Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Automotive 5G TCU: $18B by 2033, 7.6% CAGR Drivers

Automotive 5G TCU

Automotive 5G TCU: $18B by 2033, 7.6% CAGR Drivers

Automotive 5G TCU by Component (Hardware, Software, Services), by Vehicle Type (Passenger Vehicles, Commercial Vehicles), by Communication Mode (V2X) (Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Network (V2N), Others), by End User (Automotive OEMs, Aftermarket suppliers), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 119

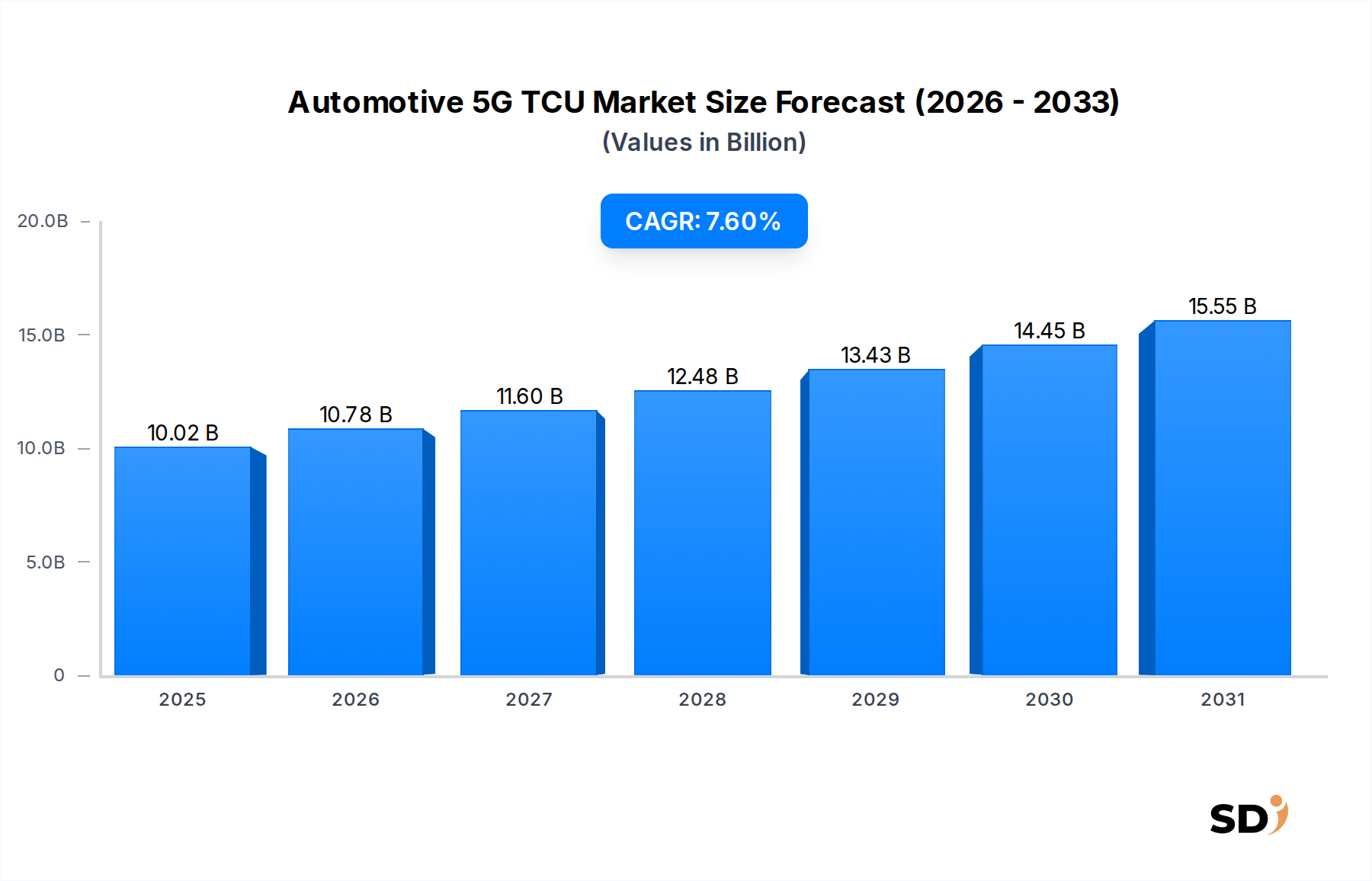

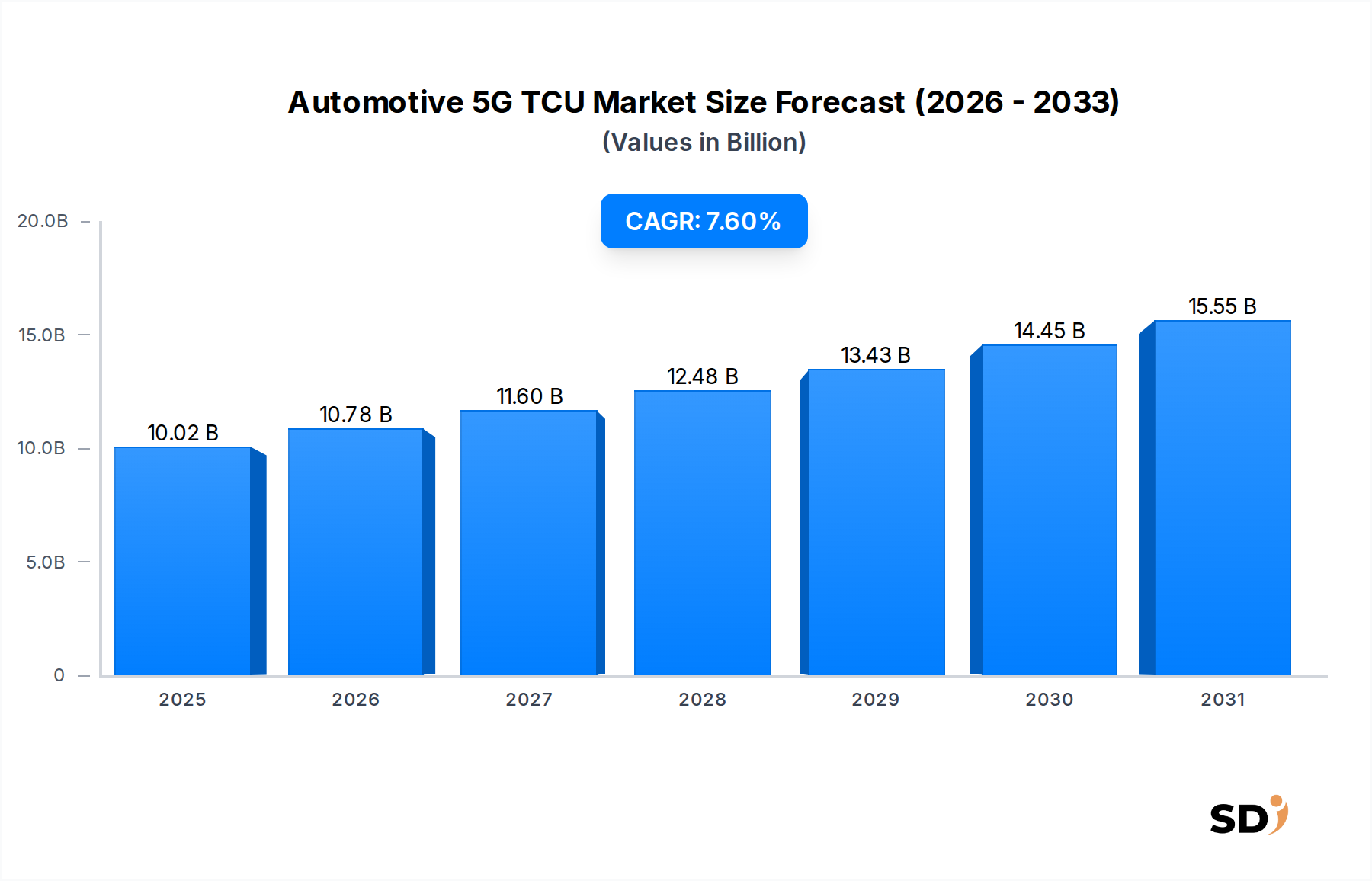

The Global Automotive 5G TCU Market is poised for substantial expansion, demonstrating a robust compound annual growth rate (CAGR) of 7.6% from its base year valuation in 2025. This trajectory is projected to propel the market value from USD 10.02 billion in 2025 towards a significantly higher valuation by the end of the forecast period. The primary impetus behind this accelerated growth is the escalating demand for high-speed, low-latency connectivity within the automotive sector, crucial for enabling advanced driver-assistance systems (ADAS), autonomous driving functionalities, and sophisticated in-vehicle infotainment experiences. The integration of 5G technology into Telematics Control Units (TCUs) transforms vehicles into highly connected, data-rich nodes capable of real-time communication with other vehicles, infrastructure, and network services. This capability is fundamental for the proliferation of the Connected Car Market, which increasingly relies on resilient and ultra-fast wireless communication to deliver enhanced safety, efficiency, and comfort.

Automotive 5G TCU Market Size (In Billion)

20.0B

15.0B

10.0B

5.0B

0

10.02 B

2025

10.78 B

2026

11.60 B

2027

12.48 B

2028

13.43 B

2029

14.45 B

2030

15.55 B

2031

Key demand drivers include the global push for smarter urban mobility solutions, increasing regulatory mandates for vehicle-to-everything (V2X) communication standards, and the widespread adoption of over-the-air (OTA) software updates. These updates reduce recall costs for original equipment manufacturers (OEMs) and enable continuous feature