Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Automotive Audio Amplifier IC Market: $5.18B Growth, 6.2% CAGR

Automotive Audio Amplifier IC

Automotive Audio Amplifier IC Market: $5.18B Growth, 6.2% CAGR

Automotive Audio Amplifier IC by Amplifier Class (Class A, Class B, Class AB, Class D, Others), by Vehicle Type (Passenger Vehicles, Commercial Vehicles), by Signal Type (Analog Amplifier IC, Digital Amplifier IC), by Application (Infotainment Systems, Head Units, Digital Cockpit Systems, Rear-seat Entertainment, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 87

Key Insights for Automotive Audio Amplifier IC Market

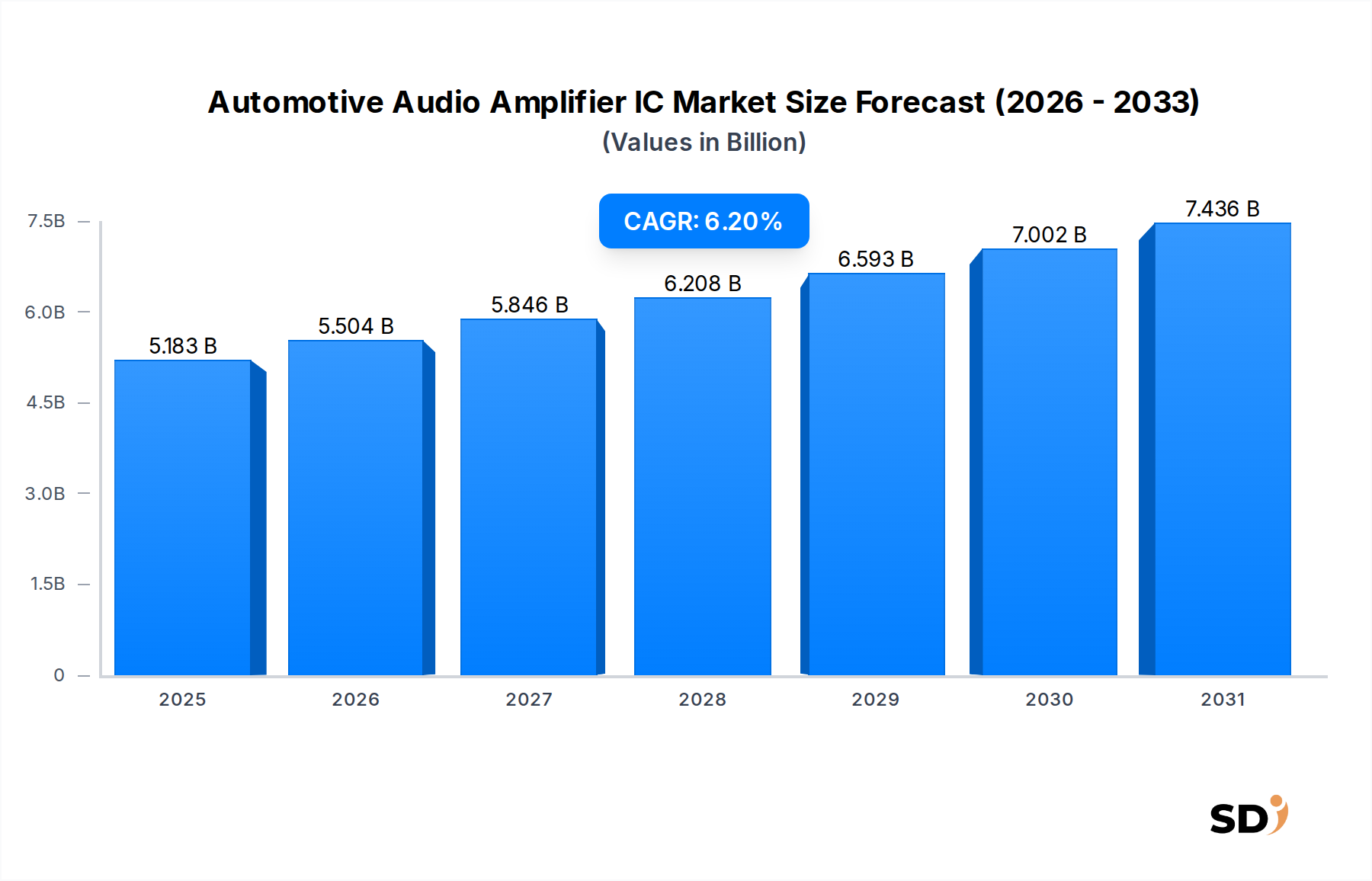

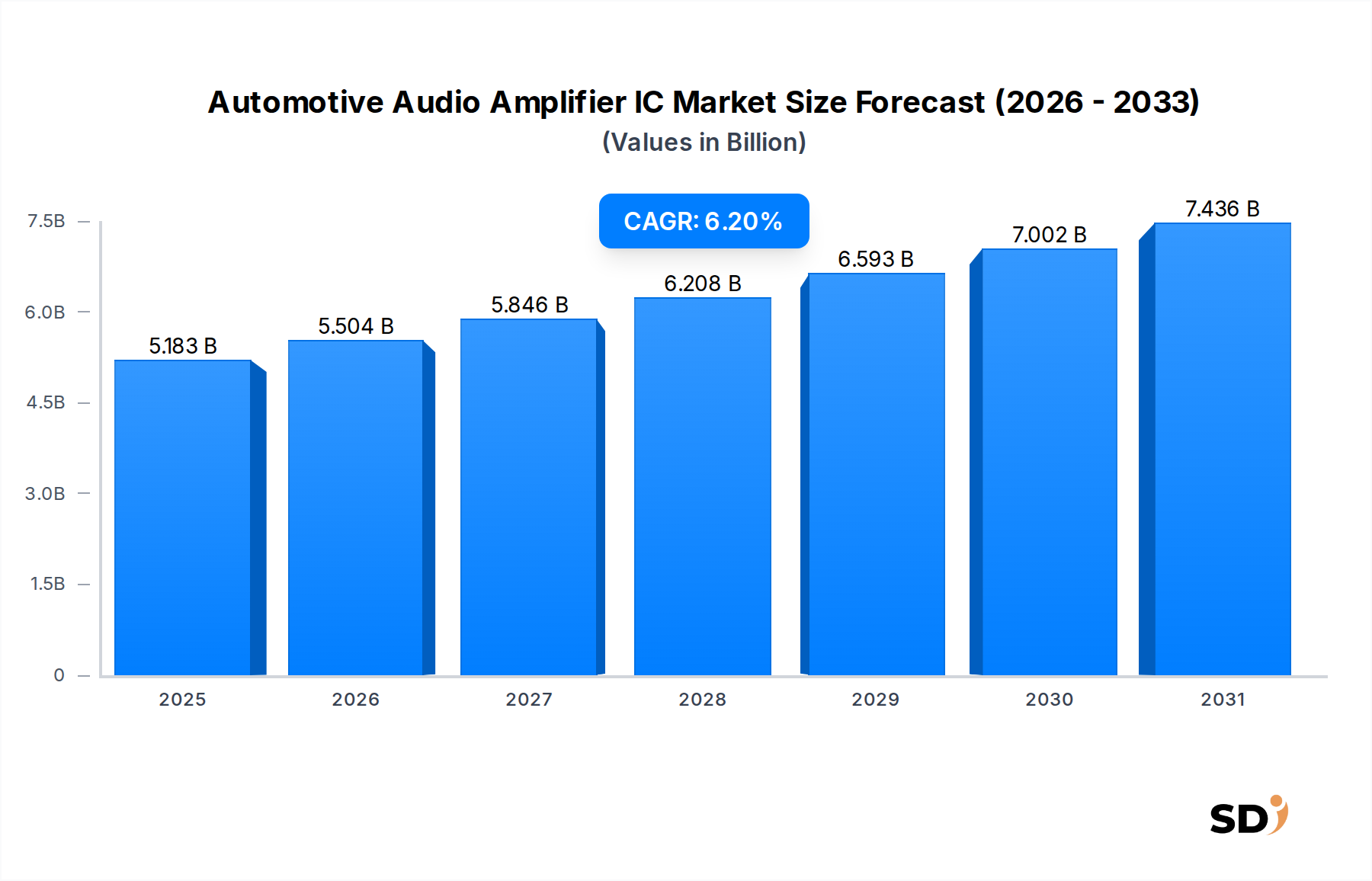

The Automotive Audio Amplifier IC Market is poised for substantial expansion, underpinned by a confluence of technological advancements and evolving consumer demands within the automotive sector. As of 2025, the market is valued at USD 5183 million, demonstrating robust growth prospects. Projections indicate a compound annual growth rate (CAGR) of 6.2% from 2025, driven largely by the increasing integration of sophisticated infotainment systems, the proliferation of electric vehicles (EVs), and the growing demand for premium audio experiences across all vehicle segments. The shift towards digital cockpits and advanced driver-assistance systems (ADAS) also indirectly fuels this market by necessitating high-performance, low-power audio solutions that integrate seamlessly with complex digital architectures. The ongoing evolution in amplifier technologies, particularly the efficiency gains of Class D architectures, is a critical enabler, allowing for higher power output in smaller footprints, essential for space-constrained automotive environments. Furthermore, the global Automotive Electronics Market continues its upward trajectory, directly benefiting the demand for specialized ICs like audio amplifiers. Regional dynamics, particularly the burgeoning automotive manufacturing hubs in Asia Pacific and the strong premium segment demand in Europe and North America, are instrumental in shaping market growth. Manufacturers are focusing on highly integrated solutions that offer enhanced digital signal processing capabilities and network connectivity, facilitating richer audio experiences and supporting multi-zone audio within vehicles. The pervasive trend of vehicle electrification also mandates more power-efficient components, making the advanced Automotive Audio Amplifier IC Market a crucial contributor to overall vehicle performance and passenger comfort. This sustained innovation and demand underscore a resilient and expanding market outlook, positioning it as a pivotal segment within the broader Automotive Semiconductor Market.

