Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Automotive Gas Charged Shock Absorbers: Trends & 2033 Outlook

Automotive Gas Charged Shock Absorbers

Automotive Gas Charged Shock Absorbers: Trends & 2033 Outlook

Automotive Gas Charged Shock Absorbers by Product Type (Twin-Tube, Mono-Tube, Others), by Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs)), by Distribution Channel (OEM, Aftermarket), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 90

Key Insights into the Automotive Gas Charged Shock Absorbers Market

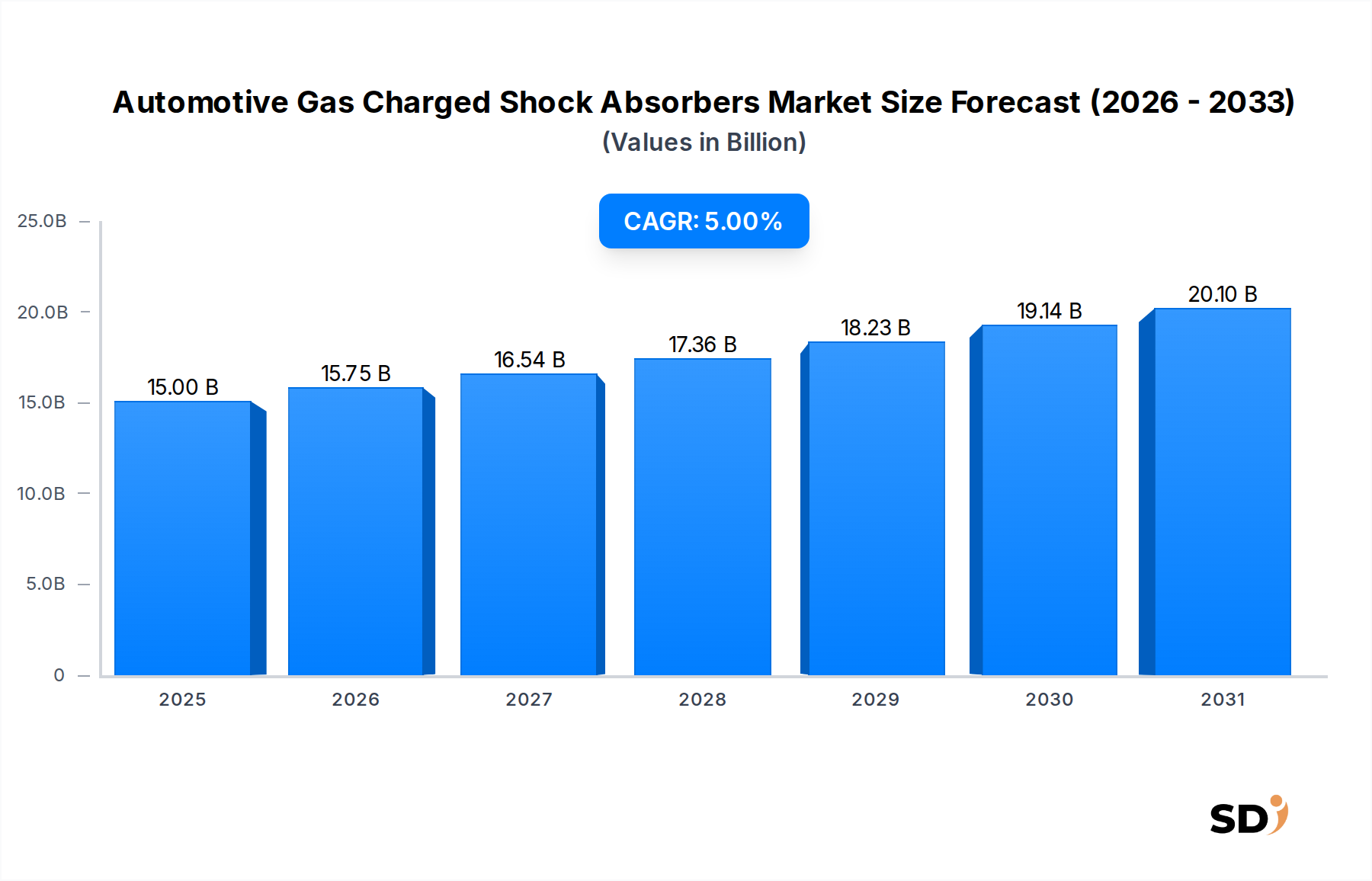

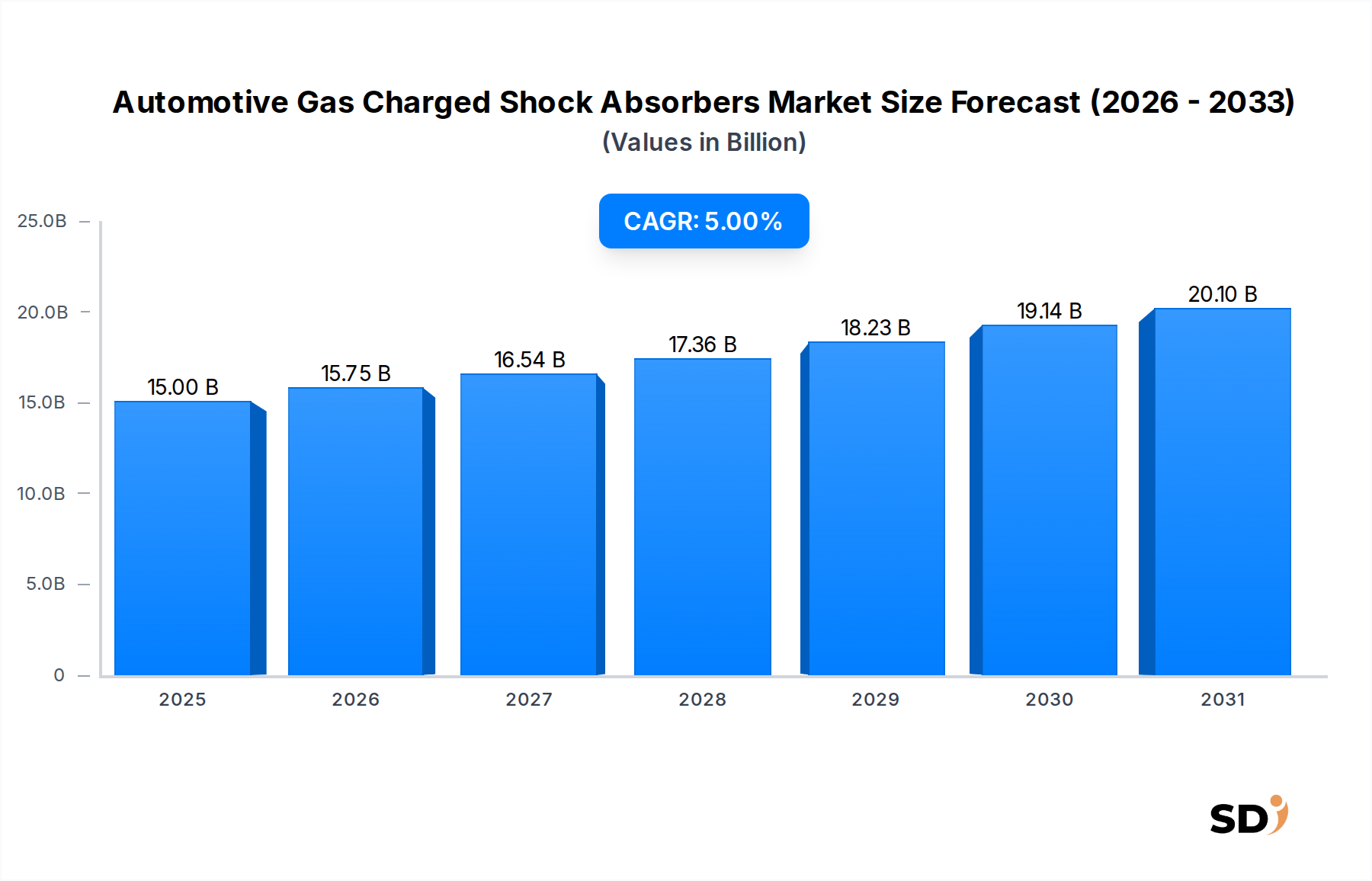

The global Automotive Gas Charged Shock Absorbers Market, valued at an estimated $15 billion in 2025, is poised for robust expansion, driven by persistent demand for enhanced vehicle dynamics, safety, and comfort. Projections indicate a compound annual growth rate (CAGR) of 5% from 2025 to 2030, propelling the market to approximately $19.14 billion by the end of the forecast period. This growth trajectory is underpinned by several macro-tailwinds, including increasing global vehicle production, particularly in emerging economies, and a burgeoning Automotive Aftermarket Parts Market. The inherent benefits of gas-charged shock absorbers—superior damping characteristics, reduced aeration, and consistent performance across varying temperatures—make them a preferred choice over conventional hydraulic units, ensuring their continued adoption in both original equipment manufacturer (OEM) and aftermarket segments.

Automotive Gas Charged Shock Absorbers Market Size (In Billion)

25.0B

20.0B

15.0B

10.0B

5.0B

0

15.00 B

2025

15.75 B

2026

16.54 B

2027

17.36 B

2028

18.23 B

2029

19.14 B

2030

20.10 B

2031

Demand acceleration is critically influenced by evolving consumer expectations for superior ride quality and vehicle stability, alongside stringent safety regulations that necessitate advanced suspension components. The expansion of the global vehicle parc contributes significantly to the aftermarket segment, as aging vehicles require replacement parts, including shock absorbers. Furthermore, advancements in material science and manufacturing processes are yielding more durable and efficient gas-charged units, enhancing product lifecycle and performance. The integration of semi-active and active suspension technologies, while a separate market, often builds upon the foundational principles of advanced damping, positioning gas Charged Shock Absorbers as a critical component within the broader Automotive Suspension Systems Market. The competitive landscape is characterized by a mix of established global players and regional specialists, who continuously innovate to meet diverse application requirements across passenger cars and commercial vehicles. While the transition towards electric vehicles introduces new design considerations for weight distribution and energy regeneration, gas-charged shock absorbers continue to be essential for managing ride dynamics and chassis control, ensuring their enduring relevance. The sustained focus on infrastructure development in developing nations, coupled with increasing disposable incomes, further fuels the demand for new vehicles and, consequently, for high-performance Automotive Components Market.

