Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Automotive Starter Motor and Alternator by Product Type (Starter Motors, Alternators), by Technology (12V Systems, 24V Systems, 48V Systems, Others), by Application (Engine Starting, Battery Charging, Start-Stop Systems, Regenerative Energy Recovery, Auxiliary Power Generation), by Sales Channel (OEM, Aftermarket), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 109

Key Insights into the Automotive Starter Motor and Alternator Market

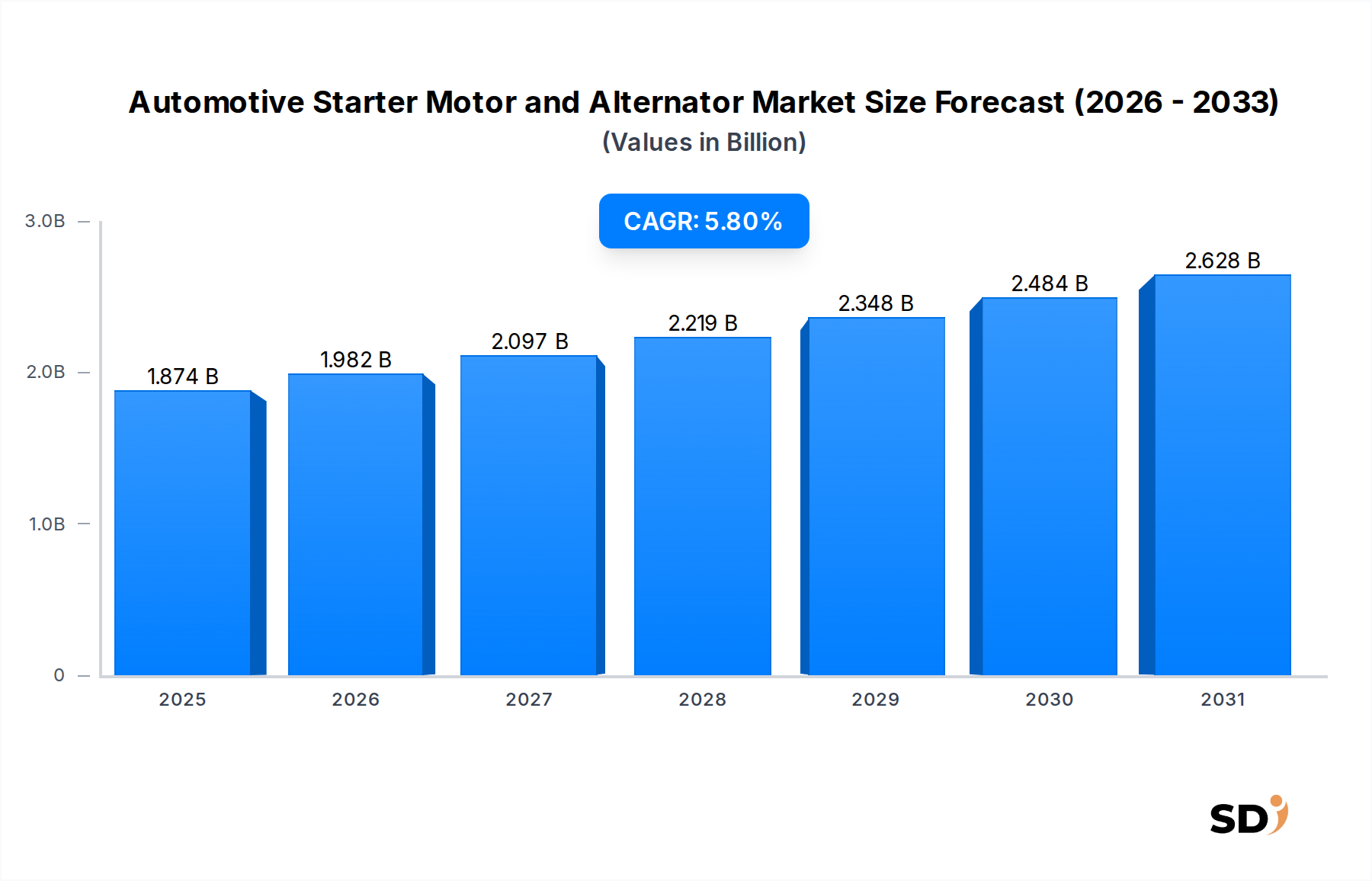

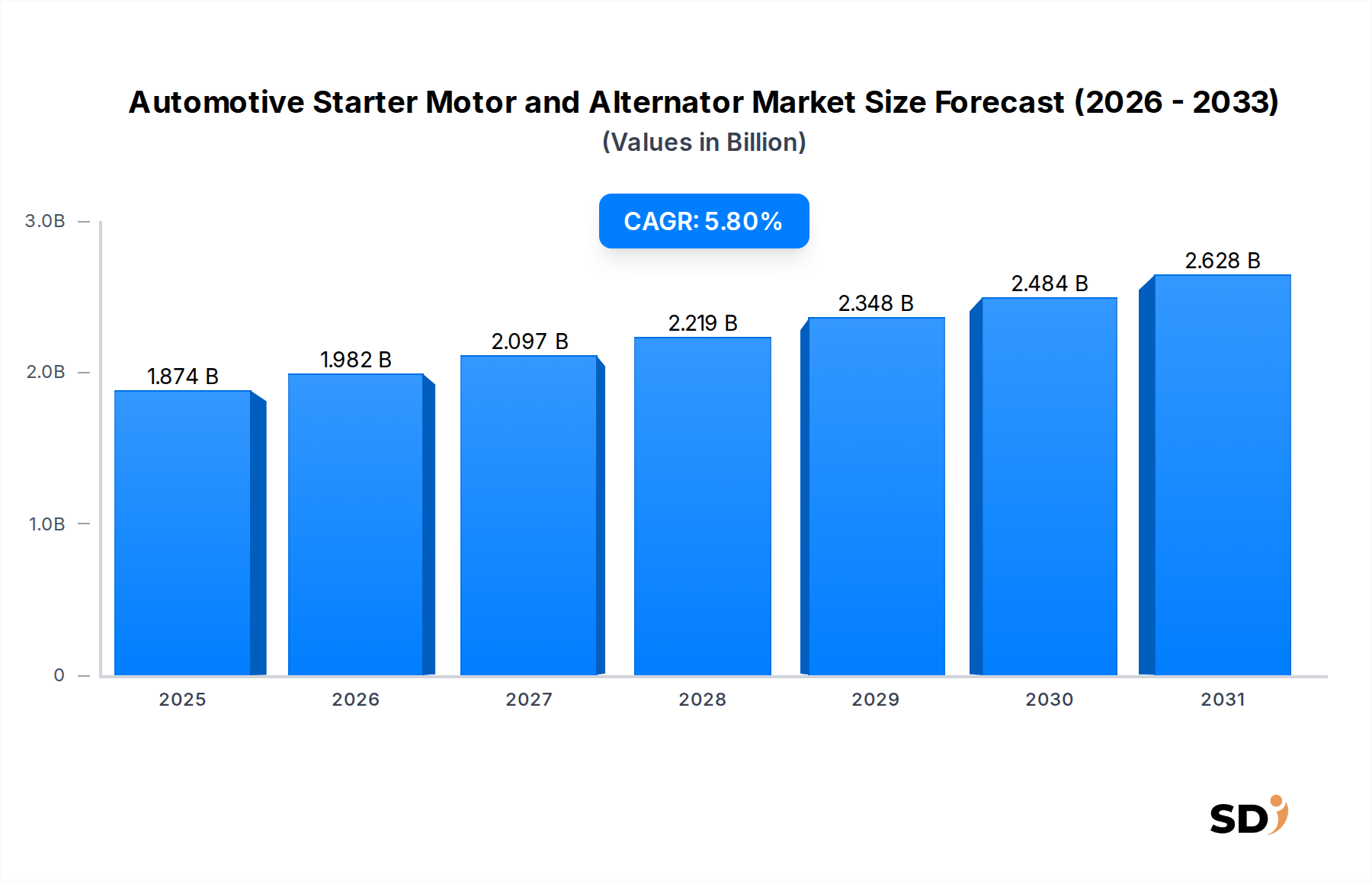

The Automotive Starter Motor and Alternator Market, a critical segment within the broader Automotive Components Market, is valued at $1873.8 million. Projections indicate a steady expansion at a Compound Annual Growth Rate (CAGR) of 5.8%, anticipating sustained growth through 2034. This trajectory is underpinned by an array of factors, including consistent global vehicle production, the robust demand from the aftermarket segment, and the ongoing evolution in vehicle electrification. Traditional internal combustion engine (ICE) vehicles continue to constitute the majority of the global vehicle parc, necessitating reliable starter motors and alternators for fundamental operations such as engine cranking and on-board power generation. The demand is further buoyed by the increasing adoption of advanced start-stop systems, which require more durable and efficient starter motors, and the integration of smart alternators designed to optimize power delivery and fuel efficiency.

Automotive Starter Motor and Alternator Market Size (In Billion)

3.0B

2.0B

1.0B

0

1.874 B

2025

1.982 B

2026

2.097 B

2027

2.219 B

2028

2.348 B

2029

2.484 B

2030

2.628 B

2031