Automotive Audio Amplifier IC Market Size (In Billion)

7.5B

6.0B

4.5B

3.0B

1.5B

0

5.183 B

2025

5.504 B

2026

5.846 B

2027

6.208 B

2028

6.593 B

2029

7.002 B

2030

7.436 B

2031

Dominant Class D Amplifier Segment in Automotive Audio Amplifier IC Market

The Class D Amplifier segment stands as the unequivocal leader within the Automotive Audio Amplifier IC Market, commanding the largest revenue share and exhibiting strong growth momentum. This dominance is primarily attributed to Class D amplifiers' inherent high efficiency, compact form factor, and superior thermal performance, qualities that are critically important in the power- and space-constrained automotive environment. Unlike their Class A, B, or AB counterparts, Class D amplifiers operate by rapidly switching between fully on and fully off states, significantly minimizing power dissipation as heat. This efficiency translates directly into lower power consumption, which is a paramount consideration for vehicle manufacturers, especially with the accelerating adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) where every watt of power saved extends range or reduces battery drain. The reduced heat generation also simplifies thermal management systems, leading to smaller heatsinks or even fan-less designs, which further contributes to miniaturization and cost reduction. The integration of advanced digital signal processing (DSP) capabilities within these Class D architectures enables sophisticated audio tuning, active noise cancellation, and personalized sound zones, enhancing the overall in-vehicle audio experience. This capability aligns perfectly with the rising consumer expectations for high-fidelity sound and immersive multimedia experiences in vehicles, particularly within the rapidly expanding In-Vehicle Infotainment Market. Leading players in the Automotive Semiconductor Market are heavily investing in research and development to push the boundaries of Class D amplifier performance, focusing on higher switching frequencies to improve audio fidelity, reducing electromagnetic interference (EMI) to ensure compatibility with other sensitive automotive electronics, and integrating advanced protection features. The convergence of these technological advantages solidifies the Class D Amplifier Market's position as the cornerstone of automotive audio amplification, driving innovation and setting performance benchmarks for the entire industry. As the Passenger Vehicles Market continues to emphasize advanced connectivity and entertainment features, the demand for high-performance, efficient Class D solutions is projected to grow further, reinforcing its dominant market share. Similarly, even the Commercial Vehicles Market is slowly adopting higher quality audio, albeit at a slower pace.