Dominant OEM Segment Dynamics in Automotive Gas Charged Shock Absorbers Market

The Original Equipment Manufacturer (OEM) segment stands as the preeminent revenue contributor within the Automotive Gas Charged Shock Absorbers Market, accounting for a substantial majority of the market share. This dominance is primarily attributable to the foundational role these components play in new vehicle assembly, where they are integral to the initial design, performance, and safety specifications of all vehicle types. OEMs, including major automotive manufacturers globally, demand high volumes of precisely engineered gas-charged shock absorbers that meet stringent quality controls, performance benchmarks, and specific vehicle model requirements. The intrinsic link between new vehicle production rates and OEM demand means that growth in the global automotive manufacturing sector directly translates into expansion for this segment. Factors such as increasing disposable incomes in developing economies, leading to higher passenger car sales, and the robust expansion of the Light Commercial Vehicle Parts Market, significantly bolster OEM order books for these critical damping components. Key players like ZF Friedrichshafen, Tenneco Inc., KYB Corporation, and Hitachi Automotive Systems are deeply entrenched in the OEM supply chain, serving a wide array of global automakers with customized solutions. Their long-standing relationships, technological prowess, and ability to deliver at scale are critical competitive advantages. These companies invest heavily in R&D to develop next-generation shock absorbers that integrate seamlessly with evolving vehicle architectures, including those for electric and hybrid platforms.

While the OEM segment's share is substantial, it is also subject to the cyclical nature of the global automotive production industry and the intense price pressures exerted by large automakers. Suppliers in the Automotive OEM Parts Market must demonstrate exceptional manufacturing efficiency, supply chain reliability, and consistent product quality to secure and retain contracts. Furthermore, the trend towards vehicle lightweighting and enhanced fuel efficiency drives innovation in shock absorber design, requiring OEMs to constantly adapt their product offerings. The push for more advanced suspension systems, including those capable of dynamic adjustments, often starts within the OEM realm, eventually influencing the broader Automotive Damping Systems Market. Despite these challenges, the OEM segment is expected to maintain its leading position, primarily due to the continuous global demand for new vehicles and the non-negotiable requirement for high-quality suspension components from initial vehicle design. The scale of manufacturing for new vehicles ensures that the volume of gas-charged shock absorbers supplied to OEMs remains higher than that channeled through the aftermarket for replacement purposes. Furthermore, the lifecycle of a vehicle, before significant maintenance or component replacement becomes necessary, typically extends for several years, ensuring a constant baseline demand from the OEM sector for new vehicle builds.

Key Growth Drivers and Restraints in Automotive Gas Charged Shock Absorbers Market

The Automotive Gas Charged Shock Absorbers Market is primarily propelled by several synergistic factors. A significant driver is the increasing global vehicle production, particularly in emerging markets across Asia Pacific and Latin America. As disposable incomes rise, the demand for both Passenger Car Components Market and Light Commercial Vehicle Parts Market grows, directly translating into higher unit sales for OEM-installed gas-charged shock absorbers. This trend is underscored by data indicating consistent year-over-year increases in new vehicle registrations in key developing economies. Secondly, the escalating consumer preference for enhanced ride comfort and vehicle safety is a crucial demand stimulant. Modern vehicles, whether premium or economy class, are expected to offer superior handling and a smooth ride, a performance characteristic heavily dependent on the effectiveness of the suspension system. Gas-charged units, with their ability to resist fluid aeration and provide consistent damping, meet these expectations more effectively than conventional hydraulic shocks.

Thirdly, the expansion of the global Automotive Aftermarket Parts Market due to an aging vehicle parc plays a vital role. As vehicles accumulate mileage, their original shock absorbers wear out, creating a persistent demand for replacements. The average age of vehicles in operation has been steadily increasing in many regions, directly fueling the replacement market for essential components. Furthermore, the deteriorating road infrastructure in numerous developing countries and even parts of mature markets necessitates frequent replacement of suspension components, providing a steady revenue stream. Conversely, the market faces certain constraints. Volatility in raw material prices, particularly for steel, aluminum, and specialized rubber compounds, can impact manufacturing costs and profit margins. The capital-intensive nature of precision engineering and manufacturing facilities for these components presents a barrier to entry for new players. Moreover, the long-term shift towards electric vehicles (EVs) and the potential adoption of more advanced active or semi-active Automotive Suspension Systems Market could influence the design and perhaps the volume of traditional gas-charged shock absorbers, although they remain critical for basic damping and chassis control even in advanced systems.

Competitive Ecosystem of Automotive Gas Charged Shock Absorbers Market

The Automotive Gas Charged Shock Absorbers Market is characterized by intense competition among a few global titans and several specialized regional players, all vying for market share in both the OEM and aftermarket segments.

ZF Friedrichshafen: A global technology company supplying systems for passenger cars, commercial vehicles, and industrial technology. ZF is a major player in automotive suspension, offering a broad portfolio of shock absorbers, including advanced gas-charged variants, focusing on performance, comfort, and safety across various vehicle platforms.

Tenneco Inc.: A leading global designer, manufacturer, and marketer of clean air and ride performance products and systems for the automotive and commercial vehicle markets. Its Monroe brand is particularly well-known in the aftermarket for its extensive range of shock absorbers.

Meritor: A global supplier of drivetrain, mobility, braking, aftermarket, and electric powertrain solutions for commercial vehicle and industrial markets. While primarily focused on heavy-duty applications, their expertise extends to robust suspension components.

Gabriel: An established brand with a long history in shock absorber manufacturing, particularly strong in the aftermarket in several regions. Gabriel focuses on offering reliable and cost-effective replacement solutions for a wide range of vehicles.

