Dental Bibs by Application (Hospital, Clinic, Other), by Types (Polyethylene, Paper, Polyester, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 16, 2026|Base Year : 2025|Pages : 126

Amit Mardhekar

Research Analyst

About Sector Data Insights

Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

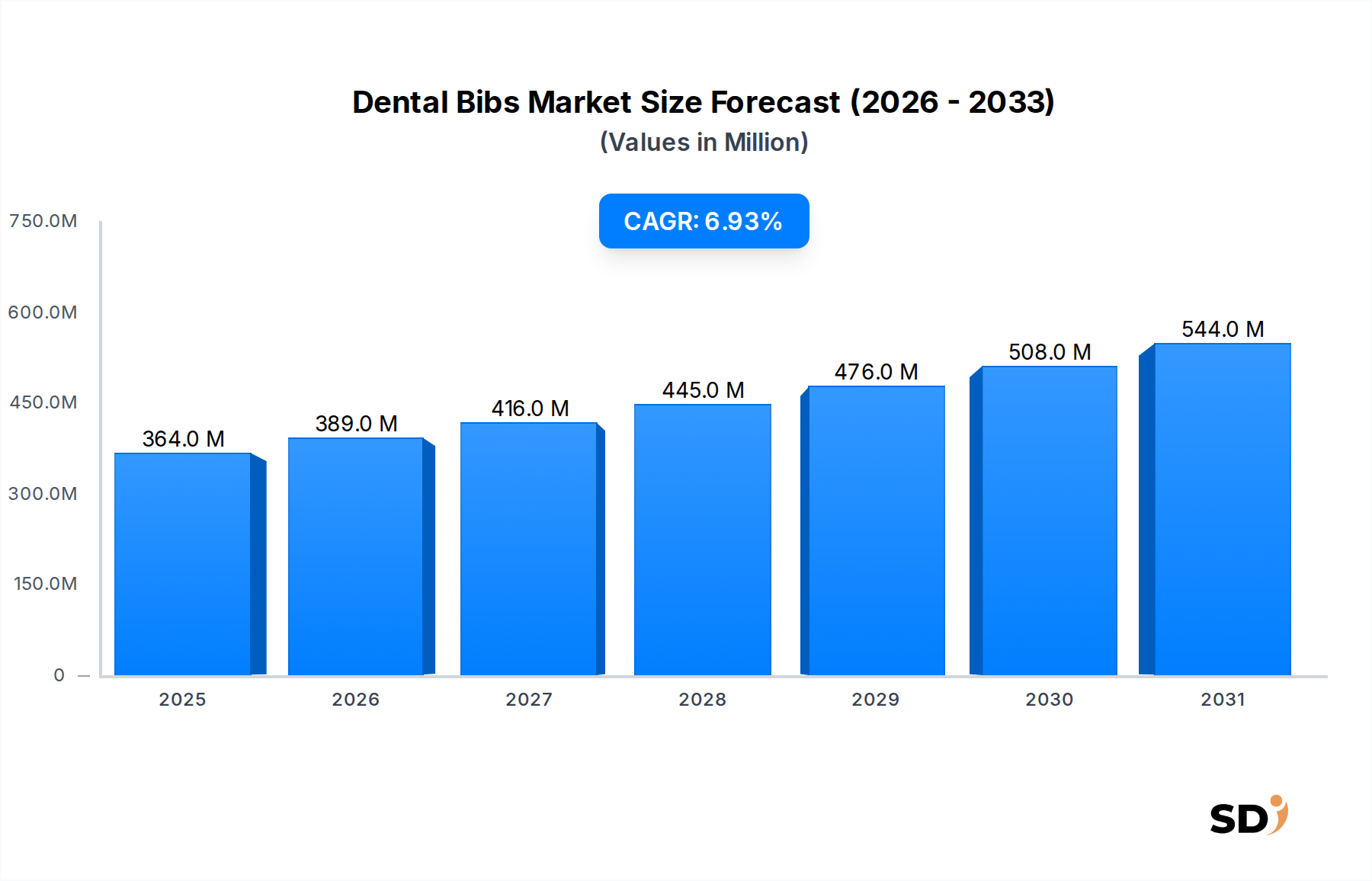

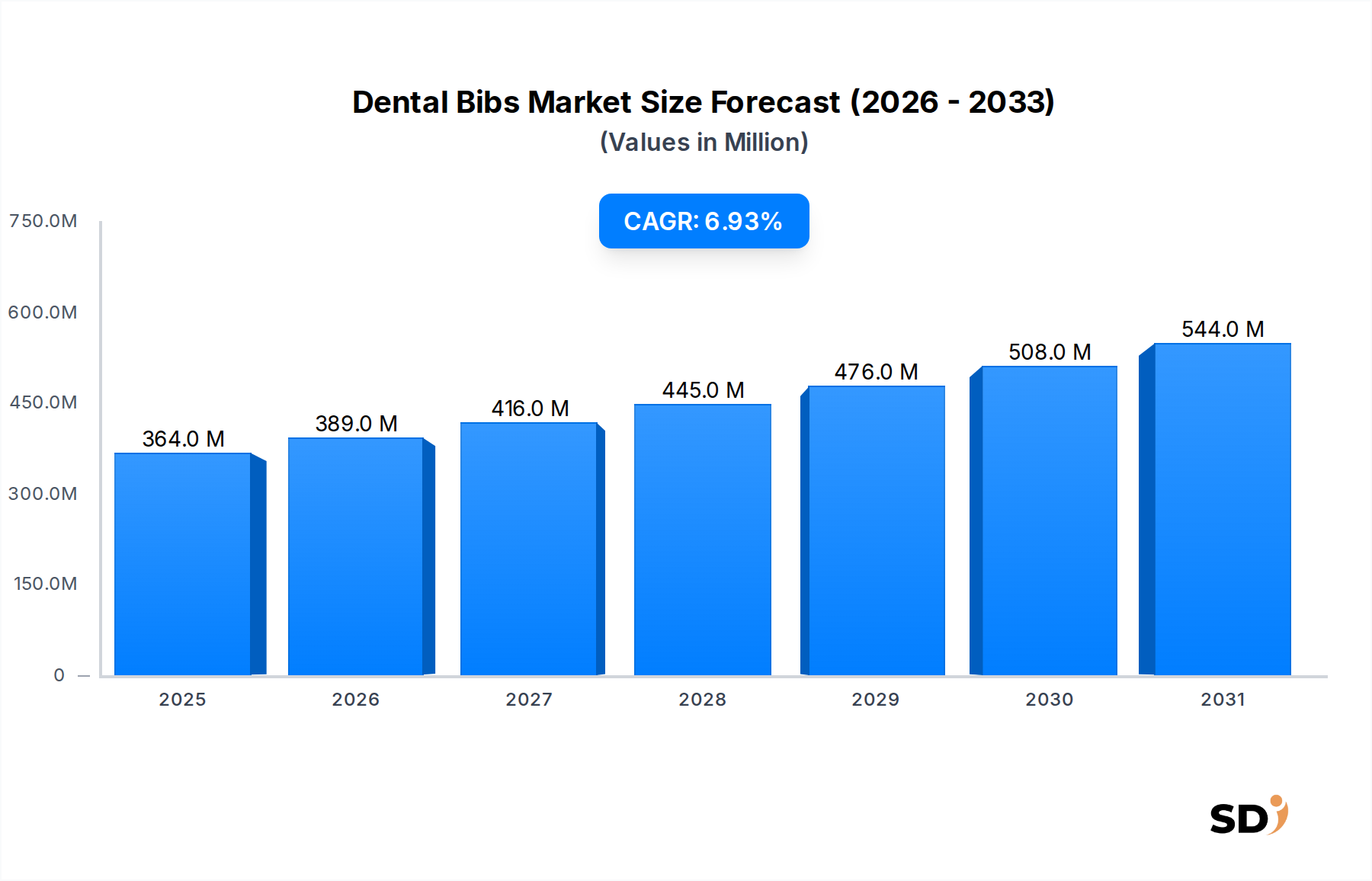

The Global Dental Bibs Market was valued at a substantial USD 364.25 million in 2025, demonstrating its integral role within the broader healthcare and dental industries. Projections indicate a robust expansion, with the market anticipated to grow at a Compound Annual Growth Rate (CAGR) of 6.9% through 2034, reaching an estimated valuation of USD 670.03 million. This consistent growth trajectory is primarily underpinned by escalating global awareness regarding oral hygiene and the imperative of stringent infection control protocols in dental settings. Dental bibs serve as a critical barrier, protecting patients' clothing and minimizing cross-contamination during various dental procedures.

Dental Bibs Market Size (In Million)

750.0M

600.0M

450.0M

300.0M

150.0M

0

364.0 M

2025

389.0 M

2026

416.0 M

2027

445.0 M

2028

476.0 M

2029

508.0 M

2030

544.0 M

2031

A significant demand driver is the increasing prevalence of dental disorders, coupled with a growing elderly population worldwide that requires more extensive dental care, from routine check-ups to complex restorative and cosmetic procedures. This demographic shift, alongside rising disposable incomes in emerging economies, fuels greater access to and demand for professional dental services. Furthermore, advancements in dental technology and the expansion of dental tourism contribute to higher patient footfall in dental clinics and hospitals, directly translating to increased consumption of dental bibs. The push for single-use products to enhance hygiene and reduce the risk of infection further solidifies the market's growth. Regulatory bodies across regions are also reinforcing guidelines for medical and dental waste management, inadvertently boosting the demand for high-quality, disposable protective gear.