Key Growth Drivers & Technological Shifts in Automotive Audio Amplifier IC Market

The Automotive Audio Amplifier IC Market is significantly propelled by several key drivers and concurrent technological shifts. A primary driver is the escalating consumer demand for enhanced in-car audio quality and sophisticated infotainment systems. Modern vehicles are increasingly viewed as mobile entertainment hubs, prompting automotive original equipment manufacturers (OEMs) to integrate premium audio solutions, multi-channel sound systems, and personalized audio zones, which inherently require more advanced and powerful audio amplifier ICs. This trend directly fuels the In-Vehicle Infotainment Market, creating a cascading demand for high-performance audio components. Another crucial driver is the rapid global transition to electric vehicles (EVs). EVs present unique challenges and opportunities; their quiet powertrains reveal previously masked road and wind noise, necessitating sophisticated active noise cancellation (ANC) systems, often driven by dedicated audio amplifier ICs. Furthermore, the imperative for energy efficiency in EVs to maximize range makes the high-efficiency Class D Amplifier Market particularly attractive, as these devices minimize power draw from the battery. The expansion of Digital Cockpit Systems Market is also a significant catalyst. These integrated systems merge various functions—infotainment, navigation, ADAS alerts, and communication—into a cohesive digital experience. Audio amplifier ICs are vital for delivering clear, distinct audio cues for navigation, safety warnings, and hands-free communication, requiring high reliability and low latency. The continuous innovation in semiconductor fabrication processes, leading to smaller, more powerful, and feature-rich Integrated Circuit Market components, also serves as a fundamental enabler. These advancements allow manufacturers to develop highly integrated audio amplifier ICs with embedded DSP, power management, and diagnostic capabilities, streamlining vehicle design and reducing system complexity. However, the market faces constraints such as intense cost pressures from OEMs, particularly for mass-market vehicles, and the persistent challenge of global supply chain volatility, which can impact the availability and pricing of critical semiconductor components, affecting the broader Automotive Semiconductor Market.

Sustainability & ESG Pressures on Automotive Audio Amplifier IC Market

The Automotive Audio Amplifier IC Market is increasingly navigating a complex landscape shaped by sustainability and ESG (Environmental, Social, and Governance) pressures. Environmental regulations, particularly those concerning hazardous substances like lead, mercury, cadmium, and hexavalent chromium (e.g., RoHS, REACH directives), mandate the development and use of eco-friendly materials and manufacturing processes for all Integrated Circuit Market components. This pushes IC manufacturers to innovate in packaging materials, solder alloys, and internal component compositions to comply with global standards, ensuring that Automotive Audio Amplifier ICs are not only high-performing but also environmentally benign throughout their lifecycle. Energy efficiency, a hallmark of modern Class D amplifier designs, is a significant ESG driver. The push for electric vehicles (EVs) intensifies the need for components that minimize power consumption, directly impacting vehicle range and energy footprint. Consequently, suppliers in the Automotive Electronics Market are prioritizing ultra-efficient amplifier designs, reducing quiescent current, and optimizing power stages to meet strict OEM energy targets. Circular economy principles are also gaining traction, encouraging manufacturers to design ICs for durability and recyclability, considering end-of-life management. This includes using fewer rare earth materials, designing for modularity, and enabling easier material recovery. Social aspects involve ethical sourcing of raw materials, fair labor practices in manufacturing facilities, and ensuring supply chain transparency—especially critical given the global nature of semiconductor production. Governance factors include robust corporate ethics, anti-corruption policies, and data security, vital for companies operating in the highly competitive and sensitive automotive supply chain. ESG investor criteria are increasingly influencing corporate valuations and access to capital, compelling companies within the Automotive Semiconductor Market to adopt comprehensive sustainability strategies and publicly report their progress. This holistic approach to sustainability and ESG is not merely a compliance burden but a strategic imperative, driving innovation in product design, manufacturing, and supply chain management for the Automotive Audio Amplifier IC Market.

Export, Trade Flow & Tariff Impact on Automotive Audio Amplifier IC Market

The Automotive Audio Amplifier IC Market is intrinsically linked to global export and trade flows, significantly influenced by macroeconomic policies, geopolitical dynamics, and regional manufacturing hubs. Major trade corridors for these specialized ICs primarily involve Asia Pacific (notably China, Japan, South Korea, Taiwan) as leading exporting regions, supplying components to automotive assembly plants and Tier 1 suppliers in North America and Europe. This intricate global supply chain for the Integrated Circuit Market is subject to various tariff and non-tariff barriers. Recent trade policies, such as the US-China trade tensions, have imposed tariffs on specific electronic components, leading to increased landed costs for Automotive Audio Amplifier ICs in certain markets. These tariffs can compel manufacturers to re-evaluate their supply chain strategies, potentially leading to diversification of manufacturing bases or reshoring efforts to mitigate import duties and reduce geopolitical risks. For instance, a tariff on digital amplifier ICs manufactured in one region could increase the final cost of an infotainment system in another, directly impacting the Digital Amplifier IC Market and the broader In-Vehicle Infotainment Market. Non-tariff barriers, including stringent regulatory compliance (e.g., cybersecurity standards, environmental certifications) and complex customs procedures, also affect trade flow by increasing lead times and administrative burdens. Furthermore, regional trade agreements (e.g., USMCA, EU-ASEAN agreements) play a crucial role in facilitating smoother cross-border movement of goods by reducing tariffs and harmonizing standards, thereby promoting regional specialization and efficiency. Conversely, the absence or breakdown of such agreements can fragment the market and increase operational costs. The global automotive industry’s reliance on just-in-time (JIT) inventory management makes it highly vulnerable to disruptions in trade flows caused by tariffs, logistical bottlenecks, or geopolitical conflicts. Such disruptions can lead to component shortages, production delays for vehicle manufacturers, and volatile pricing for Automotive Audio Amplifier ICs. The long-term impact includes a potential shift towards more localized supply chains, increasing resilience but possibly at the cost of global cost efficiencies, thereby influencing strategic sourcing decisions within the Automotive Electronics Market.