Thyssenkrupp AG: A diversified industrial group with a significant presence in automotive technology, including chassis and suspension components. They develop advanced damping solutions for various vehicle segments, emphasizing innovation and quality.

ITT Corporation: A diversified manufacturer of highly engineered critical components and customized technology solutions. Through its KONI brand, ITT offers premium shock absorbers known for performance and adjustability, particularly favored in sports and enthusiast segments.

Arnott: A leading provider of aftermarket air suspension products. While primarily focused on air suspension, their offerings often complement or integrate with traditional shock absorber systems, addressing a niche in the high-end replacement market.

KONI: A brand under ITT Corporation, specializing in high-performance shock absorbers for passenger cars, racing, and commercial vehicles. KONI products are known for their quality, adjustability, and durability.

Samvardhana Motherson Group (SMG): A diversified global manufacturing conglomerate, active in automotive components. SMG offers a range of suspension and chassis components, leveraging its extensive manufacturing capabilities and global footprint.

Magneti Marelli: A global advanced automotive technology company, now part of Marelli. They provide a wide array of automotive systems, including sophisticated suspension components and damping systems for OEMs globally.

Hitachi Automotive Systems: A major supplier of automotive components, including chassis systems and shock absorbers. Hitachi focuses on developing high-performance and electronically controlled damping solutions for global automotive manufacturers.

Showa: A prominent Japanese manufacturer of automotive and motorcycle components, including shock absorbers and power steering systems. Showa is a key OEM supplier, known for its precision engineering and high-quality products.

KYB Corporation: One of the world's largest manufacturers of hydraulic equipment, including shock absorbers, for both OEM and aftermarket applications. KYB is recognized for its extensive product range and global distribution network in the Automotive Damping Systems Market.

Recent Developments & Milestones in Automotive Gas Charged Shock Absorbers Market

Innovation and strategic positioning remain crucial for players in the Automotive Gas Charged Shock Absorbers Market. Companies continuously strive to enhance product performance, expand their market reach, and adapt to evolving vehicle technologies.

May 2024: KYB Corporation announced the expansion of its manufacturing capabilities in Southeast Asia, aimed at addressing the growing demand for Mono-Tube Shock Absorbers Market and Twin-Tube Shock Absorbers Market in the regional aftermarket and for local OEM partners.

February 2024: Tenneco's Monroe brand introduced a new line of OE Spectrum gas-charged shock absorbers featuring an advanced valving system, promising superior ride comfort and handling characteristics for a wider range of Passenger Car Components Market models.

November 2023: ZF Friedrichshafen secured a significant OEM contract with a leading European automotive manufacturer to supply next-generation gas-charged shock absorbers for their new electric vehicle platform, emphasizing the component's continued relevance in EV applications.

August 2023: Hitachi Automotive Systems entered into a strategic partnership with a prominent Indian automaker to co-develop cost-effective, durable gas-charged shock absorbers specifically engineered for the challenging road conditions prevalent in the Indian Light Commercial Vehicle Parts Market.

June 2023: Gabriel unveiled a new series of heavy-duty gas-charged shock absorbers designed for fleet vehicles, focusing on extended durability and enhanced load-carrying capacity, targeting the burgeoning logistics and transportation sectors.

April 2023: Industry reports highlighted a trend towards increased adoption of nitrogen-charged shock absorbers within the performance segment, offering improved heat dissipation and fade resistance, showcasing continuous product evolution within the broader Automotive Damping Systems Market.

January 2023: Samvardhana Motherson Group announced an investment in new testing facilities to accelerate the development and validation of advanced suspension components, including gas-charged shock absorbers, for both domestic and international Automotive OEM Parts Market.

