Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Aspartame by Product Form (Powder, Granular, Liquid), by Sales Channel (Offline, Online), by End-User Industry (Food Processing Companies, Beverage Manufacturers, Pharmaceutical Companies, Nutraceutical & Supplement Brands, Retail/Consumer, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 112

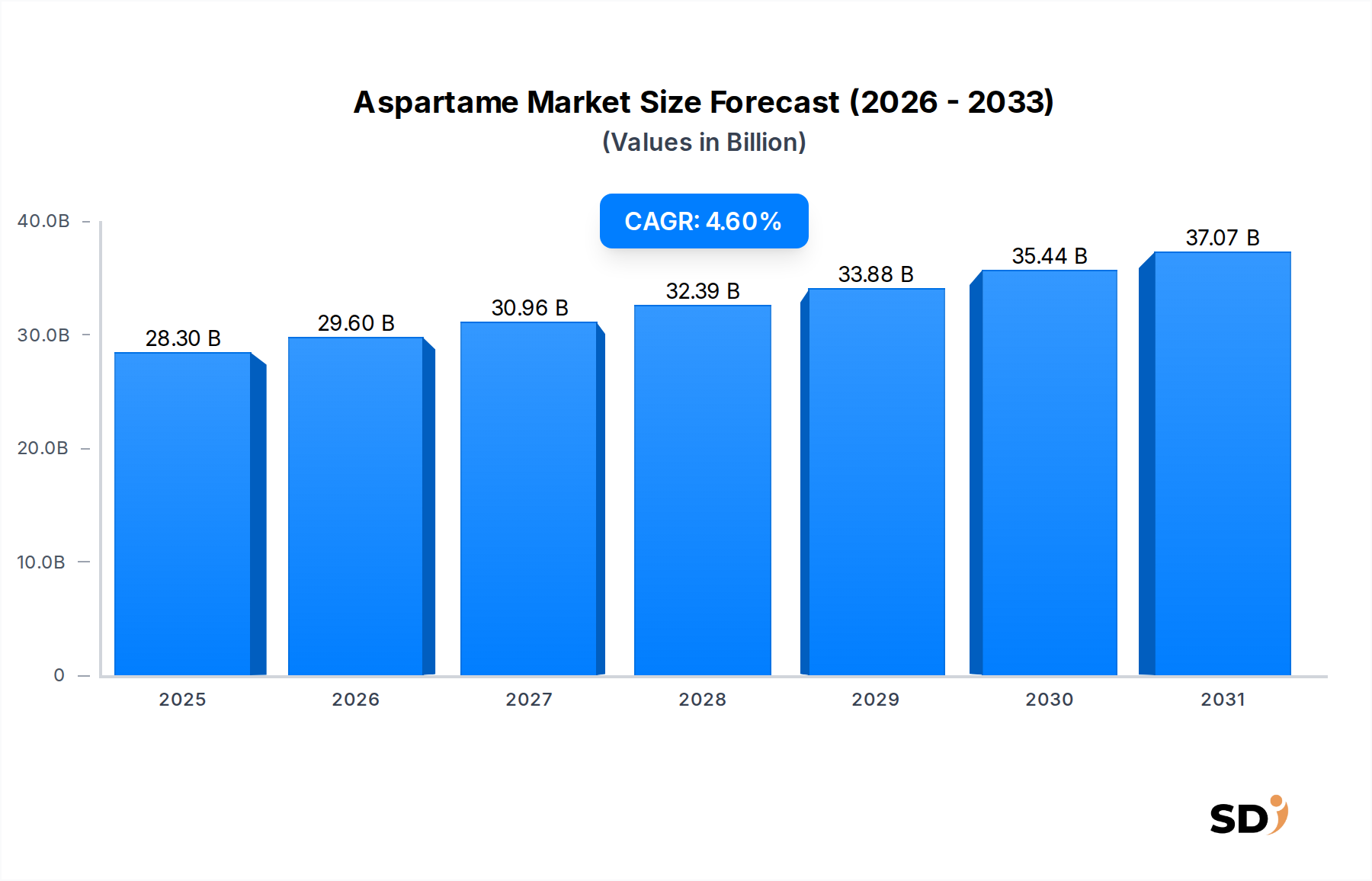

The global Aspartame Market, a crucial segment within the broader Food Additives Market, demonstrated a valuation of approximately $28.3 billion in 2021. Analysts project this market to expand at a Compound Annual Growth Rate (CAGR) of 4.6% through the forecast period, potentially reaching an estimated $42.1 billion by 2030. This robust growth trajectory is underpinned by several key demand drivers and macroeconomic tailwinds. A primary driver is the accelerating global prevalence of chronic lifestyle diseases such as obesity and diabetes, which has significantly amplified consumer preference for low-calorie and sugar-free food and beverage options. Consequently, the demand for high-intensity sweeteners like aspartame has surged, directly impacting the Sugar Substitutes Market and bolstering the Low-Calorie Food Market.