enhancements, thereby extending the vehicle's lifecycle and value proposition. Furthermore, the Automotive Telematics Market is undergoing a significant transformation, with 5G TCUs serving as the central nervous system for data acquisition, processing, and transmission. This facilitates a plethora of services ranging from predictive maintenance and fleet management to emergency calling (eCall) and stolen vehicle recovery systems. The robust growth observed in the Passenger Vehicle Market and the Commercial Vehicle Market, particularly in emerging economies, further underpins the demand for advanced connectivity solutions. As autonomous driving capabilities mature, the criticality of reliable 5G connectivity for sensor data fusion, remote operation, and real-time mapping will solidify the Automotive 5G TCU Market's indispensable role in the future automotive landscape. The continuous evolution of network infrastructure and the decline in the cost of 5G modem chipsets are expected to further catalyze market expansion.

Component Segment Dominance in the Automotive 5G TCU Market

The Component segment is anticipated to hold the largest revenue share within the Global Automotive 5G TCU Market, primarily driven by the high value and technological sophistication embedded within its sub-segments: Hardware, Software, and Services. Hardware components, particularly 5G modem chipsets and GNSS modules, represent the foundational elements enabling the high-speed data transmission and precise positioning capabilities inherent to 5G TCUs. The ongoing innovation in semiconductor manufacturing, coupled with the increasing complexity of 5G New Radio (NR) standards, translates into significant research and development investments and, consequently, higher unit costs for these critical components. The demand for multi-mode chipsets that support various cellular technologies (4G LTE, 5G NR) and frequency bands ensures a continuous revenue stream for chipset manufacturers. The GNSS Module Market, crucial for accurate location-based services, navigation, and V2X applications, also contributes substantially to this segment's dominance, with enhanced precision requirements for autonomous driving scenarios.

