Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Automotive Piston Rings Market: Growth Trends to 2033

Automotive Piston Rings

Automotive Piston Rings Market: Growth Trends to 2033

Automotive Piston Rings by Ring Type (Compression Rings, Oil Control Rings, Scraper Rings, Others), by Material Type (Cast Iron Piston Rings, Ductile Iron Piston Rings, Steel Piston Rings, Others), by Coating Type (Chromium-Coated Rings, Molybdenum-Coated Rings, Ceramic-Coated Rings, Others), by Sales Channel (OEM, Aftermarket), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 8, 2026|Base Year : 2025|Pages : 111

Key Insights into the Automotive Piston Rings Market

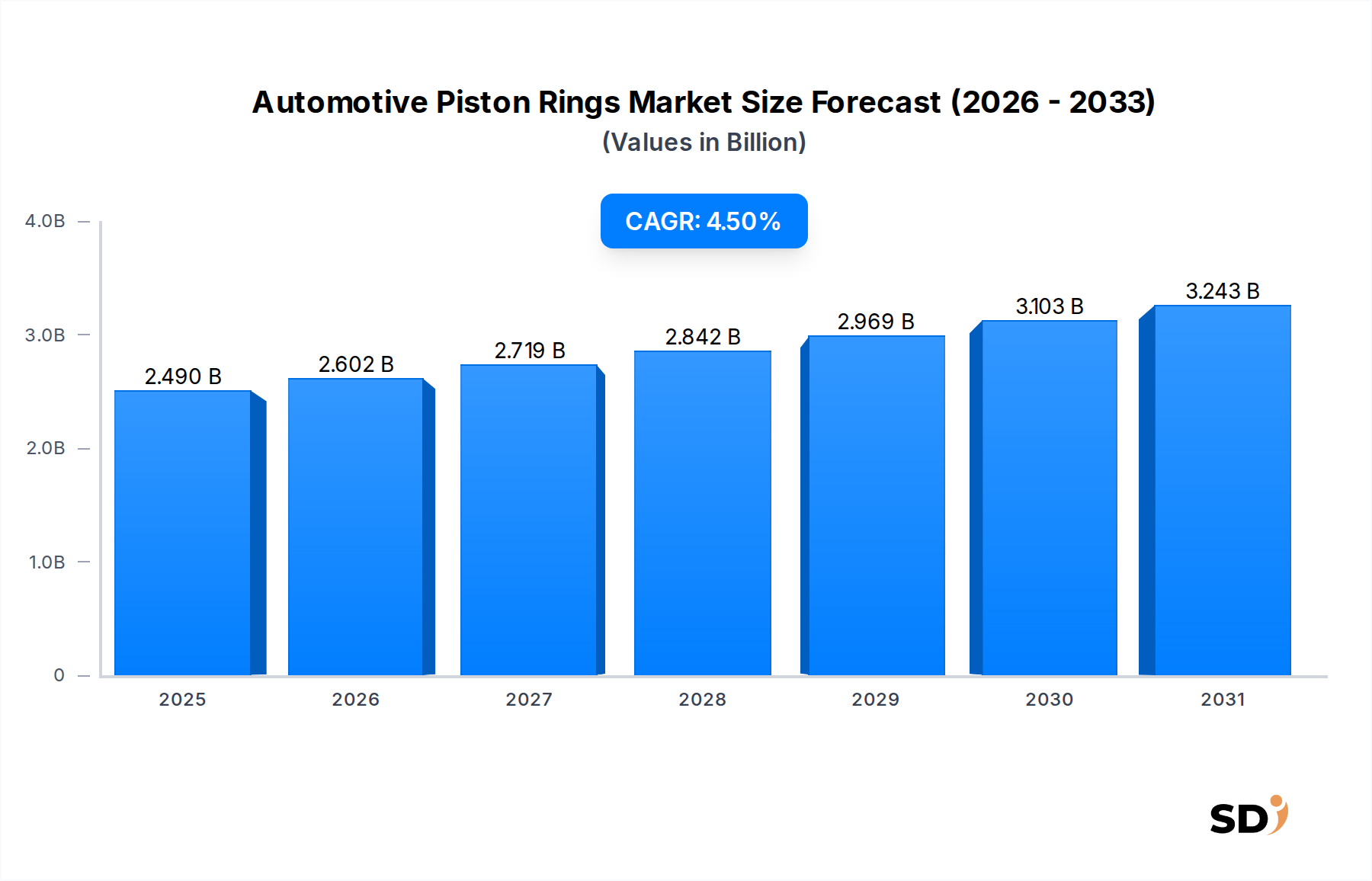

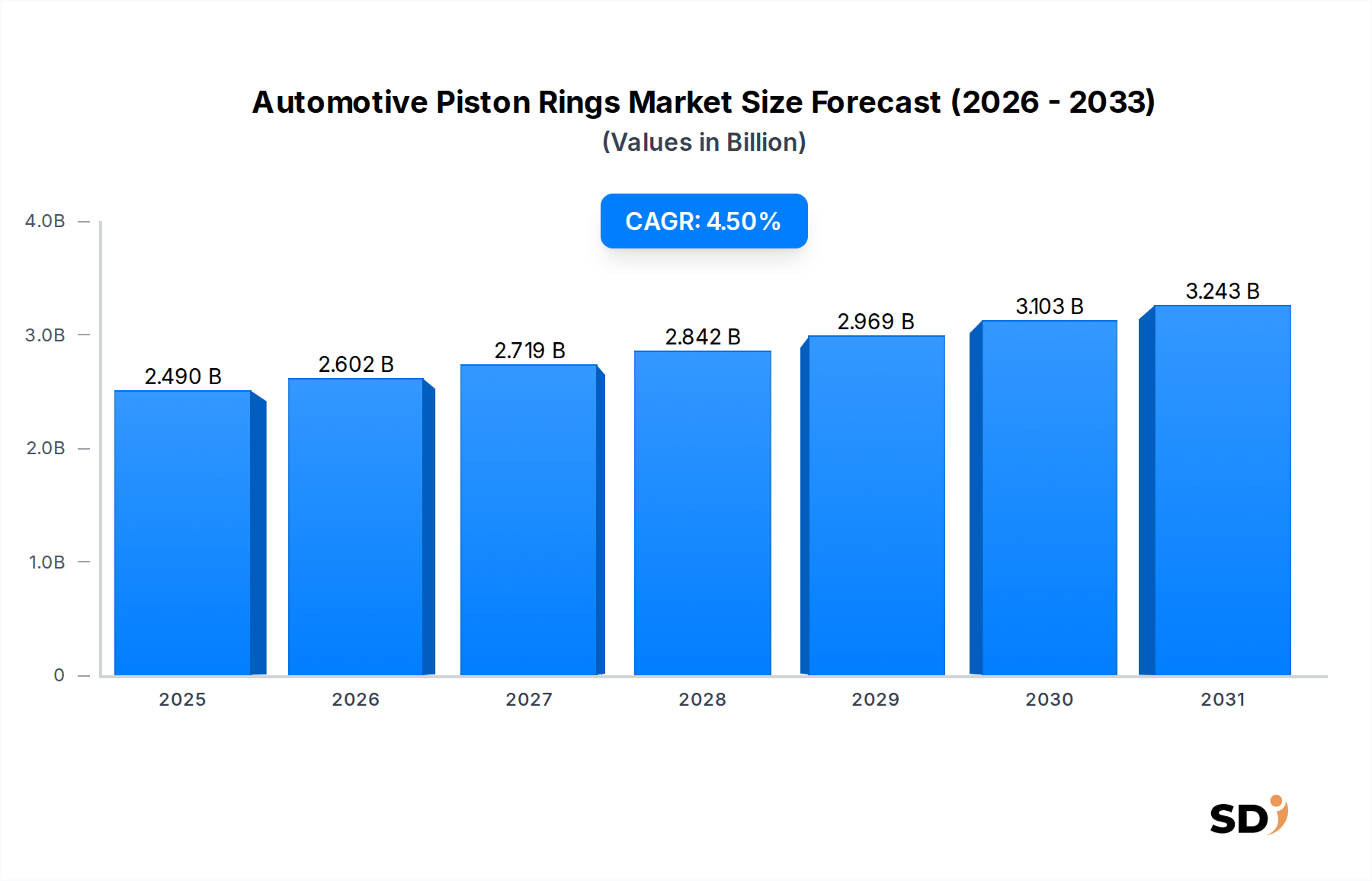

The Global Automotive Piston Rings Market demonstrated a valuation of $2.49 billion in 2023, with projections indicating a compound annual growth rate (CAGR) of 4.5% through the forecast period. This trajectory is expected to lead the market to approximately $3.38 billion by 2030. The market's resilience is underpinned by the enduring demand within the Internal Combustion Engine Market, particularly in hybrid vehicle powertrains and the robust Automotive Aftermarket. Despite the escalating global shift towards electrification, the pervasive nature of existing internal combustion engine (ICE) vehicles and continuous production of hybrid variants ensure sustained demand for piston rings.

Automotive Piston Rings Market Size (In Billion)

4.0B

3.0B

2.0B

1.0B

0

2.490 B

2025

2.602 B

2026

2.719 B

2027

2.842 B

2028

2.969 B

2029

3.103 B

2030

3.243 B

2031

Key drivers include increasingly stringent emission regulations, which necessitate advanced piston ring designs for enhanced sealing, reduced friction, and improved fuel efficiency. Moreover, the expanding global vehicle parc directly contributes to the growth of the Automotive Aftermarket, as aging vehicles require regular component