Aspartame Market Size (In Billion)

40.0B

30.0B

20.0B

10.0B

0

28.30 B

2025

29.60 B

2026

30.96 B

2027

32.39 B

2028

33.88 B

2029

35.44 B

2030

37.07 B

2031

Furthermore, the burgeoning health and wellness trend, coupled with increasing disposable incomes in emerging economies, is fueling innovation and product diversification across the food and beverage industry. Manufacturers are actively reformulating products to meet evolving consumer demands for healthier alternatives, thereby integrating aspartame into a wider array of applications, from diet beverages to fortified foods. The rapid expansion of the Nutraceutical Ingredients Market also contributes significantly, as aspartame finds increasing utility in supplements and functional foods designed for health-conscious consumers. Despite facing scrutiny and competition from natural sweeteners, the established efficacy, cost-effectiveness, and widespread regulatory approval of aspartame continue to secure its position as a preferred choice for numerous food and beverage manufacturers. The forward-looking outlook for the Aspartame Market remains positive, driven by continuous advancements in food science and technology, ongoing product innovation, and an expanding application scope, particularly in regions experiencing rapid urbanization and dietary shifts.

End-User Industry Dominance in the Aspartame Market

The Aspartame Market is characterized by a significant concentration of revenue share within specific end-user industries, with "Beverage Manufacturers" emerging as the single largest segment. This dominance stems from the widespread application of aspartame in the production of diet sodas, sugar-free juices, and various other low-calorie beverages. Aspartame's high sweetness intensity, coupled with its relatively clean taste profile compared to other artificial sweeteners, makes it an ideal choice for beverage formulators aiming to reduce sugar content without compromising palatability. The global trend towards healthier lifestyles and the imperative for companies to offer diet-friendly options have solidified this segment's leading position, significantly driving demand within the Beverage Sweeteners Market. Major global beverage corporations are key players within this segment, consistently utilizing aspartame in their extensive product portfolios to cater to an increasingly health-aware consumer base.

While beverage manufacturing holds the largest share, the "Food Processing Companies" segment also represents a substantial portion of the Aspartame Market. This segment encompasses a diverse range of applications, including sugar-free chewing gum, confectionery, dairy products like yogurts, and various baked goods. The versatility of aspartame in providing sweetness without the caloric burden makes it indispensable for these producers. The "Pharmaceutical Companies" segment represents a more niche but critical application, where aspartame is used as an excipient in medications, chewable tablets, and sugar-free syrups, owing to its taste-masking properties and lack of caloric contribution. The "Nutraceutical & Supplement Brands" segment is rapidly expanding, driven by the increasing demand for protein powders, dietary supplements, and functional beverages that require low-calorie or sugar-free formulations, thereby boosting the Nutraceutical Ingredients Market.

While the market share of "Beverage Manufacturers" might experience subtle shifts due to the ongoing innovation in the Artificial Sweeteners Market and the introduction of new natural alternatives, its foundational role in satisfying global demand for diet products is expected to ensure its continued dominance. Consolidation within this segment is more likely to occur among ingredient suppliers rather than a significant decline in the segment's overall volume demand for aspartame. The growing emphasis on reducing added sugars globally, often influenced by public health initiatives and consumer preferences, continues to underscore the strategic importance of aspartame for these key end-user industries.

Key Market Drivers and Constraints in the Aspartame Market

The Aspartame Market's trajectory is primarily shaped by a confluence of powerful drivers and inherent constraints.

Market Drivers:

Global Health Crises (Obesity & Diabetes Epidemic): The escalating global prevalence of obesity and type 2 diabetes is a paramount driver. According to the World Health Organization (WHO), global obesity has nearly tripled since 1975, leading to widespread public health campaigns advocating for reduced sugar intake. This societal shift directly fuels the demand for sugar substitutes and low-calorie alternatives, driving expansion in the Sugar Substitutes Market and the Low-Calorie Food Market. Aspartame, as an established low-calorie sweetener, directly benefits from this imperative for healthier dietary choices among consumers.