Beyond hardware, the Software sub-segment, encompassing embedded operating systems (OS) and cybersecurity software, is experiencing rapid growth in value. As TCUs become more sophisticated, the need for robust, secure, and efficient embedded OS solutions becomes paramount to manage complex applications and ensure seamless communication. The rising prevalence of cyber threats targeting connected vehicles underscores the critical importance of specialized Automotive Cybersecurity Market solutions integrated directly into the TCU. These solutions protect sensitive vehicle data, ensure the integrity of over-the-air updates, and safeguard against unauthorized access or manipulation. The increasing software-defined vehicle paradigm further solidifies the software component's pivotal role and revenue contribution.

Moreover, the Services sub-segment, which includes connectivity services and cloud integration, plays a crucial role in maximizing the utility of 5G TCUs. These services enable real-time data exchange between vehicles and cloud platforms, facilitating advanced telematics, remote diagnostics, predictive maintenance, and personalized infotainment experiences. The recurring revenue model associated with these services, often offered on a subscription basis, provides a stable and growing revenue stream for market players. The synergistic combination of advanced hardware, intricate software, and value-added services positions the Component segment as the undeniable leader in the Automotive 5G TCU Market, dictating technological advancements and market dynamics. This dominance is expected to persist as the industry moves towards increasingly connected and autonomous vehicles, with continuous innovation in 5G modem chipsets and embedded software solutions driving further growth.

Key Market Drivers Fueling the Automotive 5G TCU Market

The Automotive 5G TCU Market is propelled by several macro-economic and technological drivers, each contributing significantly to its projected 7.6% CAGR. Foremost among these is the accelerating global deployment of 5G network infrastructure. As countries worldwide invest heavily in 5G, the operational environment for 5G TCUs expands, enabling their full potential in latency-sensitive applications. This includes real-time communication for collision avoidance, traffic management, and remote driving assistance, which are critical for the advancement of autonomous vehicle technology.

A second significant driver is the increasing regulatory pressure for enhanced vehicle safety and environmental performance. Mandates for eCall systems in regions like Europe, which require automated emergency calls in the event of a crash, are evolving to incorporate advanced connectivity for faster and more precise incident reporting. Furthermore, emerging regulations for Vehicle-to-Everything (V2X) Communication Market standards aim to improve road safety by enabling vehicles to communicate with each other (V2V), infrastructure (V2I), pedestrians (V2P), and the network (V2N). These regulatory frameworks directly necessitate the adoption of 5G TCUs capable of robust and reliable V2X functionality.

The growing consumer demand for connected services and rich in-vehicle experiences also serves as a potent driver. Modern vehicle owners expect seamless integration of their digital lives with their driving experience, demanding features such as high-definition streaming, cloud-based navigation, remote vehicle monitoring, and sophisticated voice assistants. 5G TCUs provide the necessary bandwidth and low latency to deliver these services reliably, supporting the expansion of the Passenger Vehicle Market by meeting these evolving consumer expectations. Similarly, in the Commercial Vehicle Market, demand for real-time fleet management, logistics optimization, and predictive maintenance solutions driven by 5G connectivity is growing rapidly, directly benefiting the Automotive 5G TCU Market. The increasing need for secure and efficient over-the-air (OTA) updates for software-defined vehicles is also a critical factor. OTA updates require high-bandwidth, secure connections, a capability inherently offered by 5G TCUs, enabling manufacturers to deploy new features, fix bugs, and enhance vehicle security post-sale, reducing costly physical recalls.

Competitive Ecosystem of the Automotive 5G TCU Market

The Automotive 5G TCU Market features a competitive landscape comprising established automotive suppliers, telecommunications giants, and specialized electronics manufacturers. Key players are continually investing in R&D to enhance product capabilities, integrate advanced security features, and secure supply chain partnerships.

LG: A prominent electronics and automotive component supplier, LG leverages its extensive expertise in consumer electronics and mobile communication to develop advanced 5G TCU solutions for a global automotive client base, focusing on infotainment and ADAS integration.

Harman (Samsung): As a subsidiary of Samsung, Harman benefits from its parent company's semiconductor and 5G technology prowess, offering integrated automotive solutions that include advanced TCUs, telematics, and cybersecurity for the connected car ecosystem.

Continental: A leading global automotive technology company, Continental develops comprehensive 5G TCU solutions that integrate connectivity, cybersecurity, and vehicle control functions, supporting a broad range of OEM requirements for future mobility.

Bosch: A diversified technology and services company, Bosch offers robust 5G TCU solutions as part of its broader automotive electronics portfolio, focusing on reliability, security, and seamless integration with vehicle architectures for various applications.

Marelli: Specializing in automotive components, Marelli provides advanced 5G TCUs that are crucial for connected vehicle features, emphasizing modularity and scalability to meet the diverse needs of global automakers.

Visteon: An automotive cockpit electronics specialist, Visteon integrates 5G connectivity into its digital cockpit platforms and telematics systems, aiming to deliver enhanced user experiences and advanced connected services.

Valeo: A global automotive supplier, Valeo develops intelligent 5G TCU systems that enhance vehicle safety, connectivity, and automated driving capabilities, contributing to its portfolio of smart mobility solutions.

Ficosa: A global provider of vision, safety, and connectivity solutions for the automotive industry, Ficosa offers advanced 5G TCUs that facilitate V2X communication and telematics services, leveraging its expertise in integrated systems.

Huawei: A leading global provider of ICT infrastructure and smart devices, Huawei has entered the automotive sector with its extensive 5G technology, offering highly integrated and performant 5G TCUs and related intelligent vehicle solutions.

Flaircomm Microelectronics: A specialist in wireless communication modules, Flaircomm Microelectronics develops and supplies 5G communication modules and TCUs for the automotive sector, focusing on high performance and reliability for diverse applications.