Regional Market Breakdown for Automotive Gas Charged Shock Absorbers Market

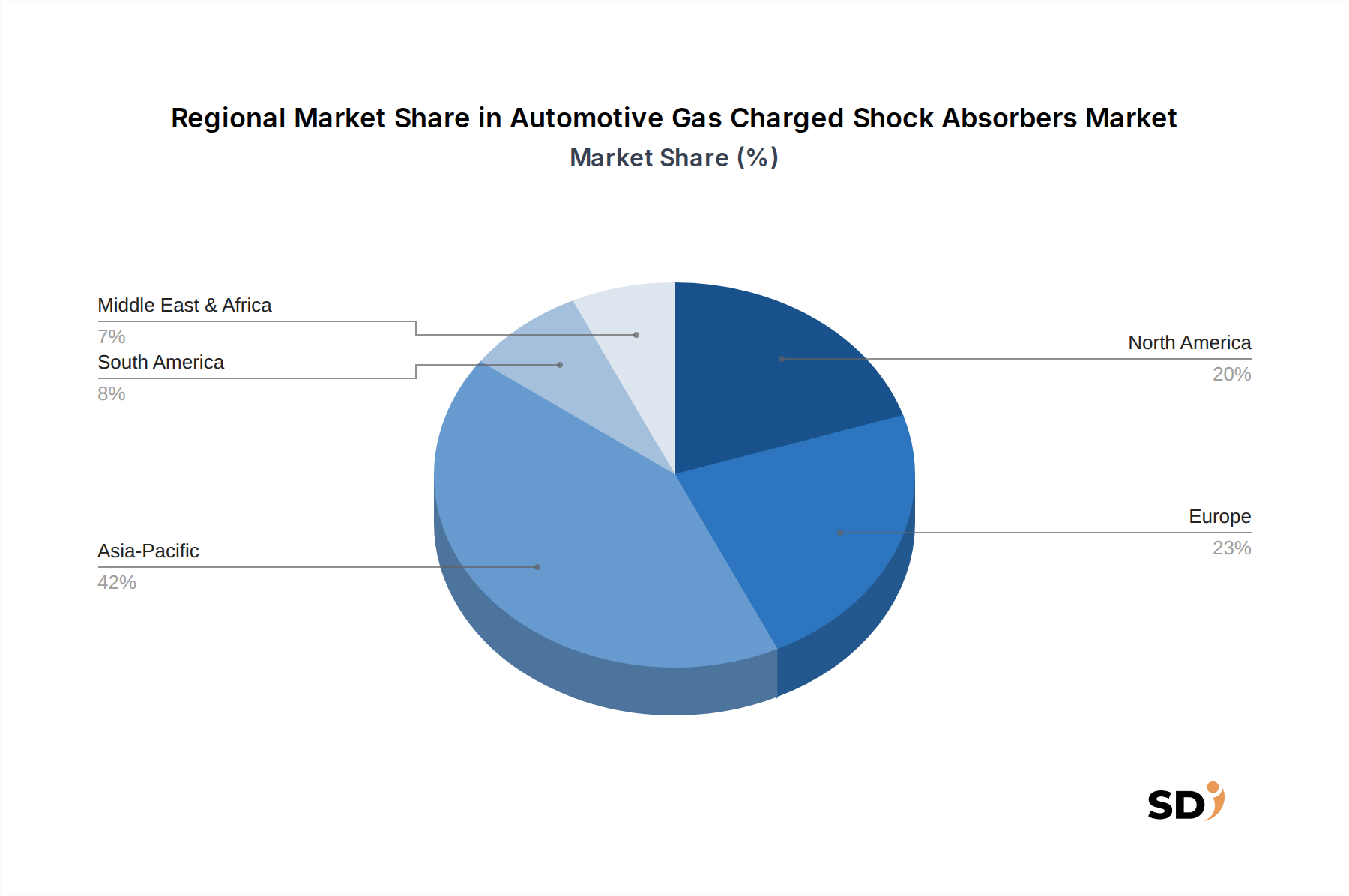

The global Automotive Gas Charged Shock Absorbers Market exhibits distinct regional dynamics, influenced by varying vehicle production rates, aging vehicle fleets, and regulatory landscapes. Asia Pacific currently holds the largest revenue share and is projected to be the fastest-growing region, driven by burgeoning automotive manufacturing hubs in China, India, Japan, and South Korea. This region benefits from rising disposable incomes, rapid urbanization, and a growing middle class, leading to sustained demand for new vehicles and, consequently, an increased need for Automotive Suspension Systems Market components. The regional CAGR for Asia Pacific is anticipated to exceed 6.5%, significantly contributing to the expansion of the global market.

North America represents a mature market with substantial aftermarket demand. While new vehicle production rates show steady growth, the extensive existing vehicle parc fuels a robust Automotive Aftermarket Parts Market for replacement shock absorbers. Consumer preferences for larger vehicles, such as SUVs and light trucks, also drive demand for more robust and higher-performance gas-charged units. The North American market is expected to demonstrate a stable CAGR of around 4.0%, with demand primarily driven by replacement cycles and the increasing average age of vehicles. Europe, another mature market, mirrors North America in its strong aftermarket presence and established OEM production. Stringent safety and emission regulations, alongside a preference for vehicle performance and comfort, dictate the quality and technological sophistication of shock absorbers. The European market is projected to grow at a CAGR of approximately 3.8%, with a focus on advanced materials and integration into sophisticated vehicle control systems. Finally, South America and the Middle East & Africa regions present emerging opportunities. South America, particularly Brazil and Argentina, shows promising growth due to increasing vehicle sales and infrastructure development, leading to a CAGR of approximately 5.5%. The Middle East & Africa region, while smaller in absolute terms, is witnessing gradual expansion driven by fleet modernization and rising vehicle ownership, contributing to the overall Automotive Components Market growth.

Customer Segmentation & Buying Behavior in Automotive Gas Charged Shock Absorbers Market

Customer segmentation in the Automotive Gas Charged Shock Absorbers Market primarily delineates between Original Equipment Manufacturers (OEMs) and various aftermarket end-users, each exhibiting distinct buying behaviors and procurement criteria. OEMs, including major global automakers (e.g., Ford, Toyota, Volkswagen), constitute the largest segment. Their purchasing decisions are driven by stringent technical specifications, long-term supply agreements, cost-effectiveness at high volumes, and supplier's R&D capabilities. Procurement channels involve direct, long-term contracts with tier-1 suppliers such as KYB Corporation, ZF Friedrichshafen, and Tenneco Inc., often involving joint development processes to integrate shock absorbers seamlessly into new vehicle designs. Price sensitivity for OEMs is high due to the scale of procurement, but quality, reliability, and compliance with safety standards are non-negotiable.