Competitive Ecosystem of Automotive Audio Amplifier IC Market

The Automotive Audio Amplifier IC Market is characterized by a competitive landscape dominated by several global semiconductor giants, alongside specialized players renowned for their innovation and product reliability. These companies continuously invest in R&D to deliver high-performance, energy-efficient, and feature-rich amplifier solutions crucial for modern automotive applications. The intense competition is driven by the demand for advanced audio quality, power efficiency, and seamless integration within complex vehicle architectures.

STMicroelectronics: A diversified semiconductor leader offering a broad portfolio of automotive-grade ICs, including advanced audio amplifiers for various infotainment and telematics applications, emphasizing robust performance and reliability.

TI: A prominent player in analog and embedded processing, Texas Instruments provides a wide range of automotive audio amplifiers, known for their high efficiency, low distortion, and integrated diagnostic features for safety-critical applications.

NXP: Specializing in secure connections for a smarter world, NXP offers innovative audio solutions for automotive, focusing on high-performance Class D amplifiers and integrated audio platforms that support multi-zone audio and active noise cancellation.

Infineon: A global leader in automotive semiconductors, Infineon delivers high-quality audio amplifier ICs, emphasizing power efficiency and integration, particularly relevant for electric vehicle applications and premium sound systems.

Cirrus Logic: Known for its high-performance mixed-signal circuits, Cirrus Logic supplies advanced audio solutions, including sophisticated Class D amplifiers and audio codecs, that enable immersive audio experiences in automotive infotainment systems.

Renesas: A leading provider of advanced semiconductor solutions, Renesas offers a portfolio of audio amplifier ICs designed for automotive applications, focusing on robust performance, low power consumption, and integration with its broader automotive microcontrollers.

ROHM: A Japanese semiconductor manufacturer with a strong presence in automotive, ROHM provides a range of audio amplifier ICs, emphasizing compact size, high efficiency, and quality sound reproduction for in-vehicle audio systems.

Nisshinbo Micro Devices: Offers specialized analog ICs, including audio amplifiers, with a focus on high reliability and performance tailored for the demanding automotive environment, contributing to advanced audio experiences.

Diodes Incorporated: Known for its broad range of discrete, logic, analog, and mixed-signal semiconductors, Diodes Incorporated provides a selection of audio amplifier solutions suitable for various automotive applications, emphasizing compact designs and efficiency.

Recent Developments & Milestones in Automotive Audio Amplifier IC Market

January 2024: A major semiconductor firm launched a new generation of Automotive Audio Amplifier ICs featuring integrated digital signal processors (DSPs) and advanced networking capabilities, designed to support multi-zone audio and active noise cancellation in premium electric vehicles, addressing demand in the Automotive Electronics Market.

September 2023: A Tier 1 automotive supplier announced a strategic partnership with a leading Class D Amplifier Market specialist to co-develop highly efficient and compact audio amplifier modules for next-generation Passenger Vehicles Market platforms, aiming to reduce system footprint and power consumption.

April 2023: Developments in GaN (Gallium Nitride) and SiC (Silicon Carbide) based power stages for high-power Class D audio amplifiers were showcased, promising even greater efficiency and smaller form factors. These advancements are expected to penetrate the high-end Automotive Audio Amplifier IC Market for ultra-premium sound systems and contribute to the broader Automotive Semiconductor Market innovation.

November 2022: Regulatory bodies in Europe released updated guidelines for electromagnetic compatibility (EMC) testing for in-vehicle electronic components, including audio amplifier ICs. This development requires manufacturers to enhance their design processes to ensure robust interference suppression, impacting the development of new Digital Amplifier IC Market products.

July 2022: Several Integrated Circuit Market companies announced new low-power, multi-channel audio amplifier ICs specifically optimized for Digital Cockpit Systems Market, enabling seamless integration of navigation alerts, voice commands, and infotainment audio within a unified digital environment, reducing component count and complexity.