Recent Developments & Milestones in the Automotive 5G TCU Market

Recent developments in the Automotive 5G TCU Market indicate a strong push towards standardization, enhanced security, and broader deployment, reflecting the industry's commitment to advancing connected mobility.

October 2025: Multiple automotive OEMs and telecommunications providers announced a joint initiative to standardize 5G V2X communication protocols, aiming to accelerate the interoperability and widespread adoption of Vehicle-to-Everything (V2X) Communication Market technologies globally.

August 2025: A major tier-one supplier launched its next-generation 5G TCU, featuring enhanced cybersecurity hardware and software integration, designed to meet forthcoming Automotive Cybersecurity Market regulations and protect against evolving threats.

June 2025: Leading 5G modem chipset manufacturers unveiled new chipsets specifically optimized for automotive grade, offering lower power consumption and higher reliability, addressing the critical demands of the 5G Modem Chipset Market for vehicle integration.

April 2025: A prominent European automaker announced the full integration of 5G TCUs as standard across its new lineup of premium passenger vehicles, highlighting the increasing penetration of advanced connectivity in the Passenger Vehicle Market.

February 2025: Several logistics companies initiated pilot programs in North America and Europe, testing 5G-enabled TCUs in their fleets for real-time tracking, predictive maintenance, and optimized route planning, demonstrating the impact on the Commercial Vehicle Market.

December 2024: Collaborations between automotive suppliers and GNSS Module Market providers led to the development of highly accurate multi-frequency GNSS modules integrated into 5G TCUs, supporting centimeter-level positioning crucial for autonomous driving.

November 2024: Software developers released new Embedded Software Market platforms designed for 5G TCUs, focusing on over-the-air (OTA) update capabilities and improved application performance within the connected vehicle architecture.

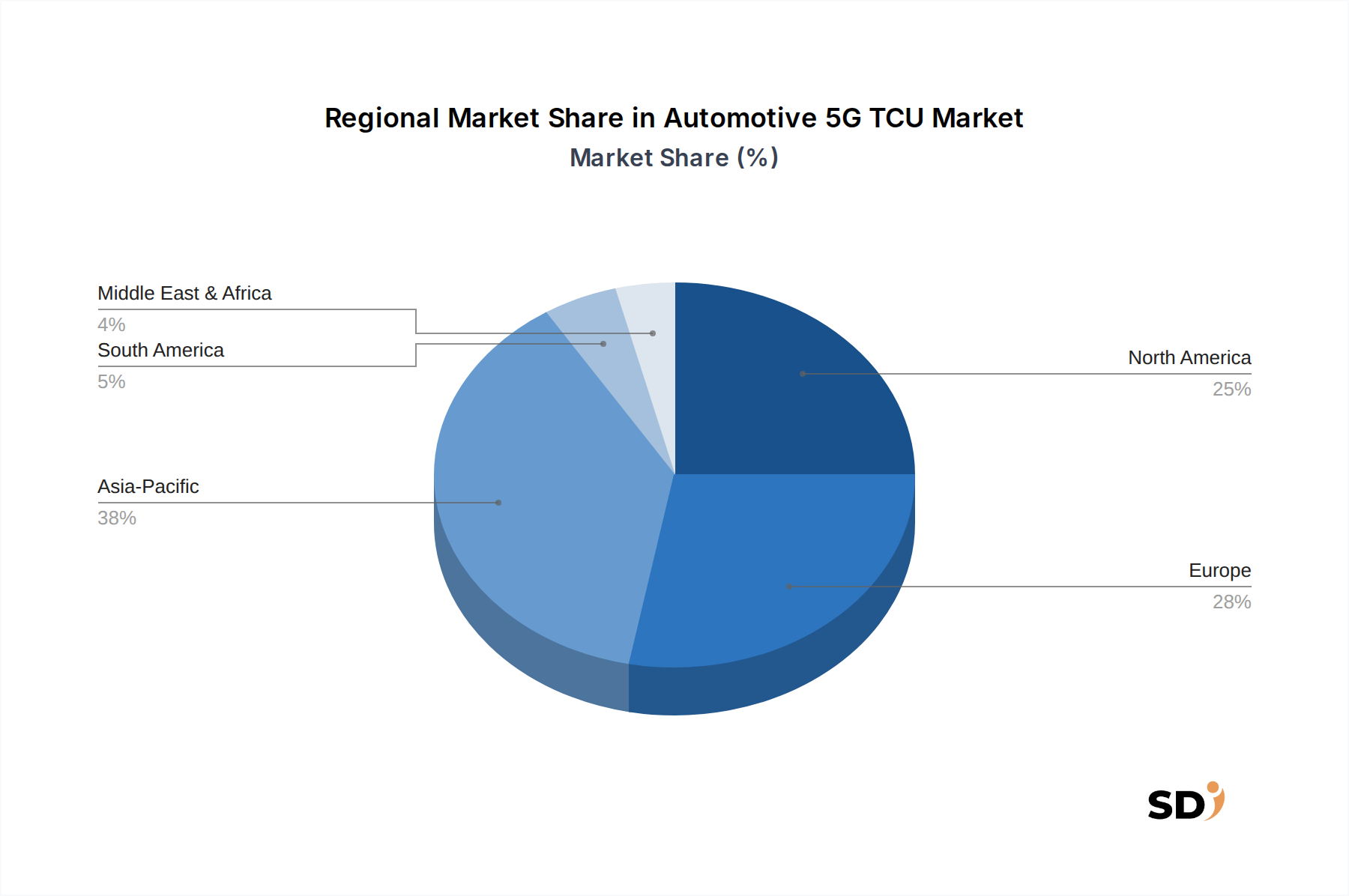

Regional Market Breakdown for the Automotive 5G TCU Market

The Automotive 5G TCU Market exhibits distinct regional dynamics, influenced by varying levels of 5G infrastructure deployment, regulatory environments, and consumer adoption rates of connected vehicle technologies. Asia Pacific is projected to emerge as the fastest-growing region, driven by aggressive 5G network rollouts, rapid urbanization, and a burgeoning electric vehicle (EV) market, particularly in China, South Korea, and Japan. These countries are at the forefront of automotive technological innovation, with robust government support for connected and autonomous driving initiatives. The region's large manufacturing base and significant investments in smart city projects further fuel the demand for 5G TCUs, enabling services from advanced telematics to sophisticated V2X applications. The strong growth in both the Passenger Vehicle Market and Commercial Vehicle Market across Asia Pacific is a key driver for 5G TCU adoption.