replacements, including piston rings. Technological advancements in material science, such as the development of specialized alloys and sophisticated coating techniques (e.g., chromium, molybdenum, and ceramic coatings), are pivotal in meeting these evolving performance demands. These innovations are critical for optimizing engine performance and extending component lifespan. The OEM segment continues to represent a substantial share, driven by new vehicle production, while the aftermarket segment, fueled by maintenance and repair, provides a stable revenue stream. Regional growth is notably strong in Asia Pacific, propelled by high volume automotive manufacturing and a burgeoning middle class, alongside significant contributions from North America and Europe, which prioritize performance and emission compliance. Overall, while the Automotive Piston Rings Market faces strategic shifts due to electrification, its immediate and medium-term outlook remains positive, driven by technological evolution and persistent demand for efficient engine components within the broader Automotive Components Market.

Dominant Segment Analysis in Automotive Piston Rings Market

The dominant segment within the Automotive Piston Rings Market, based on ring type, is unequivocally the Compression Rings segment. This category, further delineated into Top Compression Rings and Second Compression Rings, holds the largest revenue share due to its critical function in an internal combustion engine. Compression rings are fundamental for sealing the combustion chamber, preventing the escape of combustion gases into the crankcase, and transferring heat from the piston to the cylinder wall. Their direct impact on engine performance, fuel efficiency, and emissions control makes them indispensable components. Top Compression Rings, specifically, bear the brunt of the combustion pressure and high temperatures, demanding robust materials and advanced designs.

