Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Aqueous Zinc-ion Rechargeable Batteries by Battery Type (Primary Aqueous Zinc-ion Rechargeable Batteries, Secondary (Deep-Cycle) Aqueous Zinc-ion Rechargeable Batteries, Others), by Capacity Range (Low, Medium, High), by Application (Grid Energy Storage Systems, Consumer Electronics, Wearable Electronics, Electric Mobility & E-bikes, Industrial Backup Power Systems, Renewable Energy Storage Systems, Others), by Distribution Channel (Offline, Online), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 76

Key Insights into the Aqueous Zinc-ion Rechargeable Batteries Market

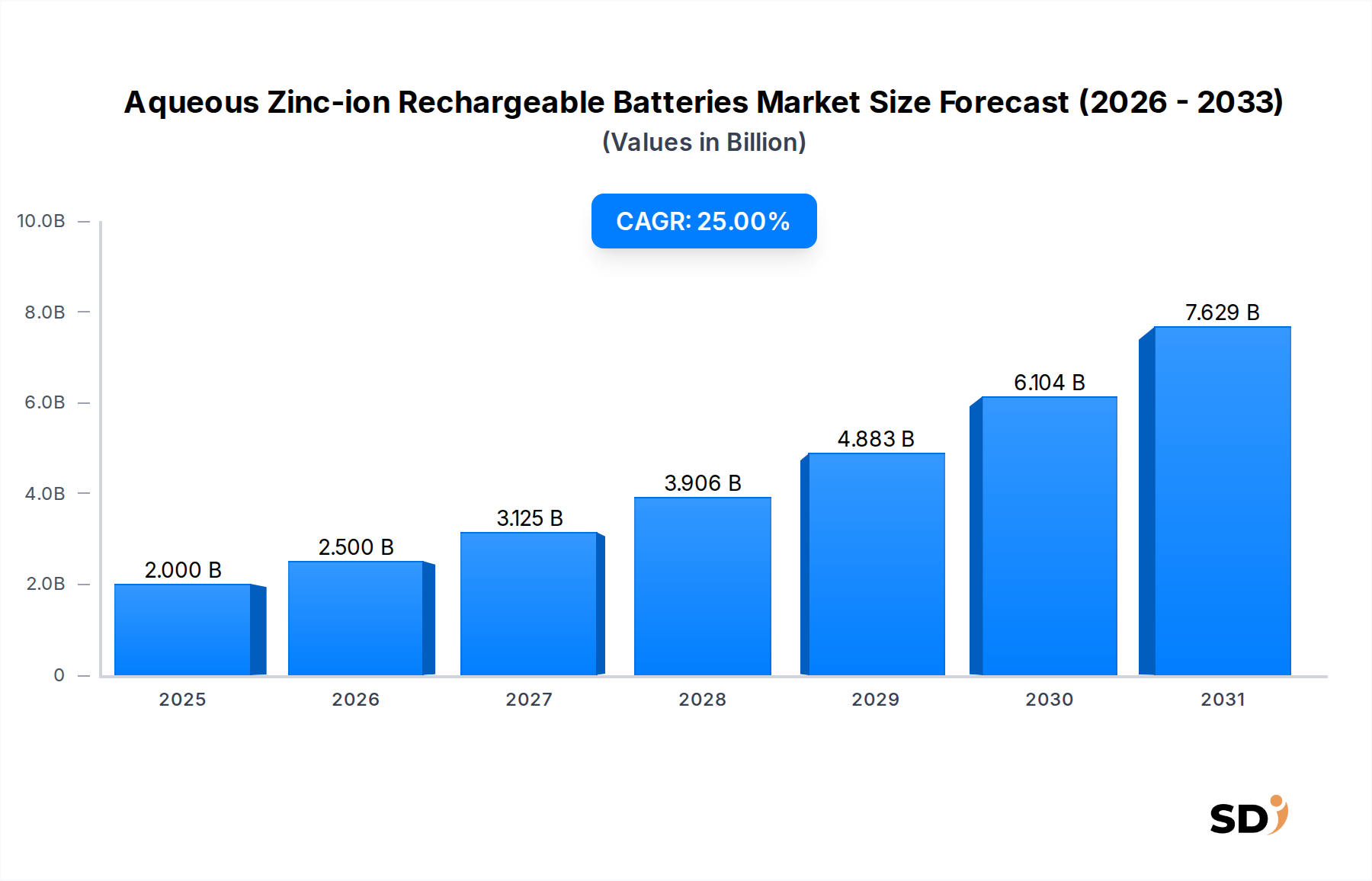

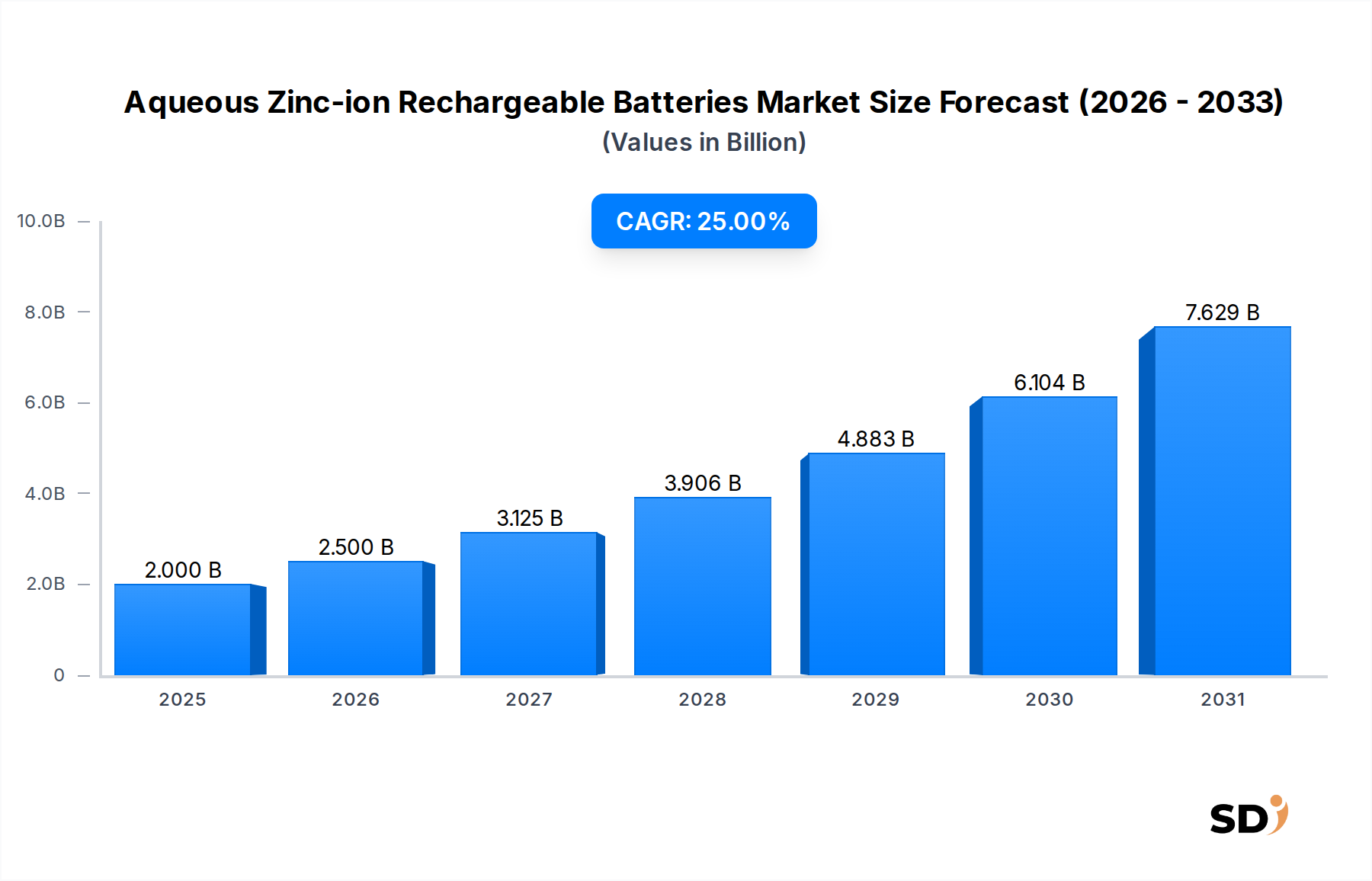

The Aqueous Zinc-ion Rechargeable Batteries Market is positioned for robust expansion, driven by increasing demand for safe, cost-effective, and sustainable energy storage solutions across various applications. The market was valued at an estimated $2 billion in 2025 and is projected to reach approximately $9.54 billion by 2032, exhibiting an impressive Compound Annual Growth Rate (CAGR) of 25% over the forecast period. This significant growth trajectory is primarily fueled by a global shift towards decarbonization, the imperative for grid modernization, and the inherent safety advantages offered by aqueous zinc-ion chemistry.

Aqueous Zinc-ion Rechargeable Batteries Market Size (In Billion)

10.0B

8.0B

6.0B

4.0B

2.0B

0

2.000 B

2025

2.500 B

2026

3.125 B

2027

3.906 B

2028

4.883 B

2029

6.104 B

2030

7.629 B

2031

Key demand drivers include the escalating deployment of renewable energy sources, which necessitates reliable and scalable energy storage to ensure grid stability and continuous power supply. Unlike the established Lithium-ion Battery Market, aqueous zinc-ion batteries leverage abundant and inexpensive raw materials, such as zinc and water-based electrolytes, contributing to a lower overall system cost and reduced geopolitical supply chain risks. Their non-flammable nature and absence of toxic heavy metals provide a crucial safety advantage, making them particularly attractive for urban installations, residential storage, and critical infrastructure applications within the Grid Energy Storage Systems Market.

While the market for Aqueous Zinc-ion Rechargeable Batteries is still maturing compared to more entrenched technologies, ongoing research and development efforts are rapidly improving energy density, cycle life, and overall performance. Innovations in electrolyte formulations and electrode architectures are addressing historical challenges like dendrite formation and capacity degradation, enhancing their competitive standing against alternatives like the Redox Flow Battery Market, especially for long-duration stationary storage. The forward outlook for the Aqueous Zinc-ion Rechargeable Batteries Market remains exceptionally positive, poised to capture a substantial share in the evolving energy storage landscape, driven by its compelling value proposition in terms of safety, sustainability, and economic viability.