The aftermarket segment is more diverse, encompassing independent workshops, franchised dealerships, fleet operators, and DIY (do-it-yourself) consumers. Independent workshops and dealerships prioritize brand reputation (e.g., Monroe, KONI), product availability, ease of installation, and distributor support. Their purchasing criteria often balance cost with perceived quality and customer satisfaction, sourcing through established wholesale distributors. Fleet operators, managing large vehicle inventories, emphasize durability, extended warranty, and competitive pricing to minimize downtime and operational costs; they often procure in bulk directly from distributors or through specialized service providers. DIY consumers, driven by cost savings, typically focus on brand recognition, online reviews, and accessibility through retail auto parts stores or e-commerce platforms. Price sensitivity varies significantly across these aftermarket sub-segments, with DIY consumers often being the most price-conscious, while performance enthusiasts prioritize specific technical features and brand legacy, leading to differing preferences within the Mono-Tube Shock Absorbers Market and Twin-Tube Shock Absorbers Market. A notable shift in recent cycles is the increasing influence of online channels and digital information, empowering all aftermarket buyers with greater product knowledge and price comparison capabilities, pushing manufacturers and distributors to enhance their digital presence and transparency.

The Automotive Gas Charged Shock Absorbers Market is subject to a complex web of regulatory frameworks and industry standards that vary across key geographies, influencing product design, manufacturing processes, and market access. These regulations primarily aim to enhance vehicle safety, environmental performance, and manufacturing quality. Globally, ISO/TS 16949 (now integrated into IATF 16949) serves as the fundamental quality management system standard for the Automotive OEM Parts Market, ensuring consistent quality and reliability in component manufacturing, including gas-charged shock absorbers. Compliance with such standards is non-negotiable for suppliers seeking to engage with major automakers.

In North America, standards set by organizations like the Society of Automotive Engineers (SAE) dictate various aspects of vehicle performance and component testing. The National Highway Traffic Safety Administration (NHTSA) in the U.S. indirectly influences shock absorber design through overall vehicle safety regulations related to braking, handling, and stability, as effective suspension is critical to these functions. Europe's regulatory environment is shaped by the European Union (EU) directives, particularly those related to vehicle type approval (e.g., EC whole vehicle type approval), which ensure that all components, including shock absorbers, meet rigorous safety and environmental criteria before they can be sold within the EU. The UNECE (United Nations Economic Commission for Europe) regulations, adopted by many countries globally, provide harmonized standards for vehicle components. Recent policy changes, such as stricter emission norms (e.g., Euro 7) and increasing focus on vehicle lightweighting to improve fuel economy or EV range, exert pressure on shock absorber manufacturers to innovate with lighter materials and more efficient designs. While there are no direct regulations specifically for "gas-charged" shock absorbers as a category, their performance directly contributes to vehicle safety and handling characteristics, which are heavily regulated. Moreover, environmental policies governing manufacturing processes and materials (e.g., REACH in Europe, RoHS directives for certain substances) impact the supply chain of the Automotive Components Market, driving manufacturers to adopt greener processes and materials. The cumulative effect of these regulations is a continuous push towards higher quality, improved performance, and more sustainable manufacturing practices within the Automotive Gas Charged Shock Absorbers Market.

Automotive Gas Charged Shock Absorbers Segmentation

1. Product Type

1.1. Twin-Tube

1.2. Mono-Tube

1.3. Others

2. Vehicle Type

2.1. Passenger Cars

2.2. Light Commercial Vehicles (LCVs)

3. Distribution Channel

3.1. OEM

3.2. Aftermarket

Automotive Gas Charged Shock Absorbers Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Automotive Gas Charged Shock Absorbers REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 5% from 2020-2034

Segmentation

By Product Type

Twin-Tube

Mono-Tube

Others

By Vehicle Type

Passenger Cars

Light Commercial Vehicles (LCVs)

