Chemical Mechanical Planarization by Equipment Type (CMP Polishing Tools, Cleaning Systems, Monitoring & Metrology Systems, Others), by Material Application (Oxide CMP, Copper CMP, Tungsten CMP, Barrier CMP, Others), by Technology Node (Advanced Node (≤7nm), Mid Node (10–28nm), Mature Node (>28nm)), by End-Use Industry (Logic Semiconductor Manufacturers, Memory Manufacturers (DRAM, NAND), Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 5, 2026|Base Year : 2025|Pages : 102

Srinwanti Kar

Senior Research Analyst

About Sector Data Insights

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Key Insights for Chemical Mechanical Planarization Market

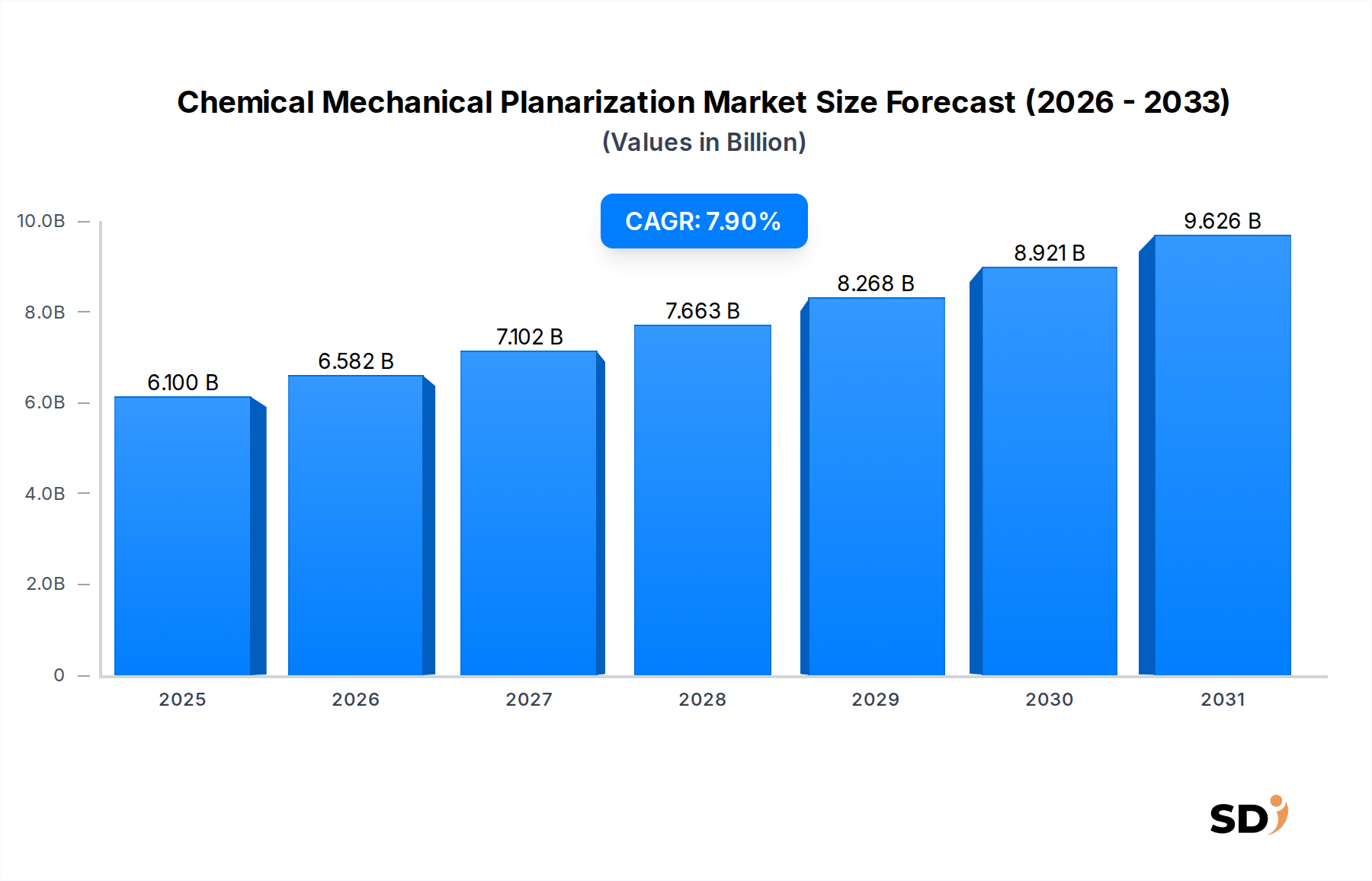

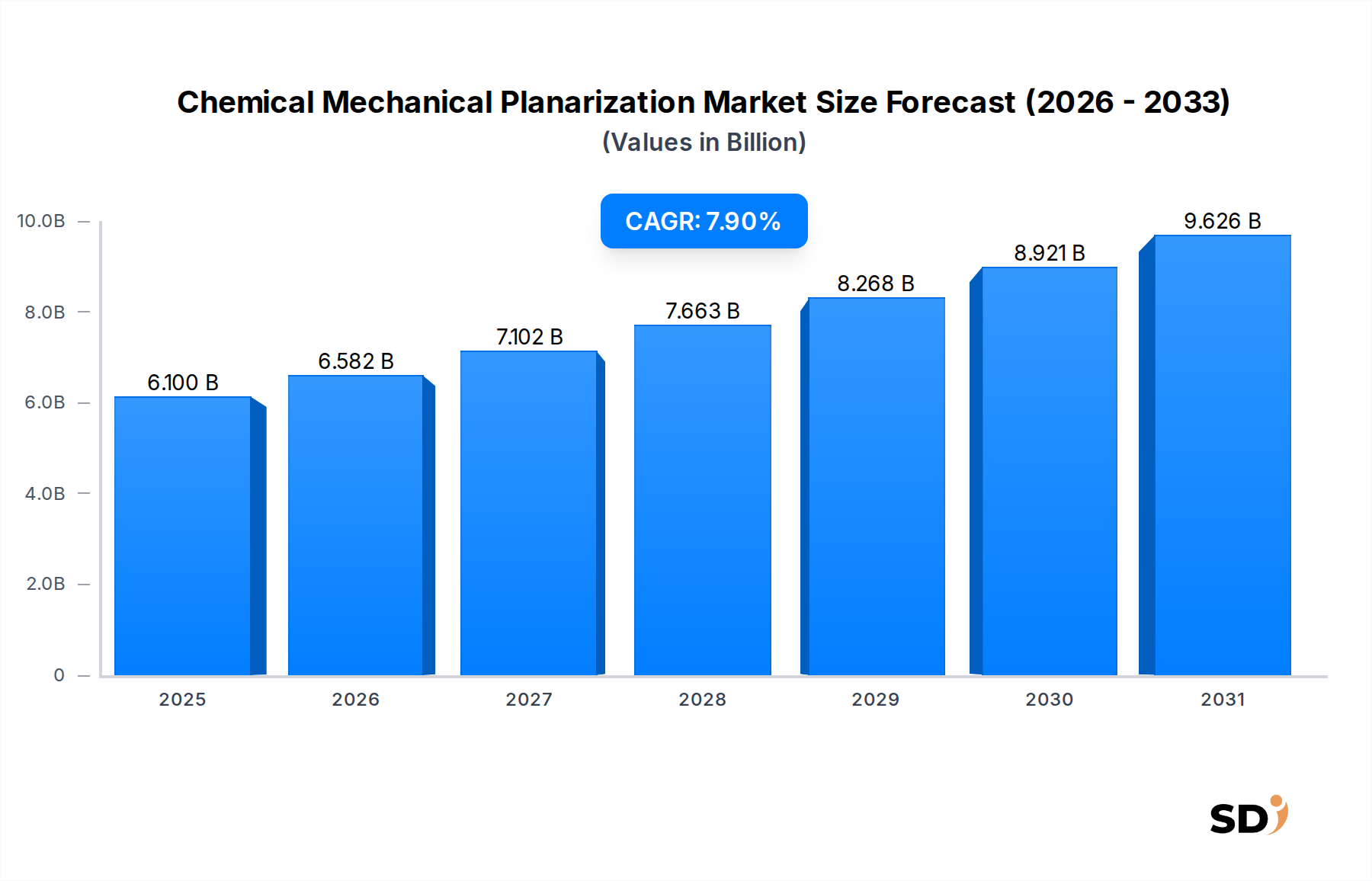

The Chemical Mechanical Planarization Market, a critical enabler of advanced semiconductor fabrication, was valued at approximately $6.1 billion in 2024. Projections indicate a robust expansion, with the market anticipated to grow at a Compound Annual Growth Rate (CAGR) of 7.9% through the forecast period, potentially exceeding $12 billion by 2034. This growth trajectory is fundamentally driven by the relentless pursuit of semiconductor miniaturization, the increasing complexity of 3D integrated circuits (ICs), and the burgeoning demand from high-growth application areas such as artificial intelligence (AI), the Internet of Things (IoT), and high-performance computing (HPC). Chemical Mechanical Planarization (CMP) is an indispensable process in modern microchip manufacturing, responsible for creating ultra-flat surfaces necessary for subsequent photolithography steps, multilayer interconnect formation, and advanced packaging techniques.

