Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Automated Boarding Pass Control: Market Trends, Growth & Outlook to 2033

Automated Boarding Pass Control

Automated Boarding Pass Control: Market Trends, Growth & Outlook to 2033

Automated Boarding Pass Control by Type of Control (Fully Automated Boarding Pass Control, Semi-Automated Boarding Pass Control, Manual Boarding Pass Control), by Solution Type (Hardware, Software, Services), by Deployment Mode (On-Premise, Cloud-based), by End User (Airports, Airlines, Government & Aviation Authorities, Airport Security Agencies), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 107

Key Insights into the Automated Boarding Pass Control Market

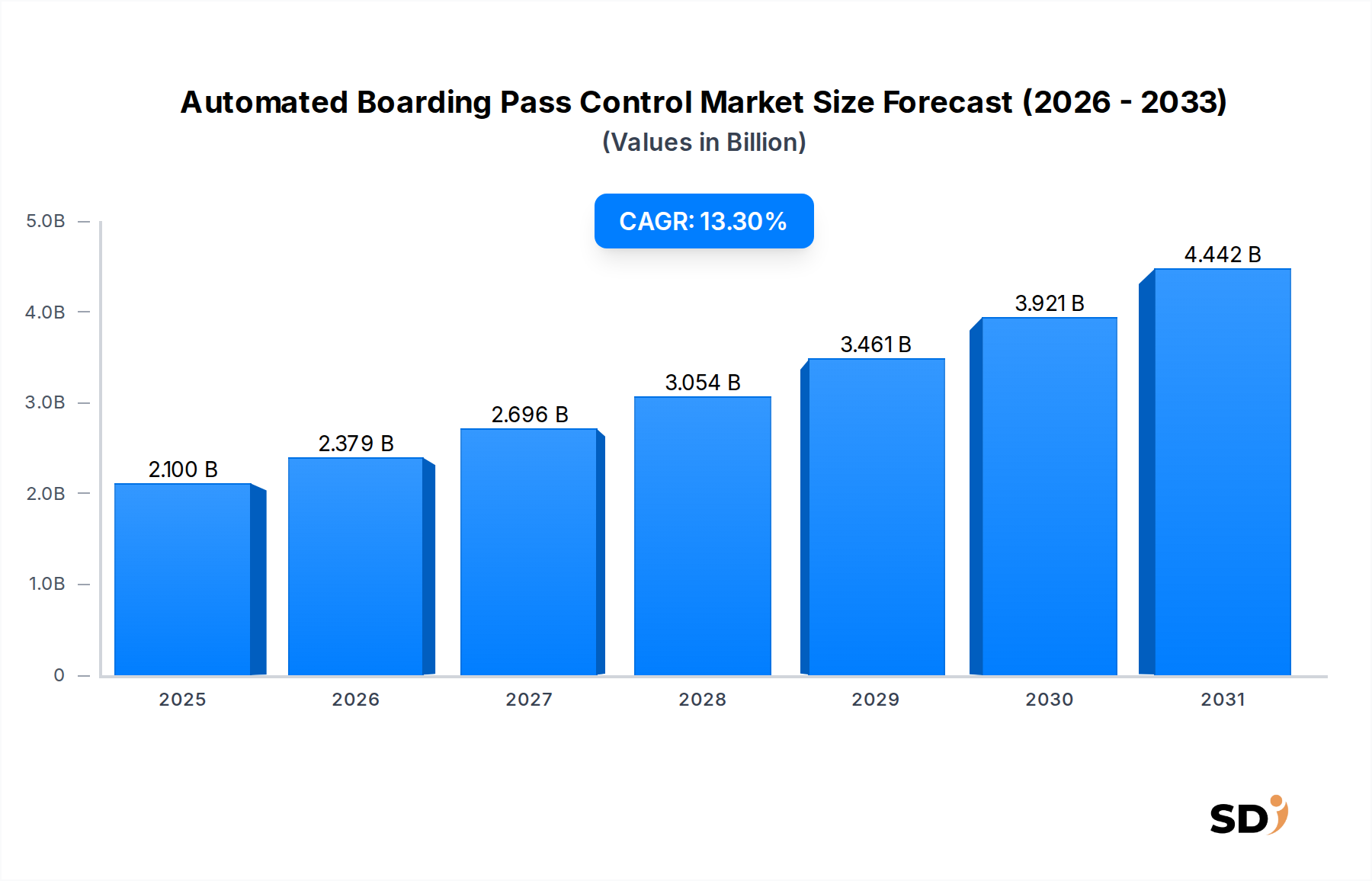

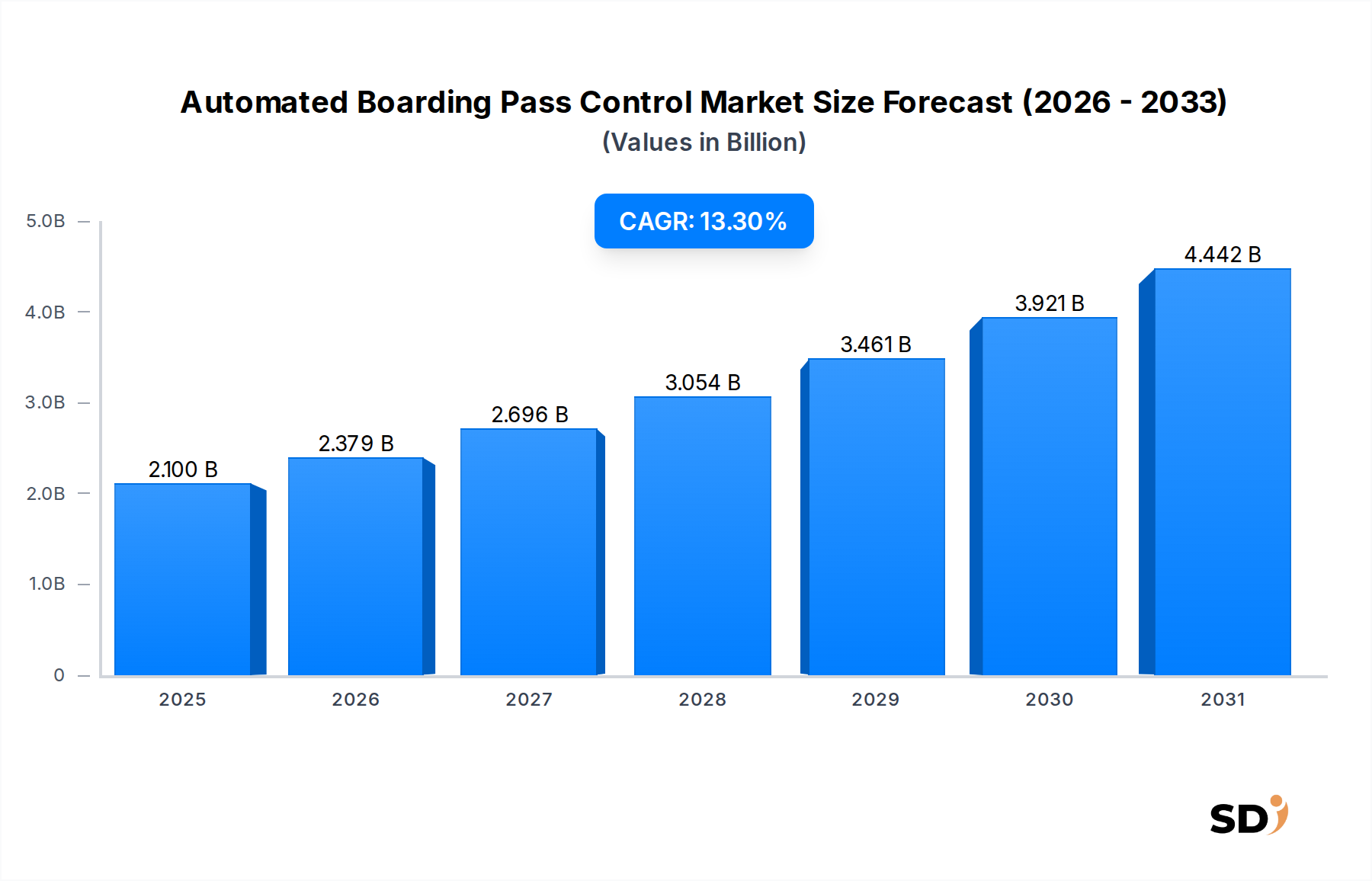

The Automated Boarding Pass Control Market is experiencing robust expansion, driven by the imperative for enhanced airport operational efficiency, stringent security protocols, and an elevated passenger experience. Valued at an estimated $2.1 billion in 2023, the market is projected to grow at a compelling Compound Annual Growth Rate (CAGR) of 13.3% from 2023 to 2034. This trajectory suggests a market valuation reaching approximately $8.59 billion by 2034, underlining significant investment and technological adoption in the aviation sector. Key demand drivers include surging global air passenger volumes, necessitating faster and more seamless boarding processes, and a heightened focus on contactless solutions post-pandemic. Airports and airlines are increasingly investing in sophisticated hardware and software solutions to streamline security checks and gate operations, thereby reducing wait times and improving throughput.

Automated Boarding Pass Control Market Size (In Billion)

5.0B

4.0B

3.0B

2.0B

1.0B

0

2.100 B

2025

2.379 B

2026

2.696 B

2027

3.054 B

2028

3.461 B

2029

3.921 B

2030

4.442 B

2031

The macro tailwinds supporting this growth are multifaceted, encompassing accelerated digitalization initiatives across the travel industry, increasing integration of advanced biometrics for identity verification, and a global trend towards smart airport infrastructure. The development of the Automated Access Control Systems Market is intrinsically linked to the expansion of automated boarding pass control, as the underlying technologies for secure entry and exit points are shared. Furthermore, the burgeoning Biometric Identification Systems Market plays a pivotal role, offering enhanced security and convenience through technologies like facial recognition and fingerprint scanning, which are increasingly deployed at boarding gates. This market’s growth is also influenced by broader trends within the Intelligent Transportation Systems Market, where automation and smart solutions are paramount for optimizing passenger flow and connectivity. The need for precise and rapid passenger verification at critical junctures positions automated boarding pass control as a cornerstone technology for modern aviation security and efficiency paradigms. As airports evolve into smart hubs, the integration of these control systems into a wider digital ecosystem becomes crucial, driving continued innovation and investment.