The dominance of compression rings is multifaceted. Firstly, their direct correlation with engine power output and efficiency means that even minor improvements in their design or material can yield significant performance gains, thus driving continuous innovation. Secondly, stringent global emission standards, such as Euro 7 and CAFE regulations, compel manufacturers to integrate high-performance compression rings that minimize blow-by and oil consumption, thereby reducing particulate emissions. This regulatory pressure contributes substantially to the segment's ongoing growth and technological evolution. Major players like MAHLE GmbH, Tenneco (Federal-Mogul), and NIPPON PISTON RING invest heavily in the research and development of these critical components, focusing on low-friction coatings and specialized materials to enhance durability and efficiency. The adoption of advanced Steel Piston Rings Market solutions, particularly for top compression rings in high-performance and heavy-duty applications, exemplifies the segment's focus on material innovation.

While the Oil Control Rings segment is also vital for preventing excessive oil consumption, its design and function are secondary to the primary sealing role of compression rings, especially Top Compression Rings. The growth in the Passenger Vehicles Market and Commercial Vehicles Market across all regions directly translates to higher demand for compression rings in both OEM and Automotive Aftermarket channels. OEMs prioritize precision-engineered compression rings for new vehicle assemblies to meet initial performance benchmarks and warranty requirements. Meanwhile, the aftermarket sustains demand for replacement compression rings, as they are subject to significant wear over an engine's lifespan, directly impacting engine longevity and performance. The Cast Iron Piston Rings Market also plays a significant role in this segment for cost-effective, durable solutions, particularly in certain vehicle types and regions. The segment's market share is not only significant but also poised for sustained growth, driven by technological advancements and the foundational role compression rings play in every internal combustion engine.

Key Market Drivers and Constraints for Automotive Piston Rings Market Growth

The Automotive Piston Rings Market is shaped by a confluence of powerful drivers and notable constraints, dictating its growth trajectory:

Increasing Global Vehicle Production and Parc: Despite the surge in electric vehicles, global automotive production, particularly in emerging economies and the continued manufacturing of hybrid vehicles, sustains substantial OEM demand for piston rings. For instance, global light vehicle production was estimated at over 85 million units in 2023, directly fueling the need for Engine Components Market in new vehicles. Concurrently, an expanding global vehicle parc, which has surpassed 1.4 billion units, directly translates into consistent replacement demand for the Automotive Aftermarket, driven by maintenance cycles and wear.

Stringent Emission Regulations: Regulatory bodies worldwide continue to tighten emission standards, such as Euro 7 in Europe, CAFE standards in North America, and China 6. These regulations mandate significant improvements in engine efficiency and reductions in pollutant emissions. Piston ring manufacturers are thus compelled to innovate, developing advanced low-friction and high-sealing designs, often involving sophisticated coatings (e.g., Ceramic-Coated Rings) and materials, to meet these compliance requirements. This directly influences the evolution of the Automotive Engine Management System Market by requiring precise control over combustion and emissions.

Technological Advancements in Hybrid Powertrains: The proliferation of hybrid electric vehicles (HEVs) ensures the continued relevance of the Internal Combustion Engine Market. HEV engines, which cycle between on and off states, place unique demands on piston rings, requiring enhanced durability, wear resistance, and reduced friction to support frequent start-stop operations and optimize fuel economy. This provides a specialized growth avenue for advanced piston ring technologies.

Constraints:

Accelerated Electrification of the Automotive Industry: The most significant long-term constraint is the rapid global shift towards Battery Electric Vehicles (BEVs), which do not utilize internal combustion engines. While hybrid vehicles mitigate some impact, the projected decline in pure ICE vehicle production will inevitably diminish the overall addressable market for automotive piston rings in the long run.

Enhanced Durability and Lifespan of Piston Rings: Continuous advancements in material science, manufacturing precision, and coating technologies have significantly extended the operational lifespan of modern piston rings. While beneficial for consumers, this increased durability can slow down replacement cycles in the Automotive Aftermarket, potentially tempering growth.

Raw Material Price Volatility: The manufacturing of piston rings relies on various materials, including cast iron and steel. Fluctuations in the global Cast Iron Market or specialty steel prices can directly impact production costs and profit margins for manufacturers, posing a challenge for stable pricing strategies and supply chain management.

Competitive Ecosystem of Automotive Piston Rings Market

The Automotive Piston Rings Market is characterized by the presence of several established global and regional players, alongside specialized manufacturers. The competitive landscape is driven by innovation in materials, coating technologies, and design optimization to meet evolving performance and emission standards. Key companies shaping this ecosystem include:

ASIMCO: A global supplier of automotive components, ASIMCO is recognized for its precision-engineered piston rings that cater to both the OEM and aftermarket segments, maintaining a focus on performance and durability across diverse engine applications.

Tenneco(Federal-Mogul): A leading global supplier of powertrain components, Tenneco's Federal-Mogul brand offers an extensive portfolio of piston rings, leveraging advanced materials and coatings to enhance engine efficiency and reduce emissions for Passenger Vehicles Market and Commercial Vehicles Market.

MAHLE GmbH: As a prominent international development partner and supplier to the automotive industry, MAHLE GmbH specializes in high-performance piston systems, including advanced piston rings, known for their innovative designs and contribution to fuel economy.

