Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Children's Yogurt Market Trends: $2.9B by 2034 Growth

Children's Yogurt

Children's Yogurt Market Trends: $2.9B by 2034 Growth

Children's Yogurt by Product Type (Regular Yogurt, Greek Yogurt, Drinkable Yogurt, Probiotic Yogurt, Others), by Flavor Type (Plain/Unflavored, Fruit-Flavored, Vanilla-Flavored, Chocolate-Flavored, Mixed & Specialty Flavors), by Packaging Format (Cups & Tubs, Pouches, Bottles, Others), by Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 5, 2026|Base Year : 2025|Pages : 105

Key Insights into Children's Yogurt Market Dynamics

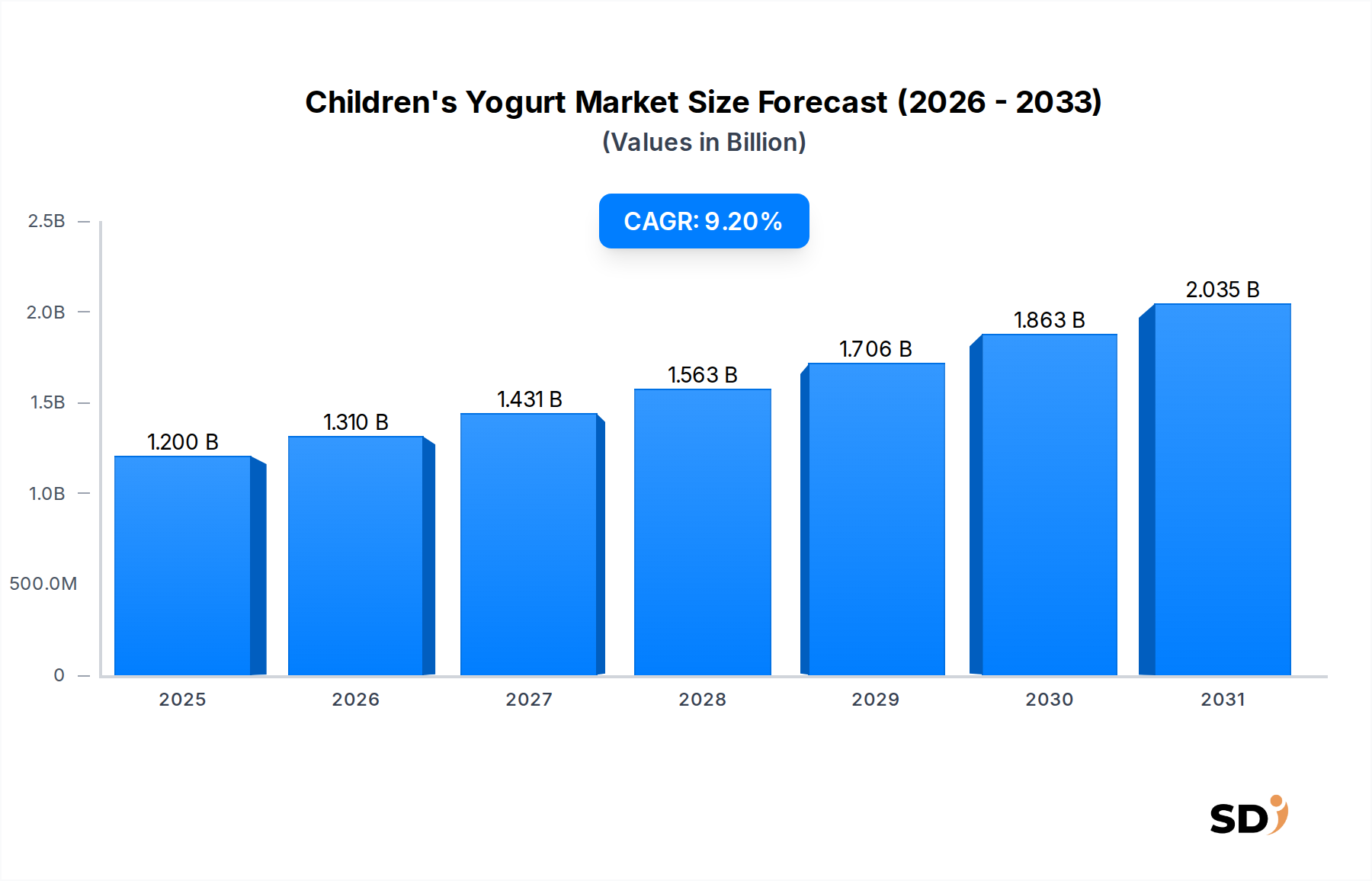

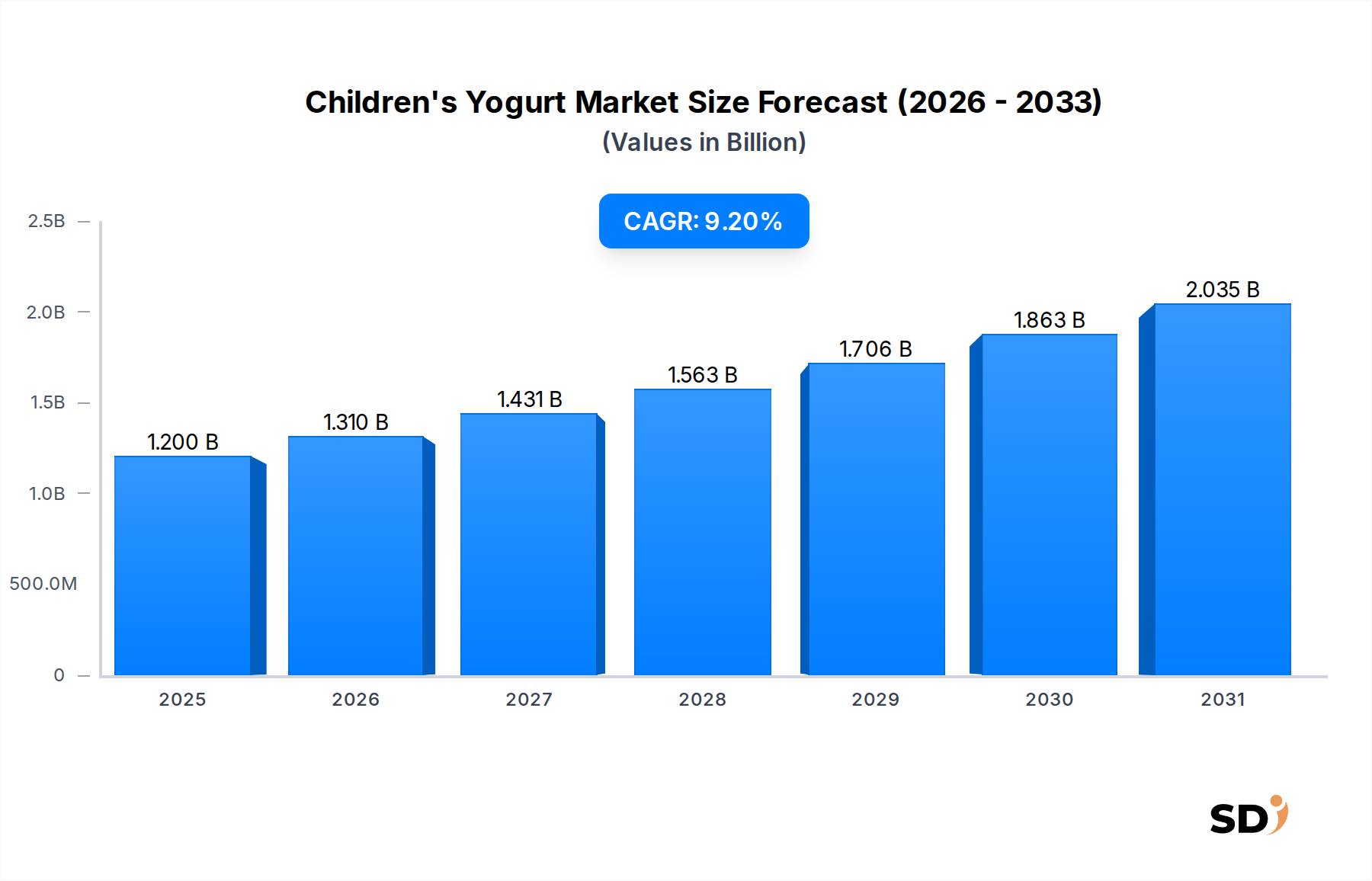

The Children's Yogurt Market is poised for substantial expansion, demonstrating a robust Compound Annual Growth Rate (CAGR) of 9.2% from 2024 to 2034. Valued at an estimated $1.2 billion in 2024, the global market is projected to reach approximately $2.9 billion by 2034. This growth trajectory is primarily propelled by increasing parental awareness concerning children's nutritional intake and the rising demand for convenient, healthy snacking options. Macroeconomic tailwinds, such as burgeoning disposable incomes in emerging economies and evolving dietary preferences towards healthier alternatives, significantly contribute to this market's upward trend. The market benefits from continuous product innovation, particularly in flavor profiles and functional ingredients, addressing both children's palates and parents' health concerns. The inclusion of probiotics, reduced sugar formulations, and fortification with essential vitamins and minerals are key drivers. Furthermore, the strategic emphasis on attractive and child-friendly Food Packaging Market designs, coupled with diverse distribution channels including online retail, enhances product accessibility and consumer engagement. The competitive landscape is characterized by both established dairy giants and agile niche players vying for market share through aggressive marketing and R&D investments. The rising penetration of organized retail and the increasing consumer preference for branded products also play a crucial role. As consumer lifestyles become more dynamic, the demand for on-the-go snack solutions continues to grow, positioning children's yogurt as a prime candidate within the broader Food & Beverage Market. Innovations in the Dairy Products Market, specifically related to milk sourcing and processing technologies, further bolster the supply chain and product quality. The outlook for the Children's Yogurt Market remains exceedingly positive, driven by persistent innovation, strategic market expansion by key players, and an overarching global shift towards health-conscious dietary habits among parents for their children.