Dominant End-User Segment: Airports in the Automated Boarding Pass Control Market

Within the multifaceted Automated Boarding Pass Control Market, the 'Airports' segment stands out as the predominant end-user, commanding the largest share of revenue and driving substantial investment. This dominance is attributable to airports being the primary implementation sites for automated boarding pass control systems. As central hubs for air travel, airports bear the direct responsibility for passenger processing, security, and operational efficiency. Their imperative to manage ever-increasing passenger volumes, minimize queue times, and comply with evolving security mandates directly translates into significant capital expenditure on these advanced systems. The integration of fully automated or semi-automated boarding pass control solutions enables airports to enhance throughput, reallocate staff to more complex security tasks, and elevate the overall passenger journey, from check-in to aircraft boarding.

Major players like Kaba Gallenschuetz, IER Blue Solutions, Gunnebo, and Boon Edam are key solution providers focusing on this segment, offering robust hardware and software platforms tailored to the demanding environment of airport operations. These systems are integral to the broader Smart City Infrastructure Market, with airports often serving as early adopters of advanced technologies that subsequently influence wider urban planning. The revenue share from airports is expected to remain dominant as continuous upgrades, expansions, and new airport constructions globally fuel demand. The trend towards self-service and contactless travel, largely propelled by health and safety concerns, further solidifies airports' position as the primary consumers of these systems. Furthermore, the growing sophistication of the Computer Vision Technology Market directly benefits automated boarding pass control, enabling more accurate and faster processing of boarding documents and passenger identities. Investments by airports extend beyond initial procurement to include ongoing software upgrades, maintenance services, and the integration of new functionalities such as biometric identification, ensuring sustained revenue streams for solution providers. The push for seamless and secure passenger journeys continues to reinforce the Airports segment's commanding position in the Automated Boarding Pass Control Market, with substantial room for future growth as technological advancements further refine these critical operational tools.

Key Market Drivers and Constraints in the Automated Boarding Pass Control Market

Several critical factors are shaping the growth trajectory and presenting challenges within the Automated Boarding Pass Control Market. A primary driver is the accelerating global air passenger traffic, which has consistently outpaced airport infrastructure development in many regions. For instance, the International Air Transport Association (IATA) projects passenger numbers could reach 7.8 billion by 2036, demanding more efficient processing capabilities to prevent congestion. This necessitates the deployment of automated systems capable of processing passengers rapidly without compromising security. Another significant driver is the increasing focus on enhancing aviation security. Regulatory bodies worldwide are continuously updating security mandates, prompting airports and airlines to invest in advanced solutions, including biometric verification, as a core component of the Digital Identity Verification Market. Automated boarding pass controls integrate these biometric systems, offering a more reliable and less error-prone method of identity confirmation compared to manual checks.

The demand for a seamless and contactless passenger experience, particularly amplified by global health crises, also acts as a strong market driver. Passengers increasingly expect minimal human interaction and faster transit times through airports, driving the adoption of self-service technologies. The push for operational efficiency and cost reduction by airlines and airport authorities is another key impetus. By automating the boarding process, airports can optimize staff deployment, reduce operational overheads, and improve resource utilization. This directly contributes to the expansion of the IoT in Transportation Market, as these systems often rely on networked sensors and data analytics for optimal performance. The integration of advanced Embedded Systems Market components further enhances the reliability and processing speed of these gates.

Conversely, the Automated Boarding Pass Control Market faces significant constraints. The high initial capital expenditure required for deploying these sophisticated systems is a major barrier, especially for smaller airports or those with limited budgets. A complex challenge involves the integration of new automated systems with existing legacy infrastructure. Many airports operate on aging IT systems, making seamless integration a costly and time-consuming endeavor. Furthermore, privacy concerns surrounding the collection and storage of biometric data represent a substantial constraint. Compliance with stringent data protection regulations, such as GDPR, requires robust security frameworks and transparent data handling practices, which can add complexity and cost to implementations. The fragmented regulatory landscape across different countries and regions also presents challenges, as systems must be adaptable to varying security standards and legal frameworks.

Competitive Ecosystem of Automated Boarding Pass Control Market

The Automated Boarding Pass Control Market features a competitive landscape comprising established aviation technology providers and specialized security solution manufacturers. These companies continually innovate to offer advanced hardware and software solutions that address the evolving needs for speed, security, and passenger experience at airports globally:

Kaba Gallenschuetz: A prominent player known for its comprehensive range of physical access systems, including automated boarding gates and turnstiles, integrated with advanced authentication technologies for enhanced airport security and passenger flow.

IER Blue Solutions: Specializes in self-service solutions for airports, providing a wide array of automated boarding gates, kiosks, and baggage drop systems designed to streamline passenger processing and improve operational efficiency.

Gunnebo: Offers secure entrance solutions, including speed gates and turnstiles, which are adaptable for airport environments to manage access control and automate boarding processes, focusing on high security and throughput.