Consumer Health Consciousness & Clean Label Trends: A heightened awareness regarding diet and wellness is steering consumer preferences towards products perceived as healthier. While the "clean label" trend often favors natural ingredients, the consistent drive for calorie and sugar reduction still creates significant opportunities for aspartame, particularly in the Beverage Sweeteners Market. Consumers are actively seeking products that offer sweetness without the caloric burden of sugar, even if they are aware of the "artificial" nature of some ingredients.

Food & Beverage Industry Innovation and Reformulation: The continuous need for product innovation and reformulation by food and beverage manufacturers to meet evolving consumer tastes and regulatory guidelines is a significant growth catalyst. Companies are perpetually exploring ingredient solutions that offer desirable taste profiles, extended shelf life, and cost-effectiveness. Aspartame’s high sweetness intensity (approximately 200 times sweeter than sucrose) means only small quantities are needed, making it an efficient and economically viable option for broad application across various product categories.

Market Constraints:

Intense Regulatory Scrutiny and Safety Concerns: Despite extensive research affirming its safety by regulatory bodies worldwide, aspartame frequently faces public skepticism and negative media attention regarding potential health risks. This ongoing debate, particularly amplified by social media, can deter a segment of consumers and lead manufacturers to explore alternative sweeteners. For instance, some European markets have stricter public perception challenges than others, influencing product development in those regions.

Competition from Alternative Sweeteners: The Aspartame Market is witnessing increasingly fierce competition from both natural and other artificial sweeteners. Natural alternatives like stevia, monk fruit, and erythritol are gaining significant market share, especially among consumers demanding "natural" and "clean label" ingredients, directly impacting the Artificial Sweeteners Market. Additionally, other high-intensity artificial sweeteners like sucralose and saccharin offer different taste profiles and stability characteristics, providing manufacturers with a wider array of choices and potentially fragmenting demand for aspartame.

Taste Profile & Stability Issues: While generally well-regarded, aspartame can exhibit a slight lingering aftertaste for some consumers, which can be a limiting factor in certain applications. Furthermore, aspartame's stability is reduced at high temperatures and over extended periods in liquid solutions, limiting its use in baked goods that undergo prolonged heating or products with very long shelf lives, compelling formulators to consider more stable alternatives in these specific contexts.

Competitive Ecosystem of the Aspartame Market

The Aspartame Market is characterized by a competitive landscape comprising global chemical and food ingredient manufacturers, specialty sweetener producers, and diversified conglomerates. Key players leverage their production capabilities, R&D investments, and distribution networks to maintain market presence.

Ajinomoto Group: A leading global manufacturer, primarily known for its amino acid-based products, including high-quality aspartame. The company focuses on leveraging its biotechnological expertise to produce specialty chemicals and food ingredients, including key components for the Amino Acids Market.

NutraSweet: Historically a significant producer and brand owner of aspartame, known for its strong presence in the consumer and industrial sweetener markets. The company maintains its position through brand recognition and established supply chains.

Cargill Incorporated: A diversified agricultural product and food ingredient giant, Cargill participates in the sweetener market by offering a broad portfolio of ingredients, including various sugar substitutes and food additives.

Foodchem: A prominent Chinese supplier that provides a comprehensive range of food additives and ingredients, including aspartame, to global markets. Its strategic focus is on competitive pricing and extensive product availability within the Food Additives Market.

Daesang: A South Korean conglomerate with a significant presence in food ingredients, bio-products, and consumer foods. Daesang manufactures and supplies various food additives and sweeteners, contributing to the broader food ingredient landscape.

Merisant: Known for its consumer-facing brands like Equal and Canderel, Merisant specializes in tabletop sweeteners. The company focuses on consumer branding and distribution in the retail segment of the Sugar Substitutes Market.

Niutang Chemical: A major Chinese manufacturer of food additives, including a range of high-intensity sweeteners. Niutang is known for its large-scale production capacities and global export capabilities.

Gsweet: A supplier specializing in various sweeteners for the food and beverage industry, often focusing on customized solutions and blends. Gsweet aims to cater to diverse client needs with a flexible product offering.

Hanguang Group: A Chinese chemical enterprise involved in the production of various chemical products, including those used in food additives. The group leverages its chemical manufacturing expertise to serve the ingredient sector.

Vitasweet: A producer of a range of artificial sweeteners and food additives, often catering to industrial clients. Vitasweet emphasizes product quality and consistency in its offerings.

