Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Artificial Insemination In Cattle: $3.39B, 7.1% CAGR (2026-2034)

Artificial Insemination In Cattle

Artificial Insemination In Cattle: $3.39B, 7.1% CAGR (2026-2034)

Artificial Insemination In Cattle by Product Type (Semen Straws, Artificial Insemination Guns, Catheters & Sheaths, Semen Storage Tanks, Liquid Nitrogen Containers, Others), by Semen Type (Conventional Semen, Sexed Semen), by Cattle Type (Dairy Cattle, Beef Cattle), by Service Provider (Veterinary Clinics, Cooperative Breeding Centers, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 85

Key Insights into Artificial Insemination In Cattle

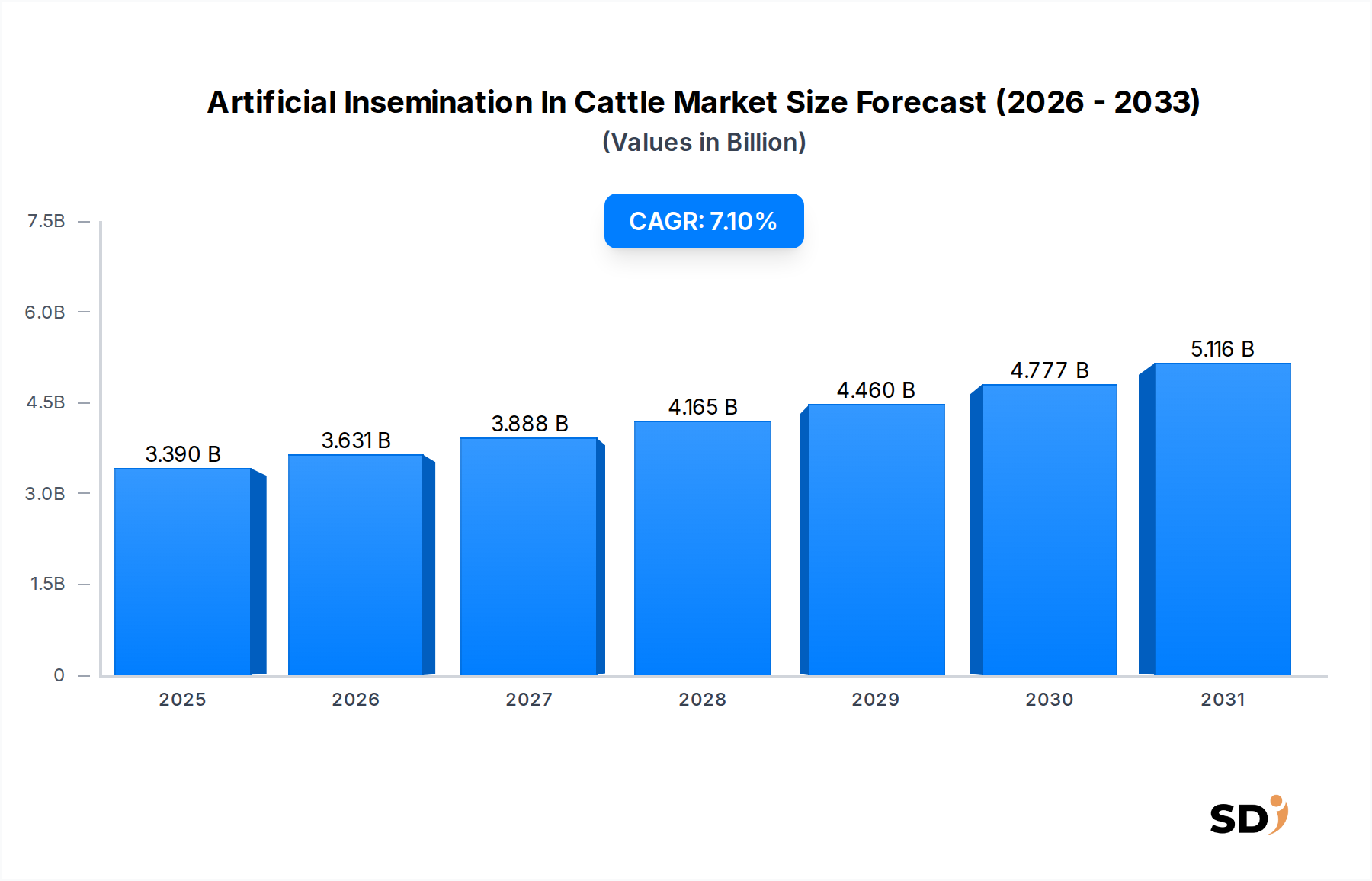

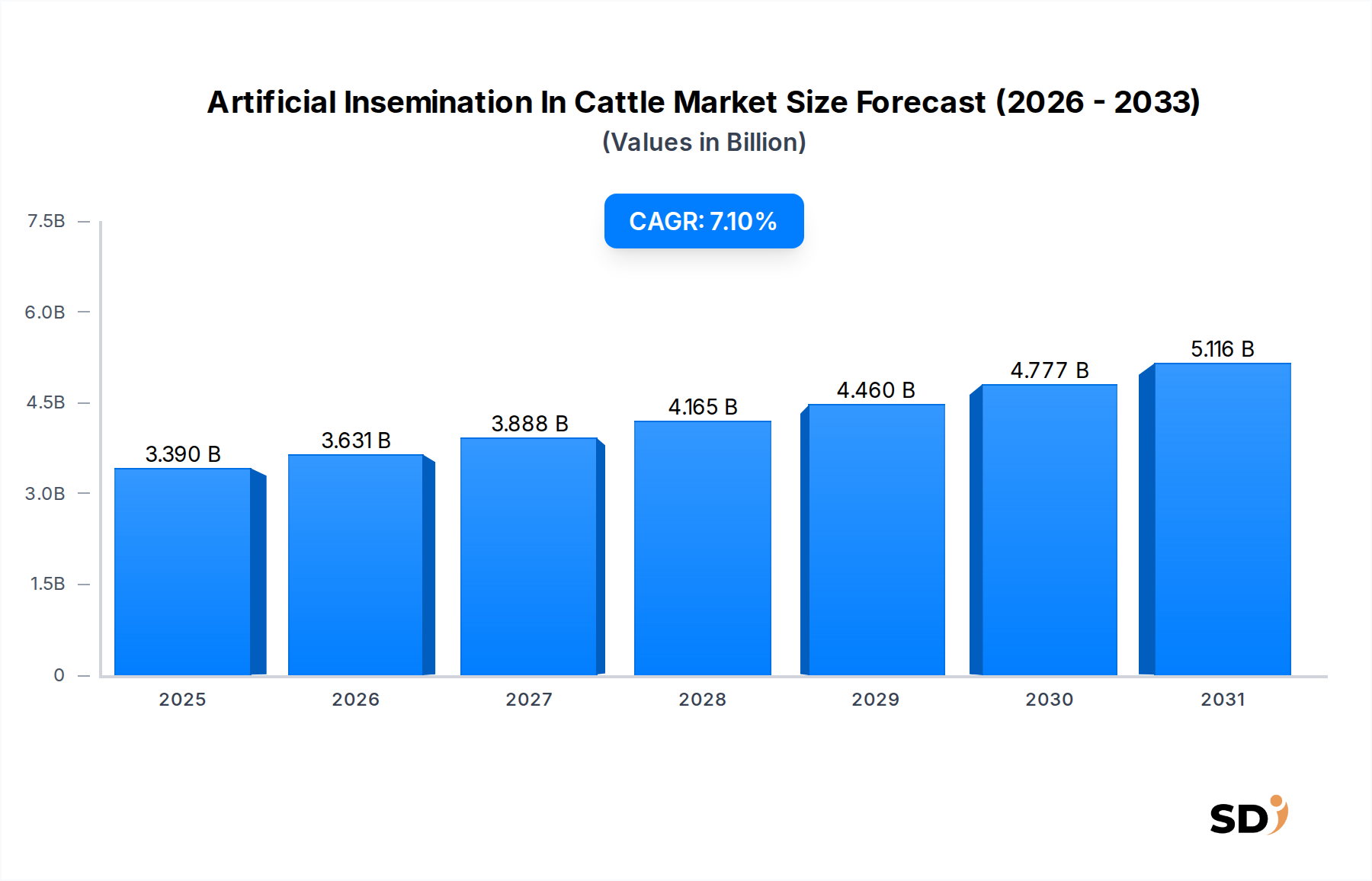

The Artificial Insemination In Cattle Market is currently valued at USD 3.39 billion in 2025 and is projected to expand significantly, reaching an estimated USD 6.27 billion by 2034, demonstrating a robust Compound Annual Growth Rate (CAGR) of 7.1% over the forecast period. This growth trajectory is underpinned by several macro-economic tailwinds and technological advancements poised to redefine livestock reproduction. A primary demand driver is the escalating global demand for high-quality dairy and beef products, necessitating advanced breeding techniques to enhance genetic merit and productivity in cattle herds. Artificial insemination (AI) offers unparalleled advantages in genetic selection, disease control, and herd management efficiency, making it an indispensable tool for modern livestock operations.

Artificial Insemination In Cattle Market Size (In Billion)

7.5B

6.0B

4.5B

3.0B

1.5B

0

3.390 B

2025

3.631 B

2026

3.888 B

2027

4.165 B

2028

4.460 B

2029

4.777 B

2030

5.116 B

2031

The widespread adoption of sexed semen technology has significantly contributed to market expansion, enabling producers to control the gender of offspring, thereby optimizing breeding programs for either milk production in dairy farms or lean meat production in beef operations. This innovation, coupled with advancements in estrus synchronization protocols and reproductive