Boon Edam: A global leader in entry solutions, providing revolving doors, speed gates, and automated security access points that contribute to efficient and secure passenger movement within airport terminals.

Magnetic Autocontrol: Manufactures barriers and access control systems, with offerings applicable to airport environments for regulating vehicle and pedestrian traffic, including solutions for automated boarding pass control areas.

Materna ips: Focuses on integrated passenger services, delivering self-bag drop, check-in, and automated boarding solutions that leverage software and hardware to create a seamless digital journey for travelers.

Emaratech: A technology and management consulting company, often involved in large-scale government and aviation projects, providing biometric and automated solutions for border control and passenger processing, including boarding.

Wanzl: Known for its airport equipment, including baggage trolleys and check-in counters, also offers solutions for passenger guidance and access control, contributing to efficient and organized boarding procedures.

Recent Developments & Milestones in the Automated Boarding Pass Control Market

Recent advancements and strategic initiatives continue to shape the Automated Boarding Pass Control Market, driving innovation and expanding its global footprint. These developments reflect a concerted effort by industry players and aviation authorities to enhance operational efficiency, security, and passenger convenience:

February 2024: A major European airport group announced the successful completion of a pilot program integrating advanced facial recognition technology into its fully automated boarding gates, significantly reducing boarding times for international flights. This highlights the growing reliance on the Biometric Identification Systems Market for seamless travel.

November 2023: A leading provider of airport technology unveiled its next-generation automated boarding gate, featuring enhanced Computer Vision Technology Market capabilities for faster document verification and improved fraud detection at multiple airports in North America, demonstrating continuous product evolution.

September 2023: Several Middle Eastern airlines partnered to standardize protocols for biometric-enabled self-boarding, aiming to create a more consistent and efficient passenger experience across their networks and streamline operations within the Automated Access Control Systems Market.

June 2023: An Asia-Pacific hub airport initiated a large-scale deployment of new automated boarding pass control systems across all its terminals, part of a broader Smart City Infrastructure Market initiative to digitalize and enhance urban connectivity.

March 2023: A collaborative effort between a global airline alliance and a technology firm resulted in the launch of a new software platform designed to integrate automated boarding pass data with flight operations systems, leveraging insights from the IoT in Transportation Market for predictive analytics.

January 2023: North American aviation authorities released updated guidelines for the implementation of automated boarding pass control systems, emphasizing data privacy and cybersecurity standards for biometric data, impacting future deployments of the Digital Identity Verification Market.