Chemical Mechanical Planarization Market Size (In Billion)

10.0B

8.0B

6.0B

4.0B

2.0B

0

6.100 B

2025

6.582 B

2026

7.102 B

2027

7.663 B

2028

8.268 B

2029

8.921 B

2030

9.626 B

2031

The core function of CMP involves meticulously removing excess material to create a uniformly flat surface, a process critical for advanced interconnects (e.g., copper damascene) and shallow trench isolation, thereby supporting segments such as the Oxide CMP Market. The rising complexity of integrated circuits, with an increasing number of metal layers and intricate device architectures, directly correlates with a higher number of CMP steps per wafer. This escalating demand fuels innovation across the entire Chemical Mechanical Planarization Market ecosystem, encompassing specialized CMP Polishing Tools Market, high-purity slurries, and advanced metrology solutions. The need for precise material removal, minimal defectivity, and superior surface quality is more acute than ever, particularly for sub-10nm technology nodes where even atomic-level irregularities can compromise device performance. Key drivers include the transition to larger wafer sizes, the proliferation of heterogeneous integration, and the critical role CMP plays in enabling advanced memory technologies like the DRAM Market and sophisticated processors within the Logic Semiconductor Market. Furthermore, the expanding global Semiconductor Manufacturing Market continues to be the primary engine of growth for CMP consumables and equipment, pushing the boundaries of material science and process control, including continuous advancements in the Slurry Market and Metrology Equipment Market to meet future demands.