Macroeconomic tailwinds such as rising disposable incomes in emerging economies, coupled with rapid urbanization, contribute to the expansion of the global vehicle fleet, thereby stimulating both OEM and aftermarket demand. Regulatory pressures driving stricter emission norms also play a pivotal role, pushing manufacturers towards developing more efficient and integrated power management solutions, including those offered by the Automotive Starter Motor and Alternator Market. While the shift towards the Electric Vehicle Market presents a long-term transformative challenge, the sustained production of conventional and hybrid vehicles ensures the enduring relevance of these components. Innovations in materials, manufacturing processes, and power electronics are further enhancing product lifespan and performance, which, while extending replacement cycles, also solidifies the market's foundational demand. The complex interplay of these elements suggests a stable yet dynamically evolving market landscape, requiring continuous innovation and strategic adaptation from key players to capitalize on growth opportunities while navigating technological shifts.

Aftermarket Sales Dominance in Automotive Starter Motor and Alternator Market

The aftermarket sales channel stands as the dominant segment by revenue share within the Automotive Starter Motor and Alternator Market. This segment's preeminence is primarily driven by the sheer size and aging profile of the global vehicle parc. As vehicles accumulate mileage and age, components like starter motors and alternators are subjected to wear and tear, necessitating periodic replacement or repair. The average lifespan of a vehicle often exceeds the warranty period of these critical electrical components, funnelling demand into the aftermarket. Industry statistics consistently indicate that the average vehicle age is steadily increasing across major economies, with some regions reporting average ages exceeding 12 years. This extended operational life directly translates into a larger pool of vehicles requiring maintenance and component replacement, thus solidifying the aftermarket's stronghold.