Macroeconomic tailwinds such as increasing healthcare expenditure, improving healthcare infrastructure, and the expansion of private dental practices and large dental clinic chains are creating a fertile ground for market growth. The convenience, cost-effectiveness, and ease of disposal associated with dental bibs make them an indispensable component of the Dental Consumables Market. The ongoing emphasis on patient safety and the prevention of hospital-acquired infections (HAIs) positions dental bibs as a cornerstone of the Infection Control Products Market. Manufacturers are continuously innovating, focusing on enhanced absorbency, improved barrier properties, and more environmentally friendly material options to meet evolving market demands and sustainability concerns. The outlook for the Dental Bibs Market remains highly positive, driven by persistent demand from the expanding global dental patient base and an unwavering commitment to hygiene standards.

Paper Type Segment Dominance in Dental Bibs Market

The "Paper" type segment is projected to maintain its dominant position within the Dental Bibs Market, driven by a confluence of factors including cost-effectiveness, superior absorbency, and widespread acceptance across diverse dental practices globally. Paper-based dental bibs typically feature multiple layers of tissue paper, often backed with a thin layer of polyethylene. This composite structure provides a dual benefit: the paper layers efficiently absorb fluids and saliva, while the polyethylene backing acts as an impermeable barrier, preventing liquid penetration and protecting the patient's clothing from moisture, debris, and potential contaminants. This functional efficacy, combined with their disposable nature, aligns perfectly with stringent hygiene requirements in modern dentistry, making them a staple product for daily operations in every dental setting.

The ubiquity of paper-based dental bibs stems from their economical production cost, which allows manufacturers to offer competitive pricing. This affordability is a significant factor for dental practices, especially those operating on tighter budgets, ensuring that high standards of patient protection can be maintained without excessive operational expenditure. Furthermore, the convenience of single-use disposability inherent in paper products streamlines clinic workflows, eliminating the need for sterilization or cleaning, thereby enhancing operational efficiency and reducing turnaround times between patients. This aspect contributes significantly to the Disposable Dental Products Market landscape.