Changmao Biochemical Engineering: A key player in the production of malic acid and other biochemicals, which are essential precursors and ingredients in various food and beverage applications, indirectly supporting the broader sweetener industry.

Huaxing: A Chinese chemical company with diverse product offerings, including ingredients relevant to the food and beverage industry. Huaxing focuses on expanding its market reach through a broad product portfolio.

Shaoxing Marina Biotechnology (Yamei Aspartame): This company specializes specifically in aspartame production, with a notable focus on biotechnology-driven manufacturing processes and strong export capabilities, particularly in the Asian market.

Recent Developments & Milestones in the Aspartame Market

Recent developments in the Aspartame Market have largely centered around regulatory reaffirmations, product innovation, and shifts in supplier strategies.

June 2023: The World Health Organization (WHO)'s cancer agency, IARC, classified aspartame as "possibly carcinogenic to humans," while JECFA (the joint WHO and FAO expert committee on food additives) reaffirmed the acceptable daily intake (ADI). This dual announcement led to extensive industry discussion but a general reaffirmation of safe consumption levels by major global food safety authorities, easing immediate panic among manufacturers in the Beverage Sweeteners Market.

November 2022: Several major food and beverage manufacturers announced product reformulations, either reducing sugar content with a blend of high-intensity sweeteners including aspartame or launching new zero-sugar versions of existing popular products. This trend highlights the ongoing demand for diverse sweetener solutions within the Low-Calorie Food Market.

April 2022: Key aspartame manufacturers, including some listed in the competitive landscape, invested in optimizing their production processes to enhance efficiency and reduce costs. This move aims to maintain aspartame's competitive pricing edge against the rising popularity of natural sweeteners in the Artificial Sweeteners Market.

February 2022: A partnership between a leading nutraceutical brand and an ingredient supplier was announced, focusing on developing new aspartame-fortified protein powders and health supplements. This indicates a growing adoption of aspartame in the rapidly expanding Nutraceutical Ingredients Market.

September 2021: Regional regulatory bodies in Southeast Asia issued updated guidelines for the use of aspartame in food and beverages, aligning with international standards and facilitating easier market access for products containing the sweetener. This is expected to streamline trade for the Food Additives Market in the region.

July 2021: New research studies were published exploring the synergistic effects of aspartame when blended with other sweeteners to achieve optimal taste profiles and reduced aftertastes. These studies aim to enhance the appeal and application versatility of aspartame in complex food matrices, especially for High-Intensity Sweeteners Market applications.