biotechnologies, has lowered operational complexities and improved conception rates. Furthermore, the increasing focus on sustainable livestock farming practices, including reducing the environmental footprint of cattle production through more efficient feed conversion and disease resistance, positions AI as a crucial enabler. The market is also benefiting from favorable government initiatives and subsidies in various regions aimed at supporting livestock farmers and improving indigenous cattle breeds through genetic upgrading programs. The outlook for the Artificial Insemination In Cattle Market remains exceedingly positive, with continuous innovation in semen processing, AI equipment, and integration with digital agriculture platforms driving future growth. Emerging markets, particularly in Asia Pacific and Latin America, are expected to exhibit high adoption rates as their livestock sectors modernize to meet growing domestic and export demands. The strategic alliances between genetic companies and technology providers are anticipated to further accelerate research and development, introducing more precise and user-friendly AI solutions to the global cattle industry.

Dairy Cattle Dominance in Artificial Insemination In Cattle

The Dairy Cattle segment holds a predominant revenue share within the Artificial Insemination In Cattle Market, primarily driven by the intensive genetic selection pressures applied in the dairy industry to optimize milk production, composition, and herd health. Dairy farmers globally prioritize genetic improvement to enhance economically important traits such as milk yield, butterfat and protein content, fertility, mastitis resistance, and longevity. Artificial insemination offers the most efficient and cost-effective method to introduce superior genetics from elite bulls into dairy herds, allowing for rapid genetic progress across generations. The high economic value associated with each dairy animal, coupled with the long production cycle and significant investment in each cow, makes the adoption of advanced reproductive technologies like AI a critical component of successful dairy farming.