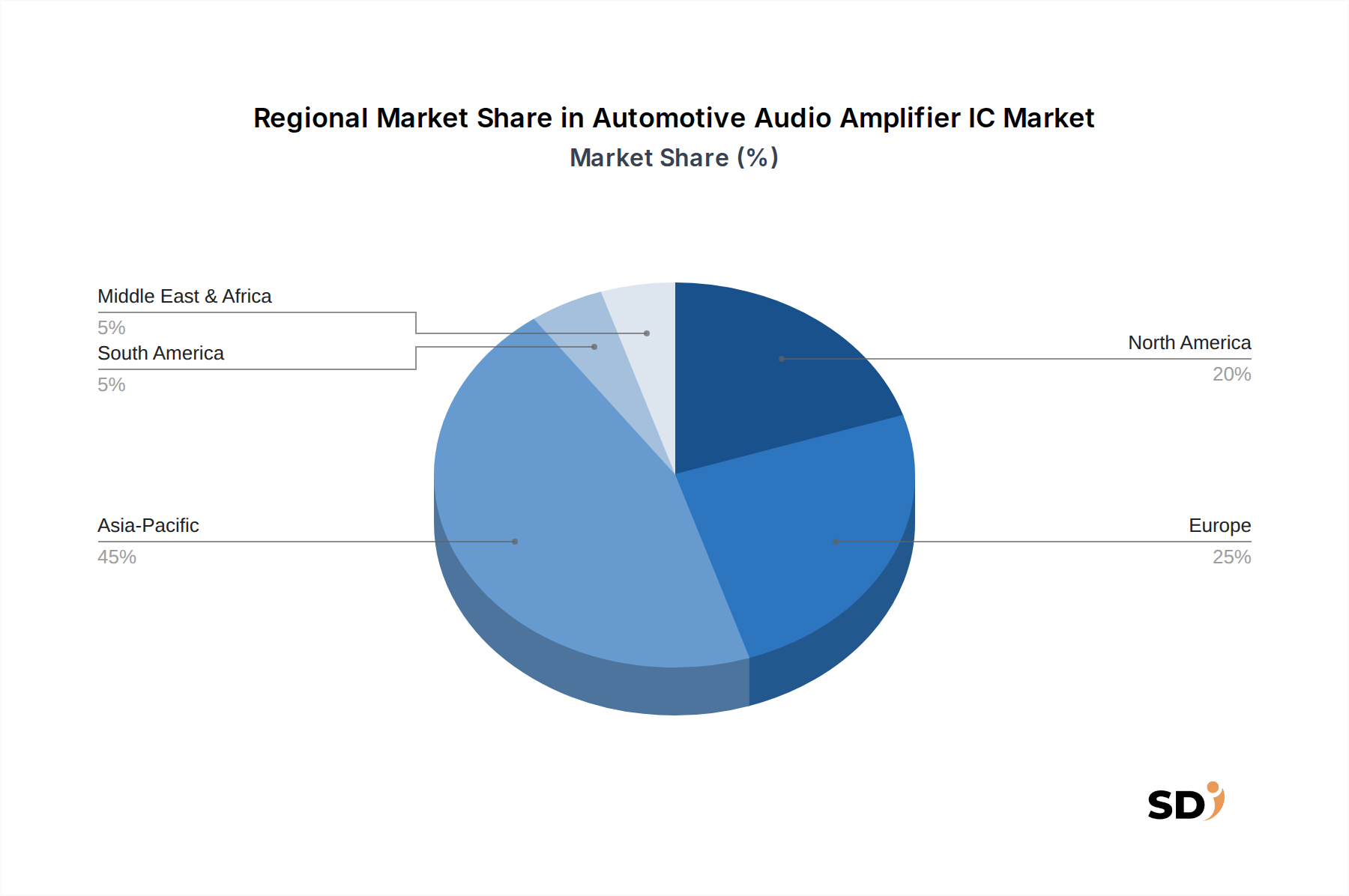

Regional Market Breakdown for Automotive Audio Amplifier IC Market

The global Automotive Audio Amplifier IC Market exhibits distinct regional dynamics, influenced by varying automotive production volumes, consumer preferences, and technological adoption rates. Asia Pacific stands as the dominant region, primarily driven by the massive automotive manufacturing bases in China, Japan, South Korea, and India. This region benefits from rapid adoption of electric vehicles and increasing demand for advanced in-vehicle infotainment systems, making it a critical hub for the Automotive Electronics Market. China, in particular, leads in both production and consumption, driving significant demand for Automotive Audio Amplifier ICs. The region is expected to demonstrate the highest CAGR, fueled by expanding middle-class populations and aggressive government policies promoting EV adoption.

Europe represents a significant market share, characterized by the presence of premium automotive brands and stringent quality standards. Countries like Germany, France, and Italy are key contributors, focusing on high-fidelity audio systems and integrated digital cockpits in their luxury and high-performance vehicle segments. The demand here is driven by consumers' willingness to pay for superior audio experiences and the continuous innovation from European OEMs in In-Vehicle Infotainment Market solutions. The regional CAGR is robust, albeit slightly lower than Asia Pacific, due to market maturity but sustained by technological leadership.

North America, led by the United States and Canada, also holds a substantial share of the Automotive Audio Amplifier IC Market. This region is driven by strong demand for large SUVs and pickup trucks equipped with feature-rich infotainment systems and advanced connectivity. The growth of electric vehicle manufacturing and aftermarket audio upgrades further contributes to the market. Investments in autonomous driving technologies and Digital Cockpit Systems Market also necessitate sophisticated audio solutions for alerts and communication, ensuring a stable growth trajectory.

South America, with Brazil and Argentina as key economies, represents an emerging market. While smaller in absolute terms, it is poised for moderate growth, primarily from increasing vehicle production volumes and gradual adoption of more advanced in-car entertainment systems in both the Passenger Vehicles Market and Commercial Vehicles Market. Economic stability and foreign investments in automotive manufacturing will be crucial for accelerating this region's expansion. The Middle East & Africa region is currently the smallest market but is expected to experience growth driven by increasing disposable incomes and urbanization, leading to higher vehicle sales and a gradual upgrade in vehicle technology. However, infrastructural challenges and political instability in certain parts may moderate its growth rate compared to other regions.

Automotive Audio Amplifier IC Segmentation

1. Amplifier Class

1.1. Class A

1.2. Class B

1.3. Class AB

1.4. Class D

1.5. Others

2. Vehicle Type

2.1. Passenger Vehicles

2.2. Commercial Vehicles

3. Signal Type

3.1. Analog Amplifier IC

3.2. Digital Amplifier IC

4. Application

4.1. Infotainment Systems

4.2. Head Units

4.3. Digital Cockpit Systems

4.4. Rear-seat Entertainment

4.5. Others

Automotive Audio Amplifier IC Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Automotive Audio Amplifier IC REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 6.2% from 2020-2034