Dominant Segment: Grid Energy Storage Systems in Aqueous Zinc-ion Rechargeable Batteries Market

The Grid Energy Storage Systems Market emerges as the undeniably dominant segment within the broader Aqueous Zinc-ion Rechargeable Batteries Market, accounting for a substantial revenue share and demonstrating the highest growth potential. This prominence is intrinsically linked to the global energy transition agenda, which mandates significant investment in large-scale, stationary energy storage solutions to support the integration of intermittent renewable energy sources like solar and wind power. Aqueous zinc-ion batteries, particularly the Secondary (Deep-Cycle) Aqueous Zinc-ion Rechargeable Batteries Market subset, are ideally suited for grid-scale applications due to their inherent characteristics.

Their primary advantages in this segment include superior safety profiles, being non-flammable and avoiding thermal runaway risks, which is critical for large-scale deployments in populated areas or near sensitive infrastructure. Furthermore, the use of abundant and inexpensive raw materials like zinc and aqueous electrolytes contributes to a significantly lower levelized cost of storage (LCOS) compared to many conventional battery technologies. This cost-effectiveness, combined with the technology's scalability and ability to provide long-duration discharge, positions it as a preferred choice for utilities and independent power producers seeking robust solutions for peak shaving, load shifting, frequency regulation, and black start capabilities. The robust demand from the Grid Energy Storage Systems Market is also bolstering the broader Renewable Energy Storage Market, where zinc-ion solutions offer a sustainable alternative to traditional fossil fuel peaker plants.

Key players like Eos Energy Enterprises and Salient Energy are heavily invested in developing and deploying grid-scale aqueous zinc-ion solutions, focusing on modular designs that simplify installation and maintenance. While Primary Aqueous Zinc-ion Rechargeable Batteries Market applications exist for niche, smaller-scale use, it is the deep-cycle, long-duration capabilities of the secondary variants that truly empower the dominance of the grid storage segment. The segment's share is anticipated to continue its rapid growth, consolidating its position as the core application area as global grids undergo modernization and decentralization, further amplified by supportive government policies and incentives for clean energy infrastructure development.

The growth trajectory of the Aqueous Zinc-ion Rechargeable Batteries Market is being propelled by several compelling drivers, while also navigating specific constraints.

Drivers:

Enhanced Safety Profile: A paramount driver is the intrinsic safety of aqueous zinc-ion batteries. Utilizing non-flammable, water-based electrolytes mitigates the risk of thermal runaway and fire, which is a significant concern for the Lithium-ion Battery Market, especially in large-scale deployments. This makes them highly attractive for critical applications within the Industrial Backup Power Systems Market, where safety and reliability are non-negotiable. This characteristic significantly reduces installation complexities and operational safety protocols, thereby lowering overall project costs.

Cost-Effectiveness and Abundant Raw Materials: Zinc is the fourth most consumed metal globally and is widely available and significantly less expensive than lithium, cobalt, or vanadium. This abundance translates directly into lower material costs for aqueous zinc-ion batteries. The widespread availability of materials for the Zinc Sulfate Market, a key electrolyte component, ensures a stable and resilient supply chain, insulating the market from the price volatility and geopolitical risks associated with critical minerals for other battery chemistries. This economic advantage is crucial for enabling the widespread adoption of grid-scale storage solutions, thereby supporting the broader Renewable Energy Storage Market.

Environmental Sustainability: Aqueous zinc-ion batteries are inherently more environmentally friendly. They utilize non-toxic, easily recyclable components, including zinc and water, making them a more sustainable alternative. This aligns with increasing environmental, social, and governance (ESG) mandates and circular economy principles, attracting investment and regulatory support.

Constraints:

Energy Density Limitations: Compared to lithium-ion batteries, aqueous zinc-ion systems typically exhibit lower gravimetric and volumetric energy densities. While sufficient for stationary applications like the Grid Energy Storage Systems Market, this limitation curtails their suitability for many portable and electric mobility applications where compact size and light weight are paramount.

Cycle Life and Performance Degradation: Challenges such as zinc dendrite formation and passivation on the zinc electrode during repeated charging and discharging cycles can lead to capacity fade and reduced cycle life. Although significant research advancements are being made to overcome these hurdles through novel electrolyte additives and electrode designs, achieving consistently high cycle stability comparable to mature battery chemistries remains an ongoing area of focus.

Market Maturity and Commercialization: The Aqueous Zinc-ion Rechargeable Batteries Market is relatively nascent compared to the well-established Lithium-ion Battery Market. This means fewer large-scale deployments, less manufacturing infrastructure, and a smaller skilled workforce, which can pose challenges for rapid scaling and widespread commercialization. Bridging this gap requires substantial capital investment and continued technological validation.

Competitive Ecosystem of Aqueous Zinc-ion Rechargeable Batteries Market

The Aqueous Zinc-ion Rechargeable Batteries Market features a dynamic competitive landscape, comprising innovative startups and established energy solution providers. These companies are actively engaged in advancing the technology, scaling manufacturing, and deploying their solutions across various applications:

Eos Energy Enterprises: This company is a leading player focused on long-duration, utility-scale zinc-based battery energy storage systems, primarily targeting the Grid Energy Storage Systems Market. They offer a non-flammable, cobalt-free, and sustainable solution designed for a 20-year operational life.