North America, encompassing the United States, Canada, and Mexico, represents a mature market with significant revenue share. The region benefits from early adoption of connected car technologies and strong consumer demand for high-end infotainment and safety features. Stringent regulatory requirements for vehicle safety and emergency services, alongside significant private sector investment in autonomous driving research, propel the demand for advanced 5G TCUs. Key demand drivers include the widespread deployment of 5G networks in urban areas and increasing sales of premium vehicles that integrate sophisticated connectivity as a standard feature. The Automotive Telematics Market is well-established here, facilitating the quick uptake of 5G-enabled solutions.

Europe also holds a substantial share of the Automotive 5G TCU Market, characterized by proactive regulatory frameworks such as the eCall mandate and ongoing efforts to establish common V2X communication standards. Countries like Germany, France, and the UK are driving innovation through strong automotive OEM presence and a focus on sustainable and intelligent transportation systems. While growth rates might be slightly lower than in Asia Pacific due to market maturity, consistent investment in 5G infrastructure and a high penetration of premium vehicles ensure steady demand. The focus on reducing road fatalities and improving traffic efficiency through connected technologies underpins the market's stability.

The Middle East & Africa and South America regions are expected to demonstrate moderate to high growth, albeit from a smaller base. These regions are experiencing initial phases of 5G network expansion and a gradual increase in connected vehicle adoption. Government initiatives to modernize infrastructure and improve road safety, coupled with growing vehicle sales and increasing consumer awareness of connectivity benefits, are stimulating market growth. However, challenges related to infrastructure costs and fragmented regulatory landscapes may temper the pace of adoption compared to more developed markets. The rising demand for fleet management solutions is a notable driver for the Commercial Vehicle Market in these regions.

Export, Trade Flow & Tariff Impact on the Automotive 5G TCU Market

The Automotive 5G TCU Market is intrinsically linked to global export and trade flows, reflecting the complex, international nature of automotive manufacturing and electronics supply chains. Major trade corridors for 5G TCUs and their critical components primarily run from Asia (especially China, South Korea, Japan) to North America and Europe, and intra-Europe. Leading exporting nations for these advanced communication modules are typically those with strong semiconductor manufacturing bases and established automotive electronics suppliers, such as South Korea, Taiwan, and China. Conversely, major importing nations include Germany, the United States, and Japan, which host large automotive OEM production facilities that integrate these TCUs into new vehicles.

Tariff and non-tariff barriers have exerted a quantifiable impact on the cross-border volume and pricing of 5G TCUs. The US-China trade tensions, for instance, led to the imposition of tariffs on various electronic components, including those critical for TCU manufacturing, driving up costs for automotive OEMs that rely on a global supply chain. This has forced companies to re-evaluate their sourcing strategies, potentially shifting production or component acquisition to avoid tariff implications, thus fragmenting the supply chain and sometimes increasing lead times. Non-tariff barriers, such as complex certification processes and varying national cybersecurity standards for connected devices, also create hurdles for market entry and necessitate customized product development for different regions, impacting trade efficiency. For example, strict data localization laws in certain countries can influence where data associated with 5G TCUs can be processed and stored, affecting the global deployment of connectivity services. The increasing focus on secure supply chains and national security concerns surrounding certain technology providers have further complicated trade dynamics, leading to scrutiny of component origins and potential geopolitical implications for market access.

Supply Chain & Raw Material Dynamics for the Automotive 5G TCU Market

The supply chain for the Automotive 5G TCU Market is characterized by a high degree of complexity and upstream dependencies, making it vulnerable to disruptions and price volatility. Key inputs include advanced semiconductors, such as 5G modem chipsets and microcontrollers, as well as specialized electronic components like GNSS modules, RF transceivers, memory chips, and passive components. The upstream segment of this supply chain is dominated by a few global semiconductor foundries and component manufacturers, creating potential single-source risks. The recent global semiconductor shortage underscored this vulnerability, causing significant production delays and cost increases for automotive OEMs and TCU manufacturers alike. This disruption highlighted the necessity for more resilient and diversified sourcing strategies.

Raw material dynamics play a crucial role, with materials like silicon (for semiconductors), rare earth elements (for specialized magnets in some components), copper (for wiring and PCBs), and precious metals such as palladium and gold (for connectors and circuit boards) being essential. Price volatility for these materials can significantly impact manufacturing costs. For example, the price of silicon, driven by demand from various electronics industries, has seen an upward trend, influencing the cost of 5G modem chipsets. Palladium, used in catalytic converters and certain electronic components, has also experienced substantial price fluctuations, affecting the overall bill of materials. Sourcing risks are amplified by geopolitical tensions, natural disasters, and pandemics, which can disrupt global logistics and material extraction. Efforts to mitigate these risks include multi-sourcing, inventory building, and localization of certain manufacturing processes, though the highly specialized nature of semiconductor fabrication often limits such flexibility. The Automotive Cybersecurity Market's focus on secure hardware also adds a layer of complexity, demanding specific, traceable, and reliable material origins to prevent counterfeiting or tampering at the foundational level.