By Distribution Channel

OEM

Aftermarket

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Type

5.1.1. Twin-Tube

5.1.2. Mono-Tube

5.1.3. Others

5.2. Market Analysis, Insights and Forecast - by Vehicle Type

5.2.1. Passenger Cars

5.2.2. Light Commercial Vehicles (LCVs)

5.3. Market Analysis, Insights and Forecast - by Distribution Channel

5.3.1. OEM

5.3.2. Aftermarket

5.4. Market Analysis, Insights and Forecast - by Region

5.4.1. North America

5.4.2. South America

5.4.3. Europe

5.4.4. Middle East & Africa

5.4.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Product Type

6.1.1. Twin-Tube

6.1.2. Mono-Tube

6.1.3. Others

6.2. Market Analysis, Insights and Forecast - by Vehicle Type

6.2.1. Passenger Cars

6.2.2. Light Commercial Vehicles (LCVs)

6.3. Market Analysis, Insights and Forecast - by Distribution Channel

6.3.1. OEM

6.3.2. Aftermarket

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Product Type

7.1.1. Twin-Tube

7.1.2. Mono-Tube

7.1.3. Others

7.2. Market Analysis, Insights and Forecast - by Vehicle Type

7.2.1. Passenger Cars

7.2.2. Light Commercial Vehicles (LCVs)

7.3. Market Analysis, Insights and Forecast - by Distribution Channel

7.3.1. OEM

7.3.2. Aftermarket

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Product Type

8.1.1. Twin-Tube

8.1.2. Mono-Tube

8.1.3. Others

8.2. Market Analysis, Insights and Forecast - by Vehicle Type

8.2.1. Passenger Cars

8.2.2. Light Commercial Vehicles (LCVs)

8.3. Market Analysis, Insights and Forecast - by Distribution Channel

8.3.1. OEM

8.3.2. Aftermarket

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Product Type

9.1.1. Twin-Tube

9.1.2. Mono-Tube

9.1.3. Others

9.2. Market Analysis, Insights and Forecast - by Vehicle Type

9.2.1. Passenger Cars

9.2.2. Light Commercial Vehicles (LCVs)

9.3. Market Analysis, Insights and Forecast - by Distribution Channel

9.3.1. OEM

9.3.2. Aftermarket

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Product Type

10.1.1. Twin-Tube

10.1.2. Mono-Tube

10.1.3. Others

10.2. Market Analysis, Insights and Forecast - by Vehicle Type

10.2.1. Passenger Cars

10.2.2. Light Commercial Vehicles (LCVs)

10.3. Market Analysis, Insights and Forecast - by Distribution Channel

10.3.1. OEM

10.3.2. Aftermarket

11. Competitive Analysis

11.1. Company Profiles

11.1.1. ZF Friedrichshafen

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Tenneco Inc.

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Meritor

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Gabriel

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Thyssenkrupp AG

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. ITT Corporation

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Arnott

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. KONI

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Samvardhana Motherson Group (SMG)

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Magneti Marelli

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Hitachi Automotive Systems

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Showa

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.1.13. KYB Corporation

11.1.13.1. Company Overview

11.1.13.2. Products

11.1.13.3. Company Financials

11.1.13.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Product Type 2025 & 2033

Figure 3: Revenue Share (%), by Product Type 2025 & 2033

Figure 4: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 5: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 6: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 7: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 8: Revenue (billion), by Country 2025 & 2033

Figure 9: Revenue Share (%), by Country 2025 & 2033

Figure 10: Revenue (billion), by Product Type 2025 & 2033

Figure 11: Revenue Share (%), by Product Type 2025 & 2033

Figure 12: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 13: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 14: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 15: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 16: Revenue (billion), by Country 2025 & 2033

Figure 17: Revenue Share (%), by Country 2025 & 2033

Figure 18: Revenue (billion), by Product Type 2025 & 2033

Figure 19: Revenue Share (%), by Product Type 2025 & 2033

Figure 20: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 21: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 22: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 23: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 24: Revenue (billion), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Revenue (billion), by Product Type 2025 & 2033

Figure 27: Revenue Share (%), by Product Type 2025 & 2033

Figure 28: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 29: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 30: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 31: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 32: Revenue (billion), by Country 2025 & 2033

Figure 33: Revenue Share (%), by Country 2025 & 2033

Figure 34: Revenue (billion), by Product Type 2025 & 2033

Figure 35: Revenue Share (%), by Product Type 2025 & 2033

Figure 36: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 37: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 38: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 39: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 40: Revenue (billion), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Product Type 2020 & 2033

Table 2: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 3: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 4: Revenue billion Forecast, by Region 2020 & 2033

Table 5: Revenue billion Forecast, by Product Type 2020 & 2033

Table 6: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 7: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 8: Revenue billion Forecast, by Country 2020 & 2033

Table 9: Revenue (billion) Forecast, by Application 2020 & 2033

Table 10: Revenue (billion) Forecast, by Application 2020 & 2033

Table 11: Revenue (billion) Forecast, by Application 2020 & 2033

Table 12: Revenue billion Forecast, by Product Type 2020 & 2033

Table 13: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 14: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 15: Revenue billion Forecast, by Country 2020 & 2033

Table 16: Revenue (billion) Forecast, by Application 2020 & 2033

Table 17: Revenue (billion) Forecast, by Application 2020 & 2033

Table 18: Revenue (billion) Forecast, by Application 2020 & 2033

Table 19: Revenue billion Forecast, by Product Type 2020 & 2033

Table 20: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 21: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 22: Revenue billion Forecast, by Country 2020 & 2033

Table 23: Revenue (billion) Forecast, by Application 2020 & 2033

Table 24: Revenue (billion) Forecast, by Application 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Revenue (billion) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue (billion) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Revenue (billion) Forecast, by Application 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue billion Forecast, by Product Type 2020 & 2033

Table 33: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 34: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 35: Revenue billion Forecast, by Country 2020 & 2033

Table 36: Revenue (billion) Forecast, by Application 2020 & 2033

Table 37: Revenue (billion) Forecast, by Application 2020 & 2033

Table 38: Revenue (billion) Forecast, by Application 2020 & 2033

Table 39: Revenue (billion) Forecast, by Application 2020 & 2033

Table 40: Revenue (billion) Forecast, by Application 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue billion Forecast, by Product Type 2020 & 2033

Table 43: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 44: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 45: Revenue billion Forecast, by Country 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Revenue (billion) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Revenue (billion) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our market sizing and forecasting methodology heavily relies on primary research, constituting approximately 75-80% of our total research efforts. This approach ensures the most current and granular insights directly from industry participants across the value chain. Our interviews are conducted globally, covering key regional markets specified in the report.

The primary research phase involves in-depth interviews (IDI) with these stakeholders to validate secondary data, obtain qualitative insights, understand market dynamics, competitive landscapes, technological trends, pricing strategies, and future outlooks. Each interview is structured to extract data points pertinent to product type, vehicle type, distribution channel, and regional specificities.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Senior R&D Engineer, Shock Absorbers

30%

Head of Product Development, Suspension Systems (OEM)

25%

Global Category Manager, Chassis Components (Aftermarket Distributor)

Automotive Gas Charged Shock Absorber Manufacturers

30%

Automotive Original Equipment Manufacturers (OEMs)

25%

Aftermarket Parts Distributors & Retailers

20%

Specialty Material & Component Suppliers

15%

Independent Automotive Service Garages & Franchise Repair Networks

10%

Secondary Research & Industry Benchmarking

The remaining 20-25% of our research is dedicated to robust secondary research and industry benchmarking. This phase provides foundational data and context for primary research validation. Our team meticulously scours a vast array of proprietary and publicly available sources to gather critical information.