ZincFive: Specializes in nickel-zinc (NiZn) battery technology, which shares many advantages with aqueous zinc-ion, particularly regarding safety and power density. ZincFive's batteries are deployed in mission-critical applications such as data centers, intelligent transportation, and industrial backup power systems.

Salient Energy: Known for its groundbreaking low-cost, high-performance zinc-ion battery architecture. Salient Energy focuses on providing sustainable and safe stationary storage solutions that can replace lithium-ion batteries in various applications, including grid services and commercial energy storage.

AEsir Technologies: This firm is dedicated to developing and commercializing safe, high-performance, and sustainable zinc-air and zinc-ion battery technologies. Their solutions aim to address the critical need for reliable and environmentally friendly energy storage across a broad spectrum of uses.

Enerpoly: An innovative company focused on developing and commercializing sustainable zinc-ion battery solutions for stationary energy storage. Enerpoly emphasizes the eco-friendly aspect and cost-effectiveness of its technology for various applications, including residential and commercial use.

Urban Electric Power: Specializes in zinc-manganese dioxide (Zn-MnO2) battery technology, offering a safe, long-duration, and cost-effective energy storage solution. Their batteries are designed for grid-scale and industrial applications, including those requiring robust Industrial Backup Power Systems Market solutions.

ZAF Energy Systems: A pioneer in advanced nickel-zinc battery technology, offering solutions with high power density, long cycle life, and inherent safety. Their focus is on providing next-generation battery technology for various sectors, demonstrating the versatility of zinc-based chemistries.

Recent Developments & Milestones in Aqueous Zinc-ion Rechargeable Batteries Market

Recent years have witnessed significant strides in the Aqueous Zinc-ion Rechargeable Batteries Market, marked by technological advancements, strategic partnerships, and capacity expansions aimed at accelerating market penetration:

June 2025: Salient Energy announced a successful pilot deployment of their zinc-ion battery system for a community microgrid project in California, demonstrating seamless integration with renewable energy sources and enhancing grid resilience.

March 2025: AEsir Technologies secured a substantial funding round to scale up its manufacturing capabilities for next-generation zinc-ion batteries, specifically targeting military and critical infrastructure applications that demand high safety standards.

November 2024: Enerpoly unveiled a new battery module design, significantly increasing the volumetric energy density of their aqueous zinc-ion cells by 10%, making them more competitive for space-constrained installations in the Grid Energy Storage Systems Market.

August 2024: Eos Energy Enterprises reported surpassing 200 MWh of deployed zinc-based battery systems globally, solidifying its position as a leader in long-duration energy storage and showcasing the commercial viability of the technology.

April 2024: Breakthroughs in electrolyte chemistry by an unnamed university research consortium led to a 15% improvement in the cycle life of aqueous zinc-ion batteries, effectively addressing one of the key historical constraints of the technology and opening new avenues for the Secondary (Deep-Cycle) Aqueous Zinc-ion Rechargeable Batteries Market.

January 2024: Urban Electric Power forged a strategic partnership with a major European utility provider to develop a series of urban energy storage projects, leveraging their safe zinc-manganese dioxide battery technology for local grid support and peak demand management.

