2020 & 2033

Table 90: Volume (K) Forecast, by Application 2020 & 2033

Table 91: Revenue (million) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is the cornerstone of our market intelligence, accounting for a substantial 75% of our overall research efforts. This intensive approach ensures the collection of real-time, granular data directly from industry experts and key stakeholders, providing invaluable qualitative insights and validating quantitative findings. Our primary interviews are conducted through a structured questionnaire designed to elicit detailed information regarding market dynamics, technological advancements, competitive landscape, growth opportunities, and challenges specific to the CXL Memory Expander Controller market. Participants are carefully selected based on their expertise and position within the value chain.

Key stakeholders interviewed for this report include:

Director of Product Management (Memory/CXL)

Head of Server Architecture

Principal Hardware Engineer (Data Centers)

VP of AI Platform Strategy

Companies targeted for primary interviews span the entire value chain of the CXL Memory Expander Controller market, ensuring comprehensive coverage:

CXL Controller IC Manufacturers

Memory Module Manufacturers

Server/System OEMs

Hyperscale Data Center Operators

High-Performance Computing (HPC) & AI System Integrators

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Director of Product Management (Memory/CXL)

35%

Head of Server Architecture

30%

Principal Hardware Engineer (Data Centers)

20%

VP of AI Platform Strategy

15%

Industry Ecosystem Breakdown

Company Type

Representation (%)

CXL Controller IC Manufacturers

30%

Memory Module Manufacturers

25%

Server/System OEMs

25%

Hyperscale Data Center Operators

20%

Secondary Research & Industry Benchmarking

The remaining 25% of our research is dedicated to robust secondary research and industry benchmarking. This phase involves a rigorous review of publicly available information, financial reports, technical specifications, and industry whitepapers. Our objective is to build a foundational understanding of the market, identify key trends, validate primary research findings, and construct preliminary market sizing models. We strictly avoid data from other market research websites to maintain the integrity and originality of our findings.

Our secondary research sources include, but are not limited to:

Standard Financial Databases: Bloomberg, Factiva, Hoovers, and PitchBook, providing company financials, investment trends, and strategic initiatives.

Government Publications: Relevant government (.gov domains) economic reports, technology foresight documents, and trade statistics offering macroeconomic context and regional market indicators.

Industry Associations & Regulatory Bodies: Publications, standards documents, and whitepapers from globally recognized entities directly influencing the CXL Memory Expander Controller market:

Corporate Filings & Investor Presentations: Annual reports, quarterly earnings calls, and investor presentations of public companies involved in the CXL ecosystem.

Technical Journals & Whitepapers: Academic research and industry-specific technical documentation focusing on memory architectures, data center technologies, and AI hardware.

Demand Modeling & Market Estimation

Our market sizing and forecasting approach employs a sophisticated combination of top-down and bottom-up methodologies, complemented by multi-level data triangulation. This ensures a robust and verifiable market assessment.

Top-Down Approach: This involves estimating the total available market based on broader industry trends, macroeconomic indicators, and overall technology spending in relevant sectors (e.g., global server shipments, data center infrastructure investments, AI hardware expenditures). These macro-level figures are then disaggregated by application, type, and geography.

Bottom-Up Approach: This methodology builds the market size from the ground up, aggregating data points at the component or system level. Key metrics and variables used for bottom-up calculation in the CXL Memory Expander Controller market include:

Annual shipment volume of CXL-enabled servers/accelerator cards

Average Selling Price (ASP) of CXL memory expander controllers

CXL attach rate in new server deployments (by application segment)

Revenue per terabyte of CXL-enabled memory deployed

Market estimations are further triangulated by cross-referencing data from primary interviews, secondary research, and our internal proprietary databases. This iterative process allows for continuous refinement and validation of market figures across different data sources and analytical perspectives.

Data Accuracy & Quality Check

We are committed to delivering highly accurate and reliable market intelligence. Our rigorous quality control processes include:

Data Verification: All collected data, both primary and secondary, undergoes a thorough verification process to check for consistency, reliability, and relevance.

Expert Validation: Key findings, market sizes, and forecasts are reviewed and validated by a panel of internal and external subject matter experts to ensure alignment with current industry realities.

Methodological Review: Our methodologies are continuously reviewed and updated to incorporate the latest analytical techniques and industry best practices.

Iterative Refinement: Market estimates are iteratively refined based on new information, expert feedback, and comparative analysis.

Through these stringent measures, we guarantee an estimated data accuracy level of 85-90% for our market reports. Furthermore, our commitment to providing the most current market insights means that every report is meticulously updated with the latest available data and market developments up to the date of purchase, ensuring our clients receive timely and actionable intelligence.

Frequently Asked Questions

1. Which end-user industries drive demand for CXL Memory Expander Controllers?

The primary demand for CXL Memory Expander Controllers originates from data centers, artificial intelligence applications, and high-performance computing in general. These sectors increasingly require efficient memory expansion and pooling solutions, leading to significant adoption in server and accelerator systems.

2. How does the regulatory environment impact the CXL Memory Expander Controller market?

The CXL Memory Expander Controller market operates primarily under industry-driven standards rather than government-specific regulations. The CXL Consortium ensures interoperability and specification adherence, which is critical for ecosystem development and broad adoption across various vendor platforms.

3. What are the primary challenges affecting the CXL Memory Expander Controller market?

Key challenges include the complexity of integrating new CXL infrastructure into existing data center architectures and the initial investment costs associated with upgrading memory subsystems. Ensuring seamless compatibility across diverse hardware components from various suppliers also presents a hurdle.

4. What investment trends are observed in the CXL Memory Expander Controller sector?

Investment activity in the CXL Memory Expander Controller sector is driven by major players like Astera Labs and Microchip focusing on R&D and product development. With a projected 25% CAGR, significant capital is being directed towards advancing CXL technology to meet the expanding demands of data-intensive workloads.

5. What technological innovations are shaping the CXL Memory Expander Controller industry?

Innovations are centered on enhancing memory bandwidth, reducing latency, and supporting next-generation memory standards such as DDR5. The ongoing development of CXL 2.0 and future iterations aims to enable advanced memory pooling and sharing capabilities, optimizing resource utilization in computing environments.

6. How are enterprise purchasing trends evolving for CXL Memory Expander Controllers?

Enterprise purchasing trends are shifting towards solutions that offer superior total cost of ownership through improved memory utilization and system scalability. Adopters are prioritizing controllers that provide robust performance for AI and data analytics workloads, seeking long-term value and flexibility in memory infrastructure.