The segment's dominance is further reinforced by the sophisticated infrastructure and established breeding programs in major dairy-producing regions like North America, Europe, and Oceania. These regions have a long history of utilizing AI, with cooperative breeding centers and private genetic companies providing a wide array of high-merit dairy genetics. Key players such as Genus plc (through its ABS Global subsidiary), Semex Alliance, and Select Sires Inc. have built extensive genetic catalogs focusing on dairy breeds like Holstein, Jersey, and Brown Swiss, continuously developing and marketing semen from top-ranking sires. The increasing adoption of sexed semen, particularly for dairy heifers, is a significant driver within this segment, allowing dairy producers to ensure a higher percentage of female calves, thus accelerating herd expansion and replacement rates without incurring the costs associated with rearing male calves. While the Beef Cattle Breeding Market is also growing, the intensive management and genetic focus in dairy operations mean that the Dairy Cattle Breeding Market typically commands a larger share of AI-related expenditure. The sophisticated data management and genetic evaluation systems employed in the dairy industry also facilitate better decision-making regarding sire selection and breeding programs, further entrenching AI as a core practice. As global demand for dairy products continues to rise, especially in developing economies, the expansion of the Dairy Cattle Breeding Market through AI is expected to continue its upward trajectory, with continued innovation in genomic selection and reproductive management tools.

Key Market Drivers in Artificial Insemination In Cattle

The Artificial Insemination In Cattle Market is propelled by several robust drivers, each contributing significantly to its expansion and adoption across global livestock industries. A primary driver is the escalating global demand for animal protein, specifically dairy and beef products. According to FAO projections, global meat consumption is expected to increase by nearly 15% by 2030, while dairy consumption is also on an upward trend, particularly in emerging economies. This rising demand necessitates more efficient and productive livestock systems, where AI plays a pivotal role in enhancing genetic potential and output per animal. By enabling selective breeding for traits like higher milk yield, faster growth rates, and improved feed conversion efficiency, AI directly contributes to meeting this growing demand.

Another significant driver is the advancement in genetic improvement and reproductive technologies. Innovations such as genomic selection allow for more accurate and rapid identification of superior breeding animals, shortening the genetic interval and accelerating herd improvement. The increasing availability and affordability of sexed semen have revolutionized breeding strategies, allowing producers to achieve specific herd structures more predictably. For instance, in the Dairy Cattle Breeding Market, sexed semen can result in over 90% female calves, enabling faster expansion and replacement of milking herds. This precision significantly optimizes resource utilization and profitability. Furthermore, the role of AI in disease control and biosecurity is a critical, albeit often overlooked, driver. Unlike natural breeding, AI eliminates direct physical contact between animals, thereby significantly reducing the risk of transmitting infectious diseases such as brucellosis, leptospirosis, and trichomoniasis. This is particularly crucial for large commercial farms and for international trade of genetic material, safeguarding herd health and ensuring compliance with stringent veterinary regulations. The development of advanced Veterinary Equipment Market for semen collection, processing, and storage, including more efficient Liquid Nitrogen Containers Market, also supports the logistical demands of AI programs. Additionally, increasing investments in Precision Livestock Farming Market technologies, which integrate AI with real-time data on animal health and productivity, are further boosting adoption. These systems facilitate precise estrus detection and optimized insemination timing, leading to improved conception rates and overall breeding efficiency. As livestock producers increasingly seek to maximize productivity while minimizing environmental impact, the role of AI as a cornerstone of modern, sustainable livestock management continues to expand.

Competitive Ecosystem of Artificial Insemination In Cattle

The Artificial Insemination In Cattle Market is characterized by a mix of large multinational genetic companies, specialized biotechnology firms, and regional cooperatives. Competition primarily revolves around genetic quality, technological innovation (e.g., sexed semen processing, genomic services), and the breadth of product and service offerings.

Genus plc: A global pioneer in animal genetics, operating through its ABS Global and PIC divisions. The company focuses on developing and marketing high-merit bovine genetics, with significant investments in R&D to enhance traits like milk production, meat quality, and disease resistance.

ABS Global: A subsidiary of Genus plc, it is one of the world's leading providers of bovine genetics, reproductive services, and technologies. ABS Global is known for its extensive sire directory and advancements in Sexed Semen Market production.

STgenetics: A prominent player specializing in sexed semen technology. The company's proprietary sex-sorting technology, SexedULTRA, allows for highly accurate sexing of semen, catering to the growing demand for gender-specific offspring in both dairy and beef operations.

Semex Alliance: A leading global supplier of bovine genetics, owned by Canadian dairy farmers. Semex is recognized for its commitment to research and development, offering innovative genetic solutions and a strong emphasis on herd health and longevity traits.

CRV Holding B.V.: A Dutch-Belgian cooperative focused on cattle improvement. CRV provides genetics, data management, and consulting services to dairy and beef farmers, with a strong emphasis on sustainability and efficiency traits.

URUS Group LP: A holding company with a portfolio of leading dairy and beef genetics businesses, including Alta Genetics, Trans Ova Genetics, and Genex. URUS aims to deliver comprehensive genetic solutions and services to livestock producers worldwide.

Select Sires Inc.: A North American cooperative that provides superior genetics and reproductive programs to dairy and beef producers. Select Sires is known for its farmer-owner structure and focus on delivering profitable genetic solutions.

Alta Genetics Inc.: A subsidiary of URUS Group LP, Alta Genetics is a global leader in dairy cattle genetics. The company is known for its progressive breeding programs and commitment to customer profitability through genetic improvement.