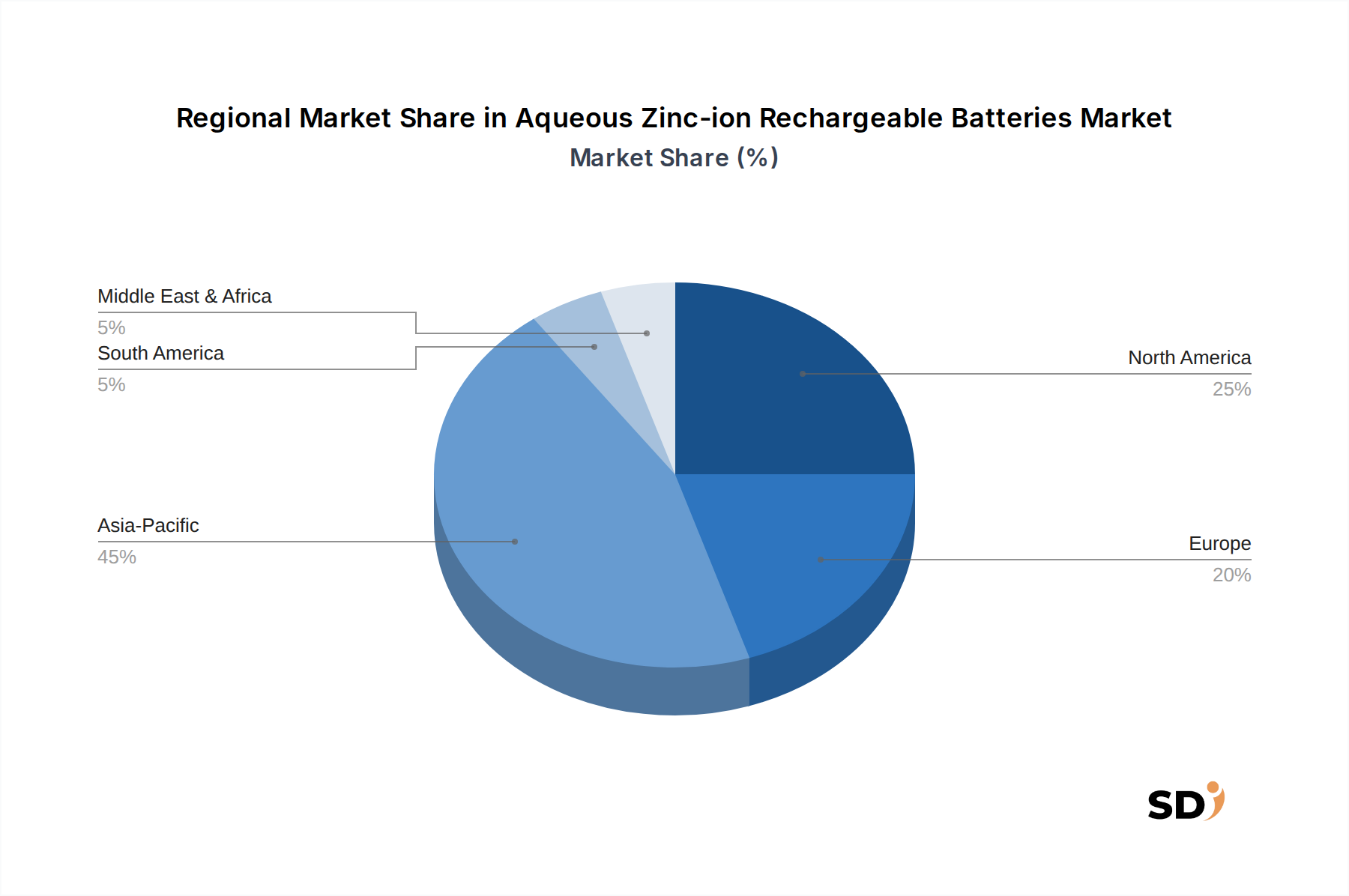

Regional Market Breakdown for Aqueous Zinc-ion Rechargeable Batteries Market

The global Aqueous Zinc-ion Rechargeable Batteries Market exhibits varied dynamics across key geographical regions, with each contributing uniquely to the overall market expansion driven by specific energy policies, economic factors, and industrial landscapes.

Asia Pacific is anticipated to dominate the market and is projected to be the fastest-growing region, with an estimated CAGR exceeding 28%. This rapid expansion is fueled by ambitious renewable energy targets in countries like China, India, Japan, and South Korea, leading to massive investments in the Renewable Energy Storage Market. The region's robust manufacturing capabilities and increasing industrialization also drive demand for reliable Industrial Backup Power Systems Market solutions. Government incentives for domestic battery production and grid modernization further bolster the adoption of aqueous zinc-ion batteries.

North America holds a significant revenue share and is expected to grow at a healthy CAGR of around 24-26%. The region's growth is primarily driven by substantial investments in grid infrastructure upgrades, increasing penetration of intermittent renewables, and a strong emphasis on battery safety for utility-scale and commercial installations. Policies such as the Inflation Reduction Act (IRA) in the United States provide significant tax credits and incentives for domestic energy storage manufacturing and deployment, creating a conducive environment for the Grid Energy Storage Systems Market. Demand for safe and long-duration storage solutions for industrial and commercial applications is also a key driver.

Europe is projected to demonstrate a steady growth trajectory, with an estimated CAGR in the range of 22-24%. Decarbonization goals set by the European Union, coupled with stringent environmental regulations, encourage the adoption of sustainable and non-toxic battery chemistries. Germany, the UK, and France are leading the charge in grid stabilization projects and the integration of renewable energy. The region's focus on circular economy principles and sustainable sourcing further aligns with the value proposition of aqueous zinc-ion batteries.

Middle East & Africa and South America represent emerging markets with considerable potential. While currently holding a smaller market share, these regions are poised for accelerated growth, driven by increasing electrification efforts, significant untapped renewable energy resources, and the need for resilient power infrastructure. Investments in large-scale solar and wind projects, particularly in the Middle East and parts of South America, will create a growing demand for cost-effective and reliable energy storage solutions, including those from the Aqueous Zinc-ion Rechargeable Batteries Market.

Supply Chain & Raw Material Dynamics for Aqueous Zinc-ion Rechargeable Batteries Market

The supply chain for the Aqueous Zinc-ion Rechargeable Batteries Market is characterized by its relative simplicity and reduced dependency on geopolitically sensitive materials compared to conventional battery technologies. Upstream dependencies primarily revolve around zinc metal, water, and various salts and additives for the electrolyte.

Zinc metal is a globally abundant resource, with major mining operations located across China, Australia, Peru, and the United States. This broad geographical distribution significantly mitigates sourcing risks and price volatility often seen with critical battery minerals like lithium or cobalt. The availability of zinc metal ensures a stable input for electrode manufacturing. A critical component for the electrolyte is often zinc sulfate, and the Zinc Sulfate Market benefits from the abundance and relatively stable pricing of zinc.