Children's Yogurt Market Size (In Billion)

2.5B

2.0B

1.5B

1.0B

500.0M

0

1.200 B

2025

1.310 B

2026

1.431 B

2027

1.563 B

2028

1.706 B

2029

1.863 B

2030

2.035 B

2031

Dominance of Fruit-Flavored Varieties in Children's Yogurt Market

Within the Children's Yogurt Market, the Fruit-Flavored Yogurt Market segment stands out as the dominant category by revenue share, largely attributable to its intrinsic appeal to young consumers and strategic product development efforts. Children are naturally drawn to sweet and vibrant flavors, making fruit-infused yogurts a highly palatable option. This segment encompasses a wide array of offerings, from common strawberry, blueberry, and mixed berry flavors to more exotic tropical fruit combinations, continually innovated to capture children's interest. The prominence of fruit-flavored varieties is further reinforced by parental preference for products that offer perceived nutritional benefits, with fruit content often marketed as a source of vitamins and natural sugars, even though added sugars remain a consideration. This balance between taste and nutrition is a critical factor in consumer purchasing decisions for the Children's Yogurt Market. Key players such as Danone (with brands like Danimals), General Mills (Yoplait Kids), and Stonyfield Farm have heavily invested in this segment, launching diverse fruit-flavored lines that incorporate fun characters and appealing packaging. Their dominance is maintained through extensive marketing campaigns targeted at both children and parents, emphasizing natural fruit ingredients and essential nutrients. The proliferation of fruit purees and natural flavoring agents has also enabled manufacturers to expand their product portfolios within this segment, offering options like smoothies and Drinkable Yogurt Market formats that maintain the fruit-forward appeal. While other flavor types like vanilla and chocolate hold significant shares, the sheer variety, consistent innovation, and consumer acceptance of fruit-flavored options grant them the leading position. Furthermore, the ability of these products to mask the sometimes tart taste of plain yogurt makes them more accessible to children who are developing their taste preferences. As a result, the Fruit-Flavored Yogurt Market continues to grow and consolidate its leadership, with manufacturers focusing on expanding organic and low-sugar fruit-flavored options to address evolving health trends within the Children's Yogurt Market.

Key Growth Drivers and Nutritional Imperatives in Children's Yogurt Market

The Children's Yogurt Market's robust growth, characterized by a 9.2% CAGR, is underpinned by several critical drivers rooted in evolving consumer demands and industry innovations. A primary driver is the escalating parental awareness of children's nutritional requirements. Parents are increasingly seeking food products that offer tangible health benefits beyond basic caloric intake. This manifests as a strong demand for fortified yogurts, rich in calcium for bone development, vitamin D, and often probiotics for gut health. The surge in the Probiotic Yogurt Market, particularly within the children's segment, exemplifies this trend, as parents associate gut health with improved immunity and overall well-being. This focus positions children's yogurt as a Functional Foods Market category. Another significant driver is the convenience factor. Modern lifestyles, characterized by busy schedules, have amplified the need for ready-to-eat and on-the-go snack solutions. Children's yogurt, often available in portable pouches or single-serving cups, perfectly aligns with this demand, offering a quick and nutritious option for school lunches, after-school snacks, or travel. Product innovation, especially in reducing sugar content while maintaining palatability, is also a crucial catalyst. Manufacturers are responding to health concerns by introducing "less sugar" or "no added sugar" variants, often using natural sweeteners or leveraging the sweetness of fruits. The increasing prevalence of lactose intolerance and dairy allergies has also spurred the growth of plant-based children's yogurt alternatives, broadening the market's reach. Finally, the strategic marketing and branding efforts, leveraging child-friendly characters and vibrant packaging, effectively capture children's attention while reassuring parents about product quality and safety, contributing significantly to sustained market expansion within the Children's Yogurt Market. The influence of the Infant Nutrition Market also indirectly impacts this segment, as dietary habits established in early childhood often extend to the children's segment.

Competitive Ecosystem of Children's Yogurt Market

The Children's Yogurt Market features a dynamic competitive landscape dominated by global food and beverage conglomerates alongside specialized dairy producers, all vying for consumer preference through innovation and strategic market penetration.

Danone: A global leader in fresh dairy products, Danone holds a significant share in the Children's Yogurt Market through its Danimals brand, known for its focus on nutrition, fun packaging, and diverse fruit flavors. Their strategy includes product diversification and regional market penetration.

General Mills (Yoplait): With its Yoplait Kids line, General Mills is a strong contender, offering popular flavors and convenient packaging solutions like pouches. The company leverages its extensive distribution network and brand recognition.

Lactalis Group: A prominent player in the global dairy sector, Lactalis offers a range of children's yogurt products under various regional brands, emphasizing quality dairy and appealing formulations.

Nestlé: Operating across multiple food categories, Nestlé contributes to the Children's Yogurt Market with products designed to meet specific nutritional needs for growing children, often incorporating fortified ingredients.

Chobani: Known for popularizing Greek Yogurt Market in North America, Chobani has expanded into the children's segment with products like Chobani Gimmies, focusing on high protein content and natural ingredients.

FAGE International: While primarily known for its adult Greek yogurt, FAGE selectively participates in the broader dairy segment, influencing product quality benchmarks.

Arla Foods: A European dairy cooperative, Arla Foods offers a range of children's dairy products, focusing on natural ingredients and sustainable sourcing within its key markets.

Stonyfield Farm: A pioneer in organic dairy, Stonyfield Farm commands a strong position in the Children's Yogurt Market with its organic YoBaby and YoKids lines, appealing to health-conscious parents.

Müller Group: A major European dairy company, Müller offers various children's yogurt and dessert options, known for their creamy texture and diverse flavor profiles.

Yeo Valley: A leading organic dairy brand in the UK, Yeo Valley provides organic children's yogurts, emphasizing natural ingredients and ethical farming practices.

The Kraft Heinz Company: While not a primary yogurt player, Kraft Heinz may offer dairy-adjacent products or strategically partner to expand its presence in the children's food sector.

Valio: A Finnish dairy and food company, Valio offers various dairy products, including children's yogurts, focusing on innovative nutritional solutions and high-quality milk.

Morinaga Milk Industry: A major Japanese dairy company, Morinaga Milk Industry offers a wide array of dairy products, including those tailored for the children's segment, with a strong focus on research and development.