IMV Technologies: A French company specializing in animal reproduction and artificial insemination equipment. IMV Technologies offers a wide range of products including Artificial Insemination Guns Market, semen straws, laboratory equipment, and cryopreservation solutions, serving the global market.

VikingGenetics: A Nordic cattle breeding company owned by dairy farmers in Denmark, Sweden, and Finland. VikingGenetics is renowned for its focus on health and welfare traits, producing robust and efficient dairy cattle genetics.

Cogent Breeding Ltd.: A UK-based cattle breeding company, part of the STgenetics group. Cogent is recognized for its expertise in dairy genetics and its pioneering work in sexed semen technology, serving both domestic and international markets.

Others: This category includes numerous regional cooperatives, smaller genetic companies, and providers of specialized AI equipment and services that collectively contribute to the market's dynamic competitive landscape.

Recent Developments & Milestones in Artificial Insemination In Cattle

The Artificial Insemination In Cattle Market continues to evolve rapidly, driven by technological innovations and strategic collaborations:

May 2024: Genus plc announced a strategic partnership with a leading genomics firm to integrate advanced genomic sequencing data into its sire selection programs. This collaboration aims to accelerate the identification of cattle with superior genetic traits for enhanced productivity and disease resistance, further solidifying the Animal Biotechnology Market's influence.

August 2023: IMV Technologies launched its latest generation of smart Artificial Insemination Guns Market, featuring integrated IoT sensors for real-time data collection on insemination depth, temperature, and semen delivery. This innovation is designed to improve conception rates and provide valuable data for herd management via the Livestock Management Software Market.

February 2023: Regulatory bodies in the European Union finalized updated guidelines for the cross-border trade of bovine semen, streamlining import and export procedures for high-genetic-merit material while maintaining rigorous biosecurity standards. This move is expected to facilitate greater access to elite genetics for European farmers.

November 2022: A rising agri-tech startup, specializing in reproductive management solutions, successfully closed a Series A funding round totaling USD 15 million. The capital infusion is earmarked for scaling its AI-powered estrus detection and breeding optimization platform for both Dairy Cattle Breeding Market and Beef Cattle Breeding Market operations.

July 2022: A consortium of academic researchers and a major semen producer announced a breakthrough in the efficiency of Sexed Semen Market production. The new methodology promises to reduce manufacturing costs by 10-15% and increase the availability of sex-sorted straws, making the technology more accessible to a wider range of cattle farmers globally.

April 2022: Select Sires Inc. initiated a new program to offer extended warranty and maintenance services for Liquid Nitrogen Containers Market used by its customers. This initiative aims to ensure the optimal storage conditions and longevity of genetic material, enhancing reliability for AI programs.