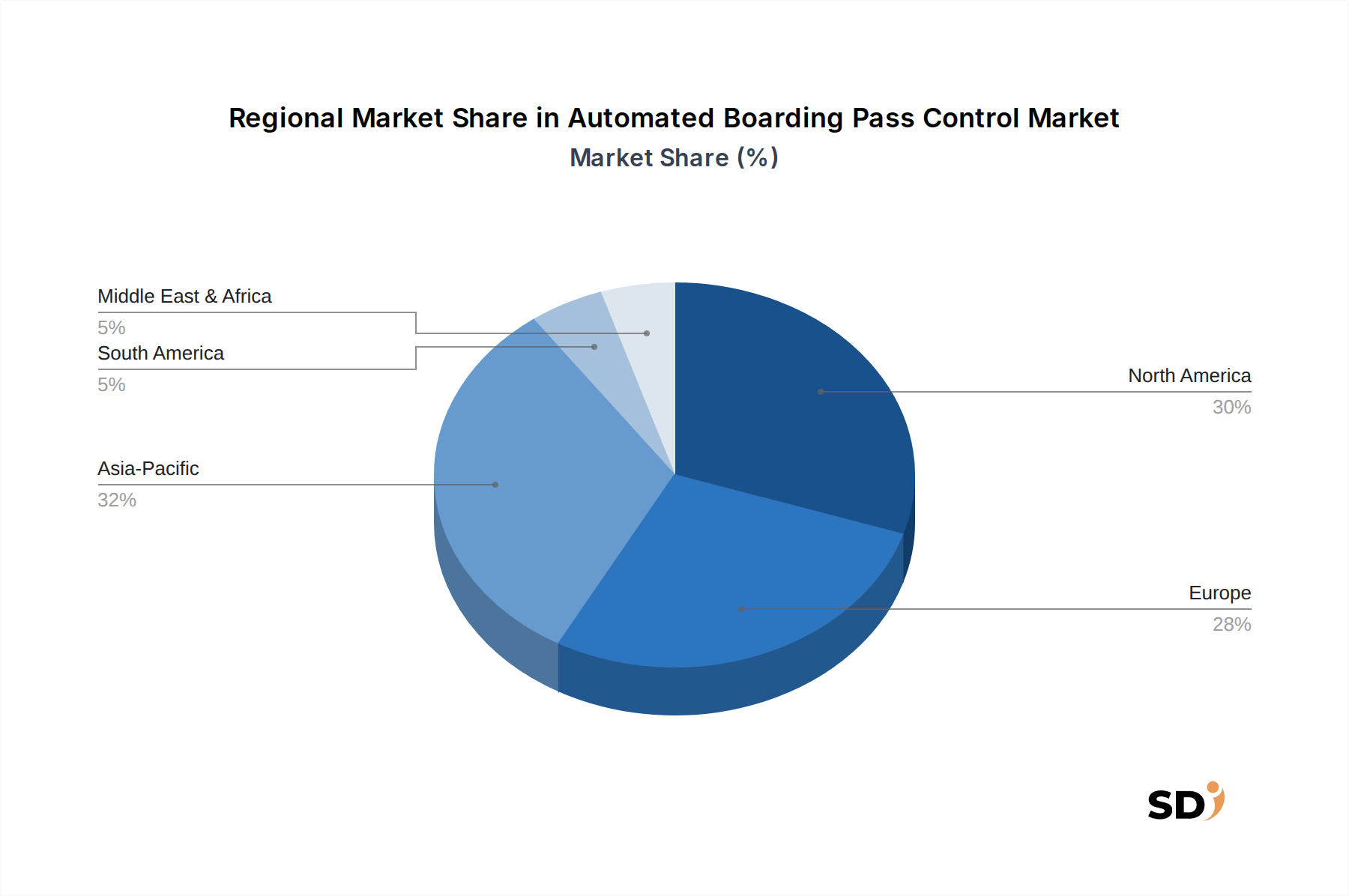

Regional Market Breakdown for Automated Boarding Pass Control Market

Geographic analysis reveals diverse adoption rates and growth trajectories for the Automated Boarding Pass Control Market across various regions. North America and Europe represent mature markets, characterized by high adoption rates and a strong emphasis on upgrading existing infrastructure. In these regions, the primary demand driver is the continuous push for operational efficiency and the integration of advanced biometric technologies to enhance security and streamline passenger flow. Countries like the United States and the United Kingdom have seen early and significant investments in automated solutions, often driven by strict security mandates and high passenger volumes.

Asia Pacific emerges as the fastest-growing region in the Automated Boarding Pass Control Market. This rapid expansion is fueled by extensive new airport construction projects, significant upgrades to existing facilities, and a booming increase in air travel demand, particularly in countries such as China and India. Governments and airport authorities in this region are proactively investing in modern, automated systems to cope with unprecedented passenger growth and establish themselves as global aviation hubs. The demand here is largely driven by capacity expansion and the desire to adopt cutting-edge technology from the outset. This robust growth further underpins the global Intelligent Transportation Systems Market expansion, as airports often serve as critical nodes.

The Middle East & Africa region is also demonstrating substantial growth, albeit from a smaller base. Countries within the GCC (Gulf Cooperation Council) are making significant investments in aviation infrastructure, transforming their airports into major international transit points. The focus here is on prestige, efficiency, and providing a premium passenger experience through advanced technologies, including highly automated boarding pass controls. South America, while showing steady progress, is still in earlier stages of adoption compared to other regions. Growth is more gradual, with demand primarily stemming from efforts to modernize existing airports and improve passenger processing capabilities in key countries like Brazil and Argentina. Each region's unique blend of regulatory environment, passenger volume dynamics, and economic development dictates the specific pace and nature of Automated Boarding Pass Control Market penetration, reflecting varied strategic priorities in global aviation. The integration of advanced Embedded Systems Market and Computer Vision Technology Market components varies by regional investment capacity and regulatory frameworks, further influencing deployment patterns.

Technology Innovation Trajectory in the Automated Boarding Pass Control Market

The technological innovation trajectory in the Automated Boarding Pass Control Market is primarily characterized by the pervasive adoption of advanced biometrics, the integration of IoT ecosystems, and the leveraging of Artificial Intelligence (AI) and Machine Learning (ML). These disruptive technologies are profoundly reshaping how passengers interact with airport infrastructure, promising unprecedented levels of security, efficiency, and personalization.

1. Advanced Biometric Authentication (e.g., Facial Recognition): Facial recognition technology is at the forefront of innovation. Its non-contact nature, speed, and accuracy make it ideal for high-throughput environments like airport boarding gates. R&D investments are significant, focusing on improving accuracy across diverse demographics, enhancing liveness detection to thwart fraud, and ensuring seamless integration with existing airport systems. Adoption timelines are accelerating, with major international airports already implementing "curb-to-gate" biometric journeys. This technology threatens incumbent manual verification processes by offering superior speed and security, simultaneously reinforcing business models that prioritize passenger experience and operational fluidity. The expansion of the Biometric Identification Systems Market is a direct consequence.

2. Internet of Things (IoT) Integration: The application of IoT in the Automated Boarding Pass Control Market enables real-time monitoring, predictive maintenance, and data-driven operational insights. Smart sensors embedded in boarding gates can track passenger flow, detect anomalies, and even trigger alerts for maintenance. R&D is focused on creating a unified, interconnected airport ecosystem where boarding pass control systems communicate seamlessly with check-in kiosks, security checkpoints, and baggage handling systems. Adoption is ongoing, with airports progressively linking disparate systems to create a more cohesive operational picture. IoT reinforces incumbent business models by optimizing resource allocation and enhancing the reliability of automated systems, as seen in the growth of the IoT in Transportation Market.