Key players in the Dental Bibs Market, recognizing the sustained demand for paper-based solutions, continue to focus on optimizing material sourcing and manufacturing processes to enhance product performance and reduce environmental impact. Innovations often revolve around improving the absorbency capacity of the paper layers, reinforcing the polyethylene backing for enhanced tear resistance, and exploring sustainable paper sources. While concerns regarding single-use plastics persist, the composite nature of these bibs often necessitates the Polyethylene Film Market component for effective fluid impermeability. However, there is a growing trend towards incorporating biodegradable or compostable paper layers and exploring bio-based polyethylene alternatives to address environmental pressures. The segment's share is not only consolidating its dominance but is also experiencing growth, driven by the expanding global patient base and the consistent need for reliable, cost-efficient, and hygienic solutions in dental care. As Dental Clinics Market and Hospital Supplies Market continue to expand globally, the demand for conventional yet effective paper-based dental bibs is set to grow proportionally.

Key Market Drivers and Constraints in Dental Bibs Market

Market Drivers:

Heightened Focus on Infection Control and Patient Safety: A primary driver for the Dental Bibs Market is the escalating global emphasis on preventing cross-contamination and ensuring patient safety in dental environments. Regulatory bodies worldwide have intensified guidelines for infection control in healthcare settings, mandating the use of disposable barriers. This robust regulatory framework, coupled with increased patient awareness of hygiene standards, drives consistent demand for dental bibs as a crucial component of the Infection Control Products Market. For instance, the Centers for Disease Control and Prevention (CDC) guidelines in the United States and similar directives from the European Centre for Disease Prevention and Control (ECDC) globally underscore the importance of barrier protection, contributing to sustained market expansion.

Rising Volume of Dental Procedures and Growing Oral Health Awareness: The increasing incidence of dental caries, periodontal diseases, and other oral health issues, combined with a surge in cosmetic and elective dental procedures, directly translates to higher utilization of dental bibs. Furthermore, public health campaigns and improved access to dental care, particularly in emerging economies, are boosting the number of dental visits. Data indicates a year-over-year increase in overall dental appointments, fueled by an aging population requiring more frequent and complex dental interventions. This trend is a significant impetus for the entire Dental Consumables Market and, by extension, the dental bibs segment.

Convenience and Efficiency of Disposable Products: The shift towards disposable medical products, including dental bibs, is driven by the unparalleled convenience and efficiency they offer to dental practitioners. Disposable bibs eliminate the need for cleaning, sterilization, or re-processing, thereby saving time, reducing labor costs, and significantly minimizing the risk of infection transmission. This operational advantage makes dental bibs an indispensable part of the Disposable Dental Products Market, streamlining clinic workflows and allowing dental professionals to focus more on patient care rather than logistical concerns. The demand for such products is also seen as complementary to the market for Sterilization Equipment Market, as both aim to achieve optimal hygienic conditions.

Market Constraints:

Environmental Concerns Regarding Single-Use Plastics: A significant restraint on the Dental Bibs Market is the growing global concern over environmental pollution caused by single-use plastics, particularly the polyethylene backing in many dental bibs. With increasing consumer and regulatory pressure to reduce plastic waste, manufacturers face the challenge of developing sustainable, biodegradable, or compostable alternatives. While the Polyethylene Film Market provides essential barrier properties, the push for eco-friendly solutions necessitates substantial R&D investments, potentially increasing production costs and impacting market dynamics. This constraint is driving innovations in the Medical Nonwovens Market towards more sustainable fibers.

Price Sensitivity and Market Fragmentation: The Dental Bibs Market is characterized by intense competition and a high degree of price sensitivity, particularly from larger group practices and public health institutions seeking cost-effective bulk procurement. The availability of numerous manufacturers, including regional and local players, leads to a fragmented market where price often becomes a primary differentiator. This competitive pressure can constrain profit margins for manufacturers and suppliers, limiting investment in advanced materials or innovative product features, despite the clear benefits of enhanced hygiene.

Competitive Ecosystem of Dental Bibs Market

The Dental Bibs Market features a diverse competitive landscape, encompassing both established global players and numerous regional manufacturers. The strategies adopted by these companies often revolve around product innovation, cost-effectiveness, supply chain optimization, and adherence to international quality and safety standards. Many players also leverage robust distribution networks to cater to the widespread needs of Dental Clinics Market and hospitals.

Sanax Protective Products Inc.: This company specializes in a range of protective barriers for medical and dental applications, focusing on high-quality, absorbent, and fluid-resistant dental bibs designed for various procedural needs.

Aprons, Etc.: A supplier primarily known for protective apparel, Aprons, Etc. also offers a selection of dental bibs, emphasizing comfort, coverage, and disposable convenience for dental practices.

Beaming White, LLC: Primarily recognized for its teeth whitening products, Beaming White, LLC also provides essential dental accessories, including patient bibs that complement its core product offerings.

Med 101 Store.com: An online medical supply retailer, Med 101 Store.com offers a comprehensive catalog of medical and dental disposables, including a variety of dental bibs from multiple manufacturers, focusing on accessibility and competitive pricing.

2H Manufacturing & Distributing Corp.: This manufacturer focuses on producing a wide array of disposable medical products, with dental bibs being a key offering, often emphasizing robust barrier protection and absorbency.

Westbond Enterprises Corp.: Specializing in non-woven materials, Westbond Enterprises Corp. provides solutions for various medical and hygiene products, including high-quality dental bibs, leveraging its expertise in material science.

AMD Medicom: A global leader in infection control and prevention products, AMD Medicom offers an extensive range of dental bibs, renowned for their superior fluid absorption and impermeable barriers, aligning with strict healthcare standards.

Coltene/Whaledent Inc.: Known for its dental materials and equipment, Coltene/Whaledent Inc. also supplies essential disposables like dental bibs, integrating them into comprehensive solutions for dental professionals.

National Sorbents Inc.: As its name suggests, National Sorbents Inc. specializes in absorbent products, translating its core capabilities into effective and high-performance dental bibs designed for fluid management during procedures.

Pollyanna Hygiene: This company focuses on delivering hygiene solutions, offering dental bibs as part of its broader product line, prioritizing clean and safe environments for patients and practitioners.

Shanghai Zogear Industries Co., Ltd.: A significant player from Asia, Shanghai Zogear Industries Co., Ltd. manufactures a wide range of disposable medical and dental products, including cost-effective and functionally robust dental bibs for global distribution.