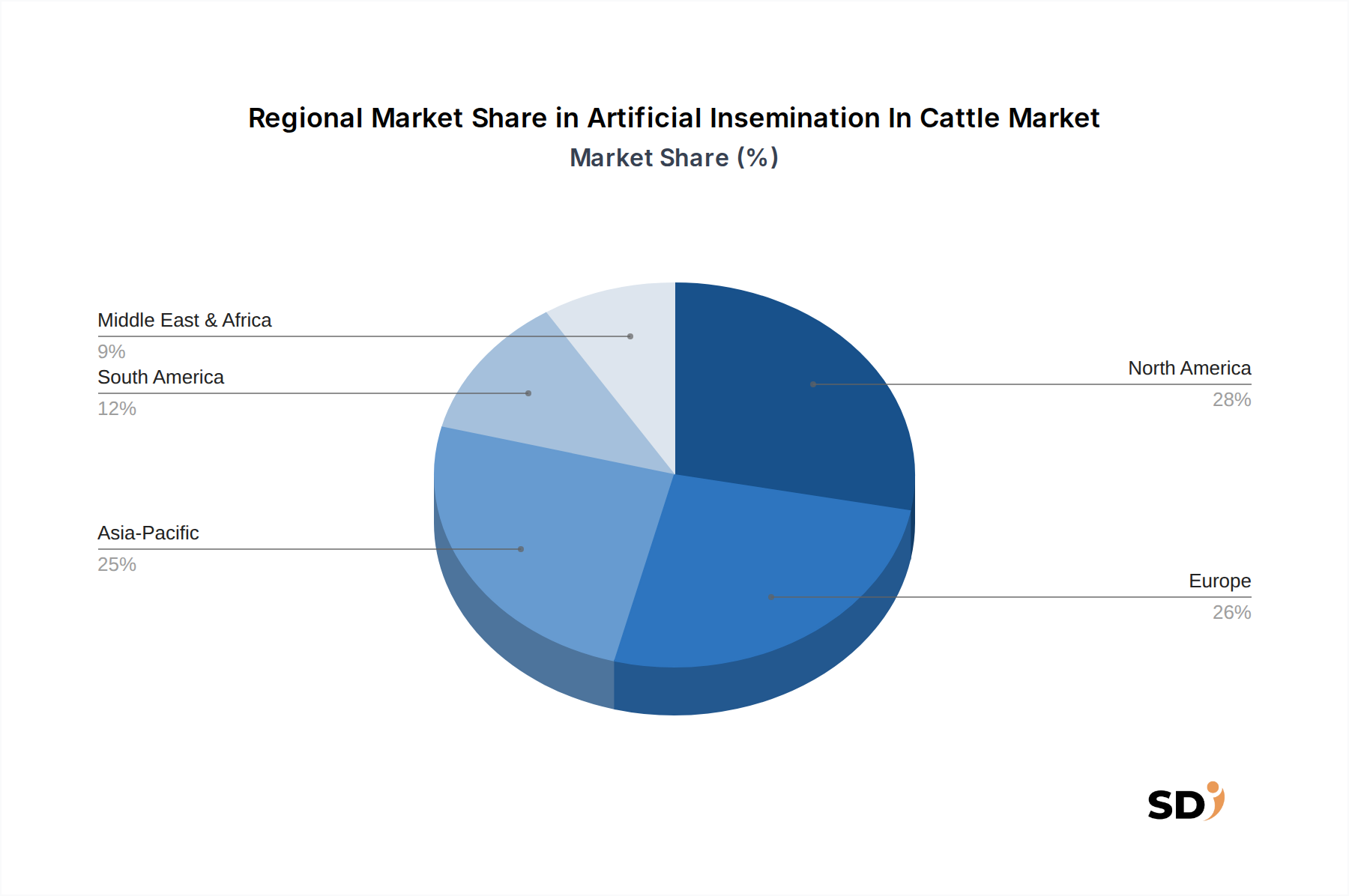

Regional Market Breakdown for Artificial Insemination In Cattle

The global Artificial Insemination In Cattle Market exhibits significant regional variations in terms of adoption rates, market size, and growth drivers. North America, primarily the United States and Canada, holds a substantial market share, characterized by highly developed dairy and beef industries that extensively utilize AI for genetic improvement. The region benefits from advanced research and development in bovine genetics and a strong infrastructure for semen production and distribution. Despite its maturity, the North American market continues to grow, driven by ongoing genetic innovation and the increasing adoption of Sexed Semen Market.

Europe, encompassing countries like the United Kingdom, Germany, France, and the Nordics, represents another major revenue contributor. This region boasts a long history of cooperative breeding organizations and a strong emphasis on animal welfare and sustainable practices. European farmers are keen adopters of genetic technologies to enhance productivity and reduce environmental impact, making it a key market for both conventional and sexed semen. The introduction of new regulations and subsidies supporting genetic improvement programs further stimulates growth in the region.

Asia Pacific is projected to be the fastest-growing region in the Artificial Insemination In Cattle Market, particularly driven by countries like China, India, and ASEAN nations. The region is witnessing a rapid modernization of its livestock sector, fueled by rising disposable incomes, increasing demand for dairy and meat products, and government initiatives aimed at improving indigenous cattle breeds. Large-scale government-backed programs promoting AI adoption, coupled with the establishment of new cooperative breeding centers, are significant growth catalysts. The potential for the Beef Cattle Breeding Market in these countries is enormous.

South America, with Brazil and Argentina as key players, also presents a robust growth outlook. These countries have vast cattle populations and are major global exporters of beef and dairy. The adoption of AI is increasing rapidly as producers seek to improve herd genetics for better meat quality, growth rates, and reproductive efficiency. Investments in local semen production facilities and genetic evaluation programs are key drivers. The Middle East & Africa region, while smaller in market size, is showing nascent growth, primarily driven by GCC countries and South Africa, focusing on enhancing domestic food security and upgrading livestock genetics through international collaborations and technology transfer. Overall, while mature markets like North America and Europe continue to innovate, the high growth potential in Asia Pacific and South America will be instrumental in driving the global Artificial Insemination In Cattle Market forward.

Export, Trade Flow & Tariff Impact on Artificial Insemination In Cattle

The global trade of genetic material, particularly bovine semen straws, is a critical component of the Artificial Insemination In Cattle Market. Major trade corridors primarily connect leading genetic production hubs in North America and Europe with importing nations across Asia Pacific, Latin America, and to a lesser extent, Africa. Countries like the United States, Canada, the Netherlands, and France are prominent exporters, leveraging their advanced Animal Biotechnology Market and sophisticated breeding programs to supply high-merit genetics worldwide. Importing nations, on the other hand, seek to enhance their domestic cattle breeds, improve productivity, and diversify genetic pools. This cross-border flow of genetics is heavily influenced by stringent veterinary regulations and phytosanitary certificates, which act as non-tariff barriers, ensuring the health status and disease-free nature of imported semen.

Recent trade policies and geopolitical shifts have had a measurable impact on cross-border volumes. For instance, increased trade tensions between major economic blocs can lead to more rigorous inspection processes or temporary bans on agricultural imports, including genetic material, causing supply chain disruptions. Health and safety protocols, especially concerning zoonotic diseases, can frequently be updated, requiring exporters to meet evolving standards. The CITES (Convention on International Trade in Endangered Species of Wild Fauna and Flora) agreement also influences trade, although bovine genetics typically fall outside its strictest regulations, related species and specific breeds might encounter unique restrictions. Furthermore, tariffs, while less common on essential agricultural inputs like semen compared to finished goods, can still marginally impact pricing and competitiveness. However, the intrinsic value of superior genetics often outweighs minor tariff increases, particularly for specialized products like the Sexed Semen Market. The overall trend indicates a continued increase in trade volume, driven by the global demand for genetic improvement, but this growth remains highly sensitive to international relations, veterinary health standards, and evolving trade agreements. Investments in robust logistics and cold chain management, including specialized Liquid Nitrogen Containers Market, are crucial for facilitating this intricate global trade.