Water, the primary solvent for the electrolyte, is universally available and inexpensive, eliminating concerns about scarcity or high costs associated with organic solvents used in other battery chemistries. Other raw materials include various polymers for separators and current collectors, which also benefit from established supply chains. This localized and diversified sourcing strategy renders the Aqueous Zinc-ion Rechargeable Batteries Market less susceptible to global supply chain disruptions that have historically plagued the Lithium-ion Battery Market, especially during periods of geopolitical tension or natural disasters.

Price trends for zinc metal are influenced by global industrial demand and commodity market dynamics, but generally exhibit more stability than critical minerals. The non-toxic nature of the raw materials and the aqueous electrolyte also simplifies manufacturing processes, reduces environmental compliance burdens, and streamlines end-of-life recycling, contributing to a more sustainable and resilient supply chain overall.

Investment & Funding Activity in Aqueous Zinc-ion Rechargeable Batteries Market

Investment and funding activity in the Aqueous Zinc-ion Rechargeable Batteries Market have seen a notable uptick in the past 2-3 years, reflecting growing investor confidence in the technology's potential to address critical energy storage needs. The majority of capital inflows are directed towards companies focused on scaling manufacturing and deploying systems for grid-scale and industrial applications.

Venture funding rounds have been crucial for several startups. Companies like Salient Energy and Enerpoly have successfully closed multi-million dollar Series A and B rounds, attracting capital from climate tech investors and strategic corporate venture arms. This funding is primarily earmarked for expanding production capacity, accelerating R&D to enhance cycle life and energy density, and expanding market reach within the Grid Energy Storage Systems Market. Investors are particularly drawn to the inherent safety, cost-effectiveness, and sustainable material profile of aqueous zinc-ion batteries, viewing them as a long-term solution in the evolving energy landscape.

Strategic partnerships between battery developers and utilities, independent power producers (IPPs), and renewable energy developers are also on the rise. These collaborations often involve pilot projects and initial commercial deployments, providing crucial validation and market traction. For instance, partnerships aimed at integrating zinc-ion batteries into large-scale solar and wind farms underscore the technology's role in the broader Renewable Energy Storage Market. Furthermore, government grants and incentives, especially in North America and Europe, are playing a significant role in de-risking early-stage investments and fostering domestic battery manufacturing capabilities.

The sub-segments attracting the most capital are clearly Grid Energy Storage Systems Market and Industrial Backup Power Systems Market. This is due to the immediate and pressing need for long-duration, safe, and reliable stationary storage solutions that can reduce reliance on fossil fuels, enhance grid resilience, and lower operating costs for commercial and industrial users. While less pronounced, some investment is also flowing into specialized applications for the Secondary (Deep-Cycle) Aqueous Zinc-ion Rechargeable Batteries Market, particularly for off-grid or remote power solutions.

10.2. Market Analysis, Insights and Forecast - by Capacity Range

10.2.1. Low

10.2.2. Medium

10.2.3. High

10.3. Market Analysis, Insights and Forecast - by Application

10.3.1. Grid Energy Storage Systems

10.3.2. Consumer Electronics

10.3.3. Wearable Electronics

10.3.4. Electric Mobility & E-bikes

10.3.5. Industrial Backup Power Systems

10.3.6. Renewable Energy Storage Systems

10.3.7. Others

10.4. Market Analysis, Insights and Forecast - by Distribution Channel

10.4.1. Offline

10.4.2. Online

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Eos Energy Enterprises

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. ZincFive

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Salient Energy

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. AEsir Technologies

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Enerpoly

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Urban Electric Power

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. ZAF Energy Systems

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Others

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Revenue (billion), by Battery Type 2025 & 2033

Figure 3: Revenue Share (%), by Battery Type 2025 & 2033

Figure 4: Revenue (billion), by Capacity Range 2025 & 2033

Figure 5: Revenue Share (%), by Capacity Range 2025 & 2033

Figure 6: Revenue (billion), by Application 2025 & 2033

Figure 7: Revenue Share (%), by Application 2025 & 2033

Figure 8: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 9: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 10: Revenue (billion), by Country 2025 & 2033

Figure 11: Revenue Share (%), by Country 2025 & 2033

Figure 12: Revenue (billion), by Battery Type 2025 & 2033

Figure 13: Revenue Share (%), by Battery Type 2025 & 2033

Figure 14: Revenue (billion), by Capacity Range 2025 & 2033

Figure 15: Revenue Share (%), by Capacity Range 2025 & 2033

Figure 16: Revenue (billion), by Application 2025 & 2033

Figure 17: Revenue Share (%), by Application 2025 & 2033

Figure 18: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 19: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 20: Revenue (billion), by Country 2025 & 2033

Figure 21: Revenue Share (%), by Country 2025 & 2033

Figure 22: Revenue (billion), by Battery Type 2025 & 2033

Figure 23: Revenue Share (%), by Battery Type 2025 & 2033

Figure 24: Revenue (billion), by Capacity Range 2025 & 2033

Figure 25: Revenue Share (%), by Capacity Range 2025 & 2033

Figure 26: Revenue (billion), by Application 2025 & 2033

Figure 27: Revenue Share (%), by Application 2025 & 2033

Figure 28: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 29: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 30: Revenue (billion), by Country 2025 & 2033