Anhui JM Healthcare Products Co., Ltd.: Based in China, Anhui JM Healthcare Products Co., Ltd. is an established manufacturer of medical protective products, with dental bibs forming a key part of its export-oriented portfolio, emphasizing quality and volume production.

Xiantao S&J Protective Products Co., Ltd: Another prominent Chinese manufacturer, Xiantao S&J Protective Products Co., Ltd. specializes in disposable non-woven products for medical and protective use, including a strong focus on high-volume production of dental bibs for international markets.

Recent Developments & Milestones in Dental Bibs Market

Recent developments in the Dental Bibs Market largely reflect the industry's response to evolving hygiene standards, sustainability pressures, and material science advancements. Innovations are geared towards enhancing product performance while addressing environmental concerns, which increasingly impact the Disposable Dental Products Market.

February 2024: Several manufacturers introduced dental bibs featuring enhanced fluid retention polymers, designed to absorb a greater volume of liquids more rapidly, thereby improving patient comfort and minimizing procedure-related mess. These advancements contribute to the overall efficiency of dental procedures.

November 2023: A leading dental supply company launched a new line of dental bibs made from a blend of recycled paper and bio-based polyethylene backing. This initiative aimed to reduce the carbon footprint associated with single-use dental products, aligning with growing ESG (Environmental, Social, and Governance) mandates across the healthcare sector.

August 2023: Collaborations between Medical Nonwovens Market suppliers and dental product manufacturers intensified, focusing on developing dental bibs with improved tear resistance and softer textures, enhancing both durability and patient experience during longer dental treatments.

May 2023: New automated manufacturing processes for dental bibs were implemented by major producers, leading to increased production efficiency, reduced material waste, and more consistent product quality. This technological upgrade also helped in scaling up supply to meet surging global demand.

January 2023: A global dental products distributor announced a strategic partnership with an innovative startup specializing in antimicrobial coatings. The objective was to explore the integration of non-leaching antimicrobial agents into dental bib materials, offering an additional layer of infection control during high-risk procedures.

September 2022: Regulatory bodies in key European markets updated guidelines regarding the disposability of dental waste, indirectly stimulating demand for dental bibs that are easier to separate into their constituent materials for recycling or composting where facilities exist.

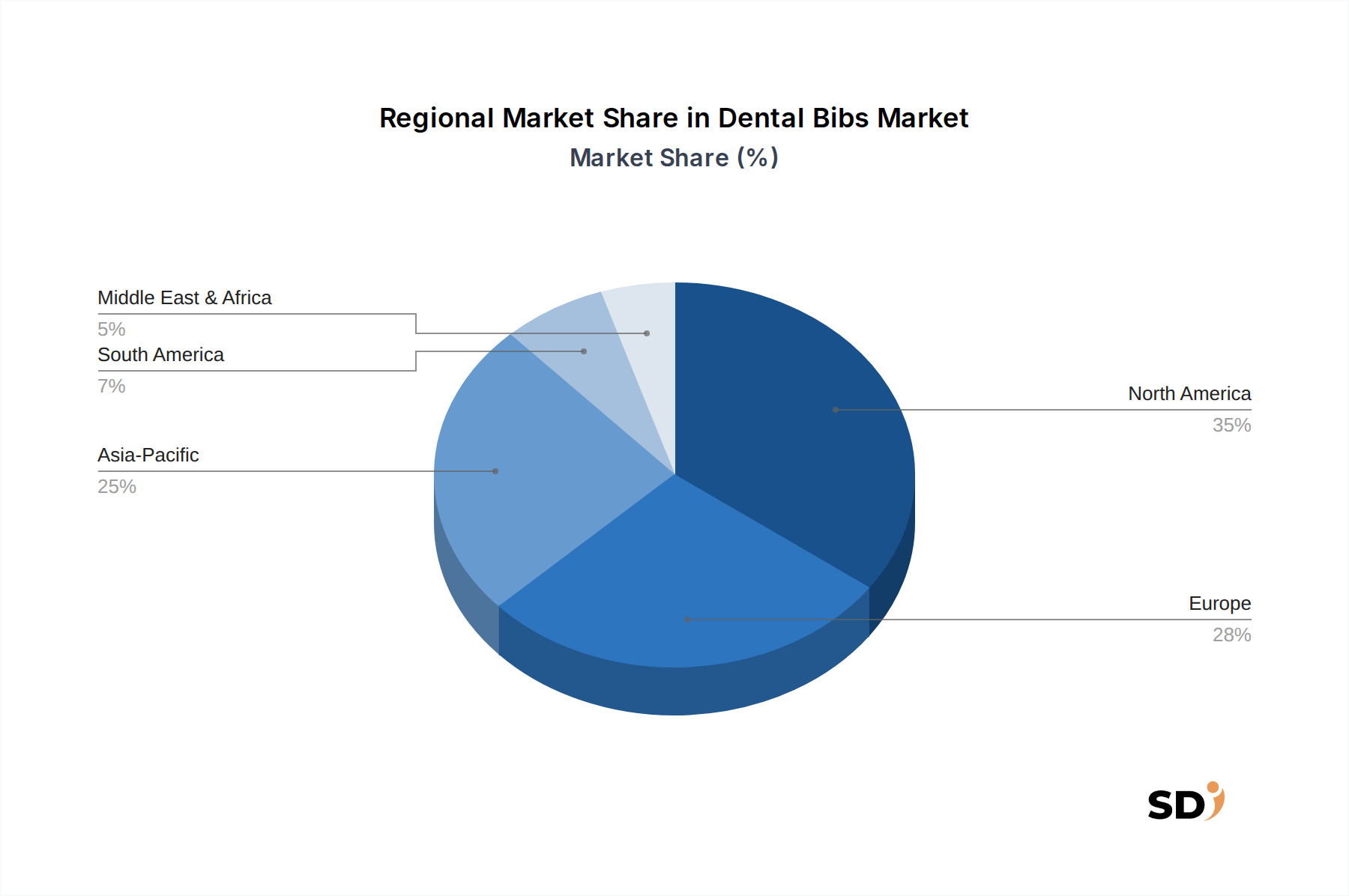

Regional Market Breakdown for Dental Bibs Market

North America: This region holds a significant share of the Dental Bibs Market, driven by a highly developed healthcare infrastructure, stringent infection control regulations, and high consumer awareness regarding oral health. The presence of a large number of dental professionals and an aging population requiring extensive dental care further bolster demand. The United States, in particular, contributes substantially due to robust healthcare expenditure and a strong emphasis on preventative dentistry. Innovation in materials and continued investment in private dental practices are key regional drivers.