Investment & Funding Activity in Artificial Insemination In Cattle

Investment and funding activity within the Artificial Insemination In Cattle Market, and the broader animal genetics sector, have seen consistent growth over the past 2-3 years, reflecting the increasing valuation placed on genetic improvement and agricultural technology. Mergers and acquisitions (M&A) have been a strategic tool for consolidation and expansion among major players. Larger genetic companies often acquire smaller, specialized firms to integrate novel technologies, expand geographic reach, or gain access to specific genetic lines. For instance, acquisitions focusing on advancements in Sexed Semen Market technology or genomic sequencing capabilities have been notable, as companies seek to enhance their competitive edge. The integration of data analytics and artificial intelligence into breeding programs has also spurred M&A activity, with traditional genetic providers partnering with or acquiring tech firms.

Venture funding rounds have primarily targeted startups innovating in adjacent technologies that support AI in cattle. Sub-segments attracting significant capital include:

Precision Livestock Farming Market: Startups developing IoT sensors, wearable devices, and AI-powered analytics platforms for estrus detection, health monitoring, and reproductive management have secured substantial seed and Series A funding. These technologies aim to optimize the timing of insemination and improve overall herd fertility.

Animal Biotechnology Market: Companies focused on advanced genetic editing, disease diagnostics, and enhanced semen processing techniques are drawing investor interest. Breakthroughs in gene-editing for disease resistance or improved productivity traits are particularly attractive to venture capitalists.

Livestock Management Software Market: Platforms offering comprehensive herd management solutions, integrating breeding records, health data, and nutritional information, are receiving funding to scale their offerings and penetrate new markets.

Strategic partnerships are also prevalent, often between genetic companies and academic institutions or research organizations. These collaborations focus on accelerating R&D in areas like cryopreservation techniques for semen and embryos, developing new genetic markers for desirable traits, or improving the efficiency of Artificial Insemination Guns Market. Pharmaceutical companies are also investing in partnerships related to reproductive hormones and synchronization protocols, further bolstering the ecosystem. The overall trend indicates a strong investor appetite for technologies that promise to enhance productivity, sustainability, and profitability in the Dairy Cattle Breeding Market and Beef Cattle Breeding Market, leveraging scientific advancements and digital transformation.

Artificial Insemination In Cattle Segmentation

1. Product Type

1.1. Semen Straws

1.2. Artificial Insemination Guns

1.3. Catheters & Sheaths

1.4. Semen Storage Tanks

1.5. Liquid Nitrogen Containers

1.6. Others

2. Semen Type

2.1. Conventional Semen

2.2. Sexed Semen

3. Cattle Type

3.1. Dairy Cattle

3.2. Beef Cattle

4. Service Provider

4.1. Veterinary Clinics

4.2. Cooperative Breeding Centers

4.3. Others

Artificial Insemination In Cattle Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Artificial Insemination In Cattle REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 7.1% from 2020-2034