Recent Developments & Milestones in Children's Yogurt Market

The Children's Yogurt Market has witnessed several strategic developments aimed at product innovation, market expansion, and addressing evolving consumer preferences. These milestones reflect the dynamic nature of the industry and its response to health trends and competitive pressures.

January 2024: Danone launched a new line of reduced-sugar Danimals smoothies fortified with Vitamin D, specifically targeting parental concerns about sugar content and bone health in children.

April 2023: Stonyfield Farm expanded its organic YoKids line with new plant-based options made from oat milk, catering to the growing demand for dairy-free alternatives in the Children's Yogurt Market.

July 2023: General Mills (Yoplait) introduced limited-edition character-themed yogurt pouches for its Yoplait Kids range, leveraging popular children's media franchises to boost market appeal and engagement.

September 2022: Chobani unveiled a new marketing campaign for its children's yogurt products, emphasizing the high protein content and absence of artificial ingredients, aligning with the broader Functional Foods Market trend.

November 2022: Arla Foods invested in new manufacturing capabilities in Europe to increase production capacity for its children's yogurt range, anticipating higher demand across key European markets.

February 2023: Several regional brands within the Children's Yogurt Market began incorporating upcycled fruit ingredients into their products, highlighting sustainable sourcing practices as a new value proposition for eco-conscious parents.

June 2024: Researchers presented findings on the efficacy of specific probiotic strains in children's yogurts for enhancing digestive health, prompting a renewed focus on scientifically-backed Probiotic Yogurt Market product development.