Dominant End-Use Segment in Chemical Mechanical Planarization Market

Within the Chemical Mechanical Planarization Market, the 'Logic Semiconductor Manufacturers' segment stands out as the dominant end-use industry by revenue share, a position it is expected to maintain and strengthen throughout the forecast period. This dominance is intrinsically linked to the escalating complexity and performance demands of central processing units (CPUs), graphics processing units (GPUs), and specialized AI accelerators, all of which are foundational to modern computing and data infrastructure. Logic devices, especially those fabricated at advanced technology nodes (≤7nm), require an exceptionally high number of CMP steps to achieve the necessary planarization for multi-patterning lithography, precise interconnect formation, and the integration of diverse materials. Each successive generation of logic chips, driven by innovations in mobile computing, cloud services, and edge AI, intensifies the need for ultra-flat surfaces to minimize defects and ensure reliable device performance.

The intricate architecture of advanced logic chips, featuring numerous dielectric and metal layers, necessitates multiple, highly selective CMP processes. For instance, copper damascene interconnects, crucial for high-speed data transmission within logic devices, rely heavily on precise copper and barrier CMP steps. The ongoing shift towards gate-all-around (GAA) transistors and other novel device structures further complicates planarization requirements, pushing the capabilities of CMP Polishing Tools Market and associated consumables to their limits. This segment also benefits from the substantial capital expenditure by leading logic foundries globally, which are continuously investing in state-of-the-art fabs equipped with the latest CMP technologies. The competitive landscape among logic manufacturers, striving for higher transistor density and improved power efficiency, directly translates into a sustained demand for cutting-edge CMP solutions. As AI and machine learning workloads become more prevalent, the demand for specialized AI chips, which are essentially advanced logic devices, will continue to fuel the expansion of this segment within the broader Semiconductor Manufacturing Market. The precision required for these high-performance devices, coupled with the sheer volume of wafers processed, cements Logic Semiconductor Manufacturers' position as the cornerstone of the Chemical Mechanical Planarization Market.

Key Growth Drivers in Chemical Mechanical Planarization Market

The Chemical Mechanical Planarization Market is propelled by several critical factors, each stemming from the foundational advancements and expanding applications within the semiconductor industry. These drivers necessitate increasing precision, efficiency, and material compatibility in CMP processes.

Miniaturization and Advanced Node Scaling: The relentless pursuit of smaller transistors and denser circuits, particularly for technology nodes of ≤7nm and beyond, is a primary driver. Achieving these dimensions requires extreme planarization to enable multi-patterning techniques (DUV, EUV) without pattern collapse or critical dimension variations. Each new node increases the number of CMP steps required per wafer and elevates the demands for planarity, driving innovation in high-precision CMP Polishing Tools Market and advanced slurries. The ongoing transition to sub-5nm nodes is further intensifying this requirement.

3D Integration and Advanced Packaging: The shift towards 3D device architectures, including 3D NAND flash, 3D DRAM, and heterogeneous integration schemes like chiplets and wafer-on-wafer stacking, significantly increases the total volume of CMP steps. Processes such as interlayer dielectric (ILD) planarization, through-silicon via (TSV) formation, and wafer thinning for stacked ICs are entirely reliant on precise CMP. This trend is a major contributor to the growth in the Advanced Packaging Market, as manufacturers seek to overcome the physical limits of 2D scaling by stacking components vertically.

Rise of AI, IoT, and Automotive Electronics: These rapidly expanding applications demand higher performance, lower power consumption, and greater integration density from their underlying semiconductor components. AI accelerators, specialized microcontrollers for IoT devices, and advanced automotive semiconductors all utilize cutting-edge fabrication processes that depend on high-quality CMP. The proliferation of these smart devices and autonomous systems directly translates into increased production of complex chips, thereby expanding the addressable market for Chemical Mechanical Planarization solutions and the Logic Semiconductor Market.

Increasing Wafer Sizes: The industry's gradual transition to larger wafer diameters (e.g., 300mm) from previous standards (e.g., 200mm) presents new planarization challenges. Maintaining exceptional uniformity and defect control across a significantly larger surface area requires more sophisticated and robust CMP equipment and consumable formulations. This scale-up necessitates higher throughput and greater process control, stimulating demand for advanced CMP systems.

Material Diversity and Complexity: The introduction of novel materials for interconnects (e.g., copper, low-k dielectrics), gates, and device structures necessitates the development of specialized CMP processes and consumables. These new materials often have different mechanical and chemical properties, requiring highly selective and tailored slurries and pads. This continuously drives innovation within the Slurry Market, as suppliers develop formulations to address specific material removal rates and selectivity requirements for diverse applications, including advanced barrier and tungsten CMP processes.

Competitive Ecosystem of Chemical Mechanical Planarization Market

The Chemical Mechanical Planarization Market is characterized by a mix of equipment manufacturers and consumable suppliers, with intense competition driving continuous innovation in process control, materials science, and equipment efficiency. Key players leverage their expertise to cater to the stringent demands of semiconductor fabrication:

DuPont: A leading global supplier of high-performance CMP slurries and polishing pads, critical for achieving precise material removal and surface finish across various semiconductor layers. The company focuses on R&D to develop advanced materials for next-generation technology nodes.

Ebara: A prominent manufacturer of CMP equipment, offering a comprehensive range of polishing systems known for their high precision, throughput, and reliability. Ebara's tools are crucial for various planarization steps in semiconductor fabs globally.

Applied Materials: A dominant force in the broader semiconductor equipment industry, Applied Materials provides integrated CMP solutions, including polishing tools, consumables, and process expertise. The company is at the forefront of driving innovation in integrated process flows and advanced CMP technologies.