The aftermarket's dominance is further reinforced by several factors. Firstly, cost-effectiveness often dictates consumer choices; repairing or replacing specific components like a starter motor or an alternator is significantly more economical than purchasing a new vehicle. Secondly, the fragmented nature of the aftermarket, encompassing independent repair shops, franchised dealerships, and specialized service centers, offers consumers a wider range of product choices, from OEM-grade replacements to more affordable, compatible alternatives. This competitive landscape, while potentially exerting margin pressure on suppliers, ultimately serves to meet diverse consumer preferences and budgets. Moreover, the increasing complexity of vehicle electrical systems and the proliferation of advanced features, such as start-stop technology, necessitate components that meet specific performance criteria, driving demand for quality aftermarket parts. Major players in the Automotive Starter Motor and Alternator Market, including Valeo Group, Denso Corporation, and The Bosch Group, maintain robust aftermarket distribution networks, leveraging their brand reputation and extensive product portfolios to capture this significant revenue stream. While OEM sales are directly tied to new vehicle production cycles, the aftermarket provides a more stable and consistent revenue base, less susceptible to short-term fluctuations in new vehicle sales, thereby asserting its position as the largest and most resilient segment.

Key Dynamics and Market Evolution for Automotive Starter Motor and Alternator Market

The Automotive Starter Motor and Alternator Market is shaped by a confluence of driving forces and inherent constraints. A primary driver is the persistent growth in global vehicle production, particularly within the Passenger Vehicle Market and Commercial Vehicle Market segments. Reports from leading automotive organizations indicate a steady increase in automotive output, with projections pointing to an annual growth rate for global light vehicle production around 2-3% post-pandemic recovery. Each new ICE vehicle produced directly necessitates the integration of both a starter motor and an alternator, creating consistent OEM demand. This trend is especially pronounced in developing regions, where vehicle penetration rates are still on the rise, supporting the overall Automotive Components Market.

Another significant driver is the widespread adoption of start-stop systems in modern vehicles. These systems, designed to improve fuel efficiency and reduce emissions by shutting off the engine at idle, place greater strain on starter motors, requiring more robust and durable designs capable of enduring tens of thousands of start cycles. Penetration rates for start-stop technology have soared, reaching over 60% in new vehicles in some developed markets, directly increasing the demand for specialized, high-performance starter motors. Furthermore, the burgeoning global vehicle parc and the aging fleet continuously fuel the aftermarket segment, ensuring a steady stream of replacement demand for both starter motors and the Automotive Alternator Market.

Conversely, a key constraint impacting the long-term outlook of the Automotive Starter Motor and Alternator Market is the accelerated global shift towards the Electric Vehicle Market. Pure Battery Electric Vehicles (BEVs) do not utilize traditional starter motors or alternators, as their propulsion systems are entirely electric, and power generation is handled by specialized DC-DC converters and battery management systems. While hybrids and mild hybrids still incorporate these components, the rapid growth trajectory of BEVs, with global sales increasing significantly year-on-year (e.g., over 60% growth in 2022 and sustained high double-digit growth projected), represents a fundamental threat to the core demand for these traditional components. Additionally, the increasing reliability and extended lifespan of modern components, a benefit for consumers, can paradoxically slow down replacement cycles in the aftermarket, posing a subtle constraint on volume growth.

Pricing Dynamics & Margin Pressure in Automotive Starter Motor and Alternator Market

Pricing dynamics within the Automotive Starter Motor and Alternator Market are intricately linked to technological advancements, raw material costs, and intense competitive pressures. The average selling price (ASP) of these components varies significantly based on type and technology, with conventional starter motors and alternators typically commanding lower prices compared to advanced units like smart alternators or components for 48V Systems Market. For instance, the ASP for a standard 12V alternator can range from $80-$150 at the OEM level, while a smart alternator or an integrated starter generator (ISG) can fetch upwards of $200-$400, reflecting the added complexity and functionality. This divergence in ASP creates a bifurcated market where suppliers must manage multiple product lines with distinct cost structures.

Margin structures across the value chain are generally tighter in the OEM segment, where automotive manufacturers exert significant pressure on suppliers to reduce costs. OEM contracts often involve high volumes but slender margins, sometimes in the low single digits. Conversely, the aftermarket segment typically offers healthier margins, potentially ranging from 20-40%, owing to brand loyalty, perceived quality, and less direct price negotiation. However, the aftermarket also faces intense competition from regional manufacturers and a proliferation of generic or remanufactured parts, which can erode pricing power for premium brands.

Key cost levers predominantly include raw material prices, particularly for copper (used extensively in windings), steel, and various magnetic materials. Fluctuations in global commodity markets can directly impact production costs, forcing manufacturers to absorb costs or pass them on, albeit cautiously, to maintain competitiveness. Labor costs, especially in regions with rising wages, and significant R&D investments required for developing more efficient, compact, and integrated solutions also contribute to the overall cost base. Competitive intensity, marked by the presence of global giants like Valeo, Denso, and Bosch, alongside numerous regional players, further limits pricing power, compelling continuous innovation and operational efficiency to sustain profitability in the Automotive Starter Motor and Alternator Market.

Technology Innovation Trajectory in Automotive Starter Motor and Alternator Market

The Automotive Starter Motor and Alternator Market is undergoing significant technological evolution, driven by the push for greater fuel efficiency, reduced emissions, and enhanced vehicle electrical systems. Two of the most disruptive emerging technologies include the proliferation of 48V Systems Market and the advancement of smart alternators and integrated starter generators (ISGs).

48V Systems: These mild-hybrid systems are rapidly gaining traction as a cost-effective solution to improve fuel economy and reduce CO2 emissions without the full cost burden of a high-voltage hybrid. In a 48V system, the traditional starter motor and alternator are often replaced by a single belt-driven starter generator (BSG) or a crankshaft-mounted ISG. This unit provides powerful engine cranking, regenerative braking, and torque assistance to the engine. R&D investment in this area is substantial, with major suppliers developing compact, high-power density 48V components. Adoption timelines are accelerating, with many new vehicle platforms from 2023 onwards integrating 48V technology, especially in Europe and China. This technology directly threatens conventional 12V starter motor and alternator businesses but reinforces those suppliers who pivot to 48V system components, integrating them more deeply into the broader Automotive Electronics Market.