Europe: Europe also represents a mature and substantial market for dental bibs, characterized by advanced dental healthcare systems and strict adherence to hygiene standards set by organizations like the European Centre for Disease Prevention and Control (ECDC). Countries such as Germany, the UK, and France are major contributors, propelled by widespread access to dental insurance, a growing cosmetic dentistry sector, and an increasing focus on patient safety. The region is also at the forefront of adopting sustainable practices, influencing product development towards eco-friendly dental bib options.

Asia Pacific: The Asia Pacific region is anticipated to be the fastest-growing market for dental bibs, exhibiting a rapidly expanding Dental Consumables Market. This growth is fueled by a burgeoning population, increasing disposable incomes, improving access to dental care, and the rise of medical tourism. Countries like China, India, and Japan are at the forefront, driven by government initiatives to improve oral health, the proliferation of dental clinics, and a growing middle class that can afford advanced dental treatments. The increasing adoption of international hygiene standards also plays a crucial role in boosting demand for dental bibs.

Latin America, Middle East & Africa (LAMEA): This combined region represents an emerging market for dental bibs, with considerable growth potential. Factors contributing to this growth include expanding healthcare infrastructure, increasing government investment in public health programs, and a rising awareness of oral hygiene. In Latin America, countries like Brazil and Mexico are seeing growth due to expanding private dental sectors. In the Middle East, high healthcare spending and a growing expatriate population contribute to demand. Africa, while starting from a lower base, is experiencing incremental growth as basic dental services become more accessible, driven by initiatives to combat oral diseases. Challenges include economic disparities and varying levels of healthcare access, yet the long-term outlook remains positive due to overall development.

Technology Innovation Trajectory in Dental Bibs Market

The technology innovation trajectory in the Dental Bibs Market is increasingly focused on material science advancements and manufacturing process optimization to meet evolving demands for enhanced performance, cost-efficiency, and sustainability. Two key disruptive areas are emerging: advanced material composites and smart manufacturing integration.

Advanced Material Composites: The primary technological disruption in dental bibs is the development of novel material composites that go beyond traditional paper and polyethylene combinations. This includes incorporating biodegradable polymers derived from renewable resources, such as polylactic acid (PLA) or compostable bio-plastics, to address environmental concerns. Furthermore, research and development (R&D) investments are escalating into materials with inherently enhanced absorbency capabilities, potentially integrating super-absorbent polymers (SAPs) or innovative Medical Nonwovens Market structures that can manage higher fluid volumes more effectively without increasing bulk. There's also exploratory work on antimicrobial treatments for bibs, designed to inhibit bacterial growth on the bib surface, adding an extra layer of infection control. These innovations aim to offer superior barrier protection and fluid management while reducing the ecological footprint, thereby potentially reinforcing incumbent business models that embrace these shifts, but threatening those reliant solely on conventional, less sustainable materials. Adoption timelines for fully biodegradable solutions are mid-to-long term, contingent on cost parity and regulatory approvals.

Smart Manufacturing and Customization: Another significant technological shift involves the integration of smart manufacturing processes, including advanced robotics and AI-driven quality control. These technologies enable higher precision in bib construction, reducing material waste during production and allowing for greater customization. While dental bibs are generally standardized, future innovations could involve tailored bibs for specific procedures or patient demographics (e.g., pediatric sizes with integrated patterns, or specialized shapes for oral surgery). Automated production lines also allow for rapid scaling and flexible adaptation to market demands, potentially making manufacturing more agile and responsive. While not 'disruptive' in the sense of creating an entirely new product, smart manufacturing can significantly lower production costs, improve consistency, and reduce lead times, thus reinforcing the competitive edge of large-scale manufacturers and increasing barriers to entry for smaller players. The Polyethylene Film Market and Medical Nonwovens Market are directly impacted by these manufacturing advancements, as material inputs must be compatible with high-speed, precise processes.

Sustainability & ESG Pressures on Dental Bibs Market

The Dental Bibs Market is increasingly influenced by significant sustainability and Environmental, Social, and Governance (ESG) pressures, reshaping product development, procurement, and waste management strategies. As a high-volume, single-use product category within the Dental Consumables Market, dental bibs face scrutiny regarding their environmental impact, particularly concerning plastic waste.

Environmental Regulations and Carbon Targets: Governments and international bodies are imposing stricter environmental regulations aimed at reducing plastic pollution and achieving carbon neutrality. This translates into mandates for reduced plastic content, increased use of recycled materials, and the development of biodegradable alternatives for disposable products. Manufacturers in the Dental Bibs Market are consequently investing heavily in R&D to develop bibs with compostable paper layers and bio-based Polyethylene Film Market backings, or even entirely plastic-free options. The push to meet carbon targets is also driving a re-evaluation of supply chains, with a focus on local sourcing and energy-efficient manufacturing processes to minimize transportation-related emissions. Non-compliance with these evolving regulations poses significant market access risks and reputational damage.

Circular Economy Mandates: The concept of a circular economy, which emphasizes reducing waste and maximizing resource utilization, is gaining traction. For dental bibs, this means exploring not just biodegradability but also designing products that can be effectively recycled or composted in existing municipal waste streams. This involves careful consideration of composite materials to ensure separability or full biodegradability of the entire product. Procurement decisions in Hospital Supplies Market and Dental Clinics Market are increasingly influenced by a product's end-of-life options and its overall lifecycle assessment. Manufacturers that can demonstrate a clear pathway for their products within a circular economy framework gain a competitive advantage and appeal to environmentally conscious customers.