Merck KGaA (Versum Materials): A key provider of high-purity process chemicals and advanced materials for semiconductor manufacturing, offering a broad portfolio of CMP slurries and post-CMP cleaning formulations essential for defect control and surface quality.

Fujifilm: Manufactures a wide array of CMP slurries, polishing pads, and cleaning solutions, with a strong presence in critical areas such as copper and oxide planarization. Fujifilm's materials are known for their performance in demanding semiconductor applications.

Fujimi: Specializes in high-performance abrasive materials and slurries specifically engineered for precision applications, including advanced CMP slurries that meet the exacting requirements of leading-edge semiconductor manufacturing processes.

3M: Leverages its extensive material science expertise to supply innovative polishing pads and specialized abrasives for CMP processes, focusing on enhancing uniformity and reducing defectivity.

Entegris: Provides critical materials control solutions, including advanced liquid filtration and purification systems. These are essential for maintaining the purity and consistency of CMP slurries and post-CMP cleaning agents, crucial for yield improvement.

FUJIBO: Offers a diverse portfolio of polishing pads and related materials for various CMP processes, emphasizing solutions that deliver superior planarity and defect performance.

Anji Microelectronics: A significant player in the Chinese domestic market, offering CMP slurries and cleaning solutions, thereby supporting the rapidly expanding local Semiconductor Manufacturing Market and reducing reliance on international suppliers.

Saesol: Specializes in the development and manufacturing of precision polishing pads and advanced material solutions for CMP, catering to the evolving demands of advanced semiconductor fabrication.

AGC: Known for its high-performance glass substrates and specialty materials, AGC also contributes to the Chemical Mechanical Planarization Market through its advanced materials used in CMP processes and other critical semiconductor applications.

Recent Developments & Milestones in Chemical Mechanical Planarization Market

The Chemical Mechanical Planarization Market is continuously evolving with strategic advancements aimed at improving precision, efficiency, and sustainability:

October 2023: Introduction of next-generation CMP polishing tools featuring integrated AI-driven process control. These systems offer real-time monitoring and adaptive planarization capabilities, specifically designed to meet the stringent uniformity and defectivity requirements of ≤7nm technology nodes, significantly enhancing yield.

August 2023: A strategic partnership was formed between a leading CMP equipment manufacturer and a specialized materials supplier. This collaboration focuses on co-developing advanced slurries and pads specifically tailored for novel materials and complex structures in the rapidly expanding Advanced Packaging Market, facilitating heterogeneous integration.

June 2023: Launch of new, environmentally friendly post-CMP Cleaning Systems Market that utilize recycled water and reduced chemical concentrations. These systems are designed for higher efficiency and lower operational costs, directly addressing sustainability concerns within the Chemical Mechanical Planarization Market.

April 2023: Breakthrough in slurry formulation with the introduction of high-selectivity slurries capable of precisely removing specific films in complex 3D NAND structures. This innovation allows for improved control over material removal rates, enabling more intricate device geometries.

February 2023: Significant investment in R&D facilities dedicated to advanced Metrology Equipment Market solutions for real-time in-situ CMP process monitoring. The goal is to develop predictive analytics and feedback loops to minimize process variability and further enhance wafer yield.

December 2022: Expansion of manufacturing capacity for key CMP consumables, including slurries and polishing pads, by a major supplier in the Asia Pacific region. This move responds to the robust growth and increasing localized demand from the Semiconductor Manufacturing Market in countries like China, South Korea, and Taiwan.

September 2022: Collaborative project initiated between key industry players and academic institutions to research and develop novel, greener CMP processes and materials, focusing on minimizing chemical waste and energy consumption across the entire CMP workflow.

