Sector Data Insights (SDI) is a specialized market intelligence and strategic consulting firm focused on delivering high-quality, data-driven syndicated research reports, industry analysis, competitive intelligence, and advisory solutions. With a strong emphasis on analytical excellence, particularly in life sciences, analytical instrumentation, and related high-tech sectors, Sector Data Insights empowers manufacturers, investors, service providers, researchers, and decision-makers with actionable insights for strategic growth, innovation, and market leadership.

SDI combines deep domain expertise in laboratory and analytical technologies with advanced analytics to provide comprehensive market assessments, technology trend analysis, vendor share data, investment intelligence, supply chain insights, and forward-looking forecasts. Our research supports organizations navigating complex global markets across industries such as life sciences, semiconductors & electronics, consumer goods, materials & chemicals, construction & manufacturing, food & beverages, energy & power, automotive & transportation, ICT & media, aerospace & defense, and BFSI.

Ankle Monitors Market: $4.8B by 2025, 8% CAGR Analysis

Ankle Monitors

Ankle Monitors Market: $4.8B by 2025, 8% CAGR Analysis

Ankle Monitors by Product Type (Radio Frequency-Based, GPS-Based, Cellular-Based, Hybrid), by Component (Hardware, Software, Services), by Monitoring Type (Active Monitoring, Passive Monitoring), by Distribution Channel (Direct Sales, Online Sales, Offline Sales), by End User (Criminal Justice, Home Detention, Healthcare, Child Tracking, Private Monitoring Service Providers, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : Jul 2, 2026|Base Year : 2025|Pages : 100