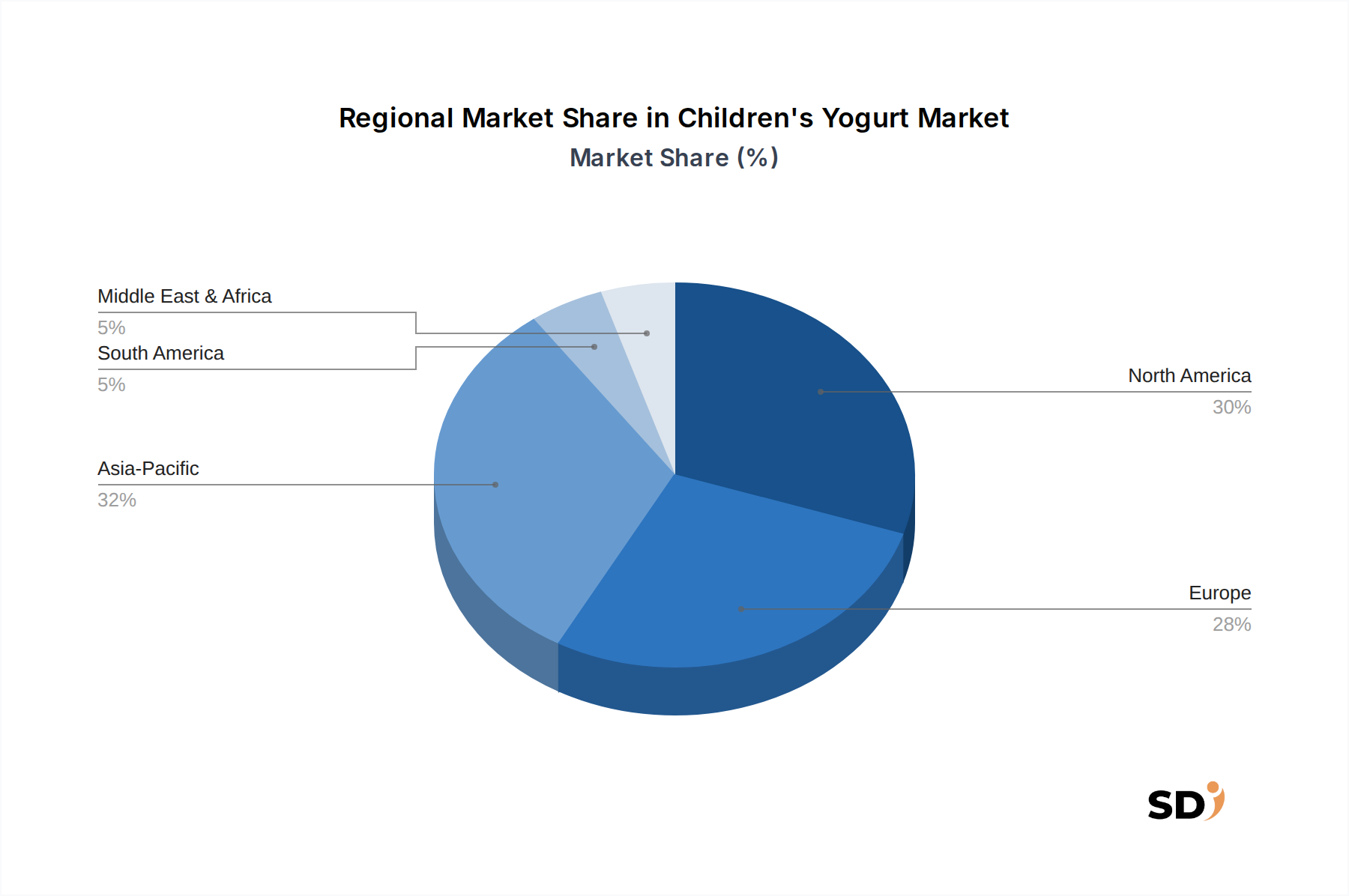

Regional Market Breakdown for Children's Yogurt Market

The Children's Yogurt Market exhibits varied growth dynamics across different global regions, influenced by economic development, dietary habits, and parental awareness. North America and Europe currently represent the most mature markets but continue to show steady growth. North America, encompassing the United States, Canada, and Mexico, holds a significant revenue share, driven by a well-established dairy industry, high disposable incomes, and a strong preference for convenient, nutritious snacks. The region's demand is primarily fueled by innovations in the Flavored Yogurt Market and the proliferation of Greek Yogurt Market products tailored for children. Europe, including the United Kingdom, Germany, and France, also accounts for a substantial share, characterized by high per capita consumption of dairy products and a strong emphasis on organic and natural ingredients. The European Children's Yogurt Market is driven by stringent food safety standards and a consumer base increasingly inclined towards products with reduced sugar and added functional benefits. Both regions show a steady CAGR, indicative of market saturation but continuous innovation.

Asia Pacific, including China, India, and Japan, is anticipated to be the fastest-growing region in the Children's Yogurt Market. This accelerated growth is attributed to rising disposable incomes, rapid urbanization, a growing middle-class population, and increasing awareness of the nutritional benefits of yogurt for children. The vast population base and cultural shifts towards Western dietary patterns significantly contribute to this expansion, particularly for products in the Drinkable Yogurt Market segment. South America, with Brazil and Argentina as key markets, also presents considerable growth opportunities, driven by economic development and improving access to packaged food products. The Middle East & Africa region, while smaller in market size, is experiencing nascent growth due to increasing health consciousness and rising birth rates, albeit from a lower base. Overall, while North America and Europe remain key revenue contributors, the Asia Pacific region is set to spearhead future growth in the Children's Yogurt Market, driven by untapped potential and evolving consumer behaviors.

Customer Segmentation & Buying Behavior in Children's Yogurt Market

The customer base in the Children's Yogurt Market is primarily segmented by age groups (toddlers, preschoolers, school-aged children) and parental demographics (health-conscious, budget-sensitive, convenience-driven). Toddler-focused products (e.g., YoBaby) often prioritize organic ingredients, smooth textures, and simple, natural flavors, catering to the early stages of solid food introduction. For preschoolers and school-aged children, products are characterized by more diverse flavors, fun packaging featuring popular characters, and convenient formats like pouches that support on-the-go consumption. Purchasing criteria for parents are multifaceted, with nutritional value (e.g., calcium, vitamin D, protein, probiotics) being paramount, followed closely by ingredients (e.g., natural, organic, low sugar, no artificial colors/flavors). The influence of the Probiotic Yogurt Market is significant here, as many parents actively seek out products offering digestive health benefits. Price sensitivity varies; while a segment of parents is willing to pay a premium for organic or functionally enriched yogurts, a larger segment seeks value without compromising on basic health attributes. Procurement channels are diverse, with supermarkets and hypermarkets remaining the dominant points of sale, often offering bulk purchase incentives. Online retail is experiencing rapid growth, driven by convenience and subscription models, allowing parents to research and compare products more easily. In recent cycles, there has been a notable shift towards increased scrutiny of sugar content and a preference for plant-based or dairy-free alternatives due to dietary restrictions or ethical considerations. This trend underscores the evolving sophistication of parental buying behavior in the Children's Yogurt Market, driving manufacturers to innovate across the product spectrum.

Export, Trade Flow & Tariff Impact on Children's Yogurt Market

The Children's Yogurt Market is subject to intricate global trade flows, influenced by regional production capabilities, consumer demand, and evolving trade policies. Major trade corridors for dairy and dairy-derived products, including yogurt, predominantly exist between dairy-rich nations and regions with high import demand or limited domestic production. European countries like Germany, France, and the Netherlands are significant exporters of various dairy products, including specialized yogurts, often serving other European nations and, to a lesser extent, international markets. North America, particularly the U.S., also participates in export, often targeting neighboring countries. Leading importing nations include those with large populations and developing dairy industries, such as China and countries in Southeast Asia, which often source specialized products like children's yogurt from established producers in Europe and Oceania. The Dairy Products Market, as a whole, sets the tone for these trade dynamics. Tariff and non-tariff barriers can significantly impact cross-border volume and market accessibility. For instance, specific import quotas, sanitary and phytosanitary (SPS) measures, and labeling requirements act as non-tariff barriers, increasing compliance costs and limiting market entry for some manufacturers. Recent trade policy shifts, such as regional free trade agreements, have facilitated smoother cross-border movement for some players in the Children's Yogurt Market, reducing tariffs and streamlining customs procedures. Conversely, trade disputes or protectionist measures in certain economies have led to increased import duties, potentially raising consumer prices or diverting trade flows to more favorable markets. Quantifying the precise impact on children's yogurt is complex, as it falls under broader dairy categories, but even minor tariff adjustments can influence pricing strategies and competitiveness, particularly for premium or specialty products. The Food & Beverage Market's global nature means that these trade dynamics are constantly evolving, requiring manufacturers to adapt their supply chain strategies to optimize export efficiency and manage regulatory compliance.