Smart Alternators and Integrated Starter Generators (ISGs): Smart alternators are electronically controlled, allowing variable voltage and current output to optimize battery charging and reduce parasitic engine load, thus improving fuel economy. These systems communicate with the engine control unit (ECU) to dynamically manage power generation based on driving conditions and electrical load. ISGs go a step further by combining the functions of a starter, alternator, and sometimes even providing supplemental torque. This integration is crucial for advanced start-stop systems and regenerative braking. R&D efforts focus on increasing power output, reducing size and weight, and improving thermal management. The adoption of smart alternators is already high in many new vehicles, while ISGs are becoming standard in mild-hybrid architectures. These innovations reinforce the business models of incumbent suppliers capable of advanced electronics and software integration, while potentially displacing manufacturers focused solely on basic, conventional components.

Competitive Ecosystem of Automotive Starter Motor and Alternator Market

The Automotive Starter Motor and Alternator Market is characterized by a mature yet dynamic competitive landscape, dominated by a few global tier-one suppliers alongside a significant number of regional and specialized manufacturers. Strategic differentiation often hinges on technological leadership, supply chain efficiency, and comprehensive aftermarket support.

Valeo Group: A leading global automotive supplier, Valeo Group is known for its extensive portfolio of powertrain electrification products, including highly efficient starter motors and alternators, particularly focusing on advanced 48V systems and mild-hybrid technologies.

Denso Corporation: As a major Japanese automotive components manufacturer, Denso Corporation specializes in advanced automotive technology, offering a wide range of high-performance starter motors and alternators known for their durability and efficiency in various vehicle applications.

The Bosch Group: A diversified technology and services company, Bosch is a prominent player in the automotive sector, providing robust and innovative starter motors, alternators, and integrated generator systems, with a strong emphasis on smart power management solutions.

Mitsuba Corporation: This Japanese company focuses on electrical components for the automotive industry, delivering compact and lightweight starter motors and alternators primarily for passenger vehicles and motorcycles, emphasizing reliability and performance.

Mitsubishi Electric Corporation: Known for its broad range of electrical and electronic products, Mitsubishi Electric Corporation supplies high-quality automotive equipment, including starter motors and alternators, that are recognized for their advanced technology and dependable operation.

Lucas Electricals: With a strong heritage in the automotive aftermarket, Lucas Electricals provides a comprehensive range of electrical components, including starter motors and alternators, catering to various vehicle types with a focus on quality replacement parts.

Controlled Power Technologies: Specializing in advanced powertrain technologies, CPT is a key innovator in the 48V Systems Market, offering cutting-edge mild-hybrid solutions that often integrate starter-generator functions for enhanced fuel efficiency.

Hella KGaAHueck&: Primarily known for lighting and electronics, Hella also offers advanced power management solutions and components within the Automotive Starter Motor and Alternator Market, contributing to vehicle efficiency and performance.

ASIMCO Technologies: A significant player in the Chinese automotive components sector, ASIMCO Technologies manufactures a wide array of automotive parts, including starter motors and alternators, serving both OEM and aftermarket segments across Asia.

Hitachi Automotive Systems: Now part of Hitachi Astemo, this entity is a global supplier of automotive components, offering a robust portfolio that includes high-efficiency starter motors and alternators designed for diverse vehicle platforms.

Cummins: Primarily known for its diesel and natural gas engines, Cummins also supplies heavy-duty alternators and related electrical systems tailored for commercial vehicle applications, particularly in its own engine platforms.

SEG Automotive GmbH: Spun off from Bosch, SEG Automotive specializes solely in starter motors and alternators, focusing on developing highly efficient, intelligent solutions for conventional and electrified powertrains, with a strong global presence.

Recent Developments & Milestones in Automotive Starter Motor and Alternator Market

Recent developments in the Automotive Starter Motor and Alternator Market reflect a concerted effort towards enhancing efficiency, integrating advanced technologies, and expanding market reach. These milestones underscore the industry's response to evolving vehicle architectures and environmental regulations.

Q4 2023: Several leading manufacturers, including Denso Corporation and Valeo Group, launched next-generation smart alternators designed for improved power density and efficiency. These new units feature enhanced thermal management and more sophisticated electronic controls, offering up to 5% better fuel economy in specific driving cycles compared to their predecessors. This development aims to capitalize on the increasing demand for optimized power delivery in modern vehicles and reduce the overall load on the engine.

Q2 2024: A significant partnership was announced between The Bosch Group and a major European OEM to co-develop compact integrated starter generators (ISGs) specifically for new mild-hybrid vehicle platforms. This collaboration is set to expedite the adoption of 48V Systems Market technology, with initial vehicle models incorporating these components expected to enter mass production by late 2025. The initiative focuses on achieving higher power output within smaller footprints to meet the stringent packaging requirements of contemporary vehicle designs.

Q1 2025: ASIMCO Technologies completed a substantial expansion of its manufacturing capabilities in Southeast Asia, aimed at increasing production capacity for both conventional and advanced starter motors and alternators. This strategic investment, valued at approximately $50 million, is intended to strengthen the company's position in the rapidly growing Asia Pacific Automotive Components Market and enhance its ability to serve both local and international aftermarket demand efficiently.