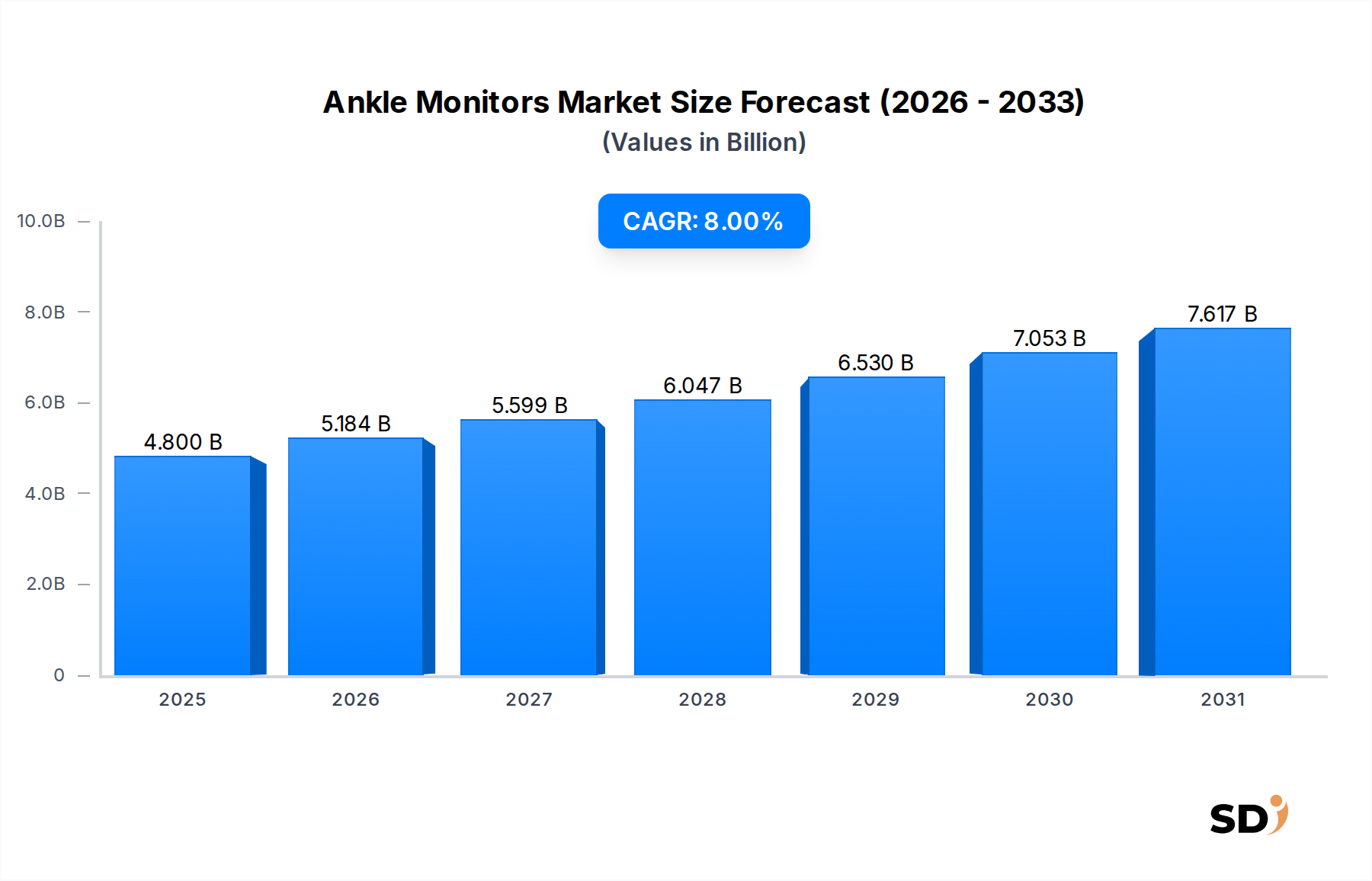

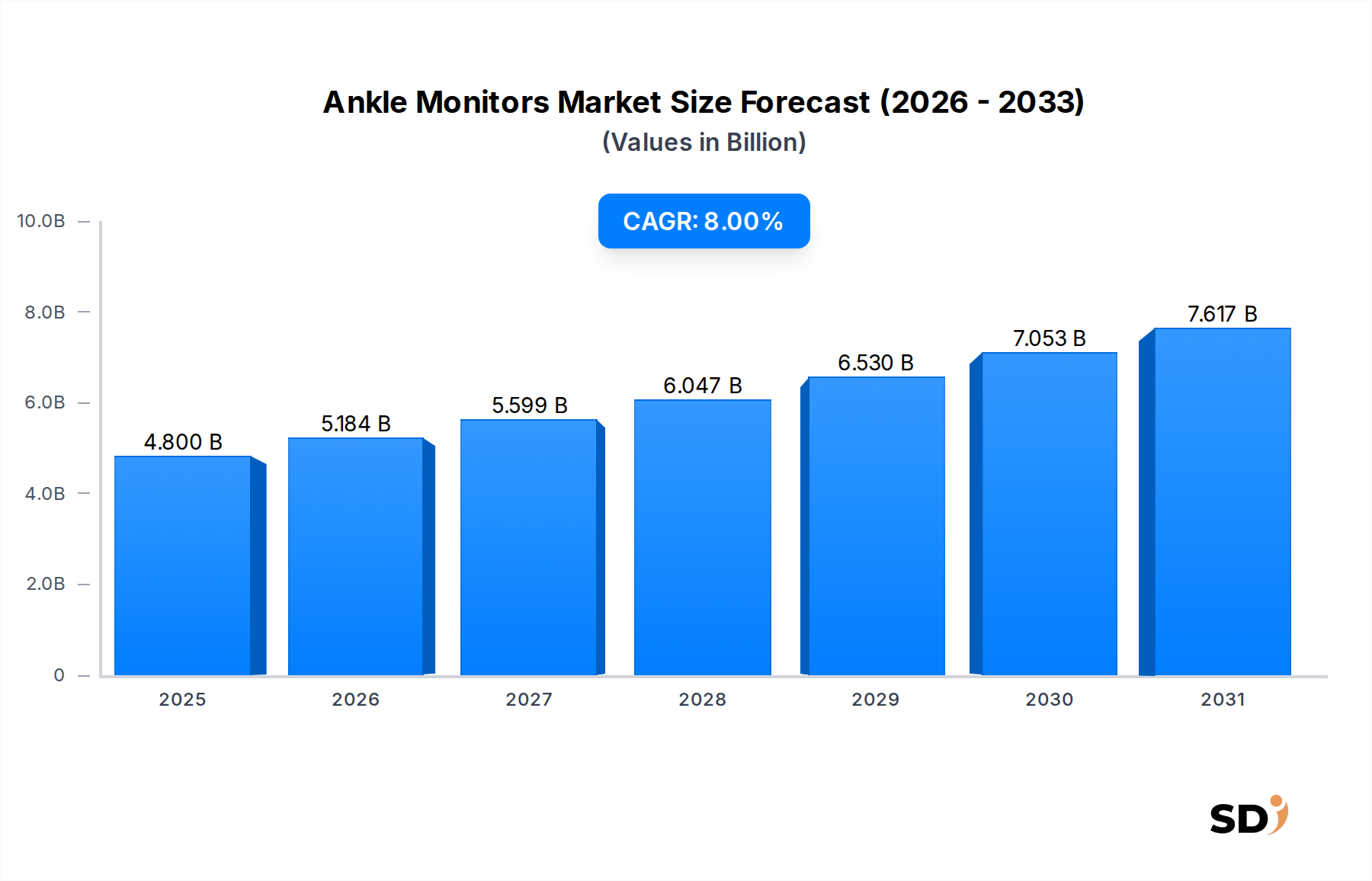

The Ankle Monitors Market is poised for substantial expansion, reflecting growing applications across various sectors beyond its traditional use in criminal justice. Valued at an estimated $4.8 billion in 2025, the market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 8% through the forecast period. This growth is primarily fueled by a paradigm shift towards alternative sentencing and community supervision, aiming to alleviate pressure on overcrowded correctional facilities while promoting rehabilitation. Technological advancements, particularly in miniaturization, battery longevity, and secure data transmission, are critical drivers. The integration of advanced communication protocols like 5G and enhanced satellite navigation systems ensures greater reliability and accuracy for monitoring solutions. Furthermore, the expansion of ankle monitors into new end-user segments, such as the Remote Patient Monitoring Market and child safety, contributes significantly to market buoyancy. Macro tailwinds include an increasing global focus on human rights and rehabilitation, pushing judicial systems to adopt less restrictive but equally effective monitoring methods. The demand for sophisticated tracking solutions is also intensifying due to rising security concerns and the need for efficient resource allocation within public safety departments. The market outlook remains positive, with continued innovation expected in hybrid monitoring systems that combine multiple technologies for superior performance and reduced false positives. Moreover, the convergence with the broader Internet of Things Devices Market and the development of AI-powered analytics will transform ankle monitors into intelligent data collection and predictive tools, offering nuanced insights into monitored individuals' behavior and location. As governments and private entities seek more cost-effective and efficient monitoring solutions, the Ankle Monitors Market is set to witness sustained innovation and adoption across an expanding spectrum of applications.

Ankle Monitors Market Size (In Billion)

10.0B

8.0B

6.0B

4.0B

2.0B

0

4.800 B

2025

5.184 B

2026

5.599 B

2027

6.047 B

2028

6.530 B

2029

7.053 B

2030

7.617 B

2031

The Dominance of GPS-Based Systems in Ankle Monitors Market

Within the diverse product type segment of the Ankle Monitors Market, GPS-Based systems are identified as the dominant category by revenue share, a trend expected to solidify its position throughout the forecast period. This dominance is primarily attributable to the unparalleled accuracy and real-time tracking capabilities that GPS technology offers, making it indispensable for stringent monitoring requirements. GPS-Based ankle monitors provide precise geographical location data, enabling authorities to enforce exclusion zones, track movements, and respond swiftly to violations. This level of oversight is crucial for applications within the Correctional Facilities Market and Home Detention Market, where continuous, verifiable location data is paramount for public safety and compliance. The inherent ability of GPS systems to integrate seamlessly with geofencing functionalities allows for the creation of virtual boundaries, alerting officials instantly if an individual deviates from pre-defined zones. Leading manufacturers in the Electronic Monitoring Market continue to invest heavily in refining GPS technology, enhancing signal acquisition in challenging environments, and reducing power consumption to extend battery life. This continuous improvement ensures that GPS-based devices remain the preferred choice for critical applications. While Radio Frequency-Based systems, traditionally used for shorter-range monitoring within a fixed perimeter, still hold a segment of the market, their utility is diminishing compared to the expansive reach of GPS. Cellular-Based systems, which leverage mobile network infrastructure for communication, offer good data transmission capabilities and are often used as a supplementary or primary method in areas with limited GPS signal, or for transmitting biometric data. However, the foundational need for accurate, wide-area location tracking firmly positions GPS as the core technology. Hybrid systems, which combine GPS, cellular, and sometimes RF technologies, represent an evolution aimed at maximizing coverage and reliability. These systems leverage the strengths of each technology, switching seamlessly between them to maintain uninterrupted monitoring. For instance, a hybrid device might use GPS for primary outdoor tracking, cellular for data transmission and indoor tracking via cell tower triangulation, and RF for proximity monitoring within a home. The continued development of the Location-Based Services Market further empowers GPS-based ankle monitors, integrating them with advanced mapping and analytical tools. The demand for these sophisticated, multi-functional devices ensures that the GPS-Based segment, including its hybrid iterations, will continue to command the largest share and drive innovation in the overall Ankle Monitors Market.

Key Market Drivers and Constraints in Ankle Monitors Market

The Ankle Monitors Market is influenced by a confluence of driving forces and significant restraints. One primary driver is the escalating demand for cost-effective alternatives to incarceration within the Criminal Justice Market. Governments and judicial systems globally are increasingly facing overcrowded prisons and high operational costs, prompting a shift towards community-based supervision. For instance, statistics from various jurisdictions indicate that electronic monitoring can be significantly less expensive than incarceration per day, driving the adoption of ankle monitors for parolees, probationers, and individuals under house arrest. Another crucial driver is the rapid advancement in underlying Sensor Technology Market and communication protocols. Modern ankle monitors integrate high-precision GPS Tracking Devices Market modules, secure cellular data transmission, and sophisticated tamper detection sensors, enhancing reliability and reducing false positives. These technological leaps also enable features like biometric authentication and activity monitoring, broadening the scope of applications. The expanding use of ankle monitors in the Remote Patient Monitoring Market, particularly for elderly individuals prone to wandering or patients requiring adherence monitoring, represents a significant growth vector. This application leverages the core tracking capability while integrating health-related functionalities. The evolution of the Internet of Things Devices Market has further propelled this, connecting monitors to broader healthcare ecosystems.