NIPPON PISTON RING: A major Japanese manufacturer, NIPPON PISTON RING boasts a strong heritage in piston ring technology, offering a wide array of products engineered for various engine types and demanding operational conditions.

RIKEN CORPORATION: RIKEN CORPORATION is distinguished by its robust R&D capabilities in materials science and manufacturing, producing high-quality piston rings and sealing solutions that meet stringent industry standards.

IP Rings: An Indian automotive component manufacturer, IP Rings serves both domestic and international OEMs, focusing on delivering reliable and cost-effective piston ring solutions for a broad range of automotive applications.

Shriram Pistons & Rings: A key player in the Indian automotive components sector, Shriram Pistons & Rings provides a comprehensive range of piston rings and associated engine parts, emphasizing quality and technological advancement.

TPR: A Japanese leader in precision engine components, TPR is known for its advanced metallurgical solutions and innovative piston ring designs that contribute to the efficiency and longevity of internal combustion engines.

Hunan ZhengYuanDongli Parts: This Chinese manufacturer is steadily expanding its footprint in the automotive parts market, offering a variety of piston rings and engine components to cater to regional and international demand.

SamKrg: An emerging participant in the Engine Components Market, SamKrg contributes to the regional supply chain, focusing on delivering competitive piston ring solutions.

Anhui Ring New Group: A significant Chinese producer, Anhui Ring New Group manufactures a diverse range of piston rings and other engine components, establishing a strong presence in the domestic and export markets.

Grover: Often specializing in particular ring types or niche applications, Grover provides tailored piston ring solutions with a focus on specific performance requirements.

Abilities India PIston & Rings: An Indian firm dedicated to the production of precision piston rings, Abilities India focuses on meeting the diverse needs of various engine types within the automotive sector.

Others: This category encompasses numerous smaller, regional, and specialized manufacturers who collectively contribute to the market's diversity and supply chain flexibility.

Recent Developments & Milestones in Automotive Piston Rings Market

Recent developments in the Automotive Piston Rings Market highlight a concerted effort towards enhancing performance, sustainability, and market reach:

Q4 2023: A leading global piston ring manufacturer introduced new low-friction coating technologies based on Diamond-Like Carbon (DLC), specifically designed for heavy-duty Commercial Vehicles Market. This innovation aims to significantly improve fuel efficiency and reduce CO2 emissions, addressing stringent environmental regulations.

Q2 2024: A major European OEM announced a strategic partnership with a prominent piston ring supplier to co-develop advanced ring designs for their next-generation hybrid electric vehicle powertrains. This collaboration emphasizes optimization for frequent start-stop operation and improved durability in the Internal Combustion Engine Market.

Q1 2024: Several key players in the Steel Piston Rings Market segment announced substantial investments in automated manufacturing lines, particularly in Asia Pacific. This expansion aims to boost production capacity and enhance precision engineering, responding to the growing demand from high-performance engine applications.

Q3 2023: Extensive research initiatives were launched across the industry to explore sustainable material alternatives and manufacturing processes for piston rings. This includes investigations into recycled content and lower-energy production methods to reduce the environmental footprint of Engine Components Market.

Q1 2023: A global supplier introduced a new line of specialized aftermarket piston ring kits tailored for extending the life and optimizing the performance of older Passenger Vehicles Market models. These kits leverage advanced metallurgy and coating technologies, providing enhanced repair solutions for the Automotive Aftermarket.