Q3 2025: Controlled Power Technologies (CPT) successfully demonstrated a novel electric supercharger integrated with a 48V starter-generator system at a prominent automotive tech conference. This innovation highlights the potential for further integration of power electronics within the Automotive Starter Motor and Alternator Market, providing additional engine boosting capabilities alongside traditional starting and charging functions, potentially paving the way for more sophisticated powertrain electrification strategies.

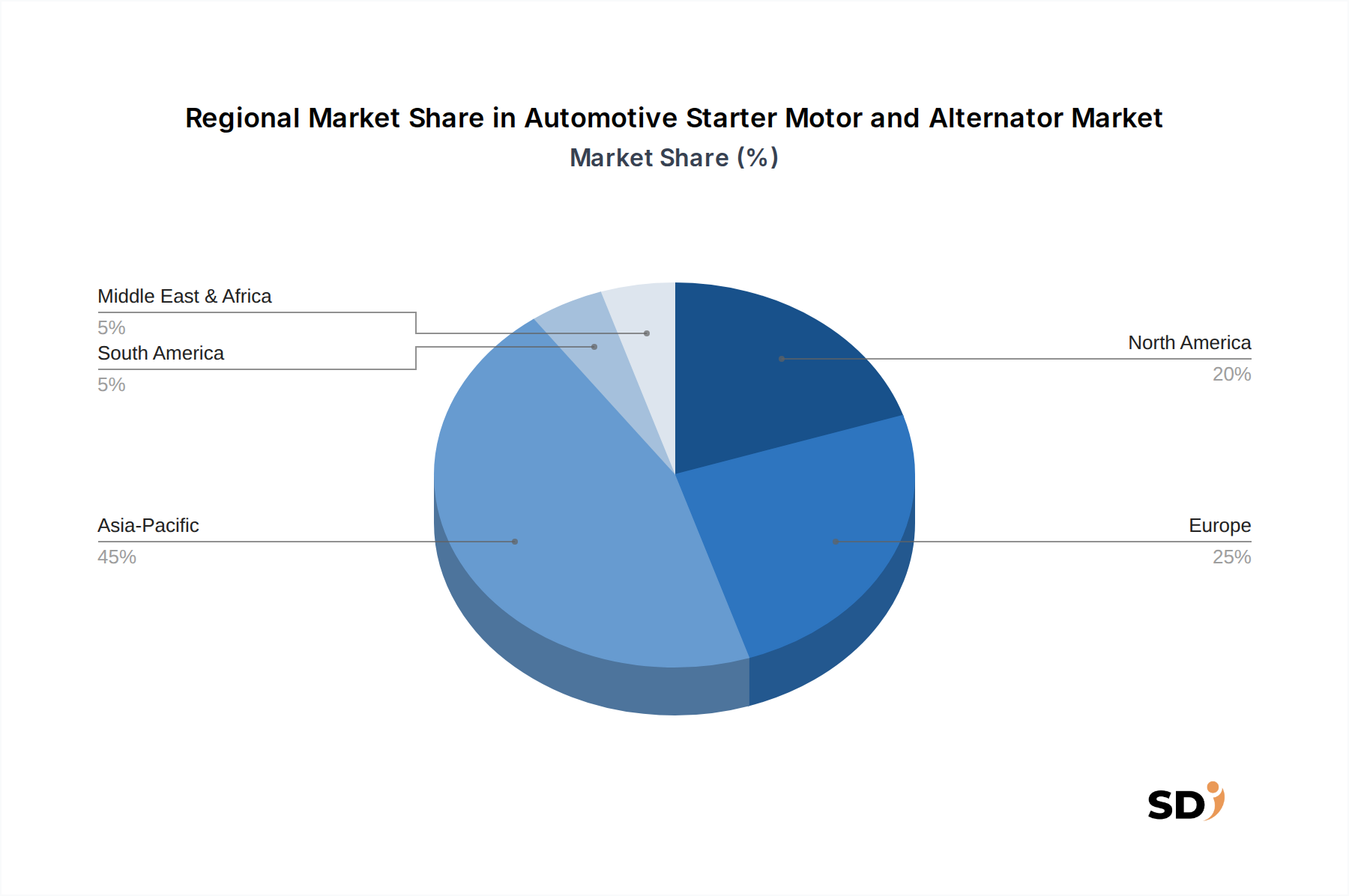

Regional Market Breakdown for Automotive Starter Motor and Alternator Market

The global Automotive Starter Motor and Alternator Market exhibits distinct regional dynamics, influenced by varying levels of vehicle production, aftermarket demand, and regulatory landscapes. Analyzing key regions provides insight into areas of robust growth and mature market characteristics.

Asia Pacific currently holds the largest revenue share and is projected to be the fastest-growing region in the Automotive Starter Motor and Alternator Market. Countries like China, India, Japan, and South Korea contribute significantly due to their high volumes of automotive manufacturing and a rapidly expanding vehicle parc. The primary demand driver here is the sustained increase in new vehicle sales, fueling both OEM and aftermarket segments, with millions of new Passenger Vehicle Market and Commercial Vehicle Market units produced annually. Furthermore, the increasing disposable income in these economies leads to higher vehicle ownership rates and a subsequent rise in maintenance and replacement demand. The region's estimated CAGR is expected to slightly exceed the global average, driven by robust industrialization and urbanization.

Europe represents a mature but technologically advanced market. The region shows consistent demand, largely driven by strict emission regulations that encourage the adoption of fuel-efficient technologies such as start-stop systems and 48V Systems Market. These advanced systems require more sophisticated and durable starter motors and smart alternators. While new vehicle sales growth might be moderate compared to Asia Pacific, the focus on technological upgrades and the stable aftermarket contribute significantly. Europe also hosts a strong base of premium automotive manufacturers, who are early adopters of advanced power management solutions, bolstering the Automotive Electronics Market within the region.