Conversely, several factors constrain market growth. Privacy concerns and ethical considerations surrounding constant surveillance represent a significant hurdle. Debates about individual liberties and the potential for misuse of personal location data often slow down adoption, particularly in non-criminal applications. The stigma associated with wearing an ankle monitor, often linked to criminal behavior, also limits its acceptance in voluntary applications like child safety or elderly care, despite technological advancements in design and discretion. Furthermore, challenges related to technological limitations, such as signal loss in dense urban environments or remote areas, and the ongoing need for improved battery life, can impact device reliability and user compliance. The initial investment required for establishing and maintaining a comprehensive electronic monitoring program, including hardware, software platforms, and monitoring personnel, can also be substantial for smaller jurisdictions, posing a financial barrier to entry or expansion.

Competitive Ecosystem of Ankle Monitors Market

The Ankle Monitors Market is characterized by a mix of established players and innovative technology providers, all vying for market share through continuous innovation and strategic partnerships.

Supercom: A global provider of secured solutions for the e-Government, Public Safety, and Cyber Security sectors, Supercom offers comprehensive Electronic Monitoring Market solutions that integrate advanced GPS Tracking Devices Market technology with secure data management platforms, serving judicial and correctional agencies worldwide.

BI Incorporated: A subsidiary of The GEO Group, BI Incorporated is a long-standing and prominent provider of electronic monitoring and supervision technologies in the Correctional Facilities Market, offering a range of GPS, radio frequency, and alcohol detection ankle bracelets, alongside comprehensive monitoring services.

Buddi: A UK-based technology company specializing in innovative location-based services and wearable technology, Buddi provides discreet and advanced electronic monitoring solutions used primarily in criminal justice, but also explores applications in the broader Wearable Technology Market for safety and care.

Geosatis: A Swiss technology company known for its secure and robust electronic monitoring solutions, Geosatis designs and manufactures state-of-the-art ankle monitors and associated software platforms, emphasizing tamper-proof design and user-friendliness for the global justice sector.

Synergye: An innovator in the field of intelligent electronic monitoring, Synergye develops advanced tracking devices and integrated software systems, focusing on real-time data analysis and predictive analytics for enhanced supervision outcomes in the Electronic Monitoring Market.

Track Group: Specializing in offender tracking and monitoring solutions, Track Group leverages cutting-edge GPS Tracking Devices Market and communication technologies to provide comprehensive services to government agencies, aiming to improve public safety and support rehabilitation efforts.

Guanwei Intelligent Technology: A prominent Chinese manufacturer, Guanwei Intelligent Technology focuses on developing a wide range of GPS tracking devices and security solutions, including robust ankle monitors for judicial and private security applications within the Asia Pacific market.

Shenzhen Xexun Technology: Based in China, Shenzhen Xexun Technology is a leading provider of GPS tracking products and solutions, offering a variety of devices, including ankle monitors, for personal safety, asset tracking, and offender management across global markets.

Megastek Technologies: A Taiwan-based company, Megastek Technologies specializes in GPS tracking and GSM/GPRS communication modules, developing devices for vehicle tracking, personal safety, and electronic monitoring, serving a diverse client base in the Location-Based Services Market.

Shanghai REFINE Technologies: An innovative Chinese company, Shanghai REFINE Technologies develops and manufactures advanced electronic monitoring equipment, including ankle monitors with sophisticated tamper detection and communication features, catering to various governmental and private sector clients.

Recent Developments & Milestones in Ankle Monitors Market

Recent developments in the Ankle Monitors Market highlight a strong trend towards enhanced technological integration and diversification of applications, moving beyond traditional criminal justice use cases.

May 2026: A leading European provider launched its next-generation hybrid ankle monitor, integrating enhanced GPS Tracking Devices Market capabilities with secure 5G cellular connectivity and a low-power Bluetooth beacon for superior indoor and outdoor location accuracy. This development aims to provide seamless monitoring for parolees and individuals under home detention.

February 2026: A North American correctional department announced a multi-million dollar contract expansion for electronic monitoring services, citing a 15% increase in caseloads requiring community supervision. This partnership emphasizes the growing reliance on advanced ankle monitors to manage offender populations efficiently.

December 2025: A major player in the Electronic Monitoring Market unveiled a new software platform featuring AI-driven predictive analytics. This system leverages data from ankle monitors to identify potential risks and behavioral patterns, offering correctional officers proactive intervention capabilities.

September 2025: A technology startup secured $10 million in Series A funding to develop discreet ankle monitors specifically for the Remote Patient Monitoring Market. These devices focus on fall detection, wander management for dementia patients, and vital sign monitoring, underscoring the market's expansion into healthcare.

July 2025: Regulatory changes in several Asian countries simplified the legal framework for the adoption of electronic monitoring, including ankle monitors, as an alternative to pre-trial detention. This is expected to significantly boost market penetration in the Asia Pacific region.

April 2025: A partnership between a hardware manufacturer and a telecommunications giant was announced to develop highly secure, cloud-based data transmission protocols for ankle monitors, ensuring privacy and integrity of location data for the Location-Based Services Market.