3. AI and Machine Learning for Predictive Analytics and Anomaly Detection: AI and ML algorithms are being deployed to analyze vast datasets generated by automated boarding pass systems. These capabilities allow for predictive analytics concerning passenger flow, enabling airports to proactively allocate resources or open additional gates to prevent bottlenecks. Moreover, AI-powered anomaly detection can identify suspicious patterns in boarding pass usage or passenger behavior that might indicate fraudulent activity, significantly bolstering security. Investment in this area is growing rapidly, with a focus on developing sophisticated algorithms that learn from continuous data streams. While still nascent in broad deployment, AI and ML are poised to fundamentally transform operational decision-making, offering a significant competitive edge to airports and airlines that embrace them. This strengthens capabilities within the Computer Vision Technology Market and enhances the overall intelligence of automated access points.

Regulatory & Policy Landscape Shaping the Automated Boarding Pass Control Market

The Automated Boarding Pass Control Market operates within a complex web of international and national regulatory frameworks, standards, and policies designed to ensure security, safety, and passenger rights. These guidelines significantly influence technology adoption, system design, and market growth across different geographies.

Globally, the International Civil Aviation Organization (ICAO) sets foundational standards and recommended practices (SARPs) for aviation security, border control, and machine-readable travel documents. These ICAO standards provide a baseline for interoperability and security features that automated boarding pass control systems must adhere to, particularly concerning the validation of travel documents and identity. The International Air Transport Association (IATA) also plays a crucial role through initiatives like 'Fast Travel' and 'One ID', which advocate for seamless, self-service passenger journeys, including automated boarding. These initiatives often drive airlines and airports to invest in compliant and future-proof automated solutions, influencing the expansion of the Digital Identity Verification Market.

At the national level, regulatory bodies such as the Transportation Security Administration (TSA) in the United States and the European Union Aviation Safety Agency (EASA) in Europe issue specific directives and requirements for airport security. Recent policy changes often focus on leveraging advanced technologies like biometrics to enhance security screening processes while maintaining efficiency. For example, directives encouraging contactless travel methods have accelerated the deployment of biometric-enabled automated gates. However, these policies are often coupled with stringent data privacy regulations, such as the General Data Protection Regulation (GDPR) in Europe, which significantly impacts the design and implementation of systems handling personal and biometric data. Compliance with these regulations necessitates robust data encryption, secure storage, and clear consent mechanisms, which can add complexity and cost to solution providers in the Biometric Identification Systems Market.

Furthermore, the increasing integration of automated boarding pass control systems into broader airport and Smart City Infrastructure Market initiatives means that urban planning and data governance policies can also indirectly shape market development. Governments are increasingly looking for interconnected, intelligent transportation systems, and automated boarding controls are a key component of this vision. The harmonization of standards for automated access control systems across international borders remains a continuous challenge but is critical for ensuring a truly seamless global travel experience, driving the need for flexible and adaptable technological solutions.

Automated Boarding Pass Control Segmentation

1. Type of Control

1.1. Fully Automated Boarding Pass Control

1.2. Semi-Automated Boarding Pass Control

1.3. Manual Boarding Pass Control

2. Solution Type

2.1. Hardware

2.2. Software

2.3. Services

3. Deployment Mode

3.1. On-Premise

3.2. Cloud-based

4. End User

4.1. Airports

4.2. Airlines

4.3. Government & Aviation Authorities

4.4. Airport Security Agencies

Automated Boarding Pass Control Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Automated Boarding Pass Control REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 13.3% from 2020-2034