Children's Yogurt Segmentation

1. Product Type

1.1. Regular Yogurt

1.2. Greek Yogurt

1.3. Drinkable Yogurt

1.4. Probiotic Yogurt

1.5. Others

2. Flavor Type

2.1. Plain/Unflavored

2.2. Fruit-Flavored

2.3. Vanilla-Flavored

2.4. Chocolate-Flavored

2.5. Mixed & Specialty Flavors

3. Packaging Format

3.1. Cups & Tubs

3.2. Pouches

3.3. Bottles

3.4. Others

4. Distribution Channel

4.1. Supermarkets & Hypermarkets

4.2. Convenience Stores

4.3. Online Retail

4.4. Others

Children's Yogurt Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Children's Yogurt REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 9.2% from 2020-2034

Segmentation

By Product Type

Regular Yogurt

Greek Yogurt

Drinkable Yogurt

Probiotic Yogurt

Others

By Flavor Type

Plain/Unflavored

Fruit-Flavored

Vanilla-Flavored

Chocolate-Flavored

Mixed & Specialty Flavors

By Packaging Format

Cups & Tubs

Pouches

Bottles

Others

By Distribution Channel

Supermarkets & Hypermarkets

Convenience Stores

Online Retail

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Type

5.1.1. Regular Yogurt

5.1.2. Greek Yogurt

5.1.3. Drinkable Yogurt

5.1.4. Probiotic Yogurt

5.1.5. Others

5.2. Market Analysis, Insights and Forecast - by Flavor Type

5.2.1. Plain/Unflavored

5.2.2. Fruit-Flavored

5.2.3. Vanilla-Flavored

5.2.4. Chocolate-Flavored

5.2.5. Mixed & Specialty Flavors

5.3. Market Analysis, Insights and Forecast - by Packaging Format

5.3.1. Cups & Tubs

5.3.2. Pouches

5.3.3. Bottles

5.3.4. Others

5.4. Market Analysis, Insights and Forecast - by Distribution Channel

5.4.1. Supermarkets & Hypermarkets

5.4.2. Convenience Stores

5.4.3. Online Retail

5.4.4. Others

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Product Type

6.1.1. Regular Yogurt

6.1.2. Greek Yogurt

6.1.3. Drinkable Yogurt

6.1.4. Probiotic Yogurt

6.1.5. Others

6.2. Market Analysis, Insights and Forecast - by Flavor Type

6.2.1. Plain/Unflavored

6.2.2. Fruit-Flavored

6.2.3. Vanilla-Flavored

6.2.4. Chocolate-Flavored

6.2.5. Mixed & Specialty Flavors

6.3. Market Analysis, Insights and Forecast - by Packaging Format

6.3.1. Cups & Tubs

6.3.2. Pouches

6.3.3. Bottles

6.3.4. Others

6.4. Market Analysis, Insights and Forecast - by Distribution Channel

6.4.1. Supermarkets & Hypermarkets

6.4.2. Convenience Stores

6.4.3. Online Retail

6.4.4. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Product Type

7.1.1. Regular Yogurt

7.1.2. Greek Yogurt

7.1.3. Drinkable Yogurt

7.1.4. Probiotic Yogurt

7.1.5. Others

7.2. Market Analysis, Insights and Forecast - by Flavor Type

7.2.1. Plain/Unflavored

7.2.2. Fruit-Flavored

7.2.3. Vanilla-Flavored

7.2.4. Chocolate-Flavored

7.2.5. Mixed & Specialty Flavors

7.3. Market Analysis, Insights and Forecast - by Packaging Format

7.3.1. Cups & Tubs

7.3.2. Pouches

7.3.3. Bottles

7.3.4. Others

7.4. Market Analysis, Insights and Forecast - by Distribution Channel

7.4.1. Supermarkets & Hypermarkets

7.4.2. Convenience Stores

7.4.3. Online Retail

7.4.4. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Product Type

8.1.1. Regular Yogurt

8.1.2. Greek Yogurt

8.1.3. Drinkable Yogurt

8.1.4. Probiotic Yogurt

8.1.5. Others

8.2. Market Analysis, Insights and Forecast - by Flavor Type

8.2.1. Plain/Unflavored

8.2.2. Fruit-Flavored

8.2.3. Vanilla-Flavored

8.2.4. Chocolate-Flavored

8.2.5. Mixed & Specialty Flavors

8.3. Market Analysis, Insights and Forecast - by Packaging Format

8.3.1. Cups & Tubs

8.3.2. Pouches

8.3.3. Bottles

8.3.4. Others

8.4. Market Analysis, Insights and Forecast - by Distribution Channel

8.4.1. Supermarkets & Hypermarkets

8.4.2. Convenience Stores

8.4.3. Online Retail

8.4.4. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Product Type

9.1.1. Regular Yogurt

9.1.2. Greek Yogurt

9.1.3. Drinkable Yogurt

9.1.4. Probiotic Yogurt

9.1.5. Others

9.2. Market Analysis, Insights and Forecast - by Flavor Type

9.2.1. Plain/Unflavored

9.2.2. Fruit-Flavored

9.2.3. Vanilla-Flavored

9.2.4. Chocolate-Flavored

9.2.5. Mixed & Specialty Flavors

9.3. Market Analysis, Insights and Forecast - by Packaging Format

9.3.1. Cups & Tubs

9.3.2. Pouches

9.3.3. Bottles

9.3.4. Others

9.4. Market Analysis, Insights and Forecast - by Distribution Channel

9.4.1. Supermarkets & Hypermarkets

9.4.2. Convenience Stores

9.4.3. Online Retail

9.4.4. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Product Type

10.1.1. Regular Yogurt

10.1.2. Greek Yogurt

10.1.3. Drinkable Yogurt

10.1.4. Probiotic Yogurt

10.1.5. Others

10.2. Market Analysis, Insights and Forecast - by Flavor Type

10.2.1. Plain/Unflavored

10.2.2. Fruit-Flavored

10.2.3. Vanilla-Flavored

10.2.4. Chocolate-Flavored

10.2.5. Mixed & Specialty Flavors

10.3. Market Analysis, Insights and Forecast - by Packaging Format

10.3.1. Cups & Tubs

10.3.2. Pouches

10.3.3. Bottles

10.3.4. Others

10.4. Market Analysis, Insights and Forecast - by Distribution Channel

10.4.1. Supermarkets & Hypermarkets

10.4.2. Convenience Stores

10.4.3. Online Retail

10.4.4. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Danone

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. General Mills (Yoplait)

