Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Bovine Embryo Services by Service Type (Embryo Collection, Embryo Transfer, In Vitro Fertilization (IVF) Services, Embryo Freezing & Storage, Genetic Testing & Screening, Others), by Technique (In Vivo Embryo Production, In Vitro Embryo Production (IVP)), by Application (Genetic Improvement, Disease Control, Herd Expansion, Research & Development), by Service Provider (Private Service Providers, Veterinary Service Providers, Research Organizations), by End-User (Dairy Farms, Beef Farms, Veterinary Clinics, Research Institutes), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 4, 2026|Base Year : 2025|Pages : 101

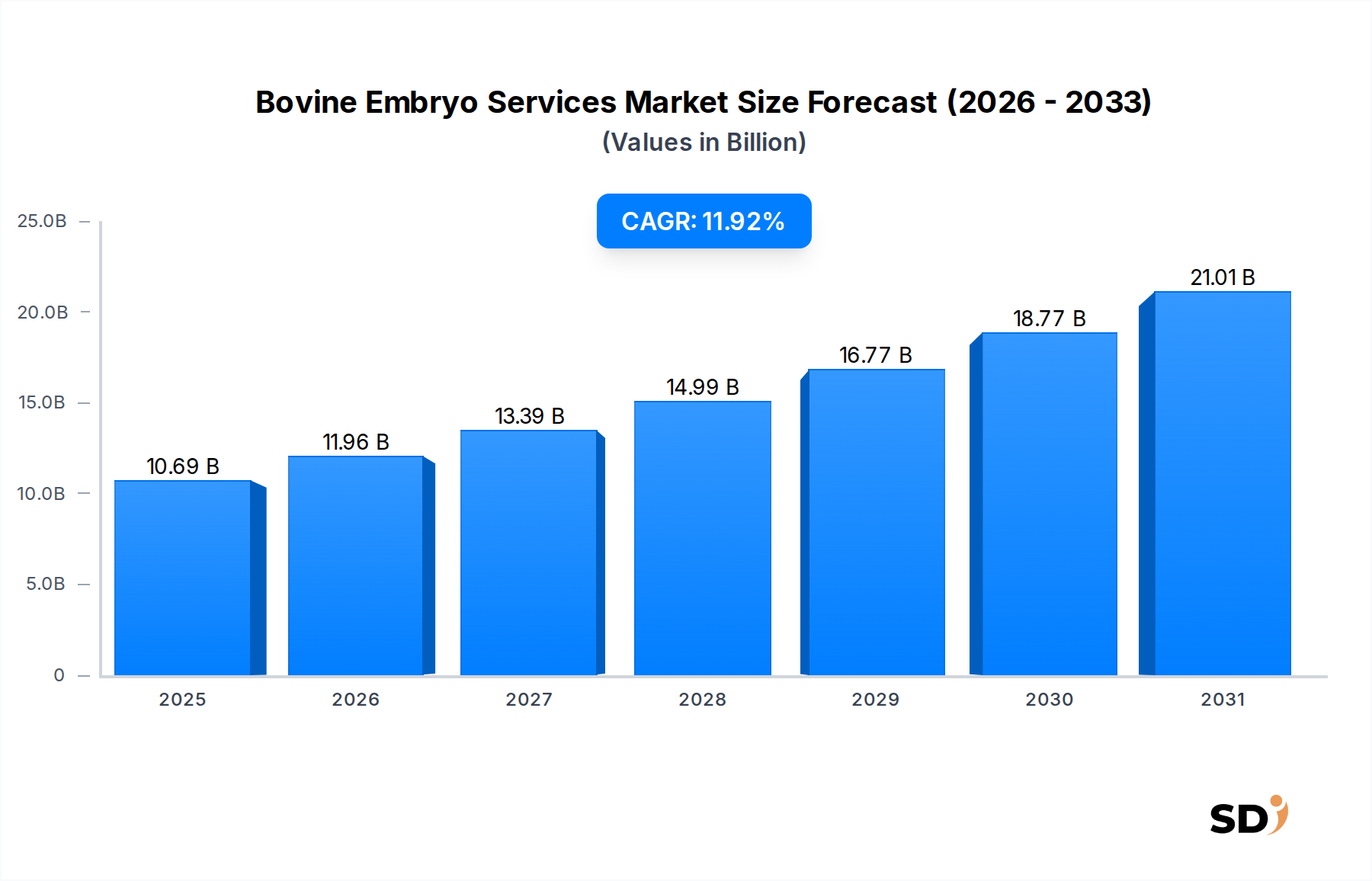

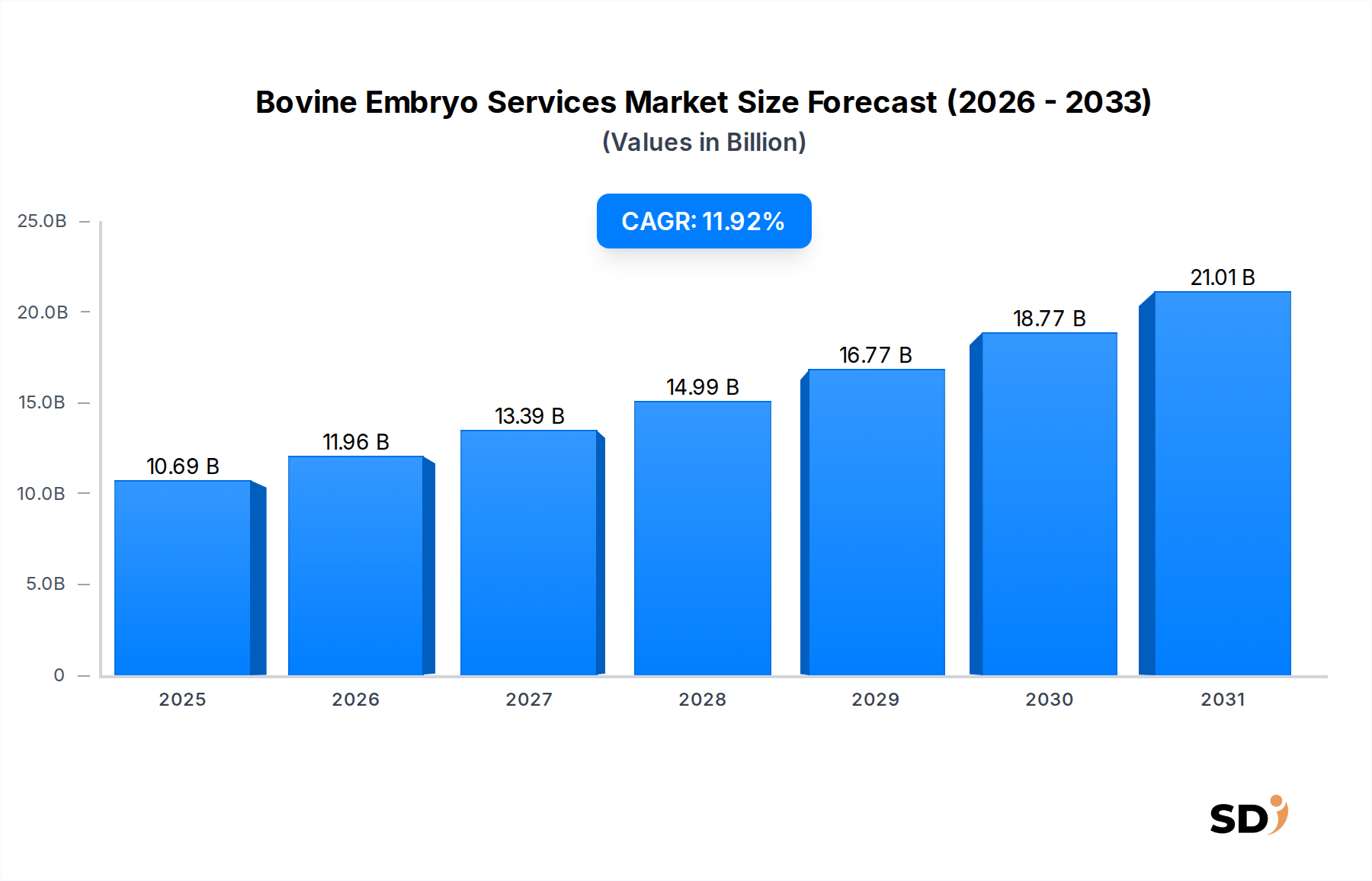

The Bovine Embryo Services Market is poised for substantial expansion, reflecting the global livestock industry's intensified focus on genetic improvement, herd health, and productivity optimization. Valued at $10.69 billion in the base year 2025, the market is projected to grow at an impressive Compound Annual Growth Rate (CAGR) of 11.92%. This robust growth trajectory is expected to elevate the market to approximately $26.18 billion by 2033, indicating a dynamic landscape driven by technological advancements and commercial viability.

Bovine Embryo Services Market Size (In Billion)

25.0B

20.0B

15.0B

10.0B

5.0B

0

10.69 B

2025

11.96 B

2026

13.39 B

2027

14.99 B

2028

16.77 B

2029

18.77 B

2030

21.01 B

2031

The core drivers underpinning this growth include the escalating global demand for high-quality dairy and beef products, necessitating advanced breeding techniques to enhance genetic merit. The increasing adoption of assisted reproductive technologies (ARTs) such as In Vitro Fertilization (IVF) and embryo transfer across major cattle-producing regions significantly contributes to market expansion. Furthermore, the imperative for disease control and biosecurity, coupled with the desire for rapid herd multiplication of superior genetics, propels the Bovine Embryo Services Market forward. Macroeconomic tailwinds, including supportive government policies for livestock development and increasing investments in animal health research, further strengthen the market's foundation. The integration of cutting-edge genomic selection tools and reproductive synchronization protocols allows for more precise and efficient breeding programs. The increasing sophistication of the Dairy Farming Market and the broader Livestock