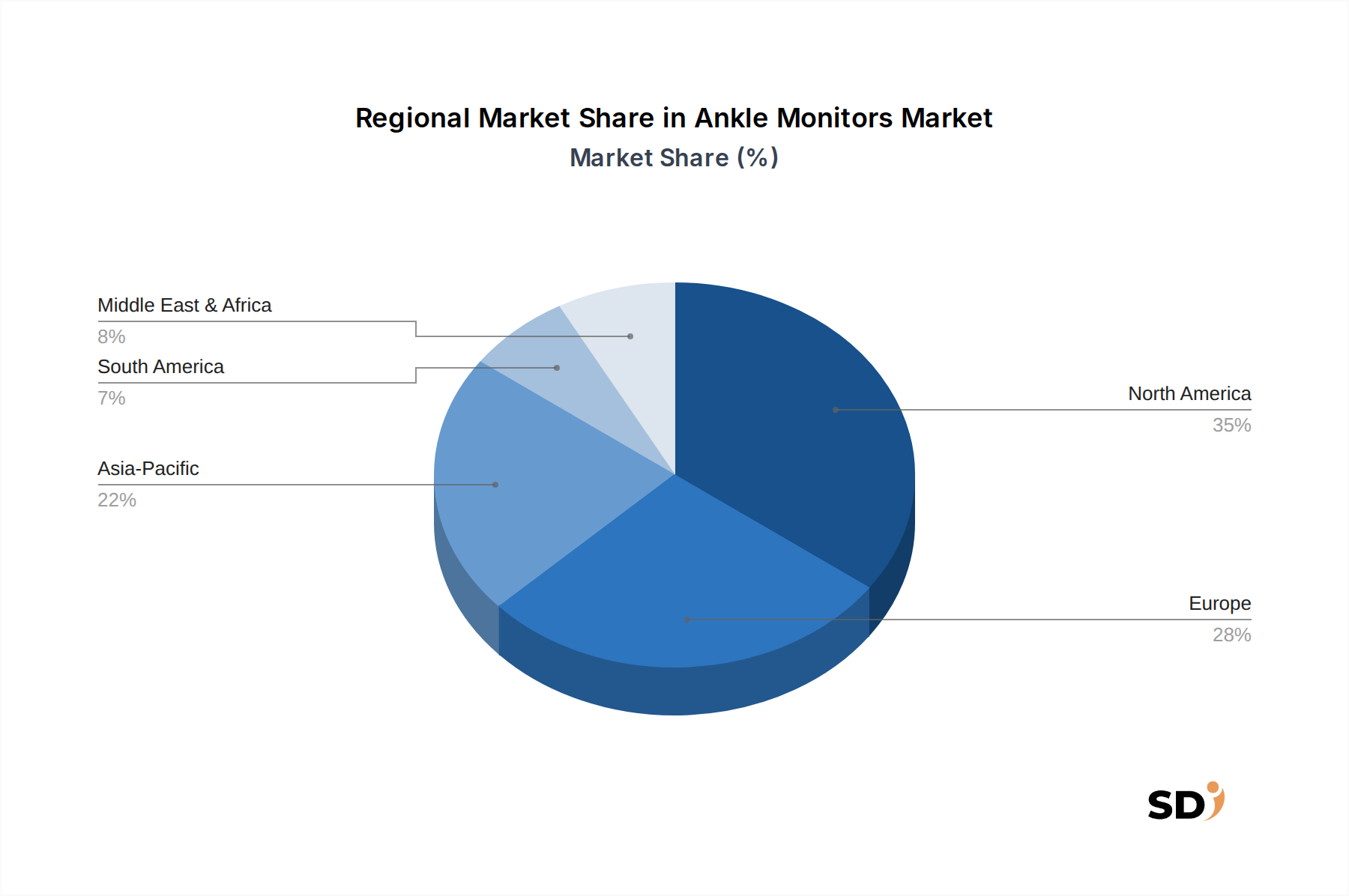

Regional Market Breakdown for Ankle Monitors Market

The global Ankle Monitors Market demonstrates significant regional disparities in adoption and growth, influenced by legal frameworks, technological infrastructure, and societal norms.

North America holds the largest revenue share in the Ankle Monitors Market. This dominance is driven by the mature and extensive use of electronic monitoring in the United States and Canada for criminal justice applications, including probation, parole, and pretrial release. The region benefits from robust technological infrastructure, high R&D investment, and a well-established regulatory environment that supports the integration of GPS Tracking Devices Market and cellular-based systems. The emphasis on reducing incarceration rates and managing large populations under community supervision significantly bolsters demand in the Correctional Facilities Market.

Europe represents a substantial and growing market for ankle monitors. Countries across the region are increasingly adopting electronic monitoring as part of broader penal reform initiatives aimed at rehabilitation and reducing recidivism. While regulatory landscapes vary, there's a concerted effort to standardize and expand the use of these devices. The growth is particularly strong in countries with overburdened prison systems seeking cost-effective alternatives and those embracing modern approaches to offender management. Demand for Electronic Monitoring Market solutions here is driven by national government initiatives and cross-border cooperation.

Asia Pacific is identified as the fastest-growing region in the Ankle Monitors Market. Although starting from a relatively smaller base, the region is experiencing rapid growth due to increasing awareness, modernization of judicial systems, and rising crime rates in several developing economies. Governments in countries like China and India are exploring and implementing electronic monitoring programs to address burgeoning inmate populations and enhance public safety. The region also shows nascent demand in niche applications such as the Child Tracking Market and private security services, reflecting a diversified interest in Wearable Technology Market solutions.

Middle East & Africa is an emerging market with significant potential. Growth here is primarily driven by efforts to modernize judicial systems, improve security infrastructure, and adopt advanced technological solutions for crime prevention and offender management. The demand for sophisticated Location-Based Services Market is also contributing. However, regulatory complexities, socio-cultural factors, and varying levels of technological infrastructure deployment can influence the pace of adoption.

Supply Chain & Raw Material Dynamics for Ankle Monitors Market

The supply chain for the Ankle Monitors Market is intricate, characterized by a reliance on advanced electronic components and specialized materials. Upstream dependencies are significant, with core components such as semiconductor chips, GPS and cellular communication modules, microcontrollers, and various sensors being critical inputs. These components are predominantly sourced from East Asian manufacturing hubs, creating vulnerability to geopolitical tensions, trade disputes, and natural disasters. For instance, global shortages in semiconductor chips, exacerbated by recent global events, have led to increased lead times and price volatility for manufacturers of GPS Tracking Devices Market and Internet of Things Devices Market. Key raw materials include lithium and cobalt for rechargeable battery cells, specialized durable plastics and polymers for device casings that must withstand environmental stressors and tampering, and various metals for connectors and antennas. The price trend for materials like lithium has seen upward pressure due to rising demand from the broader electric vehicle and consumer electronics sectors. Similarly, specific rare earth elements critical for advanced Sensor Technology Market can experience supply chain bottlenecks and price fluctuations. Sourcing risks include a high concentration of suppliers for specialized components, potentially limiting negotiation power and increasing reliance on single points of failure. Historically, disruptions such as factory shutdowns in major manufacturing regions or logistical challenges have led to production delays and increased manufacturing costs. This necessitates robust supply chain management strategies, including supplier diversification, strategic stockpiling of critical components, and investment in localized manufacturing capabilities to mitigate risks and ensure continuity in the Ankle Monitors Market.

Investment & Funding Activity in Ankle Monitors Market

Investment and funding activity in the Ankle Monitors Market over the past 2-3 years reflects a growing confidence in its expansion and technological evolution. Mergers and acquisitions (M&A) have been observed, with larger security technology firms consolidating the market by acquiring smaller, specialized electronic monitoring companies. These acquisitions are often driven by a desire to integrate advanced software analytics capabilities or to expand geographical reach and client portfolios within the Correctional Facilities Market and the broader Electronic Monitoring Market. For example, established players seek to enhance their offerings by acquiring startups focused on AI-powered behavior analytics or enhanced tamper-detection technologies. Venture funding rounds have shown a particular interest in startups developing more discreet, user-friendly, and multi-functional devices. Capital is predominantly flowing into companies innovating in areas such as miniaturization, extended battery life, and integration with health monitoring features, targeting new applications beyond criminal justice, such as the Remote Patient Monitoring Market and personal safety. Investment is also directed towards software platforms that offer advanced data analytics, predictive capabilities, and seamless integration with existing law enforcement or healthcare IT systems. Strategic partnerships are becoming increasingly common, with hardware manufacturers collaborating with software developers to create comprehensive, integrated solutions. There's also a trend of partnerships with telecommunication providers to ensure robust and secure connectivity for real-time Location-Based Services Market. This collaborative approach aims to leverage core competencies across the value chain, fostering innovation and accelerating market penetration. The continuous evolution of the Wearable Technology Market and the Internet of Things Devices Market provides a fertile ground for these investments, indicating a sustained growth trajectory as ankle monitors become more sophisticated and integrated into a broader ecosystem of connected devices.