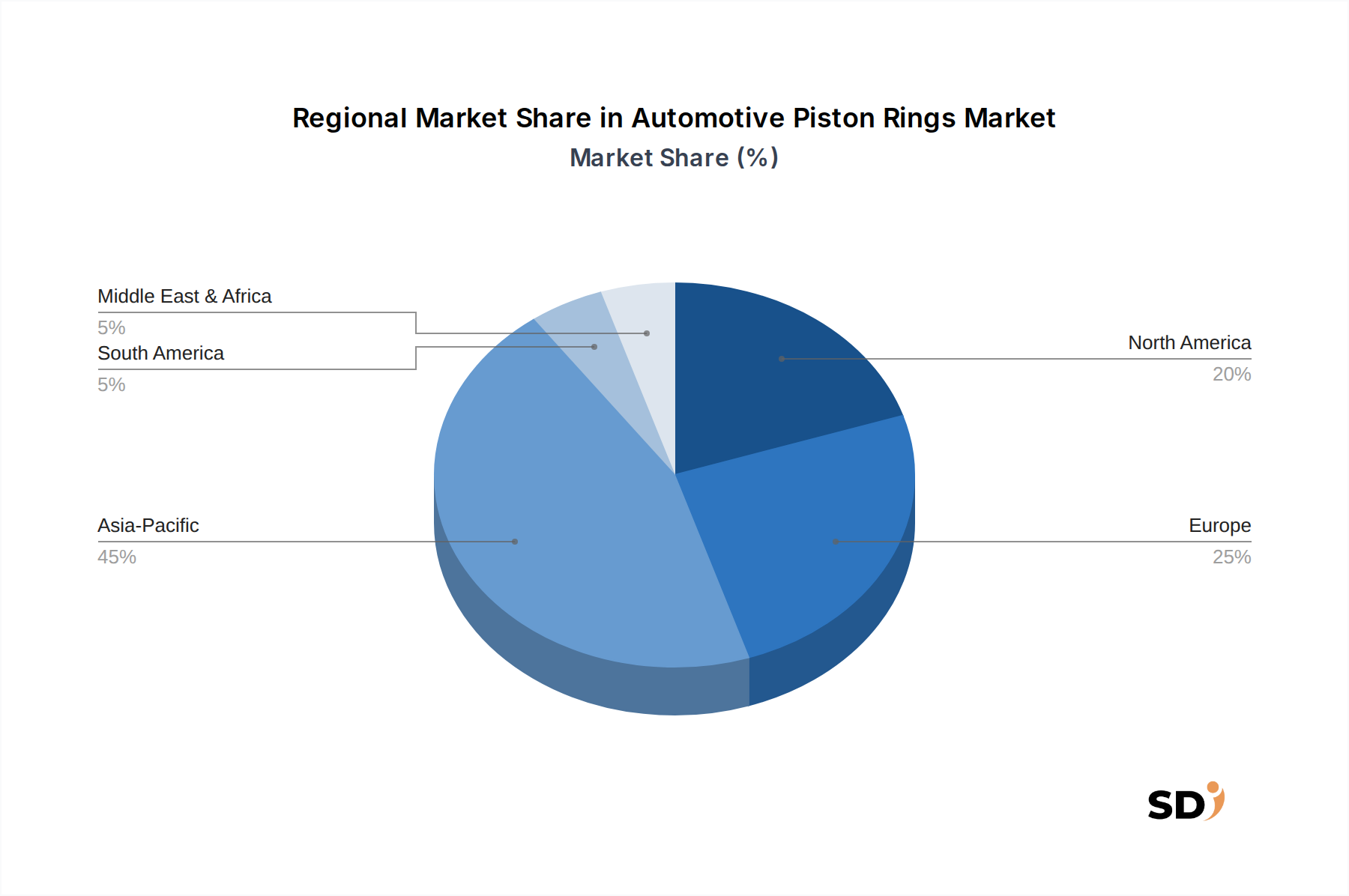

Regional Market Breakdown for Automotive Piston Rings Market

The global Automotive Piston Rings Market exhibits distinct regional dynamics, influenced by varying vehicle production volumes, regulatory frameworks, and aftermarket demand. The overall market growth of 4.5% CAGR is a weighted average of these regional performances.

Asia Pacific: This region accounts for the largest share of the Automotive Piston Rings Market, estimated at approximately 40%-45% of global revenue, and is also the fastest-growing segment with an estimated CAGR of 5.8%. The dominance is primarily driven by high-volume automotive manufacturing hubs in China, India, Japan, and South Korea. These countries are experiencing significant growth in both Passenger Vehicles Market and Commercial Vehicles Market production. Furthermore, a rapidly expanding middle class and increasing vehicle parc fuel robust demand in the Automotive Aftermarket. Stringent emission norms in these countries also necessitate the adoption of advanced piston ring technologies, contributing to higher market value.

Europe: Representing a significant portion of the market, around 25%-30%, Europe is a mature market projected to grow at a moderate CAGR of approximately 3.5%. The region's growth is primarily propelled by stringent emission regulations (e.g., Euro 7), which drive demand for high-performance, low-friction piston rings in new vehicles. The strong presence of premium automotive brands and a well-established Automotive Aftermarket also contribute to stable demand. Innovation in hybrid powertrain solutions further supports the Internal Combustion Engine Market within this technologically advanced region.

North America: This region holds a substantial market share, estimated between 18%-22%, with a stable growth rate anticipated around 3.2% CAGR. The primary demand drivers include a large existing vehicle parc, which ensures consistent demand for replacement piston rings in the Automotive Aftermarket. Additionally, the robust Commercial Vehicles Market and ongoing innovations in engine technologies to meet fuel economy standards contribute to the market's stability. Investment in advanced Engine Components Market is a constant.

Middle East & Africa (MEA) and South America: These regions collectively represent emerging markets with a combined share of roughly 10%-15%. Growth rates vary but are generally higher than mature markets, driven by increasing motorization rates, infrastructure development, and growing disposable incomes. While Cast Iron Piston Rings Market might dominate in terms of volume for more budget-conscious segments, there is a gradual shift towards more advanced materials as vehicle technology progresses.

Technology Innovation Trajectory in Automotive Piston Rings Market

The Automotive Piston Rings Market is undergoing significant technological evolution, primarily driven by the imperative to enhance engine efficiency, reduce emissions, and extend component lifespan. Two to three key disruptive technologies are shaping this trajectory:

Advanced Surface Coatings: Technologies such as Diamond-Like Carbon (DLC), Physical Vapor Deposition (PVD), and Plasma Nitriding are increasingly being applied to piston rings. These coatings drastically reduce friction, improve wear resistance, and enhance corrosion protection, which is crucial for meeting stringent emission standards and optimizing fuel efficiency in the Internal Combustion Engine Market. R&D investments in this area are substantial, with adoption timelines being immediate for high-performance and premium engine applications, gradually filtering into the mass market. These innovations reinforce incumbent manufacturers by allowing them to offer superior products that meet evolving regulatory and performance demands, especially for Steel Piston Rings Market applications.

Novel Material Development: Beyond traditional cast iron and steel, the industry is exploring advanced alloys and composite materials. Lighter, stronger, and more thermally stable materials are under development to withstand the extreme conditions within modern engines, particularly in turbocharged and downsized units. This includes specialized high-strength steels, ceramic-metal matrix composites, and advanced Cast Iron Piston Rings Market alloys with improved microstructure. R&D in this field is intense, often involving collaborations between material scientists and engine designers. Adoption timelines are typically longer due to rigorous testing and validation processes, but these materials are crucial for achieving next-generation performance benchmarks. They primarily reinforce the business models of incumbent manufacturers capable of investing in complex material science.