Automotive 5G TCU Segmentation

1. Component

1.1. Hardware

1.1.1. 5G modem chipsets

1.1.2. GNSS modules

1.1.3. Others

1.2. Software

1.2.1. Embedded OS

1.2.2. Cybersecurity software

1.2.3. Others

1.3. Services

1.3.1. Connectivity services

1.3.2. Cloud integration

1.3.3. Others

2. Vehicle Type

2.1. Passenger Vehicles

2.2. Commercial Vehicles

3. Communication Mode (V2X)

3.1. Vehicle-to-Vehicle (V2V)

3.2. Vehicle-to-Infrastructure (V2I)

3.3. Vehicle-to-Network (V2N)

3.4. Others

4. End User

4.1. Automotive OEMs

4.2. Aftermarket suppliers

Automotive 5G TCU Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Automotive 5G TCU REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 7.6% from 2020-2034

Segmentation

By Component

Hardware

5G modem chipsets

GNSS modules

Others

Software

Embedded OS

Cybersecurity software

Others

Services

Connectivity services

Cloud integration

Others

By Vehicle Type

Passenger Vehicles

Commercial Vehicles

By Communication Mode (V2X)

Vehicle-to-Vehicle (V2V)

Vehicle-to-Infrastructure (V2I)

Vehicle-to-Network (V2N)