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Lactalis Group

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Nestlé

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Chobani

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. FAGE International

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Arla Foods

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Stonyfield Farm

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Müller Group

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Yeo Valley

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. The Kraft Heinz Company

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Valio

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. Morinaga Milk Industry

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.1.14. Others

11.1.14.1. Company Overview

11.1.14.2. Products

11.1.14.3. Company Financials

11.1.14.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Product Type 2025 & 2033

Figure 3: Revenue Share (%), by Product Type 2025 & 2033

Figure 4: Revenue (billion), by Flavor Type 2025 & 2033

Figure 5: Revenue Share (%), by Flavor Type 2025 & 2033

Figure 6: Revenue (billion), by Packaging Format 2025 & 2033

Figure 7: Revenue Share (%), by Packaging Format 2025 & 2033

Figure 8: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 9: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 10: Revenue (billion), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (billion), by Product Type 2025 & 2033

Figure 13: Revenue Share (%), by Product Type 2025 & 2033

Figure 14: Revenue (billion), by Flavor Type 2025 & 2033

Figure 15: Revenue Share (%), by Flavor Type 2025 & 2033

Figure 16: Revenue (billion), by Packaging Format 2025 & 2033

Figure 17: Revenue Share (%), by Packaging Format 2025 & 2033

Figure 18: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 19: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 20: Revenue (billion), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (billion), by Product Type 2025 & 2033

Figure 23: Revenue Share (%), by Product Type 2025 & 2033

Figure 24: Revenue (billion), by Flavor Type 2025 & 2033

Figure 25: Revenue Share (%), by Flavor Type 2025 & 2033

Figure 26: Revenue (billion), by Packaging Format 2025 & 2033

Figure 27: Revenue Share (%), by Packaging Format 2025 & 2033

Figure 28: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 29: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 30: Revenue (billion), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (billion), by Product Type 2025 & 2033

Figure 33: Revenue Share (%), by Product Type 2025 & 2033

Figure 34: Revenue (billion), by Flavor Type 2025 & 2033

Figure 35: Revenue Share (%), by Flavor Type 2025 & 2033

Figure 36: Revenue (billion), by Packaging Format 2025 & 2033

Figure 37: Revenue Share (%), by Packaging Format 2025 & 2033

Figure 38: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 39: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 40: Revenue (billion), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (billion), by Product Type 2025 & 2033

Figure 43: Revenue Share (%), by Product Type 2025 & 2033

Figure 44: Revenue (billion), by Flavor Type 2025 & 2033

Figure 45: Revenue Share (%), by Flavor Type 2025 & 2033

Figure 46: Revenue (billion), by Packaging Format 2025 & 2033

Figure 47: Revenue Share (%), by Packaging Format 2025 & 2033

Figure 48: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 49: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 50: Revenue (billion), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Product Type 2020 & 2033

Table 2: Revenue billion Forecast, by Flavor Type 2020 & 2033

Table 3: Revenue billion Forecast, by Packaging Format 2020 & 2033

Table 4: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Revenue billion Forecast, by Product Type 2020 & 2033

Table 7: Revenue billion Forecast, by Flavor Type 2020 & 2033

Table 8: Revenue billion Forecast, by Packaging Format 2020 & 2033

Table 9: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 10: Revenue billion Forecast, by Country 2020 & 2033

Table 11: Revenue (billion) Forecast, by Application 2020 & 2033

Table 12: Revenue (billion) Forecast, by Application 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue billion Forecast, by Product Type 2020 & 2033

Table 15: Revenue billion Forecast, by Flavor Type 2020 & 2033

Table 16: Revenue billion Forecast, by Packaging Format 2020 & 2033

Table 17: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 18: Revenue billion Forecast, by Country 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Revenue (billion) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Revenue billion Forecast, by Product Type 2020 & 2033

Table 23: Revenue billion Forecast, by Flavor Type 2020 & 2033

Table 24: Revenue billion Forecast, by Packaging Format 2020 & 2033

Table 25: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 26: Revenue billion Forecast, by Country 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue (billion) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Revenue (billion) Forecast, by Application 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue billion Forecast, by Product Type 2020 & 2033

Table 37: Revenue billion Forecast, by Flavor Type 2020 & 2033

Table 38: Revenue billion Forecast, by Packaging Format 2020 & 2033

Table 39: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 40: Revenue billion Forecast, by Country 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue (billion) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Revenue (billion) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue billion Forecast, by Product Type 2020 & 2033

Table 48: Revenue billion Forecast, by Flavor Type 2020 & 2033

Table 49: Revenue billion Forecast, by Packaging Format 2020 & 2033

Table 50: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology forms the cornerstone of this report, accounting for 70-80% of our total research efforts. This intensive approach is designed to capture real-time market dynamics, validated insights, and nuanced perspectives directly from industry participants. We engage in structured interviews, surveys, and expert consultations across the value chain of the children's yogurt market. Our engagement strategy targets a diverse range of stakeholders, ensuring comprehensive data collection and a robust understanding of market drivers, challenges, and opportunities.