Segmentation

By Amplifier Class

Class A

Class B

Class AB

Class D

Others

By Vehicle Type

Passenger Vehicles

Commercial Vehicles

By Signal Type

Analog Amplifier IC

Digital Amplifier IC

By Application

Infotainment Systems

Head Units

Digital Cockpit Systems

Rear-seat Entertainment

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Amplifier Class

5.1.1. Class A

5.1.2. Class B

5.1.3. Class AB

5.1.4. Class D

5.1.5. Others

5.2. Market Analysis, Insights and Forecast - by Vehicle Type

5.2.1. Passenger Vehicles

5.2.2. Commercial Vehicles

5.3. Market Analysis, Insights and Forecast - by Signal Type

5.3.1. Analog Amplifier IC

5.3.2. Digital Amplifier IC

5.4. Market Analysis, Insights and Forecast - by Application

5.4.1. Infotainment Systems

5.4.2. Head Units

5.4.3. Digital Cockpit Systems

5.4.4. Rear-seat Entertainment

5.4.5. Others

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Amplifier Class

6.1.1. Class A

6.1.2. Class B

6.1.3. Class AB

6.1.4. Class D

6.1.5. Others

6.2. Market Analysis, Insights and Forecast - by Vehicle Type

6.2.1. Passenger Vehicles

6.2.2. Commercial Vehicles

6.3. Market Analysis, Insights and Forecast - by Signal Type

6.3.1. Analog Amplifier IC

6.3.2. Digital Amplifier IC

6.4. Market Analysis, Insights and Forecast - by Application

6.4.1. Infotainment Systems

6.4.2. Head Units

6.4.3. Digital Cockpit Systems

6.4.4. Rear-seat Entertainment

6.4.5. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Amplifier Class

7.1.1. Class A

7.1.2. Class B

7.1.3. Class AB

7.1.4. Class D

7.1.5. Others

7.2. Market Analysis, Insights and Forecast - by Vehicle Type

7.2.1. Passenger Vehicles

7.2.2. Commercial Vehicles

7.3. Market Analysis, Insights and Forecast - by Signal Type

7.3.1. Analog Amplifier IC

7.3.2. Digital Amplifier IC

7.4. Market Analysis, Insights and Forecast - by Application

7.4.1. Infotainment Systems

7.4.2. Head Units

7.4.3. Digital Cockpit Systems

7.4.4. Rear-seat Entertainment

7.4.5. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Amplifier Class

8.1.1. Class A

8.1.2. Class B

8.1.3. Class AB

8.1.4. Class D

8.1.5. Others

8.2. Market Analysis, Insights and Forecast - by Vehicle Type

8.2.1. Passenger Vehicles

8.2.2. Commercial Vehicles

8.3. Market Analysis, Insights and Forecast - by Signal Type

8.3.1. Analog Amplifier IC

8.3.2. Digital Amplifier IC

8.4. Market Analysis, Insights and Forecast - by Application

8.4.1. Infotainment Systems

8.4.2. Head Units

8.4.3. Digital Cockpit Systems

8.4.4. Rear-seat Entertainment

8.4.5. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Amplifier Class

9.1.1. Class A

9.1.2. Class B

9.1.3. Class AB

9.1.4. Class D

9.1.5. Others

9.2. Market Analysis, Insights and Forecast - by Vehicle Type

9.2.1. Passenger Vehicles

9.2.2. Commercial Vehicles

9.3. Market Analysis, Insights and Forecast - by Signal Type

9.3.1. Analog Amplifier IC

9.3.2. Digital Amplifier IC

9.4. Market Analysis, Insights and Forecast - by Application

9.4.1. Infotainment Systems

9.4.2. Head Units

9.4.3. Digital Cockpit Systems

9.4.4. Rear-seat Entertainment

9.4.5. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Amplifier Class

10.1.1. Class A

10.1.2. Class B

10.1.3. Class AB

10.1.4. Class D

10.1.5. Others

10.2. Market Analysis, Insights and Forecast - by Vehicle Type

10.2.1. Passenger Vehicles

10.2.2. Commercial Vehicles

10.3. Market Analysis, Insights and Forecast - by Signal Type

10.3.1. Analog Amplifier IC

10.3.2. Digital Amplifier IC

10.4. Market Analysis, Insights and Forecast - by Application

10.4.1. Infotainment Systems

10.4.2. Head Units

10.4.3. Digital Cockpit Systems

10.4.4. Rear-seat Entertainment

10.4.5. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. STMicroelectronics

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. TI

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. NXP

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Infineon

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Cirrus Logic

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Renesas

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. ROHM

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Nisshinbo Micro Devices

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Diodes Incorporated

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (million, %) by Region 2025 & 2033

Figure 2: Revenue (million), by Amplifier Class 2025 & 2033

Figure 3: Revenue Share (%), by Amplifier Class 2025 & 2033

Figure 4: Revenue (million), by Vehicle Type 2025 & 2033

Figure 5: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 6: Revenue (million), by Signal Type 2025 & 2033

Figure 7: Revenue Share (%), by Signal Type 2025 & 2033

Figure 8: Revenue (million), by Application 2025 & 2033

Figure 9: Revenue Share (%), by Application 2025 & 2033

Figure 10: Revenue (million), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (million), by Amplifier Class 2025 & 2033

Figure 13: Revenue Share (%), by Amplifier Class 2025 & 2033

Figure 14: Revenue (million), by Vehicle Type 2025 & 2033

Figure 15: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 16: Revenue (million), by Signal Type 2025 & 2033

Figure 17: Revenue Share (%), by Signal Type 2025 & 2033

Figure 18: Revenue (million), by Application 2025 & 2033

Figure 19: Revenue Share (%), by Application 2025 & 2033

Figure 20: Revenue (million), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (million), by Amplifier Class 2025 & 2033

Figure 23: Revenue Share (%), by Amplifier Class 2025 & 2033

Figure 24: Revenue (million), by Vehicle Type 2025 & 2033

Figure 25: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 26: Revenue (million), by Signal Type 2025 & 2033

Figure 27: Revenue Share (%), by Signal Type 2025 & 2033

Figure 28: Revenue (million), by Application 2025 & 2033

Figure 29: Revenue Share (%), by Application 2025 & 2033

Figure 30: Revenue (million), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (million), by Amplifier Class 2025 & 2033