Others

By End User

Automotive OEMs

Aftermarket suppliers

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Component

5.1.1. Hardware

5.1.1.1. 5G modem chipsets

5.1.1.2. GNSS modules

5.1.1.3. Others

5.1.2. Software

5.1.2.1. Embedded OS

5.1.2.2. Cybersecurity software

5.1.2.3. Others

5.1.3. Services

5.1.3.1. Connectivity services

5.1.3.2. Cloud integration

5.1.3.3. Others

5.2. Market Analysis, Insights and Forecast - by Vehicle Type

5.2.1. Passenger Vehicles

5.2.2. Commercial Vehicles

5.3. Market Analysis, Insights and Forecast - by Communication Mode (V2X)

5.3.1. Vehicle-to-Vehicle (V2V)

5.3.2. Vehicle-to-Infrastructure (V2I)

5.3.3. Vehicle-to-Network (V2N)

5.3.4. Others

5.4. Market Analysis, Insights and Forecast - by End User

5.4.1. Automotive OEMs

5.4.2. Aftermarket suppliers

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Component

6.1.1. Hardware

6.1.1.1. 5G modem chipsets

6.1.1.2. GNSS modules

6.1.1.3. Others

6.1.2. Software

6.1.2.1. Embedded OS

6.1.2.2. Cybersecurity software

6.1.2.3. Others

6.1.3. Services

6.1.3.1. Connectivity services

6.1.3.2. Cloud integration

6.1.3.3. Others

6.2. Market Analysis, Insights and Forecast - by Vehicle Type

6.2.1. Passenger Vehicles

6.2.2. Commercial Vehicles

6.3. Market Analysis, Insights and Forecast - by Communication Mode (V2X)

6.3.1. Vehicle-to-Vehicle (V2V)

6.3.2. Vehicle-to-Infrastructure (V2I)

6.3.3. Vehicle-to-Network (V2N)

6.3.4. Others

6.4. Market Analysis, Insights and Forecast - by End User

6.4.1. Automotive OEMs

6.4.2. Aftermarket suppliers

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Component

7.1.1. Hardware

7.1.1.1. 5G modem chipsets

7.1.1.2. GNSS modules

7.1.1.3. Others

7.1.2. Software

7.1.2.1. Embedded OS

7.1.2.2. Cybersecurity software

7.1.2.3. Others

7.1.3. Services

7.1.3.1. Connectivity services

7.1.3.2. Cloud integration

7.1.3.3. Others

7.2. Market Analysis, Insights and Forecast - by Vehicle Type

7.2.1. Passenger Vehicles

7.2.2. Commercial Vehicles

7.3. Market Analysis, Insights and Forecast - by Communication Mode (V2X)

7.3.1. Vehicle-to-Vehicle (V2V)

7.3.2. Vehicle-to-Infrastructure (V2I)

7.3.3. Vehicle-to-Network (V2N)

7.3.4. Others

7.4. Market Analysis, Insights and Forecast - by End User

7.4.1. Automotive OEMs

7.4.2. Aftermarket suppliers

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Component

8.1.1. Hardware

8.1.1.1. 5G modem chipsets

8.1.1.2. GNSS modules

8.1.1.3. Others

8.1.2. Software

8.1.2.1. Embedded OS

8.1.2.2. Cybersecurity software

8.1.2.3. Others

8.1.3. Services

8.1.3.1. Connectivity services

8.1.3.2. Cloud integration

8.1.3.3. Others

8.2. Market Analysis, Insights and Forecast - by Vehicle Type

8.2.1. Passenger Vehicles

8.2.2. Commercial Vehicles

8.3. Market Analysis, Insights and Forecast - by Communication Mode (V2X)

8.3.1. Vehicle-to-Vehicle (V2V)

8.3.2. Vehicle-to-Infrastructure (V2I)

8.3.3. Vehicle-to-Network (V2N)

8.3.4. Others

8.4. Market Analysis, Insights and Forecast - by End User

8.4.1. Automotive OEMs

8.4.2. Aftermarket suppliers

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Component

9.1.1. Hardware

9.1.1.1. 5G modem chipsets

9.1.1.2. GNSS modules

9.1.1.3. Others

9.1.2. Software

9.1.2.1. Embedded OS

9.1.2.2. Cybersecurity software

9.1.2.3. Others

9.1.3. Services

9.1.3.1. Connectivity services

9.1.3.2. Cloud integration

9.1.3.3. Others

9.2. Market Analysis, Insights and Forecast - by Vehicle Type

9.2.1. Passenger Vehicles

9.2.2. Commercial Vehicles

9.3. Market Analysis, Insights and Forecast - by Communication Mode (V2X)

9.3.1. Vehicle-to-Vehicle (V2V)

9.3.2. Vehicle-to-Infrastructure (V2I)

9.3.3. Vehicle-to-Network (V2N)

9.3.4. Others

9.4. Market Analysis, Insights and Forecast - by End User

9.4.1. Automotive OEMs

9.4.2. Aftermarket suppliers

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Component

10.1.1. Hardware

10.1.1.1. 5G modem chipsets

10.1.1.2. GNSS modules

10.1.1.3. Others

10.1.2. Software

10.1.2.1. Embedded OS

10.1.2.2. Cybersecurity software

10.1.2.3. Others

10.1.3. Services

10.1.3.1. Connectivity services

10.1.3.2. Cloud integration

10.1.3.3. Others

10.2. Market Analysis, Insights and Forecast - by Vehicle Type

10.2.1. Passenger Vehicles

10.2.2. Commercial Vehicles

10.3. Market Analysis, Insights and Forecast - by Communication Mode (V2X)

10.3.1. Vehicle-to-Vehicle (V2V)

10.3.2. Vehicle-to-Infrastructure (V2I)

10.3.3. Vehicle-to-Network (V2N)

10.3.4. Others

10.4. Market Analysis, Insights and Forecast - by End User

10.4.1. Automotive OEMs

10.4.2. Aftermarket suppliers

11. Competitive Analysis

11.1. Company Profiles

11.1.1. LG

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. Harman (Samsung)

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Continental

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Bosch

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Marelli

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Visteon

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Valeo

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Ficosa

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Huawei

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Flaircomm Microelectronics

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Marelli (Magneti Marelli)

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Ficosa International SA

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Component 2025 & 2033

Figure 3: Revenue Share (%), by Component 2025 & 2033

Figure 4: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 5: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 6: Revenue (billion), by Communication Mode (V2X) 2025 & 2033

Figure 7: Revenue Share (%), by Communication Mode (V2X) 2025 & 2033

Figure 8: Revenue (billion), by End User 2025 & 2033

Figure 9: Revenue Share (%), by End User 2025 & 2033

Figure 10: Revenue (billion), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (billion), by Component 2025 & 2033

Figure 13: Revenue Share (%), by Component 2025 & 2033

Figure 14: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 15: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 16: Revenue (billion), by Communication Mode (V2X) 2025 & 2033

Figure 17: Revenue Share (%), by Communication Mode (V2X) 2025 & 2033

Figure 18: Revenue (billion), by End User 2025 & 2033

Figure 19: Revenue Share (%), by End User 2025 & 2033

Figure 20: Revenue (billion), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (billion), by Component 2025 & 2033

Figure 23: Revenue Share (%), by Component 2025 & 2033

Figure 24: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 25: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 26: Revenue (billion), by Communication Mode (V2X) 2025 & 2033

Figure 27: Revenue Share (%), by Communication Mode (V2X) 2025 & 2033

Figure 28: Revenue (billion), by End User 2025 & 2033

Figure 29: Revenue Share (%), by End User 2025 & 2033

Figure 30: Revenue (billion), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (billion), by Component 2025 & 2033

Figure 33: Revenue Share (%), by Component 2025 & 2033

Figure 34: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 35: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 36: Revenue (billion), by Communication Mode (V2X) 2025 & 2033

Figure 37: Revenue Share (%), by Communication Mode (V2X) 2025 & 2033

Figure 38: Revenue (billion), by End User 2025 & 2033

Figure 39: Revenue Share (%), by End User 2025 & 2033

Figure 40: Revenue (billion), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (billion), by Component 2025 & 2033

Figure 43: Revenue Share (%), by Component 2025 & 2033

Figure 44: Revenue (billion), by Vehicle Type 2025 & 2033

Figure 45: Revenue Share (%), by Vehicle Type 2025 & 2033

Figure 46: Revenue (billion), by Communication Mode (V2X) 2025 & 2033

Figure 47: Revenue Share (%), by Communication Mode (V2X) 2025 & 2033

Figure 48: Revenue (billion), by End User 2025 & 2033

Figure 49: Revenue Share (%), by End User 2025 & 2033

Figure 50: Revenue (billion), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Component 2020 & 2033

Table 2: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 3: Revenue billion Forecast, by Communication Mode (V2X) 2020 & 2033

Table 4: Revenue billion Forecast, by End User 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Revenue billion Forecast, by Component 2020 & 2033

Table 7: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 8: Revenue billion Forecast, by Communication Mode (V2X) 2020 & 2033

Table 9: Revenue billion Forecast, by End User 2020 & 2033

Table 10: Revenue billion Forecast, by Country 2020 & 2033

Table 11: Revenue (billion) Forecast, by Application 2020 & 2033

Table 12: Revenue (billion) Forecast, by Application 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue billion Forecast, by Component 2020 & 2033

Table 15: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 16: Revenue billion Forecast, by Communication Mode (V2X) 2020 & 2033

Table 17: Revenue billion Forecast, by End User 2020 & 2033

Table 18: Revenue billion Forecast, by Country 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Revenue (billion) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Revenue billion Forecast, by Component 2020 & 2033

Table 23: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 24: Revenue billion Forecast, by Communication Mode (V2X) 2020 & 2033

Table 25: Revenue billion Forecast, by End User 2020 & 2033

Table 26: Revenue billion Forecast, by Country 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue (billion) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Revenue (billion) Forecast, by Application 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue billion Forecast, by Component 2020 & 2033

Table 37: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 38: Revenue billion Forecast, by Communication Mode (V2X) 2020 & 2033