Segmentation

By Product Type

Semen Straws

Artificial Insemination Guns

Catheters & Sheaths

Semen Storage Tanks

Liquid Nitrogen Containers

Others

By Semen Type

Conventional Semen

Sexed Semen

By Cattle Type

Dairy Cattle

Beef Cattle

By Service Provider

Veterinary Clinics

Cooperative Breeding Centers

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Type

5.1.1. Semen Straws

5.1.2. Artificial Insemination Guns

5.1.3. Catheters & Sheaths

5.1.4. Semen Storage Tanks

5.1.5. Liquid Nitrogen Containers

5.1.6. Others

5.2. Market Analysis, Insights and Forecast - by Semen Type

5.2.1. Conventional Semen

5.2.2. Sexed Semen

5.3. Market Analysis, Insights and Forecast - by Cattle Type

5.3.1. Dairy Cattle

5.3.2. Beef Cattle

5.4. Market Analysis, Insights and Forecast - by Service Provider

5.4.1. Veterinary Clinics

5.4.2. Cooperative Breeding Centers

5.4.3. Others

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Product Type

6.1.1. Semen Straws

6.1.2. Artificial Insemination Guns

6.1.3. Catheters & Sheaths

6.1.4. Semen Storage Tanks

6.1.5. Liquid Nitrogen Containers

6.1.6. Others

6.2. Market Analysis, Insights and Forecast - by Semen Type

6.2.1. Conventional Semen

6.2.2. Sexed Semen

6.3. Market Analysis, Insights and Forecast - by Cattle Type

6.3.1. Dairy Cattle

6.3.2. Beef Cattle

6.4. Market Analysis, Insights and Forecast - by Service Provider

6.4.1. Veterinary Clinics

6.4.2. Cooperative Breeding Centers

6.4.3. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Product Type

7.1.1. Semen Straws

7.1.2. Artificial Insemination Guns

7.1.3. Catheters & Sheaths

7.1.4. Semen Storage Tanks

7.1.5. Liquid Nitrogen Containers

7.1.6. Others

7.2. Market Analysis, Insights and Forecast - by Semen Type

7.2.1. Conventional Semen

7.2.2. Sexed Semen

7.3. Market Analysis, Insights and Forecast - by Cattle Type

7.3.1. Dairy Cattle

7.3.2. Beef Cattle

7.4. Market Analysis, Insights and Forecast - by Service Provider

7.4.1. Veterinary Clinics

7.4.2. Cooperative Breeding Centers

7.4.3. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Product Type

8.1.1. Semen Straws

8.1.2. Artificial Insemination Guns

8.1.3. Catheters & Sheaths

8.1.4. Semen Storage Tanks

8.1.5. Liquid Nitrogen Containers

8.1.6. Others

8.2. Market Analysis, Insights and Forecast - by Semen Type

8.2.1. Conventional Semen

8.2.2. Sexed Semen

8.3. Market Analysis, Insights and Forecast - by Cattle Type

8.3.1. Dairy Cattle

8.3.2. Beef Cattle

8.4. Market Analysis, Insights and Forecast - by Service Provider

8.4.1. Veterinary Clinics

8.4.2. Cooperative Breeding Centers

8.4.3. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Product Type

9.1.1. Semen Straws

9.1.2. Artificial Insemination Guns

9.1.3. Catheters & Sheaths

9.1.4. Semen Storage Tanks

9.1.5. Liquid Nitrogen Containers

9.1.6. Others

9.2. Market Analysis, Insights and Forecast - by Semen Type

9.2.1. Conventional Semen

9.2.2. Sexed Semen

9.3. Market Analysis, Insights and Forecast - by Cattle Type

9.3.1. Dairy Cattle

9.3.2. Beef Cattle

9.4. Market Analysis, Insights and Forecast - by Service Provider

9.4.1. Veterinary Clinics

9.4.2. Cooperative Breeding Centers

9.4.3. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Product Type

10.1.1. Semen Straws

10.1.2. Artificial Insemination Guns

10.1.3. Catheters & Sheaths

10.1.4. Semen Storage Tanks

10.1.5. Liquid Nitrogen Containers

10.1.6. Others

10.2. Market Analysis, Insights and Forecast - by Semen Type

10.2.1. Conventional Semen

10.2.2. Sexed Semen

10.3. Market Analysis, Insights and Forecast - by Cattle Type

10.3.1. Dairy Cattle

10.3.2. Beef Cattle

10.4. Market Analysis, Insights and Forecast - by Service Provider

10.4.1. Veterinary Clinics

10.4.2. Cooperative Breeding Centers

10.4.3. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Genus plc

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. ABS Global

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. STgenetics

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Semex Alliance

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. CRV Holding B.V.

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. URUS Group LP

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Select Sires Inc.

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Alta Genetics Inc.

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. IMV Technologies

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. VikingGenetics

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Cogent Breeding Ltd.

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.1.12. Others

11.1.12.1. Company Overview

11.1.12.2. Products

11.1.12.3. Company Financials

11.1.12.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Product Type 2025 & 2033

Figure 3: Revenue Share (%), by Product Type 2025 & 2033

Figure 4: Revenue (billion), by Semen Type 2025 & 2033

Figure 5: Revenue Share (%), by Semen Type 2025 & 2033

Figure 6: Revenue (billion), by Cattle Type 2025 & 2033

Figure 7: Revenue Share (%), by Cattle Type 2025 & 2033

Figure 8: Revenue (billion), by Service Provider 2025 & 2033

Figure 9: Revenue Share (%), by Service Provider 2025 & 2033

Figure 10: Revenue (billion), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (billion), by Product Type 2025 & 2033

Figure 13: Revenue Share (%), by Product Type 2025 & 2033

Figure 14: Revenue (billion), by Semen Type 2025 & 2033

Figure 15: Revenue Share (%), by Semen Type 2025 & 2033

Figure 16: Revenue (billion), by Cattle Type 2025 & 2033

Figure 17: Revenue Share (%), by Cattle Type 2025 & 2033

Figure 18: Revenue (billion), by Service Provider 2025 & 2033

Figure 19: Revenue Share (%), by Service Provider 2025 & 2033

Figure 20: Revenue (billion), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (billion), by Product Type 2025 & 2033

Figure 23: Revenue Share (%), by Product Type 2025 & 2033

Figure 24: Revenue (billion), by Semen Type 2025 & 2033

Figure 25: Revenue Share (%), by Semen Type 2025 & 2033

Figure 26: Revenue (billion), by Cattle Type 2025 & 2033

Figure 27: Revenue Share (%), by Cattle Type 2025 & 2033

Figure 28: Revenue (billion), by Service Provider 2025 & 2033

Figure 29: Revenue Share (%), by Service Provider 2025 & 2033

Figure 30: Revenue (billion), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (billion), by Product Type 2025 & 2033

Figure 33: Revenue Share (%), by Product Type 2025 & 2033

Figure 34: Revenue (billion), by Semen Type 2025 & 2033

Figure 35: Revenue Share (%), by Semen Type 2025 & 2033

Figure 36: Revenue (billion), by Cattle Type 2025 & 2033

Figure 37: Revenue Share (%), by Cattle Type 2025 & 2033

Figure 38: Revenue (billion), by Service Provider 2025 & 2033

Figure 39: Revenue Share (%), by Service Provider 2025 & 2033

Figure 40: Revenue (billion), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (billion), by Product Type 2025 & 2033

Figure 43: Revenue Share (%), by Product Type 2025 & 2033

Figure 44: Revenue (billion), by Semen Type 2025 & 2033

Figure 45: Revenue Share (%), by Semen Type 2025 & 2033

Figure 46: Revenue (billion), by Cattle Type 2025 & 2033

Figure 47: Revenue Share (%), by Cattle Type 2025 & 2033

Figure 48: Revenue (billion), by Service Provider 2025 & 2033

Figure 49: Revenue Share (%), by Service Provider 2025 & 2033

Figure 50: Revenue (billion), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Product Type 2020 & 2033

Table 2: Revenue billion Forecast, by Semen Type 2020 & 2033

Table 3: Revenue billion Forecast, by Cattle Type 2020 & 2033

Table 4: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Revenue billion Forecast, by Product Type 2020 & 2033

Table 7: Revenue billion Forecast, by Semen Type 2020 & 2033

Table 8: Revenue billion Forecast, by Cattle Type 2020 & 2033

Table 9: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 10: Revenue billion Forecast, by Country 2020 & 2033

Table 11: Revenue (billion) Forecast, by Application 2020 & 2033

Table 12: Revenue (billion) Forecast, by Application 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue billion Forecast, by Product Type 2020 & 2033