North America is another mature market with a substantial installed base of vehicles, making the aftermarket a dominant segment. Demand is steady, primarily driven by vehicle replacement cycles and routine maintenance. Although new vehicle production is significant, the market is characterized by a strong emphasis on reliability and longevity of components. The adoption of new technologies like 48V systems is gradually increasing, albeit at a slightly slower pace than in Europe, as manufacturers adapt to regional consumer preferences and regulatory frameworks.

Middle East & Africa (MEA) and South America are emerging markets characterized by moderate growth. Increasing urbanization, infrastructure development, and growing affordability of vehicles are boosting new car sales. These regions predominantly demand conventional starter motors and alternators for a diverse fleet, with growing opportunities for aftermarket sales as the vehicle parc ages. The Automotive Battery Market is also closely tied to the demand for alternators in these regions, as reliable charging systems are crucial for vehicle operation in various environmental conditions.

Automotive Starter Motor and Alternator Segmentation

1. Product Type

1.1. Starter Motors

1.1.1. Conventional Starter Motors

1.1.2. Gear Reduction Starter Motors

1.1.3. Permanent Magnet Starter Motors

1.1.4. Others

1.2. Alternators

1.2.1. Conventional Alternators

1.2.2. Smart Alternators

1.2.3. High-Output Alternators

1.2.4. Others

2. Technology

2.1. 12V Systems

2.2. 24V Systems

2.3. 48V Systems

2.4. Others

3. Application

3.1. Engine Starting

3.2. Battery Charging

3.3. Start-Stop Systems

3.4. Regenerative Energy Recovery

3.5. Auxiliary Power Generation

4. Sales Channel

4.1. OEM

4.2. Aftermarket

Automotive Starter Motor and Alternator Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Automotive Starter Motor and Alternator REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 5.8% from 2020-2034