Ankle Monitors Segmentation

1. Product Type

1.1. Radio Frequency-Based

1.2. GPS-Based

1.3. Cellular-Based

1.4. Hybrid

2. Component

2.1. Hardware

2.2. Software

2.3. Services

3. Monitoring Type

3.1. Active Monitoring

3.2. Passive Monitoring

4. Distribution Channel

4.1. Direct Sales

4.2. Online Sales

4.3. Offline Sales

5. End User

5.1. Criminal Justice

5.2. Home Detention

5.3. Healthcare

5.4. Child Tracking

5.5. Private Monitoring Service Providers

5.6. Others

Ankle Monitors Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Ankle Monitors REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 8% from 2020-2034

Segmentation

By Product Type

Radio Frequency-Based

GPS-Based

Cellular-Based

Hybrid

By Component

Hardware

Software

Services

By Monitoring Type

Active Monitoring

Passive Monitoring

By Distribution Channel

Direct Sales

Online Sales

Offline Sales

By End User

Criminal Justice

Home Detention

Healthcare

Child Tracking

Private Monitoring Service Providers

Others

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. SDI Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Product Type

5.1.1. Radio Frequency-Based

5.1.2. GPS-Based

5.1.3. Cellular-Based

5.1.4. Hybrid

5.2. Market Analysis, Insights and Forecast - by Component

5.2.1. Hardware

5.2.2. Software

5.2.3. Services

5.3. Market Analysis, Insights and Forecast - by Monitoring Type

5.3.1. Active Monitoring

5.3.2. Passive Monitoring

5.4. Market Analysis, Insights and Forecast - by Distribution Channel

5.4.1. Direct Sales

5.4.2. Online Sales

5.4.3. Offline Sales

5.5. Market Analysis, Insights and Forecast - by End User

5.5.1. Criminal Justice

5.5.2. Home Detention

5.5.3. Healthcare

5.5.4. Child Tracking

5.5.5. Private Monitoring Service Providers

5.5.6. Others

5.6. Market Analysis, Insights and Forecast - by Region

5.6.1. North America

5.6.2. South America

5.6.3. Europe

5.6.4. Middle East & Africa

5.6.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Product Type

6.1.1. Radio Frequency-Based

6.1.2. GPS-Based

6.1.3. Cellular-Based

6.1.4. Hybrid

6.2. Market Analysis, Insights and Forecast - by Component

6.2.1. Hardware

6.2.2. Software

6.2.3. Services

6.3. Market Analysis, Insights and Forecast - by Monitoring Type

6.3.1. Active Monitoring

6.3.2. Passive Monitoring

6.4. Market Analysis, Insights and Forecast - by Distribution Channel

6.4.1. Direct Sales

6.4.2. Online Sales

6.4.3. Offline Sales

6.5. Market Analysis, Insights and Forecast - by End User

6.5.1. Criminal Justice

6.5.2. Home Detention

6.5.3. Healthcare

6.5.4. Child Tracking

6.5.5. Private Monitoring Service Providers

6.5.6. Others

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Product Type

7.1.1. Radio Frequency-Based

7.1.2. GPS-Based

7.1.3. Cellular-Based

7.1.4. Hybrid

7.2. Market Analysis, Insights and Forecast - by Component

7.2.1. Hardware

7.2.2. Software

7.2.3. Services

7.3. Market Analysis, Insights and Forecast - by Monitoring Type

7.3.1. Active Monitoring

7.3.2. Passive Monitoring

7.4. Market Analysis, Insights and Forecast - by Distribution Channel

7.4.1. Direct Sales

7.4.2. Online Sales

7.4.3. Offline Sales

7.5. Market Analysis, Insights and Forecast - by End User

7.5.1. Criminal Justice

7.5.2. Home Detention

7.5.3. Healthcare

7.5.4. Child Tracking

7.5.5. Private Monitoring Service Providers

7.5.6. Others

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Product Type

8.1.1. Radio Frequency-Based

8.1.2. GPS-Based

8.1.3. Cellular-Based

8.1.4. Hybrid

8.2. Market Analysis, Insights and Forecast - by Component

8.2.1. Hardware

8.2.2. Software

8.2.3. Services

8.3. Market Analysis, Insights and Forecast - by Monitoring Type

8.3.1. Active Monitoring

8.3.2. Passive Monitoring

8.4. Market Analysis, Insights and Forecast - by Distribution Channel

8.4.1. Direct Sales

8.4.2. Online Sales

8.4.3. Offline Sales

8.5. Market Analysis, Insights and Forecast - by End User

8.5.1. Criminal Justice

8.5.2. Home Detention

8.5.3. Healthcare

8.5.4. Child Tracking

8.5.5. Private Monitoring Service Providers

8.5.6. Others

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Product Type

9.1.1. Radio Frequency-Based

9.1.2. GPS-Based

9.1.3. Cellular-Based

9.1.4. Hybrid

9.2. Market Analysis, Insights and Forecast - by Component

9.2.1. Hardware

9.2.2. Software

9.2.3. Services

9.3. Market Analysis, Insights and Forecast - by Monitoring Type

9.3.1. Active Monitoring

9.3.2. Passive Monitoring

9.4. Market Analysis, Insights and Forecast - by Distribution Channel

9.4.1. Direct Sales

9.4.2. Online Sales

9.4.3. Offline Sales

9.5. Market Analysis, Insights and Forecast - by End User

9.5.1. Criminal Justice

9.5.2. Home Detention

9.5.3. Healthcare

9.5.4. Child Tracking

9.5.5. Private Monitoring Service Providers

9.5.6. Others

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Product Type

10.1.1. Radio Frequency-Based

10.1.2. GPS-Based

10.1.3. Cellular-Based

10.1.4. Hybrid

10.2. Market Analysis, Insights and Forecast - by Component

10.2.1. Hardware

10.2.2. Software

10.2.3. Services

10.3. Market Analysis, Insights and Forecast - by Monitoring Type

10.3.1. Active Monitoring

10.3.2. Passive Monitoring

10.4. Market Analysis, Insights and Forecast - by Distribution Channel

10.4.1. Direct Sales

10.4.2. Online Sales

10.4.3. Offline Sales

10.5. Market Analysis, Insights and Forecast - by End User

10.5.1. Criminal Justice

10.5.2. Home Detention

10.5.3. Healthcare

10.5.4. Child Tracking

10.5.5. Private Monitoring Service Providers

10.5.6. Others

11. Competitive Analysis

11.1. Company Profiles

11.1.1. Supercom

11.1.1.1. Company Overview

11.1.1.2. Products

11.1.1.3. Company Financials

11.1.1.4. SWOT Analysis

11.1.2. BI Incorporated

11.1.2.1. Company Overview

11.1.2.2. Products

11.1.2.3. Company Financials

11.1.2.4. SWOT Analysis

11.1.3. Buddi

11.1.3.1. Company Overview

11.1.3.2. Products

11.1.3.3. Company Financials

11.1.3.4. SWOT Analysis

11.1.4. Geosatis

11.1.4.1. Company Overview

11.1.4.2. Products

11.1.4.3. Company Financials

11.1.4.4. SWOT Analysis

11.1.5. Synergye

11.1.5.1. Company Overview

11.1.5.2. Products