Figure 31: Revenue Share (%), by Country 2025 & 2033

Figure 32: Revenue (billion), by Battery Type 2025 & 2033

Figure 33: Revenue Share (%), by Battery Type 2025 & 2033

Figure 34: Revenue (billion), by Capacity Range 2025 & 2033

Figure 35: Revenue Share (%), by Capacity Range 2025 & 2033

Figure 36: Revenue (billion), by Application 2025 & 2033

Figure 37: Revenue Share (%), by Application 2025 & 2033

Figure 38: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 39: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 40: Revenue (billion), by Country 2025 & 2033

Figure 41: Revenue Share (%), by Country 2025 & 2033

Figure 42: Revenue (billion), by Battery Type 2025 & 2033

Figure 43: Revenue Share (%), by Battery Type 2025 & 2033

Figure 44: Revenue (billion), by Capacity Range 2025 & 2033

Figure 45: Revenue Share (%), by Capacity Range 2025 & 2033

Figure 46: Revenue (billion), by Application 2025 & 2033

Figure 47: Revenue Share (%), by Application 2025 & 2033

Figure 48: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 49: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 50: Revenue (billion), by Country 2025 & 2033

Figure 51: Revenue Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Battery Type 2020 & 2033

Table 2: Revenue billion Forecast, by Capacity Range 2020 & 2033

Table 3: Revenue billion Forecast, by Application 2020 & 2033

Table 4: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 5: Revenue billion Forecast, by Region 2020 & 2033

Table 6: Revenue billion Forecast, by Battery Type 2020 & 2033

Table 7: Revenue billion Forecast, by Capacity Range 2020 & 2033

Table 8: Revenue billion Forecast, by Application 2020 & 2033

Table 9: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 10: Revenue billion Forecast, by Country 2020 & 2033

Table 11: Revenue (billion) Forecast, by Application 2020 & 2033

Table 12: Revenue (billion) Forecast, by Application 2020 & 2033

Table 13: Revenue (billion) Forecast, by Application 2020 & 2033

Table 14: Revenue billion Forecast, by Battery Type 2020 & 2033

Table 15: Revenue billion Forecast, by Capacity Range 2020 & 2033

Table 16: Revenue billion Forecast, by Application 2020 & 2033

Table 17: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 18: Revenue billion Forecast, by Country 2020 & 2033

Table 19: Revenue (billion) Forecast, by Application 2020 & 2033

Table 20: Revenue (billion) Forecast, by Application 2020 & 2033

Table 21: Revenue (billion) Forecast, by Application 2020 & 2033

Table 22: Revenue billion Forecast, by Battery Type 2020 & 2033

Table 23: Revenue billion Forecast, by Capacity Range 2020 & 2033

Table 24: Revenue billion Forecast, by Application 2020 & 2033

Table 25: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 26: Revenue billion Forecast, by Country 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Revenue (billion) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Revenue (billion) Forecast, by Application 2020 & 2033

Table 31: Revenue (billion) Forecast, by Application 2020 & 2033

Table 32: Revenue (billion) Forecast, by Application 2020 & 2033

Table 33: Revenue (billion) Forecast, by Application 2020 & 2033

Table 34: Revenue (billion) Forecast, by Application 2020 & 2033

Table 35: Revenue (billion) Forecast, by Application 2020 & 2033

Table 36: Revenue billion Forecast, by Battery Type 2020 & 2033

Table 37: Revenue billion Forecast, by Capacity Range 2020 & 2033

Table 38: Revenue billion Forecast, by Application 2020 & 2033

Table 39: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 40: Revenue billion Forecast, by Country 2020 & 2033

Table 41: Revenue (billion) Forecast, by Application 2020 & 2033

Table 42: Revenue (billion) Forecast, by Application 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Revenue (billion) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Revenue (billion) Forecast, by Application 2020 & 2033

Table 47: Revenue billion Forecast, by Battery Type 2020 & 2033

Table 48: Revenue billion Forecast, by Capacity Range 2020 & 2033

Table 49: Revenue billion Forecast, by Application 2020 & 2033

Table 50: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research forms the cornerstone of this report, accounting for 75% of the overall research effort to ensure the highest fidelity to current market dynamics. This rigorous approach involves in-depth, semi-structured interviews and discussions with a diverse set of industry stakeholders across the value chain. Key objectives of these engagements include validating secondary findings, gathering qualitative insights on market drivers, challenges, competitive landscape, technological advancements, and future trends, as well as obtaining granular data points for market size estimation and forecasting.

Primary interviews were conducted with representatives from the following specific company types within the Aqueous Zinc-ion Rechargeable Batteries market value chain:

Aqueous Zinc-ion Battery Manufacturers

Specialty Material & Electrolyte Suppliers

Energy Storage System Integrators

Grid-Scale Project Developers

Research & Development Institutions

Stakeholders interviewed held the following specific job designations:

VP of Battery R&D

Director of Energy Storage Product Management

Head of Grid Solutions Business Development

Senior Energy Storage System Engineer

These discussions spanned across key geographic regions, ensuring a global perspective on market trends and opportunities. Our interview process is designed to elicit unbiased, expert opinions that directly inform our analysis.