Smart Piston Rings and Sensor Integration (Emerging): Although still largely in the R&D phase, the concept of "smart" piston rings integrating miniature sensors is gaining traction. These sensors could monitor real-time parameters such as ring wear, temperature, pressure, and lubrication effectiveness. This technology holds the potential to revolutionize predictive maintenance, engine diagnostics, and even adaptive engine control, significantly impacting the Automotive Engine Management System Market. While adoption is likely several years away, it represents a disruptive threat to traditional component sales, shifting focus from reactive replacement to proactive monitoring and optimization. Early investments are being made by pioneering research institutions and forward-thinking industry players.

The Automotive Piston Rings Market is profoundly influenced by a complex web of global regulatory frameworks, standards bodies, and governmental policies, primarily focused on environmental protection and vehicle performance. These policies act as significant catalysts for innovation and market direction:

Global Emission Standards: The most impactful regulations are global emission standards, including Euro 6/7 (Europe), CAFE standards and EPA regulations (United States), China 6, Bharat Stage VI (India), and equivalent norms in Japan and other regions. These standards mandate drastic reductions in greenhouse gas emissions (CO2, NOx, particulate matter) and improvements in fuel economy. For piston rings, this translates into a relentless drive for lower friction, superior sealing capabilities, and reduced oil consumption. Regulatory updates, such as the upcoming Euro 7, compel manufacturers to invest heavily in advanced Engine Components Market designs, materials, and coatings to achieve compliance. Non-compliance results in significant penalties and market access restrictions, thus policy changes directly dictate product specifications and R&D priorities.

Fuel Economy Regulations: Complementary to emission standards are fuel economy mandates, which push for overall vehicle efficiency. Piston rings, being critical for minimizing parasitic losses within the engine, play a direct role in meeting these targets. Policies encouraging lightweighting and reduced engine friction inherently promote the development and adoption of advanced piston ring technologies, including specialized Steel Piston Rings Market solutions.

Noise, Vibration, and Harshness (NVH) Standards: While not directly regulating piston rings, NVH standards indirectly influence their design. Smoother engine operation, partly achieved through optimized piston ring dynamics, contributes to reduced engine noise and vibration, thereby affecting the overall perception of vehicle quality and comfort in the Passenger Vehicles Market and Commercial Vehicles Market.

End-of-Life Vehicle (ELV) Directives and Circular Economy Policies: Regulations like the European ELV Directive promote recycling and reuse of automotive components. While piston rings are small, increasing emphasis on circular economy principles may, in the long term, influence material selection and manufacturing processes to facilitate easier recycling or promote the use of recycled content, impacting the Automotive Components Market broadly. Recent policy shifts consistently trend towards tighter environmental controls, demanding continuous innovation from piston ring manufacturers to balance performance, cost, and environmental impact.

Automotive Piston Rings Segmentation

1. Ring Type

1.1. Compression Rings

1.1.1. Top Compression Rings

1.1.2. Second Compression Rings

1.2. Oil Control Rings

1.3. Scraper Rings

1.4. Others

2. Material Type

2.1. Cast Iron Piston Rings

2.2. Ductile Iron Piston Rings

2.3. Steel Piston Rings

2.4. Others

3. Coating Type

3.1. Chromium-Coated Rings

3.2. Molybdenum-Coated Rings

3.3. Ceramic-Coated Rings

3.4. Others

4. Sales Channel

4.1. OEM

4.2. Aftermarket

Automotive Piston Rings Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Automotive Piston Rings REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 4.5% from 2020-2034