11.1.5.3. Company Financials

11.1.5.4. SWOT Analysis

11.1.6. Track Group

11.1.6.1. Company Overview

11.1.6.2. Products

11.1.6.3. Company Financials

11.1.6.4. SWOT Analysis

11.1.7. Guanwei Intelligent Technology

11.1.7.1. Company Overview

11.1.7.2. Products

11.1.7.3. Company Financials

11.1.7.4. SWOT Analysis

11.1.8. Shenzhen Xexun Technology

11.1.8.1. Company Overview

11.1.8.2. Products

11.1.8.3. Company Financials

11.1.8.4. SWOT Analysis

11.1.9. Megastek Technologies

11.1.9.1. Company Overview

11.1.9.2. Products

11.1.9.3. Company Financials

11.1.9.4. SWOT Analysis

11.1.10. Shanghai REFINE Technologies

11.1.10.1. Company Overview

11.1.10.2. Products

11.1.10.3. Company Financials

11.1.10.4. SWOT Analysis

11.1.11. Others

11.1.11.1. Company Overview

11.1.11.2. Products

11.1.11.3. Company Financials

11.1.11.4. SWOT Analysis

11.2. Market Entropy

11.2.1. Company's Key Areas Served

11.2.2. Recent Developments

11.3. Company Market Share Analysis, 2025

11.3.1. Top 5 Companies Market Share Analysis

11.3.2. Top 3 Companies Market Share Analysis

11.4. List of Potential Customers

12. Research Methodology

List of Figures

Figure 1: Revenue Breakdown (billion, %) by Region 2025 & 2033

Figure 2: Volume Breakdown (K, %) by Region 2025 & 2033

Figure 3: Revenue (billion), by Product Type 2025 & 2033

Figure 4: Volume (K), by Product Type 2025 & 2033

Figure 5: Revenue Share (%), by Product Type 2025 & 2033

Figure 6: Volume Share (%), by Product Type 2025 & 2033

Figure 7: Revenue (billion), by Component 2025 & 2033

Figure 8: Volume (K), by Component 2025 & 2033

Figure 9: Revenue Share (%), by Component 2025 & 2033

Figure 10: Volume Share (%), by Component 2025 & 2033

Figure 11: Revenue (billion), by Monitoring Type 2025 & 2033

Figure 12: Volume (K), by Monitoring Type 2025 & 2033

Figure 13: Revenue Share (%), by Monitoring Type 2025 & 2033

Figure 14: Volume Share (%), by Monitoring Type 2025 & 2033

Figure 15: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 16: Volume (K), by Distribution Channel 2025 & 2033

Figure 17: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 18: Volume Share (%), by Distribution Channel 2025 & 2033

Figure 19: Revenue (billion), by End User 2025 & 2033

Figure 20: Volume (K), by End User 2025 & 2033

Figure 21: Revenue Share (%), by End User 2025 & 2033

Figure 22: Volume Share (%), by End User 2025 & 2033

Figure 23: Revenue (billion), by Country 2025 & 2033

Figure 24: Volume (K), by Country 2025 & 2033

Figure 25: Revenue Share (%), by Country 2025 & 2033

Figure 26: Volume Share (%), by Country 2025 & 2033

Figure 27: Revenue (billion), by Product Type 2025 & 2033

Figure 28: Volume (K), by Product Type 2025 & 2033

Figure 29: Revenue Share (%), by Product Type 2025 & 2033

Figure 30: Volume Share (%), by Product Type 2025 & 2033

Figure 31: Revenue (billion), by Component 2025 & 2033

Figure 32: Volume (K), by Component 2025 & 2033

Figure 33: Revenue Share (%), by Component 2025 & 2033

Figure 34: Volume Share (%), by Component 2025 & 2033

Figure 35: Revenue (billion), by Monitoring Type 2025 & 2033

Figure 36: Volume (K), by Monitoring Type 2025 & 2033

Figure 37: Revenue Share (%), by Monitoring Type 2025 & 2033

Figure 38: Volume Share (%), by Monitoring Type 2025 & 2033

Figure 39: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 40: Volume (K), by Distribution Channel 2025 & 2033

Figure 41: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 42: Volume Share (%), by Distribution Channel 2025 & 2033

Figure 43: Revenue (billion), by End User 2025 & 2033

Figure 44: Volume (K), by End User 2025 & 2033

Figure 45: Revenue Share (%), by End User 2025 & 2033

Figure 46: Volume Share (%), by End User 2025 & 2033

Figure 47: Revenue (billion), by Country 2025 & 2033

Figure 48: Volume (K), by Country 2025 & 2033

Figure 49: Revenue Share (%), by Country 2025 & 2033

Figure 50: Volume Share (%), by Country 2025 & 2033

Figure 51: Revenue (billion), by Product Type 2025 & 2033

Figure 52: Volume (K), by Product Type 2025 & 2033

Figure 53: Revenue Share (%), by Product Type 2025 & 2033

Figure 54: Volume Share (%), by Product Type 2025 & 2033

Figure 55: Revenue (billion), by Component 2025 & 2033

Figure 56: Volume (K), by Component 2025 & 2033

Figure 57: Revenue Share (%), by Component 2025 & 2033

Figure 58: Volume Share (%), by Component 2025 & 2033

Figure 59: Revenue (billion), by Monitoring Type 2025 & 2033

Figure 60: Volume (K), by Monitoring Type 2025 & 2033

Figure 61: Revenue Share (%), by Monitoring Type 2025 & 2033

Figure 62: Volume Share (%), by Monitoring Type 2025 & 2033

Figure 63: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 64: Volume (K), by Distribution Channel 2025 & 2033

Figure 65: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 66: Volume Share (%), by Distribution Channel 2025 & 2033

Figure 67: Revenue (billion), by End User 2025 & 2033

Figure 68: Volume (K), by End User 2025 & 2033

Figure 69: Revenue Share (%), by End User 2025 & 2033

Figure 70: Volume Share (%), by End User 2025 & 2033

Figure 71: Revenue (billion), by Country 2025 & 2033

Figure 72: Volume (K), by Country 2025 & 2033

Figure 73: Revenue Share (%), by Country 2025 & 2033

Figure 74: Volume Share (%), by Country 2025 & 2033

Figure 75: Revenue (billion), by Product Type 2025 & 2033

Figure 76: Volume (K), by Product Type 2025 & 2033

Figure 77: Revenue Share (%), by Product Type 2025 & 2033

Figure 78: Volume Share (%), by Product Type 2025 & 2033

Figure 79: Revenue (billion), by Component 2025 & 2033

Figure 80: Volume (K), by Component 2025 & 2033

Figure 81: Revenue Share (%), by Component 2025 & 2033

Figure 82: Volume Share (%), by Component 2025 & 2033

Figure 83: Revenue (billion), by Monitoring Type 2025 & 2033

Figure 84: Volume (K), by Monitoring Type 2025 & 2033

Figure 85: Revenue Share (%), by Monitoring Type 2025 & 2033

Figure 86: Volume Share (%), by Monitoring Type 2025 & 2033

Figure 87: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 88: Volume (K), by Distribution Channel 2025 & 2033

Figure 89: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 90: Volume Share (%), by Distribution Channel 2025 & 2033