ESG Investor Criteria and Consumer Demand: Beyond regulations, ESG investor criteria are increasingly influencing corporate strategy, pushing companies to integrate sustainability into their core operations. Investors are scrutinizing environmental impact, ethical sourcing, and social responsibility. Concurrently, dental professionals and patients are becoming more environmentally aware, preferring products that align with sustainable values. This consumer-driven demand creates a market pull for 'green' dental bibs, compelling manufacturers to not only innovate in materials (e.g., Medical Nonwovens Market from sustainable forests) but also to transparently communicate their sustainability efforts. Companies that proactively address these ESG pressures by offering genuinely sustainable solutions are better positioned to attract investment, enhance brand loyalty, and secure market share in the evolving Dental Bibs Market.

Dental Bibs Segmentation

1. Application

1.1. Hospital

1.2. Clinic

1.3. Other

2. Types

2.1. Polyethylene

2.2. Paper

2.3. Polyester

2.4. Other

Dental Bibs Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Dental Bibs REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 6.9% from 2020-2034

Segmentation

By Application

Hospital

Clinic

Other

By Types

Polyethylene

Paper

Polyester

Other

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application

5.1.1. Hospital

5.1.2. Clinic

5.1.3. Other

5.2. Market Analysis, Insights and Forecast - by Types

5.2.1. Polyethylene

5.2.2. Paper

5.2.3. Polyester

5.2.4. Other

5.3. Market Analysis, Insights and Forecast - by Region

5.3.1. North America

5.3.2. South America

5.3.3. Europe

5.3.4. Middle East & Africa

5.3.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application

6.1.1. Hospital

6.1.2. Clinic

6.1.3. Other

6.2. Market Analysis, Insights and Forecast - by Types

6.2.1. Polyethylene

6.2.2. Paper

6.2.3. Polyester

6.2.4. Other

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application

7.1.1. Hospital

7.1.2. Clinic

7.1.3. Other

7.2. Market Analysis, Insights and Forecast - by Types

7.2.1. Polyethylene

7.2.2. Paper

7.2.3. Polyester

7.2.4. Other

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application

8.1.1. Hospital

8.1.2. Clinic

8.1.3. Other

8.2. Market Analysis, Insights and Forecast - by Types

8.2.1. Polyethylene

8.2.2. Paper

8.2.3. Polyester

8.2.4. Other

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application

9.1.1. Hospital

9.1.2. Clinic

9.1.3. Other

9.2. Market Analysis, Insights and Forecast - by Types

9.2.1. Polyethylene

9.2.2. Paper

9.2.3. Polyester

9.2.4. Other

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application

10.1.1. Hospital

10.1.2. Clinic

10.1.3. Other

10.2. Market Analysis, Insights and Forecast - by Types

10.2.1. Polyethylene

10.2.2. Paper

10.2.3. Polyester

10.2.4. Other

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Sanax Protective Products Inc.

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Aprons

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Etc.

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Beaming White

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. LLC

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Med 101 Store.com

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. 2H Manufacturing & Distributing Corp.

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Westbond Enterprises Corp.

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. AMD Medicom

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Coltene/Whaledent Inc.

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. National Sorbents Inc.

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Pollyanna Hygiene

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. Shanghai Zogear Industries Co.

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.1.14. Ltd.

11.1.14.1. Company Overview

11.1.14.2. Products

11.1.14.3. Company Financials

11.1.14.4. SWOT Analysis

11.1.15. Anhui JM Healthcare Products Co.

11.1.15.1. Company Overview

11.1.15.2. Products

11.1.15.3. Company Financials

11.1.15.4. SWOT Analysis

11.1.16. Ltd.

11.1.16.1. Company Overview

11.1.16.2. Products

11.1.16.3. Company Financials

11.1.16.4. SWOT Analysis

11.1.17. Xiantao S&J Protective Products Co.

11.1.17.1. Company Overview

11.1.17.2. Products

11.1.17.3. Company Financials

11.1.17.4. SWOT Analysis

11.1.18. Ltd

11.1.18.1. Company Overview

11.1.18.2. Products

11.1.18.3. Company Financials

11.1.18.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (million), by Application 2025 & 2033

Figure 4: Volume (K), by Application 2025 & 2033

Figure 5: Revenue Share (%), by Application 2025 & 2033

Figure 6: Volume Share (%), by Application 2025 & 2033

Figure 7: Revenue (million), by Types 2025 & 2033

Figure 8: Volume (K), by Types 2025 & 2033

Figure 9: Revenue Share (%), by Types 2025 & 2033

Figure 10: Volume Share (%), by Types 2025 & 2033

Figure 11: Revenue (million), by Country 2025 & 2033

Figure 12: Volume (K), by Country 2025 & 2033

Figure 13: Revenue Share (%), by Country 2025 & 2033

Figure 14: Volume Share (%), by Country 2025 & 2033

Figure 15: Revenue (million), by Application 2025 & 2033

Figure 16: Volume (K), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Volume Share (%), by Application 2025 & 2033

Figure 19: Revenue (million), by Types 2025 & 2033

Figure 20: Volume (K), by Types 2025 & 2033

Figure 21: Revenue Share (%), by Types 2025 & 2033

Figure 22: Volume Share (%), by Types 2025 & 2033

Figure 23: Revenue (million), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (million), by Application 2025 & 2033

Figure 28: Volume (K), by Application 2025 & 2033

Figure 29: Revenue Share (%), by Application 2025 & 2033

Figure 30: Volume Share (%), by Application 2025 & 2033

Figure 31: Revenue (million), by Types 2025 & 2033

Figure 32: Volume (K), by Types 2025 & 2033

Figure 33: Revenue Share (%), by Types 2025 & 2033

Figure 34: Volume Share (%), by Types 2025 & 2033

Figure 35: Revenue (million), by Country 2025 & 2033

Figure 36: Volume (K), by Country 2025 & 2033

Figure 37: Revenue Share (%), by Country 2025 & 2033

Figure 38: Volume Share (%), by Country 2025 & 2033

Figure 39: Revenue (million), by Application 2025 & 2033

Figure 40: Volume (K), by Application 2025 & 2033

Figure 41: Revenue Share (%), by Application 2025 & 2033

Figure 42: Volume Share (%), by Application 2025 & 2033

Figure 43: Revenue (million), by Types 2025 & 2033

Figure 44: Volume (K), by Types 2025 & 2033

Figure 45: Revenue Share (%), by Types 2025 & 2033

Figure 46: Volume Share (%), by Types 2025 & 2033

Figure 47: Revenue (million), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (million), by Application 2025 & 2033