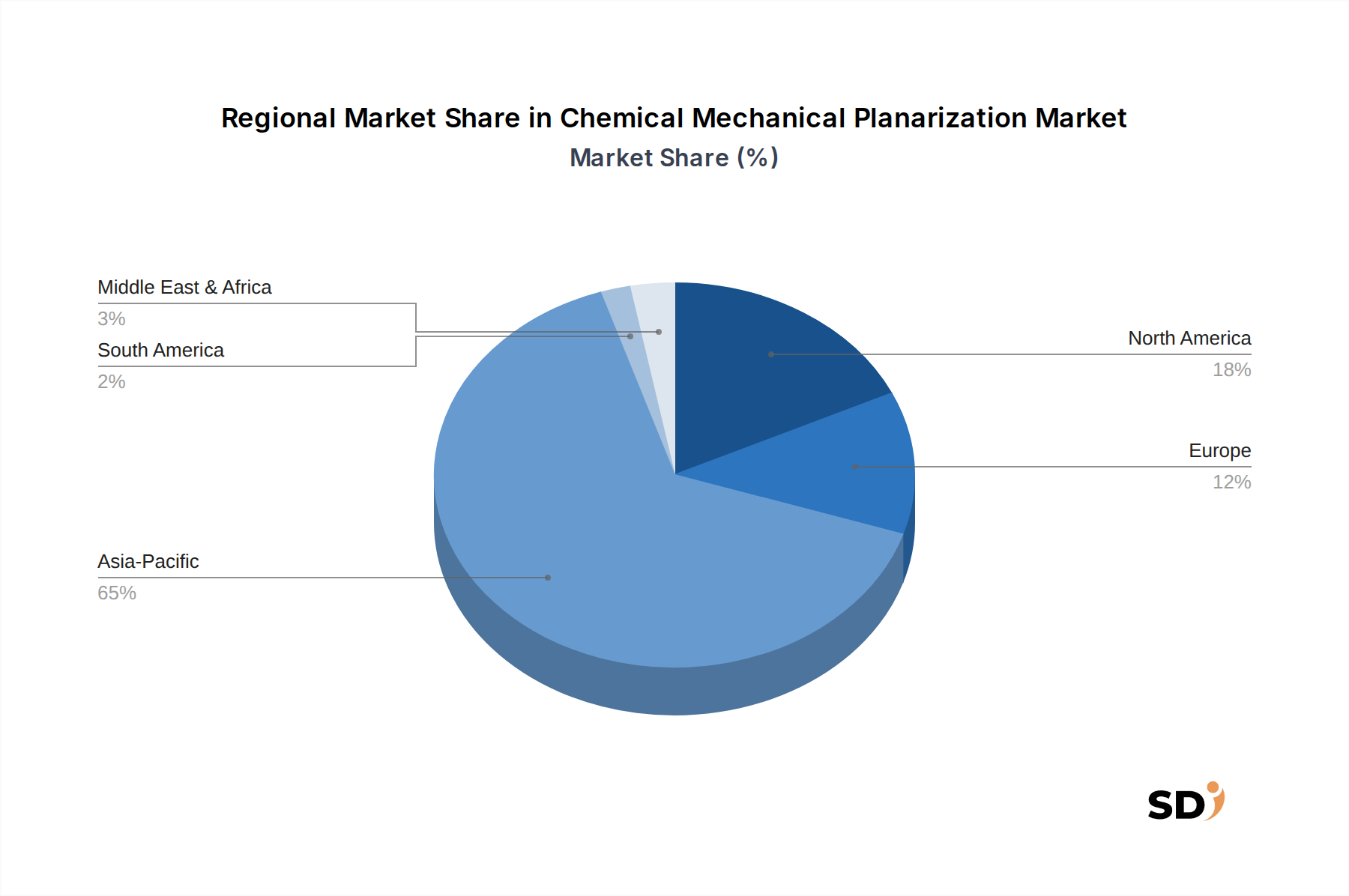

Regional Market Breakdown for Chemical Mechanical Planarization Market

The global Chemical Mechanical Planarization Market exhibits significant regional variations in growth, market share, and technological focus, largely mirroring the global distribution of semiconductor manufacturing capabilities and R&D.

Asia Pacific is poised to maintain its dominant position in the Chemical Mechanical Planarization Market, primarily driven by the robust expansion of the Semiconductor Manufacturing Market across China, South Korea, Japan, and Taiwan. These regions are global hubs for both logic and memory fabrication, including the DRAM Market and Logic Semiconductor Market. The immense investments in new fabs, particularly for advanced node production and increased local sourcing of materials and equipment, underpin this growth. Asia Pacific is expected to command the largest revenue share, potentially exceeding 60% of the global market, fueled by government incentives and increasing domestic demand for electronics.

North America is anticipated to exhibit significant growth, driven by substantial R&D investments and a strong ecosystem for advanced semiconductor design and manufacturing. Recent governmental initiatives aimed at bringing semiconductor manufacturing back onshore are bolstering demand for cutting-edge CMP solutions. This region is a hotbed for innovation in new materials and process technologies, contributing to its robust CAGR, estimated to be around 7.5%, as it focuses on high-value, advanced technology nodes and specialized applications.

Europe is also witnessing steady growth, supported by governmental initiatives like the European Chips Act aimed at increasing semiconductor production capacity and fostering a more resilient supply chain. While smaller in market share compared to Asia Pacific, Europe's focus on specialized industrial applications, automotive electronics, and R&D in materials science (e.g., the Slurry Market) will contribute to its growth, with an estimated CAGR of 6.8%. The region is strengthening its position in niche markets and collaborative research efforts.

The Middle East & Africa and South America regions, while currently representing smaller shares of the overall Chemical Mechanical Planarization Market, are projected to experience accelerating growth. This acceleration is fueled by nascent semiconductor manufacturing initiatives, expanding consumer electronics markets, and increasing integration of advanced technologies. These regions typically lag in adopting the latest technology nodes but are showing increasing demand for mature and mid-node CMP solutions, indicating significant potential for future expansion as local economies develop their technological infrastructure.

Investment & Funding Activity in Chemical Mechanical Planarization Market

The Chemical Mechanical Planarization Market has observed a dynamic landscape of investment and funding activities over the past few years, reflecting the strategic importance of CMP in advanced semiconductor manufacturing. M&A activity has largely focused on consolidating market share, bolstering material science portfolios, and integrating advanced process capabilities. Companies are strategically acquiring smaller firms specializing in novel abrasive materials, specialized pad designs, or innovative slurry formulations to gain a competitive edge in the evolving Slurry Market and enhance their R&D capabilities for next-generation planarization challenges. These acquisitions aim to secure critical supply chains and optimize performance for complex manufacturing processes.

Venture funding rounds have increasingly targeted startups and innovative ventures developing AI-driven process control software and advanced Metrology Equipment Market solutions specifically for CMP. These investments leverage machine learning and data analytics to enable real-time defect detection, predictive maintenance, and optimized polishing parameters. The objective is to achieve higher yields, reduce process variability, and accelerate time-to-market for complex devices in the Logic Semiconductor Market. Sub-segments focused on advanced materials, intelligent sensors, and automation for CMP processes are attracting the most capital, driven by the need for greater precision and efficiency at sub-10nm technology nodes.