Breeding Market is directly influencing the demand for these specialized services. Emerging markets, particularly in Asia Pacific and South America, are witnessing a surge in commercial farming operations adopting these services to boost their yield and quality, thereby contributing significantly to revenue growth. The ongoing research and development in cryopreservation techniques and embryo assessment tools are also enhancing the efficacy and accessibility of bovine embryo services. The market's future outlook remains highly positive, characterized by continuous innovation and strategic partnerships aimed at broadening service portfolios and geographic reach.

In Vitro Embryo Production Dominance in Bovine Embryo Services Market

Within the Bovine Embryo Services Market, the In Vitro Embryo Production (IVP) technique segment stands out as a dominant force, commanding a significant revenue share due to its inherent advantages in accelerating genetic progress and enhancing reproductive efficiency. IVP involves the maturation of oocytes (immature egg cells) in a laboratory setting, followed by fertilization with selected semen and subsequent culture of the embryos before transfer or cryopreservation. This technique has revolutionized bovine breeding by overcoming many limitations associated with traditional in vivo methods.

The primary reasons for IVP's dominance include its ability to utilize genetics from a wider pool of donor animals, including those that may have reproductive challenges in vivo. It enables the production of a larger number of embryos per donor, per collection cycle, significantly shortening generational intervals and rapidly multiplying superior genetics. This is particularly critical for high-value breeding programs focused on traits like increased milk yield, improved feed conversion, disease resistance, and desirable carcass characteristics. Furthermore, IVP offers enhanced biosecurity, as embryos can be screened for diseases, minimizing the risk of pathogen transmission, a key concern for the Animal Health Diagnostics Market. The global demand for animal protein, driven by a burgeoning human population, places immense pressure on the Livestock Breeding Market to maximize productivity, making IVP an indispensable tool for intensive livestock operations. The advancements in media development, culture conditions, and laboratory protocols have consistently improved IVP success rates, making it a more reliable and cost-effective option for many producers.