Table 39: Revenue billion Forecast, by End User 2020 & 2033

Table 40: Revenue billion Forecast, by Country 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue (billion) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Revenue (billion) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue billion Forecast, by Component 2020 & 2033

Table 48: Revenue billion Forecast, by Vehicle Type 2020 & 2033

Table 49: Revenue billion Forecast, by Communication Mode (V2X) 2020 & 2033

Table 50: Revenue billion Forecast, by End User 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

The foundation of our "Automotive 5G TCU Market" report is built upon a robust primary research methodology, accounting for approximately 75% of our overall research effort. This extensive approach ensures the capture of nuanced market dynamics, emerging trends, and proprietary insights directly from industry stakeholders. Our primary research encompasses in-depth, semi-structured interviews conducted globally with key opinion leaders, decision-makers, and technical experts across the automotive 5G TCU value chain. This qualitative and quantitative data collection process is designed to validate secondary findings, obtain market estimates, and understand unquantifiable market sentiments.

Key stakeholders interviewed include:

VP of Connected Car/Infotainment Systems (at Automotive OEMs)

Head of Product Management, Telematics & Connectivity (at Tier 1 Automotive Suppliers)

Director of Automotive Business Development (at Semiconductor & Software Firms)

Chief Technology Officer (CTO) or Head of IoT Solutions (at Telecommunication Service Providers)

Our research panel comprises participants from various critical company types within the market:

Automotive OEMs (e.g., Volkswagen, General Motors, Toyota)

Tier 1 Automotive Suppliers (specializing in TCUs, telematics, and connectivity solutions)

Complementing our extensive primary research, secondary research constitutes approximately 25% of our methodology. This phase involves a rigorous review and analysis of existing market data, technical publications, corporate filings, and industry reports to establish a comprehensive market landscape. Our objective is to build a strong foundational understanding, identify market size and segmentation, and corroborate primary research findings. We exclusively leverage reputable and reliable sources to ensure the highest quality of information.

Key secondary data sources include:

Financial Databases: Bloomberg, Factiva, Hoovers, PitchBook for company financials, investment trends, and strategic developments.

Government & Regulatory Data: Publications from .gov domains such as national transportation agencies, economic statistics bureaus, and telecommunications regulators.

Organizational & Trade Association Data: Reports, whitepapers, and statistical data from recognized industry associations and non-profit organizations. We specifically avoid data from other market research websites to maintain originality and prevent data recycling.

Relevant industry associations and regulatory bodies include:

Our market size estimation and forecasting employ a robust combination of top-down and bottom-up methodologies, enhanced by multi-level data triangulation. The bottom-up approach involves aggregating granular data points to build the overall market size, while the top-down approach validates these figures by disaggregating total market estimates based on various parameters. Data triangulation ensures consistency and accuracy by cross-referencing information from multiple primary and secondary sources.

For bottom-up market sizing, key metrics and variables considered include:

Estimated 5G-enabled vehicle production volume (segmented by passenger and commercial vehicles).

Average Selling Price (ASP) of 5G TCUs, broken down by component (hardware, software, services).

Penetration rate of 5G TCUs in new vehicle production and the aftermarket.

Regional adoption rates and regulatory mandates pertaining to V2X communication.

Forecasts for the period 2026-2034 are developed using advanced statistical modeling techniques, incorporating factors such as technological advancements, regulatory changes, economic indicators, and consumer adoption patterns across all identified market segments and regions.

Data Accuracy & Quality Check

We are committed to delivering highly reliable market intelligence, targeting an estimated data accuracy level of 85-90%. This commitment is upheld through a stringent, multi-stage data validation and quality check process. All collected data, both primary and secondary, undergoes rigorous cross-referencing and verification. Our internal subject matter experts conduct peer reviews, and an independent panel of industry specialists provides final validation, ensuring that the insights presented are robust and reflective of current market realities.

Furthermore, to provide the most current market perspective, every report is continuously updated up to the date of purchase, integrating the latest market developments, company announcements, and technological advancements to ensure our clients receive the most relevant and actionable intelligence.

Frequently Asked Questions

1. How has the Automotive 5G TCU market evolved post-pandemic?

The Automotive 5G TCU market shows sustained growth, projected at a 7.6% CAGR through 2033. This indicates strong structural shifts towards enhanced vehicle connectivity and advanced communication systems, driving long-term market expansion.

2. What recent developments influence the Automotive 5G TCU market?

Recent market focus involves advancements in 5G modem chipsets and cybersecurity software integration. Key players like Continental and Bosch are continuously enhancing their TCU offerings to support V2X communication modes across vehicle types.

3. Which companies lead the Automotive 5G TCU market?

Major players like Continental, Bosch, LG, Harman (Samsung), and Huawei hold significant positions in the Automotive 5G TCU market. These firms compete across hardware, software, and connectivity service segments for OEMs and aftermarket suppliers.

4. What disruptive technologies are impacting Automotive 5G TCU functionality?

The evolution of V2X communication modes, including Vehicle-to-Vehicle (V2V) and Vehicle-to-Infrastructure (V2I), significantly impacts TCU functionality. Continued advancements in GNSS modules and embedded OS software also drive innovation, enhancing connectivity features.

5. How do pricing trends affect the Automotive 5G TCU market?

Pricing dynamics in the Automotive 5G TCU market reflect evolving hardware costs, particularly for 5G modem chipsets and GNSS modules. Increasing software complexity for embedded OS and cybersecurity also influences the overall cost structure for OEMs and aftermarket suppliers.

6. What sustainability factors are relevant for Automotive 5G TCUs?

Sustainability in Automotive 5G TCUs relates to enabling efficient vehicle operation and smart infrastructure through V2X communication. This connectivity contributes to optimized traffic flow and reduced fuel consumption, indirectly supporting environmental goals through intelligent transportation systems.