Figure 33: Revenue Share (%), by Amplifier Class 2025 & 2033

Figure 34: Revenue (million), by Vehicle Type 2025 & 2033

Figure 35: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 36: Revenue (million), by Signal Type 2025 & 2033

Figure 37: Revenue Share (%), by Signal Type 2025 & 2033

Figure 38: Revenue (million), by Application 2025 & 2033

Figure 39: Revenue Share (%), by Application 2025 & 2033

Figure 40: Revenue (million), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (million), by Amplifier Class 2025 & 2033

Figure 43: Revenue Share (%), by Amplifier Class 2025 & 2033

Figure 44: Revenue (million), by Vehicle Type 2025 & 2033

Figure 45: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 46: Revenue (million), by Signal Type 2025 & 2033

Figure 47: Revenue Share (%), by Signal Type 2025 & 2033

Figure 48: Revenue (million), by Application 2025 & 2033

Figure 49: Revenue Share (%), by Application 2025 & 2033

Figure 50: Revenue (million), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue million Forecast, by Amplifier Class 2020 & 2033

Table 2: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 3: Revenue million Forecast, by Signal Type 2020 & 2033

Table 4: Revenue million Forecast, by Application 2020 & 2033

Table 5: Revenue million Forecast, by Region 2020 & 2033

Table 6: Revenue million Forecast, by Amplifier Class 2020 & 2033

Table 7: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 8: Revenue million Forecast, by Signal Type 2020 & 2033

Table 9: Revenue million Forecast, by Application 2020 & 2033

Table 10: Revenue million Forecast, by Country 2020 & 2033

Table 11: Revenue (million) Forecast, by Application 2020 & 2033

Table 12: Revenue (million) Forecast, by Application 2020 & 2033

Table 13: Revenue (million) Forecast, by Application 2020 & 2033

Table 14: Revenue million Forecast, by Amplifier Class 2020 & 2033

Table 15: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 16: Revenue million Forecast, by Signal Type 2020 & 2033

Table 17: Revenue million Forecast, by Application 2020 & 2033

Table 18: Revenue million Forecast, by Country 2020 & 2033

Table 19: Revenue (million) Forecast, by Application 2020 & 2033

Table 20: Revenue (million) Forecast, by Application 2020 & 2033

Table 21: Revenue (million) Forecast, by Application 2020 & 2033

Table 22: Revenue million Forecast, by Amplifier Class 2020 & 2033

Table 23: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 24: Revenue million Forecast, by Signal Type 2020 & 2033

Table 25: Revenue million Forecast, by Application 2020 & 2033

Table 26: Revenue million Forecast, by Country 2020 & 2033

Table 27: Revenue (million) Forecast, by Application 2020 & 2033

Table 28: Revenue (million) Forecast, by Application 2020 & 2033

Table 29: Revenue (million) Forecast, by Application 2020 & 2033

Table 30: Revenue (million) Forecast, by Application 2020 & 2033

Table 31: Revenue (million) Forecast, by Application 2020 & 2033

Table 32: Revenue (million) Forecast, by Application 2020 & 2033

Table 33: Revenue (million) Forecast, by Application 2020 & 2033

Table 34: Revenue (million) Forecast, by Application 2020 & 2033

Table 35: Revenue (million) Forecast, by Application 2020 & 2033

Table 36: Revenue million Forecast, by Amplifier Class 2020 & 2033

Table 37: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 38: Revenue million Forecast, by Signal Type 2020 & 2033

Table 39: Revenue million Forecast, by Application 2020 & 2033

Table 40: Revenue million Forecast, by Country 2020 & 2033

Table 41: Revenue (million) Forecast, by Application 2020 & 2033

Table 42: Revenue (million) Forecast, by Application 2020 & 2033

Table 43: Revenue (million) Forecast, by Application 2020 & 2033

Table 44: Revenue (million) Forecast, by Application 2020 & 2033

Table 45: Revenue (million) Forecast, by Application 2020 & 2033

Table 46: Revenue (million) Forecast, by Application 2020 & 2033

Table 47: Revenue million Forecast, by Amplifier Class 2020 & 2033

Table 48: Revenue million Forecast, by Vehicle Type 2020 & 2033

Table 49: Revenue million Forecast, by Signal Type 2020 & 2033

Table 50: Revenue million Forecast, by Application 2020 & 2033

Table 51: Revenue million Forecast, by Country 2020 & 2033

Table 52: Revenue (million) Forecast, by Application 2020 & 2033

Table 53: Revenue (million) Forecast, by Application 2020 & 2033

Table 54: Revenue (million) Forecast, by Application 2020 & 2033

Table 55: Revenue (million) Forecast, by Application 2020 & 2033

Table 56: Revenue (million) Forecast, by Application 2020 & 2033

Table 57: Revenue (million) Forecast, by Application 2020 & 2033

Table 58: Revenue (million) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research strategy forms the cornerstone of our market analysis, accounting for 70-80% of our total research effort. This extensive approach ensures that our findings are grounded in current industry realities and expert perspectives. We conducted in-depth interviews and discussions with a wide array of stakeholders across the automotive audio amplifier IC value chain.

Key participants in our primary research included:

Company Types:

Automotive Semiconductor Manufacturers

Tier 1 Automotive Electronics Suppliers

Automotive Original Equipment Manufacturers (OEMs)

Specialized Automotive Audio System Integrators

Automotive IC Design Houses

Job Designations/Stakeholders:

VP, Automotive Electronics Division

Director of Infotainment Systems Development

Head of Component Sourcing & Procurement

Senior Product Manager, Audio ICs

These interactions provided critical qualitative and quantitative insights, validating secondary data and offering nuanced perspectives on market drivers, restraints, opportunities, competitive landscape, and future trends. Our outreach spanned across all key geographical regions covered in this report, ensuring a global perspective.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP, Automotive Electronics Division

30%

Director of Infotainment Systems Development

25%

Head of Component Sourcing & Procurement

25%

Senior Product Manager, Audio ICs

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Automotive Semiconductor Manufacturers

30%

Tier 1 Automotive Electronics Suppliers

25%

Automotive Original Equipment Manufacturers (OEMs)

20%

Specialized Automotive Audio System Integrators

15%

Automotive IC Design Houses

10%

Secondary Research & Industry Benchmarking

Complementing our primary research, a rigorous secondary research phase was undertaken to establish a foundational understanding of the market and to cross-reference primary insights. This phase comprised 20-30% of our total research. Our secondary data collection adheres strictly to reputable, publicly available sources, avoiding other market research websites to maintain data integrity and independence.