Key players in the Bovine Embryo Services Market, such as Vytelle, Boviteq, and In Vitro Brasil S.A., have invested heavily in optimizing IVP protocols and expanding their service offerings. These companies are at the forefront of integrating new technologies, including artificial intelligence for embryo grading and sexing, to further enhance the efficiency and precision of IVP. While initial costs for IVP can be higher than conventional breeding, the long-term genetic gains and accelerated herd improvement often justify the investment, particularly for large-scale Dairy Farming Market and beef operations. The segment's share is not merely growing but is also consolidating, as service providers with advanced laboratory infrastructure and skilled embryologists are gaining a competitive edge. The increasing global acceptance and commercialization of IVP, driven by both private enterprises and research institutions, underscore its pivotal role in shaping the future of the Bovine Embryo Services Market and broader Animal Biotechnology Market.

Advancements and Regulatory Shifts Driving Bovine Embryo Services Market Growth

The Bovine Embryo Services Market is primarily driven by a confluence of technological advancements and strategic shifts in livestock management. One significant driver is the relentless pursuit of genetic improvement in both dairy and beef herds. For instance, the demand for embryos from genetically superior animals, validated through comprehensive genetic testing, has surged. This focus allows farms to rapidly propagate desirable traits such as higher milk production, faster growth rates, and increased disease resistance, directly impacting their profitability. The integration of advanced genomic selection tools with assisted reproductive technologies means that a new generation of cattle with superior traits can be introduced into herds at an unprecedented pace, bolstering the Genetic Testing Services Market.

Another critical driver is the imperative for rapid herd expansion and disease control. Embryo transfer, particularly from high-health status donors, minimizes the risk of vertical disease transmission compared to the movement of live animals. This aspect is vital for maintaining biosecurity in valuable herds and mitigating economic losses due to outbreaks. According to recent agricultural reports, regions facing significant disease challenges are increasingly adopting embryo services as a biosecure breeding strategy. Furthermore, the global demand for beef and dairy products continues to climb, spurring livestock producers to enhance their reproductive efficiency. Techniques like In Vitro Fertilization Market have become more accessible and efficient, enabling the production of a greater number of embryos from valuable donor animals, thus accelerating herd growth and improving productivity. This direct correlation with global food security trends underscores the market's fundamental importance.

However, the market also faces constraints. The high cost associated with these advanced services remains a barrier for smaller farm operations, limiting wider adoption despite the long-term benefits. Additionally, the Bovine Embryo Services Market requires highly specialized veterinary expertise and sophisticated laboratory infrastructure, which can be scarce in developing regions. Ethical considerations surrounding animal welfare and genetic modification also present ongoing challenges, necessitating continuous dialogue and adherence to best practices to maintain public trust. Lastly, variations in regulatory frameworks across different countries for the import and export of bovine embryos can create logistical hurdles, impacting international trade and market harmonization. For example, strict health protocols and certification requirements for the Embryo Transfer Services Market often vary significantly by region, posing challenges for global service providers.

Competitive Ecosystem of Bovine Embryo Services Market

ABS Global: A leading player in bovine genetics and reproduction, offering a comprehensive suite of services including genetic selection, semen, and embryo products, aimed at enhancing herd productivity and profitability for dairy and beef producers worldwide.

Genus plc: Specializes in animal genetics, providing breeding animals, semen, and embryos for both dairy and beef cattle through its PIC and ABS Global subsidiaries, focusing on genetic improvement and sustainable livestock production.

STgenetics: Innovator in bovine reproductive technologies, known for its sex-sorted semen and IVF services, which enable producers to control the sex of offspring and accelerate genetic progress in their herds.

Select Sires Inc.: A farmer-owned cooperative dedicated to providing high-quality genetics and reproductive solutions, offering semen and embryo services to improve the profitability and efficiency of dairy and beef operations.

Semex Alliance: A global leader in artificial insemination and genetics, offering a broad portfolio of breeding solutions, including advanced genetics and reproductive management programs, to dairy and beef producers.

CRV Holding B.V.: An international cooperative focused on cattle improvement, providing genetics, data management, and breeding advice, with a strong emphasis on health, efficiency, and sustainability in the dairy sector.

Trans Ova Genetics: A prominent provider of bovine embryo transfer and in vitro fertilization services, offering advanced reproductive technologies to maximize the genetic potential of beef and dairy cattle.

Vytelle: Specializes in accelerating genetic progress through its advanced in vitro fertilization platform, enabling rapid multiplication of superior genetics for the global beef and dairy industries.

Boviteq: A subsidiary of Semex, Boviteq is a leader in bovine in vitro fertilization (IVF) technology, offering cutting-edge embryo production services to enhance genetic gain for cattle breeders.

In Vitro Brasil S.A.: A major player in bovine in vitro fertilization in Latin America, providing advanced reproductive biotechnologies and genetic solutions to improve the productivity and quality of cattle herds in the region.

Recent Developments & Milestones in Bovine Embryo Services Market

Q4 2024: A prominent market player announced the launch of a new AI-powered platform for embryo grading, designed to improve the accuracy and consistency of embryo selection, thereby enhancing success rates for In Vitro Fertilization Market services.

Q2 2205: A leading genetic company forged a strategic partnership with a major veterinary service provider to expand its Embryo Transfer Services Market offerings into emerging markets in Southeast Asia, focusing on enhancing local dairy and beef production capabilities.

Q1 2026: Regulatory authorities in the European Union approved a novel cryopreservation media formulation, promising improved embryo viability and reduced cellular damage during freezing and thawing processes, which is set to boost the efficiency of long-term embryo storage.

Q3 2025: An investment firm specializing in Animal Biotechnology Market ventures injected significant capital into a startup focused on developing non-invasive genetic testing solutions for bovine embryos, aiming to identify genetic traits and potential diseases pre-implantation.