Key stakeholders interviewed for this study include:

Product Manager, Children's Dairy/Yogurt Category

Head of R&D, Food & Beverage Innovation (with a focus on child nutrition)

Category Buyer/Manager, Dairy & Refrigerated Foods (at major retail chains)

Food Safety & Regulatory Affairs Specialist

Companies engaged in our primary research span critical segments of the value chain, including:

Complementing our primary research, secondary research constitutes 20-30% of our data acquisition strategy. This phase focuses on establishing a strong foundational understanding of the market, identifying broad trends, and validating primary insights against established data points. We leverage a rigorous process of data collection from credible, authoritative sources to ensure accuracy and impartiality. All data is continuously cross-referenced and updated to reflect the most current market conditions, ensuring the report is up-to-date at the point of purchase.

Our secondary research extensively utilizes premium financial and business intelligence databases such as:

Bloomberg Terminal

Factiva

Hoovers

PitchBook

Furthermore, we integrate data from government publications, academic journals, and reputable industry associations to enrich our analysis and provide a macro-level perspective. Key sources include:

Official Government Statistical Bureaus (e.g., U.S. Department of Agriculture USDA, Eurostat Eurostat)

World Health Organization (WHO) and Food and Agriculture Organization (FAO) reports (e.g., Codex Alimentarius Commission)

Industry publications and reports from globally recognized associations, such as:

We strictly avoid data from other market research websites to maintain the originality and integrity of our findings.

Demand Modeling & Market Estimation

Our market estimation methodology employs a robust combination of top-down and bottom-up approaches, further reinforced by multi-level data triangulation. This ensures a comprehensive and accurate sizing of the children's yogurt market across all defined segments and geographies.

Top-Down Approach: This method involves estimating the total addressable market based on macroeconomic factors, overall food and beverage industry trends, and total dairy consumption, then segmenting it down to the specific children's yogurt market using relevant penetration rates, demographics, and product-specific factors.

Bottom-Up Approach: This highly granular approach builds the market size from the ground up by aggregating specific data points. For the children's yogurt market, key metrics and variables utilized for bottom-up calculation include:

Children population demographics and growth rates (e.g., age 0-14, 0-12 segments) by region/country.

Average per capita consumption of children's yogurt (in volume or frequency) across key geographic markets.

Average retail price per unit/pack for various product types (regular, Greek, drinkable, probiotic) and packaging formats (cups, pouches, bottles).

Market penetration rates of children's yogurt products in households within different regions.

Multi-Level Data Triangulation: This critical step involves cross-validating data points obtained from primary research, secondary sources, and both top-down and bottom-up models. Discrepancies are meticulously investigated and resolved through further expert consultation and data verification, ensuring a converged, reliable market estimate.

Data Accuracy & Quality Check

Our commitment to data integrity and reliability is paramount. We guarantee an estimated data accuracy level of 85-90% for the market size and forecast provided in this report. This high level of accuracy is achieved through:

Continuous Validation: All data, whether primary or secondary, undergoes stringent validation processes. Primary insights are cross-referenced with multiple experts and validated against secondary data. Secondary data is checked for source credibility, recency, and consistency.

Analytical Rigor: Our team of experienced analysts applies advanced statistical and econometric models to interpret data, identify trends, and generate forecasts. Models are continuously reviewed and refined.

Expert Panel Review: Preliminary findings and market estimates are subjected to review by an internal panel of senior market research analysts and external industry experts to challenge assumptions and ensure logical consistency.

Timely Updates: As a standard practice, every report is updated up to the date of purchase, incorporating the latest market developments, regulatory changes, and economic shifts to provide the most current and relevant insights.

Frequently Asked Questions

1. What technological innovations are shaping the Children's Yogurt market?

Innovations focus on functional ingredients, including enhanced probiotic strains and improved nutritional profiles (e.g., reduced sugar, added vitamins). Packaging advancements like resealable pouches, a key format, also drive R&D for convenience and waste reduction.

2. How has the Children's Yogurt market recovered post-pandemic?

The market experienced sustained demand post-pandemic due to heightened health awareness and convenience needs for at-home consumption. This trend has contributed to the projected 9.2% CAGR growth.

3. Which are the key product segments in the Children's Yogurt market?

Major product segments include Regular Yogurt, Greek Yogurt, and Drinkable Yogurt. Packaging formats like cups/tubs and pouches are dominant, with pouches specifically catering to on-the-go consumption.

4. How does the regulatory environment impact Children's Yogurt?

Regulations primarily focus on sugar content, allergen labeling, and nutritional claims for children's food. Companies like Danone and Nestlé adapt product formulations to comply with evolving regional dietary guidelines.

5. What significant barriers to entry exist in the Children's Yogurt market?

Significant barriers include high capital investment for production, stringent food safety standards, and established brand loyalty to major players like General Mills (Yoplait) and Chobani. Securing effective distribution channels, especially in supermarkets, also presents a hurdle.

6. What are the major challenges and supply-chain risks for Children's Yogurt?

Challenges include consumer concerns over sugar content, competition from alternative healthy snacks, and potential supply chain disruptions affecting ingredient sourcing. Maintaining product freshness and managing efficient distribution across diverse channels also pose ongoing risks.