Strategic partnerships are becoming increasingly prevalent between equipment manufacturers and material suppliers. These collaborations are essential for co-developing integrated solutions that span from CMP Polishing Tools Market to consumables, ensuring seamless compatibility and optimizing performance for the demanding requirements of advanced manufacturing processes. Furthermore, joint ventures are being explored to address regional supply chain resilience and build local manufacturing capabilities, particularly for critical components in the Advanced Packaging Market, influenced by geopolitical considerations and the desire for diversified production bases. These investments underscore the industry's commitment to innovation and efficiency in a highly competitive environment.

Sustainability & ESG Pressures on Chemical Mechanical Planarization Market

The Chemical Mechanical Planarization Market is facing significant environmental, social, and governance (ESG) pressures, compelling manufacturers and suppliers to innovate towards more sustainable practices. The process is inherently resource-intensive, utilizing substantial amounts of water, various chemicals (e.g., slurries, cleaning agents), and energy, leading to concerns about waste generation and environmental impact. Consequently, environmental regulations are tightening globally, pushing industry players to develop more eco-friendly Cleaning Systems Market designs and advanced slurry formulations that minimize chemical consumption and improve biodegradability.

Carbon reduction targets, driven by global climate change initiatives and corporate commitments, are prompting equipment manufacturers to design more energy-efficient polishing tools. This includes optimizing motor designs, integrating advanced control systems to reduce idle power consumption, and exploring renewable energy sources for manufacturing operations within the Semiconductor Manufacturing Market. Lifecycle assessments (LCAs) are gaining prominence, evaluating the environmental footprint of CMP materials and processes from raw material extraction to end-of-life disposal, encouraging a holistic approach to sustainability.

Circular economy mandates are influencing the industry to explore innovative recycling and reuse strategies for CMP consumables. Research is underway to develop technologies for polishing pad reconditioning, as well as closed-loop systems for slurry management, aiming to significantly reduce waste sent to landfills and conserve valuable resources. This shift also involves redesigning products for easier disassembly and material recovery. Furthermore, ESG investor criteria are increasingly factoring into corporate decisions, compelling companies in the Chemical Mechanical Planarization Market to transparently report on their environmental performance, social responsibility initiatives, and robust governance practices. This heightened scrutiny drives greater accountability and accelerates efforts in sustainable product development and responsible manufacturing across the entire value chain, fostering a culture of continuous improvement in environmental stewardship.

Chemical Mechanical Planarization Segmentation

1. Equipment Type

1.1. CMP Polishing Tools

1.2. Cleaning Systems

1.3. Monitoring & Metrology Systems

1.4. Others

2. Material Application

2.1. Oxide CMP

2.2. Copper CMP

2.3. Tungsten CMP

2.4. Barrier CMP

2.5. Others

3. Technology Node

3.1. Advanced Node (≤7nm)

3.2. Mid Node (10–28nm)

3.3. Mature Node (>28nm)

4. End-Use Industry

4.1. Logic Semiconductor Manufacturers

4.2. Memory Manufacturers (DRAM, NAND)

4.3. Others

Chemical Mechanical Planarization Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Chemical Mechanical Planarization REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 7.9% from 2020-2034

Segmentation

By Equipment Type

CMP Polishing Tools

Cleaning Systems

Monitoring & Metrology Systems

Others

By Material Application

Oxide CMP

Copper CMP

Tungsten CMP

Barrier CMP

Others

By Technology Node

Advanced Node (≤7nm)

Mid Node (10–28nm)

Mature Node (>28nm)

By End-Use Industry

Logic Semiconductor Manufacturers

Memory Manufacturers (DRAM, NAND)