Segmentation

By Product Type

Starter Motors

Conventional Starter Motors

Gear Reduction Starter Motors

Permanent Magnet Starter Motors

Others

Alternators

Conventional Alternators

Smart Alternators

High-Output Alternators

Others

By Technology

12V Systems

24V Systems

48V Systems

Others

By Application

Engine Starting

Battery Charging

Start-Stop Systems

Regenerative Energy Recovery

Auxiliary Power Generation

By Sales Channel

OEM

Aftermarket

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Type

5.1.1. Starter Motors

5.1.1.1. Conventional Starter Motors

5.1.1.2. Gear Reduction Starter Motors

5.1.1.3. Permanent Magnet Starter Motors

5.1.1.4. Others

5.1.2. Alternators

5.1.2.1. Conventional Alternators

5.1.2.2. Smart Alternators

5.1.2.3. High-Output Alternators

5.1.2.4. Others

5.2. Market Analysis, Insights and Forecast - by Technology

5.2.1. 12V Systems

5.2.2. 24V Systems

5.2.3. 48V Systems

5.2.4. Others

5.3. Market Analysis, Insights and Forecast - by Application

5.3.1. Engine Starting

5.3.2. Battery Charging

5.3.3. Start-Stop Systems

5.3.4. Regenerative Energy Recovery

5.3.5. Auxiliary Power Generation

5.4. Market Analysis, Insights and Forecast - by Sales Channel

5.4.1. OEM

5.4.2. Aftermarket

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Product Type

6.1.1. Starter Motors

6.1.1.1. Conventional Starter Motors

6.1.1.2. Gear Reduction Starter Motors

6.1.1.3. Permanent Magnet Starter Motors

6.1.1.4. Others

6.1.2. Alternators

6.1.2.1. Conventional Alternators

6.1.2.2. Smart Alternators

6.1.2.3. High-Output Alternators

6.1.2.4. Others

6.2. Market Analysis, Insights and Forecast - by Technology

6.2.1. 12V Systems

6.2.2. 24V Systems

6.2.3. 48V Systems

6.2.4. Others

6.3. Market Analysis, Insights and Forecast - by Application

6.3.1. Engine Starting

6.3.2. Battery Charging

6.3.3. Start-Stop Systems

6.3.4. Regenerative Energy Recovery

6.3.5. Auxiliary Power Generation

6.4. Market Analysis, Insights and Forecast - by Sales Channel

6.4.1. OEM

6.4.2. Aftermarket

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Product Type

7.1.1. Starter Motors

7.1.1.1. Conventional Starter Motors

7.1.1.2. Gear Reduction Starter Motors

7.1.1.3. Permanent Magnet Starter Motors

7.1.1.4. Others

7.1.2. Alternators

7.1.2.1. Conventional Alternators

7.1.2.2. Smart Alternators

7.1.2.3. High-Output Alternators

7.1.2.4. Others

7.2. Market Analysis, Insights and Forecast - by Technology

7.2.1. 12V Systems

7.2.2. 24V Systems

7.2.3. 48V Systems

7.2.4. Others

7.3. Market Analysis, Insights and Forecast - by Application

7.3.1. Engine Starting

7.3.2. Battery Charging

7.3.3. Start-Stop Systems

7.3.4. Regenerative Energy Recovery

7.3.5. Auxiliary Power Generation

7.4. Market Analysis, Insights and Forecast - by Sales Channel

7.4.1. OEM

7.4.2. Aftermarket

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Product Type

8.1.1. Starter Motors

8.1.1.1. Conventional Starter Motors

8.1.1.2. Gear Reduction Starter Motors

8.1.1.3. Permanent Magnet Starter Motors

8.1.1.4. Others

8.1.2. Alternators

8.1.2.1. Conventional Alternators

8.1.2.2. Smart Alternators

8.1.2.3. High-Output Alternators

8.1.2.4. Others

8.2. Market Analysis, Insights and Forecast - by Technology

8.2.1. 12V Systems

8.2.2. 24V Systems

8.2.3. 48V Systems

8.2.4. Others

8.3. Market Analysis, Insights and Forecast - by Application

8.3.1. Engine Starting

8.3.2. Battery Charging

8.3.3. Start-Stop Systems

8.3.4. Regenerative Energy Recovery

8.3.5. Auxiliary Power Generation

8.4. Market Analysis, Insights and Forecast - by Sales Channel

8.4.1. OEM

8.4.2. Aftermarket

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Product Type

9.1.1. Starter Motors

9.1.1.1. Conventional Starter Motors

9.1.1.2. Gear Reduction Starter Motors

9.1.1.3. Permanent Magnet Starter Motors

9.1.1.4. Others

9.1.2. Alternators

9.1.2.1. Conventional Alternators

9.1.2.2. Smart Alternators

9.1.2.3. High-Output Alternators

9.1.2.4. Others

9.2. Market Analysis, Insights and Forecast - by Technology

9.2.1. 12V Systems

9.2.2. 24V Systems

9.2.3. 48V Systems

9.2.4. Others

9.3. Market Analysis, Insights and Forecast - by Application

9.3.1. Engine Starting

9.3.2. Battery Charging

9.3.3. Start-Stop Systems

9.3.4. Regenerative Energy Recovery

9.3.5. Auxiliary Power Generation

9.4. Market Analysis, Insights and Forecast - by Sales Channel

9.4.1. OEM

9.4.2. Aftermarket

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Product Type

10.1.1. Starter Motors

10.1.1.1. Conventional Starter Motors

10.1.1.2. Gear Reduction Starter Motors

10.1.1.3. Permanent Magnet Starter Motors

10.1.1.4. Others

10.1.2. Alternators

10.1.2.1. Conventional Alternators

10.1.2.2. Smart Alternators

10.1.2.3. High-Output Alternators

10.1.2.4. Others

10.2. Market Analysis, Insights and Forecast - by Technology

10.2.1. 12V Systems

10.2.2. 24V Systems

10.2.3. 48V Systems

10.2.4. Others

10.3. Market Analysis, Insights and Forecast - by Application

10.3.1. Engine Starting

10.3.2. Battery Charging

10.3.3. Start-Stop Systems

10.3.4. Regenerative Energy Recovery

10.3.5. Auxiliary Power Generation

10.4. Market Analysis, Insights and Forecast - by Sales Channel

10.4.1. OEM

10.4.2. Aftermarket

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Valeo Group

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Denso Corporation

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. The Bosch Group

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Mitsuba Corporation

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Mitsubishi Electric Corporation

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Lucas Electricals

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Controlled Power Technologies

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Hella KGaAHueck&

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. ASIMCO Technologies

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Hitachi Automotive Systems

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Cummins

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. SEG Automotive GmbH

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. Others

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Product Type 2025 & 2033

Figure 3: Revenue Share (%), by Product Type 2025 & 2033

Figure 4: Revenue (million), by Technology 2025 & 2033

Figure 5: Revenue Share (%), by Technology 2025 & 2033

Figure 6: Revenue (million), by Application 2025 & 2033

Figure 7: Revenue Share (%), by Application 2025 & 2033

Figure 8: Revenue (million), by Sales Channel 2025 & 2033

Figure 50: Revenue (million), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Product Type 2020 & 2033

Table 2: Revenue million Forecast, by Technology 2020 & 2033

Table 3: Revenue million Forecast, by Application 2020 & 2033

Table 4: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Revenue million Forecast, by Product Type 2020 & 2033

Table 7: Revenue million Forecast, by Technology 2020 & 2033

Table 8: Revenue million Forecast, by Application 2020 & 2033

Table 9: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 10: Revenue million Forecast, by Country 2020 & 2033

Table 11: Revenue (million) Forecast, by Application 2020 & 2033

Table 12: Revenue (million) Forecast, by Application 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue million Forecast, by Product Type 2020 & 2033

Table 15: Revenue million Forecast, by Technology 2020 & 2033

Table 16: Revenue million Forecast, by Application 2020 & 2033

Table 17: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue million Forecast, by Product Type 2020 & 2033

Table 23: Revenue million Forecast, by Technology 2020 & 2033

Table 24: Revenue million Forecast, by Application 2020 & 2033

Table 25: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 26: Revenue million Forecast, by Country 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue (million) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Revenue (million) Forecast, by Application 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue million Forecast, by Product Type 2020 & 2033

Table 37: Revenue million Forecast, by Technology 2020 & 2033

Table 38: Revenue million Forecast, by Application 2020 & 2033

Table 39: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 40: Revenue million Forecast, by Country 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Table 47: Revenue million Forecast, by Product Type 2020 & 2033

Table 48: Revenue million Forecast, by Technology 2020 & 2033

Table 49: Revenue million Forecast, by Application 2020 & 2033

Table 50: Revenue million Forecast, by Sales Channel 2020 & 2033

Table 51: Revenue million Forecast, by Country 2020 & 2033

Table 52: Revenue (million) Forecast, by Application 2020 & 2033

Table 53: Revenue (million) Forecast, by Application 2020 & 2033

Table 54: Revenue (million) Forecast, by Application 2020 & 2033

Table 55: Revenue (million) Forecast, by Application 2020 & 2033

Table 56: Revenue (million) Forecast, by Application 2020 & 2033

Table 57: Revenue (million) Forecast, by Application 2020 & 2033

Table 58: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Our comprehensive market analysis for the "Automotive Starter Motor and Alternator Market" employs a robust and multi-faceted research methodology designed to deliver highly accurate and actionable insights. The approach leverages a predominant focus on primary research, complemented by rigorous secondary data validation and advanced demand modeling techniques.