Segmentation

By Ring Type

Compression Rings

Top Compression Rings

Second Compression Rings

Oil Control Rings

Scraper Rings

Others

By Material Type

Cast Iron Piston Rings

Ductile Iron Piston Rings

Steel Piston Rings

Others

By Coating Type

Chromium-Coated Rings

Molybdenum-Coated Rings

Ceramic-Coated Rings

Others

By Sales Channel

OEM

Aftermarket

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Ring Type

5.1.1. Compression Rings

5.1.1.1. Top Compression Rings

5.1.1.2. Second Compression Rings

5.1.2. Oil Control Rings

5.1.3. Scraper Rings

5.1.4. Others

5.2. Market Analysis, Insights and Forecast - by Material Type

5.2.1. Cast Iron Piston Rings

5.2.2. Ductile Iron Piston Rings

5.2.3. Steel Piston Rings

5.2.4. Others

5.3. Market Analysis, Insights and Forecast - by Coating Type

5.3.1. Chromium-Coated Rings

5.3.2. Molybdenum-Coated Rings

5.3.3. Ceramic-Coated Rings

5.3.4. Others

5.4. Market Analysis, Insights and Forecast - by Sales Channel

5.4.1. OEM

5.4.2. Aftermarket

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Ring Type

6.1.1. Compression Rings

6.1.1.1. Top Compression Rings

6.1.1.2. Second Compression Rings

6.1.2. Oil Control Rings

6.1.3. Scraper Rings

6.1.4. Others

6.2. Market Analysis, Insights and Forecast - by Material Type

6.2.1. Cast Iron Piston Rings

6.2.2. Ductile Iron Piston Rings

6.2.3. Steel Piston Rings

6.2.4. Others

6.3. Market Analysis, Insights and Forecast - by Coating Type

6.3.1. Chromium-Coated Rings

6.3.2. Molybdenum-Coated Rings

6.3.3. Ceramic-Coated Rings

6.3.4. Others

6.4. Market Analysis, Insights and Forecast - by Sales Channel

6.4.1. OEM

6.4.2. Aftermarket

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Ring Type

7.1.1. Compression Rings

7.1.1.1. Top Compression Rings

7.1.1.2. Second Compression Rings

7.1.2. Oil Control Rings

7.1.3. Scraper Rings

7.1.4. Others

7.2. Market Analysis, Insights and Forecast - by Material Type

7.2.1. Cast Iron Piston Rings

7.2.2. Ductile Iron Piston Rings

7.2.3. Steel Piston Rings

7.2.4. Others

7.3. Market Analysis, Insights and Forecast - by Coating Type

7.3.1. Chromium-Coated Rings

7.3.2. Molybdenum-Coated Rings

7.3.3. Ceramic-Coated Rings

7.3.4. Others

7.4. Market Analysis, Insights and Forecast - by Sales Channel

7.4.1. OEM

7.4.2. Aftermarket

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Ring Type

8.1.1. Compression Rings

8.1.1.1. Top Compression Rings

8.1.1.2. Second Compression Rings

8.1.2. Oil Control Rings

8.1.3. Scraper Rings

8.1.4. Others

8.2. Market Analysis, Insights and Forecast - by Material Type

8.2.1. Cast Iron Piston Rings

8.2.2. Ductile Iron Piston Rings

8.2.3. Steel Piston Rings

8.2.4. Others

8.3. Market Analysis, Insights and Forecast - by Coating Type

8.3.1. Chromium-Coated Rings

8.3.2. Molybdenum-Coated Rings

8.3.3. Ceramic-Coated Rings

8.3.4. Others

8.4. Market Analysis, Insights and Forecast - by Sales Channel

8.4.1. OEM

8.4.2. Aftermarket

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Ring Type

9.1.1. Compression Rings

9.1.1.1. Top Compression Rings

9.1.1.2. Second Compression Rings

9.1.2. Oil Control Rings

9.1.3. Scraper Rings

9.1.4. Others

9.2. Market Analysis, Insights and Forecast - by Material Type

9.2.1. Cast Iron Piston Rings

9.2.2. Ductile Iron Piston Rings

9.2.3. Steel Piston Rings

9.2.4. Others

9.3. Market Analysis, Insights and Forecast - by Coating Type

9.3.1. Chromium-Coated Rings

9.3.2. Molybdenum-Coated Rings

9.3.3. Ceramic-Coated Rings

9.3.4. Others

9.4. Market Analysis, Insights and Forecast - by Sales Channel

9.4.1. OEM

9.4.2. Aftermarket

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Ring Type

10.1.1. Compression Rings

10.1.1.1. Top Compression Rings

10.1.1.2. Second Compression Rings

10.1.2. Oil Control Rings

10.1.3. Scraper Rings

10.1.4. Others

10.2. Market Analysis, Insights and Forecast - by Material Type

10.2.1. Cast Iron Piston Rings

10.2.2. Ductile Iron Piston Rings

10.2.3. Steel Piston Rings

10.2.4. Others

10.3. Market Analysis, Insights and Forecast - by Coating Type

10.3.1. Chromium-Coated Rings

10.3.2. Molybdenum-Coated Rings

10.3.3. Ceramic-Coated Rings

10.3.4. Others

10.4. Market Analysis, Insights and Forecast - by Sales Channel

10.4.1. OEM

10.4.2. Aftermarket

11. Competitive Analysis

11.1. Company Profiles

11.1.1. ASIMCO

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Tenneco(Federal-Mogul)

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. MAHLE GmbH

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. NIPPON PISTON RING

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. RIKEN CORPORATION

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. IP Rings

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Shriram Pistons & Rings

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. TPR

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Hunan ZhengYuanDongli Parts

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. SamKrg

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Anhui Ring New Group

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Grover

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. Abilities India PIston & Rings

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.1.14. Others

11.1.14.1. Company Overview

11.1.14.2. Products

11.1.14.3. Company Financials

11.1.14.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Ring Type 2025 & 2033

Figure 3: Revenue Share (%), by Ring Type 2025 & 2033

Figure 4: Revenue (billion), by Material Type 2025 & 2033

Figure 5: Revenue Share (%), by Material Type 2025 & 2033

Figure 6: Revenue (billion), by Coating Type 2025 & 2033

Figure 7: Revenue Share (%), by Coating Type 2025 & 2033

Figure 8: Revenue (billion), by Sales Channel 2025 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our market research approach for the Automotive Piston Rings market prioritizes primary research, constituting 75-80% of our total research efforts. This intensive engagement directly with industry stakeholders provides unparalleled insights into current market dynamics, emerging trends, technological advancements, and competitive landscapes. We conduct in-depth, structured interviews through a blend of telephone conversations, virtual meetings, and, where feasible, face-to-face discussions with key opinion leaders and industry experts across the value chain. Our interview strategy is designed to gather both quantitative data for market sizing and qualitative insights for strategic analysis, ensuring a comprehensive understanding of market nuances across various geographies and segmentation parameters.

Key stakeholders targeted for primary interviews include:

Product Development Managers / R&D Leads at piston ring manufacturing firms.

VP of Global Procurement / Supply Chain Directors within automotive engine manufacturers and OEMs.

Aftermarket Sales Directors / Category Managers at major automotive parts distributors.

Materials Science Engineers / Applications Specialists focused on advanced coatings and materials for piston rings.