Q4 2024: A key industry participant acquired a specialized laboratory equipment manufacturer to enhance its in-house capabilities for developing and producing advanced instruments critical for the Bovine Embryo Services Market, such as micro-manipulators and incubators.

Q1 2025: Researchers announced a breakthrough in gene-editing techniques applicable to bovine embryos, potentially opening avenues for enhancing disease resistance and productivity traits, although commercial application remains years away.

Q2 2026: A consortium of universities and private companies secured funding for a multi-year research project aimed at understanding the epigenetic effects of in vitro embryo production on calf health and performance, addressing long-term concerns within the Bovine Embryo Services Market.

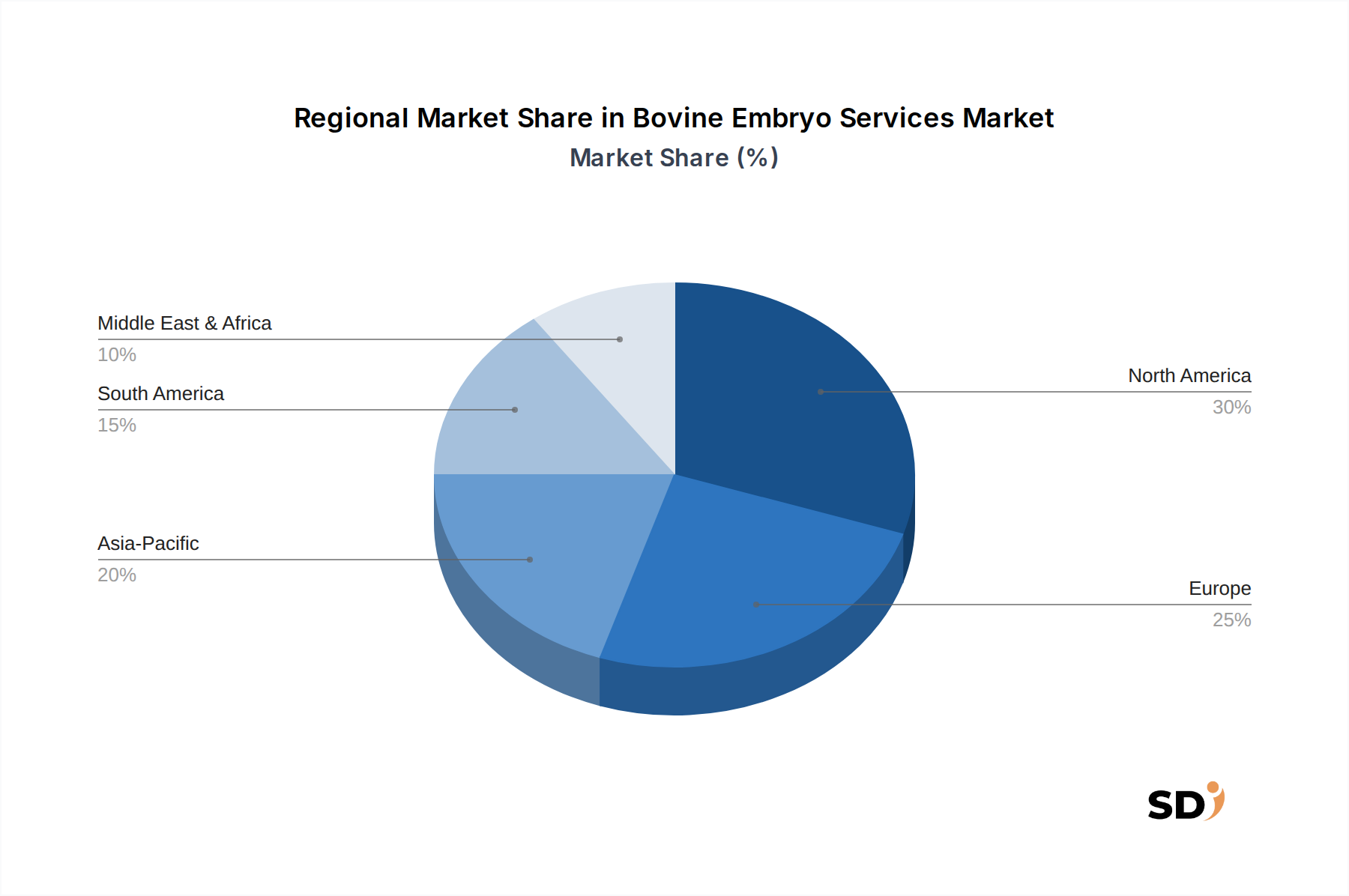

Regional Market Breakdown for Bovine Embryo Services Market

The Bovine Embryo Services Market exhibits distinct regional dynamics driven by varying agricultural practices, economic development, and technological adoption rates. North America, encompassing the United States, Canada, and Mexico, represents a mature and significant market segment. The region benefits from a robust livestock industry, high adoption rates of advanced reproductive technologies, and substantial investments in genetic research. Farmers in North America consistently seek genetic improvement for enhanced productivity and disease resistance, fueling demand for services such as Embryo Transfer Services Market and Genetic Testing Services Market. The presence of key market players and a well-established veterinary infrastructure further solidify its market position.

Europe, including countries like Germany, France, and the UK, also holds a substantial share in the Bovine Embryo Services Market. This region is characterized by stringent animal welfare regulations, a strong emphasis on sustainable farming practices, and continuous innovation in animal genetics. While growth might be more stable compared to rapidly expanding regions, the consistent demand for high-quality dairy and beef, coupled with a focus on herd health and efficiency, drives the market. The Benelux and Nordics regions are notable for their advanced research in animal biotechnology.