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Equipment Type

5.1.1. CMP Polishing Tools

5.1.2. Cleaning Systems

5.1.3. Monitoring & Metrology Systems

5.1.4. Others

5.2. Market Analysis, Insights and Forecast - by Material Application

5.2.1. Oxide CMP

5.2.2. Copper CMP

5.2.3. Tungsten CMP

5.2.4. Barrier CMP

5.2.5. Others

5.3. Market Analysis, Insights and Forecast - by Technology Node

5.3.1. Advanced Node (≤7nm)

5.3.2. Mid Node (10–28nm)

5.3.3. Mature Node (>28nm)

5.4. Market Analysis, Insights and Forecast - by End-Use Industry

5.4.1. Logic Semiconductor Manufacturers

5.4.2. Memory Manufacturers (DRAM, NAND)

5.4.3. Others

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Equipment Type

6.1.1. CMP Polishing Tools

6.1.2. Cleaning Systems

6.1.3. Monitoring & Metrology Systems

6.1.4. Others

6.2. Market Analysis, Insights and Forecast - by Material Application

6.2.1. Oxide CMP

6.2.2. Copper CMP

6.2.3. Tungsten CMP

6.2.4. Barrier CMP

6.2.5. Others

6.3. Market Analysis, Insights and Forecast - by Technology Node

6.3.1. Advanced Node (≤7nm)

6.3.2. Mid Node (10–28nm)

6.3.3. Mature Node (>28nm)

6.4. Market Analysis, Insights and Forecast - by End-Use Industry

6.4.1. Logic Semiconductor Manufacturers

6.4.2. Memory Manufacturers (DRAM, NAND)

6.4.3. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Equipment Type

7.1.1. CMP Polishing Tools

7.1.2. Cleaning Systems

7.1.3. Monitoring & Metrology Systems

7.1.4. Others

7.2. Market Analysis, Insights and Forecast - by Material Application

7.2.1. Oxide CMP

7.2.2. Copper CMP

7.2.3. Tungsten CMP

7.2.4. Barrier CMP

7.2.5. Others

7.3. Market Analysis, Insights and Forecast - by Technology Node

7.3.1. Advanced Node (≤7nm)

7.3.2. Mid Node (10–28nm)

7.3.3. Mature Node (>28nm)

7.4. Market Analysis, Insights and Forecast - by End-Use Industry

7.4.1. Logic Semiconductor Manufacturers

7.4.2. Memory Manufacturers (DRAM, NAND)

7.4.3. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Equipment Type

8.1.1. CMP Polishing Tools

8.1.2. Cleaning Systems

8.1.3. Monitoring & Metrology Systems

8.1.4. Others

8.2. Market Analysis, Insights and Forecast - by Material Application

8.2.1. Oxide CMP

8.2.2. Copper CMP

8.2.3. Tungsten CMP

8.2.4. Barrier CMP

8.2.5. Others

8.3. Market Analysis, Insights and Forecast - by Technology Node

8.3.1. Advanced Node (≤7nm)

8.3.2. Mid Node (10–28nm)

8.3.3. Mature Node (>28nm)

8.4. Market Analysis, Insights and Forecast - by End-Use Industry

8.4.1. Logic Semiconductor Manufacturers

8.4.2. Memory Manufacturers (DRAM, NAND)

8.4.3. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Equipment Type

9.1.1. CMP Polishing Tools

9.1.2. Cleaning Systems

9.1.3. Monitoring & Metrology Systems

9.1.4. Others

9.2. Market Analysis, Insights and Forecast - by Material Application

9.2.1. Oxide CMP

9.2.2. Copper CMP

9.2.3. Tungsten CMP

9.2.4. Barrier CMP

9.2.5. Others

9.3. Market Analysis, Insights and Forecast - by Technology Node

9.3.1. Advanced Node (≤7nm)

9.3.2. Mid Node (10–28nm)

9.3.3. Mature Node (>28nm)

9.4. Market Analysis, Insights and Forecast - by End-Use Industry

9.4.1. Logic Semiconductor Manufacturers

9.4.2. Memory Manufacturers (DRAM, NAND)

9.4.3. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Equipment Type

10.1.1. CMP Polishing Tools

10.1.2. Cleaning Systems

10.1.3. Monitoring & Metrology Systems

10.1.4. Others

10.2. Market Analysis, Insights and Forecast - by Material Application

10.2.1. Oxide CMP

10.2.2. Copper CMP

10.2.3. Tungsten CMP

10.2.4. Barrier CMP

10.2.5. Others

10.3. Market Analysis, Insights and Forecast - by Technology Node

10.3.1. Advanced Node (≤7nm)

10.3.2. Mid Node (10–28nm)

10.3.3. Mature Node (>28nm)

10.4. Market Analysis, Insights and Forecast - by End-Use Industry

10.4.1. Logic Semiconductor Manufacturers

10.4.2. Memory Manufacturers (DRAM, NAND)

10.4.3. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. DuPont

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Ebara

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Applied Materials

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Merck KGaA (Versum Materials)

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Fujifilm

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Fujimi

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. 3M

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Entegris

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. FUJIBO

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Anji Microelectronics

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Saesol

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. AGC

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Equipment Type 2025 & 2033

Figure 3: Revenue Share (%), by Equipment Type 2025 & 2033

Figure 4: Revenue (billion), by Material Application 2025 & 2033

Figure 5: Revenue Share (%), by Material Application 2025 & 2033

Figure 6: Revenue (billion), by Technology Node 2025 & 2033

Table 50: Revenue billion Forecast, by End-Use Industry 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is designed to gather critical, real-time insights directly from industry experts, forming the bedrock of our analysis. This robust approach constitutes approximately 75% of our total research effort, ensuring a profound understanding of market dynamics, emerging trends, and competitive landscapes. We conduct in-depth interviews and discussions with a diverse range of stakeholders across the Chemical Mechanical Planarization (CMP) value chain. These interactions provide qualitative validation, uncover nuances, and offer forward-looking perspectives that are often unavailable through secondary sources.

Key stakeholders engaged in our primary research include:

VP/Director of Process Engineering (CMP): Providing insights into operational challenges, technology adoption, and performance requirements at semiconductor manufacturing fabs.

Product Manager/Director (CMP Tools/Consumables): Offering perspectives on product development pipelines, market positioning, and customer demand from equipment and material suppliers.

Senior Research Scientist/Technologist (Advanced Materials/Processes): Contributing expertise on R&D trends, material science innovations, and the technological roadmap for next-generation CMP.

Supply Chain Director/Manager (Semiconductor Manufacturing): Detailing procurement strategies, vendor relationships, and supply chain resilience within the CMP ecosystem.

Our primary research participants are drawn from a strategic mix of company types essential to the CMP market:

CMP Equipment Manufacturers: Companies specializing in polishing tools, cleaning systems, and monitoring & metrology equipment.

CMP Slurry and Pad Manufacturers: Key suppliers of critical consumables used in the CMP process.

Advanced Semiconductor Device Manufacturers (Foundries/IDMs): Major end-users, including logic and memory fabs, driving demand for CMP solutions.

Specialty Chemical and Materials Suppliers: Providers of raw materials and precursor chemicals used in CMP slurries and pads.