Our primary respondents are carefully selected to ensure representation across the diverse ecosystem of the automotive piston rings market, encompassing key regions and market segments identified in the report title.

Secondary Research & Industry Benchmarking

Secondary research forms the foundational 20-25% of our methodology, providing essential groundwork and validation for our primary findings. This phase involves a meticulous review of an extensive array of publicly available and proprietary data sources. Our analysts leverage reputable financial databases such as Bloomberg, Factiva, Hoovers, and PitchBook to gather company-specific financial performance, strategic developments, and competitive intelligence. We also extensively consult government publications, regulatory whitepapers, and reports from recognized trade associations and organizations to ensure the highest level of authoritative data.

Key sources utilized include:

Government Publications: For economic indicators, manufacturing statistics, and automotive production data. (e.g., U.S. Census Bureau [www.census.gov], Eurostat [ec.europa.eu/eurostat])

Trade Association Reports: Providing industry-specific data, trends, and regulatory updates.

SAE International (Society of Automotive Engineers) [www.sae.org]

Automotive Aftermarket Suppliers Association (AASA) [www.aasa.org]

European Automobile Manufacturers' Association (ACEA) [www.acea.auto]

Company Annual Reports and Investor Presentations: For financial performance, product portfolios, and market strategies of key players.

Academic Research and Journals: For in-depth technical understanding of materials, coatings, and engine technologies.

This robust secondary research framework establishes market baselines, validates primary data points, and helps in identifying potential discrepancies or areas requiring further investigation.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies employ a rigorous combination of top-down and bottom-up approaches, complemented by multi-level data triangulation to ensure accuracy and reliability. The top-down approach involves estimating the total market size based on macroeconomic factors, automotive industry growth projections, and overall engine production trends, subsequently disaggregating this into various segments. Conversely, the bottom-up approach aggregates market size by building up from granular data points related to specific segments.

For the Automotive Piston Rings market, the bottom-up market size calculation is primarily driven by:

Annual New Vehicle Production Volumes: Segmented by vehicle type (passenger, commercial) and engine types (gasoline, diesel, hybrid), across all specified regions.

Average Piston Ring Set Requirement per Engine: This metric accounts for the number of cylinders and the different ring types (compression, oil control, scraper) required per engine configuration.

Vehicle Parc Data and Average Piston Ring Replacement Frequency: Critical for accurately sizing the aftermarket segment, considering regional vehicle longevity and maintenance cycles.

Average Selling Price (ASP) per Piston Ring Set: Differentiated by material type (cast iron, ductile iron, steel), coating type (chromium, molybdenum, ceramic), sales channel (OEM, aftermarket), and regional pricing variations.

All estimates are cross-referenced and validated through triangulation with multiple data sources and expert opinions obtained during primary research. This iterative process allows for continuous refinement of market figures, leading to robust and defensible forecasts for the period 2026-2034.

Data Accuracy & Quality Check

Maintaining the highest standards of data accuracy and report quality is paramount. Every data point, market figure, and strategic insight undergoes a rigorous multi-stage validation process. Our dedicated quality assurance team meticulously reviews all collected data for consistency, relevance, and reliability against established benchmarks and industry norms. This includes cross-verification between primary and secondary sources, statistical analysis of quantitative data, and expert panel reviews of qualitative insights.

Our commitment to methodological integrity ensures an estimated data accuracy level of 88-90% for all quantitative market figures. Furthermore, our research processes are designed to be dynamic and agile. Every report is updated up to the date of purchase, reflecting the latest market developments, technological breakthroughs, and shifts in the competitive landscape, thereby providing clients with the most current and actionable intelligence for strategic decision-making.

Frequently Asked Questions

1. What recent developments are impacting the Automotive Piston Rings market?

Key players in the Automotive Piston Rings market, such as MAHLE GmbH and Tenneco, are focusing on material science and advanced coating developments. These innovations aim to enhance durability, reduce friction, and improve engine efficiency to meet evolving automotive standards.

2. How are technological innovations shaping Automotive Piston Ring R&D?

Technological innovations in Automotive Piston Rings center on developing advanced materials like Steel Piston Rings and specialized coatings, including Chromium-Coated and Ceramic-Coated Rings. R&D aims to reduce friction, improve thermal management, and enhance sealing for optimized engine performance and emission control.

3. Which region exhibits the fastest growth in the Automotive Piston Rings market?

Asia-Pacific is projected as the fastest-growing region for Automotive Piston Rings, driven by substantial automotive production increases in countries like China and India. This growth is fueled by rising vehicle demand and a growing aftermarket segment in these economies.

4. What are the primary market segments for Automotive Piston Rings?

The Automotive Piston Rings market is segmented by Ring Type (e.g., Compression Rings, Oil Control Rings), Material Type (e.g., Cast Iron, Steel Piston Rings), and Coating Type. The Sales Channel segment divides the market into OEM and Aftermarket, with both contributing significantly.

5. How do sustainability factors influence the Automotive Piston Rings market?

Sustainability in Automotive Piston Rings is primarily driven by global emission regulations, pushing for designs that reduce engine friction and improve fuel efficiency. Manufacturers are also exploring more durable and potentially recyclable materials to minimize environmental impact across the product lifecycle.

6. What long-term shifts are observed in the Automotive Piston Rings market post-pandemic?

Post-pandemic, the Automotive Piston Rings market has emphasized supply chain resilience and adapted to shifts in vehicle production. Long-term trends include the ongoing optimization of piston rings for hybrid powertrains and internal combustion engines, even as the industry moves towards alternative propulsion methods.