Figure 52: Volume (K), by Application 2025 & 2033

Figure 53: Revenue Share (%), by Application 2025 & 2033

Figure 54: Volume Share (%), by Application 2025 & 2033

Figure 55: Revenue (million), by Types 2025 & 2033

Figure 56: Volume (K), by Types 2025 & 2033

Figure 57: Revenue Share (%), by Types 2025 & 2033

Figure 58: Volume Share (%), by Types 2025 & 2033

Figure 59: Revenue (million), by Country 2025 & 2033

Figure 60: Volume (K), by Country 2025 & 2033

Figure 61: Revenue Share (%), by Country 2025 & 2033

Figure 62: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Application 2020 & 2033

Table 2: Volume K Forecast, by Application 2020 & 2033

Table 3: Revenue million Forecast, by Types 2020 & 2033

Table 4: Volume K Forecast, by Types 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Volume K Forecast, by Region 2020 & 2033

Table 7: Revenue million Forecast, by Application 2020 & 2033

Table 8: Volume K Forecast, by Application 2020 & 2033

Table 9: Revenue million Forecast, by Types 2020 & 2033

Table 10: Volume K Forecast, by Types 2020 & 2033

Table 11: Revenue million Forecast, by Country 2020 & 2033

Table 12: Volume K Forecast, by Country 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Volume (K) Forecast, by Application 2020 & 2033

Table 15: Revenue (million) Forecast, by Application 2020 & 2033

Table 16: Volume (K) Forecast, by Application 2020 & 2033

Table 17: Revenue (million) Forecast, by Application 2020 & 2033

Table 18: Volume (K) Forecast, by Application 2020 & 2033

Table 19: Revenue million Forecast, by Application 2020 & 2033

Table 20: Volume K Forecast, by Application 2020 & 2033

Table 21: Revenue million Forecast, by Types 2020 & 2033

Table 22: Volume K Forecast, by Types 2020 & 2033

Table 23: Revenue million Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (million) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue million Forecast, by Application 2020 & 2033

Table 32: Volume K Forecast, by Application 2020 & 2033

Table 33: Revenue million Forecast, by Types 2020 & 2033

Table 34: Volume K Forecast, by Types 2020 & 2033

Table 35: Revenue million Forecast, by Country 2020 & 2033

Table 36: Volume K Forecast, by Country 2020 & 2033

Table 37: Revenue (million) Forecast, by Application 2020 & 2033

Table 38: Volume (K) Forecast, by Application 2020 & 2033

Table 39: Revenue (million) Forecast, by Application 2020 & 2033

Table 40: Volume (K) Forecast, by Application 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Volume (K) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (million) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue (million) Forecast, by Application 2020 & 2033

Table 50: Volume (K) Forecast, by Application 2020 & 2033

Table 51: Revenue (million) Forecast, by Application 2020 & 2033

Table 52: Volume (K) Forecast, by Application 2020 & 2033

Table 53: Revenue (million) Forecast, by Application 2020 & 2033

Table 54: Volume (K) Forecast, by Application 2020 & 2033

Table 55: Revenue million Forecast, by Application 2020 & 2033

Table 56: Volume K Forecast, by Application 2020 & 2033

Table 57: Revenue million Forecast, by Types 2020 & 2033

Table 58: Volume K Forecast, by Types 2020 & 2033

Table 59: Revenue million Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (million) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (million) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (million) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (million) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (million) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (million) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue million Forecast, by Application 2020 & 2033

Table 74: Volume K Forecast, by Application 2020 & 2033

Table 75: Revenue million Forecast, by Types 2020 & 2033

Table 76: Volume K Forecast, by Types 2020 & 2033

Table 77: Revenue million Forecast, by Country 2020 & 2033

Table 78: Volume K Forecast, by Country 2020 & 2033

Table 79: Revenue (million) Forecast, by Application 2020 & 2033

Table 80: Volume (K) Forecast, by Application 2020 & 2033

Table 81: Revenue (million) Forecast, by Application 2020 & 2033

Table 82: Volume (K) Forecast, by Application 2020 & 2033

Table 83: Revenue (million) Forecast, by Application 2020 & 2033

Table 84: Volume (K) Forecast, by Application 2020 & 2033

Table 85: Revenue (million) Forecast, by Application 2020 & 2033

Table 86: Volume (K) Forecast, by Application 2020 & 2033

Table 87: Revenue (million) Forecast, by Application 2020 & 2033

Table 88: Volume (K) Forecast, by Application 2020 & 2033

Table 89: Revenue (million) Forecast, by Application 2020 & 2033

Table 90: Volume (K) Forecast, by Application 2020 & 2033

Table 91: Revenue (million) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our market sizing and forecasting are predominantly driven by primary research, constituting approximately 75% of our overall research efforts. This rigorous approach ensures that our findings reflect current market dynamics, emerging trends, and nuanced perspectives from key industry participants. Primary interviews are conducted with stakeholders across the value chain to gather qualitative and quantitative insights.