Semiconductor Metrology and Inspection System Providers: Companies offering tools vital for process control and quality assurance in CMP.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP/Director of Process Engineering (CMP)

35%

Product Manager/Director (CMP Tools/Consumables)

30%

Senior Research Scientist/Technologist (Advanced Materials/Processes)

Semiconductor Metrology and Inspection System Providers

10%

Secondary Research & Industry Benchmarking

The remaining 25% of our research is dedicated to comprehensive secondary research, which serves to establish the initial market landscape, validate primary findings, and provide foundational data. This phase involves extensive data gathering from a multitude of credible public and proprietary sources, ensuring a well-rounded and verifiable dataset.

Our secondary research leverages renowned financial databases for company intelligence, market reports, and competitive analysis, including:

Bloomberg

Factiva

Hoovers

PitchBook

Additionally, we meticulously analyze data from official government publications (.Gov), organizational reports (.org), and recognized trade associations. We strictly avoid data from other market research websites to maintain the independence and originality of our findings. Examples of key secondary data sources and relevant industry bodies include:

Government publications and statistical agencies (e.g., U.S. Department of Commerce, European Commission).

Industry reports and technical papers from globally recognized organizations such as:

SEMI (Semiconductor Equipment and Materials International) (Source Link)

The International Roadmap for Devices and Systems (IRDS) (Source Link)

World Semiconductor Trade Statistics (WSTS) (Source Link)

National Institute of Standards and Technology (NIST) (Source Link)

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies integrate both top-down and bottom-up approaches, triangulated for robust estimation. This dual strategy ensures accuracy by accounting for macro-economic factors and detailed micro-level market drivers.

Top-Down Approach: We commence with an analysis of the overall semiconductor industry growth, global economic indicators, and investment trends impacting capital expenditure in semiconductor manufacturing. This macro-level view is then disaggregated to estimate the total CMP market size, subsequently segmented by equipment type, material application, technology node, and end-use industry, and region.

Bottom-Up Approach: Simultaneously, we build the market size by aggregating data from the granular level. This involves analyzing specific demand drivers and supply-side capabilities. Key metrics and variables used for our bottom-up market sizing include:

Number of Wafer Starts per Fab/Technology Node: Directly correlating with the volume of CMP processes required.

Average Number of CMP Steps per Wafer (by technology node and material application): Advanced nodes and complex device structures require multiple CMP steps, influencing demand for equipment and consumables.

Average Selling Price (ASP) of CMP Equipment (by type): Used for valuing the equipment market segment.

Consumption Rate and Cost of CMP Consumables (slurries, pads) per wafer pass: Essential for calculating the material application market size.

Multi-level data triangulation involves cross-referencing estimates derived from these two approaches with insights from primary interviews and validated secondary sources. This iterative process refines market figures, ensuring consistency and accuracy across all segments for the forecast period of 2026-2034, with particular attention to technology nodes (Advanced Node (≤7nm), Mid Node (10–28nm), Mature Node (>28nm)).

Data Accuracy & Quality Check

We are committed to delivering highly reliable and actionable market intelligence. Our stringent data validation and quality assurance processes guarantee an estimated data accuracy level of 85-90%. Every data point, trend, and forecast is subjected to rigorous cross-validation through multiple sources and expert panel reviews.

The quality check process includes:

Consistency Checks: Ensuring data consistency across different segments, regions, and methodologies.

Peer Review: Internal review by senior analysts to scrutinize assumptions, calculations, and interpretations.

Expert Validation: Final validation through targeted discussions with industry experts to confirm market dynamics and future projections.

Real-time Updates: Our market intelligence is continually updated, reflecting the latest market developments and data available up to the date of purchase, providing our clients with the most current insights.

Frequently Asked Questions

1. What are the key raw material sourcing considerations for CMP?

Chemical Mechanical Planarization relies heavily on slurries, pads, and cleaning agents. Suppliers like DuPont and Fujimi are critical for high-purity consumables. Supply chain stability, especially for specialty chemicals, impacts production efficiency across logic and memory fabs.

2. What major challenges impact the Chemical Mechanical Planarization market?

The Chemical Mechanical Planarization market faces challenges related to achieving extreme planarization uniformity at advanced nodes (≤7nm). High R&D investment and increasing material purity demands, crucial for reducing defects, represent significant operational restraints for manufacturers.

3. How do regulations affect the Chemical Mechanical Planarization market?

Chemical Mechanical Planarization operations are subject to stringent environmental and safety regulations for chemical handling and waste disposal. Compliance with global and regional hazardous material standards, alongside worker safety protocols, directly influences manufacturing costs and process development for companies such as Applied Materials.

4. Who are the leading companies in the Chemical Mechanical Planarization market?

The Chemical Mechanical Planarization market features key players such as DuPont, Applied Materials, Ebara, and Merck KGaA. Competition revolves around innovation in CMP polishing tools, slurries, and advanced process solutions, particularly for sub-7nm technology nodes.

5. How are purchasing trends evolving for Chemical Mechanical Planarization equipment and materials?

Purchasing trends in Chemical Mechanical Planarization are shifting towards solutions optimized for advanced node (≤7nm) manufacturing, driven by logic and memory semiconductor demand. Customers prioritize higher throughput, reduced defectivity, and lower total cost of ownership in CMP polishing tools and consumables.

6. What are the key sustainability factors in the Chemical Mechanical Planarization industry?

Sustainability in Chemical Mechanical Planarization focuses on reducing water consumption, optimizing chemical usage, and managing hazardous waste generated by slurries. Companies are investing in closed-loop systems and developing environmentally friendlier consumables to minimize the industry's ecological footprint.