Table 15: Revenue billion Forecast, by Semen Type 2020 & 2033

Table 16: Revenue billion Forecast, by Cattle Type 2020 & 2033

Table 17: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 18: Revenue billion Forecast, by Country 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Revenue (billion) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Revenue billion Forecast, by Product Type 2020 & 2033

Table 23: Revenue billion Forecast, by Semen Type 2020 & 2033

Table 24: Revenue billion Forecast, by Cattle Type 2020 & 2033

Table 25: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 26: Revenue billion Forecast, by Country 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue (billion) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Revenue (billion) Forecast, by Application 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue billion Forecast, by Product Type 2020 & 2033

Table 37: Revenue billion Forecast, by Semen Type 2020 & 2033

Table 38: Revenue billion Forecast, by Cattle Type 2020 & 2033

Table 39: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 40: Revenue billion Forecast, by Country 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue (billion) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Revenue (billion) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue billion Forecast, by Product Type 2020 & 2033

Table 48: Revenue billion Forecast, by Semen Type 2020 & 2033

Table 49: Revenue billion Forecast, by Cattle Type 2020 & 2033

Table 50: Revenue billion Forecast, by Service Provider 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology forms the cornerstone of this report, accounting for 75% of the total research effort. This robust approach ensures the collection of real-time, first-hand information directly from key market participants, providing nuanced insights into market dynamics, competitive landscapes, technological advancements, and future outlooks. Interviews are conducted through a structured questionnaire with a diverse range of stakeholders across the value chain, utilizing both telephone and in-person discussions where feasible.

Secondary research complements our primary findings, contributing 25% to the overall research framework. This phase involves a comprehensive review of existing literature, reports, and data sources to establish a foundational understanding of the market and to validate primary insights. Our rigorous approach ensures data reliability and global comparability.

Sources leveraged include:

Standard Financial Databases: Bloomberg, Factiva, Hoovers, PitchBook, providing critical company financials, mergers & acquisitions data, and competitive intelligence.

Company Annual Reports & Investor Presentations: Publicly available information from key market players to assess business strategies, performance, and market presence.

Every report is meticulously updated up to the date of purchase, ensuring that clients receive the most current and relevant market intelligence available.

Demand Modeling & Market Estimation

Our market estimation process employs a dual approach of top-down and bottom-up methodologies, triangulated across multiple data points to ensure accuracy and robustness.

Bottom-Up Approach: This method involves estimating the market size by aggregating granular data from the ground up. Key variables and metrics used include:

Total number of inseminations performed annually (segmented by cattle type and geography).

Average price per unit of conventional and sexed semen.

Sales volume and value of specific AI equipment components (e.g., AI guns, catheters, semen storage tanks).

Number of breeding female cattle (dairy cows, beef cows) and the penetration rate of AI technologies within these populations.

Top-Down Approach: This involves validating the bottom-up estimates by considering the overall market from a macro perspective, utilizing macroeconomic indicators, industry growth rates, and global livestock production trends.

Multi-Level Data Triangulation: All gathered data, whether primary or secondary, undergoes a rigorous cross-verification process. This involves comparing and contrasting information from various sources to identify discrepancies, validate trends, and establish a high degree of confidence in our estimates. Data points are validated across different regions, product types, and cattle types to ensure comprehensive coverage and accuracy.

Data Accuracy & Quality Check

Our commitment to data integrity is paramount. Through the integrated application of primary and secondary research, coupled with multi-level data triangulation, we guarantee an estimated data accuracy level of 85-90%. This rigorous quality assurance process involves:

Expert Panel Review: Insights and estimations are reviewed by internal and external subject matter experts to ensure logical consistency and market realism.

Statistical Validation: Quantitative data is subjected to statistical analysis to identify outliers, trends, and potential biases.

Iterative Refinement: Our models are continually refined based on new information and feedback, ensuring that the final output reflects the most accurate representation of the market.

Source Verification: All external data sources are carefully vetted for credibility and relevance to the Artificial Insemination in Cattle market.

Frequently Asked Questions

1. How do regulatory standards influence the Artificial Insemination In Cattle market?

Regulations govern semen collection, processing, and distribution to ensure animal health and genetic integrity. Compliance with veterinary health protocols and quality standards is critical for market players like Genus plc and ABS Global.

2. What are the sustainability considerations for artificial insemination in cattle?

Artificial insemination contributes to genetic improvement, potentially reducing the carbon footprint per unit of production through more efficient animals. Practices focus on optimizing herd health and resource utilization, aligning with ESG objectives in livestock management.

3. How have post-pandemic recovery patterns affected the Artificial Insemination In Cattle market?

Post-pandemic, the market observed stable demand as livestock farming is an essential sector. Long-term shifts include increased investment in genetic technologies and supply chain resilience, supporting a 7.1% CAGR from 2025.

4. Which region exhibits the fastest growth in the Artificial Insemination In Cattle market?

Asia-Pacific is poised for significant growth, driven by expanding dairy and beef sectors in countries like China and India. Emerging opportunities also exist in parts of South America and the Middle East as agricultural practices modernize.

5. What technological innovations are shaping the Artificial Insemination In Cattle industry?

Innovations include advancements in sexed semen technology and improved AI gun designs, enhancing breeding efficiency and outcomes. Companies like STgenetics are focusing on precision breeding tools and semen storage solutions.

6. Are there disruptive technologies or substitutes emerging for artificial insemination in cattle?

While direct substitutes are limited, genetic editing technologies represent a long-term disruptive potential for breeding. However, artificial insemination remains the most cost-effective and widely adopted method for genetic improvement in cattle farming currently.