Key secondary research sources utilized include:

Financial Databases: Bloomberg, Factiva, Hoovers, PitchBook for company profiles, financial performance, and strategic activities of key players.

Government & Regulatory Bodies: Official reports, statistics, and policy documents from relevant government agencies (e.g., national automotive safety administrations, trade departments).

Trade Associations & Industry Bodies: Comprehensive data, publications, and reports from globally recognized automotive and electronics associations. Examples include:

Company Filings: Annual reports, investor presentations, and public disclosures of listed companies operating in the automotive semiconductor and audio markets.

Academic Publications & White Papers: Peer-reviewed journals and technical papers focusing on advancements in audio IC technology and automotive electronics.

This meticulous secondary research provides essential market indicators, historical data, technological benchmarks, and industry trends that shape the automotive audio amplifier IC landscape.

Demand Modeling & Market Estimation

Our market estimation process employs a robust combination of top-down and bottom-up methodologies, rigorously cross-validated through multi-level data triangulation. This approach ensures the comprehensive and accurate sizing of the market from various vantage points.

Bottom-Up Approach: This method involves aggregating micro-level data to derive overall market figures. For the automotive audio amplifier IC market, key variables utilized include:

Global and regional automotive production volumes (by Passenger Vehicles and Commercial Vehicles segments).

Average number of audio amplifier ICs deployed per vehicle, segmented by application (e.g., Head Units, Digital Cockpit Systems, Rear-seat Entertainment) and amplifier class.

Average Selling Price (ASP) of automotive audio amplifier ICs, differentiated by amplifier class (Class A, B, AB, D), signal type (Analog, Digital), and features.

Penetration rates of advanced infotainment systems and premium audio solutions across different vehicle segments.

Top-Down Approach: This method begins with macro-economic indicators and broad industry figures, progressively disaggregating them into specific market segments. We analyze overall automotive electronics market growth, infotainment system market growth, and the semiconductor content per vehicle to estimate the addressable market for audio amplifier ICs.

Multi-Level Data Triangulation: Data points derived from both primary and secondary research, and from top-down and bottom-up analyses, are rigorously cross-referenced and validated. This iterative process helps in identifying discrepancies, refining assumptions, and ultimately converging on the most accurate market figures. All market estimates are updated dynamically, ensuring the report reflects the latest available data up to the date of purchase.

Data Accuracy & Quality Check

Our commitment to data accuracy is paramount. Through our stringent methodologies and exhaustive validation processes, we guarantee an estimated data accuracy level of 85-90%. Every data point, trend, and forecast undergoes multiple layers of quality checks by our senior analysts. This includes:

Expert Review: All findings are reviewed by subject matter experts to ensure industry relevance and logical consistency.

Statistical Validation: Quantitative data is subjected to statistical analysis to identify outliers and ensure statistical robustness.

Scenario Analysis: Multiple market scenarios are considered (optimistic, pessimistic, and most likely) to provide a comprehensive range of potential outcomes and validate the resilience of our forecasts.

Continuous Feedback Loop: Insights gained from primary interviews are continuously fed back into our models, allowing for real-time adjustments and refinements of market estimates and forecasts.

This rigorous quality assurance framework ensures that our "Automotive Audio Amplifier IC Market" report provides reliable, actionable, and highly accurate intelligence for strategic decision-making.

Frequently Asked Questions

1. Which region shows the fastest growth in the Automotive Audio Amplifier IC market?

Based on current automotive production trends and increasing adoption of advanced infotainment systems, Asia-Pacific is projected to lead market growth, driven by countries like China and India. Emerging opportunities also exist in ASEAN nations as vehicle ownership rises within this 0.45 market share region.

2. What are the key supply chain considerations for Automotive Audio Amplifier ICs?

Supply chain considerations involve securing critical semiconductor materials and manufacturing capacities from major foundries. Geopolitical factors and trade policies can impact the global availability and pricing of specialized silicon wafers and other components for these ICs, affecting companies like STMicroelectronics and NXP.

3. How do end-user industries influence Automotive Audio Amplifier IC demand?

The Automotive Audio Amplifier IC market is directly driven by demand from infotainment systems, head units, and digital cockpit systems in both passenger and commercial vehicles. The increasing integration of rear-seat entertainment also contributes to downstream demand patterns, impacting applications like Digital Cockpit Systems.

4. What challenges face the Automotive Audio Amplifier IC market?

Key challenges include the highly competitive landscape with major players like STMicroelectronics, TI, and NXP, along with potential supply chain disruptions affecting semiconductor component availability. Rapid technological evolution necessitates continuous R&D investment for product differentiation, especially in Amplifier Class innovations such as Class D.

5. What primary drivers boost the Automotive Audio Amplifier IC market?

Primary growth drivers include the rising demand for advanced in-car entertainment and infotainment systems, increasing adoption of Class D amplifiers for efficiency, and the overall growth in automotive production globally. The integration of digital cockpit systems further catalyzes demand, contributing to a projected market size of $5183 million by 2025.

6. Is there significant investment activity in the Automotive Audio Amplifier IC sector?

While specific funding rounds for ICs are often part of broader semiconductor investments, major players such as Infineon, NXP, and Renesas continually invest in R&D for advanced automotive electronics. Strategic partnerships and acquisitions in related automotive tech sectors indirectly support this market segment, driving its 6.2% CAGR.