Figure 91: Revenue (billion), by End User 2025 & 2033

Figure 92: Volume (K), by End User 2025 & 2033

Figure 93: Revenue Share (%), by End User 2025 & 2033

Figure 94: Volume Share (%), by End User 2025 & 2033

Figure 95: Revenue (billion), by Country 2025 & 2033

Figure 96: Volume (K), by Country 2025 & 2033

Figure 97: Revenue Share (%), by Country 2025 & 2033

Figure 98: Volume Share (%), by Country 2025 & 2033

Figure 99: Revenue (billion), by Product Type 2025 & 2033

Figure 100: Volume (K), by Product Type 2025 & 2033

Figure 101: Revenue Share (%), by Product Type 2025 & 2033

Figure 102: Volume Share (%), by Product Type 2025 & 2033

Figure 103: Revenue (billion), by Component 2025 & 2033

Figure 104: Volume (K), by Component 2025 & 2033

Figure 105: Revenue Share (%), by Component 2025 & 2033

Figure 106: Volume Share (%), by Component 2025 & 2033

Figure 107: Revenue (billion), by Monitoring Type 2025 & 2033

Figure 108: Volume (K), by Monitoring Type 2025 & 2033

Figure 109: Revenue Share (%), by Monitoring Type 2025 & 2033

Figure 110: Volume Share (%), by Monitoring Type 2025 & 2033

Figure 111: Revenue (billion), by Distribution Channel 2025 & 2033

Figure 112: Volume (K), by Distribution Channel 2025 & 2033

Figure 113: Revenue Share (%), by Distribution Channel 2025 & 2033

Figure 114: Volume Share (%), by Distribution Channel 2025 & 2033

Figure 115: Revenue (billion), by End User 2025 & 2033

Figure 116: Volume (K), by End User 2025 & 2033

Figure 117: Revenue Share (%), by End User 2025 & 2033

Figure 118: Volume Share (%), by End User 2025 & 2033

Figure 119: Revenue (billion), by Country 2025 & 2033

Figure 120: Volume (K), by Country 2025 & 2033

Figure 121: Revenue Share (%), by Country 2025 & 2033

Figure 122: Volume Share (%), by Country 2025 & 2033

List of Tables

Table 1: Revenue billion Forecast, by Product Type 2020 & 2033

Table 2: Volume K Forecast, by Product Type 2020 & 2033

Table 3: Revenue billion Forecast, by Component 2020 & 2033

Table 4: Volume K Forecast, by Component 2020 & 2033

Table 5: Revenue billion Forecast, by Monitoring Type 2020 & 2033

Table 6: Volume K Forecast, by Monitoring Type 2020 & 2033

Table 7: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 8: Volume K Forecast, by Distribution Channel 2020 & 2033

Table 9: Revenue billion Forecast, by End User 2020 & 2033

Table 10: Volume K Forecast, by End User 2020 & 2033

Table 11: Revenue billion Forecast, by Region 2020 & 2033

Table 12: Volume K Forecast, by Region 2020 & 2033

Table 13: Revenue billion Forecast, by Product Type 2020 & 2033

Table 14: Volume K Forecast, by Product Type 2020 & 2033

Table 15: Revenue billion Forecast, by Component 2020 & 2033

Table 16: Volume K Forecast, by Component 2020 & 2033

Table 17: Revenue billion Forecast, by Monitoring Type 2020 & 2033

Table 18: Volume K Forecast, by Monitoring Type 2020 & 2033

Table 19: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 20: Volume K Forecast, by Distribution Channel 2020 & 2033

Table 21: Revenue billion Forecast, by End User 2020 & 2033

Table 22: Volume K Forecast, by End User 2020 & 2033

Table 23: Revenue billion Forecast, by Country 2020 & 2033

Table 24: Volume K Forecast, by Country 2020 & 2033

Table 25: Revenue (billion) Forecast, by Application 2020 & 2033

Table 26: Volume (K) Forecast, by Application 2020 & 2033

Table 27: Revenue (billion) Forecast, by Application 2020 & 2033

Table 28: Volume (K) Forecast, by Application 2020 & 2033

Table 29: Revenue (billion) Forecast, by Application 2020 & 2033

Table 30: Volume (K) Forecast, by Application 2020 & 2033

Table 31: Revenue billion Forecast, by Product Type 2020 & 2033

Table 32: Volume K Forecast, by Product Type 2020 & 2033

Table 33: Revenue billion Forecast, by Component 2020 & 2033

Table 34: Volume K Forecast, by Component 2020 & 2033

Table 35: Revenue billion Forecast, by Monitoring Type 2020 & 2033

Table 36: Volume K Forecast, by Monitoring Type 2020 & 2033

Table 37: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 38: Volume K Forecast, by Distribution Channel 2020 & 2033

Table 39: Revenue billion Forecast, by End User 2020 & 2033

Table 40: Volume K Forecast, by End User 2020 & 2033

Table 41: Revenue billion Forecast, by Country 2020 & 2033

Table 42: Volume K Forecast, by Country 2020 & 2033

Table 43: Revenue (billion) Forecast, by Application 2020 & 2033

Table 44: Volume (K) Forecast, by Application 2020 & 2033

Table 45: Revenue (billion) Forecast, by Application 2020 & 2033

Table 46: Volume (K) Forecast, by Application 2020 & 2033

Table 47: Revenue (billion) Forecast, by Application 2020 & 2033

Table 48: Volume (K) Forecast, by Application 2020 & 2033

Table 49: Revenue billion Forecast, by Product Type 2020 & 2033

Table 50: Volume K Forecast, by Product Type 2020 & 2033

Table 51: Revenue billion Forecast, by Component 2020 & 2033

Table 52: Volume K Forecast, by Component 2020 & 2033

Table 53: Revenue billion Forecast, by Monitoring Type 2020 & 2033

Table 54: Volume K Forecast, by Monitoring Type 2020 & 2033

Table 55: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 56: Volume K Forecast, by Distribution Channel 2020 & 2033

Table 57: Revenue billion Forecast, by End User 2020 & 2033

Table 58: Volume K Forecast, by End User 2020 & 2033

Table 59: Revenue billion Forecast, by Country 2020 & 2033

Table 60: Volume K Forecast, by Country 2020 & 2033

Table 61: Revenue (billion) Forecast, by Application 2020 & 2033

Table 62: Volume (K) Forecast, by Application 2020 & 2033

Table 63: Revenue (billion) Forecast, by Application 2020 & 2033

Table 64: Volume (K) Forecast, by Application 2020 & 2033

Table 65: Revenue (billion) Forecast, by Application 2020 & 2033

Table 66: Volume (K) Forecast, by Application 2020 & 2033

Table 67: Revenue (billion) Forecast, by Application 2020 & 2033

Table 68: Volume (K) Forecast, by Application 2020 & 2033

Table 69: Revenue (billion) Forecast, by Application 2020 & 2033

Table 70: Volume (K) Forecast, by Application 2020 & 2033

Table 71: Revenue (billion) Forecast, by Application 2020 & 2033

Table 72: Volume (K) Forecast, by Application 2020 & 2033

Table 73: Revenue (billion) Forecast, by Application 2020 & 2033

Table 74: Volume (K) Forecast, by Application 2020 & 2033

Table 75: Revenue (billion) Forecast, by Application 2020 & 2033

Table 76: Volume (K) Forecast, by Application 2020 & 2033

Table 77: Revenue (billion) Forecast, by Application 2020 & 2033

Table 78: Volume (K) Forecast, by Application 2020 & 2033

Table 79: Revenue billion Forecast, by Product Type 2020 & 2033

Table 80: Volume K Forecast, by Product Type 2020 & 2033

Table 81: Revenue billion Forecast, by Component 2020 & 2033

Table 82: Volume K Forecast, by Component 2020 & 2033

Table 83: Revenue billion Forecast, by Monitoring Type 2020 & 2033

Table 84: Volume K Forecast, by Monitoring Type 2020 & 2033

Table 85: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 86: Volume K Forecast, by Distribution Channel 2020 & 2033