Automotive Original Equipment Manufacturers (OEMs)

25%

Automotive Aftermarket Distributors & Retailers

20%

Automotive System Integrators

10%

Specialized Material & Semiconductor Suppliers

10%

Primary Research

Primary research forms the cornerstone of our methodology, accounting for 70-80% of the overall research effort. This extensive engagement with industry participants ensures that our findings are grounded in real-time market dynamics, unvarnished perspectives, and proprietary data not available through public channels. Our primary research strategy involves in-depth interviews and discussions conducted across the value chain, targeting key stakeholders. This provides granular insights into market sizing, competitive landscape, technology adoption rates, pricing strategies, and future trends. Our interview program includes:

Automotive Original Equipment Manufacturers (OEMs)

Automotive Aftermarket Distributors & Retailers

Automotive System Integrators (especially for 48V systems)

Specialized Material & Semiconductor Suppliers (e.g., for magnetics, power electronics)

Key Stakeholders Interviewed:

VP/Director of Product Management

Head of Procurement/Purchasing

Senior Engineer/R&D Lead (Powertrain & Electrical Systems)

Aftermarket Sales Manager/Category Manager

Secondary Research & Industry Benchmarking

The remaining 20-30% of our research is dedicated to comprehensive secondary research and industry benchmarking. This phase provides a foundational understanding of the market, validates primary research findings, and fills any data gaps. Our secondary research draws from a wide array of credible sources, strictly avoiding data from other market research websites. Key sources include:

Company Annual Reports & Investor Presentations: Publicly available financial statements and strategic outlooks of key market participants.

Academic Research & White Papers: Peer-reviewed studies on automotive electrical systems, materials science, and emerging technologies.

Demand Modeling & Market Estimation

Our market size estimation and forecasting leverage a combination of top-down and bottom-up methodologies, followed by multi-level data triangulation to ensure robustness. The bottom-up approach starts by segmenting the market at a granular level and aggregating these figures to derive the total market size. Key metrics and variables utilized for bottom-up market sizing include:

Vehicle Production Volumes: Disaggregated by vehicle type (passenger cars, LCVs, HCVs) and region, multiplied by the average number of starter motors/alternators per vehicle (considering traditional ICE and mild-hybrid configurations).

Average Selling Price (ASP) per Unit: Differentiated by product type (starter motor, alternator), technology (12V, 24V, 48V), and application, factoring in regional variations and sales channel (OEM vs. Aftermarket).

Aftermarket Replacement Rate/Cycle: Calculated based on average product lifespan, vehicle parc age, and regional maintenance practices.

Vehicle Parc (Fleet Size) by Region/Country: Provides the total addressable market for aftermarket demand over the forecast period.

The top-down approach validates these figures by assessing the overall automotive production outlook, economic indicators, and general industry trends. Data triangulation involves cross-referencing findings from primary interviews, secondary sources, and our quantitative models across various market segments and geographical regions. This iterative process refines market estimates and ensures consistency.

Data Accuracy & Quality Check

We guarantee an estimated data accuracy level of 85-90%. This high level of precision is achieved through our rigorous methodology, which includes:

Expert Validation: All market estimates and forecasts are critically reviewed by a panel of internal subject matter experts and, where appropriate, external industry consultants.

Cross-Verification: Information gathered from primary interviews is cross-referenced with multiple secondary sources and quantitative models.

Scenario Analysis: We employ various market growth scenarios (optimistic, conservative, realistic) to account for potential market fluctuations and provide a robust forecast range.

Continuous Updates: Every report is dynamically updated to reflect the latest market conditions, technological advancements, and regulatory changes up to the exact date of purchase, ensuring our clients receive the most current and relevant information available.

Frequently Asked Questions

1. How do sustainability factors influence the Automotive Starter Motor and Alternator market?

Growing demands for fuel efficiency and reduced emissions drive innovation in efficient starter motors and smart alternators. Manufacturers like Valeo Group and Denso Corporation focus on optimizing component lifespan and material recyclability to align with ESG goals.

2. What are the key export-import dynamics for automotive starter motors and alternators?

Global automotive supply chains, led by players like The Bosch Group, result in significant cross-border trade. Regional manufacturing hubs, particularly in Asia-Pacific and Europe, facilitate both OEM and aftermarket supply, influencing international trade flows.

3. What major challenges impact the Automotive Starter Motor and Alternator market?

The transition towards electric vehicles (EVs) presents a primary restraint, potentially reducing demand for conventional components. Additionally, raw material price volatility and supply chain vulnerabilities, seen across the automotive sector, pose ongoing risks.

4. Which recent technological developments affect starter motor and alternator products?

Evolution includes the proliferation of 48V systems for mild hybrids and advanced start-stop applications to enhance fuel economy. Companies like SEG Automotive GmbH and Mitsubishi Electric Corporation are innovating in high-efficiency and smart alternator technologies.

5. What is the projected valuation and growth rate of the Automotive Starter Motor and Alternator market?

The market is projected to reach $1873.8 million, demonstrating a Compound Annual Growth Rate (CAGR) of 5.8%. This growth is driven by the continued demand in conventional and mild-hybrid vehicle segments through 2033.

6. Are there notable investment trends or venture capital interests in this sector?

Investment primarily focuses on research and development by established players such as Hitachi Automotive Systems, enhancing product efficiency and integrating new technologies like 48V systems. Venture capital interest is limited in this mature component segment, with major funding coming from corporate R&D budgets.