Segmentation

By Type of Control

Fully Automated Boarding Pass Control

Semi-Automated Boarding Pass Control

Manual Boarding Pass Control

By Solution Type

Hardware

Software

Services

By Deployment Mode

On-Premise

Cloud-based

By End User

Airports

Airlines

Government & Aviation Authorities

Airport Security Agencies

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Type of Control

5.1.1. Fully Automated Boarding Pass Control

5.1.2. Semi-Automated Boarding Pass Control

5.1.3. Manual Boarding Pass Control

5.2. Market Analysis, Insights and Forecast - by Solution Type

5.2.1. Hardware

5.2.2. Software

5.2.3. Services

5.3. Market Analysis, Insights and Forecast - by Deployment Mode

5.3.1. On-Premise

5.3.2. Cloud-based

5.4. Market Analysis, Insights and Forecast - by End User

5.4.1. Airports

5.4.2. Airlines

5.4.3. Government & Aviation Authorities

5.4.4. Airport Security Agencies

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Type of Control

6.1.1. Fully Automated Boarding Pass Control

6.1.2. Semi-Automated Boarding Pass Control

6.1.3. Manual Boarding Pass Control

6.2. Market Analysis, Insights and Forecast - by Solution Type

6.2.1. Hardware

6.2.2. Software

6.2.3. Services

6.3. Market Analysis, Insights and Forecast - by Deployment Mode

6.3.1. On-Premise

6.3.2. Cloud-based

6.4. Market Analysis, Insights and Forecast - by End User

6.4.1. Airports

6.4.2. Airlines

6.4.3. Government & Aviation Authorities

6.4.4. Airport Security Agencies

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Type of Control

7.1.1. Fully Automated Boarding Pass Control

7.1.2. Semi-Automated Boarding Pass Control

7.1.3. Manual Boarding Pass Control

7.2. Market Analysis, Insights and Forecast - by Solution Type

7.2.1. Hardware

7.2.2. Software

7.2.3. Services

7.3. Market Analysis, Insights and Forecast - by Deployment Mode

7.3.1. On-Premise

7.3.2. Cloud-based

7.4. Market Analysis, Insights and Forecast - by End User

7.4.1. Airports

7.4.2. Airlines

7.4.3. Government & Aviation Authorities

7.4.4. Airport Security Agencies

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Type of Control

8.1.1. Fully Automated Boarding Pass Control

8.1.2. Semi-Automated Boarding Pass Control

8.1.3. Manual Boarding Pass Control

8.2. Market Analysis, Insights and Forecast - by Solution Type

8.2.1. Hardware

8.2.2. Software

8.2.3. Services

8.3. Market Analysis, Insights and Forecast - by Deployment Mode

8.3.1. On-Premise

8.3.2. Cloud-based

8.4. Market Analysis, Insights and Forecast - by End User

8.4.1. Airports

8.4.2. Airlines

8.4.3. Government & Aviation Authorities

8.4.4. Airport Security Agencies

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Type of Control

9.1.1. Fully Automated Boarding Pass Control

9.1.2. Semi-Automated Boarding Pass Control

9.1.3. Manual Boarding Pass Control

9.2. Market Analysis, Insights and Forecast - by Solution Type

9.2.1. Hardware

9.2.2. Software

9.2.3. Services

9.3. Market Analysis, Insights and Forecast - by Deployment Mode

9.3.1. On-Premise

9.3.2. Cloud-based

9.4. Market Analysis, Insights and Forecast - by End User

9.4.1. Airports

9.4.2. Airlines

9.4.3. Government & Aviation Authorities

9.4.4. Airport Security Agencies

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Type of Control

10.1.1. Fully Automated Boarding Pass Control

10.1.2. Semi-Automated Boarding Pass Control

10.1.3. Manual Boarding Pass Control

10.2. Market Analysis, Insights and Forecast - by Solution Type

10.2.1. Hardware

10.2.2. Software

10.2.3. Services

10.3. Market Analysis, Insights and Forecast - by Deployment Mode

10.3.1. On-Premise

10.3.2. Cloud-based

10.4. Market Analysis, Insights and Forecast - by End User

10.4.1. Airports

10.4.2. Airlines

10.4.3. Government & Aviation Authorities

10.4.4. Airport Security Agencies

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Kaba Gallenschuetz

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. IER Blue Solutions

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Gunnebo

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Boon Edam

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Magnetic Autocontrol

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Materna ips

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Emaratech

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Wanzl

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Type of Control 2025 & 2033

Figure 4: Volume (K), by Type of Control 2025 & 2033

Figure 5: Revenue Share (%), by Type of Control 2025 & 2033

Figure 6: Volume Share (%), by Type of Control 2025 & 2033

Figure 7: Revenue (billion), by Solution Type 2025 & 2033

Figure 8: Volume (K), by Solution Type 2025 & 2033

Figure 9: Revenue Share (%), by Solution Type 2025 & 2033

Figure 10: Volume Share (%), by Solution Type 2025 & 2033

Figure 11: Revenue (billion), by Deployment Mode 2025 & 2033

Figure 12: Volume (K), by Deployment Mode 2025 & 2033

Table 98: Volume K Forecast, by Deployment Mode 2020 & 2033

Table 99: Revenue billion Forecast, by End User 2020 & 2033

Table 100: Volume K Forecast, by End User 2020 & 2033

Table 101: Revenue billion Forecast, by Country 2020 & 2033

Table 102: Volume K Forecast, by Country 2020 & 2033

Table 103: Revenue (billion) Forecast, by Application 2020 & 2033

Table 104: Volume (K) Forecast, by Application 2020 & 2033

Table 105: Revenue (billion) Forecast, by Application 2020 & 2033

Table 106: Volume (K) Forecast, by Application 2020 & 2033

Table 107: Revenue (billion) Forecast, by Application 2020 & 2033

Table 108: Volume (K) Forecast, by Application 2020 & 2033

Table 109: Revenue (billion) Forecast, by Application 2020 & 2033

Table 110: Volume (K) Forecast, by Application 2020 & 2033

Table 111: Revenue (billion) Forecast, by Application 2020 & 2033

Table 112: Volume (K) Forecast, by Application 2020 & 2033

Table 113: Revenue (billion) Forecast, by Application 2020 & 2033

Table 114: Volume (K) Forecast, by Application 2020 & 2033

Table 115: Revenue (billion) Forecast, by Application 2020 & 2033

Table 116: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our research methodology places a significant emphasis on primary research, dedicating 75% of our total research efforts to direct engagement with industry stakeholders. This approach is crucial for gathering first-hand insights, validating secondary data, and understanding the intricate nuances of the Automated Boarding Pass Control market. We conduct structured, semi-structured, and in-depth interviews across various levels of the value chain to capture diverse perspectives and critical market intelligence.