Table 87: Revenue billion Forecast, by End User 2020 & 2033

Table 88: Volume K Forecast, by End User 2020 & 2033

Table 89: Revenue billion Forecast, by Country 2020 & 2033

Table 90: Volume K Forecast, by Country 2020 & 2033

Table 91: Revenue (billion) Forecast, by Application 2020 & 2033

Table 92: Volume (K) Forecast, by Application 2020 & 2033

Table 93: Revenue (billion) Forecast, by Application 2020 & 2033

Table 94: Volume (K) Forecast, by Application 2020 & 2033

Table 95: Revenue (billion) Forecast, by Application 2020 & 2033

Table 96: Volume (K) Forecast, by Application 2020 & 2033

Table 97: Revenue (billion) Forecast, by Application 2020 & 2033

Table 98: Volume (K) Forecast, by Application 2020 & 2033

Table 99: Revenue (billion) Forecast, by Application 2020 & 2033

Table 100: Volume (K) Forecast, by Application 2020 & 2033

Table 101: Revenue (billion) Forecast, by Application 2020 & 2033

Table 102: Volume (K) Forecast, by Application 2020 & 2033

Table 103: Revenue billion Forecast, by Product Type 2020 & 2033

Table 104: Volume K Forecast, by Product Type 2020 & 2033

Table 105: Revenue billion Forecast, by Component 2020 & 2033

Table 106: Volume K Forecast, by Component 2020 & 2033

Table 107: Revenue billion Forecast, by Monitoring Type 2020 & 2033

Table 108: Volume K Forecast, by Monitoring Type 2020 & 2033

Table 109: Revenue billion Forecast, by Distribution Channel 2020 & 2033

Table 110: Volume K Forecast, by Distribution Channel 2020 & 2033

Table 111: Revenue billion Forecast, by End User 2020 & 2033

Table 112: Volume K Forecast, by End User 2020 & 2033

Table 113: Revenue billion Forecast, by Country 2020 & 2033

Table 114: Volume K Forecast, by Country 2020 & 2033

Table 115: Revenue (billion) Forecast, by Application 2020 & 2033

Table 116: Volume (K) Forecast, by Application 2020 & 2033

Table 117: Revenue (billion) Forecast, by Application 2020 & 2033

Table 118: Volume (K) Forecast, by Application 2020 & 2033

Table 119: Revenue (billion) Forecast, by Application 2020 & 2033

Table 120: Volume (K) Forecast, by Application 2020 & 2033

Table 121: Revenue (billion) Forecast, by Application 2020 & 2033

Table 122: Volume (K) Forecast, by Application 2020 & 2033

Table 123: Revenue (billion) Forecast, by Application 2020 & 2033

Table 124: Volume (K) Forecast, by Application 2020 & 2033

Table 125: Revenue (billion) Forecast, by Application 2020 & 2033

Table 126: Volume (K) Forecast, by Application 2020 & 2033

Table 127: Revenue (billion) Forecast, by Application 2020 & 2033

Table 128: Volume (K) Forecast, by Application 2020 & 2033

Research Methodology & Data Sources

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Primary Research

Our primary research methodology forms the bedrock of our market analysis, accounting for approximately 75% of our overall research efforts. This robust approach involves direct engagement with key stakeholders across the ankle monitor value chain to gather first-hand intelligence, validate secondary findings, and uncover nuanced market dynamics that are often not captured in published data. Our primary interviews are meticulously structured, employing a combination of qualitative and quantitative questioning techniques to extract actionable insights.

Key participants in our primary research include:

Company Types:

Ankle Monitor Hardware Manufacturers (e.g., design, production, distribution of RF, GPS, Cellular, Hybrid devices)

Electronic Monitoring Software & Platform Developers (e.g., providers of monitoring, analytics, and reporting solutions)

Correctional & Home Detention Service Providers (e.g., third-party companies managing monitoring programs for agencies)

Complementing our primary efforts, secondary research constitutes approximately 25% of our methodology. This phase is critical for establishing a foundational understanding of the market, identifying key trends, competitive landscapes, and regulatory frameworks. We rigorously sift through a wide array of credible sources to ensure comprehensive data collection.

Our secondary research primarily leverages:

Financial Databases: Extensive use of platforms such as Bloomberg, Factiva, Hoovers, and PitchBook to analyze company financials, investment trends, and competitive positioning.

Government & Regulatory Publications: Data and insights from official government reports, justice department statistics, correctional facility operational data, and policy documents (e.g., U.S. Bureau of Justice Statistics [https://bjs.ojp.gov/], European Union Agency for Fundamental Rights [https://fra.europa.eu/]).

Industry Associations & Trade Bodies: Reports, white papers, and statistics published by relevant industry groups, providing an overview of market trends, technological advancements, and best practices. Examples include:

Academic Research & White Papers: Peer-reviewed journals and research papers offering deeper theoretical and empirical insights into the socio-economic impacts and technological evolution of electronic monitoring.

Demand Modeling & Market Estimation

Our market sizing and forecasting methodologies employ a robust combination of top-down and bottom-up approaches, further reinforced by multi-level data triangulation. This ensures a comprehensive and accurate representation of the market's current state and future trajectory.

Top-Down Approach: We estimate the total market size by analyzing macro-economic indicators, government spending on correctional technologies, criminal justice system budgets, and overall trends in probation and parole populations across different regions. This provides a broad market scope, which is then disaggregated by product type, component, monitoring type, distribution channel, and end-user segments.

Bottom-Up Approach: This method involves aggregating market data from granular levels. For the Ankle Monitors market, key variables and metrics used for bottom-up calculation include:

Number of individuals under electronic monitoring: By jurisdiction and type of offense/program (e.g., pre-trial, post-conviction, home detention).

Average Annual Device & Service Cost per User: Reflecting the combined cost of hardware, software, and monitoring services.

New Device Deployments and Replacement Rates: Annual volumes of new devices entering service and existing units being replaced or upgraded.

Governmental & Private Sector Budget Allocations: Specific spending on electronic monitoring solutions by correctional agencies, private monitoring service providers, and healthcare entities.

Multi-level Data Triangulation: All market estimates derived from both top-down and bottom-up analyses are cross-referenced and validated with data obtained through primary interviews, expert opinions, and secondary research. This iterative process allows for continuous refinement and ensures consistency across various data points and segments.

Data Accuracy & Quality Check

Our commitment to data integrity is paramount. We guarantee an estimated data accuracy level of 85-90% for all quantitative figures presented in the report. This high level of accuracy is achieved through:

Expert Validation: All market figures, growth rates, and forecasts are rigorously reviewed and validated by a panel of industry experts and key opinion leaders interviewed during the primary research phase.

Iterative Refinement: Our research process is iterative, with data continually updated and refined based on new information, market shifts, and expert feedback.

Real-time Updates: To ensure relevance, every report is updated up to the date of purchase, incorporating the latest market developments, regulatory changes, and competitive intelligence to provide the most current and accurate market snapshot available.

Frequently Asked Questions

1. What are the key pricing trends for ankle monitors?

Ankle monitor pricing trends are influenced by component costs like hardware and software, alongside service fees. GPS-based units typically command higher prices due to advanced functionality, impacting overall cost structures.

2. How do ankle monitors impact sustainability or ESG factors?

Sustainability in ankle monitors relates to device longevity, power consumption, and material sourcing. While not directly a high-impact sector, manufacturers like Supercom and Buddi may focus on reducing electronic waste and energy efficiency.

3. Which regions dominate ankle monitor export-import flows?

International trade for ankle monitors sees significant activity from North America and Europe, given the established legal frameworks and technology providers. Asia-Pacific, particularly China, also contributes to component and finished product supply.

4. What are the primary barriers to entry in the ankle monitor market?

Barriers include high R&D costs for advanced technologies like cellular and hybrid systems, regulatory compliance, and the need for robust service infrastructure. Established players such as Supercom and BI Incorporated benefit from existing client contracts.

5. What technological innovations are shaping the ankle monitor industry?

Innovations are focused on enhancing GPS accuracy, improving battery life for active monitoring, and integrating cellular-based communication. Hybrid systems combining multiple technologies represent a significant R&D trend for providers like Geosatis.

6. Which are the key end-user segments for ankle monitors?

The primary end-user segments include Criminal Justice, Home Detention, and Healthcare, accounting for significant demand. Child Tracking and Private Monitoring Service Providers also represent growing application areas for these devices.