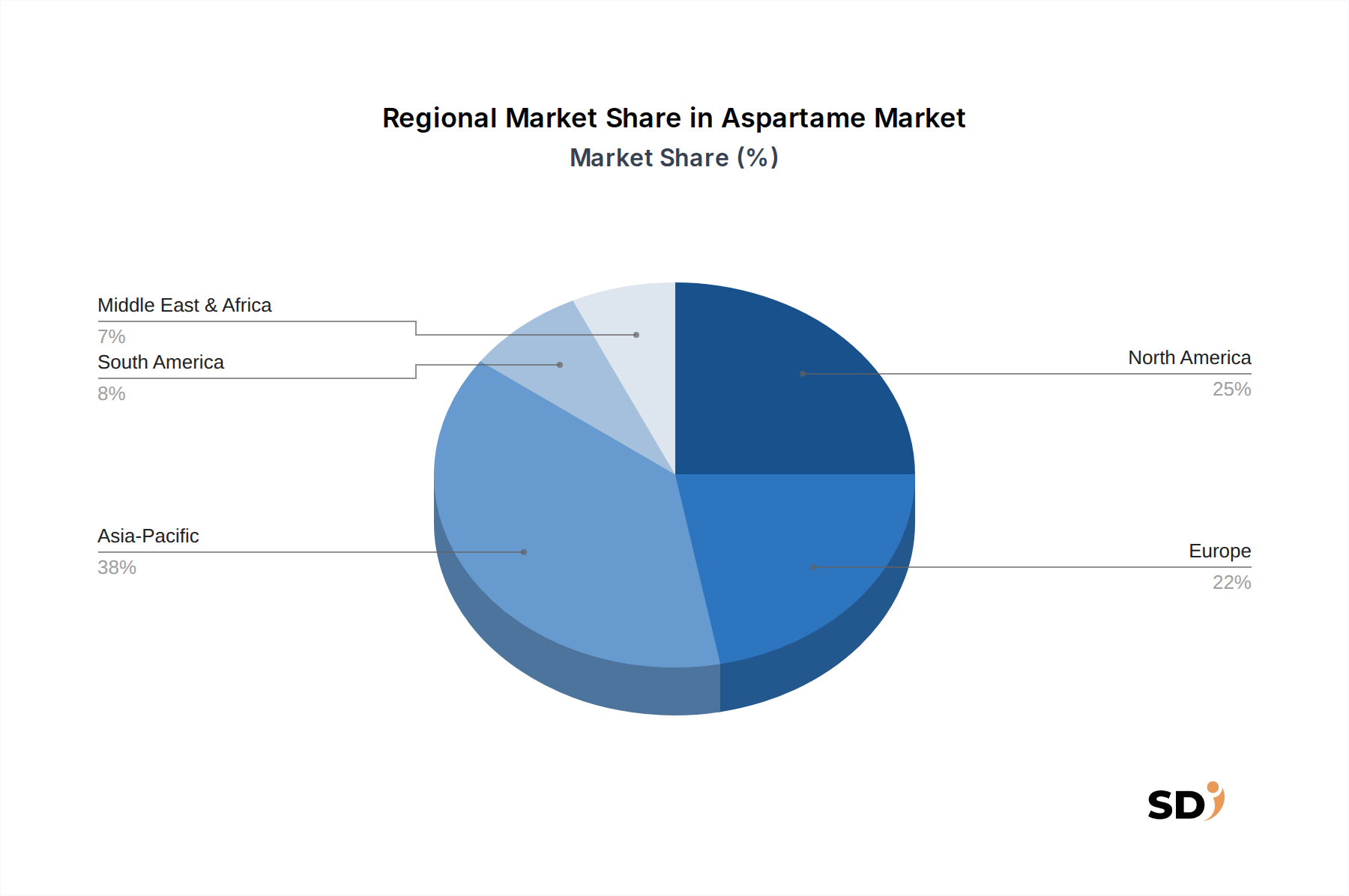

Regional Market Breakdown for the Aspartame Market

Geographic distribution plays a critical role in the dynamics of the Aspartame Market, with distinct consumption patterns and regulatory landscapes influencing regional growth. While specific regional CAGRs are not provided, general trends indicate significant variances across continents.

Asia Pacific is recognized as the fastest-growing region in the Aspartame Market. This acceleration is driven by several factors, including rapid urbanization, a burgeoning middle class, increasing disposable incomes, and the westernization of dietary habits. Countries like China and India, with their massive populations, are witnessing a surge in demand for processed foods, beverages, and functional products. The expanding food and beverage manufacturing sector in these nations, coupled with a growing awareness of health and wellness, significantly boosts the regional consumption of Sugar Substitutes Market products. This region also benefits from being a major production hub, particularly for generic aspartame, contributing to its dominance.

North America represents a mature yet substantial market for aspartame. The primary demand driver in this region is the well-established health consciousness among consumers, leading to high consumption of diet beverages and low-calorie food products. The presence of major food and beverage manufacturers and stringent regulatory frameworks for food additives further solidifies its market position. While growth may be more moderate compared to Asia Pacific, sustained innovation in the Low-Calorie Food Market ensures consistent demand.

Europe is another mature market, characterized by stringent food safety regulations and a strong consumer preference for both health-conscious and "natural" products. Despite the regulatory hurdles and public debate surrounding artificial sweeteners, the continuous demand for sugar reduction in line with public health initiatives drives the Aspartame Market. Countries like Germany, France, and the UK are key consumers, propelled by the need for low-calorie options in their Beverage Sweeteners Market and confectionery sectors.

Latin America and Middle East & Africa are emerging regions exhibiting considerable growth potential. In Latin America, rising disposable incomes, changing lifestyles, and the increasing availability of Western food products are stimulating demand. Similarly, in the Middle East & Africa, growing urbanization and awareness of health issues like diabetes are leading to increased adoption of low-calorie sweeteners. These regions represent significant opportunities for expansion as local food and beverage industries develop and expand their product offerings to include more diet-friendly options.

Export, Trade Flow & Tariff Impact on Aspartame Market

The Aspartame Market's global supply chain is heavily influenced by international trade flows, characterized by a concentration of production in Asia, particularly China, and significant import demand from developed economies. Major trade corridors for aspartame originate from Asian manufacturing hubs, extending primarily to North America and Europe, and increasingly to emerging markets in Latin America and the Middle East.