Key stakeholders interviewed include:

Director of Product Management (from manufacturing and distribution firms)

Procurement Manager (at dental clinics, hospitals, and large group practices)

Head of Dental Operations / Clinical Director (at clinics and hospitals, focusing on product usage and preference)

Supply Chain Director (at major distributors and manufacturing firms)

Companies targeted for primary interviews span the entire dental bibs value chain, ensuring comprehensive data collection:

Dental Bib Manufacturers

Dental Product Distributors

Dental Clinic Chains / Hospitals

Raw Material Suppliers (Polymer/Paper)

Dental Group Purchasing Organizations (GPOs)

This direct engagement with industry experts allows us to validate secondary findings, obtain proprietary data, and gain forward-looking perspectives critical for accurate market forecasts. All primary data is meticulously cross-referenced and triangulated.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Director of Product Management

35%

Procurement Manager

30%

Head of Dental Operations / Clinical Director

20%

Supply Chain Director

15%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Dental Bib Manufacturers

40%

Dental Product Distributors

30%

Dental Clinic Chains / Hospitals

15%

Raw Material Suppliers

10%

Dental Group Purchasing Organizations (GPOs)

5%

Secondary Research & Industry Benchmarking

The remaining 25% of our research effort is dedicated to comprehensive secondary research and industry benchmarking. This phase provides the foundational data, establishes market boundaries, and identifies key industry players. Our secondary research draws from a diverse array of credible sources, strictly excluding data from other market research websites to maintain the originality and integrity of our findings.

Sources leveraged include:

Government & Regulatory Bodies: Publications from national health agencies (e.g., CDC, NHS), trade statistics from customs and economic departments (e.g., US Census Bureau, Eurostat).

Industry Associations: Reports, whitepapers, and statistical data published by globally recognized dental and medical associations such as:

International Organization for Standardization (ISO) (www.iso.org) – relevant for quality standards of dental materials and medical devices.

Company Financials & Publications: Annual reports, investor presentations, and press releases of public and private companies active in the dental supplies market.

Financial Databases: Subscription-based financial intelligence platforms for market sizing, company profiling, and competitive analysis including Bloomberg, Factiva, Hoovers, and PitchBook.

Academic & Technical Literature: Peer-reviewed journals and technical specifications related to dental materials and infection control.

This phase also involves competitor analysis, technological landscaping, and macro-economic factor analysis to provide a robust context for market development.

Demand Modeling & Market Estimation

Our market sizing employs a sophisticated blend of top-down and bottom-up methodologies, complemented by multi-level data triangulation to ensure maximum accuracy and reliability.

Bottom-Up Approach: This method begins at the micro-level, aggregating individual market segments. For the dental bibs market, key metrics and variables used include:

Number of Active Dental Professionals / Dental Clinics (by region)

Average Dental Bibs Consumed Per Patient Visit (accounting for multi-bib procedures)

Average Selling Price (ASP) per Bib Type (Polyethylene, Paper, Polyester, Other) and per geographic region

Utilization Rate of Disposable Products in Dental Procedures (factoring in regulatory compliance and hygiene standards)

This granular data is then scaled up to determine regional and global market sizes.

Top-Down Approach: Simultaneously, we use a top-down approach, starting with broader economic indicators and dental healthcare expenditure data. This involves estimating the total available market based on macro trends in healthcare, dental tourism, and disposable medical supply consumption, then disaggregating it to the dental bibs segment.

Data Triangulation: All market figures derived from both top-down and bottom-up analyses are rigorously cross-verified and triangulated with data from primary interviews, secondary sources, and our proprietary internal databases. This multi-layered validation process helps to identify and reconcile discrepancies, enhancing the overall robustness of the market estimates.

Forecasts are generated using advanced statistical modeling techniques, considering historical trends, projected growth rates of dental procedures, technological advancements, raw material price fluctuations, and evolving regulatory landscapes, across all defined segments (Application, Types, and Regions).

Data Accuracy & Quality Check

Our commitment to data integrity is paramount. We guarantee an estimated data accuracy level of 85-90% for our market size and forecast figures. This high level of accuracy is achieved through a multi-stage validation process that includes:

Expert Panel Review: Insights and data points are regularly reviewed and challenged by an internal panel of senior analysts and external industry experts.

Real-time Updates: Every report is updated up to the date of purchase, incorporating the latest market developments, company announcements, and economic shifts to ensure the most current and relevant information is presented.

Proprietary Algorithms: Utilization of custom-built algorithms to identify data anomalies and project future market trajectories with greater precision.

Ethical Data Practices: Adherence to strict ethical guidelines in data collection and analysis, ensuring confidentiality and unbiased reporting.

This meticulous approach ensures that our clients receive a highly reliable, actionable, and up-to-date market intelligence report, enabling informed strategic decision-making.

Frequently Asked Questions

1. How are pricing trends and cost structures evolving in the Dental Bibs market?

Pricing for dental bibs typically reflects material costs (Polyethylene, Paper, Polyester) and manufacturing efficiency. Competition among key players like Sanax Protective Products Inc. and AMD Medicom influences market pricing, with a trend towards cost-effective bulk procurement for hospitals and clinics.

2. What regulations impact the Dental Bibs market?

The Dental Bibs market operates under medical device regulations concerning material safety, sterility, and manufacturing standards. Compliance is essential for market entry and product distribution across regions such as North America and Europe, ensuring product quality for applications in hospitals and clinics.

3. How are consumer behavior and purchasing trends changing for Dental Bibs?

Purchasing trends for dental bibs are primarily driven by dental facilities' demand for hygiene and patient protection. There's a consistent demand from hospitals and clinics, with a preference for specific types like polyethylene and paper bibs based on cost-effectiveness and performance requirements. The market saw robust demand leading to a 6.9% CAGR forecast through 2034.

4. Which companies lead the Dental Bibs market?

The Dental Bibs market features key players such as Sanax Protective Products Inc., AMD Medicom, and Coltene/Whaledent Inc. These companies compete on product innovation, material quality, and distribution networks, especially across major markets like North America and Europe.

5. What post-pandemic recovery patterns are evident in the Dental Bibs market?

The Dental Bibs market experienced a post-pandemic recovery driven by the resumption of elective dental procedures and heightened awareness of infection control. This has reinforced consistent demand from clinics and hospitals globally, supporting the market's projected 6.9% CAGR from 2026 to 2034.

6. What sustainability and environmental factors influence the Dental Bibs market?

Sustainability concerns are increasing pressure on the Dental Bibs market, particularly regarding single-use plastics. Manufacturers are exploring more biodegradable materials or improved waste management solutions for products like polyethylene and paper bibs, aligning with growing ESG standards from purchasers.