Asia Pacific is projected to be the fastest-growing region in the Bovine Embryo Services Market. Countries such as China, India, and Japan are witnessing a rapid increase in demand for dairy and meat products, leading to large-scale investments in modernizing their livestock sectors. Government initiatives to improve the genetic pool of local cattle breeds and the expanding commercial dairy and beef farming operations are primary demand drivers. The adoption of technologies like In Vitro Fertilization Market is accelerating, offering immense growth opportunities for service providers. The sheer scale of the Dairy Farming Market in countries like India presents a vast untapped potential.

South America, particularly Brazil and Argentina, represents a dynamically growing segment due to its vast cattle populations and significant beef export industry. The focus here is increasingly on genetic improvement to enhance production efficiency and meet international market demands. While cost-sensitivity remains a factor, the increasing awareness of the long-term benefits of embryo services is driving adoption. The Middle East & Africa region is also showing nascent growth, driven by efforts to reduce reliance on imports and develop local food security, with GCC countries leading in technological adoption. The global landscape indicates a market moving towards widespread adoption, with regional nuances dictating specific growth patterns and technological preferences.

Investment & Funding Activity in Bovine Embryo Services Market

Investment and funding activities within the Bovine Embryo Services Market have shown a consistent upward trend over the past two to three years, signaling strong investor confidence in the sector's long-term potential. Much of this capital is directed towards companies specializing in advanced reproductive technologies, particularly those innovating in In Vitro Fertilization Market (IVF) and genetic selection. Venture capital firms are increasingly looking at startups that leverage artificial intelligence and machine learning for embryo assessment, genetic data analytics, and predictive breeding, aiming to enhance efficiency and success rates in the Livestock Breeding Market.

Strategic partnerships between large animal health companies and specialized embryo service providers are a common theme, often focusing on expanding geographical reach or integrating new genetic testing capabilities. For instance, partnerships aimed at establishing new IVF laboratories in high-growth regions like Asia Pacific or Latin America have attracted significant capital, as these areas represent substantial untapped markets for genetic improvement in the Dairy Farming Market and beef sectors. Mergers and acquisitions (M&A) have also played a role, with larger players acquiring smaller, innovative firms to consolidate market share, gain access to proprietary technologies, or broaden their service portfolios. Sub-segments attracting the most capital include those involved in advanced cryopreservation techniques, genomics for precision breeding, and platforms that integrate multiple reproductive technologies. Investors are drawn to the potential for high returns through accelerated genetic gain, improved animal health, and increased productivity, all of which contribute to global food security.

Supply Chain & Raw Material Dynamics for Bovine Embryo Services Market

The supply chain for the Bovine Embryo Services Market is complex, relying on a diverse array of specialized inputs and highly skilled personnel. Upstream dependencies include the sourcing of high-quality Reproductive Hormones Market (such as FSH and prostaglandin) essential for superovulation in donor animals and synchronization in recipients. The availability and price stability of these pharmaceutical-grade hormones are critical, as fluctuations can directly impact the cost and scheduling of embryo collection and transfer procedures. Another key input is the specialized media and reagents used for in vitro embryo production, cryopreservation, and handling. These include cell culture media, serum substitutes, and cryoprotectants, which require stringent quality control and often proprietary formulations.

Sourcing risks are primarily associated with the global supply chain for these specialized chemicals and biologics. Geopolitical events, trade restrictions, or disruptions in chemical manufacturing can lead to shortages or price volatility, impacting service providers. The intellectual property rights associated with specific media formulations or genetic testing reagents also play a role in market dynamics. Furthermore, the market relies on a steady supply of high-grade Veterinary Consumables Market such as catheters, syringes, sterile gloves, and laboratory disposables, which are sensitive to general medical supply chain disruptions. Specialized equipment, including microscopes, incubators, micro-manipulators, and cryostorage tanks, represents another significant upstream dependency, often sourced from a limited number of global manufacturers.

Historically, price volatility for generic consumables has been relatively stable, but specialized media and reproductive hormones have experienced price fluctuations due to raw material costs, research and development investments, and regulatory compliance. For instance, the demand for purified FSH can influence its market price. The growing demand from the Animal Biotechnology Market for various applications further intensifies the competition for these raw materials. Service providers often manage these risks by maintaining diverse supplier relationships, stocking critical consumables, and engaging in long-term contracts. Ensuring a robust and resilient supply chain is paramount for the uninterrupted provision of bovine embryo services and for maintaining competitive pricing in a rapidly evolving market.

Bovine Embryo Services Segmentation

1. Service Type

1.1. Embryo Collection

1.2. Embryo Transfer

1.3. In Vitro Fertilization (IVF) Services

1.4. Embryo Freezing & Storage

1.5. Genetic Testing & Screening

1.6. Others

2. Technique

2.1. In Vivo Embryo Production

2.2. In Vitro Embryo Production (IVP)

3. Application

3.1. Genetic Improvement

3.2. Disease Control

3.3. Herd Expansion

3.4. Research & Development

4. Service Provider

4.1. Private Service Providers

4.2. Veterinary Service Providers

4.3. Research Organizations

5. End-User

5.1. Dairy Farms

5.2. Beef Farms

5.3. Veterinary Clinics

5.4. Research Institutes

Bovine Embryo Services Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Bovine Embryo Services REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 11.92% from 2020-2034

Segmentation

By Service Type

Embryo Collection

Embryo Transfer

In Vitro Fertilization (IVF) Services

Embryo Freezing & Storage

Genetic Testing & Screening

Others

By Technique

In Vivo Embryo Production

In Vitro Embryo Production (IVP)