Leading Exporting Nations: China stands as the undisputed leader in aspartame production and export, leveraging cost-effective manufacturing and substantial production capacities. Other countries, while smaller in scale, also contribute to exports, but China's output dictates global supply and pricing. The availability of key raw materials for the Amino Acids Market in Asia further reinforces this dominance.

Leading Importing Nations: The United States, countries within the European Union (e.g., Germany, UK, France), and Japan are among the top importers. These nations have robust food and beverage industries and high consumer demand for low-calorie and sugar-free products, driving significant volumes of aspartame imports. The Food Additives Market in these regions is highly dependent on international supply.

Tariff and Non-Tariff Barriers:

Tariffs: Historically, anti-dumping duties or import tariffs have been implemented by importing regions (e.g., the EU or US) against specific exporting countries to protect domestic industries or address perceived unfair trade practices. For instance, temporary anti-dumping measures on certain chemical imports from China have been observed, which can influence the cost structure for importers of aspartame, a synthetic organic chemical. While specific aspartame tariffs fluctuate, the general trend for chemical and food ingredient imports can impact overall trade costs. Such duties can increase landed costs by 5-15%, affecting the competitiveness of imported aspartame.

Non-Tariff Barriers: These include strict quality control standards, certification requirements (e.g., HACCP, ISO), and health regulations. European countries, for example, have rigorous food safety and additive approval processes that can act as barriers for producers not meeting specific EU standards. Labeling requirements and origin declarations also contribute to non-tariff barriers, requiring significant compliance efforts from exporters. Changes in food additive lists or maximum permissible levels, even if not directly tariffs, can effectively restrict trade flow. In some cases, consumer preference for domestically sourced ingredients, driven by perceived quality or safety, also acts as a subtle non-tariff barrier, influencing procurement decisions in the Artificial Sweeteners Market.

Customer Segmentation & Buying Behavior in Aspartame Market

The Aspartame Market serves a diverse customer base, each segment exhibiting distinct purchasing criteria, price sensitivities, and procurement channels. Understanding these behaviors is crucial for market participants.

End-User Segments and Purchasing Criteria:

Food Processing Companies: This is a primary segment, purchasing aspartame in bulk for incorporation into a wide array of products (e.g., confectionery, dairy, baked goods). Their primary criteria include cost-effectiveness, consistent quality and purity, supply chain reliability, and compliance with food safety regulations. They often require technical support for formulation and seek sweeteners with predictable functional properties. Price sensitivity is relatively high for this segment, as ingredient costs directly impact their profit margins. This segment is a major contributor to the demand in the Powdered Sweeteners Market.

Beverage Manufacturers: Similar to food processors, beverage companies procure large volumes. Their key criteria are consistent taste profile (especially the lack of an aftertaste), stability in liquid formulations, regulatory approval for beverages, and competitive pricing. Brand reputation and consistent supply are paramount, given the high volumes involved in the Beverage Sweeteners Market. They may also be interested in blends of high-intensity sweeteners to achieve specific taste profiles.

Pharmaceutical Companies: This segment demands the highest levels of purity, regulatory compliance (USP/EP standards), and detailed technical documentation. Aspartame is used as an excipient, sweetener, or taste-masking agent. Price is less sensitive than for food processors, with quality and stringent adherence to pharmacopeial standards being the overriding factors.

Nutraceutical & Supplement Brands: A growing segment, these companies seek aspartame for protein powders, health drinks, and dietary supplements. Their purchasing criteria focus on clean label compatibility (where applicable for sugar-free claims), purity, functional benefits, and suitability for specific dietary claims (e.g., keto-friendly). They are moderately price-sensitive but prioritize ingredients that align with their brand's health and wellness image, significantly influencing the Nutraceutical Ingredients Market.

Retail/Consumer (Tabletop Sweeteners): This segment represents individual consumers purchasing aspartame-based tabletop sweeteners (e.g., Equal, Canderel). Buying behavior here is driven by brand loyalty, convenience, perceived health benefits (low-calorie), and taste preference. Price sensitivity exists but is often secondary to brand trust. These products are typically bought through retail channels like supermarkets and online stores.

Procurement Channels and Shifts in Buyer Preference:

Industrial buyers (food, beverage, pharma, nutraceutical) primarily procure aspartame directly from manufacturers, distributors, or through specialized ingredient brokers. Long-term contracts are common to ensure supply security and stable pricing. The growing trend towards customized blends of sweeteners is notable, as companies seek unique taste solutions and synergistic effects, driving demand in the High-Intensity Sweeteners Market. There's also a discernible shift, particularly among consumer-facing brands, to diversify sweetener portfolios to mitigate risks associated with public perception of single artificial sweeteners and to offer a wider range of "natural" and "artificial" sweetener options. This has led to increased demand for hybrid formulations and a more consultative approach from ingredient suppliers.