Key Stakeholders Interviewed

Stakeholder Role

Interview Share (%)

VP of Battery R&D

25%

Director of Energy Storage Product Management

30%

Head of Grid Solutions Business Development

25%

Senior Energy Storage System Engineer

20%

Industry Ecosystem Breakdown

Company Type

Representation (%)

Aqueous Zinc-ion Battery Manufacturers

30%

Specialty Material & Electrolyte Suppliers

20%

Energy Storage System Integrators

25%

Grid-Scale Project Developers

15%

Research & Development Institutions

10%

Secondary Research & Industry Benchmarking

Secondary research contributes 25% to our total research methodology, providing foundational data, validating primary findings, and offering a broad understanding of the market landscape. This phase involves extensive data mining from a multitude of credible, authoritative sources. We systematically collect and analyze information from:

Corporate Filings & Investor Presentations: Annual reports, quarterly earnings calls, and investor presentations of public companies operating in the energy storage and battery sectors.

Academic Journals & Patents: Peer-reviewed articles and patent databases to track technological innovations and research trends in aqueous zinc-ion battery chemistry.

Crucially, data from other market research websites is strictly excluded to maintain the independence and integrity of our research.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies combine both top-down and bottom-up approaches, complemented by multi-level data triangulation to ensure robust and accurate estimations. This iterative process involves:

Top-Down Approach: Initial estimation of the total addressable market based on macro-economic indicators, energy storage market penetration rates, and overall battery market growth trends, then disaggregated by battery type, capacity, application, and region.

Bottom-Up Approach: Detailed aggregation of market data from the ground up, starting with granular data points at the product and application level. Key variables and metrics utilized for the bottom-up market size calculation include:

Annual deployed capacity (GWh) of aqueous zinc-ion batteries across key applications.

Average System Price (ASP) per kWh across different battery types and capacity segments.

Number of new commercial deployments/projects utilizing aqueous zinc-ion technology.

Regional investment trends in grid modernization and renewable energy integration.

Multi-Level Data Triangulation: Cross-referencing and validating data points from primary interviews, secondary sources, and internal databases. This includes comparing supply-side estimates with demand-side projections, and reconciling quantitative data with qualitative insights to identify discrepancies and refine our models. This iterative validation ensures a comprehensive and accurate market view.

Data Accuracy & Quality Check

We adhere to the highest standards of data integrity and analytical rigor. Our robust quality control procedures involve multiple levels of review by senior analysts and domain experts. Through our comprehensive methodology, we guarantee an estimated data accuracy level of 88-90%. Furthermore, our commitment to providing timely and relevant insights means that every report is updated with the latest market intelligence and data up to the date of purchase, reflecting the most current market realities and forecasts.

Frequently Asked Questions

1. How do Aqueous Zinc-ion Rechargeable Batteries impact environmental sustainability?

Aqueous Zinc-ion Rechargeable Batteries offer enhanced environmental sustainability due to their non-flammable aqueous electrolytes and use of abundant zinc. This reduces reliance on critical materials and minimizes environmental risks compared to traditional battery chemistries. They are considered a safer, more recyclable alternative for energy storage.

2. What are the primary growth drivers for Aqueous Zinc-ion Rechargeable Batteries?

The market for Aqueous Zinc-ion Rechargeable Batteries is driven by demand in grid energy storage systems, consumer electronics, and renewable energy integration. These applications benefit from the batteries' enhanced safety, lower cost, and longer cycle life, propelling a projected 25% CAGR. Expansion into electric mobility also contributes significantly.

3. Which technological innovations are shaping the Aqueous Zinc-ion Battery industry?

Innovations focus on improving electrode materials and electrolyte formulations to enhance energy density, cycle life, and power output across low, medium, and high capacity ranges. R&D targets secondary (deep-cycle) battery types to optimize performance for prolonged discharge applications. Advancements in cell architecture are also critical for commercial viability.

4. What is the current investment landscape for Aqueous Zinc-ion Battery companies?

Investment in Aqueous Zinc-ion Rechargeable Batteries is growing, with companies like Eos Energy Enterprises, ZincFive, and Salient Energy attracting significant capital. Funding rounds primarily support R&D, scaling manufacturing capacities, and expanding application portfolios. Venture capital interest is focused on firms demonstrating advanced material science and commercial readiness in grid storage.

5. What are the key export-import dynamics in the Aqueous Zinc-ion Rechargeable Batteries market?

International trade flows in Aqueous Zinc-ion Rechargeable Batteries are influenced by manufacturing concentrations, particularly in the Asia-Pacific region, supplying global markets. Key components and raw materials for these batteries, such as zinc, are sourced globally, driving import activities for production hubs. Demand from North America and Europe for grid storage further shapes export dynamics.

6. Who are the leading companies in the Aqueous Zinc-ion Rechargeable Batteries market?

Key players in the Aqueous Zinc-ion Rechargeable Batteries market include Eos Energy Enterprises, ZincFive, Salient Energy, and AEsir Technologies. Other significant companies like Enerpoly and Urban Electric Power are also developing solutions. The competitive landscape is characterized by innovation in battery design and strategic partnerships aimed at commercialization.