By Application

Genetic Improvement

Disease Control

Herd Expansion

Research & Development

By Service Provider

Private Service Providers

Veterinary Service Providers

Research Organizations

By End-User

Dairy Farms

Beef Farms

Veterinary Clinics

Research Institutes

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Service Type

5.1.1. Embryo Collection

5.1.2. Embryo Transfer

5.1.3. In Vitro Fertilization (IVF) Services

5.1.4. Embryo Freezing & Storage

5.1.5. Genetic Testing & Screening

5.1.6. Others

5.2. Market Analysis, Insights and Forecast - by Technique

5.2.1. In Vivo Embryo Production

5.2.2. In Vitro Embryo Production (IVP)

5.3. Market Analysis, Insights and Forecast - by Application

5.3.1. Genetic Improvement

5.3.2. Disease Control

5.3.3. Herd Expansion

5.3.4. Research & Development

5.4. Market Analysis, Insights and Forecast - by Service Provider

5.4.1. Private Service Providers

5.4.2. Veterinary Service Providers

5.4.3. Research Organizations

5.5. Market Analysis, Insights and Forecast - by End-User

5.5.1. Dairy Farms

5.5.2. Beef Farms

5.5.3. Veterinary Clinics

5.5.4. Research Institutes

5.6. Market Analysis, Insights and Forecast - by Region

5.6.1. North America

5.6.2. South America

5.6.3. Europe

5.6.4. Middle East & Africa

5.6.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Service Type

6.1.1. Embryo Collection

6.1.2. Embryo Transfer

6.1.3. In Vitro Fertilization (IVF) Services

6.1.4. Embryo Freezing & Storage

6.1.5. Genetic Testing & Screening

6.1.6. Others

6.2. Market Analysis, Insights and Forecast - by Technique

6.2.1. In Vivo Embryo Production

6.2.2. In Vitro Embryo Production (IVP)

6.3. Market Analysis, Insights and Forecast - by Application

6.3.1. Genetic Improvement

6.3.2. Disease Control

6.3.3. Herd Expansion

6.3.4. Research & Development

6.4. Market Analysis, Insights and Forecast - by Service Provider

6.4.1. Private Service Providers

6.4.2. Veterinary Service Providers

6.4.3. Research Organizations

6.5. Market Analysis, Insights and Forecast - by End-User

6.5.1. Dairy Farms

6.5.2. Beef Farms

6.5.3. Veterinary Clinics

6.5.4. Research Institutes

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Service Type

7.1.1. Embryo Collection

7.1.2. Embryo Transfer

7.1.3. In Vitro Fertilization (IVF) Services

7.1.4. Embryo Freezing & Storage

7.1.5. Genetic Testing & Screening

7.1.6. Others

7.2. Market Analysis, Insights and Forecast - by Technique

7.2.1. In Vivo Embryo Production

7.2.2. In Vitro Embryo Production (IVP)

7.3. Market Analysis, Insights and Forecast - by Application

7.3.1. Genetic Improvement

7.3.2. Disease Control

7.3.3. Herd Expansion

7.3.4. Research & Development

7.4. Market Analysis, Insights and Forecast - by Service Provider

7.4.1. Private Service Providers

7.4.2. Veterinary Service Providers

7.4.3. Research Organizations

7.5. Market Analysis, Insights and Forecast - by End-User

7.5.1. Dairy Farms

7.5.2. Beef Farms

7.5.3. Veterinary Clinics

7.5.4. Research Institutes

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Service Type

8.1.1. Embryo Collection

8.1.2. Embryo Transfer

8.1.3. In Vitro Fertilization (IVF) Services

8.1.4. Embryo Freezing & Storage

8.1.5. Genetic Testing & Screening

8.1.6. Others

8.2. Market Analysis, Insights and Forecast - by Technique

8.2.1. In Vivo Embryo Production

8.2.2. In Vitro Embryo Production (IVP)

8.3. Market Analysis, Insights and Forecast - by Application

8.3.1. Genetic Improvement

8.3.2. Disease Control

8.3.3. Herd Expansion

8.3.4. Research & Development

8.4. Market Analysis, Insights and Forecast - by Service Provider

8.4.1. Private Service Providers

8.4.2. Veterinary Service Providers

8.4.3. Research Organizations

8.5. Market Analysis, Insights and Forecast - by End-User

8.5.1. Dairy Farms

8.5.2. Beef Farms

8.5.3. Veterinary Clinics

8.5.4. Research Institutes

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Service Type

9.1.1. Embryo Collection

9.1.2. Embryo Transfer

9.1.3. In Vitro Fertilization (IVF) Services

9.1.4. Embryo Freezing & Storage

9.1.5. Genetic Testing & Screening

9.1.6. Others

9.2. Market Analysis, Insights and Forecast - by Technique

9.2.1. In Vivo Embryo Production

9.2.2. In Vitro Embryo Production (IVP)

9.3. Market Analysis, Insights and Forecast - by Application

9.3.1. Genetic Improvement

9.3.2. Disease Control

9.3.3. Herd Expansion

9.3.4. Research & Development

9.4. Market Analysis, Insights and Forecast - by Service Provider

9.4.1. Private Service Providers

9.4.2. Veterinary Service Providers

9.4.3. Research Organizations

9.5. Market Analysis, Insights and Forecast - by End-User

9.5.1. Dairy Farms

9.5.2. Beef Farms

9.5.3. Veterinary Clinics

9.5.4. Research Institutes

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Service Type

10.1.1. Embryo Collection

10.1.2. Embryo Transfer

10.1.3. In Vitro Fertilization (IVF) Services

10.1.4. Embryo Freezing & Storage

10.1.5. Genetic Testing & Screening

10.1.6. Others

10.2. Market Analysis, Insights and Forecast - by Technique

10.2.1. In Vivo Embryo Production

10.2.2. In Vitro Embryo Production (IVP)

10.3. Market Analysis, Insights and Forecast - by Application

10.3.1. Genetic Improvement

10.3.2. Disease Control

10.3.3. Herd Expansion

10.3.4. Research & Development

10.4. Market Analysis, Insights and Forecast - by Service Provider

10.4.1. Private Service Providers

10.4.2. Veterinary Service Providers

10.4.3. Research Organizations

10.5. Market Analysis, Insights and Forecast - by End-User

10.5.1. Dairy Farms

10.5.2. Beef Farms

10.5.3. Veterinary Clinics

10.5.4. Research Institutes

11. Competitive Analysis

11.1. Company Profiles

11.1.1. ABS Global

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Genus plc

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. STgenetics

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Select Sires Inc.