Aspartame Segmentation

1. Product Form

1.1. Powder

1.2. Granular

1.3. Liquid

2. Sales Channel

2.1. Offline

2.2. Online

3. End-User Industry

3.1. Food Processing Companies

3.2. Beverage Manufacturers

3.3. Pharmaceutical Companies

3.4. Nutraceutical & Supplement Brands

3.5. Retail/Consumer

3.6. Others

Aspartame Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Aspartame REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 4.6% from 2020-2034

Segmentation

By Product Form

Powder

Granular

Liquid

By Sales Channel

Offline

Online

By End-User Industry

Food Processing Companies

Beverage Manufacturers

Pharmaceutical Companies

Nutraceutical & Supplement Brands

Retail/Consumer

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Form

5.1.1. Powder

5.1.2. Granular

5.1.3. Liquid

5.2. Market Analysis, Insights and Forecast - by Sales Channel

5.2.1. Offline

5.2.2. Online

5.3. Market Analysis, Insights and Forecast - by End-User Industry

5.3.1. Food Processing Companies

5.3.2. Beverage Manufacturers

5.3.3. Pharmaceutical Companies

5.3.4. Nutraceutical & Supplement Brands

5.3.5. Retail/Consumer

5.3.6. Others

5.4. Market Analysis, Insights and Forecast - by Region

5.4.1. North America

5.4.2. South America

5.4.3. Europe

5.4.4. Middle East & Africa

5.4.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Product Form

6.1.1. Powder

6.1.2. Granular

6.1.3. Liquid

6.2. Market Analysis, Insights and Forecast - by Sales Channel

6.2.1. Offline

6.2.2. Online

6.3. Market Analysis, Insights and Forecast - by End-User Industry

6.3.1. Food Processing Companies

6.3.2. Beverage Manufacturers

6.3.3. Pharmaceutical Companies

6.3.4. Nutraceutical & Supplement Brands

6.3.5. Retail/Consumer

6.3.6. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Product Form

7.1.1. Powder

7.1.2. Granular

7.1.3. Liquid

7.2. Market Analysis, Insights and Forecast - by Sales Channel

7.2.1. Offline

7.2.2. Online

7.3. Market Analysis, Insights and Forecast - by End-User Industry

7.3.1. Food Processing Companies

7.3.2. Beverage Manufacturers

7.3.3. Pharmaceutical Companies

7.3.4. Nutraceutical & Supplement Brands

7.3.5. Retail/Consumer

7.3.6. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Product Form

8.1.1. Powder

8.1.2. Granular

8.1.3. Liquid

8.2. Market Analysis, Insights and Forecast - by Sales Channel

8.2.1. Offline

8.2.2. Online

8.3. Market Analysis, Insights and Forecast - by End-User Industry

8.3.1. Food Processing Companies

8.3.2. Beverage Manufacturers

8.3.3. Pharmaceutical Companies

8.3.4. Nutraceutical & Supplement Brands

8.3.5. Retail/Consumer

8.3.6. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Product Form

9.1.1. Powder

9.1.2. Granular

9.1.3. Liquid

9.2. Market Analysis, Insights and Forecast - by Sales Channel

9.2.1. Offline

9.2.2. Online

9.3. Market Analysis, Insights and Forecast - by End-User Industry

9.3.1. Food Processing Companies

9.3.2. Beverage Manufacturers

9.3.3. Pharmaceutical Companies

9.3.4. Nutraceutical & Supplement Brands

9.3.5. Retail/Consumer

9.3.6. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Product Form

10.1.1. Powder

10.1.2. Granular

10.1.3. Liquid

10.2. Market Analysis, Insights and Forecast - by Sales Channel

10.2.1. Offline

10.2.2. Online

10.3. Market Analysis, Insights and Forecast - by End-User Industry

Table 44: Revenue billion Forecast, by End-User Industry 2020 & 2033

Table 45: Revenue billion Forecast, by Country 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Revenue (billion) Forecast, by Application 2020 & 2033

Table 49: Revenue (billion) Forecast, by Application 2020 & 2033

Table 50: Revenue (billion) Forecast, by Application 2020 & 2033

Table 51: Revenue (billion) Forecast, by Application 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology is the cornerstone of our market estimations, contributing approximately 75% of the total research effort. This robust approach involves extensive direct engagement with key stakeholders across the Aspartame value chain. We conduct in-depth, structured interviews with industry experts, thought leaders, and decision-makers to gather first-hand qualitative and quantitative insights. These interviews help validate assumptions, identify emerging trends, understand competitive landscapes, and gauge market dynamics from an operational perspective. Our primary interviews are meticulously designed to cover granular details pertaining to product forms (powder, granular, liquid), sales channels, end-user industry applications, and regional market nuances.