Sources leveraged include:

Financial & Business Databases: Bloomberg, Factiva, Hoovers, PitchBook.

Government & Regulatory Bodies: Data from national transportation authorities, statistical offices, and economic ministries globally (e.g., U.S. Bureau of Economic Analysis BEA, Eurostat Eurostat).

Industry Associations & Trade Bodies:

Society of Automotive Engineers (SAE International) SAE International

Automotive Aftermarket Suppliers Association (AASA) AASA

International Organization of Motor Vehicle Manufacturers (OICA) OICA

Motor & Equipment Manufacturers Association (MEMA) MEMA

Company Annual Reports, Investor Presentations, and Press Releases: Direct publications from key market players.

Academic Research & Journals: Peer-reviewed studies on automotive engineering and market trends.

This exhaustive secondary research helps in identifying market trends, competitive intelligence, technological advancements, regulatory impacts, and macroeconomic factors influencing the automotive gas-charged shock absorber market.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodology integrates both top-down and bottom-up approaches, critically triangulated across multiple levels to ensure robust and reliable market estimates.

Bottom-Up Approach: This method begins with granular data points and aggregates them to derive total market size.

Specific Metrics/Variables Used:

New vehicle production volumes by vehicle type (passenger cars, LCVs) and regional country forecasts (e.g., units of new vehicles requiring shock absorbers).

Average shock absorber replacement rate per vehicle based on vehicle age and mileage, influencing aftermarket demand.

Average selling price (ASP) of gas-charged shock absorbers by product type (twin-tube, mono-tube, others) and distribution channel (OEM vs. Aftermarket).

Total vehicle parc (vehicles in operation) by region, serving as the installed base for aftermarket potential.

Top-Down Approach: This approach involves estimating the total market size based on macroeconomic indicators, total automotive industry revenue, and then segmenting it down to the specific market for gas-charged shock absorbers.

Multi-Level Data Triangulation: Data from both primary and secondary research, and from top-down and bottom-up analyses, is rigorously cross-referenced and validated. This iterative process helps in reconciling discrepancies, identifying potential biases, and refining market estimates to achieve a highly consistent and defensible market model.

Data Accuracy & Quality Check

We are committed to delivering data with an estimated accuracy level of 85-90%. This high standard is achieved through a meticulous, multi-stage data validation and quality assurance process:

Expert Panel Review: Insights and data points collected are reviewed by an internal panel of senior analysts with extensive experience in the automotive sector.

Statistical Analysis & Modeling: Sophisticated statistical tools and proprietary models are employed to analyze data, identify trends, and project future market scenarios.

Primary Data Verification: Key findings from primary interviews are re-validated through subsequent calls or cross-referenced with other primary sources to ensure consistency.

Secondary Data Cross-Verification: Information gathered from secondary sources is always cross-referenced with at least two independent sources to confirm its reliability.

Continuous Updates: Our market intelligence is dynamic. Every report is updated up to the date of purchase, incorporating the latest industry developments, economic shifts, and technological advancements to provide the most current market view possible. This ensures that clients receive timely and relevant data for strategic decision-making.

Frequently Asked Questions

1. Which region leads the Automotive Gas Charged Shock Absorbers market and why?

Asia-Pacific is projected to lead the market, driven by high automotive production volumes in countries like China, India, and Japan, alongside a robust aftermarket. This region is estimated to hold approximately 42% of the global market share.

2. What are the key international trade flows for Automotive Gas Charged Shock Absorbers?

International trade primarily involves components and finished shock absorbers moving from major manufacturing centers in Asia and Europe to global vehicle assembly plants and aftermarket distribution networks. Key players like ZF Friedrichshafen and KYB Corporation manage extensive international supply chains.

3. How are consumer purchasing trends evolving for automotive shock absorbers?

Consumer purchasing decisions increasingly prioritize vehicle safety, ride comfort, and overall performance, fueling demand for advanced gas-charged shock absorbers. The aftermarket segment is also growing as consumers replace worn components on an aging global vehicle fleet.

4. What disruptive technologies or substitutes are emerging in the shock absorber market?

While traditional gas-charged shocks remain standard, advancements in adaptive and active suspension systems, often electronically controlled, offer enhanced vehicle dynamics. However, these high-cost alternatives typically target premium vehicle segments and are not direct substitutes for the mass market.

5. What are the primary growth drivers for the Automotive Gas Charged Shock Absorbers market?

Market growth is primarily driven by consistent global vehicle production, increasing average vehicle age which boosts aftermarket demand, and rising consumer awareness regarding vehicle safety and performance. The market is projected to reach approximately $22.16 billion by 2033.

6. What is the current investment landscape for automotive shock absorber manufacturers?

Investment in this sector is mainly concentrated on research and development for new materials, manufacturing automation, and expanding production capacities by established manufacturers such as Tenneco Inc. and Thyssenkrupp AG. Venture capital interest is generally limited in this mature automotive component segment.