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Semex Alliance

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. CRV Holding B.V.

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Trans Ova Genetics

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Vytelle

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Boviteq

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. In Vitro Brasil S.A.

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Others

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Service Type 2025 & 2033

Figure 3: Revenue Share (%), by Service Type 2025 & 2033

Figure 4: Revenue (billion), by Technique 2025 & 2033

Figure 5: Revenue Share (%), by Technique 2025 & 2033

Figure 6: Revenue (billion), by Application 2025 & 2033

Figure 7: Revenue Share (%), by Application 2025 & 2033

Figure 8: Revenue (billion), by Service Provider 2025 & 2033

Figure 9: Revenue Share (%), by Service Provider 2025 & 2033

Figure 10: Revenue (billion), by End-User 2025 & 2033

Figure 11: Revenue Share (%), by End-User 2025 & 2033

Figure 12: Revenue (billion), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Revenue (billion), by Service Type 2025 & 2033

Figure 15: Revenue Share (%), by Service Type 2025 & 2033

Figure 16: Revenue (billion), by Technique 2025 & 2033

Figure 17: Revenue Share (%), by Technique 2025 & 2033

Figure 18: Revenue (billion), by Application 2025 & 2033

Figure 19: Revenue Share (%), by Application 2025 & 2033

Figure 20: Revenue (billion), by Service Provider 2025 & 2033

Figure 21: Revenue Share (%), by Service Provider 2025 & 2033

Figure 22: Revenue (billion), by End-User 2025 & 2033

Figure 23: Revenue Share (%), by End-User 2025 & 2033

Figure 24: Revenue (billion), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (billion), by Service Type 2025 & 2033

Figure 27: Revenue Share (%), by Service Type 2025 & 2033

Figure 28: Revenue (billion), by Technique 2025 & 2033

Figure 29: Revenue Share (%), by Technique 2025 & 2033

Figure 30: Revenue (billion), by Application 2025 & 2033

Figure 31: Revenue Share (%), by Application 2025 & 2033

Figure 32: Revenue (billion), by Service Provider 2025 & 2033

Figure 33: Revenue Share (%), by Service Provider 2025 & 2033

Figure 34: Revenue (billion), by End-User 2025 & 2033

Figure 35: Revenue Share (%), by End-User 2025 & 2033

Figure 36: Revenue (billion), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Revenue (billion), by Service Type 2025 & 2033

Figure 39: Revenue Share (%), by Service Type 2025 & 2033

Figure 40: Revenue (billion), by Technique 2025 & 2033

Figure 41: Revenue Share (%), by Technique 2025 & 2033

Figure 42: Revenue (billion), by Application 2025 & 2033

Figure 43: Revenue Share (%), by Application 2025 & 2033

Figure 44: Revenue (billion), by Service Provider 2025 & 2033

Figure 45: Revenue Share (%), by Service Provider 2025 & 2033

Figure 46: Revenue (billion), by End-User 2025 & 2033

Figure 47: Revenue Share (%), by End-User 2025 & 2033

Figure 48: Revenue (billion), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Revenue (billion), by Service Type 2025 & 2033

Figure 51: Revenue Share (%), by Service Type 2025 & 2033

Figure 52: Revenue (billion), by Technique 2025 & 2033

Figure 53: Revenue Share (%), by Technique 2025 & 2033

Figure 54: Revenue (billion), by Application 2025 & 2033

Figure 55: Revenue Share (%), by Application 2025 & 2033

Figure 56: Revenue (billion), by Service Provider 2025 & 2033

Figure 57: Revenue Share (%), by Service Provider 2025 & 2033

Figure 58: Revenue (billion), by End-User 2025 & 2033

Figure 59: Revenue Share (%), by End-User 2025 & 2033

Figure 60: Revenue (billion), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Service Type 2020 & 2033

Table 2: Revenue billion Forecast, by Technique 2020 & 2033

Table 3: Revenue billion Forecast, by Application 2020 & 2033

Table 4: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 5: Revenue billion Forecast, by End-User 2020 & 2033

Table 6: Revenue billion Forecast, by Region 2020 & 2033

Table 7: Revenue billion Forecast, by Service Type 2020 & 2033

Table 8: Revenue billion Forecast, by Technique 2020 & 2033

Table 9: Revenue billion Forecast, by Application 2020 & 2033

Table 10: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 11: Revenue billion Forecast, by End-User 2020 & 2033

Table 12: Revenue billion Forecast, by Country 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue (billion) Forecast, by Application 2020 & 2033

Table 15: Revenue (billion) Forecast, by Application 2020 & 2033

Table 16: Revenue billion Forecast, by Service Type 2020 & 2033

Table 17: Revenue billion Forecast, by Technique 2020 & 2033

Table 18: Revenue billion Forecast, by Application 2020 & 2033

Table 19: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 20: Revenue billion Forecast, by End-User 2020 & 2033

Table 21: Revenue billion Forecast, by Country 2020 & 2033

Table 22: Revenue (billion) Forecast, by Application 2020 & 2033

Table 23: Revenue (billion) Forecast, by Application 2020 & 2033

Table 24: Revenue (billion) Forecast, by Application 2020 & 2033

Table 25: Revenue billion Forecast, by Service Type 2020 & 2033

Table 26: Revenue billion Forecast, by Technique 2020 & 2033

Table 27: Revenue billion Forecast, by Application 2020 & 2033

Table 28: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 29: Revenue billion Forecast, by End-User 2020 & 2033

Table 30: Revenue billion Forecast, by Country 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue (billion) Forecast, by Application 2020 & 2033