Comprising approximately 25% of our total research, secondary research forms the foundational layer for market understanding and validation. We leverage a multi-faceted approach to gather data from credible and authoritative sources. This includes detailed analysis of annual reports, investor presentations, financial statements, and white papers from public companies. Additionally, we tap into a comprehensive array of governmental publications, trade association data, and scientific journals to ensure a broad and accurate data landscape. Our analysts are trained to avoid market research websites to maintain the integrity and originality of our findings.

Standard Financial Databases & Industry Sources Utilized:

Every report is diligently updated up to the date of purchase, ensuring that our clients receive the most current and relevant market intelligence.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies combine top-down and bottom-up approaches, triangulated with multi-level data points to ensure robustness and accuracy. The top-down approach involves estimating the total market size for aspartame by analyzing macro-economic indicators, overall food & beverage ingredient trends, and regulatory landscapes across regions. This estimation is then broken down into specific product forms, sales channels, and end-user industries.

The bottom-up approach, conversely, focuses on aggregating market data from granular levels. We calculate market size by summing up the consumption and sales of aspartame at the application level, considering penetration rates and average consumption volumes within specific end-user segments. Data triangulation across various primary and secondary sources validates the initial market estimates, reducing potential biases and enhancing the reliability of our projections.

Specific Metrics and Variables Used for Bottom-Up Market Sizing:

Production volumes and capacities of major aspartame manufacturers (in metric tons).

Average aspartame inclusion rates in key end-products (e.g., diet beverages, chewing gum, tabletop sweeteners, pharmaceuticals).

Per capita consumption trends of aspartame-sweetened products in key regional markets.

Average selling price (ASP) per kilogram of aspartame across different product forms (powder, granular, liquid) and regions.

Data Accuracy & Quality Check

We are committed to delivering highly reliable market intelligence. Our stringent data validation process ensures an estimated data accuracy level of 88%. This is achieved through multiple rounds of cross-verification: comparing primary interview insights with secondary data, triangulating findings from different stakeholders, and applying advanced statistical models to identify and correct discrepancies. All raw data undergoes rigorous scrubbing and normalization. Our team of senior analysts performs a final quality assurance check, scrutinizing the coherence of market trends, logical consistency of forecasts, and the robustness of the underlying assumptions before final publication.

Frequently Asked Questions

1. How do Aspartame's export-import dynamics influence global trade?

The global Aspartame market relies on international trade flows for raw material sourcing and product distribution, especially from major producers like China. Trade policies and tariffs can impact supply chain efficiency and product availability across regions.

2. What sustainability and ESG factors impact the Aspartame market?

Producers face scrutiny regarding energy consumption, waste management, and raw material sourcing. Consumer demand for environmentally responsible products increasingly influences brand perception and purchasing decisions in the food and beverage industry.

3. What are the primary challenges and supply chain risks in the Aspartame market?

The market faces challenges from fluctuating raw material prices, regulatory scrutiny over safety, and competition from alternative sweeteners. Geopolitical events and logistics disruptions can also pose significant supply chain risks.

4. How did the COVID-19 pandemic affect the Aspartame market and what are its long-term shifts?

The pandemic initially disrupted supply chains but also accelerated demand for packaged foods and beverages, stabilizing the Aspartame market. Long-term shifts include a heightened focus on health-conscious products and resilient supply networks.

5. What is the impact of the regulatory environment on the Aspartame market?

Aspartame is subject to strict regulatory oversight by bodies like the FDA and EFSA, which dictates its approved uses and dosage limits. Compliance with these regulations is critical for market access and consumer trust, impacting manufacturers like Ajinomoto Group and NutraSweet.

6. Who are the leading companies shaping the competitive landscape of the Aspartame market?

Key players such as Ajinomoto Group, NutraSweet, and Cargill Incorporated dominate the Aspartame market through production capacity and distribution networks. The competitive landscape also includes regional manufacturers like Foodchem and Daesang.