Key primary research participants include:

Company Types:

Automated Boarding Pass System Manufacturers/Providers (e.g., SITA, Materna IPS, Vision-Box)

Biometric Technology Providers (suppliers to boarding pass control systems)

Key Stakeholders Interviewed:

Head of Airport Operations / VP Airport IT

Chief Information Officer (CIO) / VP Digital Transformation (Airlines)

Director of Security and Facilitation (Government & Aviation Authorities)

Product Manager / Solution Architect (Automated Boarding Pass System Vendors)

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

Head of Airport Operations / VP Airport IT

30%

Chief Information Officer (CIO) / VP Digital Transformation (Airlines)

25%

Director of Security and Facilitation (Government & Aviation Authorities)

20%

Product Manager / Solution Architect (Automated Boarding Pass System Vendors)

25%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Automated Boarding Pass System Manufacturers/Providers

35%

Airport Operators & Management Companies

25%

Airlines

20%

Airport IT Integrators & Consultants

10%

Biometric Technology Providers

10%

Secondary Research & Industry Benchmarking

The remaining 25% of our research leverages extensive secondary sources to establish a robust market baseline, identify key trends, conduct competitive analysis, and validate findings from our primary research. Our secondary research is meticulously curated to ensure data reliability and relevance.

It is imperative to note that our secondary research explicitly excludes data from other market research websites to maintain originality and avoid potential biases. All sourced information is cross-referenced for accuracy, and the report is continuously updated up to the date of purchase, ensuring the most current market view.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies integrate both top-down and bottom-up approaches, further enhanced by multi-level data triangulation. This comprehensive strategy ensures a robust and accurate market estimation for the Automated Boarding Pass Control sector.

Bottom-up Approach: This method involves segment-level analysis, starting from the smallest market units and aggregating them upwards to derive the total market size. Specific metrics and variables employed for this market include:

Number of active automated boarding gates installed globally and regionally.

Average capital expenditure (CapEx) per automated boarding gate (hardware, software, and services components).

Passenger traffic growth rates and projections at major international and regional airports.

New airport infrastructure projects, terminal expansions, and modernization initiatives.

Expected retrofit/upgrade cycles for existing manual or semi-automated systems.

Top-down Approach: This method validates the bottom-up estimates by examining the total addressable market (TAM) from a broader industry perspective, considering global airport investment trends, airline IT spending, and aviation security budgets. It provides a macro-level sanity check for the granular bottom-up figures.

Multi-level Data Triangulation: We combine insights from primary interviews, validated secondary data, and our proprietary internal databases. This rigorous cross-validation process minimizes discrepancies, enhances data reliability, and mitigates potential biases, leading to more precise and defensible market figures across all segments.

Data Accuracy & Quality Check

Our commitment to data integrity ensures an estimated data accuracy level of 85-90%. Every data point, market estimate, and forecast undergoes a rigorous multi-stage validation process. This includes:

Cross-Referencing: All primary and secondary data are meticulously cross-referenced against multiple independent sources.

Expert Panel Reviews: Insights and figures are reviewed by an internal panel of senior analysts and external industry experts to ensure conceptual soundness and practical applicability.

Statistical Analysis: Advanced statistical models are applied to identify trends, extrapolate data, and ensure the reliability of forecasts.

Data Cleansing and Normalization: Raw data is subjected to comprehensive cleansing and normalization processes to eliminate inconsistencies and ensure comparability across different regions and segments.

This iterative and stringent quality assurance process is integral to providing our clients with highly reliable and actionable market intelligence. The final report reflects the most current market dynamics and is updated up to the date of purchase, guaranteeing timely and relevant insights.

Frequently Asked Questions

1. What technological innovations are shaping the Automated Boarding Pass Control market?

Innovations focus on fully automated systems and cloud-based deployments. These advancements enhance processing speed, reduce human intervention, and improve data security for aviation end-users like airports.

2. How does the Automated Boarding Pass Control market address sustainability concerns?

The market contributes to sustainability by reducing paper usage through digital processes. Automated systems also optimize passenger flow, potentially minimizing energy consumption related to terminal operations and wait times.

3. Which companies are key players receiving investment in Automated Boarding Pass Control?

Investment activity focuses on established players like Kaba Gallenschuetz, IER Blue Solutions, and Gunnebo. These firms drive innovation in hardware and software solutions within the $2.1 billion Automated Boarding Pass Control market.

4. What are the key segments and solution types within Automated Boarding Pass Control?

Key segments include Fully Automated and Semi-Automated control systems. Solution types comprise Hardware, Software, and Services, primarily serving end-users such as Airports and Airlines.

5. What notable developments are occurring in Automated Boarding Pass Control solutions?

Developments in Automated Boarding Pass Control focus on integration with wider airport systems to enhance security and passenger experience. Firms like Materna ips and Emaratech are innovating, contributing to the market's 13.3% CAGR.

6. Which region offers the most significant growth opportunities for Automated Boarding Pass Control?

Asia-Pacific presents significant growth opportunities, driven by expanding air travel and new airport construction. The region's projected adoption rates are contributing to the global market's expansion, targeting enhanced efficiency.