Table 37: Revenue (billion) Forecast, by Application 2020 & 2033

Table 38: Revenue (billion) Forecast, by Application 2020 & 2033

Table 39: Revenue (billion) Forecast, by Application 2020 & 2033

Table 40: Revenue billion Forecast, by Service Type 2020 & 2033

Table 41: Revenue billion Forecast, by Technique 2020 & 2033

Table 42: Revenue billion Forecast, by Application 2020 & 2033

Table 43: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 44: Revenue billion Forecast, by End-User 2020 & 2033

Table 45: Revenue billion Forecast, by Country 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Revenue (billion) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Revenue (billion) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Revenue billion Forecast, by Service Type 2020 & 2033

Table 53: Revenue billion Forecast, by Technique 2020 & 2033

Table 54: Revenue billion Forecast, by Application 2020 & 2033

Table 55: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 56: Revenue billion Forecast, by End-User 2020 & 2033

Table 57: Revenue billion Forecast, by Country 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Table 59: Revenue (billion) Forecast, by Application 2020 & 2033

Table 60: Revenue (billion) Forecast, by Application 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Revenue (billion) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is designed to capture nuanced market insights directly from industry participants, constituting approximately 75% of our overall research effort. This extensive qualitative and quantitative engagement ensures the highest level of data granularity and validation. Our structured interview program targeted a diverse range of stakeholders across the bovine embryo services value chain, including:

Reproductive Veterinarians / Theriogenologists specializing in bovine reproduction.

Directors of Embryology Laboratories / IVF Center Managers within specialized service providers.

Product Development Leads / R&D Managers at animal biotechnology firms creating reproductive technologies and media.

Sales & Marketing Directors for Bovine Genetic Services and Embryo Technologies companies.

Interviews were conducted through a structured questionnaire, prioritizing senior-level executives and domain experts. The insights gathered from these discussions were critical for understanding market dynamics, competitive landscapes, technological advancements, pricing trends, and regional specificities.

Complementing our primary efforts, secondary research accounted for approximately 25% of the total research, serving as a foundational layer for market understanding and validation. This phase involved an exhaustive review of published literature and authenticated data sources.

Key sources utilized include:

Reputable financial databases such as Bloomberg, Factiva, Hoovers, and PitchBook for corporate profiles, financial performance, and M&A activities.

Relevant sections of the Food and Drug Administration (FDA) FDA and European Medicines Agency (EMA) EMA pertaining to veterinary products and services.

White papers, annual reports, investor presentations, and product literature from key market players.

Academic journals and scientific publications focused on bovine reproduction, genetics, and biotechnology.

Trade journals and publications specific to the livestock and veterinary industries.

Our methodology strictly excludes data from other market research websites to maintain the integrity and originality of our findings.

Demand Modeling & Market Estimation

The market size and forecast were derived using a robust blend of top-down and bottom-up approaches, triangulated across multiple data points to ensure accuracy. This multi-level data triangulation involved cross-referencing insights from primary interviews with validated secondary data.

Bottom-up Approach: Market sizing began by aggregating granular data points. Key metrics and variables used for bottom-up calculation included:

Annual number of embryo collection and transfer procedures performed by region and service type.

Average service fees/costs per embryo collection, transfer, and In Vitro Fertilization (IVF) cycle.

Volume of embryos frozen and stored, combined with associated storage fees.

Number of genetic tests performed on embryos and offspring.

Penetration rates of advanced reproductive technologies (ARTs) within dairy and beef cattle populations in key regions.

Top-down Approach: This involved estimating the total available market based on macro-economic indicators, bovine livestock population data, agricultural GDP, and overall veterinary services spending, then segmenting down to bovine embryo services.

All market values are presented in current USD, reflecting prevailing exchange rates and inflation at the time of publication.

Data Accuracy & Quality Check

Our rigorous methodology guarantees an estimated data accuracy level between 85% and 90%. Every data point and market insight undergoes a stringent validation process involving:

Multi-stage Validation: Information gathered from primary sources is cross-referenced with multiple secondary sources and peer-reviewed by internal subject matter experts.

Quantitative Modeling: Advanced statistical models are employed to identify trends, extrapolate data, and forecast market movements, mitigating potential biases and refining projections.

Constant Refresh: Our market data is continuously updated to reflect the latest industry developments, technological advancements, and economic shifts, ensuring that every report is current up to the date of purchase. This includes monitoring for new service offerings, regulatory changes, and shifts in end-user adoption patterns.

This meticulous approach ensures that our clients receive reliable, actionable, and highly accurate market intelligence.

Frequently Asked Questions

1. What technological innovations are shaping the Bovine Embryo Services industry?

Technological innovations include advancements in In Vitro Fertilization (IVF) services, embryo freezing, and genetic testing. Companies like Vytelle and Boviteq are prominent in developing and applying these techniques for herd improvement.

2. Why are specific barriers influencing competition in Bovine Embryo Services?

Competition is influenced by high initial investment in R&D and specialized equipment, alongside the need for expert veterinary skills. Established providers such as ABS Global and Genus plc leverage significant operational experience and proprietary genetic lines.

3. How are end-user demands shifting within Bovine Embryo Services?

End-user demand is shifting towards enhanced genetic improvement and accelerated herd expansion for both Dairy Farms and Beef Farms. There is also increasing interest from research institutes for disease control and genetic studies.

4. Which companies are attracting investment in Bovine Embryo Services?

Investment targets companies offering advanced In Vitro Fertilization (IVF) and genetic testing services. Players focused on innovative techniques, such as Vytelle and Boviteq, indicate areas of active capital interest for market expansion.

5. Which region presents the fastest growth opportunities for Bovine Embryo Services?

Asia-Pacific, particularly China and India, represents significant growth opportunities due to expanding livestock populations and adoption of advanced breeding technologies. South America, especially Brazil and Argentina, also shows robust growth.

6. What is the projected market size and CAGR for Bovine Embryo Services by 2033?

The Bovine Embryo Services market was valued at $10.69 billion in 2025. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.92% through 2033, driven by genetic improvement and herd expansion requirements.